Business Finance Report: Trend Ltd. Cash Flow and Working Capital

VerifiedAdded on 2022/12/26

|12

|3096

|42

Report

AI Summary

This report provides a detailed analysis of the business finance practices of Trend Ltd., a company manufacturing gym clothing and footwear. The report explores key concepts such as profit, cash flow, working capital, receivables, inventories, and payables, and assesses their impact on the company's financial results. It explains the difference between profit and cash flow, and how working capital management influences cash flow. The report highlights the impact of the company's operational management on its financial results, particularly focusing on the actions of the owner, Arpha, and the management of working capital. It concludes with recommendations to improve the company's cash flow through better working capital management, including strategies for debt recovery, dispute resolution, and inventory control. Additionally, the report includes an executive summary and a section on the business finance practices of Thorne Estates Limited, with a focus on cash budgeting and recommendations for improved cash management, especially considering the challenges faced by the company.

Business finance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Executive Summary ........................................................................................................................3

Task 1...............................................................................................................................................3

1. Explain....................................................................................................................................3

2. Impact of company's operational management on financial results.......................................5

3. Steps recommended to improve company's cash flow through better working capital

management................................................................................................................................5

Executive Summary.........................................................................................................................7

Task 2...............................................................................................................................................7

1. Monthly cash budgets from 1st Jan to 30th April 2021..........................................................7

2. Recommendations to the management of Thorne Estates Limited.........................................7

References......................................................................................................................................10

Appendix........................................................................................................................................11

Monthly cash budgets...............................................................................................................11

2

Executive Summary ........................................................................................................................3

Task 1...............................................................................................................................................3

1. Explain....................................................................................................................................3

2. Impact of company's operational management on financial results.......................................5

3. Steps recommended to improve company's cash flow through better working capital

management................................................................................................................................5

Executive Summary.........................................................................................................................7

Task 2...............................................................................................................................................7

1. Monthly cash budgets from 1st Jan to 30th April 2021..........................................................7

2. Recommendations to the management of Thorne Estates Limited.........................................7

References......................................................................................................................................10

Appendix........................................................................................................................................11

Monthly cash budgets...............................................................................................................11

2

Executive Summary

Business finance involves taking up financial management of the business concerns. It

includes both revenue and capital management in order to ensure smooth financial health of the

business (Burns and Dewhurst, 2016). This report aims to cover business finance practices of

Trend Ltd (TL) which manufactures gym clothing and footwear. For Trend Ltd, concepts such as

profit, cash flow, working capital, receivables, inventories and payables are discussed and their

impact over the financial results of the company are determined. Steps to improve company's

cash flow through better working capital management are also discussed.

Task 1

1. Explain

A. Profit and cash flow

Profit - Profit is any revenue in excess of cost. In accounting, profit refers to the financial

benefit that is derived when total revenue of the business exceeds over the total expenses of the

company. It is either retained by a company to provide for future operations or is distributed to

shareholders as dividend. It is obtained in profit and loss account which is also known as Income

Statement. A company divides its profit and loss account into various stages - first is

manufacturing profit which is known as gross profit. Further, other administrative and selling

expenses are reduced from the gross profit to arrive at operating profit. Furthermore, all non-

operating expenses and income are adjusted to arrive at the final figure of net profit, also known

as net income. This profit is then adjusted with corporate tax to arrive at the figure of profit after

tax. This amount is said to be profit available for shareholders.

Cash flow - Cash flow refers to the total flow of cash in a business concern over a

specific period. Cash receipts are taken as inflow while cash payments are taken as outflow.

When inflow of cash exceeds outflow in a business, it is known as favourable position for the

business and company is able to generate more value for the stakeholders. Cash flow

management is extremely important for companies to ensure smooth business operations.

Therefore, companies prepare cash budgets to act as standards for operations. These budgets are

monitored and reviewed periodically like monthly, quarterly, semi-annually or annually, to make

necessary adjustments. Further cash flow statement is prepared as a part of financial statements

of a company to assess overall cash inflow-outflow position during the year or reported period.

3

Business finance involves taking up financial management of the business concerns. It

includes both revenue and capital management in order to ensure smooth financial health of the

business (Burns and Dewhurst, 2016). This report aims to cover business finance practices of

Trend Ltd (TL) which manufactures gym clothing and footwear. For Trend Ltd, concepts such as

profit, cash flow, working capital, receivables, inventories and payables are discussed and their

impact over the financial results of the company are determined. Steps to improve company's

cash flow through better working capital management are also discussed.

