Audit Report for Trunkey Creek Wines Limited: Financial Evaluation

VerifiedAdded on 2023/06/07

|14

|3401

|139

Report

AI Summary

This audit report provides a detailed financial analysis of Trunkey Creek Wines Limited (TCW), a client of Miller Yates Howarth (MYH), an Australian accounting firm. The report includes a ratio assessment to identify financial deficiencies and risks, focusing on marketing costs, investments, accounts receivable, and property assets. It assesses business risks related to declining return on equity, gross margin, and net profit margin, as well as liquidity management and debt recovery. The report also examines internal control mechanisms and tests of control related to repairs, supplies management, payment processes, and IT system management, highlighting potential audit risks and suggesting steps to mitigate them. The analysis uses unaudited data from 2018 and compares it with audited data from 2017 and 2016 to provide a comprehensive overview of TCW's financial performance and risk profile.

A DU IT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

Executive summary

Organizations in the corporate world are more likely to empower themselves owing to the

presence of properly explained audit procedures. Hence, possessing effective processes of

audit are compulsory in this era because it assists in detection of material risks in the financial

statements. Moreover, prevalence of internal control mechanisms also facilitates in

smoothening the audit processes. This report has focused on the audit measures adopted by

MYH in its affairs. The company is basically an accounting firm that is headquartered in

Australia. Nevertheless, this report progresses with the evaluation part wherein computation

of ratios is done. After this, the report has discussed the assessment of audit risks together

with the risks and steps to avoid the same. Moreover, enhanced discussion on the company is

also made so that other material business risks can be studied, thereby reflecting all the

mechanisms of internal control and test control in a tabular manner.

1

Executive summary

Organizations in the corporate world are more likely to empower themselves owing to the

presence of properly explained audit procedures. Hence, possessing effective processes of

audit are compulsory in this era because it assists in detection of material risks in the financial

statements. Moreover, prevalence of internal control mechanisms also facilitates in

smoothening the audit processes. This report has focused on the audit measures adopted by

MYH in its affairs. The company is basically an accounting firm that is headquartered in

Australia. Nevertheless, this report progresses with the evaluation part wherein computation

of ratios is done. After this, the report has discussed the assessment of audit risks together

with the risks and steps to avoid the same. Moreover, enhanced discussion on the company is

also made so that other material business risks can be studied, thereby reflecting all the

mechanisms of internal control and test control in a tabular manner.

1

Audit

Introduction

Both audit strategy and audit processes are crucial aspects of identification of material risk of

misstatements in an organization. This can assist companies to become capable of thriving in

this complicated environment. This report has highlighted the processes of audit that must be

present in all the organizations. Further, with this report, risk management mechanisms have

also been reflected together with the role played by the mechanisms of internal control.

Overall, a plan of audit has been established so that the financials can be effectively assessed.

Nonetheless, there has been effective discussion upon various legal measures and the same is

based on the significance of internal control mechanisms (Cappelleto, 2010). Overall, such

mechanisms play a vital role in allowing organizations thrive in this environment and attain

sustainable development on a whole.

2

Introduction

Both audit strategy and audit processes are crucial aspects of identification of material risk of

misstatements in an organization. This can assist companies to become capable of thriving in

this complicated environment. This report has highlighted the processes of audit that must be

present in all the organizations. Further, with this report, risk management mechanisms have

also been reflected together with the role played by the mechanisms of internal control.

Overall, a plan of audit has been established so that the financials can be effectively assessed.

Nonetheless, there has been effective discussion upon various legal measures and the same is

based on the significance of internal control mechanisms (Cappelleto, 2010). Overall, such

mechanisms play a vital role in allowing organizations thrive in this environment and attain

sustainable development on a whole.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

1A. Ratio assessment

This report has significantly concentrated on aspects like ratio evaluation in addition to the

business material risks associated to the company so that audit processes can be effectively

developed. Further, if the ratios are considered, it plays a key role in determining the

deficiencies and the place at which the company stands. Overall, the relevance of internal

control mechanisms in addition to the drawbacks of the scenario must be appropriately taken

into consideration (Elder et. al, 2010). The following table can be accounted for the

assessment of material ratios and risks associated to the same.

Marketing cost

Analysis Audit Risk Audit steps to reduce risk

The company’s marketing

costs have increased in

comparison to the last two

years and the reason behind

this can be due to increased

exposure of the company

towards its beef operations.

The audit risk here is that

marketing costs consists of

personal expenses of

directors and other costs that

are not allowed. This is

because the proportion of

increment in such expenses

does not go together with

sales increment or present

years return in comparison

to the previous tenures.

The auditor’s group must

monitor all documents and

vouchers of such expense.

Besides, they must observe

whether superior authorities

have permitted such

expenses (Elder et. al,

2010). Further, the personal

expenses bill that are of a

relevant value must be

accounted by the auditors as

well.

Investments

Analysis Audit Risk Audit steps to reduce risk

The times income earned

from this account has

deteriorated in comparison

to the last years.

The audit risk here is that

the same may possess a risk

of material misstatement or

can be undervalued in nature

because the interest on

investments has deteriorated

with due course of time.

Auditors must analyze the

cause behind deterioration in

such interest earned.

Further, investments must be

monitored when it comes to

their disposal process

(Matthew, 2015).

