Treasury Wine Estates Limited Audit Plan for Year Ended 2017

VerifiedAdded on 2023/06/06

|18

|4662

|477

Report

AI Summary

This report presents a detailed audit plan for Treasury Wine Estates Limited (TWE) for the year ended June 30, 2017. It begins with a business risk assessment, evaluating entity-level, industry-level, and economic risks that could impact TWE's strategies. The report analyzes TWE's financial performance through a preliminary analytical review, including ratio and trend analyses of key financial metrics like profitability, liquidity, and solvency. An inherent risk assessment is conducted, with a specific focus on fraud risks. The report uses data from 2015-2017 to assess the company's performance. The analysis covers revenue, cost of sales, gross profit, operating expenses, and net profit before tax, providing insights into TWE's financial health and potential areas of concern. The report highlights key financial ratios, trend analysis, and interpretations. It also discusses the use of experts in specific technical areas of the audit, such as business planning and impairment assessments.

TREASURY WINE ESTATES LIMITED AUDIT PLAN

Audit Planning Memorandum Date:

Client name: Treasury Wine Estates Limited Prepared by:

Year ended: 30 June 2017 Reviewed by:

1.0 Business Risk Assessment

1.1 Summary of Client Background Information

Treasury Wine Estates Limited is a global winemaking company founded in 2011. It was formerly operational as a division of the Foster’s Group

and TWE became an officially listed company as the Fosters group split its wine and brewing companies. It is one of the largest publicly listed

wine companies.

It has its headquarters in Melbourne, Australia and has distribution business across the world. The business is spread across four major

locations which include Asia, Europe, America and Australia and New Zealand.

The brands dealt with by TWE are different across countries based upon the tastes and preferences of the respective regions. Thus it has to its

list a diverse portfolio of outstanding wine brands with wine sales in more than 100 countries across the world.

It employs approximately 3,400 winemakers and viticulturists including marketing, sales and support staff around the four continents.

TWE is viewed as a high performing company with a consistent performance and enhancing sustainability and value addition. Due to its

constant innovations, it is also viewed as the fastest growing company.

1.2 Business Risks – Entity Level

There are various risks that could have an impact on the achievement of TWE’s strategies. The threats of business survival in wine industry are

numerous. Based on the materiality, a few risks are discussed in this report (Matthew, 2015).

Constrained grape supply is one such risk. To meet the ever growing demand, TWE is faced with the challenge of restricted availability of

grapes. This is largely dependent on the climatic conditions, agricultural factors such as pests, bad weather conditions, water scarcity,

competing land use and biodiversity loss. Thus TWE is unable to fulfil its demand. Apart from this, grapes on the vine might suffer from smoke

Page 1 of 18

Audit Planning Memorandum Date:

Client name: Treasury Wine Estates Limited Prepared by:

Year ended: 30 June 2017 Reviewed by:

1.0 Business Risk Assessment

1.1 Summary of Client Background Information

Treasury Wine Estates Limited is a global winemaking company founded in 2011. It was formerly operational as a division of the Foster’s Group

and TWE became an officially listed company as the Fosters group split its wine and brewing companies. It is one of the largest publicly listed

wine companies.

It has its headquarters in Melbourne, Australia and has distribution business across the world. The business is spread across four major

locations which include Asia, Europe, America and Australia and New Zealand.

The brands dealt with by TWE are different across countries based upon the tastes and preferences of the respective regions. Thus it has to its

list a diverse portfolio of outstanding wine brands with wine sales in more than 100 countries across the world.

It employs approximately 3,400 winemakers and viticulturists including marketing, sales and support staff around the four continents.

TWE is viewed as a high performing company with a consistent performance and enhancing sustainability and value addition. Due to its

constant innovations, it is also viewed as the fastest growing company.

1.2 Business Risks – Entity Level

There are various risks that could have an impact on the achievement of TWE’s strategies. The threats of business survival in wine industry are

numerous. Based on the materiality, a few risks are discussed in this report (Matthew, 2015).

Constrained grape supply is one such risk. To meet the ever growing demand, TWE is faced with the challenge of restricted availability of

grapes. This is largely dependent on the climatic conditions, agricultural factors such as pests, bad weather conditions, water scarcity,

competing land use and biodiversity loss. Thus TWE is unable to fulfil its demand. Apart from this, grapes on the vine might suffer from smoke

Page 1 of 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TREASURY WINE ESTATES LIMITED AUDIT PLAN

taint and might get damaged due to collision or overturn.

Business is dependent largely on the availability of IT infrastructure and installation of such systems and processes that will support the

ongoing growth of the business. If infrastructure is not updated, it could lead to the risk of processing inefficiencies and increasing the costs

and processing time ultimately damaging the business reputation ( Livne, 2015).

The liabilities are pretty high as accidents and legal actions lead to lawsuits and court proceedings.

The agricultural risks range from plant diseases, insects infestations and wildfires. Product contamination, leakages, spillages and the

accidental mixings pose the risk of damaging the wine in transit or storage. Transportation, supply chain and logistics issue could lead to delays

(Messier & Emby, 2005).

Equipment breakdowns are also to be managed on an everyday basis.

Heavy investment in Research and Development to innovate unique taste and formula which in turn becomes a trade secret to be

safeguarded.

1.3 Business Risks – Industry Level

TWE is able to achieve its goals and strategies due to the manpower and retention of skilled, motivated and talented workforce. But due to the

increasing competition, it is getting increasingly difficult to retain key leaders and the inability to retain strong relations with key partners due

to mergers and takeovers can lead to a loss of business excellence, increased business risk to deliver the key initiatives (Livne, 2015).

TWE is a brand led organization and any attempt to damage the brand either due to social media or black market trading, unsatisfactory

supplier performance, product quality and environmental issues can all lead to hamper the brand and pose a challenge for TWE’s ongoing

success. The failure to protect the existing portfolio of brands can have significant financial and reputational repercussions (Hoffelder, 2012).

