Accounting Assignment: Trial Balance to Financial Statements

VerifiedAdded on 2023/03/23

|15

|1937

|75

Practical Assignment

AI Summary

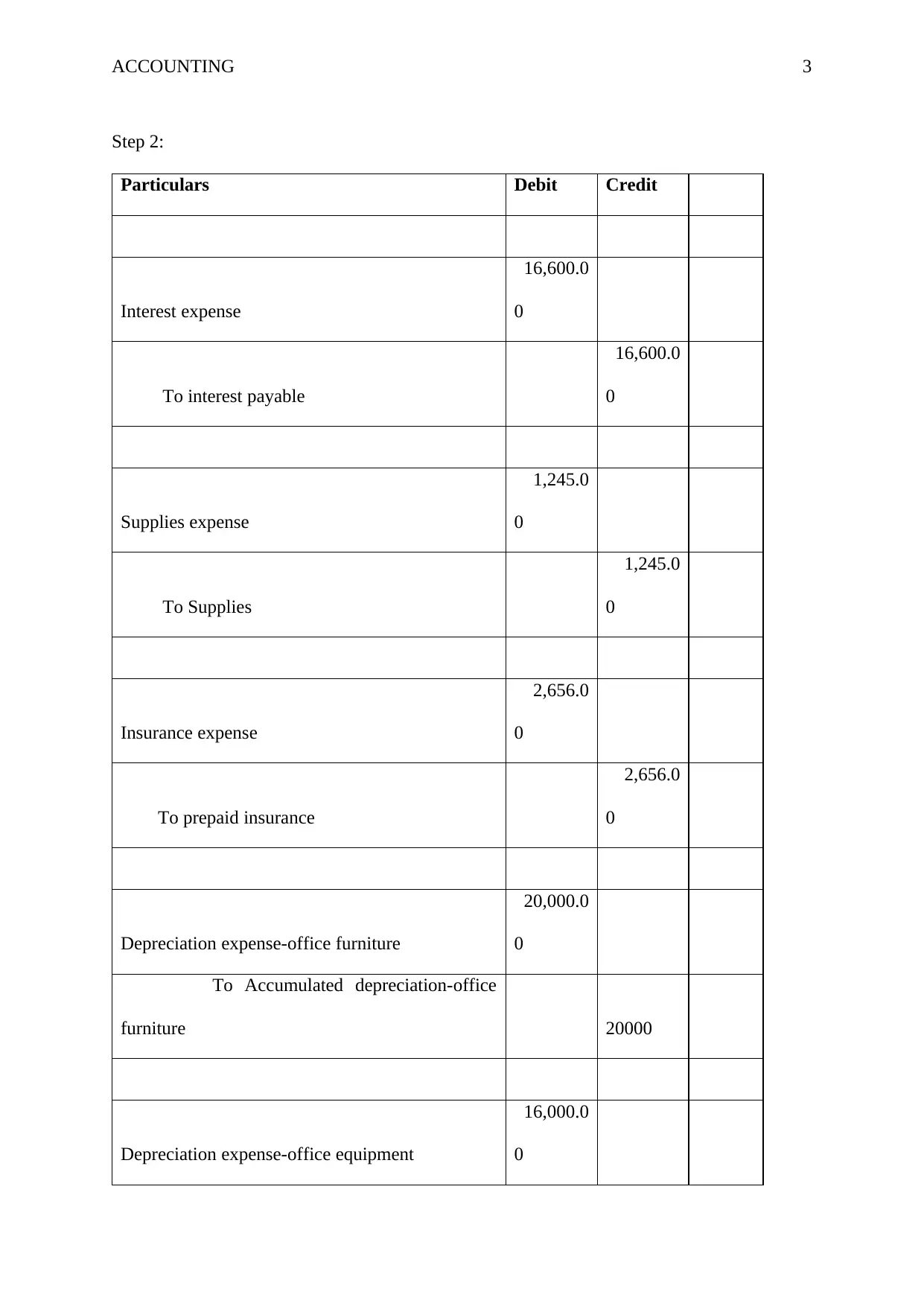