3

1A. Ratio assessment

This report has significantly concentrated on aspects like ratio evaluation in addition to the

business material risks associated to the company so that audit processes can be effectively

developed. Further, if the ratios are considered, it plays a key role in determining the

deficiencies and the place at which the company stands. Overall, the relevance of internal

control mechanisms in addition to the drawbacks of the scenario must be appropriately taken

into consideration (Elder et. al, 2010). The following table can be accounted for the

assessment of material ratios and risks associated to the same.

Marketing cost

Analysis Audit Risk Audit steps to reduce risk

The company’s marketing

costs have increased in

comparison to the last two

years and the reason behind

this can be due to increased

exposure of the company

towards its beef operations.

The audit risk here is that

marketing costs consists of

personal expenses of

directors and other costs that

are not allowed. This is

because the proportion of

increment in such expenses

does not go together with

sales increment or present

years return in comparison

to the previous tenures.

The auditor’s group must

monitor all documents and

vouchers of such expense.

Besides, they must observe

whether superior authorities

have permitted such

expenses (Elder et. al,

2010). Further, the personal

expenses bill that are of a

relevant value must be

accounted by the auditors as

well.

Investments

Analysis Audit Risk Audit steps to reduce risk

The times income earned

from this account has

deteriorated in comparison

to the last years.

The audit risk here is that

the same may possess a risk

of material misstatement or

can be undervalued in nature

because the interest on

investments has deteriorated

with due course of time.

Auditors must analyze the

cause behind deterioration in

such interest earned.

Further, investments must be

monitored when it comes to

their disposal process

(Matthew, 2015).

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

Nevertheless, if these have

been disposed, proper

verification of documents

must be made for the same.

In addition, receipts attained

from sale of investments

must be monitored by the

auditors collectively

(Matthew, 2015).

Accounts receivable

Number of debt collection

days has primarily increased

in the year 2018 in

comparison the last year.

Bad debts can reflect an

improper depiction of the

performance of the

company. Further, the aging

of debtors can be misled by

the company as well

(Baldwin, 2010).

The aging register of the

debtors must be verified by

the auditors. In addition, bad

debts must also be analysed

with the allowances for such

bad debts that has been

permitted by the

management (Baldwin,

2010).

Property assets

The return on property

assets has reflected the

upcoming trends:

Return on assets on

production of beef has

reflected a potential

increment that reports at

1.67% in 2018.

Nevertheless, the same

The audit risk in association

to property assets is that the

company must have

increased the sales of beef to

reflect an efficient financial

situation ay(G & Simnet,

2015). Nevertheless, in

relation to the last two years,

the organization is obtaining

In relation to property

assets, the auditor must

evaluate the sales and

revenue aspects to check the

reason behind the sudden

increment in the returns for

beef production ay(G &

Simnet, 2015). In addition,

the sales ledgers must also

4

Nevertheless, if these have

been disposed, proper

verification of documents

must be made for the same.

In addition, receipts attained

from sale of investments

must be monitored by the

auditors collectively

(Matthew, 2015).

Accounts receivable

Number of debt collection

days has primarily increased

in the year 2018 in

comparison the last year.

Bad debts can reflect an

improper depiction of the

performance of the

company. Further, the aging

of debtors can be misled by

the company as well

(Baldwin, 2010).

The aging register of the

debtors must be verified by

the auditors. In addition, bad

debts must also be analysed

with the allowances for such

bad debts that has been

permitted by the

management (Baldwin,

2010).

Property assets

The return on property

assets has reflected the

upcoming trends:

Return on assets on

production of beef has

reflected a potential

increment that reports at

1.67% in 2018.

