Treasury Wine Estates Ltd. (TWE) Valuation Report - FIN2SEV

VerifiedAdded on 2022/10/10

|16

|2530

|91

Report

AI Summary

This report provides a detailed analysis of Treasury Wine Estates Ltd (TWE), a major player in the global wine industry. It begins with an introduction and industry overview, examining external factors and competitive positioning. The report delves into the financial analysis of TWE, including ratio analysis and projections based on historical data. Valuation is assessed using P/E and EV/EBITDA ratios. The report also addresses investment risks and concludes with a summary of findings and recommendations. The analysis incorporates data from 2018 and 2019, projecting future performance based on various assumptions. The report provides a comprehensive assessment of TWE's financial health and investment potential, covering aspects such as political, economic, social, and technological factors impacting the company.

INVESTMENT SECURITIES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TREASURY WINE ESTATES LTD: 1

Contents

Introduction...........................................................................................................................................2

Industry overview..................................................................................................................................2

Analysis of external factors...................................................................................................................3

Competitive analysis.............................................................................................................................5

Financial analysis..................................................................................................................................7

Valuation...............................................................................................................................................8

Investment risk......................................................................................................................................9

Conclusion.............................................................................................................................................9

References...........................................................................................................................................11

Appendix.............................................................................................................................................13

Contents

Introduction...........................................................................................................................................2

Industry overview..................................................................................................................................2

Analysis of external factors...................................................................................................................3

Competitive analysis.............................................................................................................................5

Financial analysis..................................................................................................................................7

Valuation...............................................................................................................................................8

Investment risk......................................................................................................................................9

Conclusion.............................................................................................................................................9

References...........................................................................................................................................11

Appendix.............................................................................................................................................13

TREASURY WINE ESTATES LTD: 2

Introduction

Treasury wine estates is the largest wine corporation as listed on ASX enabled with global

distribution headquartered in Australia founded in 2011 with the revenue of 2.5 billion dollars

in 2017 and $2.3 billion of net income in 2016. The company is formerly as wine division of

brewing organisation as “Foster`s Group”. The company operates in 70 countries in four

main regions including Europe, Asia, New Zealand, and Australia (Treasury wine estates

limited, 2017). The company employs more than 3400 people with 13000-planted hectares of

vineyards in the wine making regions. The report brings out a discussion on treasury wine

estates and its financial analysis Creditriskmonitor, 2019). This analysis includes dividend

discount model, P/E ratio, external situational factors, ratio analysis based on its historical

data for 2018 and 2019. Further, there is a projection made which is based on certain

assumption and appropriate to the data of the annual reports of 2019. To analyse the valuation

of company, the report has used P/E ratio and EV/EBITDA ratio (Chua, DE Lisle, Feng, &

Lee, 2015).

