Audit Plan for Trunkey Creek Wines: Financial Accounting Analysis

VerifiedAdded on 2023/06/04

|14

|2189

|384

Report

AI Summary

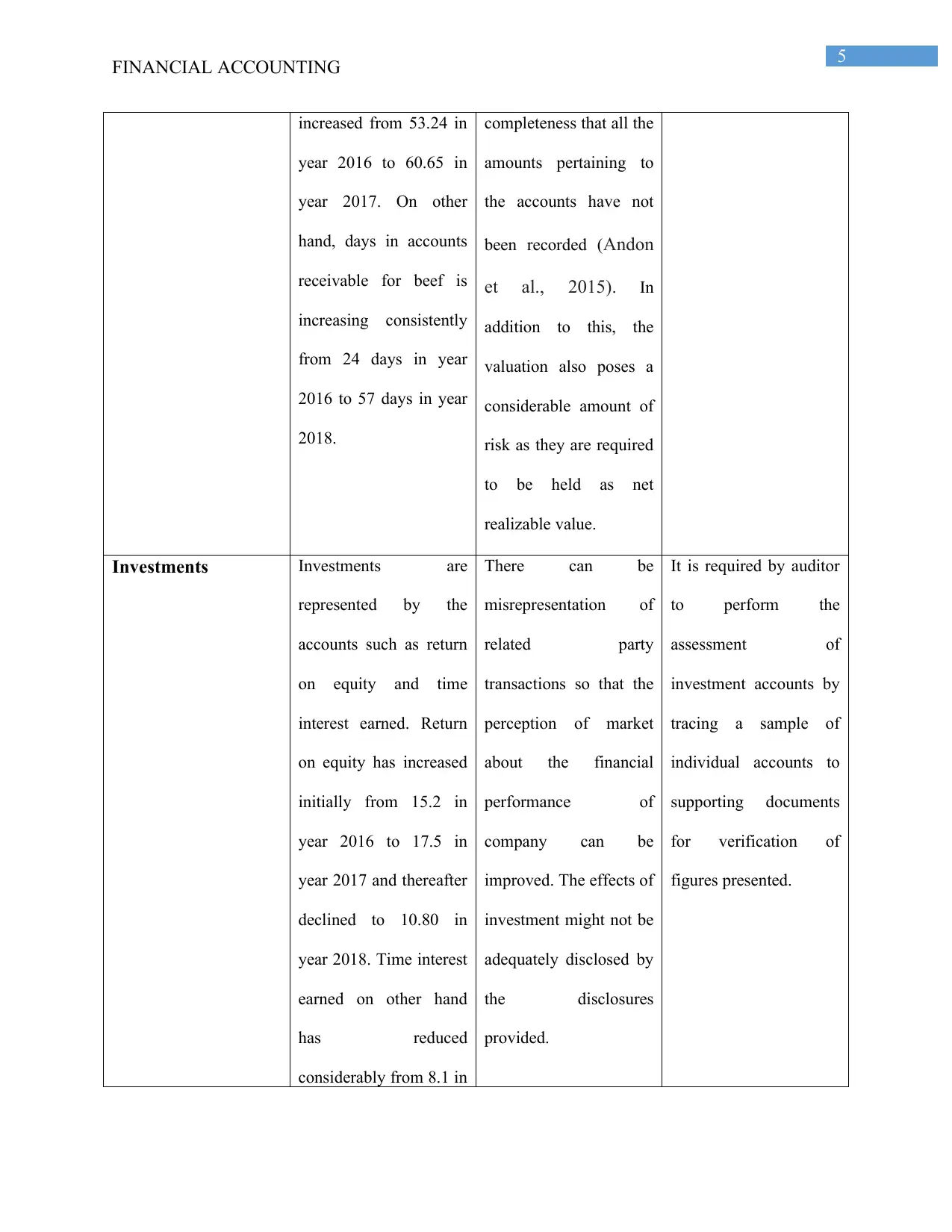

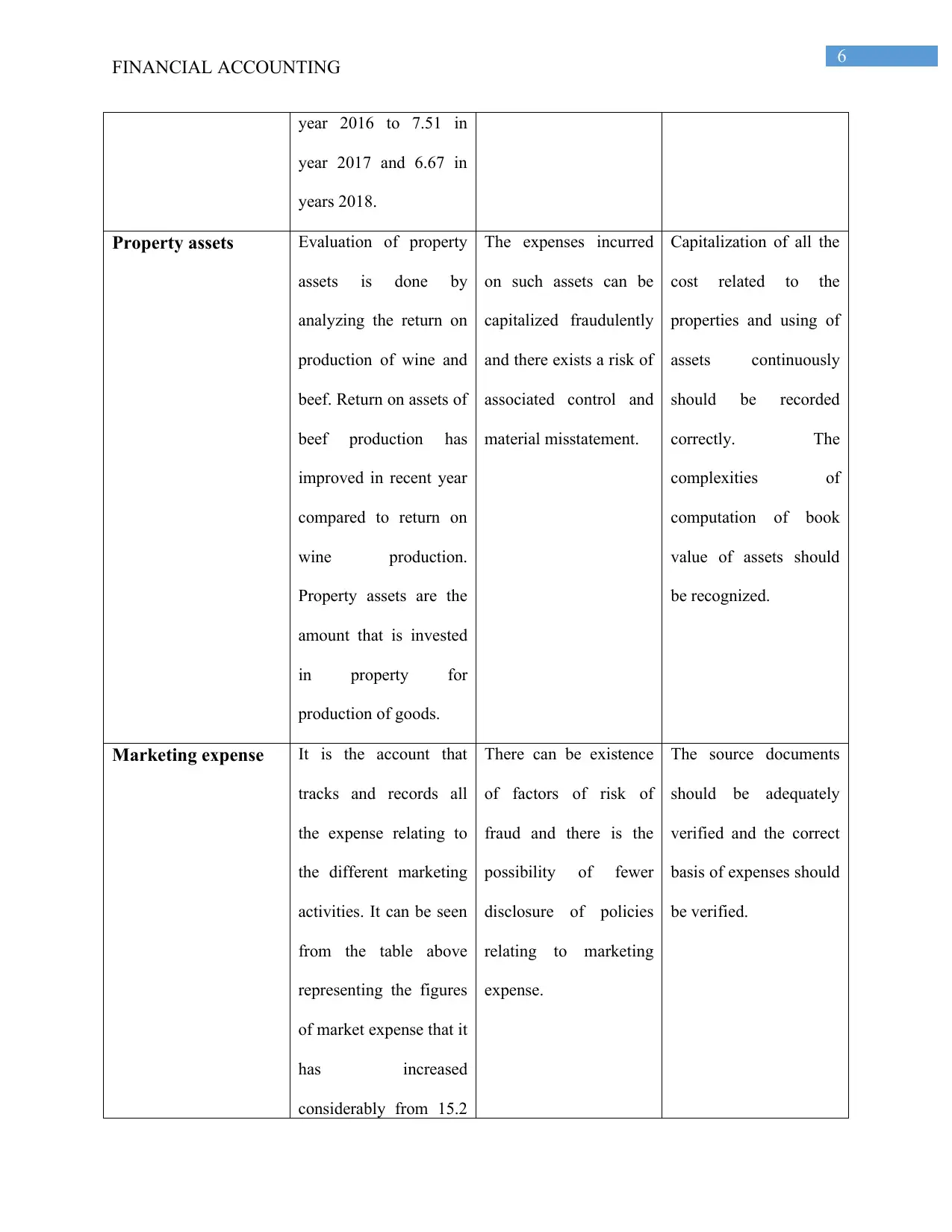

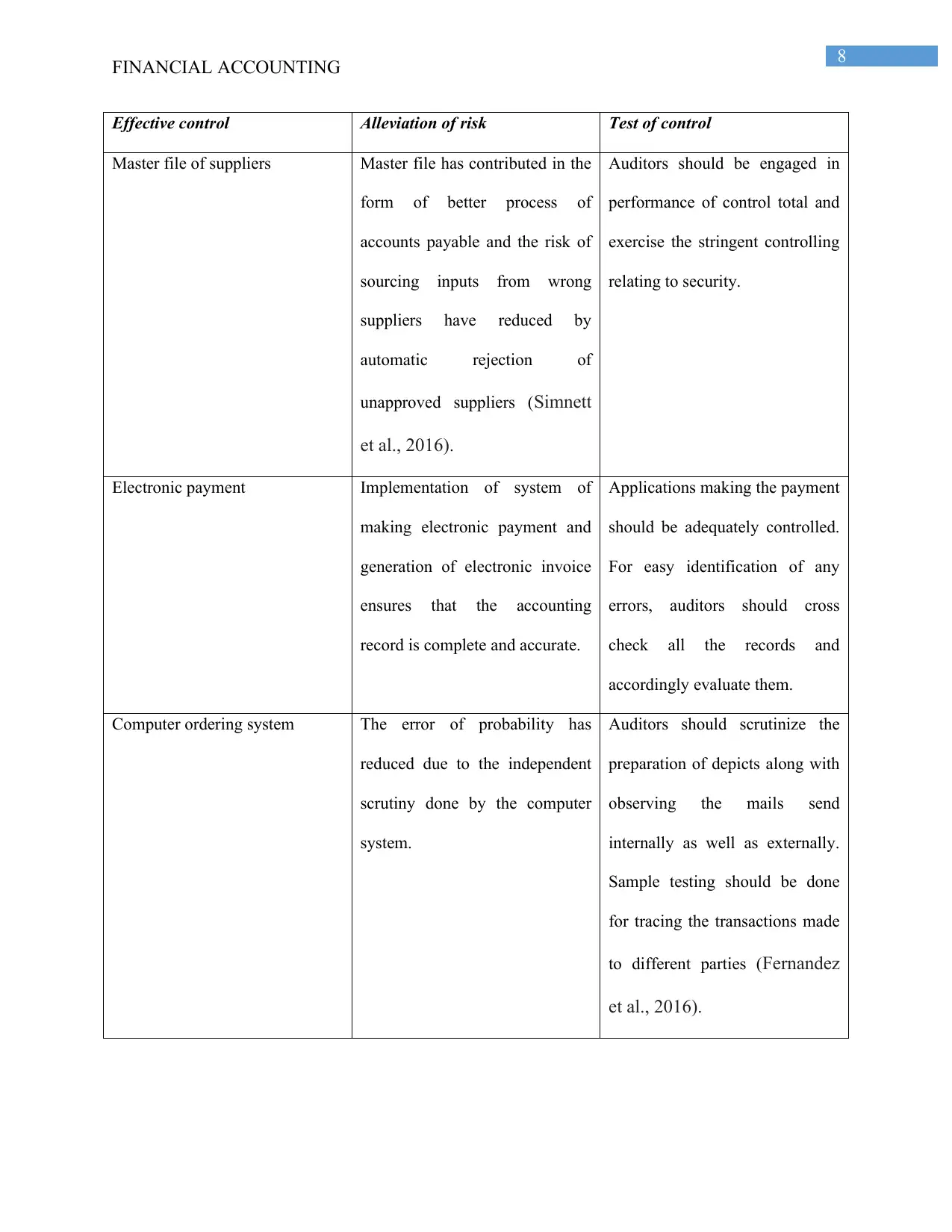

