Financial Audit and Assurance: Analysis of Trunkey Creek Wines Ltd

VerifiedAdded on 2023/06/07

|21

|5541

|439

Report

AI Summary

This report provides a financial analysis of Trunkey Creek Wines Limited (TCW), focusing on audit risk assessment and key financial ratios. It identifies potential material misstatements in TCW's financial statements, analyzes accounts receivables, investments, property assets, and marketing expenses, and suggests audit steps to mitigate these risks. The report also evaluates business risks by examining financial ratios such as return on equity, return on assets from beef and wine production, gross margin, marketing expenditure over selling and administrative expenses, times interest earned, and days in inventory. The analysis includes a comparison of financial data from 2016 and 2017, along with unaudited estimates for 2018, to provide a comprehensive overview of TCW's financial health and performance.

Running head: AUDITING AND ASSURANCE IN AUSTRALIA

Auditing and Assurance in Australia

University Name

Student Name

Authors’ Note

Auditing and Assurance in Australia

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

AUDITING AND ASSURANCE IN AUSTRALIA

Executive summary

The study elucidates about the audit risk that indicates towards the issue that is encountered

by the assessor while examining the material misstatement. This may perhaps occur by

reason of error or else fraud. The study presents ways to assess the business risks by

conducting thorough analysis of a ratio that can assist in acquiring a quick indication of the

health and financial of the firm. It also can help the management to identify the strength as

well as weaknesses of the firm and assist in taking a variety of initiatives and framing of

strategies. In the current case, the chosen firm TCW has been evaluated in the present report.

AUDITING AND ASSURANCE IN AUSTRALIA

Executive summary

The study elucidates about the audit risk that indicates towards the issue that is encountered

by the assessor while examining the material misstatement. This may perhaps occur by

reason of error or else fraud. The study presents ways to assess the business risks by

conducting thorough analysis of a ratio that can assist in acquiring a quick indication of the

health and financial of the firm. It also can help the management to identify the strength as

well as weaknesses of the firm and assist in taking a variety of initiatives and framing of

strategies. In the current case, the chosen firm TCW has been evaluated in the present report.

3

AUDITING AND ASSURANCE IN AUSTRALIA

Table of Contents

Solution to Task 1A...................................................................................................................2

Solution to Task 1B....................................................................................................................6

Solution to Task 2A.................................................................................................................12

Solution to Task 2B..................................................................................................................16

References................................................................................................................................18

AUDITING AND ASSURANCE IN AUSTRALIA

Table of Contents

Solution to Task 1A...................................................................................................................2

Solution to Task 1B....................................................................................................................6

Solution to Task 2A.................................................................................................................12

Solution to Task 2B..................................................................................................................16