Nevertheless, the same

The audit risk in association

to property assets is that the

company must have

increased the sales of beef to

reflect an efficient financial

situation ay(G & Simnet,

2015). Nevertheless, in

relation to the last two years,

the organization is obtaining

In relation to property

assets, the auditor must

evaluate the sales and

revenue aspects to check the

reason behind the sudden

increment in the returns for

beef production ay(G &

Simnet, 2015). In addition,

the sales ledgers must also

4

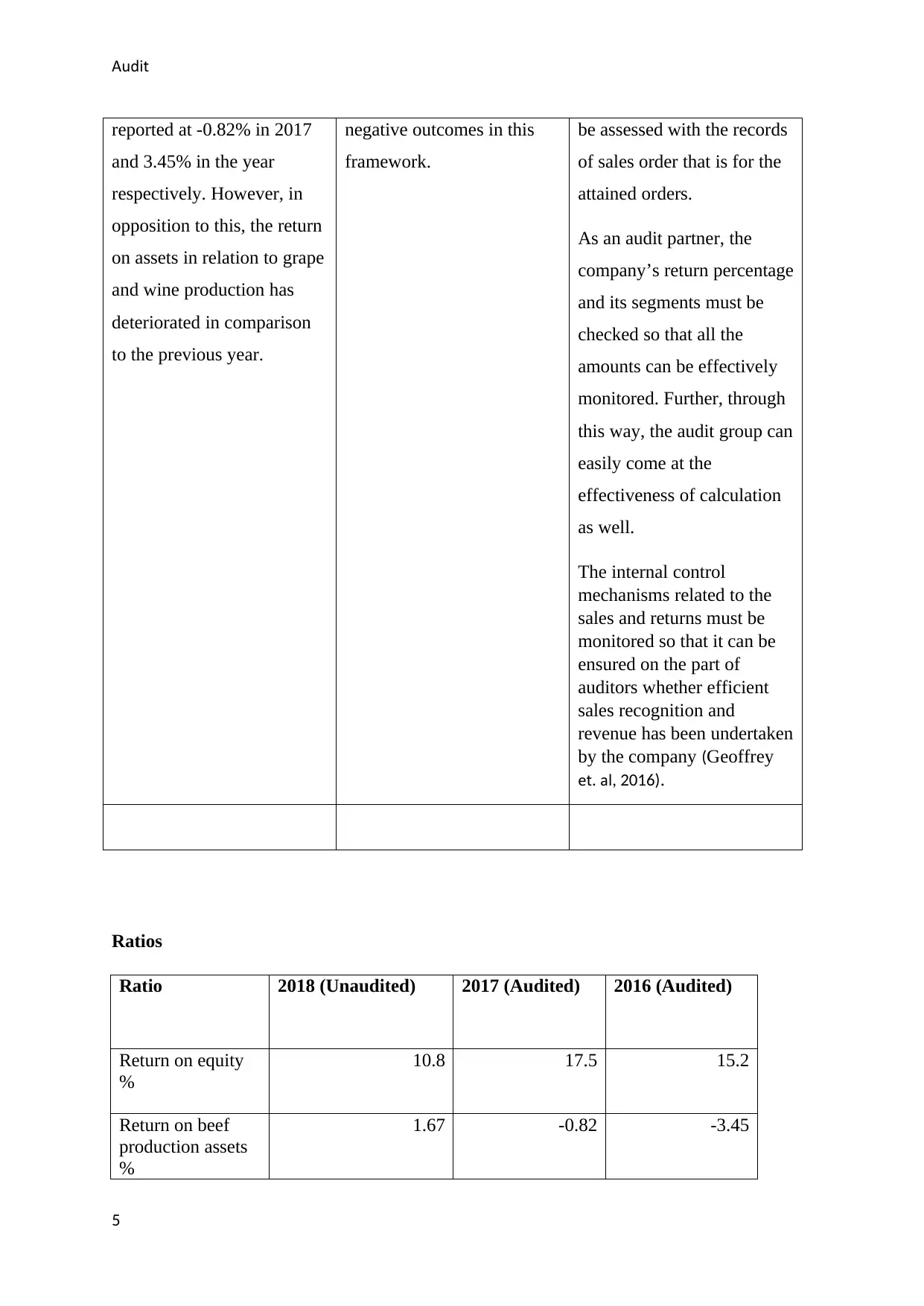

Audit

reported at -0.82% in 2017

and 3.45% in the year

respectively. However, in

opposition to this, the return

on assets in relation to grape

and wine production has

deteriorated in comparison

to the previous year.

negative outcomes in this

framework.

be assessed with the records

of sales order that is for the

attained orders.

As an audit partner, the

company’s return percentage

and its segments must be

checked so that all the

amounts can be effectively

monitored. Further, through

this way, the audit group can

easily come at the

effectiveness of calculation

as well.

The internal control

mechanisms related to the

sales and returns must be

monitored so that it can be

ensured on the part of

auditors whether efficient

sales recognition and

revenue has been undertaken

by the company (Geoffrey

et al. , 2016).

Ratios

Ratio 2018 (Unaudited) 2017 (Audited) 2016 (Audited)

Return on equity

%

10.8 17.5 15.2

Return on beef

production assets

%

1.67 -0.82 -3.45

5

reported at -0.82% in 2017

and 3.45% in the year

respectively. However, in

opposition to this, the return

on assets in relation to grape

and wine production has

deteriorated in comparison

to the previous year.

negative outcomes in this

framework.

be assessed with the records

of sales order that is for the

attained orders.

As an audit partner, the

company’s return percentage

and its segments must be

checked so that all the

amounts can be effectively

monitored. Further, through

this way, the audit group can

easily come at the

effectiveness of calculation

as well.

The internal control

mechanisms related to the

sales and returns must be

monitored so that it can be

ensured on the part of

auditors whether efficient

sales recognition and

revenue has been undertaken

by the company (Geoffrey

et al. , 2016).

Ratios

Ratio 2018 (Unaudited) 2017 (Audited) 2016 (Audited)