Task 1

1. Explain

A. Profit and cash flow

Profit - Profit is any revenue in excess of cost. In accounting, profit refers to the financial

benefit that is derived when total revenue of the business exceeds over the total expenses of the

company. It is either retained by a company to provide for future operations or is distributed to

shareholders as dividend. It is obtained in profit and loss account which is also known as Income

Statement. A company divides its profit and loss account into various stages - first is

manufacturing profit which is known as gross profit. Further, other administrative and selling

expenses are reduced from the gross profit to arrive at operating profit. Furthermore, all non-

operating expenses and income are adjusted to arrive at the final figure of net profit, also known

as net income. This profit is then adjusted with corporate tax to arrive at the figure of profit after

tax. This amount is said to be profit available for shareholders.

Cash flow - Cash flow refers to the total flow of cash in a business concern over a

specific period. Cash receipts are taken as inflow while cash payments are taken as outflow.

When inflow of cash exceeds outflow in a business, it is known as favourable position for the

business and company is able to generate more value for the stakeholders. Cash flow

management is extremely important for companies to ensure smooth business operations.

Therefore, companies prepare cash budgets to act as standards for operations. These budgets are

monitored and reviewed periodically like monthly, quarterly, semi-annually or annually, to make

necessary adjustments. Further cash flow statement is prepared as a part of financial statements

of a company to assess overall cash inflow-outflow position during the year or reported period.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash flow statement is divided into three parts - cash flow from operating activities, cash flow

from investing activities and cash flow from financing activities. Operating activities includes

activities related to sales, purchase, payroll, etc. Investing activities takes into consideration

inflow and outflow related to investments of the company, loans forwarded, interest received,

fixed assets sale - purchase, etc. Financing activities takes into account change in capital

structure, loans availed, interest paid, dividend paid, etc.

Difference between two - Most primary difference between profit and cash flow is that

the profit is only an accounting entity which is used to report net income generated in business

while cash flows represents inflow and outflow of real cash. In other words, profit represents

profitability of the business while cash flow represents liquidity of the business. Another

difference is that profit of a company is generated using accrual accounting system while cash

flow of the business is determined using cash accounting system.

B. Working Capital, receivables, inventories and payables

Working Capital - Working capital includes two components - current assets such as

cash, receivables, etc. and current liabilities like payables, short-term loans, etc. and is

represented as the net difference of the two. When current assets exceeds current liabilities, it is

taken as positive working capital of the business (Cheng, Li and Tong, 2016).

Receivables - Account receivables represents those people who owe money to business

such as trade debtors. These are currents assets of the company and reflects such amount that

will generate revenue for company in near future. Company maintains a separate system for

negotiating with trade debtors to manage debtors payment cycle.

Inventories - Inventories refers to all the merchandise that a company manufactures and

trades in. It is held by company between manufacturing or ordering till order fulfilment for

delivery. It can be either in form of raw materials, intermediate products or finished goods.

Payables - Account payables represents those people who business owe money to, such

as trade creditors. These are currents liabilities of the company and reflects such amount that will

have to be paid by company in near future. Company maintains a separate system for negotiating

with trade creditors to manage creditors' payment cycle.

C. Impact of change in working capital on cash flow

4

from investing activities and cash flow from financing activities. Operating activities includes

activities related to sales, purchase, payroll, etc. Investing activities takes into consideration

inflow and outflow related to investments of the company, loans forwarded, interest received,

fixed assets sale - purchase, etc. Financing activities takes into account change in capital

structure, loans availed, interest paid, dividend paid, etc.

Difference between two - Most primary difference between profit and cash flow is that

the profit is only an accounting entity which is used to report net income generated in business

while cash flows represents inflow and outflow of real cash. In other words, profit represents

profitability of the business while cash flow represents liquidity of the business. Another

difference is that profit of a company is generated using accrual accounting system while cash

flow of the business is determined using cash accounting system.

B. Working Capital, receivables, inventories and payables

Working Capital - Working capital includes two components - current assets such as

cash, receivables, etc. and current liabilities like payables, short-term loans, etc. and is

represented as the net difference of the two. When current assets exceeds current liabilities, it is

taken as positive working capital of the business (Cheng, Li and Tong, 2016).

Receivables - Account receivables represents those people who owe money to business

such as trade debtors. These are currents assets of the company and reflects such amount that

will generate revenue for company in near future. Company maintains a separate system for

negotiating with trade debtors to manage debtors payment cycle.