TWE’s delivery of key strategic initiatives is dependent upon the performance of its key partners like suppliers, distributors and retailers. Their

optimal performance, market concentration and power are all significant risk areas to the success of TWE’s performance (Mock et. al, 2013).

Customer needs and preferences keep changing and the success of the business depends on how efficiently it is able to manage the same. The

current and non-current inventory is linked to the forecast customer demand especially in wine business as the product lead time is pretty

Page 2 of 18

taint and might get damaged due to collision or overturn.

Business is dependent largely on the availability of IT infrastructure and installation of such systems and processes that will support the

ongoing growth of the business. If infrastructure is not updated, it could lead to the risk of processing inefficiencies and increasing the costs

and processing time ultimately damaging the business reputation ( Livne, 2015).

The liabilities are pretty high as accidents and legal actions lead to lawsuits and court proceedings.

The agricultural risks range from plant diseases, insects infestations and wildfires. Product contamination, leakages, spillages and the

accidental mixings pose the risk of damaging the wine in transit or storage. Transportation, supply chain and logistics issue could lead to delays

(Messier & Emby, 2005).

Equipment breakdowns are also to be managed on an everyday basis.

Heavy investment in Research and Development to innovate unique taste and formula which in turn becomes a trade secret to be

safeguarded.

1.3 Business Risks – Industry Level

TWE is able to achieve its goals and strategies due to the manpower and retention of skilled, motivated and talented workforce. But due to the

increasing competition, it is getting increasingly difficult to retain key leaders and the inability to retain strong relations with key partners due

to mergers and takeovers can lead to a loss of business excellence, increased business risk to deliver the key initiatives (Livne, 2015).

TWE is a brand led organization and any attempt to damage the brand either due to social media or black market trading, unsatisfactory

supplier performance, product quality and environmental issues can all lead to hamper the brand and pose a challenge for TWE’s ongoing

success. The failure to protect the existing portfolio of brands can have significant financial and reputational repercussions (Hoffelder, 2012).

TWE’s delivery of key strategic initiatives is dependent upon the performance of its key partners like suppliers, distributors and retailers. Their

optimal performance, market concentration and power are all significant risk areas to the success of TWE’s performance (Mock et. al, 2013).

Customer needs and preferences keep changing and the success of the business depends on how efficiently it is able to manage the same. The

current and non-current inventory is linked to the forecast customer demand especially in wine business as the product lead time is pretty

Page 2 of 18

TREASURY WINE ESTATES LIMITED AUDIT PLAN

long. The unanticipated changes in customer preferences is a business risk as it can have adverse effects on the ability of the business to

capture growth opportunities and manage the orders and supplies.

Wine industry is a highly regulated industry which is exposed to the fulfilment and compliance with the various laws and regulations. Expansion

into new markets also means the exposure to the different regulations including taxation, manufacturing, marketing, advertising, distribution

and sale of wine. This requires the ongoing monitoring of the changes and updates in the regulations that can have a significant impact on the

nature of operations in these markets (Ghandhar & Tsahuridu, 2013).

1.4 Business Risks – Economy Level

TWE has business connections with more than 100 countries around the world. Hence foreign exchange risks from the key offshore markets

are a significant risk area. These foreign exchange rate movements impact the earnings of TWE on a transactional and translational basis

(Moroney & Trotman, 2016).

Information security is vital for the protection of intellectual property and private data. Due to the advancements in technology and

communication channels, increasing amounts of private data is now stored electronically due to which confidentiality is a major issue and the

increasing rate of cyber crimes necessitate robust data security measures (Gay & Simnet, 2015).

The exposure of business operations to a number of environmental catastrophes and manmade hazards can lead to the disruption of business

and operations. Politically motivated violence can lead to the loss of key infrastructure, employees being harmed, customer dissatisfaction,

inventory shortages or loss and loss of finance and reputation (Gay & Simnet, 2015).

1.5 Use of an Expert

The auditors are responsible to express an opinion on the financial statements but a few technical areas in every business require the use of

the services of an expert. In the case of TWE, the use of expert can be considered for the following areas:

Adequacy of the assumptions and judgements made in relation to the key business planning prospects (Wright & Charles, 2012)

Impairments and contingences based upon the past experience and expected future performance which an expert in the respective field can

evaluate (Ghandhar & Tsahuridu, 2013).

Page 3 of 18

long. The unanticipated changes in customer preferences is a business risk as it can have adverse effects on the ability of the business to

capture growth opportunities and manage the orders and supplies.

Wine industry is a highly regulated industry which is exposed to the fulfilment and compliance with the various laws and regulations. Expansion

into new markets also means the exposure to the different regulations including taxation, manufacturing, marketing, advertising, distribution

and sale of wine. This requires the ongoing monitoring of the changes and updates in the regulations that can have a significant impact on the

nature of operations in these markets (Ghandhar & Tsahuridu, 2013).

1.4 Business Risks – Economy Level

TWE has business connections with more than 100 countries around the world. Hence foreign exchange risks from the key offshore markets

are a significant risk area. These foreign exchange rate movements impact the earnings of TWE on a transactional and translational basis

(Moroney & Trotman, 2016).

Information security is vital for the protection of intellectual property and private data. Due to the advancements in technology and

communication channels, increasing amounts of private data is now stored electronically due to which confidentiality is a major issue and the

increasing rate of cyber crimes necessitate robust data security measures (Gay & Simnet, 2015).

The exposure of business operations to a number of environmental catastrophes and manmade hazards can lead to the disruption of business

and operations. Politically motivated violence can lead to the loss of key infrastructure, employees being harmed, customer dissatisfaction,

inventory shortages or loss and loss of finance and reputation (Gay & Simnet, 2015).