References................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

AUDITING AND ASSURANCE IN AUSTRALIA

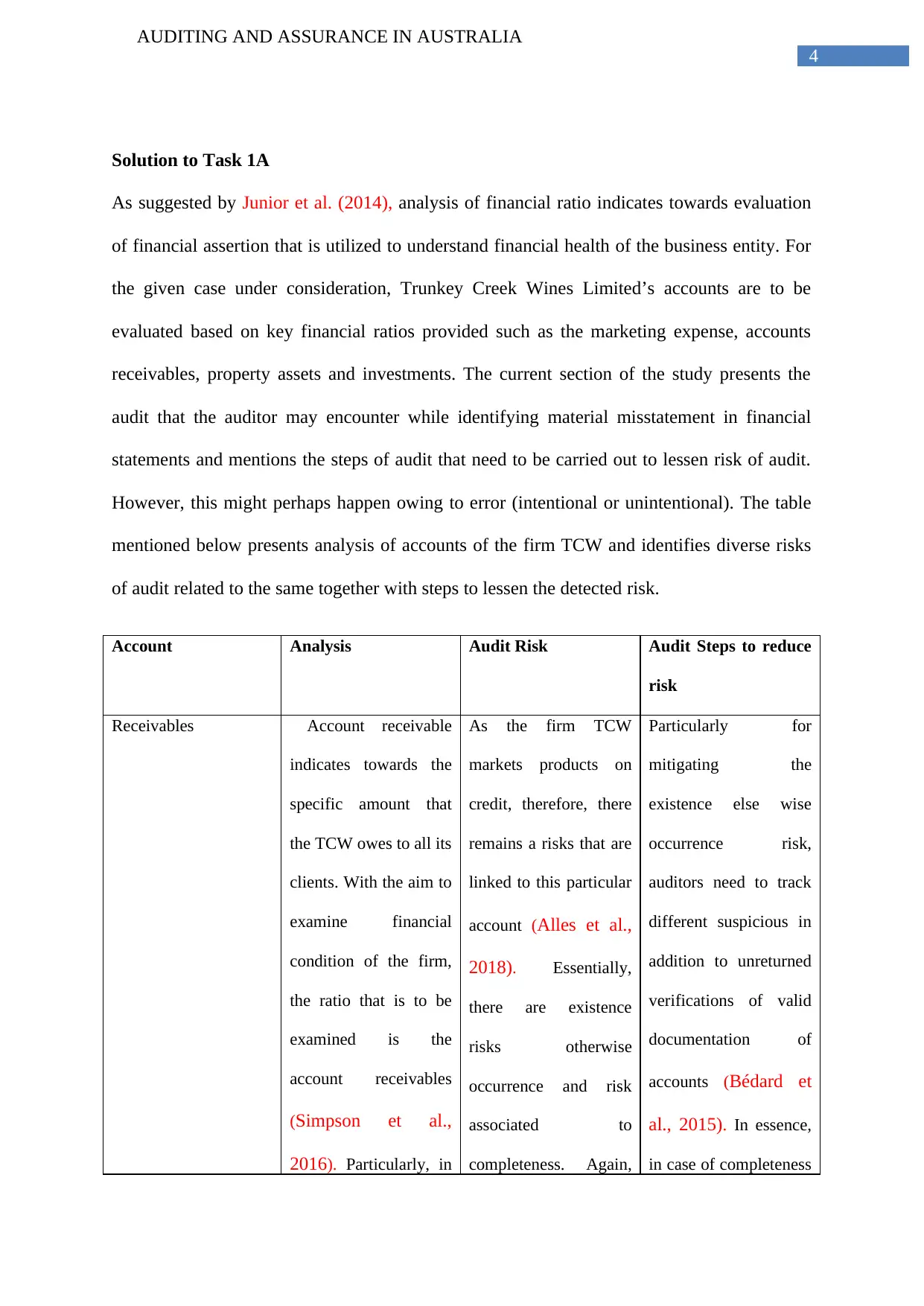

Solution to Task 1A

As suggested by Junior et al. (2014), analysis of financial ratio indicates towards evaluation

of financial assertion that is utilized to understand financial health of the business entity. For

the given case under consideration, Trunkey Creek Wines Limited’s accounts are to be

evaluated based on key financial ratios provided such as the marketing expense, accounts

receivables, property assets and investments. The current section of the study presents the

audit that the auditor may encounter while identifying material misstatement in financial

statements and mentions the steps of audit that need to be carried out to lessen risk of audit.

However, this might perhaps happen owing to error (intentional or unintentional). The table

mentioned below presents analysis of accounts of the firm TCW and identifies diverse risks

of audit related to the same together with steps to lessen the detected risk.

Account Analysis Audit Risk Audit Steps to reduce

risk

Receivables Account receivable

indicates towards the

specific amount that

the TCW owes to all its

clients. With the aim to

examine financial

condition of the firm,

the ratio that is to be

examined is the

account receivables

(Simpson et al.,

2016). Particularly, in

As the firm TCW

markets products on

credit, therefore, there

remains a risks that are

linked to this particular

account (Alles et al.,

2018). Essentially,

there are existence

risks otherwise

occurrence and risk

associated to

completeness. Again,

Particularly for

mitigating the

existence else wise

occurrence risk,

auditors need to track

different suspicious in

addition to unreturned

verifications of valid

documentation of

accounts (Bédard et

al., 2015). In essence,

in case of completeness

AUDITING AND ASSURANCE IN AUSTRALIA

Solution to Task 1A

As suggested by Junior et al. (2014), analysis of financial ratio indicates towards evaluation

of financial assertion that is utilized to understand financial health of the business entity. For

the given case under consideration, Trunkey Creek Wines Limited’s accounts are to be

evaluated based on key financial ratios provided such as the marketing expense, accounts

receivables, property assets and investments. The current section of the study presents the

audit that the auditor may encounter while identifying material misstatement in financial

statements and mentions the steps of audit that need to be carried out to lessen risk of audit.