Inventories - Inventories refers to all the merchandise that a company manufactures and

trades in. It is held by company between manufacturing or ordering till order fulfilment for

delivery. It can be either in form of raw materials, intermediate products or finished goods.

Payables - Account payables represents those people who business owe money to, such

as trade creditors. These are currents liabilities of the company and reflects such amount that will

have to be paid by company in near future. Company maintains a separate system for negotiating

with trade creditors to manage creditors' payment cycle.

C. Impact of change in working capital on cash flow

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managing working capital and cash flow are both fundamental to the organisation and

interact with each other during financial performance analysis of the company. Working capital

represents difference between a company's current assets and current liabilities or in other words,

it determines the short-term money a company is required to pay to its short-term liabilities.

Current assets includes cash and cash equivalents which are point of discussion in the cash flow

management. Positive working capital means business have sufficient funds to cover its current

liabilities and be a reflection of its strong financial position and good cash flow position. On the

other hand, negative working capital could have meant that business does not have sufficient

funds to cover its current liabilities. It could also mean that company has either made a huge cash

outlay in near time that it is now short of funds or large funds are required in near future which is

not available in business. Such situation extended for a long time is not positive situation for the

company and might be able to create liquidity challenges for the businesses in future (Tenca,

Croce and Ughetto, 2018).

2. Impact of company's operational management on financial results

In the given company Trend Ltd., operating profit of £60 million was reported last year.

This is a respectable figure and shows the profit making capabilities of the business. However, as

per the information provided, profitability was compromised with the attitude of owner Arpha as

well as because of the way the working capital was being managed. £10 million was owed to

company by debtor Tkechers, £12.5 million amount is outstanding from another debtor which

has run into dispute and company is stock piling materials to avoid work halt in the meantime a

dispute is resolved with major supplier. Also, to avoid further disputes, Arpha is not ready to

pressurise other clients for payments. All these are capable of having huge negative influence on

working capital and profitability of the business. It has also been provided that company's debt

has increased from £60 million in the last year to £95 million in the present year. This means that

company had £35 million more funds in the company while £20 million has been outflow

because of the investment it made in a company. This has not only impacted financing decisions

of the company but also investing decisions of the cash flow.

3. Steps recommended to improve company's cash flow through better working capital

management

On the basis of above-mentioned analysis, following recommendations is suggested to

the company for improving their working capital management:

5

interact with each other during financial performance analysis of the company. Working capital

represents difference between a company's current assets and current liabilities or in other words,

it determines the short-term money a company is required to pay to its short-term liabilities.

Current assets includes cash and cash equivalents which are point of discussion in the cash flow

management. Positive working capital means business have sufficient funds to cover its current

liabilities and be a reflection of its strong financial position and good cash flow position. On the

other hand, negative working capital could have meant that business does not have sufficient

funds to cover its current liabilities. It could also mean that company has either made a huge cash

outlay in near time that it is now short of funds or large funds are required in near future which is

not available in business. Such situation extended for a long time is not positive situation for the

company and might be able to create liquidity challenges for the businesses in future (Tenca,

Croce and Ughetto, 2018).

2. Impact of company's operational management on financial results

In the given company Trend Ltd., operating profit of £60 million was reported last year.

This is a respectable figure and shows the profit making capabilities of the business. However, as

per the information provided, profitability was compromised with the attitude of owner Arpha as

well as because of the way the working capital was being managed. £10 million was owed to

company by debtor Tkechers, £12.5 million amount is outstanding from another debtor which

has run into dispute and company is stock piling materials to avoid work halt in the meantime a

dispute is resolved with major supplier. Also, to avoid further disputes, Arpha is not ready to

pressurise other clients for payments. All these are capable of having huge negative influence on

working capital and profitability of the business. It has also been provided that company's debt

has increased from £60 million in the last year to £95 million in the present year. This means that

company had £35 million more funds in the company while £20 million has been outflow

because of the investment it made in a company. This has not only impacted financing decisions

of the company but also investing decisions of the cash flow.

3. Steps recommended to improve company's cash flow through better working capital

management

On the basis of above-mentioned analysis, following recommendations is suggested to

the company for improving their working capital management:

5

Company must try to recover the money as soon as possible from all its debtors to avoid

further interest loss and the risk of running in under-liquidation. Further, such debtors

who have history or track record of non-payment or late payment must be dealt in a

different manner or not dealt with altogether.

Company has £12.5 million in dispute with Sadidas which has withheld its payment.

Manager Arpha believes this dispute arose due to sub-standard supply of materials by a

supplier and as a result, has withheld its payment. Now, the supplier is threatening legal

action. Company is running into disputes which is not only harmful for cash flow and

working capital of the company but also, for its operations and growth opportunities.