Return on equity

%

10.8 17.5 15.2

Return on beef

production assets

%

1.67 -0.82 -3.45

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

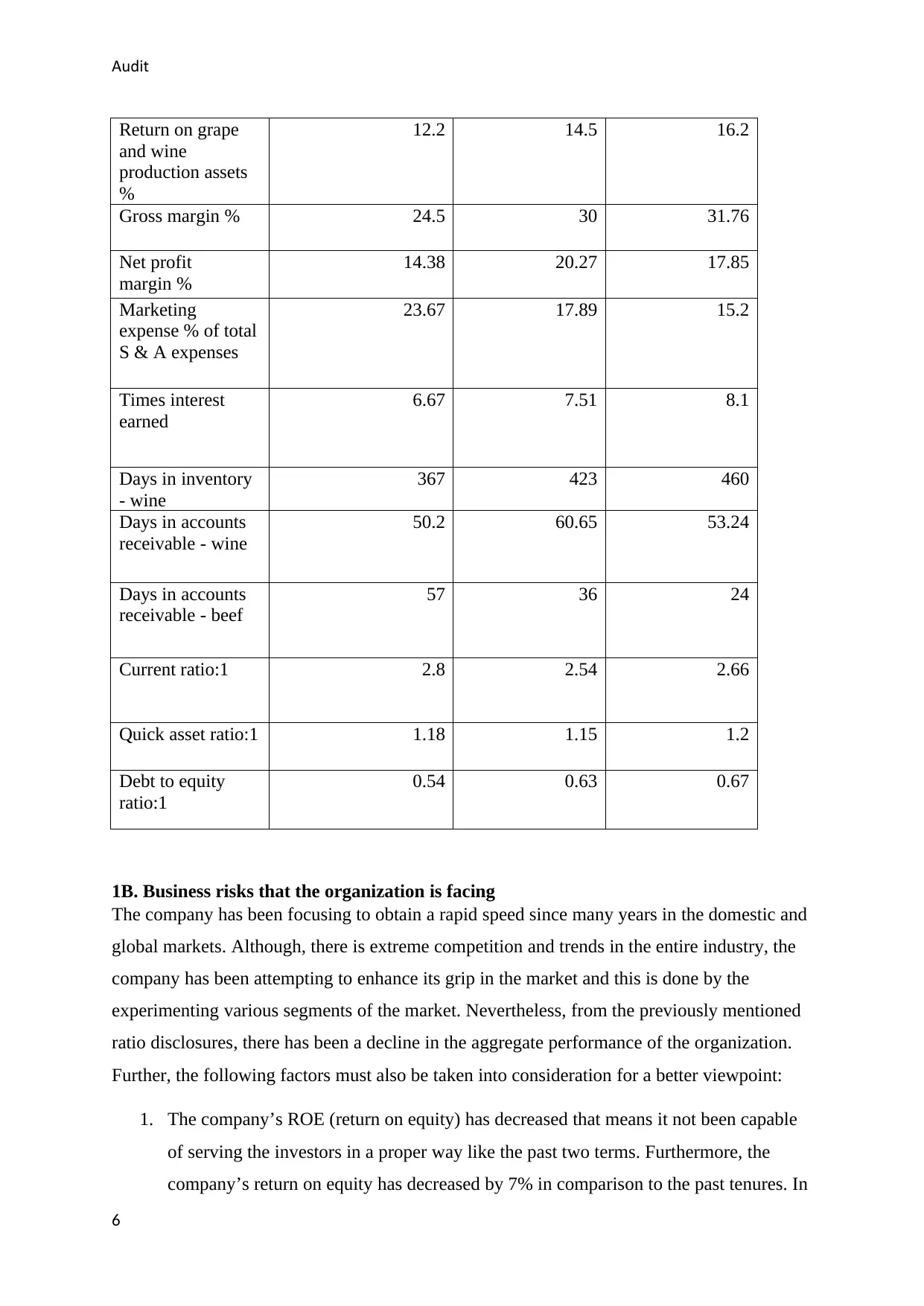

Return on grape

and wine

production assets

%

12.2 14.5 16.2

Gross margin % 24.5 30 31.76

Net profit

margin %

14.38 20.27 17.85

Marketing

expense % of total

S & A expenses

23.67 17.89 15.2

Times interest

earned

6.67 7.51 8.1

Days in inventory

- wine

367 423 460

Days in accounts

receivable - wine

50.2 60.65 53.24

Days in accounts

receivable - beef

57 36 24

Current ratio:1 2.8 2.54 2.66

Quick asset ratio:1 1.18 1.15 1.2

Debt to equity

ratio:1

0.54 0.63 0.67

1B. Business risks that the organization is facing

The company has been focusing to obtain a rapid speed since many years in the domestic and

global markets. Although, there is extreme competition and trends in the entire industry, the

company has been attempting to enhance its grip in the market and this is done by the

experimenting various segments of the market. Nevertheless, from the previously mentioned

ratio disclosures, there has been a decline in the aggregate performance of the organization.

Further, the following factors must also be taken into consideration for a better viewpoint:

1. The company’s ROE (return on equity) has decreased that means it not been capable

of serving the investors in a proper way like the past two terms. Furthermore, the

company’s return on equity has decreased by 7% in comparison to the past tenures. In

6

Return on grape

and wine

production assets

%

12.2 14.5 16.2

Gross margin % 24.5 30 31.76

Net profit

margin %

14.38 20.27 17.85

Marketing

expense % of total

S & A expenses

23.67 17.89 15.2

Times interest

earned

6.67 7.51 8.1

Days in inventory

- wine

367 423 460

Days in accounts

receivable - wine

50.2 60.65 53.24

Days in accounts

receivable - beef

57 36 24

Current ratio:1 2.8 2.54 2.66

Quick asset ratio:1 1.18 1.15 1.2

Debt to equity

ratio:1

0.54 0.63 0.67

1B. Business risks that the organization is facing

The company has been focusing to obtain a rapid speed since many years in the domestic and

global markets. Although, there is extreme competition and trends in the entire industry, the

company has been attempting to enhance its grip in the market and this is done by the

experimenting various segments of the market. Nevertheless, from the previously mentioned

ratio disclosures, there has been a decline in the aggregate performance of the organization.