However, this might perhaps happen owing to error (intentional or unintentional). The table

mentioned below presents analysis of accounts of the firm TCW and identifies diverse risks

of audit related to the same together with steps to lessen the detected risk.

Account Analysis Audit Risk Audit Steps to reduce

risk

Receivables Account receivable

indicates towards the

specific amount that

the TCW owes to all its

clients. With the aim to

examine financial

condition of the firm,

the ratio that is to be

examined is the

account receivables

(Simpson et al.,

2016). Particularly, in

As the firm TCW

markets products on

credit, therefore, there

remains a risks that are

linked to this particular

account (Alles et al.,

2018). Essentially,

there are existence

risks otherwise

occurrence and risk

associated to

completeness. Again,

Particularly for

mitigating the

existence else wise

occurrence risk,

auditors need to track

different suspicious in

addition to unreturned

verifications of valid

documentation of

accounts (Bédard et

al., 2015). In essence,

in case of completeness

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

AUDITING AND ASSURANCE IN AUSTRALIA

the business concern,

the ratio for accounts

receivable for the

particular division of

wine is necessarily

60.65 days and it is 36

days for beef.

Essentially, this

replicates the total

number of days for

which a standard

customer invoice stays

outstanding.

the existence risk

otherwise occurrence

risk indicates towards

the validity risk of the

firm’s debt (Arens et

al., 2014). Conversely,

the completeness risk

refers towards the risk

of incomplete

documentation

risk, the assessor might

consider checking all

the sales proceeds and

analyze the company’s

procedures of business

transactions.

Investment The investment

condition of the firm

can be appropriately

assessed by the ratio of

total number of times

firm earns interest from

its investment (Wong

& Millington, 2014).

During the period

2016, the interest

accepted by the firm

was registered to be

8.10. However, during

the period 2017, it was

If the level of risk is

high, then it is

important on the part of

financiers to make

planned disbursements.

In itself, this would

alarm the business

enterprise, since this

would exert impact on

firm’s working capital

(Marques, 2018).

Particularly, there

subsists an inherent

risk of occurrence of

In this case the assessor

might perhaps acquire

evidence regarding

investment undertaken

at cost value else wise

fair value as has been

divulged in the

financial assertion

(Louwers et al.,

2015). Also, they too

have the need to

identify diverse

approaches for

ascertainment of fair

AUDITING AND ASSURANCE IN AUSTRALIA

the business concern,

the ratio for accounts

receivable for the

particular division of

wine is necessarily

60.65 days and it is 36

days for beef.

Essentially, this

replicates the total

number of days for

which a standard

customer invoice stays

outstanding.

the existence risk

otherwise occurrence

risk indicates towards

the validity risk of the

firm’s debt (Arens et

al., 2014). Conversely,

the completeness risk

refers towards the risk

of incomplete

documentation

risk, the assessor might

consider checking all

the sales proceeds and

analyze the company’s

procedures of business

transactions.

Investment The investment

condition of the firm

can be appropriately

assessed by the ratio of

total number of times

firm earns interest from

its investment (Wong

& Millington, 2014).

During the period

2016, the interest

accepted by the firm

was registered to be

8.10. However, during

the period 2017, it was

If the level of risk is

high, then it is

important on the part of

financiers to make

planned disbursements.

In itself, this would

alarm the business

enterprise, since this

would exert impact on

firm’s working capital

(Marques, 2018).

Particularly, there

subsists an inherent

risk of occurrence of

In this case the assessor

might perhaps acquire

evidence regarding

investment undertaken

at cost value else wise

fair value as has been

divulged in the

financial assertion

(Louwers et al.,

2015). Also, they too

have the need to

identify diverse

approaches for

ascertainment of fair

6

AUDITING AND ASSURANCE IN AUSTRALIA

recorded to be 7.51.