Industry overview

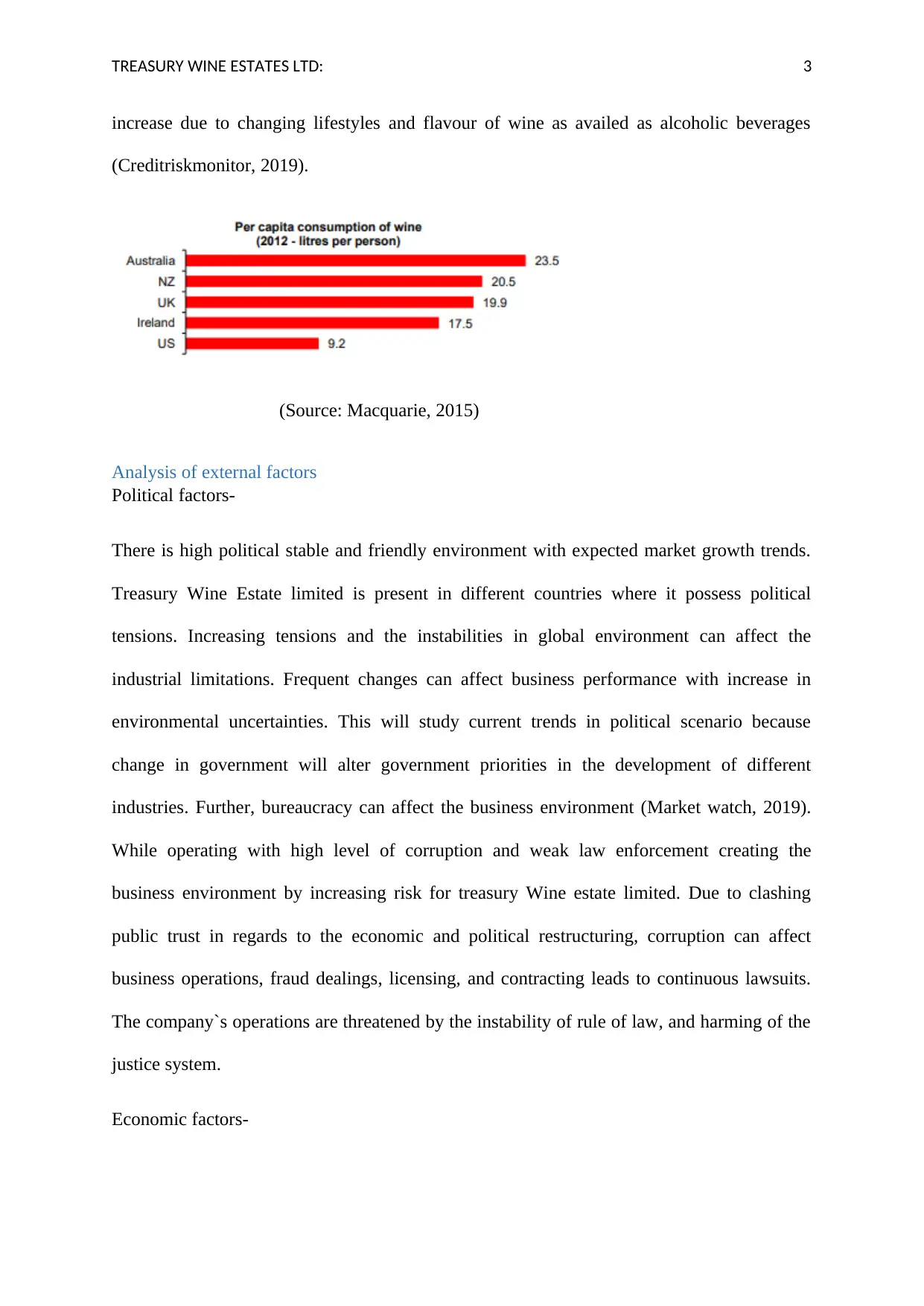

Domestic consumption of wine keeps increasing with the increase in the Australian per capita

income that shows upside in the current consumption level. Exports have become important

for critically increasing the Australian wine industry (macquarie.com, 2015). For the last 25

years of growth in the Australian wine industry, it is seen that it is directly related to the

demand of the export. The exports has been increased from 16 percent to 60 percent of total

wine sales of Australians (macquarie.com, 2015). The global industry of wine was primarily

engaged in the manufacturing wines, and brandy spirits that has crossed 300 USD millions

until 2017. Asian markets have been fighting to catch up to market leader “North America” in

terms of market share and regional markets. It is seen that demand for wine continues to

Introduction

Treasury wine estates is the largest wine corporation as listed on ASX enabled with global

distribution headquartered in Australia founded in 2011 with the revenue of 2.5 billion dollars

in 2017 and $2.3 billion of net income in 2016. The company is formerly as wine division of

brewing organisation as “Foster`s Group”. The company operates in 70 countries in four

main regions including Europe, Asia, New Zealand, and Australia (Treasury wine estates

limited, 2017). The company employs more than 3400 people with 13000-planted hectares of

vineyards in the wine making regions. The report brings out a discussion on treasury wine

estates and its financial analysis Creditriskmonitor, 2019). This analysis includes dividend

discount model, P/E ratio, external situational factors, ratio analysis based on its historical

data for 2018 and 2019. Further, there is a projection made which is based on certain

assumption and appropriate to the data of the annual reports of 2019. To analyse the valuation

of company, the report has used P/E ratio and EV/EBITDA ratio (Chua, DE Lisle, Feng, &

Lee, 2015).

Industry overview

Domestic consumption of wine keeps increasing with the increase in the Australian per capita

income that shows upside in the current consumption level. Exports have become important

for critically increasing the Australian wine industry (macquarie.com, 2015). For the last 25

years of growth in the Australian wine industry, it is seen that it is directly related to the

demand of the export. The exports has been increased from 16 percent to 60 percent of total

wine sales of Australians (macquarie.com, 2015). The global industry of wine was primarily

engaged in the manufacturing wines, and brandy spirits that has crossed 300 USD millions

until 2017. Asian markets have been fighting to catch up to market leader “North America” in

terms of market share and regional markets. It is seen that demand for wine continues to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TREASURY WINE ESTATES LTD: 3

increase due to changing lifestyles and flavour of wine as availed as alcoholic beverages

(Creditriskmonitor, 2019).

(Source: Macquarie, 2015)

Analysis of external factors

Political factors-

There is high political stable and friendly environment with expected market growth trends.

Treasury Wine Estate limited is present in different countries where it possess political

tensions. Increasing tensions and the instabilities in global environment can affect the

industrial limitations. Frequent changes can affect business performance with increase in

environmental uncertainties. This will study current trends in political scenario because

change in government will alter government priorities in the development of different

industries. Further, bureaucracy can affect the business environment (Market watch, 2019).

While operating with high level of corruption and weak law enforcement creating the

business environment by increasing risk for treasury Wine estate limited. Due to clashing

public trust in regards to the economic and political restructuring, corruption can affect

business operations, fraud dealings, licensing, and contracting leads to continuous lawsuits.