1.5 Use of an Expert

The auditors are responsible to express an opinion on the financial statements but a few technical areas in every business require the use of

the services of an expert. In the case of TWE, the use of expert can be considered for the following areas:

Adequacy of the assumptions and judgements made in relation to the key business planning prospects (Wright & Charles, 2012)

Impairments and contingences based upon the past experience and expected future performance which an expert in the respective field can

evaluate (Ghandhar & Tsahuridu, 2013).

Page 3 of 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TREASURY WINE ESTATES LIMITED AUDIT PLAN

2.0 Preliminary Analytical Review

2.1 Formula used

(in words)

Actual Formula 2016

(in numbers)

Actual Formula 2017

(in numbers)

Results

2016

Results

2017

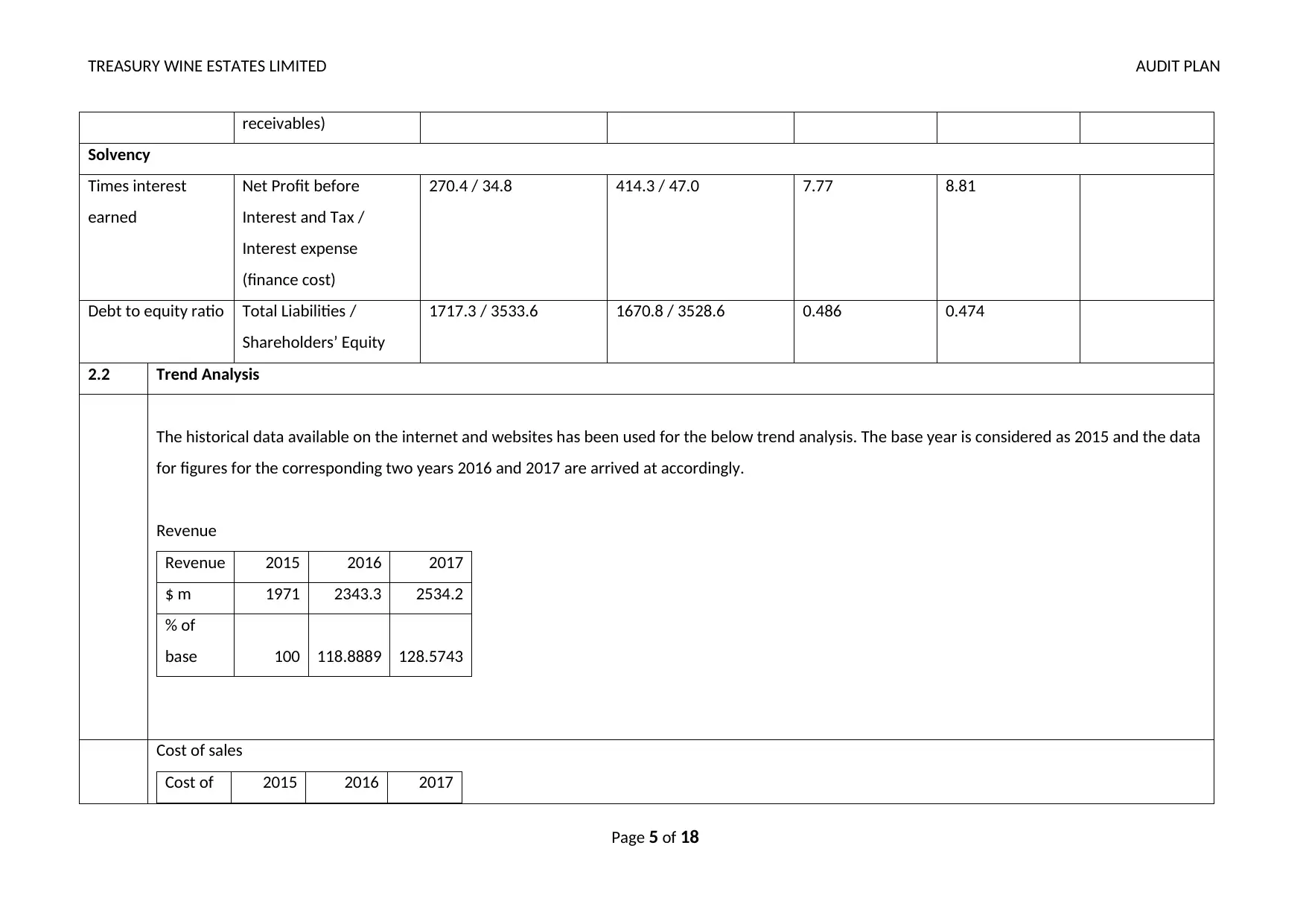

Profitability

Gross profit ratio Gross Profit / Net Sales

Revenue

826 / 2232.6 965.9 / 2401.7 0.3700 0.4022

Net profit ratio Net Profit after tax / Net

Sales Revenue

173.4 / 2232.6 269.1 / 2401.7 0.0776 0.1120

Return on assets Net Profit before

Interest and Tax / Total

Assets

270.4 / 5286.5 414.3 / 5279.3 0.0511 0.0785

Return on equity Net Profit After tax /

Ordinary Shareholders’

Equity

173.4 / 3533.6 269.9 / 3528.6 0.0490 0.0765

Liquidity

Current ratio Current Assets / Current

Liabilities

1827.6 / 761.5 1835.2 / 779.3 2.4 2.35

Quick asset ratio Liquid Assets / Current

Liabilities

(Cash and cash

equivalents plus trade

(256.1+603.4) / 761.5 (240.8+606.5) / 779.3 1.13 1.09

Page 4 of 18

2.0 Preliminary Analytical Review

2.1 Formula used

(in words)

Actual Formula 2016

(in numbers)

Actual Formula 2017

(in numbers)