Therefore, it can be

hereby mentioned that

investment for the firm

TCW has enhanced

considerably.

Basically, debt to

equity ratio reflects

overall risk of

investment of the firm

and higher debt equity

ratio replicates risk

linked to investment

(Kocken & Hulstijn,

2017).

material misstatement. value according to

regulations of the

(Generally Accepted

Accounting Principles-

GAAP).

Property assets In a bid to assess audit

risk associated to

property assets, then

the ratio return on

firm’s assets of both

sections of both wine

as well as beef of the

firm is to be evaluated.

Based on the provided

information, it can be

recognized that return

The risk that is related

to registering of

property assets

comprises of accurate

cost basis registering

and intricacy in assets

valuation (Liao et al.,

2018).

It is the task of the

assessor to inspect

whether the firm TCW

has capitalized

different cost

associated to the

purchase of firm’s

assets together with

documentation of

preservation and

maintenance of firm’s

AUDITING AND ASSURANCE IN AUSTRALIA

recorded to be 7.51.

Therefore, it can be

hereby mentioned that

investment for the firm

TCW has enhanced

considerably.

Basically, debt to

equity ratio reflects

overall risk of

investment of the firm

and higher debt equity

ratio replicates risk

linked to investment

(Kocken & Hulstijn,

2017).

material misstatement. value according to

regulations of the

(Generally Accepted

Accounting Principles-

GAAP).

Property assets In a bid to assess audit

risk associated to

property assets, then

the ratio return on

firm’s assets of both

sections of both wine

as well as beef of the

firm is to be evaluated.

Based on the provided

information, it can be

recognized that return

The risk that is related

to registering of

property assets

comprises of accurate

cost basis registering

and intricacy in assets

valuation (Liao et al.,

2018).

It is the task of the

assessor to inspect

whether the firm TCW

has capitalized

different cost

associated to the

purchase of firm’s

assets together with

documentation of

preservation and

maintenance of firm’s

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

AUDITING AND ASSURANCE IN AUSTRALIA

on beef production of

the firm’s asset during

the period 2017 has

been enhanced to -

0.82% from the level -

3.45% that was

registered during the

period 2016.

assets. Over and above

that the assessor must

lessen the intricacy of

the evidence of firm’s

assets and make it

more moderately

simple so as to avert

gap in the audit

procedure and

accounting method

(Chan & Vasarhelyi,

2018).

Marketing Expense Percentage of

marketing expenditure

of overall S & A

expenditure of the firm

will reflect

examination of

marketing expenditure

of the TCW firm.

Particularly, the

audited financial ratio

during the year 2017 is

roughly 17.89% that

has enhanced from

15.2% as recorded

Particularly, the risks

engaged in the process

of audit of firm’s

marketing expenditure

ratio are essentially the

understatement risk,

duplicate disbursement

risk and inappropriate

vendors’ risk (Farooq

& de Villiers, 2017).

Also, there are also

different control risks

of accounting in this

regard.

Different steps of

alleviating the risk

associated to audit of

marketing expenditure

for the assessor are to

carry out a sensible

check on records

regularly plus timely

processing of the

expends (Griffiths,

2016). As a division of

internal control

assessment, the

assessor must also

AUDITING AND ASSURANCE IN AUSTRALIA

on beef production of

the firm’s asset during

the period 2017 has

been enhanced to -

0.82% from the level -

3.45% that was

registered during the

period 2016.

assets. Over and above

that the assessor must

lessen the intricacy of

the evidence of firm’s

assets and make it

more moderately

simple so as to avert

gap in the audit

procedure and

accounting method

(Chan & Vasarhelyi,

2018).

Marketing Expense Percentage of

marketing expenditure

of overall S & A

expenditure of the firm

will reflect

examination of

marketing expenditure

of the TCW firm.