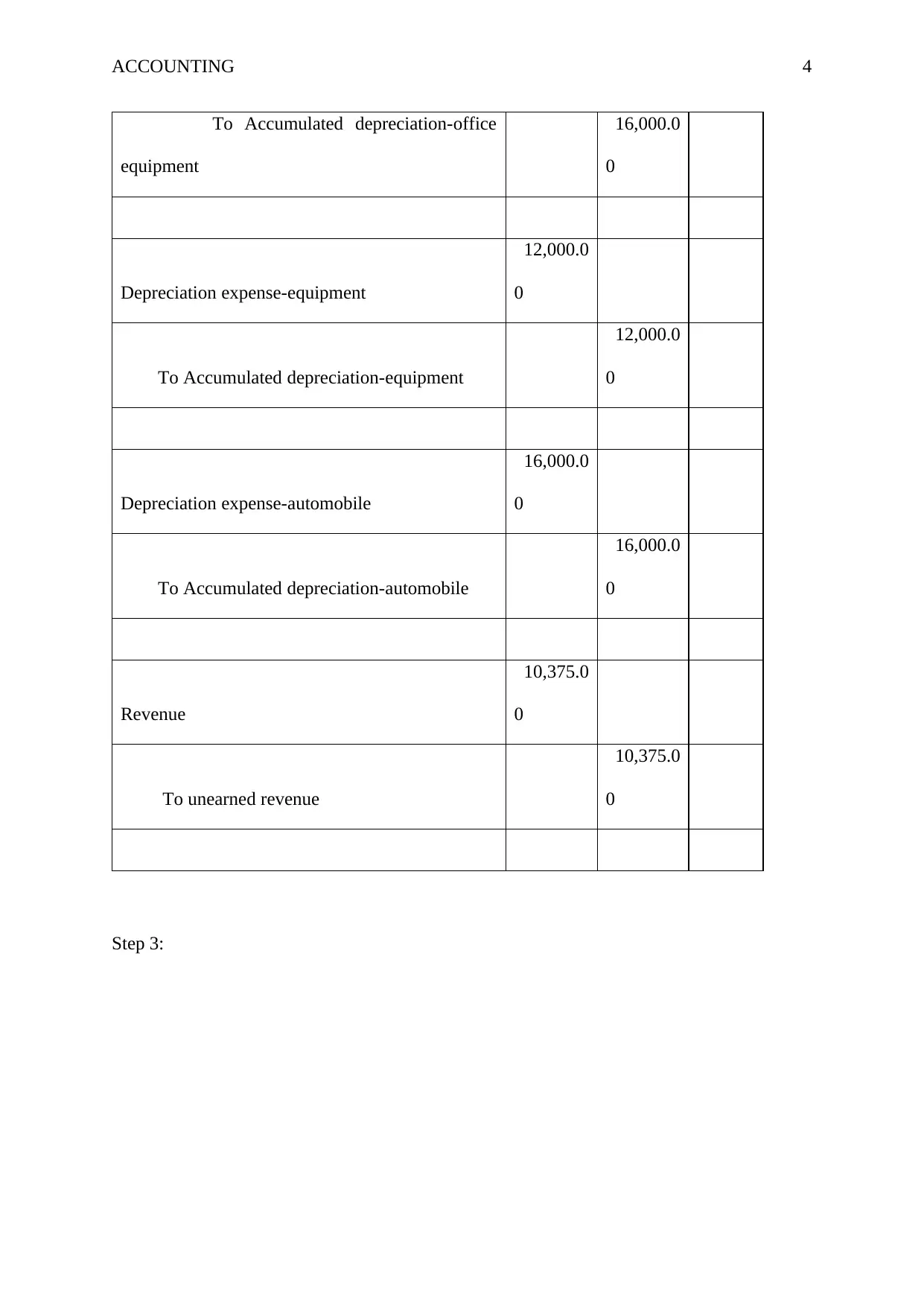

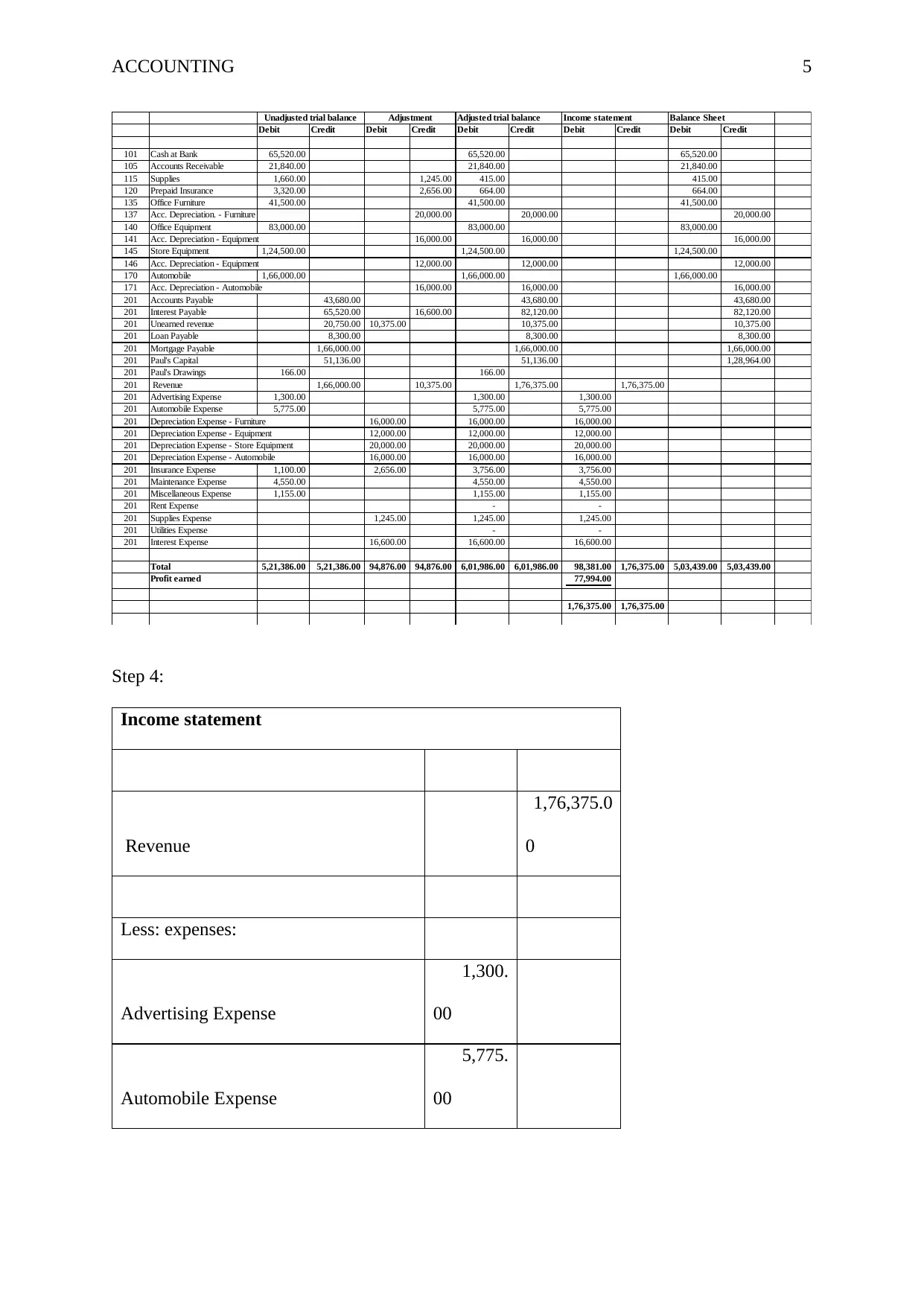

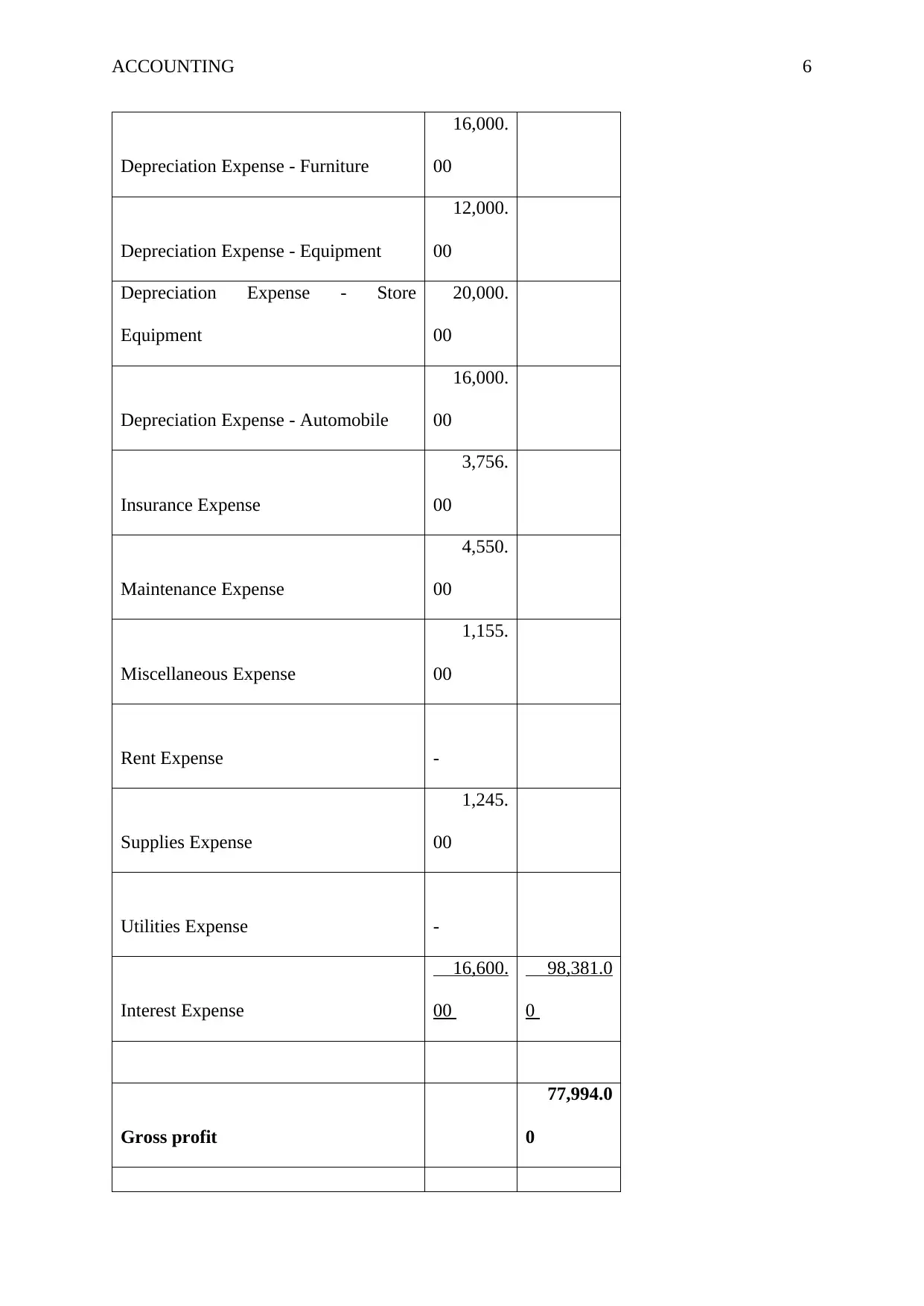

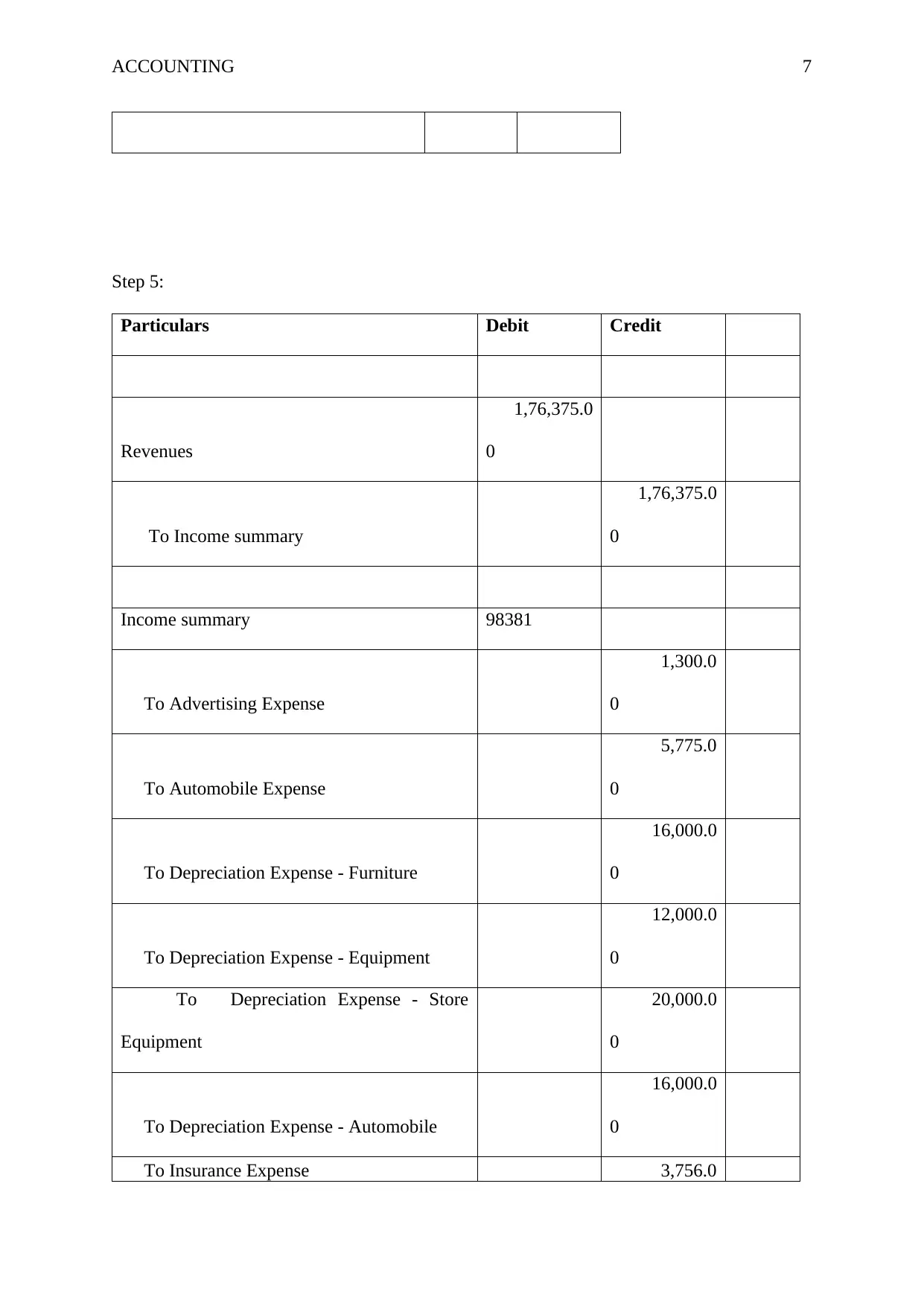

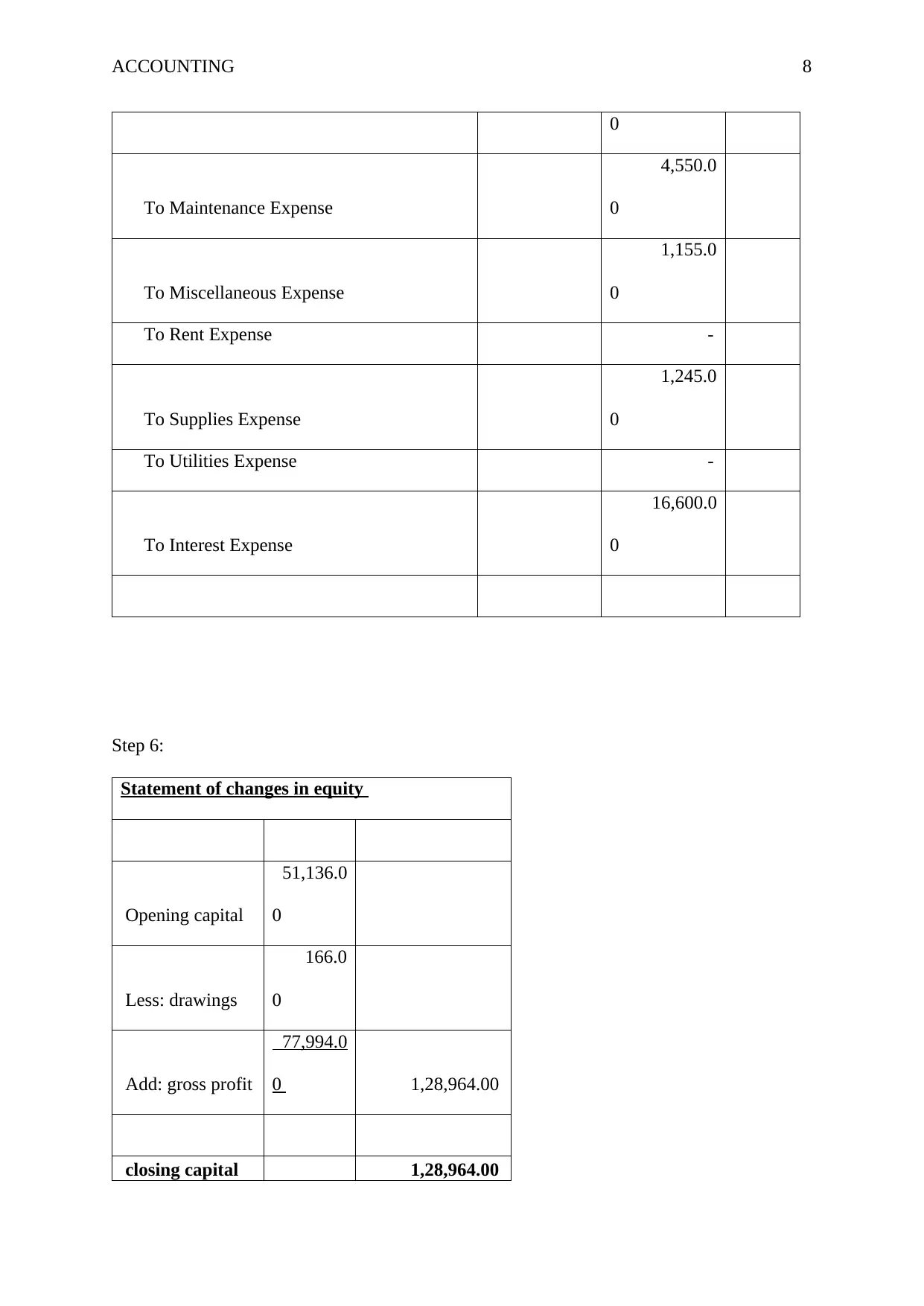