Therefore, it shall try to settle disputes as soon as possible (Akan and Tevfik, 2020).

Furthermore, Arpha has built a level of stock in one of its warehouse which is more than

required to avoid disruptions during dispute resolution period. Company shall avoid over-

stocking as it would cause unnecessary cost of holding inventories. Rather, it should

make provisions for emergency supply of raw materials by some other supplier.

6

further interest loss and the risk of running in under-liquidation. Further, such debtors

who have history or track record of non-payment or late payment must be dealt in a

different manner or not dealt with altogether.

Company has £12.5 million in dispute with Sadidas which has withheld its payment.

Manager Arpha believes this dispute arose due to sub-standard supply of materials by a

supplier and as a result, has withheld its payment. Now, the supplier is threatening legal

action. Company is running into disputes which is not only harmful for cash flow and

working capital of the company but also, for its operations and growth opportunities.

Therefore, it shall try to settle disputes as soon as possible (Akan and Tevfik, 2020).

Furthermore, Arpha has built a level of stock in one of its warehouse which is more than

required to avoid disruptions during dispute resolution period. Company shall avoid over-

stocking as it would cause unnecessary cost of holding inventories. Rather, it should

make provisions for emergency supply of raw materials by some other supplier.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Executive Summary

Primary goal of business finance is to maximise wealth of the shareholders for which it

needs to undertake necessary decisions related to the working capital management, cash

management, etc. This report aims to cover business finance practices of Thorne Estates Limited

which advertises and sell residential property on behalf of its customers. For Thorne Estates

Limited, an illustrative cash budget is prepared for four months and then further

recommendations are made to management of company to improve cash management on the

basis of observations made during preparation of cash budget.