Particularly, the

audited financial ratio

during the year 2017 is

roughly 17.89% that

has enhanced from

15.2% as recorded

Particularly, the risks

engaged in the process

of audit of firm’s

marketing expenditure

ratio are essentially the

understatement risk,

duplicate disbursement

risk and inappropriate

vendors’ risk (Farooq

& de Villiers, 2017).

Also, there are also

different control risks

of accounting in this

regard.

Different steps of

alleviating the risk

associated to audit of

marketing expenditure

for the assessor are to

carry out a sensible

check on records

regularly plus timely

processing of the

expends (Griffiths,

2016). As a division of

internal control

assessment, the

assessor must also

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

AUDITING AND ASSURANCE IN AUSTRALIA

during the year 2016. validate the vendors on

normal basis to avert

the fraudulent

exercises.

Solution to Task 1B

As rightly indicated by Moroney (2015), business risk indicates towards the risk that is

associated to the income variation of the firm. As the firm TCW has considerably stable

earnings over the period, they can simply forecast the utility bills of the clientele within a

specific range. Particularly, the best means to evaluate business risks is to carry out ratio

analysis that would assist in acquiring a quick indication of firm performance in several

important areas. It would assist the administration to identify the strength as well as

weaknesses from different varied initiatives and stratagems can be fashioned. However, for

the firm TCW the financial ratio that are provided and needs to be assessed are mentioned

below:

Return on equity: As correctly mentioned by Kocken and Hulstijn (2017), the return

on equity can be referred to as the technique to assess firm’s profitability that

enumerates that specific amount of profit that the firm TCW shall generate with each

unit of money from equity of shareholders. For the current case under consideration,

return on equity calculated for period 2017 has enhanced to 17.5 from the level of

15.5 as compared to the year ago period of 2016. Nevertheless, it is estimated that

return on equity enumerated for the firm would decline to roughly 10.80 in the year

2018 according to unaudited declarations of the firm TCW.

AUDITING AND ASSURANCE IN AUSTRALIA

during the year 2016. validate the vendors on

normal basis to avert

the fraudulent

exercises.

Solution to Task 1B

As rightly indicated by Moroney (2015), business risk indicates towards the risk that is

associated to the income variation of the firm. As the firm TCW has considerably stable

earnings over the period, they can simply forecast the utility bills of the clientele within a

specific range. Particularly, the best means to evaluate business risks is to carry out ratio

analysis that would assist in acquiring a quick indication of firm performance in several

important areas. It would assist the administration to identify the strength as well as

weaknesses from different varied initiatives and stratagems can be fashioned. However, for

the firm TCW the financial ratio that are provided and needs to be assessed are mentioned

below:

Return on equity: As correctly mentioned by Kocken and Hulstijn (2017), the return

on equity can be referred to as the technique to assess firm’s profitability that

enumerates that specific amount of profit that the firm TCW shall generate with each

unit of money from equity of shareholders. For the current case under consideration,

return on equity calculated for period 2017 has enhanced to 17.5 from the level of

15.5 as compared to the year ago period of 2016. Nevertheless, it is estimated that

return on equity enumerated for the firm would decline to roughly 10.80 in the year

2018 according to unaudited declarations of the firm TCW.

9

AUDITING AND ASSURANCE IN AUSTRALIA

Return earned by the firm on beef making assets: The return earned by the firm on

production assets indicates towards the production power and enumeration of profit

out of the firm’s assets invested in operation (Wong & Millington, 2014). However,

for the current case under consideration, essentially production indicates towards

production of beef of the business concern TCW. The overall percentage of return

earned on assets from beef production has enhanced from approximately-3.45 during

the year 2016 to around 0.82 during the year 2017. Nevertheless, according to

unaudited statements it is predicted that the return from assets of beef production

would enhance to 1.67 during the year 2018.

Return earned on assets such as grape as well as wine production: Return earned

assets such as grape plus wine production in the same way signifies overall power of

production as well as enumeration of profit with firm’s total assets invested in

operation (Kocken & Hulstijn, 2017). For the current case under consideration,

production indicates towards grape as well as vine production of the firm TCW. The

percentage of return earned by the firm TCW on grape as well as assets from wine

production during the year 2016 was registered to be 16.2. However, the same was

observed to decline to 14.5 during the period 2017. TCW’s unaudited return that is

estimated to be below the prior two year’s figure that is registered to be 12.2.