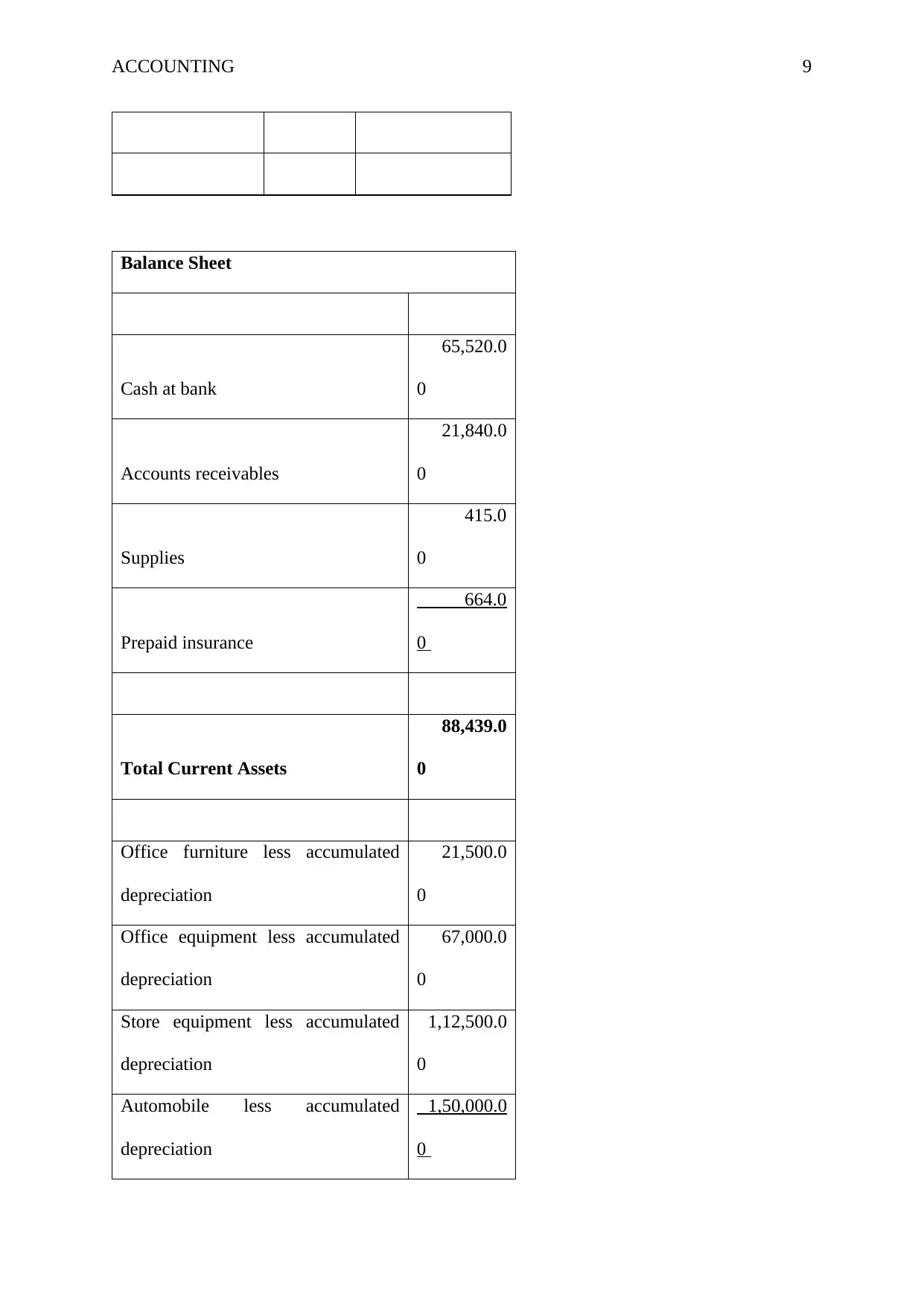

This accounting assignment solution demonstrates the process of preparing and analyzing a trial balance, making necessary adjusting entries, and constructing financial statements. It includes steps such as adjusting entries for interest, supplies, insurance, and depreciation, and then preparing an adjusted trial balance. The solution further illustrates the creation of an income statement, balance sheet, and statement of changes in equity. It also explains the purpose of each step, from ensuring the general ledger is balanced to adhering to the accrual concept of accounting. The document also explains the significance of adjusting and closing entries in maintaining accurate financial records and provides an overview of how these elements connect to provide a comprehensive view of a company's financial position. Desklib provides a range of similar solved assignments and past papers to assist students in their studies.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.