The company`s operations are threatened by the instability of rule of law, and harming of the

justice system.

Economic factors-

increase due to changing lifestyles and flavour of wine as availed as alcoholic beverages

(Creditriskmonitor, 2019).

(Source: Macquarie, 2015)

Analysis of external factors

Political factors-

There is high political stable and friendly environment with expected market growth trends.

Treasury Wine Estate limited is present in different countries where it possess political

tensions. Increasing tensions and the instabilities in global environment can affect the

industrial limitations. Frequent changes can affect business performance with increase in

environmental uncertainties. This will study current trends in political scenario because

change in government will alter government priorities in the development of different

industries. Further, bureaucracy can affect the business environment (Market watch, 2019).

While operating with high level of corruption and weak law enforcement creating the

business environment by increasing risk for treasury Wine estate limited. Due to clashing

public trust in regards to the economic and political restructuring, corruption can affect

business operations, fraud dealings, licensing, and contracting leads to continuous lawsuits.

The company`s operations are threatened by the instability of rule of law, and harming of the

justice system.

Economic factors-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TREASURY WINE ESTATES LTD: 4

Increasing economic and growth opportunities to Treasury Wine estate limited can affect

opportunities to Treasury Wine estate limited. Entering in mature industry can become more

challenging because of market saturation at the growth stage. The performance of Treasury

Wine estate limited is affected to extent where government of host country spent time on the

development of core infrastructure. GDP will decide the ability of treasury Wine estate

limited to pursue the long-term enhancement strategies. High GDP signals customer`s ability

to spend more on the offered products. High GDP indicates that there is the availability of

customers to consume more products. Higher employment rate signals the availability of the

surplus workforce at lower wages. The company will have to bear lower production cost,

interest rate, impact on the borrowing attitude in regards to investment. High rate of interest

will further encourage attitude to investment and it will increase the growth opportunities for

the company. The exchange fluctuation rate can affect the profitability of international trade.

The business actions can be affected by prevailing economic structure. The regulatory and

economic environment differs in different market such as oligopolistic and monopolistic

structure.

Social factors

The company is affected by the demographic trends, gender roles, equality, and power

distance, pattern of spending, online shopping, class distribution, and societal norms.

Dynamic situation such as patterns in the ageing population, social, and economic variables,

which have paramount significant for international companies. Marketing strategy is

influenced through migration. Further, it is quite important to perceive the people`s attitude

when it can affect organisation`s ability to bring the international managers to the host

country. Power distance shows the acceptance of the income inequality. The company will

have to adjust the business management practises when entering market with low and high

power distance. According to the cultural context, the company develops local partnership to

Increasing economic and growth opportunities to Treasury Wine estate limited can affect

opportunities to Treasury Wine estate limited. Entering in mature industry can become more

challenging because of market saturation at the growth stage. The performance of Treasury

Wine estate limited is affected to extent where government of host country spent time on the

development of core infrastructure. GDP will decide the ability of treasury Wine estate

limited to pursue the long-term enhancement strategies. High GDP signals customer`s ability

to spend more on the offered products. High GDP indicates that there is the availability of

customers to consume more products. Higher employment rate signals the availability of the

surplus workforce at lower wages. The company will have to bear lower production cost,

interest rate, impact on the borrowing attitude in regards to investment. High rate of interest

will further encourage attitude to investment and it will increase the growth opportunities for

the company. The exchange fluctuation rate can affect the profitability of international trade.

The business actions can be affected by prevailing economic structure. The regulatory and

economic environment differs in different market such as oligopolistic and monopolistic

structure.

Social factors

The company is affected by the demographic trends, gender roles, equality, and power

distance, pattern of spending, online shopping, class distribution, and societal norms.

Dynamic situation such as patterns in the ageing population, social, and economic variables,

which have paramount significant for international companies. Marketing strategy is

influenced through migration. Further, it is quite important to perceive the people`s attitude

when it can affect organisation`s ability to bring the international managers to the host

country. Power distance shows the acceptance of the income inequality. The company will

have to adjust the business management practises when entering market with low and high

power distance. According to the cultural context, the company develops local partnership to

TREASURY WINE ESTATES LTD: 5

understand societal attitude to construct the marketing strategies. Treasury wine estates offer

luxury items at the premium prices to the market where high ending market is smaller and

needs the company to adopt the niche marketing strategies. The advent of electronic media

has permitted online shopping to consider the differences as their young consumers who are

more inclined to grab older customers. The company should invest on the understanding of

the consumption motivation that has been defining consumption behaviour. The company

will have to attempt to grab the extent of the consumer`s interest to check customers prefer

experimental offerings over traditional offerings (Sim, & Wright, 2017).