Gross margin enumerated for the firm TCW: The gross profit margin of TCW

indicates ratio of cost of goods of TCWs deducted from the sales revenue and firm’s

total sales (Liao et al., 2018). Essentially, this enumerates overall percentage of the

company’s sales that is retained after the firm incurs different direct cost associated to

manufacturing of products, specifically, beef as well as vine. In case if the enumerated

percentage is observed to be high, then in that case it can be hereby said that the firm

can retain higher in terms of its sales (Fuhrmann et al., 2017). As per the given case,

AUDITING AND ASSURANCE IN AUSTRALIA

Return earned by the firm on beef making assets: The return earned by the firm on

production assets indicates towards the production power and enumeration of profit

out of the firm’s assets invested in operation (Wong & Millington, 2014). However,

for the current case under consideration, essentially production indicates towards

production of beef of the business concern TCW. The overall percentage of return

earned on assets from beef production has enhanced from approximately-3.45 during

the year 2016 to around 0.82 during the year 2017. Nevertheless, according to

unaudited statements it is predicted that the return from assets of beef production

would enhance to 1.67 during the year 2018.

Return earned on assets such as grape as well as wine production: Return earned

assets such as grape plus wine production in the same way signifies overall power of

production as well as enumeration of profit with firm’s total assets invested in

operation (Kocken & Hulstijn, 2017). For the current case under consideration,

production indicates towards grape as well as vine production of the firm TCW. The

percentage of return earned by the firm TCW on grape as well as assets from wine

production during the year 2016 was registered to be 16.2. However, the same was

observed to decline to 14.5 during the period 2017. TCW’s unaudited return that is

estimated to be below the prior two year’s figure that is registered to be 12.2.

Gross margin enumerated for the firm TCW: The gross profit margin of TCW

indicates ratio of cost of goods of TCWs deducted from the sales revenue and firm’s

total sales (Liao et al., 2018). Essentially, this enumerates overall percentage of the

company’s sales that is retained after the firm incurs different direct cost associated to

manufacturing of products, specifically, beef as well as vine. In case if the enumerated

percentage is observed to be high, then in that case it can be hereby said that the firm

can retain higher in terms of its sales (Fuhrmann et al., 2017). As per the given case,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

AUDITING AND ASSURANCE IN AUSTRALIA

the gross margin of the firm TCW was recorded to be the highest during the year 2016

(that is 31.76). However, the same declined to roughly 14.5 during the year 2017.

However, the estimated figure for the gross margin is also decreased to around 12.2

for the year 2018. In essence, this advocates that the firm TCW can retain lesser

dollars out of its sales.

Marketing expenditure over S&A expends: As suggested by Griffiths (2016), the

marketing expenditures indicates towards total percentage of wealth that is spent out

of the earned profit of the firm from firm’s selling as well as administrative

expenditure so as to augment sales. Essentially, this can be considered to be an

indirect cost of the firm. According to audited accounts for the year 2017 and the year

2016, the total fraction of marketing expenditure is observed to decrease from 15.2

recorded during the year 2016 to around 17.89 registered during the year 2017.

Essentially, it estimated that marketing expense ratio would enhance to the level of

23.67 as per the unaudited documentation.

Times interest earned: As suggested by Cohen and Simnett (2014), the times to

interest earned indicates towards coverage ratio which enumerates overall capability

of the firm for disbursement of debt amount. If it is observed that the interest coverage

ratio is lower than 1, then that implies that the firm is not generating adequate cash

from its operations (Chan & Vasarhelyi, 2018). For the current case, the interest

earned calculated for the company TCW is declining that reflects that there is not

enough cash earnings. During the year 2017 this interest earned was recorded to be

7.51; while in the year 2016 it was registered to be 8.10. However, the estimated

figure was recorded to be 6.67 during the period 2018.

