Trust Plc: Capital Cost, WACC, and Valuation Techniques Report

VerifiedAdded on 2023/06/11

|14

|3760

|172

Report

AI Summary

This report provides a detailed analysis of Trust Plc's financial management, focusing on the calculation of book value and market value cost of capital for both the current and revised capital structures. It evaluates the impact of introducing gearing on the overall cost of capital and discusses the relationship between WACC and IRR. Furthermore, the report examines different valuation techniques used by Kings Plc, including the dividend growth model, price earnings ratio method, and discounted cash flow method. It also addresses the problems associated with each technique and offers recommendations to the management regarding the most viable model for their specific needs. The analysis incorporates formulas and calculations to support the findings and provides insights into the financial decision-making processes within the companies.

MANGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................2

MAIN BODY...................................................................................................................................2

Question No 1:.................................................................................................................................2

A) Calculation of Book value and market value cost of capital for Trust Plc:......................2

B) Recalculation of cost of capital of the company and making comments to projection of the

finance director:......................................................................................................................5

C) Critical discussion on whether by introduction of gearing the overall cost of capital has

been reduced to an acceptable level:......................................................................................6

D) Evaluation of relationship between WACC and IRR with respect to the investment.

Relationship between WACC and IRR:.................................................................................7

Question no 3:..................................................................................................................................8

A) Price earnings ratio model for valuation:..........................................................................8

B) Discounted cash flow method:..........................................................................................9

C)Dividend valuation method:...............................................................................................9

D) Problems associated with usage of the above techniques along with recommendation that

which technique is viable along with justification to board of Kings Plc:...........................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

1

INTRODUCTION...........................................................................................................................2

MAIN BODY...................................................................................................................................2

Question No 1:.................................................................................................................................2

A) Calculation of Book value and market value cost of capital for Trust Plc:......................2

B) Recalculation of cost of capital of the company and making comments to projection of the

finance director:......................................................................................................................5

C) Critical discussion on whether by introduction of gearing the overall cost of capital has

been reduced to an acceptable level:......................................................................................6

D) Evaluation of relationship between WACC and IRR with respect to the investment.

Relationship between WACC and IRR:.................................................................................7

Question no 3:..................................................................................................................................8

A) Price earnings ratio model for valuation:..........................................................................8

B) Discounted cash flow method:..........................................................................................9

C)Dividend valuation method:...............................................................................................9

D) Problems associated with usage of the above techniques along with recommendation that

which technique is viable along with justification to board of Kings Plc:...........................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

1

INTRODUCTION

Financial management is a technique used in various organisation that help the financial

activities carried during the financial year. Financial management provides a systematic

approach to carry the transaction in such a way that effectiveness and efficiency will get

enhanced. It is combined part of various function such as preparation, classification, guiding and

monitoring the financial transaction takes place with the corporate. This report covers different

set of question which comprises of financial management question. Out of the three question two

question has been addressed in this report which are related to calculation of book value and

market value debts for the current and revised capital structure of the entity. The another set of

question is related to different valuation techniques that has been used by Kings plc to evaluate

the valuation of the entity. Such models which are used herein are Dividend growth model, Price

earnings ratio method, discounted cash flow method. At the end of this report the suggestion

have been given to the management that which models is best suited for the amongst the various

model they have applied.

MAIN BODY

Question No 1:

A) Calculation of Book value and market value cost of capital for Trust Plc:

It shows that the amount of money company invests in some assets in order to get return by using

of that particular machinery is called as cost of capital. For example: If a person invests some

money for installing a new machinery in their business for achieving the target goals in the

organization then the cost included in the machinery is cost of capital and against this company

wants some returns to justify its cost.