Task 2

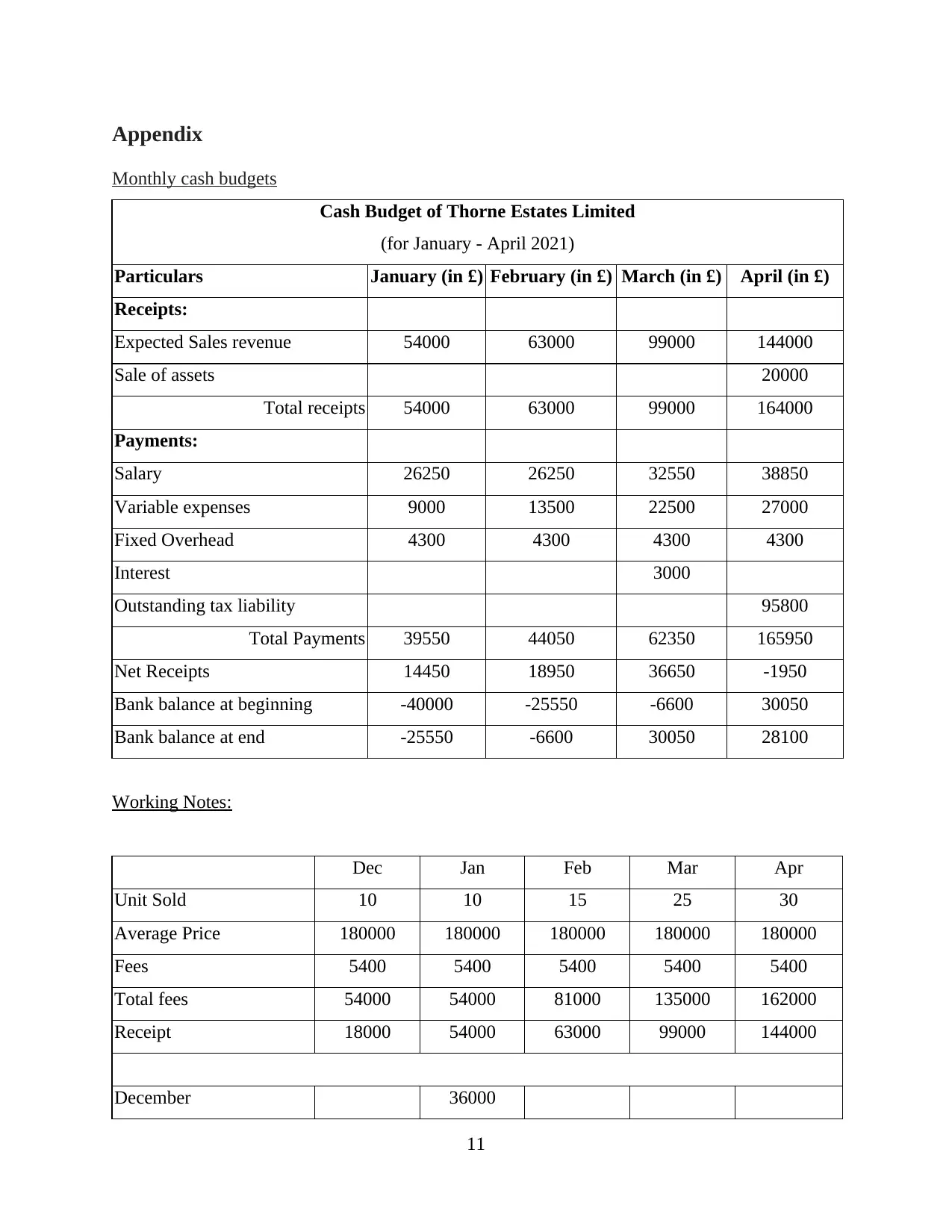

1. Monthly cash budgets from 1st Jan to 30th April 2021

Cash budget is an estimation prepared to assess cash receipts and disbursements in a

defined future period. In other words, it is an estimated projection of position of cash and cash

equivalents in the company in a future period. It includes forecasting changes in inflows and

outflows of cash due to revenue received, expenses incurred and loan payments and receipts

(Bouma, Jeucken and Klinkers, 2017).

It has been provided that Thorne Estate Limited is in the business of advertising and

selling residential property on the behalf of its customers. Average price of the property sold by

the company is £180,000 on which company charges a fee of 3% on sales. One-third fee is

received in the same month of sale and two-third is received next month. Further, it has been

stated that company has nine employees who gets paid monthly and are also, given bonus of

£140 for each additional property sold over 20 properties. Furthermore, company incurs variable

and fixed costs as per its operational process. Additionally, it has been provided that company

intends to dispose surplus vehicles and expects to earn £20,000 out of them for a net book value

of £15000. Cash Balance at the beginning of January 2021 is expected to be a deficit of £20,000.

2. Recommendations to the management of Thorne Estates Limited

Challenges

In the information provide noteworthy points are that company has been in business for a

short time only and therefore, does not have much of the trends related to its past performance

that can help it and act as reference point for forecasting future cash cycles' development. It has

also been provided that company has an outstanding tax liability amount and that it intends to

7

Primary goal of business finance is to maximise wealth of the shareholders for which it

needs to undertake necessary decisions related to the working capital management, cash

management, etc. This report aims to cover business finance practices of Thorne Estates Limited

which advertises and sell residential property on behalf of its customers. For Thorne Estates

Limited, an illustrative cash budget is prepared for four months and then further

recommendations are made to management of company to improve cash management on the

basis of observations made during preparation of cash budget.

Task 2

1. Monthly cash budgets from 1st Jan to 30th April 2021

Cash budget is an estimation prepared to assess cash receipts and disbursements in a

defined future period. In other words, it is an estimated projection of position of cash and cash

equivalents in the company in a future period. It includes forecasting changes in inflows and

outflows of cash due to revenue received, expenses incurred and loan payments and receipts

(Bouma, Jeucken and Klinkers, 2017).

It has been provided that Thorne Estate Limited is in the business of advertising and

selling residential property on the behalf of its customers. Average price of the property sold by

the company is £180,000 on which company charges a fee of 3% on sales. One-third fee is

received in the same month of sale and two-third is received next month. Further, it has been

stated that company has nine employees who gets paid monthly and are also, given bonus of

£140 for each additional property sold over 20 properties. Furthermore, company incurs variable

and fixed costs as per its operational process. Additionally, it has been provided that company

intends to dispose surplus vehicles and expects to earn £20,000 out of them for a net book value

of £15000. Cash Balance at the beginning of January 2021 is expected to be a deficit of £20,000.

2. Recommendations to the management of Thorne Estates Limited

Challenges

In the information provide noteworthy points are that company has been in business for a

short time only and therefore, does not have much of the trends related to its past performance

that can help it and act as reference point for forecasting future cash cycles' development. It has

also been provided that company has an outstanding tax liability amount and that it intends to

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

dispose surplus vehicles for an expected gain of £5000. Company is expecting to have a deficit

cash balance at the starting of budgeted period. All these points paint company in a different

picture. Challenges with company:

No large historical trends - From above-mentioned points, it can be deduced that

company does not have large past to draw upon references as well as company cannot be

sure of the estimates it has taken, to prepare the budget as the future is unpredictable and

company is preparing budgets on its present operational standards without giving any due

provision or reserve. Therefore, in case any contingency arise in the future, cash budget

prepared by the company will be render ineffective (Katz and Green, 2018).