Results

2016

Results

2017

Profitability

Gross profit ratio Gross Profit / Net Sales

Revenue

826 / 2232.6 965.9 / 2401.7 0.3700 0.4022

Net profit ratio Net Profit after tax / Net

Sales Revenue

173.4 / 2232.6 269.1 / 2401.7 0.0776 0.1120

Return on assets Net Profit before

Interest and Tax / Total

Assets

270.4 / 5286.5 414.3 / 5279.3 0.0511 0.0785

Return on equity Net Profit After tax /

Ordinary Shareholders’

Equity

173.4 / 3533.6 269.9 / 3528.6 0.0490 0.0765

Liquidity

Current ratio Current Assets / Current

Liabilities

1827.6 / 761.5 1835.2 / 779.3 2.4 2.35

Quick asset ratio Liquid Assets / Current

Liabilities

(Cash and cash

equivalents plus trade

(256.1+603.4) / 761.5 (240.8+606.5) / 779.3 1.13 1.09

Page 4 of 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TREASURY WINE ESTATES LIMITED AUDIT PLAN

receivables)

Solvency

Times interest

earned

Net Profit before

Interest and Tax /

Interest expense

(finance cost)

270.4 / 34.8 414.3 / 47.0 7.77 8.81

Debt to equity ratio Total Liabilities /

Shareholders’ Equity

1717.3 / 3533.6 1670.8 / 3528.6 0.486 0.474

2.2 Trend Analysis

The historical data available on the internet and websites has been used for the below trend analysis. The base year is considered as 2015 and the data

for figures for the corresponding two years 2016 and 2017 are arrived at accordingly.

Revenue

Revenue 2015 2016 2017

$ m 1971 2343.3 2534.2

% of

base 100 118.8889 128.5743

Cost of sales

Cost of 2015 2016 2017

Page 5 of 18

receivables)

Solvency

Times interest

earned

Net Profit before

Interest and Tax /

Interest expense

(finance cost)

270.4 / 34.8 414.3 / 47.0 7.77 8.81

Debt to equity ratio Total Liabilities /

Shareholders’ Equity

1717.3 / 3533.6 1670.8 / 3528.6 0.486 0.474

2.2 Trend Analysis

The historical data available on the internet and websites has been used for the below trend analysis. The base year is considered as 2015 and the data

for figures for the corresponding two years 2016 and 2017 are arrived at accordingly.

Revenue

Revenue 2015 2016 2017

$ m 1971 2343.3 2534.2

% of

base 100 118.8889 128.5743

Cost of sales

Cost of 2015 2016 2017

Page 5 of 18

TREASURY WINE ESTATES LIMITED AUDIT PLAN

Sales

$ m 1342.7 1517.3 1568.3

% of

base 100 113.0036 116.802

Gross profit

Gross

Profit 2015 2016 2017

$ m 628.3 826 965.9

% of

base 100 131.4659 153.7323

Total operating expenses

Total

Operating

Expenses 2015 2016 2017

$ m 1838.5 2072.9 2119.9

% of base 100 112.7495 115.306

Page 6 of 18

Sales

$ m 1342.7 1517.3 1568.3

% of

base 100 113.0036 116.802

Gross profit

Gross

Profit 2015 2016 2017

$ m 628.3 826 965.9

% of

base 100 131.4659 153.7323

Total operating expenses

Total

Operating

Expenses 2015 2016 2017

$ m 1838.5 2072.9 2119.9

% of base 100 112.7495 115.306

Page 6 of 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TREASURY WINE ESTATES LIMITED AUDIT PLAN