Days in inventory (for particularly wine): Essentially, the days sales reflects the

total number of days the firm took for marketing all its stocks available during a

AUDITING AND ASSURANCE IN AUSTRALIA

the gross margin of the firm TCW was recorded to be the highest during the year 2016

(that is 31.76). However, the same declined to roughly 14.5 during the year 2017.

However, the estimated figure for the gross margin is also decreased to around 12.2

for the year 2018. In essence, this advocates that the firm TCW can retain lesser

dollars out of its sales.

Marketing expenditure over S&A expends: As suggested by Griffiths (2016), the

marketing expenditures indicates towards total percentage of wealth that is spent out

of the earned profit of the firm from firm’s selling as well as administrative

expenditure so as to augment sales. Essentially, this can be considered to be an

indirect cost of the firm. According to audited accounts for the year 2017 and the year

2016, the total fraction of marketing expenditure is observed to decrease from 15.2

recorded during the year 2016 to around 17.89 registered during the year 2017.

Essentially, it estimated that marketing expense ratio would enhance to the level of

23.67 as per the unaudited documentation.

Times interest earned: As suggested by Cohen and Simnett (2014), the times to

interest earned indicates towards coverage ratio which enumerates overall capability

of the firm for disbursement of debt amount. If it is observed that the interest coverage

ratio is lower than 1, then that implies that the firm is not generating adequate cash

from its operations (Chan & Vasarhelyi, 2018). For the current case, the interest

earned calculated for the company TCW is declining that reflects that there is not

enough cash earnings. During the year 2017 this interest earned was recorded to be

7.51; while in the year 2016 it was registered to be 8.10. However, the estimated

figure was recorded to be 6.67 during the period 2018.

Days in inventory (for particularly wine): Essentially, the days sales reflects the

total number of days the firm took for marketing all its stocks available during a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

AUDITING AND ASSURANCE IN AUSTRALIA

specific time period (Junior et al., 2014). For the current case, the inventory indicates

towards the wine production. For the wine production of the company, the days of

inventory registered for the year 2016 was observed to be 460, while in the year 2017

it was registered to be 423. This indicates increase in ability of the firm to sell its

inventory. However, the estimated figure was the same was recorded to be 367

reflecting further decline in the requisite days to sell the firm’s inventory.

Days in accounts receivables (for wine production): According to Simpson et al.

(2016), days in accounts receivables indicates towards the average days that the firm

TCW would require to gather the payments made on the sold goods. In case, the total

numbers of days are high, in that case it points out that there is a hitch in the process

of collection and stream of cash (Alles et al., 2018). Again, if the total numbers of

days are low, then that might also indicate that the company has a stringent credit

policy that in turn might lower the sales. As per the given case study, the goods

indicate towards wine production of the firm TCW. Essentially, the account

receivable (in terms of days) for particularly wine was registered to be 53.24 during

the year 2016. However, the same increased to 60.65 in the year 2017 and the figures

(unaudited) was record to be 50.2.

Days in accounts receivables (for production of beef): Arens et al. (2014) suggest

that the accounts receivables (days) of production of beef indicates towards total days

needed for amassing the payments made on the sale of particularly beef. However, an

increasing trend in accounts receivables can be observed in this regard. The days of

account receivable for the purpose of beef was recorded to be 24 during the year

2016. However, the same was observed to increase to 36 during the year 2017.

However, the unaudited figure was recorded to be 57.

AUDITING AND ASSURANCE IN AUSTRALIA

specific time period (Junior et al., 2014). For the current case, the inventory indicates

towards the wine production. For the wine production of the company, the days of

inventory registered for the year 2016 was observed to be 460, while in the year 2017

it was registered to be 423. This indicates increase in ability of the firm to sell its

inventory. However, the estimated figure was the same was recorded to be 367

reflecting further decline in the requisite days to sell the firm’s inventory.

Days in accounts receivables (for wine production): According to Simpson et al.

(2016), days in accounts receivables indicates towards the average days that the firm

TCW would require to gather the payments made on the sold goods. In case, the total

numbers of days are high, in that case it points out that there is a hitch in the process

of collection and stream of cash (Alles et al., 2018). Again, if the total numbers of

days are low, then that might also indicate that the company has a stringent credit

policy that in turn might lower the sales. As per the given case study, the goods

indicate towards wine production of the firm TCW. Essentially, the account

receivable (in terms of days) for particularly wine was registered to be 53.24 during

the year 2016. However, the same increased to 60.65 in the year 2017 and the figures

(unaudited) was record to be 50.2.