Technological factors-

Some of the important inducing factors affecting the technological factors are social media

marketing, innovation in technological development, research, development affect the value

chain, cost structure and the shortened life cycles of products. Treasury Wine estate limited

will have to consider investments as made by the competitors at both micro and macro level

when understanding how technology transform organisation’s value chain (Mugoša, &

Popović, 2015). The adoption of effective technology can reduce the lifecycle of new product

development. It pressurises the company to develop and create new products by increasing

diversity of product range, developing healthy relationships between integrating flexibility in

the value chain, enabled with partners. The company has to invest in creative disruption

where it can maximise the profitability and finally reinvest profits for the future disruption

(Mugoša, & Popović, 2015).

Competitive analysis

Threat of new entrants-

The economies of scale is difficult to achieve such an industry where treasury Wine Estates

operate. This does it in the easier way for those producing greater capacities so that they can

understand societal attitude to construct the marketing strategies. Treasury wine estates offer

luxury items at the premium prices to the market where high ending market is smaller and

needs the company to adopt the niche marketing strategies. The advent of electronic media

has permitted online shopping to consider the differences as their young consumers who are

more inclined to grab older customers. The company should invest on the understanding of

the consumption motivation that has been defining consumption behaviour. The company

will have to attempt to grab the extent of the consumer`s interest to check customers prefer

experimental offerings over traditional offerings (Sim, & Wright, 2017).

Technological factors-

Some of the important inducing factors affecting the technological factors are social media

marketing, innovation in technological development, research, development affect the value

chain, cost structure and the shortened life cycles of products. Treasury Wine estate limited

will have to consider investments as made by the competitors at both micro and macro level

when understanding how technology transform organisation’s value chain (Mugoša, &

Popović, 2015). The adoption of effective technology can reduce the lifecycle of new product

development. It pressurises the company to develop and create new products by increasing

diversity of product range, developing healthy relationships between integrating flexibility in

the value chain, enabled with partners. The company has to invest in creative disruption

where it can maximise the profitability and finally reinvest profits for the future disruption

(Mugoša, & Popović, 2015).

Competitive analysis

Threat of new entrants-

The economies of scale is difficult to achieve such an industry where treasury Wine Estates

operate. This does it in the easier way for those producing greater capacities so that they can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TREASURY WINE ESTATES LTD: 6

have higher cost advantage. This can create it easy for the producing greater capacities in

order to have cost advantage (Houmes, R., & Chira, 2015).

Bargaining power of the suppliers-

The number of the suppliers operates more as compared to the number of organisation’s

producing products. This results into few organisations to choose from which do not control

the prices (Houmes, R., & Chira, 2015).

Bargaining power of the customers-

The buying behaviour of the people is determined by their income level. The quality of

products is quite important to make people in such a way that they can make frequent

purchases. Although, there is not significant threat of customers to integrate it backwards.

The company can emphasis on differentiation and innovation to induce the buyers. The

company can build larger customer base, as the power of customers is quite weak. The

company can take advantage of the economies of scale in order to develop cost advantage

and sell it at lower price to the buyers who earn less. This will lead to induce large number of

customers.

Threat of substitution-

There are many other substitution availed as their products where Treasury Wine estates

operate. There is no other ceiling on the maximum profit to be earned where the company

operates. Threat of substitution is a weaker force in the industry. Few substitutes’ availability

are of high quality but at the same time, it is expensive too. Treasury wine estates operate

selling lower price as compared to the substitutes. It is seen that buyers are less likely to

switch to the substitute products.

have higher cost advantage. This can create it easy for the producing greater capacities in

order to have cost advantage (Houmes, R., & Chira, 2015).

Bargaining power of the suppliers-

The number of the suppliers operates more as compared to the number of organisation’s

producing products. This results into few organisations to choose from which do not control

the prices (Houmes, R., & Chira, 2015).

Bargaining power of the customers-

The buying behaviour of the people is determined by their income level. The quality of

products is quite important to make people in such a way that they can make frequent

purchases. Although, there is not significant threat of customers to integrate it backwards.

The company can emphasis on differentiation and innovation to induce the buyers. The

company can build larger customer base, as the power of customers is quite weak. The

company can take advantage of the economies of scale in order to develop cost advantage

and sell it at lower price to the buyers who earn less. This will lead to induce large number of

customers.

Threat of substitution-

There are many other substitution availed as their products where Treasury Wine estates

operate. There is no other ceiling on the maximum profit to be earned where the company

operates. Threat of substitution is a weaker force in the industry. Few substitutes’ availability

are of high quality but at the same time, it is expensive too. Treasury wine estates operate

selling lower price as compared to the substitutes. It is seen that buyers are less likely to

switch to the substitute products.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TREASURY WINE ESTATES LTD: 7

In order to tackle threat of substitution, the company has to focus on availing greater quality

in their products. Customers choose from the products that can avail high quality to the

products. The company has to focus on differentiating the products. This will ensure buyer’s

overview the products as unique and it do not shift to substitute products leading it to avail

unique benefits. It can avail unique benefits to the customers with better understanding the

need through research and availing what actually a customer needs.