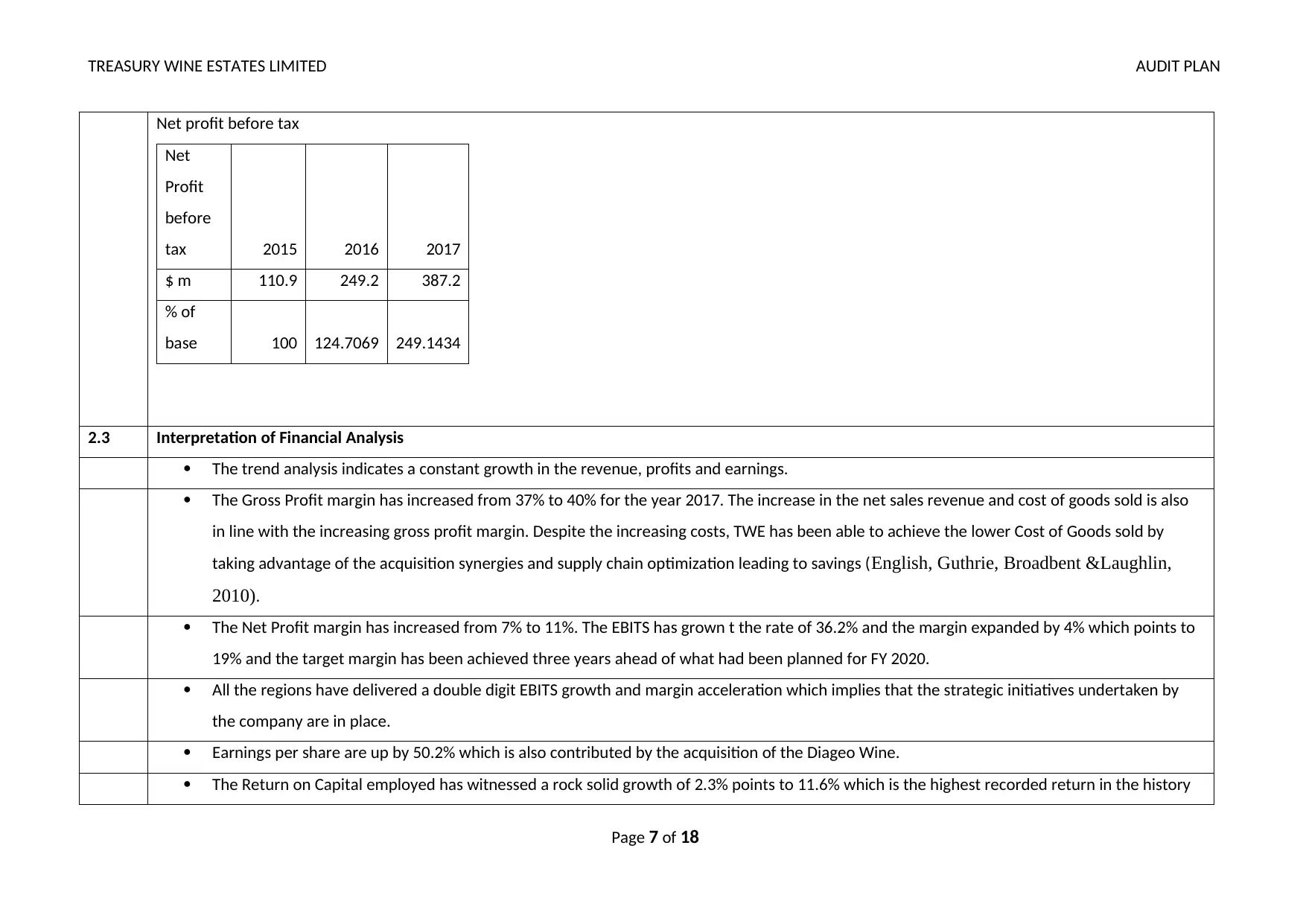

Net profit before tax

Net

Profit

before

tax 2015 2016 2017

$ m 110.9 249.2 387.2

% of

base 100 124.7069 249.1434

2.3 Interpretation of Financial Analysis

The trend analysis indicates a constant growth in the revenue, profits and earnings.

The Gross Profit margin has increased from 37% to 40% for the year 2017. The increase in the net sales revenue and cost of goods sold is also

in line with the increasing gross profit margin. Despite the increasing costs, TWE has been able to achieve the lower Cost of Goods sold by

taking advantage of the acquisition synergies and supply chain optimization leading to savings (English, Guthrie, Broadbent &Laughlin,

2010).

The Net Profit margin has increased from 7% to 11%. The EBITS has grown t the rate of 36.2% and the margin expanded by 4% which points to

19% and the target margin has been achieved three years ahead of what had been planned for FY 2020.

All the regions have delivered a double digit EBITS growth and margin acceleration which implies that the strategic initiatives undertaken by

the company are in place.

Earnings per share are up by 50.2% which is also contributed by the acquisition of the Diageo Wine.

The Return on Capital employed has witnessed a rock solid growth of 2.3% points to 11.6% which is the highest recorded return in the history

Page 7 of 18

Net profit before tax

Net

Profit

before

tax 2015 2016 2017

$ m 110.9 249.2 387.2

% of

base 100 124.7069 249.1434

2.3 Interpretation of Financial Analysis

The trend analysis indicates a constant growth in the revenue, profits and earnings.

The Gross Profit margin has increased from 37% to 40% for the year 2017. The increase in the net sales revenue and cost of goods sold is also

in line with the increasing gross profit margin. Despite the increasing costs, TWE has been able to achieve the lower Cost of Goods sold by

taking advantage of the acquisition synergies and supply chain optimization leading to savings (English, Guthrie, Broadbent &Laughlin,

2010).

The Net Profit margin has increased from 7% to 11%. The EBITS has grown t the rate of 36.2% and the margin expanded by 4% which points to

19% and the target margin has been achieved three years ahead of what had been planned for FY 2020.

All the regions have delivered a double digit EBITS growth and margin acceleration which implies that the strategic initiatives undertaken by

the company are in place.

Earnings per share are up by 50.2% which is also contributed by the acquisition of the Diageo Wine.

The Return on Capital employed has witnessed a rock solid growth of 2.3% points to 11.6% which is the highest recorded return in the history

Page 7 of 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TREASURY WINE ESTATES LIMITED AUDIT PLAN

of TWE.

The return on assets has seen an increase from 5% to 7% implying a better and more efficient utilization of the assets.

Current ratio and Quick Ratio have been almost in line with the previous year and is stronger than the industry average indicting the healthy

financial position and stability of the company (Elder, Beasley & Arens, 2010).

The corporate costs have increased by $6.8 million and the finance costs have also increased owing to the investment in Diageo Wine and the

new IT systems.

Despite the increasing costs, TWE has been able to deliver increasing NPAT and EPS.

The lower balance of cash and cash equivalents is due to fact of higher capital expenditure, higher dividends released and the profit growth

across all the regions.

Higher working capital is drive by higher inventory levels, lower payables and lower receivables reflecting better settlement terms and faster

movement of cash by TWE.

Thus an overall review of the operating and financial performance indicates a strong growth of TWE in all the areas of operation and the

company is well poised to achieve long term growth (Elder, Beasley & Arens, 2010).

3.0 Inherent Risk Assessment

3.1 Fraud Risk

Fraud risk is said to exist when all the three factors are present namely, opportunity to commit fraud, incentive to commit fraud and the

attitude to commit a fraud.

In cases where the company is making ongoing losses or the management is willing to window dress the financial statements and make it look

rosy by the use of unearned revenue or customer and employee dissatisfaction can lead to the occurrence of a fraud (Dauber, 2009).

But as TWE has displayed a strong financial growth and is also enjoying a positive reputation across regions and also on media, the instances of

committing a fraud get reduced (Dauber, 2009). There is no requirement for the management or the employees to adopt fraudulent

measures to achieve the desired results as the company is already achieving its targets by carrying out ethical business practices.

Page 8 of 18

of TWE.

The return on assets has seen an increase from 5% to 7% implying a better and more efficient utilization of the assets.

Current ratio and Quick Ratio have been almost in line with the previous year and is stronger than the industry average indicting the healthy

financial position and stability of the company (Elder, Beasley & Arens, 2010).