Further, the following factors must also be taken into consideration for a better viewpoint:

1. The company’s ROE (return on equity) has decreased that means it not been capable

of serving the investors in a proper way like the past two terms. Furthermore, the

company’s return on equity has decreased by 7% in comparison to the past tenures. In

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

relation to this, the business risk is associated to drawing on the part of investors

owing to a lesser return on equity (Hoffelder, 2012).

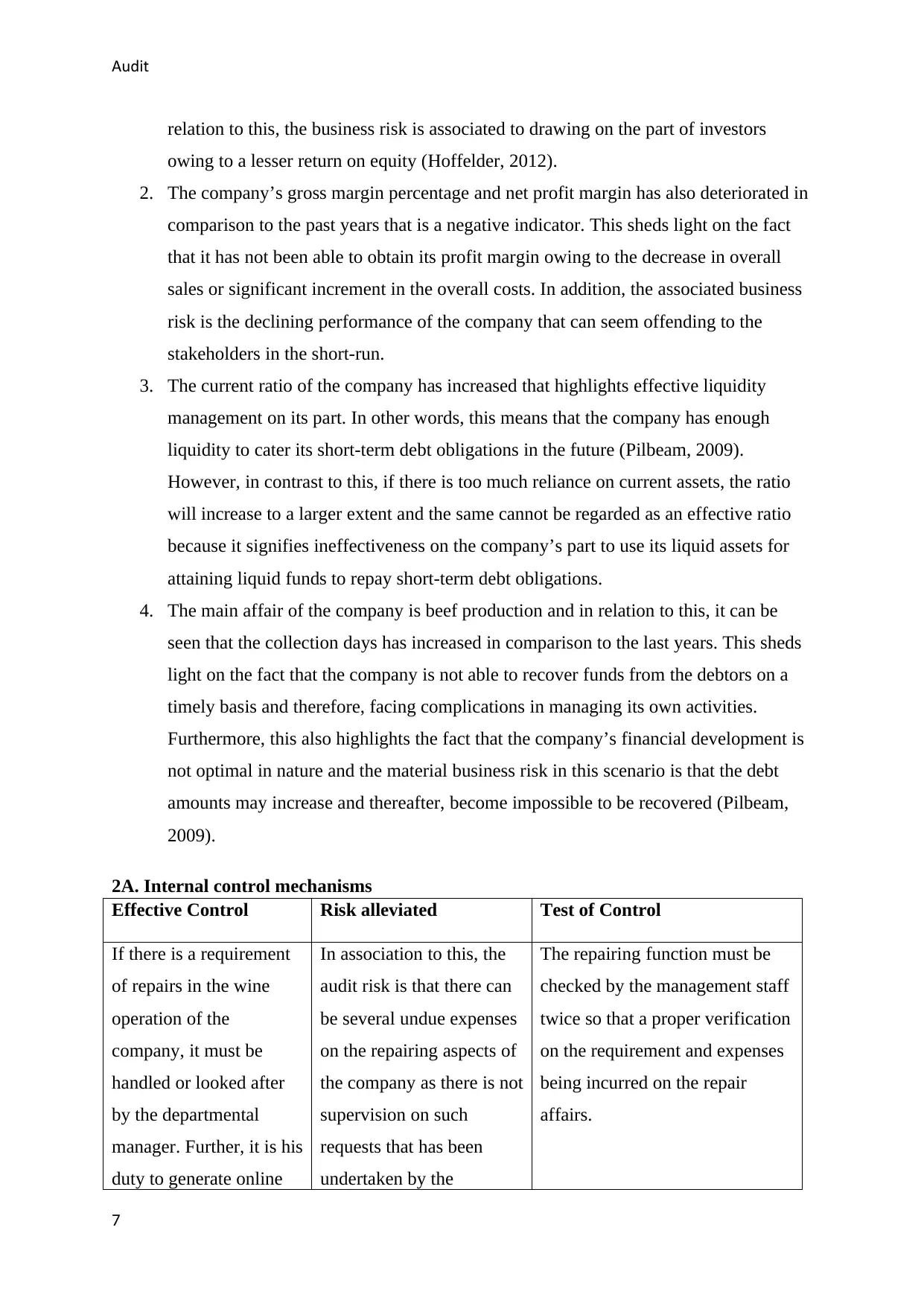

2. The company’s gross margin percentage and net profit margin has also deteriorated in

comparison to the past years that is a negative indicator. This sheds light on the fact

that it has not been able to obtain its profit margin owing to the decrease in overall

sales or significant increment in the overall costs. In addition, the associated business

risk is the declining performance of the company that can seem offending to the

stakeholders in the short-run.

3. The current ratio of the company has increased that highlights effective liquidity

management on its part. In other words, this means that the company has enough

liquidity to cater its short-term debt obligations in the future (Pilbeam, 2009).

However, in contrast to this, if there is too much reliance on current assets, the ratio

will increase to a larger extent and the same cannot be regarded as an effective ratio

because it signifies ineffectiveness on the company’s part to use its liquid assets for

attaining liquid funds to repay short-term debt obligations.