Rivalry among the competitors

Some of the important competitors include constellation brands, Wine group, E & J. Gallo.

The competitors operating in this industry are very few and they are large. This results into

weaker force in the rivalry among the existing organisations, which stimulates companies to

become stronger and become market leaders. Treasury wine estates operate with fixed costs

to push it to full extent. Treasury wine estate offers highly differentiated products. It is

difficult to compete to the organisations to win maximum customers as every organisation

produces differentiated products. In order to handle the rivalry between the existing

companies, it is seen that there is a need to create market research so that it can understand

the demand and supply in the industry. As there is, rivalry among the existing companies is

intense, which will drive prices down and reduce the overall profitability of industry

(Edwards, Schwab, & Shevlin, 2015).

Financial analysis

The projection statements of the company for the upcoming three years 2020, 2021, and 2022

are based on major Assumptions-

As far as sales is considered, it has been assumed that sales of company in 2019 is $2883000

and it is estimated that it will increase by 10 percent in 2020. Further, for the upcoming years

2021 and 2022, the revenue will increase by 20 percent.

In order to tackle threat of substitution, the company has to focus on availing greater quality

in their products. Customers choose from the products that can avail high quality to the

products. The company has to focus on differentiating the products. This will ensure buyer’s

overview the products as unique and it do not shift to substitute products leading it to avail

unique benefits. It can avail unique benefits to the customers with better understanding the

need through research and availing what actually a customer needs.

Rivalry among the competitors

Some of the important competitors include constellation brands, Wine group, E & J. Gallo.

The competitors operating in this industry are very few and they are large. This results into

weaker force in the rivalry among the existing organisations, which stimulates companies to

become stronger and become market leaders. Treasury wine estates operate with fixed costs

to push it to full extent. Treasury wine estate offers highly differentiated products. It is

difficult to compete to the organisations to win maximum customers as every organisation

produces differentiated products. In order to handle the rivalry between the existing

companies, it is seen that there is a need to create market research so that it can understand

the demand and supply in the industry. As there is, rivalry among the existing companies is

intense, which will drive prices down and reduce the overall profitability of industry

(Edwards, Schwab, & Shevlin, 2015).

Financial analysis

The projection statements of the company for the upcoming three years 2020, 2021, and 2022

are based on major Assumptions-

As far as sales is considered, it has been assumed that sales of company in 2019 is $2883000

and it is estimated that it will increase by 10 percent in 2020. Further, for the upcoming years

2021 and 2022, the revenue will increase by 20 percent.