WACC represents the average cost of capital for the company which company pay to his

shareholders or bondholders. Basically in weighted average cost of capital if company needs

funds to invest in their business for its expansion then company issue common stock or bonds for

the peoples so, they buy them and invest money in the company and against this firm provide

some expected returns to their investors. For Example: if a company needs funds then they issue

2

Financial management is a technique used in various organisation that help the financial

activities carried during the financial year. Financial management provides a systematic

approach to carry the transaction in such a way that effectiveness and efficiency will get

enhanced. It is combined part of various function such as preparation, classification, guiding and

monitoring the financial transaction takes place with the corporate. This report covers different

set of question which comprises of financial management question. Out of the three question two

question has been addressed in this report which are related to calculation of book value and

market value debts for the current and revised capital structure of the entity. The another set of

question is related to different valuation techniques that has been used by Kings plc to evaluate

the valuation of the entity. Such models which are used herein are Dividend growth model, Price

earnings ratio method, discounted cash flow method. At the end of this report the suggestion

have been given to the management that which models is best suited for the amongst the various

model they have applied.

MAIN BODY

Question No 1:

A) Calculation of Book value and market value cost of capital for Trust Plc:

It shows that the amount of money company invests in some assets in order to get return by using

of that particular machinery is called as cost of capital. For example: If a person invests some

money for installing a new machinery in their business for achieving the target goals in the

organization then the cost included in the machinery is cost of capital and against this company

wants some returns to justify its cost.

WACC represents the average cost of capital for the company which company pay to his

shareholders or bondholders. Basically in weighted average cost of capital if company needs

funds to invest in their business for its expansion then company issue common stock or bonds for

the peoples so, they buy them and invest money in the company and against this firm provide

some expected returns to their investors. For Example: if a company needs funds then they issue