4. The main affair of the company is beef production and in relation to this, it can be

seen that the collection days has increased in comparison to the last years. This sheds

light on the fact that the company is not able to recover funds from the debtors on a

timely basis and therefore, facing complications in managing its own activities.

Furthermore, this also highlights the fact that the company’s financial development is

not optimal in nature and the material business risk in this scenario is that the debt

amounts may increase and thereafter, become impossible to be recovered (Pilbeam,

2009).

2A. Internal control mechanisms

Effective Control Risk alleviated Test of Control

If there is a requirement

of repairs in the wine

operation of the

company, it must be

handled or looked after

by the departmental

manager. Further, it is his

duty to generate online

In association to this, the

audit risk is that there can

be several undue expenses

on the repairing aspects of

the company as there is not

supervision on such

requests that has been

undertaken by the

The repairing function must be

checked by the management staff

twice so that a proper verification

on the requirement and expenses

being incurred on the repair

affairs.

7

relation to this, the business risk is associated to drawing on the part of investors

owing to a lesser return on equity (Hoffelder, 2012).

2. The company’s gross margin percentage and net profit margin has also deteriorated in

comparison to the past years that is a negative indicator. This sheds light on the fact

that it has not been able to obtain its profit margin owing to the decrease in overall

sales or significant increment in the overall costs. In addition, the associated business

risk is the declining performance of the company that can seem offending to the

stakeholders in the short-run.

3. The current ratio of the company has increased that highlights effective liquidity

management on its part. In other words, this means that the company has enough

liquidity to cater its short-term debt obligations in the future (Pilbeam, 2009).

However, in contrast to this, if there is too much reliance on current assets, the ratio

will increase to a larger extent and the same cannot be regarded as an effective ratio

because it signifies ineffectiveness on the company’s part to use its liquid assets for

attaining liquid funds to repay short-term debt obligations.

4. The main affair of the company is beef production and in relation to this, it can be

seen that the collection days has increased in comparison to the last years. This sheds

light on the fact that the company is not able to recover funds from the debtors on a

timely basis and therefore, facing complications in managing its own activities.

Furthermore, this also highlights the fact that the company’s financial development is

not optimal in nature and the material business risk in this scenario is that the debt

amounts may increase and thereafter, become impossible to be recovered (Pilbeam,

2009).

2A. Internal control mechanisms

Effective Control Risk alleviated Test of Control

If there is a requirement

of repairs in the wine

operation of the

company, it must be

handled or looked after

by the departmental

manager. Further, it is his

duty to generate online

In association to this, the

audit risk is that there can

be several undue expenses

on the repairing aspects of

the company as there is not

supervision on such

requests that has been

undertaken by the

The repairing function must be

checked by the management staff

twice so that a proper verification

on the requirement and expenses

being incurred on the repair

affairs.

7

Audit

orders and final payment

procedure will be

automatically eradicated

by the approval on the

part of the management.

departmental manager

(Rezaee & Kedia, 2012).

Furthermore, the

management accountant

and clerk must come into

light when the services are

vanquished and the

provider has also offered

an invoice to the company.