Deficit cash flow- It has been provided that company is expected to have a deficit cash

balance in the opening of January, 2021. It has prepared budget for 4 months and is

expecting to have positive cash flows by the end of 4 months budgeted period. In

addition, if in the budgeted period company gets erratic cash flows, every planning will

be render ineffective. Under-liquidation and over-liquidation both are issues for financial

planning of a business for under-liquidation can lead to halt in operations while over-

liquidation can be result of wasted growth opportunity.

Recommendations

In light of the above conditions, below mentioned recommendations are suggested to

company so that it can be sure of having smooth cash flow management:

In order to ensure that deficit cash balance problem does not arise again, company needs

to reconsider negotiating with its business associates like suppliers, lenders, vendors, and

other creditors, etc. It should be made clear with business associates that company needs

to revise its contracts to suit its cash flow position and a win-win situation would be

created for both the sides. A good business partner is always supported by associates and

therefore, they should provide company with better terms. Other than negotiating deals

with business associates, company must try to increase its sales and reduce costs. It

should try to change its marketing practises to get more customers and then sale them. It

can offer discounts and other incentives to attract customers.

Success of cash budget of the company is based on achievement of revenue targets

otherwise, whole budget target will be missed and cash planning of the company would

be disrupted. In order to avoid such issues, company shall make a flexible budget and

8

cash balance at the starting of budgeted period. All these points paint company in a different

picture. Challenges with company:

No large historical trends - From above-mentioned points, it can be deduced that

company does not have large past to draw upon references as well as company cannot be

sure of the estimates it has taken, to prepare the budget as the future is unpredictable and

company is preparing budgets on its present operational standards without giving any due

provision or reserve. Therefore, in case any contingency arise in the future, cash budget

prepared by the company will be render ineffective (Katz and Green, 2018).

Deficit cash flow- It has been provided that company is expected to have a deficit cash

balance in the opening of January, 2021. It has prepared budget for 4 months and is

expecting to have positive cash flows by the end of 4 months budgeted period. In

addition, if in the budgeted period company gets erratic cash flows, every planning will

be render ineffective. Under-liquidation and over-liquidation both are issues for financial

planning of a business for under-liquidation can lead to halt in operations while over-

liquidation can be result of wasted growth opportunity.

Recommendations

In light of the above conditions, below mentioned recommendations are suggested to

company so that it can be sure of having smooth cash flow management:

In order to ensure that deficit cash balance problem does not arise again, company needs

to reconsider negotiating with its business associates like suppliers, lenders, vendors, and

other creditors, etc. It should be made clear with business associates that company needs

to revise its contracts to suit its cash flow position and a win-win situation would be

created for both the sides. A good business partner is always supported by associates and

therefore, they should provide company with better terms. Other than negotiating deals

with business associates, company must try to increase its sales and reduce costs. It

should try to change its marketing practises to get more customers and then sale them. It

can offer discounts and other incentives to attract customers.

Success of cash budget of the company is based on achievement of revenue targets

otherwise, whole budget target will be missed and cash planning of the company would

be disrupted. In order to avoid such issues, company shall make a flexible budget and

8

monthly review them to identify any variations before it can turn disruptive. Variance

analysis helps prepare corrective actions that keeps cash management of the business on

track. Further, company can also create a budget which have multiple scenarios of

different revenues and expenses to understand the method to be adopted to if such

situation arises. However, budget preparation can be expensive and company need not

make it at the cost of its cash flow management.

Budget prepared by the company is very compact and has neither considered

contingencies nor included room for other expenses that can put cash management to

trouble. Therefore, company shall make more elaborate budget and also, provide for

additional funds as reserve and provisions. Budget shall be carefully divided into right

heads so that correct expenses and their pattern can be identified. This will help company

optimise their revenue and expenses structure (Cowling, Liu and Zhang, 2016).

9

analysis helps prepare corrective actions that keeps cash management of the business on

track. Further, company can also create a budget which have multiple scenarios of

different revenues and expenses to understand the method to be adopted to if such

situation arises. However, budget preparation can be expensive and company need not

make it at the cost of its cash flow management.