The corporate costs have increased by $6.8 million and the finance costs have also increased owing to the investment in Diageo Wine and the

new IT systems.

Despite the increasing costs, TWE has been able to deliver increasing NPAT and EPS.

The lower balance of cash and cash equivalents is due to fact of higher capital expenditure, higher dividends released and the profit growth

across all the regions.

Higher working capital is drive by higher inventory levels, lower payables and lower receivables reflecting better settlement terms and faster

movement of cash by TWE.

Thus an overall review of the operating and financial performance indicates a strong growth of TWE in all the areas of operation and the

company is well poised to achieve long term growth (Elder, Beasley & Arens, 2010).

3.0 Inherent Risk Assessment

3.1 Fraud Risk

Fraud risk is said to exist when all the three factors are present namely, opportunity to commit fraud, incentive to commit fraud and the

attitude to commit a fraud.

In cases where the company is making ongoing losses or the management is willing to window dress the financial statements and make it look

rosy by the use of unearned revenue or customer and employee dissatisfaction can lead to the occurrence of a fraud (Dauber, 2009).

But as TWE has displayed a strong financial growth and is also enjoying a positive reputation across regions and also on media, the instances of

committing a fraud get reduced (Dauber, 2009). There is no requirement for the management or the employees to adopt fraudulent

measures to achieve the desired results as the company is already achieving its targets by carrying out ethical business practices.

Page 8 of 18

TREASURY WINE ESTATES LIMITED AUDIT PLAN

The strong corporate governance framework and the compliance with ASX guidelines mitigate the opportunities and incentives to commit a

fraud. Thus the overall fraud risk for TWE is low.

3.2 Going Concern Risk

ASA 570 Paragraph 10 requires the auditor to assess the risk regarding the going concern nature of the entity. A company can be said to be at

the risk of going concern if it is having ongoing losses or high debts and poor performance and such indicators which pose a question on the

existence of the company in the future years (Cooper & Coram, 2015).

TWE is not having any such indicators which point out towards the winding up of the company in the near foreseeable future. It is enjoying

strong profits, revenue and cash position. Thus the going concern risk is low.

3.3 Related Parties Risk

TWE has a list of subsidiaries and the material ownership interests in the same are disclosed in Note 28 of the Annual Report. The transactions

entered into with the related parties are insignificant in amounts with the Executive and non executive directors and within the normal range

with the employees, customers and suppliers. All the transactions are carried out at an arm’s length price. These transactions include payment

of salaries and benefits and purchase of group products. Some of the directors of TWE who are also directors in these subsidiaries with whom

TWE has carried out transactions believe that they do not have the individual capacity to control or significantly influence the financial policies

of those companies (Cooper & Coram, 2015). Hence the transactions do not fall under the disclosure requirements of the Corporations Act

2001.

Thus the related parties risk is also classified at a low range.