TREASURY WINE ESTATES LTD: 8

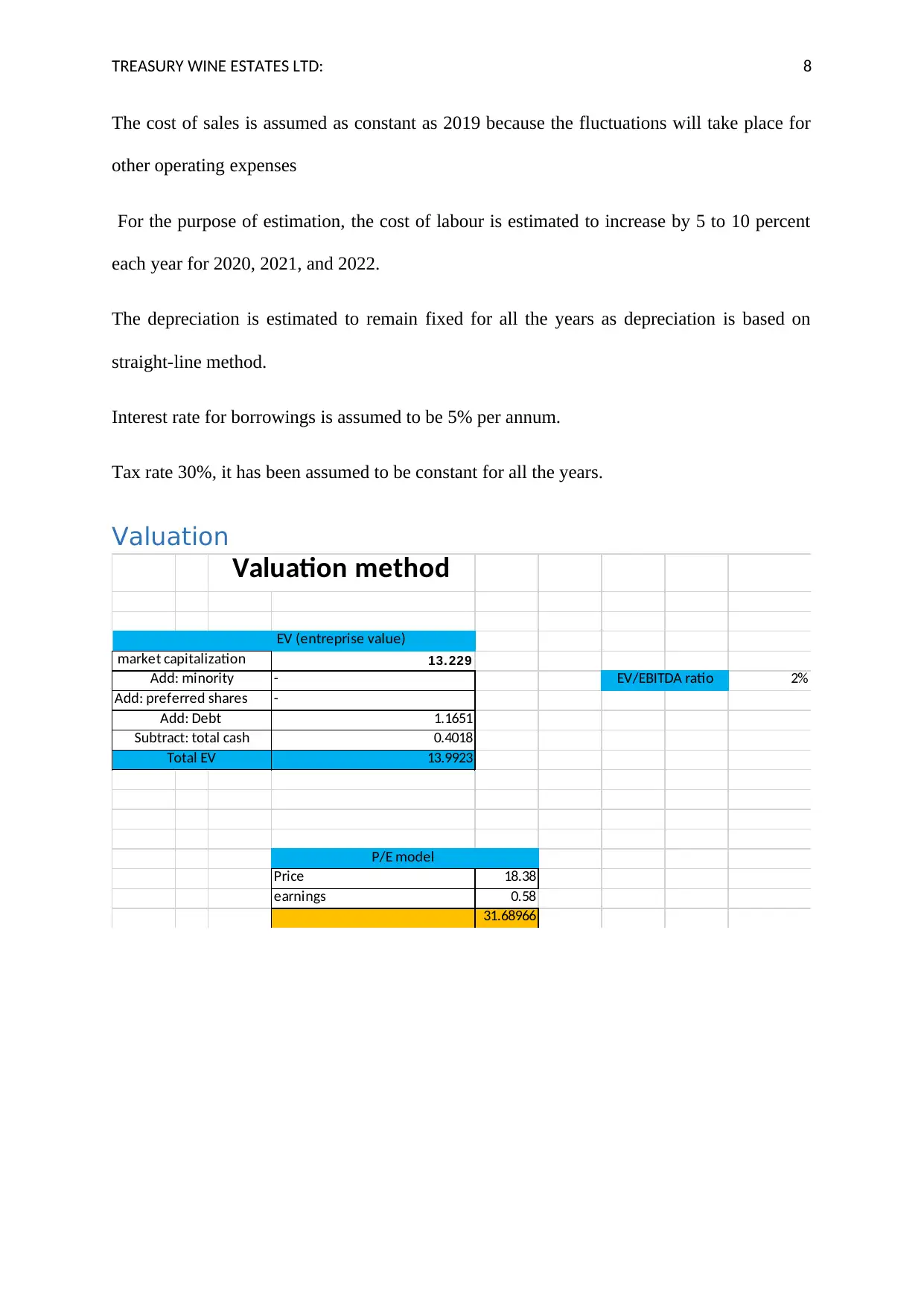

The cost of sales is assumed as constant as 2019 because the fluctuations will take place for

other operating expenses

For the purpose of estimation, the cost of labour is estimated to increase by 5 to 10 percent

each year for 2020, 2021, and 2022.

The depreciation is estimated to remain fixed for all the years as depreciation is based on

straight-line method.

Interest rate for borrowings is assumed to be 5% per annum.

Tax rate 30%, it has been assumed to be constant for all the years.

Valuation

market capitalization 13. 229

- 2%

Add: preferred shares -

1.1651

0.4018

13.9923

Price 18.38

earnings 0.58

31.68966

EV/EBITDA ratio

P/E model

Valuation method

EV (entreprise value)

Add: minority

Add: Debt

Subtract: total cash

Total EV

The cost of sales is assumed as constant as 2019 because the fluctuations will take place for

other operating expenses

For the purpose of estimation, the cost of labour is estimated to increase by 5 to 10 percent

each year for 2020, 2021, and 2022.

The depreciation is estimated to remain fixed for all the years as depreciation is based on

straight-line method.

Interest rate for borrowings is assumed to be 5% per annum.

Tax rate 30%, it has been assumed to be constant for all the years.

Valuation

market capitalization 13. 229

- 2%

Add: preferred shares -

1.1651

0.4018

13.9923

Price 18.38

earnings 0.58

31.68966

EV/EBITDA ratio

P/E model

Valuation method

EV (entreprise value)

Add: minority

Add: Debt

Subtract: total cash

Total EV

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TREASURY WINE ESTATES LTD: 9