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

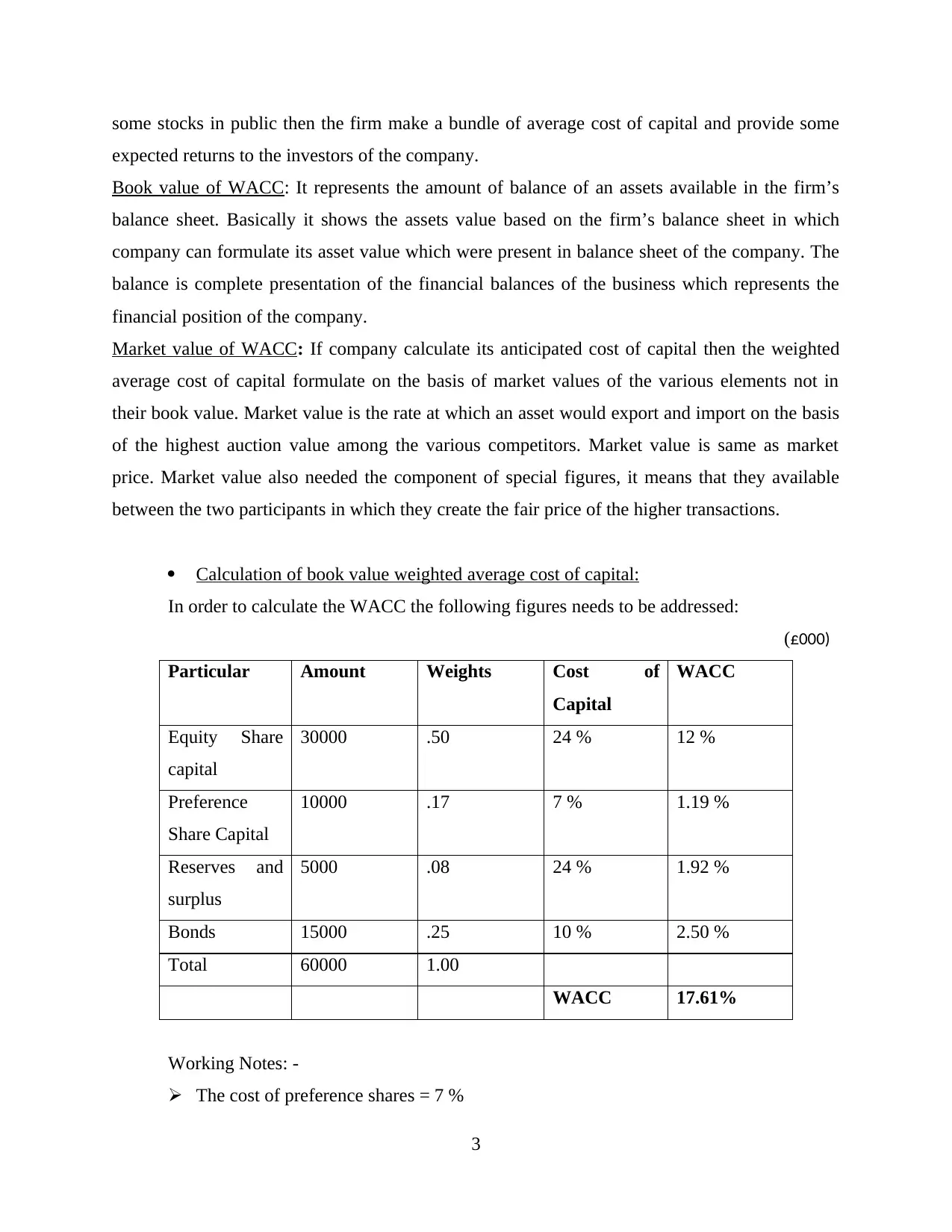

some stocks in public then the firm make a bundle of average cost of capital and provide some

expected returns to the investors of the company.

Book value of WACC: It represents the amount of balance of an assets available in the firm’s

balance sheet. Basically it shows the assets value based on the firm’s balance sheet in which

company can formulate its asset value which were present in balance sheet of the company. The

balance is complete presentation of the financial balances of the business which represents the

financial position of the company.

Market value of WACC: If company calculate its anticipated cost of capital then the weighted

average cost of capital formulate on the basis of market values of the various elements not in

their book value. Market value is the rate at which an asset would export and import on the basis

of the highest auction value among the various competitors. Market value is same as market

price. Market value also needed the component of special figures, it means that they available

between the two participants in which they create the fair price of the higher transactions.

Calculation of book value weighted average cost of capital:

In order to calculate the WACC the following figures needs to be addressed:

(£000)

Particular Amount Weights Cost of

Capital

WACC

Equity Share

capital

30000 .50 24 % 12 %

Preference

Share Capital

10000 .17 7 % 1.19 %

Reserves and

surplus

5000 .08 24 % 1.92 %

Bonds 15000 .25 10 % 2.50 %

Total 60000 1.00

WACC 17.61%

Working Notes: -

The cost of preference shares = 7 %

3

expected returns to the investors of the company.

Book value of WACC: It represents the amount of balance of an assets available in the firm’s

balance sheet. Basically it shows the assets value based on the firm’s balance sheet in which

company can formulate its asset value which were present in balance sheet of the company. The

balance is complete presentation of the financial balances of the business which represents the

financial position of the company.

Market value of WACC: If company calculate its anticipated cost of capital then the weighted

average cost of capital formulate on the basis of market values of the various elements not in

their book value. Market value is the rate at which an asset would export and import on the basis

of the highest auction value among the various competitors. Market value is same as market

price. Market value also needed the component of special figures, it means that they available

between the two participants in which they create the fair price of the higher transactions.

Calculation of book value weighted average cost of capital:

In order to calculate the WACC the following figures needs to be addressed:

(£000)