3.4 Inherent Risk Assessment

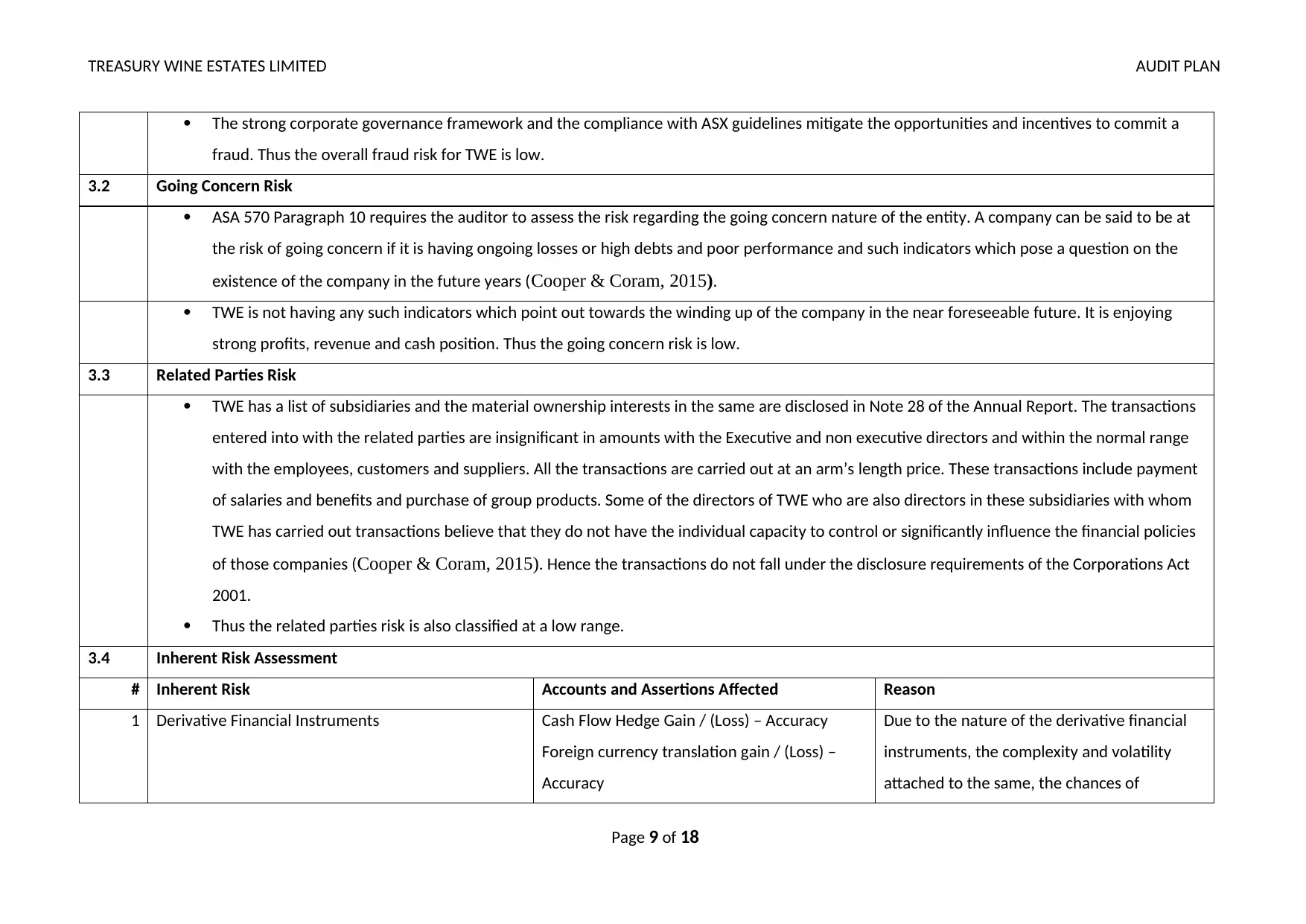

# Inherent Risk Accounts and Assertions Affected Reason

1 Derivative Financial Instruments Cash Flow Hedge Gain / (Loss) – Accuracy

Foreign currency translation gain / (Loss) –

Accuracy

Due to the nature of the derivative financial

instruments, the complexity and volatility

attached to the same, the chances of

Page 9 of 18

The strong corporate governance framework and the compliance with ASX guidelines mitigate the opportunities and incentives to commit a

fraud. Thus the overall fraud risk for TWE is low.

3.2 Going Concern Risk

ASA 570 Paragraph 10 requires the auditor to assess the risk regarding the going concern nature of the entity. A company can be said to be at

the risk of going concern if it is having ongoing losses or high debts and poor performance and such indicators which pose a question on the

existence of the company in the future years (Cooper & Coram, 2015).

TWE is not having any such indicators which point out towards the winding up of the company in the near foreseeable future. It is enjoying

strong profits, revenue and cash position. Thus the going concern risk is low.

3.3 Related Parties Risk

TWE has a list of subsidiaries and the material ownership interests in the same are disclosed in Note 28 of the Annual Report. The transactions

entered into with the related parties are insignificant in amounts with the Executive and non executive directors and within the normal range

with the employees, customers and suppliers. All the transactions are carried out at an arm’s length price. These transactions include payment

of salaries and benefits and purchase of group products. Some of the directors of TWE who are also directors in these subsidiaries with whom

TWE has carried out transactions believe that they do not have the individual capacity to control or significantly influence the financial policies

of those companies (Cooper & Coram, 2015). Hence the transactions do not fall under the disclosure requirements of the Corporations Act

2001.

Thus the related parties risk is also classified at a low range.

3.4 Inherent Risk Assessment

# Inherent Risk Accounts and Assertions Affected Reason

1 Derivative Financial Instruments Cash Flow Hedge Gain / (Loss) – Accuracy

Foreign currency translation gain / (Loss) –

Accuracy

Due to the nature of the derivative financial

instruments, the complexity and volatility

attached to the same, the chances of

Page 9 of 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TREASURY WINE ESTATES LIMITED AUDIT PLAN

Interest and other costs - Accuracy misrepresentation becomes high. Irrespective

of the valuation and disclosure guidelines laid

down, the company should be able to meet its

obligations when it falls due. TWE is thus

exposed to liquidity risk from its core

operating activities (Christensen, 2011).

2 Interest rate risk Bank Overdraft

US Private Placement Notes

Bank Loans

Floating rate agreements including receivable

purchasing agreements, interest bearing

investments, creditors and debtors accounts

offering discounts are exposed to interest rate

risk (Cappelleto, 2010).

3 Foreign Exchange Risk Trade Receivables

Trade Payables

Borrowings

All transactions denominated in foreign

currencies and also earnings from foreign

subsidiaries, revaluation of monetary assets

and liabilities are impacted by this risk

(Christensen, 2011).

4 Credit Risk Cash and cash equivalents

Trade and other receivables

Derivative instruments

The risk of default by any party and setting

limits within which the transaction can take

place, risk of dishonour and such other

volatile risk factors exists (Cappelleto, 2010).

3.5 Inherent Risk Conclusion

TWE is having risk mitigation policy for each type of the risk discussed above and so it is able to meet the uncertainties and contingencies to

Page 10 of 18

Interest and other costs - Accuracy misrepresentation becomes high. Irrespective

of the valuation and disclosure guidelines laid

down, the company should be able to meet its

obligations when it falls due. TWE is thus

exposed to liquidity risk from its core

operating activities (Christensen, 2011).

2 Interest rate risk Bank Overdraft

US Private Placement Notes

Bank Loans

Floating rate agreements including receivable

purchasing agreements, interest bearing

investments, creditors and debtors accounts

offering discounts are exposed to interest rate

risk (Cappelleto, 2010).

3 Foreign Exchange Risk Trade Receivables

Trade Payables

Borrowings

All transactions denominated in foreign

currencies and also earnings from foreign

subsidiaries, revaluation of monetary assets

and liabilities are impacted by this risk

(Christensen, 2011).

4 Credit Risk Cash and cash equivalents

Trade and other receivables

Derivative instruments

The risk of default by any party and setting

limits within which the transaction can take

place, risk of dishonour and such other

volatile risk factors exists (Cappelleto, 2010).

3.5 Inherent Risk Conclusion

TWE is having risk mitigation policy for each type of the risk discussed above and so it is able to meet the uncertainties and contingencies to

Page 10 of 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TREASURY WINE ESTATES LIMITED AUDIT PLAN

the extent possible. Due to the systematic set of steps undertaken, the inherent risk can be said to be at a minimum level.

4.0 Control Risk Assessment

4.1 Entity Level Internal Controls

The Corporate Governance framework is in line with the ASX policies and recommendations.

The directors are responsible for the implementation of the necessary internal controls that give a true and fair view of the financial

statements that is free from material misstatement.