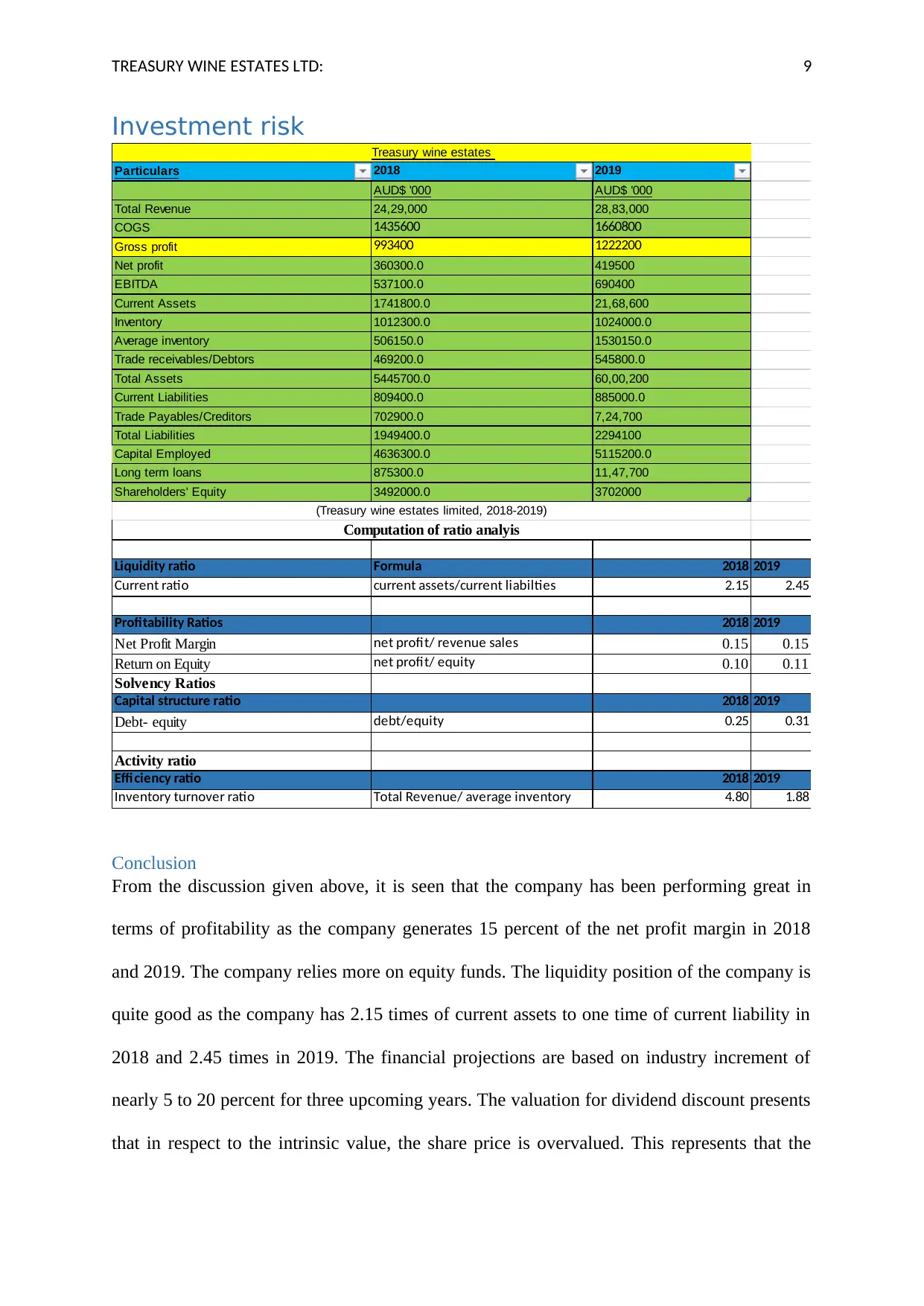

Investment risk

Particulars 2018 2019

AUD$ '000 AUD$ '000

Total Revenue 24,29,000 28,83,000

COGS 1435600 1660800

Gross profit 993400 1222200

Net profit 360300.0 419500

EBITDA 537100.0 690400

Current Assets 1741800.0 21,68,600

Inventory 1012300.0 1024000.0

Average inventory 506150.0 1530150.0

Trade receivables/Debtors 469200.0 545800.0

Total Assets 5445700.0 60,00,200

Current Liabilities 809400.0 885000.0

Trade Payables/Creditors 702900.0 7,24,700

Total Liabilities 1949400.0 2294100

Capital Employed 4636300.0 5115200.0

Long term loans 875300.0 11,47,700

Shareholders' Equity 3492000.0 3702000

Liquidity ratio Formula 2018 2019

Current ratio current assets/current liabilties 2.15 2.45

Profitability Ratios 2018 2019

Net Profit Margin net profit/ revenue sales 0.15 0.15

Return on Equity net profit/ equity 0.10 0.11

Solvency Ratios

Capital structure ratio 2018 2019

Debt- equity debt/equity 0.25 0.31

Activity ratio

Efficiency ratio 2018 2019

Inventory turnover ratio Total Revenue/ average inventory 4.80 1.88

Treasury wine estates

Computation of ratio analyis

(Treasury wine estates limited, 2018-2019)

Conclusion

From the discussion given above, it is seen that the company has been performing great in

terms of profitability as the company generates 15 percent of the net profit margin in 2018

and 2019. The company relies more on equity funds. The liquidity position of the company is

quite good as the company has 2.15 times of current assets to one time of current liability in

2018 and 2.45 times in 2019. The financial projections are based on industry increment of

nearly 5 to 20 percent for three upcoming years. The valuation for dividend discount presents

that in respect to the intrinsic value, the share price is overvalued. This represents that the

Investment risk

Particulars 2018 2019

AUD$ '000 AUD$ '000

Total Revenue 24,29,000 28,83,000

COGS 1435600 1660800

Gross profit 993400 1222200

Net profit 360300.0 419500

EBITDA 537100.0 690400

Current Assets 1741800.0 21,68,600

Inventory 1012300.0 1024000.0

Average inventory 506150.0 1530150.0

Trade receivables/Debtors 469200.0 545800.0

Total Assets 5445700.0 60,00,200

Current Liabilities 809400.0 885000.0

Trade Payables/Creditors 702900.0 7,24,700

Total Liabilities 1949400.0 2294100

Capital Employed 4636300.0 5115200.0

Long term loans 875300.0 11,47,700

Shareholders' Equity 3492000.0 3702000

Liquidity ratio Formula 2018 2019

Current ratio current assets/current liabilties 2.15 2.45

Profitability Ratios 2018 2019

Net Profit Margin net profit/ revenue sales 0.15 0.15

Return on Equity net profit/ equity 0.10 0.11

Solvency Ratios

Capital structure ratio 2018 2019

Debt- equity debt/equity 0.25 0.31

Activity ratio

Efficiency ratio 2018 2019

Inventory turnover ratio Total Revenue/ average inventory 4.80 1.88

Treasury wine estates

Computation of ratio analyis

(Treasury wine estates limited, 2018-2019)