Particular Amount Weights Cost of

Capital

WACC

Equity Share

capital

30000 .50 24 % 12 %

Preference

Share Capital

10000 .17 7 % 1.19 %

Reserves and

surplus

5000 .08 24 % 1.92 %

Bonds 15000 .25 10 % 2.50 %

Total 60000 1.00

WACC 17.61%

Working Notes: -

The cost of preference shares = 7 %

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

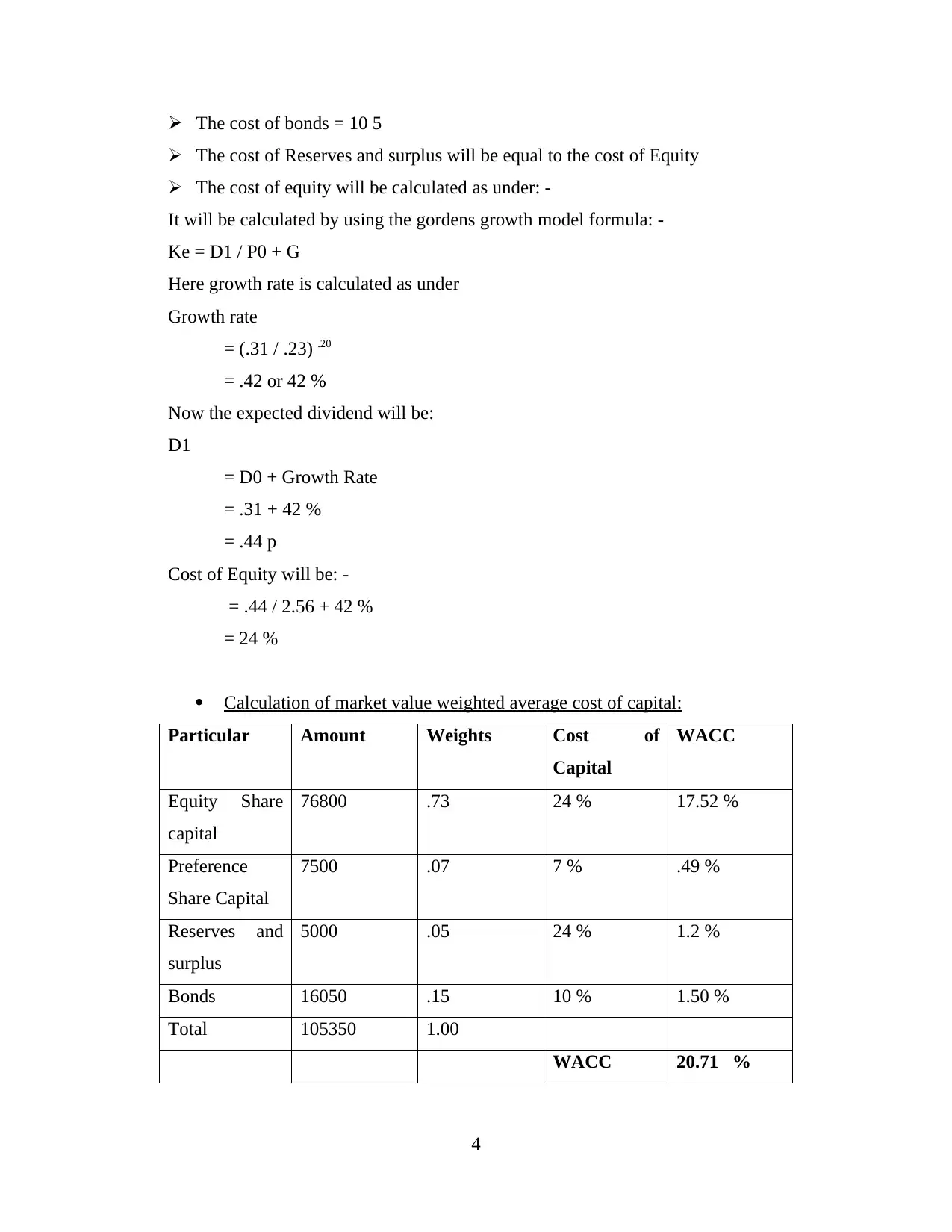

The cost of bonds = 10 5

The cost of Reserves and surplus will be equal to the cost of Equity

The cost of equity will be calculated as under: -

It will be calculated by using the gordens growth model formula: -

Ke = D1 / P0 + G

Here growth rate is calculated as under

Growth rate

= (.31 / .23) .20

= .42 or 42 %

Now the expected dividend will be:

D1

= D0 + Growth Rate

= .31 + 42 %

= .44 p

Cost of Equity will be: -

= .44 / 2.56 + 42 %

= 24 %

Calculation of market value weighted average cost of capital:

Particular Amount Weights Cost of

Capital

WACC

Equity Share

capital

76800 .73 24 % 17.52 %

Preference

Share Capital

7500 .07 7 % .49 %

Reserves and

surplus

5000 .05 24 % 1.2 %

Bonds 16050 .15 10 % 1.50 %

Total 105350 1.00

WACC 20.71 %

4

The cost of Reserves and surplus will be equal to the cost of Equity

The cost of equity will be calculated as under: -

It will be calculated by using the gordens growth model formula: -

Ke = D1 / P0 + G

Here growth rate is calculated as under

Growth rate

= (.31 / .23) .20

= .42 or 42 %

Now the expected dividend will be:

D1

= D0 + Growth Rate

= .31 + 42 %

= .44 p

Cost of Equity will be: -

= .44 / 2.56 + 42 %

= 24 %

Calculation of market value weighted average cost of capital:

Particular Amount Weights Cost of

Capital

WACC

Equity Share

capital

76800 .73 24 % 17.52 %

Preference

Share Capital

7500 .07 7 % .49 %

Reserves and

surplus

5000 .05 24 % 1.2 %

Bonds 16050 .15 10 % 1.50 %

Total 105350 1.00

WACC 20.71 %

4

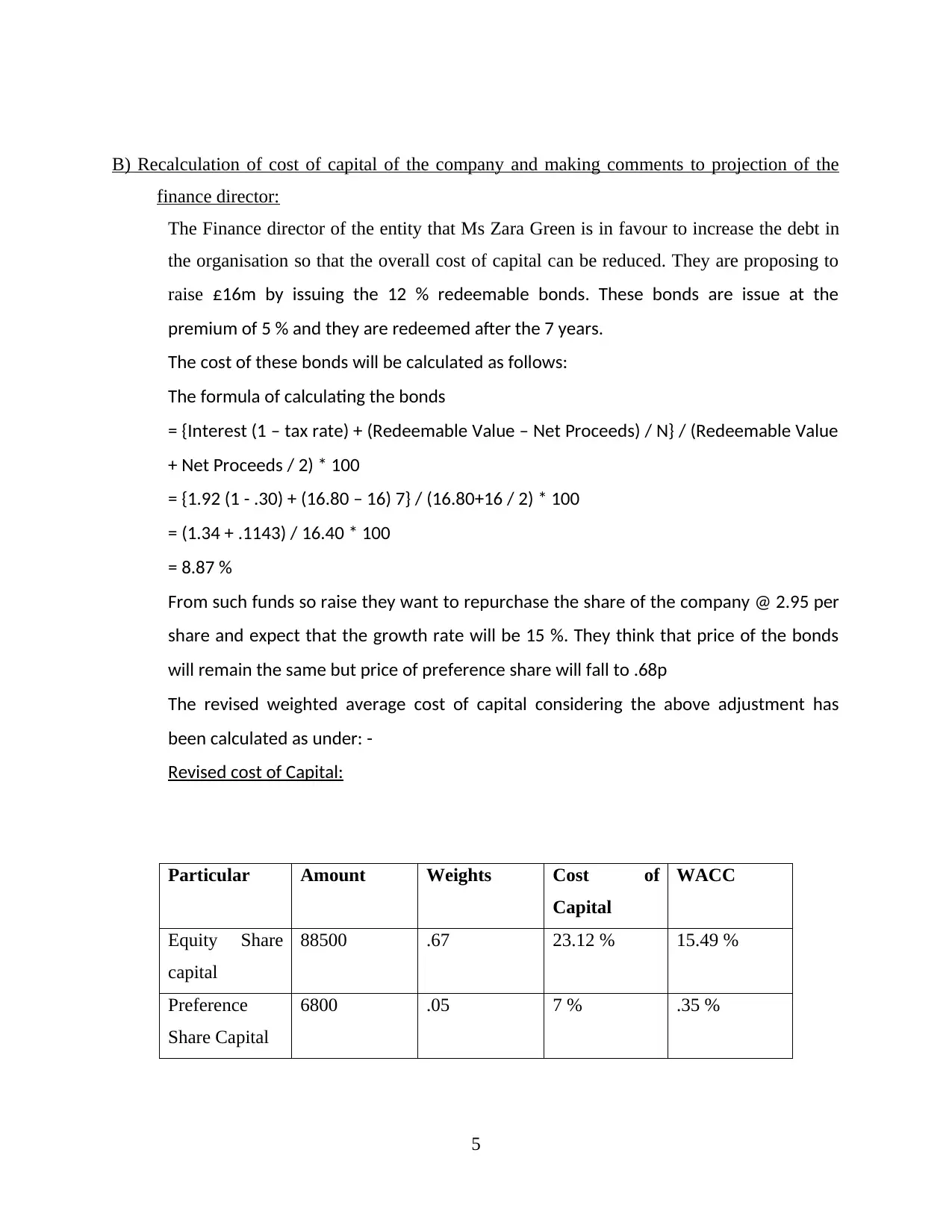

B) Recalculation of cost of capital of the company and making comments to projection of the

finance director:

The Finance director of the entity that Ms Zara Green is in favour to increase the debt in

the organisation so that the overall cost of capital can be reduced. They are proposing to

raise £16m by issuing the 12 % redeemable bonds. These bonds are issue at the

premium of 5 % and they are redeemed after the 7 years.

The cost of these bonds will be calculated as follows:

The formula of calculating the bonds

= {Interest (1 – tax rate) + (Redeemable Value – Net Proceeds) / N} / (Redeemable Value

+ Net Proceeds / 2) * 100

= {1.92 (1 - .30) + (16.80 – 16) 7} / (16.80+16 / 2) * 100

= (1.34 + .1143) / 16.40 * 100

= 8.87 %

From such funds so raise they want to repurchase the share of the company @ 2.95 per

share and expect that the growth rate will be 15 %. They think that price of the bonds

will remain the same but price of preference share will fall to .68p

The revised weighted average cost of capital considering the above adjustment has

been calculated as under: -

Revised cost of Capital:

Particular Amount Weights Cost of

Capital

WACC

Equity Share

capital

88500 .67 23.12 % 15.49 %

Preference

Share Capital

6800 .05 7 % .35 %

5

finance director:

The Finance director of the entity that Ms Zara Green is in favour to increase the debt in

the organisation so that the overall cost of capital can be reduced. They are proposing to

raise £16m by issuing the 12 % redeemable bonds. These bonds are issue at the

premium of 5 % and they are redeemed after the 7 years.

The cost of these bonds will be calculated as follows:

The formula of calculating the bonds

= {Interest (1 – tax rate) + (Redeemable Value – Net Proceeds) / N} / (Redeemable Value

+ Net Proceeds / 2) * 100

= {1.92 (1 - .30) + (16.80 – 16) 7} / (16.80+16 / 2) * 100

= (1.34 + .1143) / 16.40 * 100

= 8.87 %

From such funds so raise they want to repurchase the share of the company @ 2.95 per

share and expect that the growth rate will be 15 %. They think that price of the bonds

will remain the same but price of preference share will fall to .68p

The revised weighted average cost of capital considering the above adjustment has

been calculated as under: -

Revised cost of Capital:

Particular Amount Weights Cost of

Capital

WACC

Equity Share

capital

88500 .67 23.12 % 15.49 %

Preference

Share Capital

6800 .05 7 % .35 %

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reserves and

surplus

5000 .04 23.12 % .92 %

Bonds

Irredeemable

15000 .11 10 % 1.10 %

Bonds

Redeemable

16000 .13 8.87 % 1.15 %

Total 131300 1.00 WACC 19.01 %

Working Notes: -

The cost of equity will be calculated as under: -

It will be calculated by using the gordens growth model formula: -

Ke = D1 / P0 + G

Revised Growth rate

= 42 % + 15 %

= 48.30 %

Now the expected dividend will be:

D1

= D0 + Growth Rate

= .31 + 48.30 %

= .46 p

Cost of Equity will be: -

= .46 / 2.95 + 48.30 %

= 23. 12 %

The cost of preference share remains the same that is 7 %

C) Critical discussion on whether by introduction of gearing the overall cost of capital has been

reduced to an acceptable level:

When an organisation introduced more debt in their capital structure then the overall cost

of capital of the organisation has been reduced by 1.70 % and their revised weighted

average cost of capital will be 19.01 %. When the fixed rate cost of capital is higher in