Budget prepared by the company is very compact and has neither considered

contingencies nor included room for other expenses that can put cash management to

trouble. Therefore, company shall make more elaborate budget and also, provide for

additional funds as reserve and provisions. Budget shall be carefully divided into right

heads so that correct expenses and their pattern can be identified. This will help company

optimise their revenue and expenses structure (Cowling, Liu and Zhang, 2016).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Books and Journal

Akan, M. and Tevfik, A. T., 2020. Fundamentals of finance. In Fundamentals of Finance. De

Gruyter.

Bouma, J. J., Jeucken, M. and Klinkers, L. eds., 2017. Sustainable banking: The greening of

finance. Routledge.

Burns, P. and Dewhurst, J. eds., 2016. Small business and entrepreneurship. Macmillan

International Higher Education.

Cheng, P., Li, L. and Tong, W. H., 2016. Target information asymmetry and acquisition

price. Journal of Business Finance & Accounting, 43(7-8), pp.976-1016.

Cowling, M., Liu, W. and Zhang, N., 2016. Access to bank finance for UK SMEs in the wake of

the recent financial crisis. International Journal of Entrepreneurial Behavior &

Research.

Katz, J. A. and Green, R. P., 2018. Entrepreneurial small business. McGraw-Hill Education,.

Tenca, F., Croce, A. and Ughetto, E., 2018. Business angels research in entrepreneurial finance:

A literature review and a research agenda. Journal of Economic Surveys, 32(5),

pp.1384-1413.

10

Books and Journal

Akan, M. and Tevfik, A. T., 2020. Fundamentals of finance. In Fundamentals of Finance. De

Gruyter.

Bouma, J. J., Jeucken, M. and Klinkers, L. eds., 2017. Sustainable banking: The greening of

finance. Routledge.

Burns, P. and Dewhurst, J. eds., 2016. Small business and entrepreneurship. Macmillan

International Higher Education.

Cheng, P., Li, L. and Tong, W. H., 2016. Target information asymmetry and acquisition

price. Journal of Business Finance & Accounting, 43(7-8), pp.976-1016.

Cowling, M., Liu, W. and Zhang, N., 2016. Access to bank finance for UK SMEs in the wake of

the recent financial crisis. International Journal of Entrepreneurial Behavior &

Research.

Katz, J. A. and Green, R. P., 2018. Entrepreneurial small business. McGraw-Hill Education,.

Tenca, F., Croce, A. and Ughetto, E., 2018. Business angels research in entrepreneurial finance:

A literature review and a research agenda. Journal of Economic Surveys, 32(5),

pp.1384-1413.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appendix

Monthly cash budgets

Cash Budget of Thorne Estates Limited

(for January - April 2021)

Particulars January (in £) February (in £) March (in £) April (in £)

Receipts:

Expected Sales revenue 54000 63000 99000 144000

Sale of assets 20000

Total receipts 54000 63000 99000 164000

Payments:

Salary 26250 26250 32550 38850

Variable expenses 9000 13500 22500 27000

Fixed Overhead 4300 4300 4300 4300

Interest 3000

Outstanding tax liability 95800

Total Payments 39550 44050 62350 165950

Net Receipts 14450 18950 36650 -1950

Bank balance at beginning -40000 -25550 -6600 30050

Bank balance at end -25550 -6600 30050 28100

Working Notes:

Dec Jan Feb Mar Apr

Unit Sold 10 10 15 25 30

Average Price 180000 180000 180000 180000 180000

Fees 5400 5400 5400 5400 5400

Total fees 54000 54000 81000 135000 162000

Receipt 18000 54000 63000 99000 144000

December 36000

11

Monthly cash budgets

Cash Budget of Thorne Estates Limited

(for January - April 2021)

Particulars January (in £) February (in £) March (in £) April (in £)

Receipts:

Expected Sales revenue 54000 63000 99000 144000

Sale of assets 20000

Total receipts 54000 63000 99000 164000

Payments:

Salary 26250 26250 32550 38850

Variable expenses 9000 13500 22500 27000

Fixed Overhead 4300 4300 4300 4300

Interest 3000

Outstanding tax liability 95800

Total Payments 39550 44050 62350 165950

Net Receipts 14450 18950 36650 -1950

Bank balance at beginning -40000 -25550 -6600 30050

Bank balance at end -25550 -6600 30050 28100

Working Notes:

