Auriel's Trial Balance: Source, Structure, and Year-End Adjustments

VerifiedAdded on 2024/06/03

|6

|767

|196

Report

AI Summary

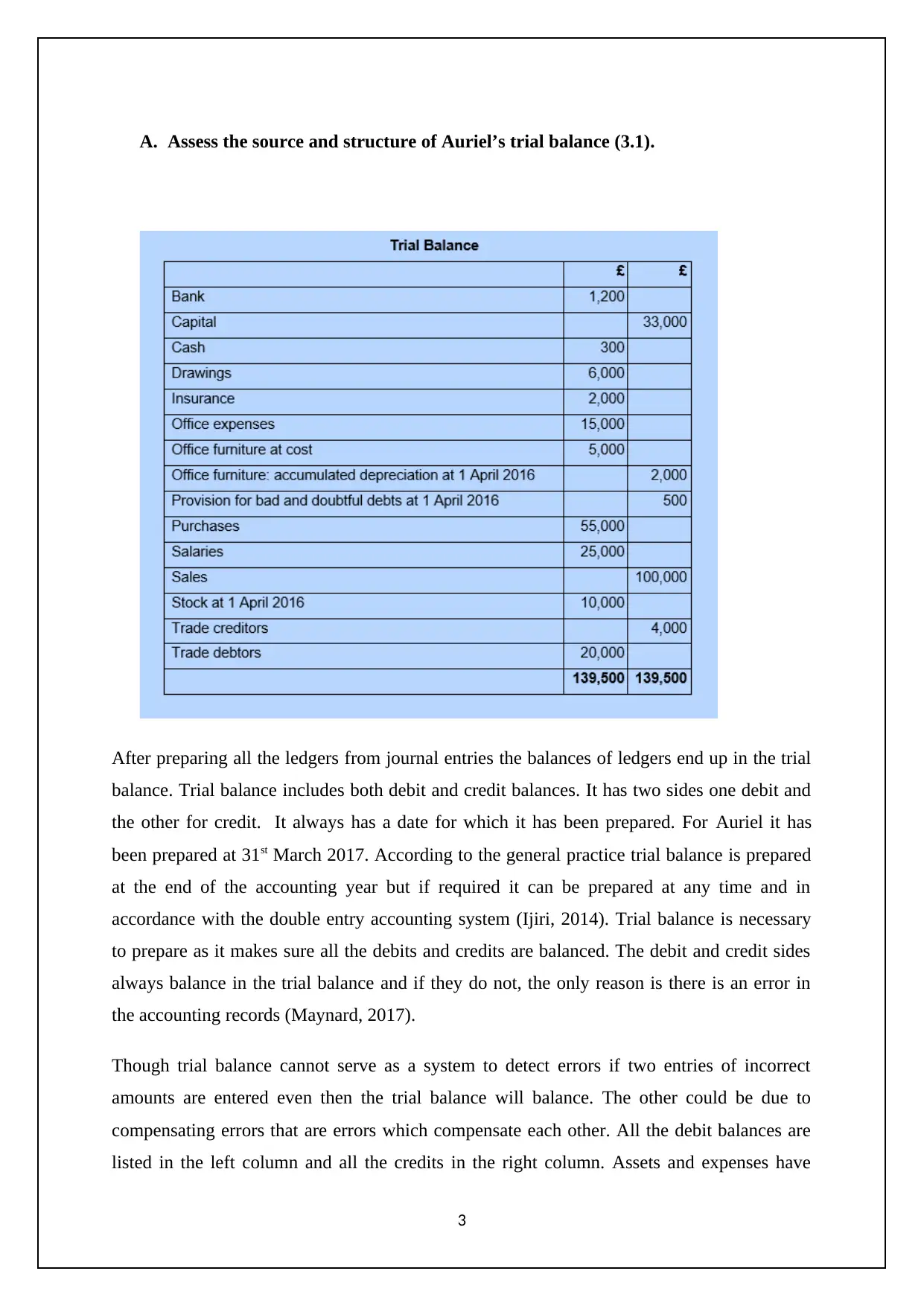

This report provides a detailed analysis of Auriel's trial balance, assessing its source and structure, which originates from ledger balances after journal entries, ensuring debits and credits are balanced as per double-entry accounting principles. It evaluates the impact of year-end adjustments, including accrual expenses (unpaid expenses like salaries), prepaid expenses (advance payments like insurance), depreciation (wear and tear on fixed assets), and provision for doubtful debts (estimated bad debts), on the business's income statement and balance sheet, explaining how these adjustments affect the presentation of financial information and the overall financial position of the company. The report references key accounting texts to support its analysis and conclusions.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.