6

surplus

5000 .04 23.12 % .92 %

Bonds

Irredeemable

15000 .11 10 % 1.10 %

Bonds

Redeemable

16000 .13 8.87 % 1.15 %

Total 131300 1.00 WACC 19.01 %

Working Notes: -

The cost of equity will be calculated as under: -

It will be calculated by using the gordens growth model formula: -

Ke = D1 / P0 + G

Revised Growth rate

= 42 % + 15 %

= 48.30 %

Now the expected dividend will be:

D1

= D0 + Growth Rate

= .31 + 48.30 %

= .46 p

Cost of Equity will be: -

= .46 / 2.95 + 48.30 %

= 23. 12 %

The cost of preference share remains the same that is 7 %

C) Critical discussion on whether by introduction of gearing the overall cost of capital has been

reduced to an acceptable level:

When an organisation introduced more debt in their capital structure then the overall cost

of capital of the organisation has been reduced by 1.70 % and their revised weighted

average cost of capital will be 19.01 %. When the fixed rate cost of capital is higher in

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the organisation then the entity has to pay the fixed rate of interest and their expectation

is also restricted to interest they want to earn. Whereas when an entity is geared by more

equity in their capital structure then it that case the entity has to pay the higher amount to

fulfil the need of shareholder’s expectation as they taking the risk when they invest in a

particular organisation. In the given case when Faith Plc change their capital structure by

adding on more redeemable debt in their capital structure the overall cost of them has

been curtailed down because the risk that is taken by equity has been shifted to

debtholders.