The Audit and Risk management committee is also responsible for carrying out the internal audit function to ensure that the controls are in

place and a majority of the directors in this committee are independent directors (Baldwin, 2010).

Their scope of activities also includes overseeing and reviewing the working of internal controls and identification of new areas wherein

controls are required.

4.2 Control Risk Conclusion

Thus TWE is having a strong internal control set up and hence the control risk is detected to be low.

5.0 Audit Strategy

5.1 Risk Profile

Audit risk is a combined function of inherent risk and control risk. In the case of TWE, since inherent risk is assessed to be medium and control

risk is assesses to be low, the overall audit risk can also be judged to be at a low level (Arens, Best, Shailer & Loebbecke, 2013).

A moderate level of detection risk also requires the collection of moderate to high level of evidence.

5.2 Audit Strategy

The inherent risks will always exist and hence the reasonable level of preparedness of the company in terms of risk mitigation needs to be

audited. The control risk needs o be audited in terms of the extent of relance that can be placed on the existing internal controls and also the

loopholes in the same (Baldwin, 2010).

Thus an extensive controls testing can confirm the same and if more reliance can be placed on the internal controls then less substantive

Page 11 of 18

the extent possible. Due to the systematic set of steps undertaken, the inherent risk can be said to be at a minimum level.

4.0 Control Risk Assessment

4.1 Entity Level Internal Controls

The Corporate Governance framework is in line with the ASX policies and recommendations.

The directors are responsible for the implementation of the necessary internal controls that give a true and fair view of the financial

statements that is free from material misstatement.

The Audit and Risk management committee is also responsible for carrying out the internal audit function to ensure that the controls are in

place and a majority of the directors in this committee are independent directors (Baldwin, 2010).

Their scope of activities also includes overseeing and reviewing the working of internal controls and identification of new areas wherein

controls are required.

4.2 Control Risk Conclusion

Thus TWE is having a strong internal control set up and hence the control risk is detected to be low.

5.0 Audit Strategy

5.1 Risk Profile

Audit risk is a combined function of inherent risk and control risk. In the case of TWE, since inherent risk is assessed to be medium and control

risk is assesses to be low, the overall audit risk can also be judged to be at a low level (Arens, Best, Shailer & Loebbecke, 2013).

A moderate level of detection risk also requires the collection of moderate to high level of evidence.

5.2 Audit Strategy

The inherent risks will always exist and hence the reasonable level of preparedness of the company in terms of risk mitigation needs to be

audited. The control risk needs o be audited in terms of the extent of relance that can be placed on the existing internal controls and also the

loopholes in the same (Baldwin, 2010).

Thus an extensive controls testing can confirm the same and if more reliance can be placed on the internal controls then less substantive

Page 11 of 18

TREASURY WINE ESTATES LIMITED AUDIT PLAN

procedures need to be undertaken. If the control risk is high, then more substantive tests need to be undertaken.

6.0 Overall Materiality

6.1 Base Selected

For a publicly listed company like TWE, Profit before tax can be used as a base for materiality.

The financial statements for the year 2017 have reported profit before tax of $387.2 million.

6.2 Overall Materiality

The relevant base chosen is 5% to 10% of the profits.

Upon application of this to the profit before tax, the materiality range is calculated between $19.36 million and $38.72 million.

The overall materiality is set at $29 million which is just the midpoint in this range.

6.3 Relationship to Risk Assessment

As the detection risk is at a moderate to low level, the materiality has also been set up accordingly to a low to moderate level.

Other Assurance Services

Considering the range and expansion of operations of TWE into various countries, the services of an expert are required in the areas where the audit firm might

not be able to visit physically. Such instances are confirmation of valuations of tangible and intangible assets, and ASA 620 (Using the work of auditor’s expert)

and ASA 600 (Special Considerations – Audits of Group Financial Reports) need to be complied with.

Apart from this, the statutory auditors, KPMG have also provided non audit services and been remunerated for the same. But an undertaking in the annual

report states that none of these non audit services are likely to interfere with the carrying out of the audit functions and both these areas are treated as

independent.

Reference List

Arens, A. A, Best, P. J, Shailer, G. E. P & Loebbecke, J. K. (2013) Assurance Services and Ethics in Australia, 9th ed, Australia: Pearson.

Baldwin, S. (2010) Doing a content audit or inventory. Pearson Press.

Page 12 of 18

procedures need to be undertaken. If the control risk is high, then more substantive tests need to be undertaken.

6.0 Overall Materiality

6.1 Base Selected

For a publicly listed company like TWE, Profit before tax can be used as a base for materiality.

The financial statements for the year 2017 have reported profit before tax of $387.2 million.

6.2 Overall Materiality

The relevant base chosen is 5% to 10% of the profits.

Upon application of this to the profit before tax, the materiality range is calculated between $19.36 million and $38.72 million.

The overall materiality is set at $29 million which is just the midpoint in this range.

6.3 Relationship to Risk Assessment

As the detection risk is at a moderate to low level, the materiality has also been set up accordingly to a low to moderate level.

Other Assurance Services

Considering the range and expansion of operations of TWE into various countries, the services of an expert are required in the areas where the audit firm might

not be able to visit physically. Such instances are confirmation of valuations of tangible and intangible assets, and ASA 620 (Using the work of auditor’s expert)

and ASA 600 (Special Considerations – Audits of Group Financial Reports) need to be complied with.

Apart from this, the statutory auditors, KPMG have also provided non audit services and been remunerated for the same. But an undertaking in the annual

report states that none of these non audit services are likely to interfere with the carrying out of the audit functions and both these areas are treated as

independent.

Reference List

Arens, A. A, Best, P. J, Shailer, G. E. P & Loebbecke, J. K. (2013) Assurance Services and Ethics in Australia, 9th ed, Australia: Pearson.

Baldwin, S. (2010) Doing a content audit or inventory. Pearson Press.

Page 12 of 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.