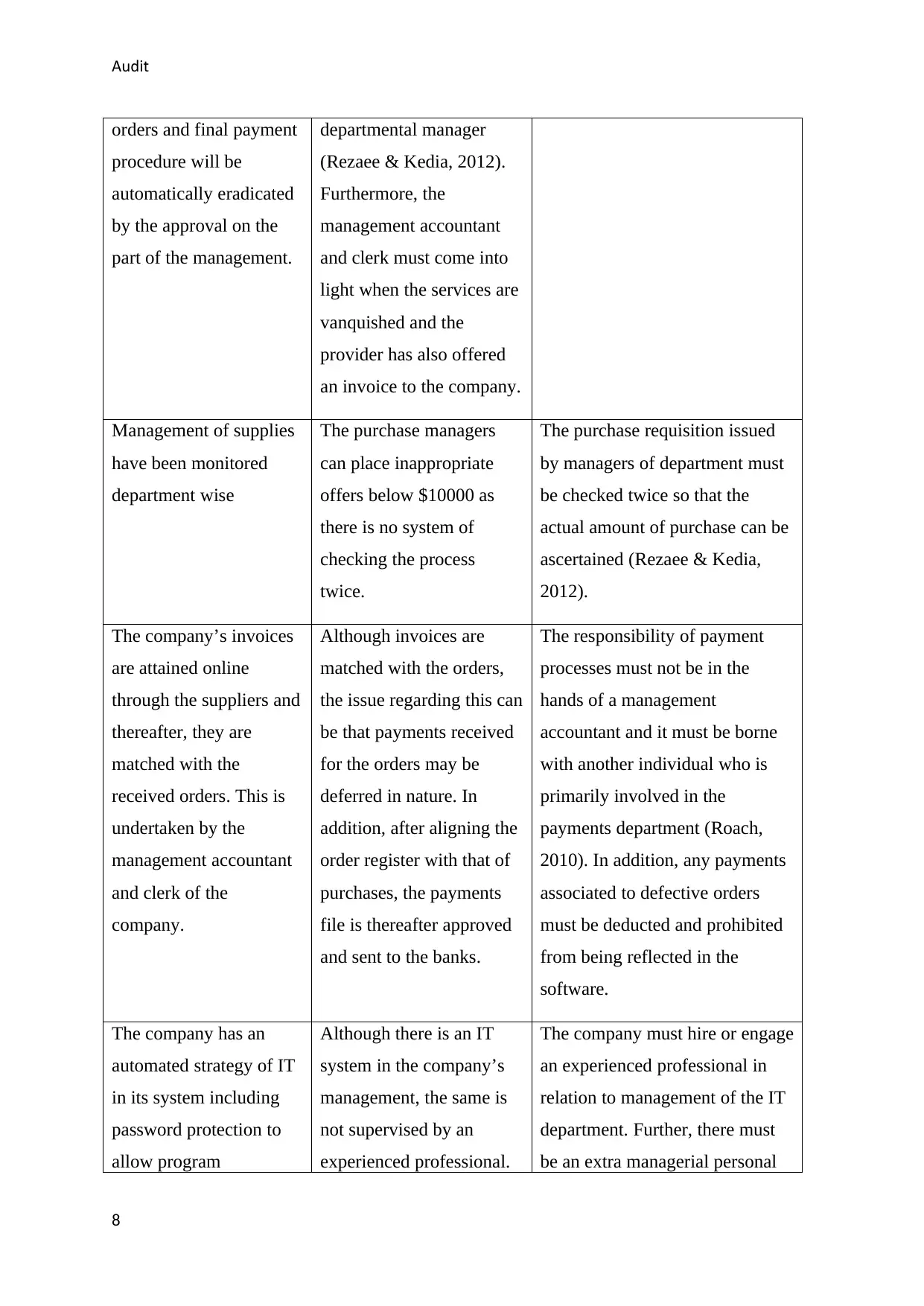

Management of supplies

have been monitored

department wise

The purchase managers

can place inappropriate

offers below $10000 as

there is no system of

checking the process

twice.

The purchase requisition issued

by managers of department must

be checked twice so that the

actual amount of purchase can be

ascertained (Rezaee & Kedia,

2012).

The company’s invoices

are attained online

through the suppliers and

thereafter, they are

matched with the

received orders. This is

undertaken by the

management accountant

and clerk of the

company.

Although invoices are

matched with the orders,

the issue regarding this can

be that payments received

for the orders may be

deferred in nature. In

addition, after aligning the

order register with that of

purchases, the payments

file is thereafter approved

and sent to the banks.

The responsibility of payment

processes must not be in the

hands of a management

accountant and it must be borne

with another individual who is

primarily involved in the

payments department (Roach,

2010). In addition, any payments

associated to defective orders

must be deducted and prohibited

from being reflected in the

software.

The company has an

automated strategy of IT

in its system including

password protection to

allow program

Although there is an IT

system in the company’s

management, the same is

not supervised by an

experienced professional.

The company must hire or engage

an experienced professional in

relation to management of the IT

department. Further, there must

be an extra managerial personal

8

orders and final payment

procedure will be

automatically eradicated

by the approval on the

part of the management.

departmental manager

(Rezaee & Kedia, 2012).

Furthermore, the

management accountant

and clerk must come into

light when the services are

vanquished and the

provider has also offered

an invoice to the company.

Management of supplies

have been monitored

department wise

The purchase managers

can place inappropriate

offers below $10000 as

there is no system of

checking the process

twice.

The purchase requisition issued

by managers of department must

be checked twice so that the

actual amount of purchase can be

ascertained (Rezaee & Kedia,

2012).

The company’s invoices

are attained online

through the suppliers and

thereafter, they are

matched with the

received orders. This is

undertaken by the

management accountant

and clerk of the

company.

Although invoices are

matched with the orders,

the issue regarding this can

be that payments received

for the orders may be

deferred in nature. In

addition, after aligning the

order register with that of

purchases, the payments

file is thereafter approved

and sent to the banks.

The responsibility of payment

processes must not be in the

hands of a management

accountant and it must be borne

with another individual who is

primarily involved in the

payments department (Roach,

2010). In addition, any payments

associated to defective orders

must be deducted and prohibited

from being reflected in the

software.

The company has an

automated strategy of IT

in its system including

password protection to

allow program

Although there is an IT

system in the company’s

management, the same is

not supervised by an

experienced professional.

The company must hire or engage

an experienced professional in

relation to management of the IT

department. Further, there must

be an extra managerial personal

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

accessibility. Furthermore, the

organization has offered

this job to a management

accountant who does not

have proper knowledge

regarding the same.

Therefore, this can result

in detection and generation

of various business risks

for the company.

The company does not

have password protection

for the base of IT that is

also a major threat to its

affairs.

who can advice or counsel the

authority of IT department to

smoothen the process. The reason

is that this can assist in

identification of flaws or errors so

that corrective measures can be

taken rapidly.

The IT database must be

protected with the help of a

stronger password and the details

of the department must also be

checked manually so that no

errors can be found later (Roach,

2010).

The staff has received

bonus based on

fulfilment of goals like

monthly sales, etc. This

can be an appropriate

method to involve the

staff in sales promotion.

There can be a possibility

that such staff is involved

in illegal affairs to address

all major goals and attain

maximum revenues.

There must be an appropriate

check on the staff affairs so that

the sales can be promoted on an

effective basis. In addition, the

same must be monitored whether

the staff is not involved in illegal

activities that can hamper the

goodwill of the company. If the

staff has been creating nuisance

to spoil the company’s reputation,

it is not bound upon the company

to address such matter.