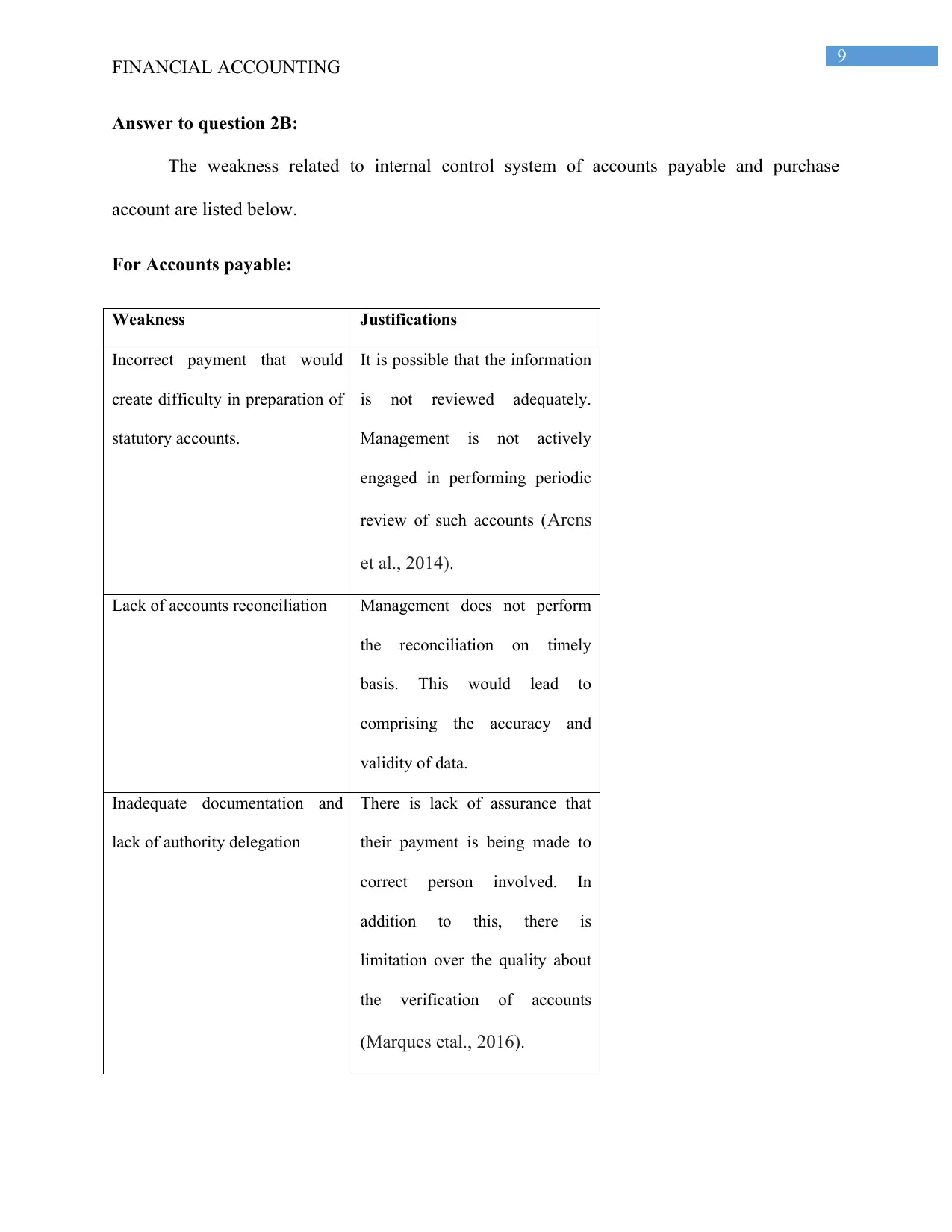

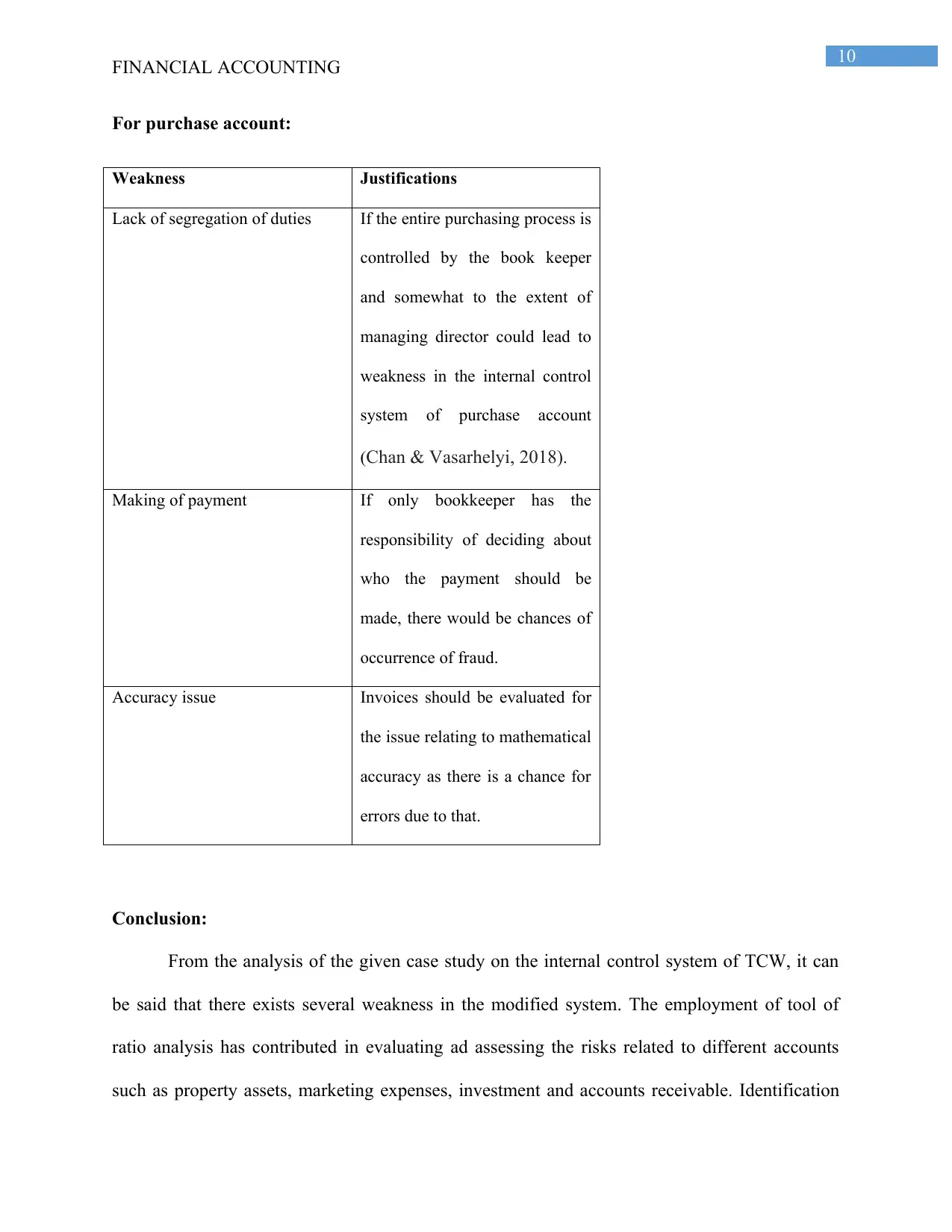

This report details an audit plan for Trunkey Creek Wines (TCW), a significant client of Miller Yates Howarth (MYH). The report analyzes various financial aspects, including accounts receivable, property assets, and marketing expenses, using ratio analysis to assess audit risks. It evaluates the effectiveness of TCW's internal control system, identifies weaknesses in accounts payable and purchase accounts, and recommends audit procedures to mitigate identified risks. The analysis covers the period ending June 30, 2018, comparing financial data with previous years to identify trends and potential areas of concern. The report provides a comprehensive overview of the audit process, addressing key areas of financial accounting and internal controls to ensure the accuracy and reliability of TCW's financial statements.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.