Days in accounts receivables (for production of beef): Arens et al. (2014) suggest

that the accounts receivables (days) of production of beef indicates towards total days

needed for amassing the payments made on the sale of particularly beef. However, an

increasing trend in accounts receivables can be observed in this regard. The days of

account receivable for the purpose of beef was recorded to be 24 during the year

2016. However, the same was observed to increase to 36 during the year 2017.

However, the unaudited figure was recorded to be 57.

12

AUDITING AND ASSURANCE IN AUSTRALIA

Current ratio: According to Basu (2016), current ratio that is essentially a liquidity

ratio assists in the process of enumerating overall capability firm to cope up with

different obligations that include both short-term as well as long term obligations. It is

essentially the ratio of the current assets and the current liabilities of the firm. For the

current case under consideration, the total assets signify both liquid plus liquid assets

of the firm TCW. In this case, the current ratio was registered to be 2.66 during the

year 2016 that declined to 2.54 in the year 2017(although insignificantly). The

unaudited records for the same stood at 2.80.

Quick asset ratio: As suggested by Marques (2018), the quick ratio or else acid -test

ratio points out towards the current assets that can effortlessly converted into liquid

cash. For the given case under consideration, the current ratio was registered to be

1.20 during the year 2016, while the same was registered to be 1.15 in the year 2017.

The decline in this ratio implies an unfavorable condition of the firm as this suggests

that the liquidity condition of the firm has deteriorated. However, the unaudited

record was observed to be 1.18.

Debts to equity ratio: Wong and Millington (2014) suggest that ratio of debt to

equity signifies a specific financial ratio that is enumerated to reflect the relative

fraction of debt and equity of the firm to fund its operations. Higher debt equity

reflects higher risk for the firm as the firm has obligations to pay off the debt amount

as well as interest. Debt to equity ratio for the firm TCW was recorded to be 0.67 in

the year 2016. However, the figure declined to 0.63 in the year 2017, while the

unaudited record was documented to be 0.54.

Based on analysis of key financial ratio presented above, diverse kinds of risks can be

identified. Essentially, business risk indicates towards the possibility of not getting back a

AUDITING AND ASSURANCE IN AUSTRALIA

Current ratio: According to Basu (2016), current ratio that is essentially a liquidity

ratio assists in the process of enumerating overall capability firm to cope up with

different obligations that include both short-term as well as long term obligations. It is

essentially the ratio of the current assets and the current liabilities of the firm. For the

current case under consideration, the total assets signify both liquid plus liquid assets

of the firm TCW. In this case, the current ratio was registered to be 2.66 during the

year 2016 that declined to 2.54 in the year 2017(although insignificantly). The

unaudited records for the same stood at 2.80.

Quick asset ratio: As suggested by Marques (2018), the quick ratio or else acid -test

ratio points out towards the current assets that can effortlessly converted into liquid

cash. For the given case under consideration, the current ratio was registered to be

1.20 during the year 2016, while the same was registered to be 1.15 in the year 2017.

The decline in this ratio implies an unfavorable condition of the firm as this suggests

that the liquidity condition of the firm has deteriorated. However, the unaudited

record was observed to be 1.18.

Debts to equity ratio: Wong and Millington (2014) suggest that ratio of debt to

equity signifies a specific financial ratio that is enumerated to reflect the relative

fraction of debt and equity of the firm to fund its operations. Higher debt equity

reflects higher risk for the firm as the firm has obligations to pay off the debt amount

as well as interest. Debt to equity ratio for the firm TCW was recorded to be 0.67 in

the year 2016. However, the figure declined to 0.63 in the year 2017, while the

unaudited record was documented to be 0.54.

Based on analysis of key financial ratio presented above, diverse kinds of risks can be

identified. Essentially, business risk indicates towards the possibility of not getting back a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.