The details of suppliers

have been accumulated

in the file of suppliers

and the placed orders are

also undertaken with the

There is a material

business risk that these

approved suppliers may

change their rates as the

same has not been entered

Every time when a particular

order is being placed, the rates

must be confirmed before placing

the orders, thereby assisting in

safeguarding such issues in the

9

accessibility. Furthermore, the

organization has offered

this job to a management

accountant who does not

have proper knowledge

regarding the same.

Therefore, this can result

in detection and generation

of various business risks

for the company.

The company does not

have password protection

for the base of IT that is

also a major threat to its

affairs.

who can advice or counsel the

authority of IT department to

smoothen the process. The reason

is that this can assist in

identification of flaws or errors so

that corrective measures can be

taken rapidly.

The IT database must be

protected with the help of a

stronger password and the details

of the department must also be

checked manually so that no

errors can be found later (Roach,

2010).

The staff has received

bonus based on

fulfilment of goals like

monthly sales, etc. This

can be an appropriate

method to involve the

staff in sales promotion.

There can be a possibility

that such staff is involved

in illegal affairs to address

all major goals and attain

maximum revenues.

There must be an appropriate

check on the staff affairs so that

the sales can be promoted on an

effective basis. In addition, the

same must be monitored whether

the staff is not involved in illegal

activities that can hamper the

goodwill of the company. If the

staff has been creating nuisance

to spoil the company’s reputation,

it is not bound upon the company

to address such matter.

The details of suppliers

have been accumulated

in the file of suppliers

and the placed orders are

also undertaken with the

There is a material

business risk that these

approved suppliers may

change their rates as the

same has not been entered

Every time when a particular

order is being placed, the rates

must be confirmed before placing

the orders, thereby assisting in

safeguarding such issues in the

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

assistance of an ordering

system. Moreover, the

same is undertaken for

the approved suppliers

and if any unapproved

suppliers are granted any

orders, the same will be

eradicated and sent to the

accounts department.

in the master file of

suppliers. Therefore, this

can result in hampering the

smooth flow of affairs of

the company, thereby

requiring corrective

measures in the future

(Peirson et. al, 2015).

future.

2B. Justification in association with issues in internal control measures

Accounts payable

Weakness Justification

There is no

continuous check of

payment registers

The payment registers must be regularly monitored and the same

must be conducted by the management accountant only (Needles &

Powers, 2013).

There are no proper

reconciliations to the

payments and

accounts payable

section.

The management accountant must depend on the IT system to

generate file of payments and other aspects as well. However, no

ledgers have been prepared in relation to the same.

There is no check by

the higher authorities

when it comes to

payment approval

process.

The management accountant must be liable for approving the same

and thereafter, uploading it to the banks. Moreover, there must be a

system that can assist in addressing all contingencies.

Purchases

Weakness Justification

Separate files are not The clerk matches the order details and records it in the payment

10

assistance of an ordering

system. Moreover, the

same is undertaken for

the approved suppliers

and if any unapproved

suppliers are granted any

orders, the same will be

eradicated and sent to the

accounts department.

in the master file of

suppliers. Therefore, this

can result in hampering the

smooth flow of affairs of

the company, thereby

requiring corrective

measures in the future

(Peirson et. al, 2015).

future.

2B. Justification in association with issues in internal control measures

Accounts payable

Weakness Justification

There is no

continuous check of

payment registers

The payment registers must be regularly monitored and the same

must be conducted by the management accountant only (Needles &

Powers, 2013).

There are no proper

reconciliations to the

payments and

accounts payable

section.

The management accountant must depend on the IT system to

generate file of payments and other aspects as well. However, no

ledgers have been prepared in relation to the same.

There is no check by

the higher authorities

when it comes to

payment approval

process.

The management accountant must be liable for approving the same

and thereafter, uploading it to the banks. Moreover, there must be a

system that can assist in addressing all contingencies.

Purchases

Weakness Justification

Separate files are not The clerk matches the order details and records it in the payment

10

Audit

present for lower

quality goods

register later. There may be several items of low quality but the same

is not considered by the clerk. Besides, only paper vouchering is

done.

There is no check of

present registers.

The purchase orders are often not checked properly with the present

items that can result in extra stocking in the warehouses. Therefore,

variations can arise and the same must be considered for facilitating

decision-making processes (Peirson et. al, 2015).

There is unwanted

reliance on the

company’s approved

suppliers

When suppliers are provided orders based on their reputation, other

material aspects like price changes, changes in terms and conditions,

etc are not evaluated. This issue can be problematic in the decision-

making process.

11

present for lower

quality goods

register later. There may be several items of low quality but the same

is not considered by the clerk. Besides, only paper vouchering is

done.

There is no check of

present registers.

The purchase orders are often not checked properly with the present

items that can result in extra stocking in the warehouses. Therefore,

variations can arise and the same must be considered for facilitating

decision-making processes (Peirson et. al, 2015).

There is unwanted

reliance on the

company’s approved

suppliers

When suppliers are provided orders based on their reputation, other

material aspects like price changes, changes in terms and conditions,

etc are not evaluated. This issue can be problematic in the decision-

making process.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.