Dec Jan Feb Mar Apr

Unit Sold 10 10 15 25 30

Average Price 180000 180000 180000 180000 180000

Fees 5400 5400 5400 5400 5400

Total fees 54000 54000 81000 135000 162000

Receipt 18000 54000 63000 99000 144000

December 36000

11

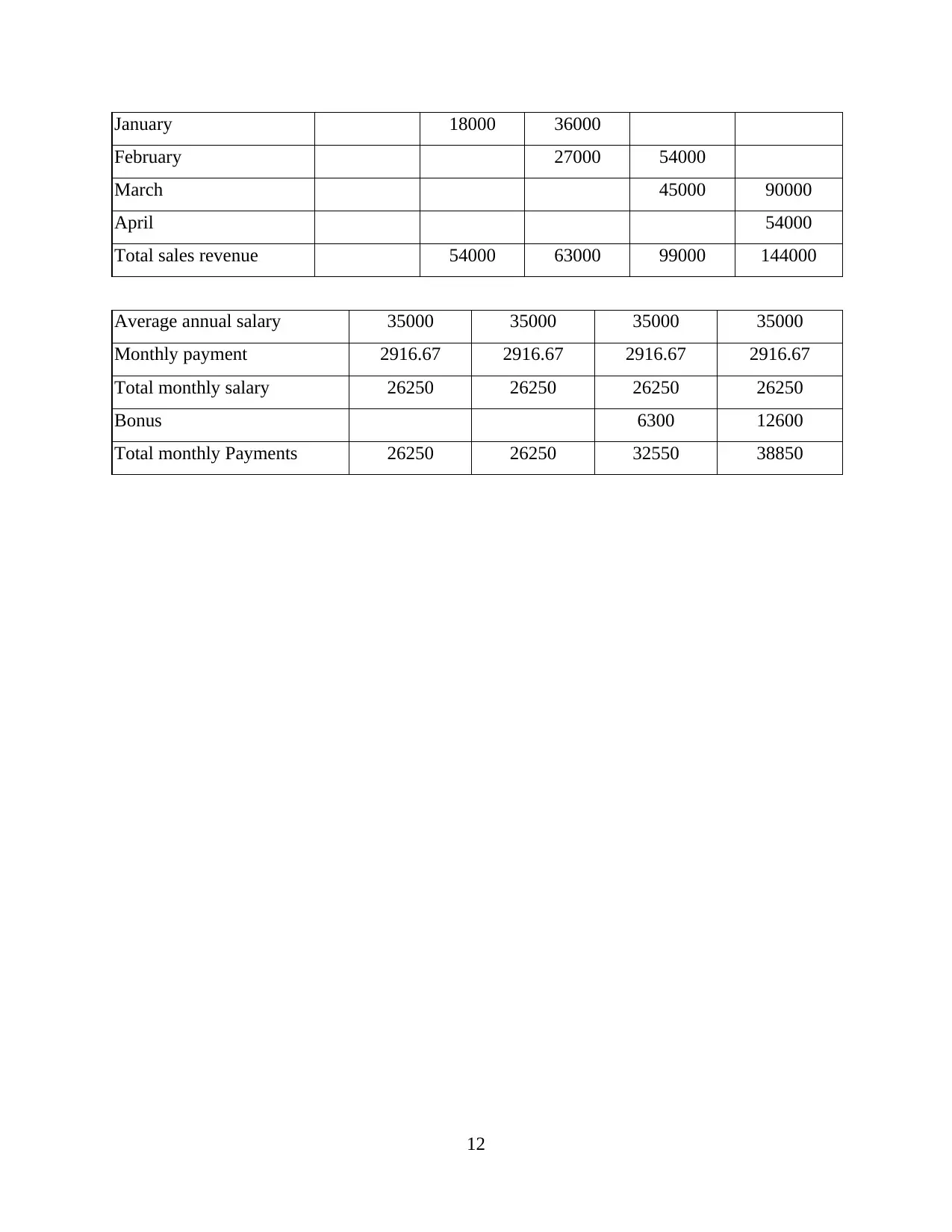

January 18000 36000

February 27000 54000

March 45000 90000

April 54000

Total sales revenue 54000 63000 99000 144000

Average annual salary 35000 35000 35000 35000

Monthly payment 2916.67 2916.67 2916.67 2916.67

Total monthly salary 26250 26250 26250 26250

Bonus 6300 12600

Total monthly Payments 26250 26250 32550 38850

12

February 27000 54000

March 45000 90000

April 54000

Total sales revenue 54000 63000 99000 144000

Average annual salary 35000 35000 35000 35000

Monthly payment 2916.67 2916.67 2916.67 2916.67

Total monthly salary 26250 26250 26250 26250

Bonus 6300 12600

Total monthly Payments 26250 26250 32550 38850

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.