Conclusion

From the discussion given above, it is seen that the company has been performing great in

terms of profitability as the company generates 15 percent of the net profit margin in 2018

and 2019. The company relies more on equity funds. The liquidity position of the company is

quite good as the company has 2.15 times of current assets to one time of current liability in

2018 and 2.45 times in 2019. The financial projections are based on industry increment of

nearly 5 to 20 percent for three upcoming years. The valuation for dividend discount presents

that in respect to the intrinsic value, the share price is overvalued. This represents that the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TREASURY WINE ESTATES LTD: 10

company enjoys goodwill but investors can have two perspective. First can be the share price

will keep increasing whereas, on the other hand, an investor may wait to decrease the market

price so that they can purchase it at the appropriate price.

company enjoys goodwill but investors can have two perspective. First can be the share price

will keep increasing whereas, on the other hand, an investor may wait to decrease the market

price so that they can purchase it at the appropriate price.

TREASURY WINE ESTATES LTD: 11

References

Chua, A., DeLisle, R. J., Feng, S. S., & Lee, B. S. (2015). Price‐to‐Earnings Ratios and

Option Prices. Journal of Futures Markets, 35(8), 738-752.

Creditriskmonitor, (2019). Treasury Wine Estates Ltd. Retrieved from:

https://info.creditriskmonitor.com/Report/ReportPreview.aspx?BusinessId=17985390

Edwards, A., Schwab, C., & Shevlin, T. (2015). Financial constraints and cash tax

savings. The Accounting Review, 91(3), 859-881.

Guru focus, (2019b). Economic indicators (Long-Term Government Bond Yields: 10-year:

Main (Including Benchmark) for Australia). Retrieved from:

https://www.gurufocus.com/economic_indicators/118/10year-treasury-constant-

maturity-rate

Gurufocus, (2019a). WACC. Retrieved from:

https://www.gurufocus.com/term/wacc/TSRYY/WACC-/Treasury-Wine-Estates-Ltd

Houmes, R., & Chira, I. (2015). The effect of ownership structure on the price earnings ratio

—returns anomaly. International Review of Financial Analysis, 37, 140-147.

macquarie.com, (2015). Retail newsletter 2015. Retrieved from:

https://www.macquarie.com.au/dafiles/Internet/mgl/au/apps/retail-newsletter/docs/

2015-04/TWE150415e.pdf

Market watch, (2019). Treasury Wine Estates Ltd. Retrieved from:

https://www.marketwatch.com/investing/stock/twe?countrycode=au

Mugoša, A., & Popović, S. (2015). Towards and Effective Financial Management: Relevance

of Dividend Discount Model in Stock Price Valuation. Economic analysis, 48(1-2),

39-53.

References

Chua, A., DeLisle, R. J., Feng, S. S., & Lee, B. S. (2015). Price‐to‐Earnings Ratios and

Option Prices. Journal of Futures Markets, 35(8), 738-752.

Creditriskmonitor, (2019). Treasury Wine Estates Ltd. Retrieved from:

https://info.creditriskmonitor.com/Report/ReportPreview.aspx?BusinessId=17985390

Edwards, A., Schwab, C., & Shevlin, T. (2015). Financial constraints and cash tax

savings. The Accounting Review, 91(3), 859-881.

Guru focus, (2019b). Economic indicators (Long-Term Government Bond Yields: 10-year:

Main (Including Benchmark) for Australia). Retrieved from:

https://www.gurufocus.com/economic_indicators/118/10year-treasury-constant-

maturity-rate

Gurufocus, (2019a). WACC. Retrieved from:

https://www.gurufocus.com/term/wacc/TSRYY/WACC-/Treasury-Wine-Estates-Ltd

Houmes, R., & Chira, I. (2015). The effect of ownership structure on the price earnings ratio

—returns anomaly. International Review of Financial Analysis, 37, 140-147.

macquarie.com, (2015). Retail newsletter 2015. Retrieved from:

https://www.macquarie.com.au/dafiles/Internet/mgl/au/apps/retail-newsletter/docs/

2015-04/TWE150415e.pdf

Market watch, (2019). Treasury Wine Estates Ltd. Retrieved from:

https://www.marketwatch.com/investing/stock/twe?countrycode=au

Mugoša, A., & Popović, S. (2015). Towards and Effective Financial Management: Relevance

of Dividend Discount Model in Stock Price Valuation. Economic analysis, 48(1-2),

39-53.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.