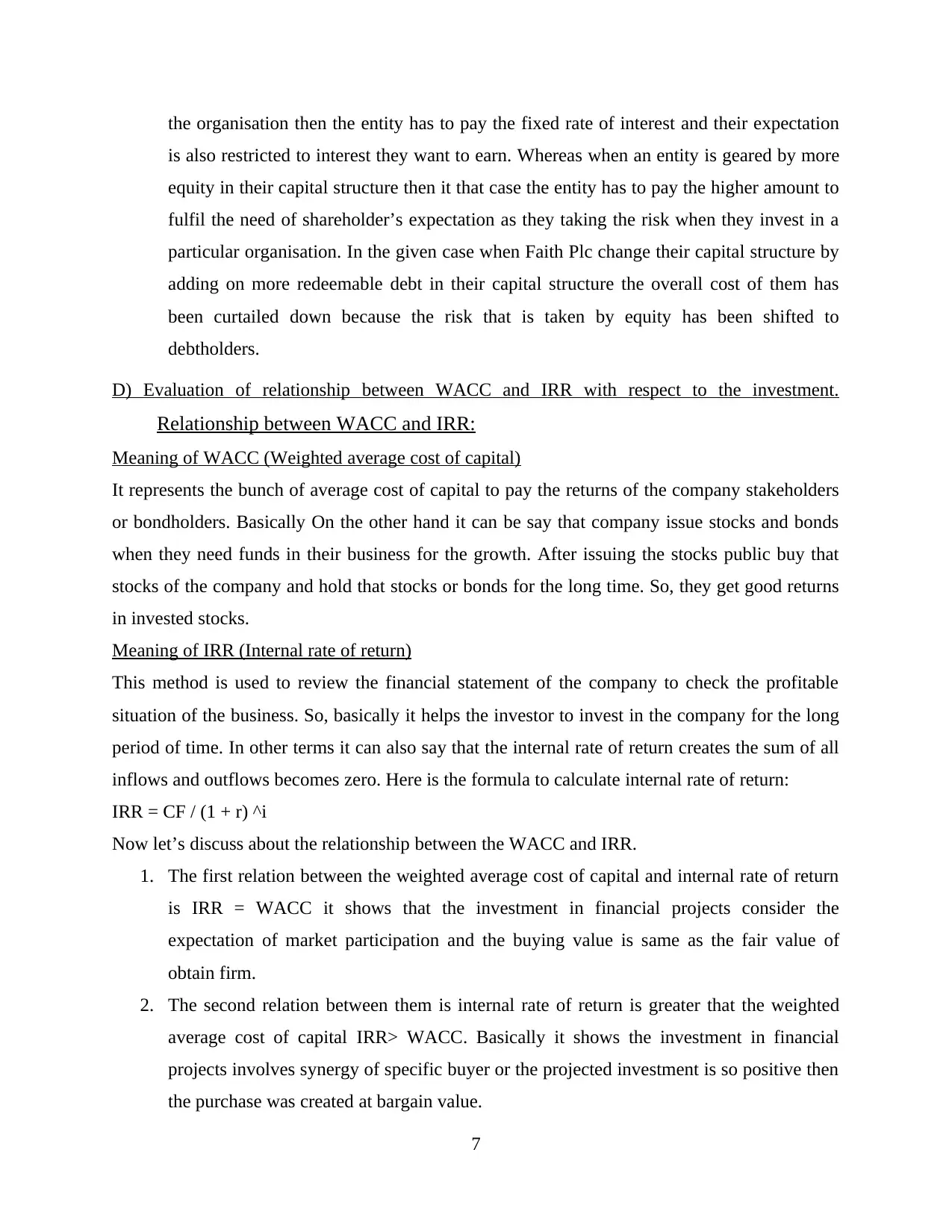

D) Evaluation of relationship between WACC and IRR with respect to the investment.

Relationship between WACC and IRR:

Meaning of WACC (Weighted average cost of capital)

It represents the bunch of average cost of capital to pay the returns of the company stakeholders

or bondholders. Basically On the other hand it can be say that company issue stocks and bonds

when they need funds in their business for the growth. After issuing the stocks public buy that

stocks of the company and hold that stocks or bonds for the long time. So, they get good returns

in invested stocks.

Meaning of IRR (Internal rate of return)

This method is used to review the financial statement of the company to check the profitable

situation of the business. So, basically it helps the investor to invest in the company for the long

period of time. In other terms it can also say that the internal rate of return creates the sum of all

inflows and outflows becomes zero. Here is the formula to calculate internal rate of return:

IRR = CF / (1 + r) ^i

Now let’s discuss about the relationship between the WACC and IRR.

1. The first relation between the weighted average cost of capital and internal rate of return

is IRR = WACC it shows that the investment in financial projects consider the

expectation of market participation and the buying value is same as the fair value of

obtain firm.

2. The second relation between them is internal rate of return is greater that the weighted

average cost of capital IRR> WACC. Basically it shows the investment in financial

projects involves synergy of specific buyer or the projected investment is so positive then

the purchase was created at bargain value.

7

is also restricted to interest they want to earn. Whereas when an entity is geared by more

equity in their capital structure then it that case the entity has to pay the higher amount to

fulfil the need of shareholder’s expectation as they taking the risk when they invest in a

particular organisation. In the given case when Faith Plc change their capital structure by

adding on more redeemable debt in their capital structure the overall cost of them has

been curtailed down because the risk that is taken by equity has been shifted to

debtholders.

D) Evaluation of relationship between WACC and IRR with respect to the investment.

Relationship between WACC and IRR:

Meaning of WACC (Weighted average cost of capital)

It represents the bunch of average cost of capital to pay the returns of the company stakeholders

or bondholders. Basically On the other hand it can be say that company issue stocks and bonds

when they need funds in their business for the growth. After issuing the stocks public buy that

stocks of the company and hold that stocks or bonds for the long time. So, they get good returns

in invested stocks.

Meaning of IRR (Internal rate of return)

This method is used to review the financial statement of the company to check the profitable

situation of the business. So, basically it helps the investor to invest in the company for the long

period of time. In other terms it can also say that the internal rate of return creates the sum of all

inflows and outflows becomes zero. Here is the formula to calculate internal rate of return:

IRR = CF / (1 + r) ^i

Now let’s discuss about the relationship between the WACC and IRR.

1. The first relation between the weighted average cost of capital and internal rate of return

is IRR = WACC it shows that the investment in financial projects consider the

expectation of market participation and the buying value is same as the fair value of

obtain firm.

2. The second relation between them is internal rate of return is greater that the weighted

average cost of capital IRR> WACC. Basically it shows the investment in financial

projects involves synergy of specific buyer or the projected investment is so positive then

the purchase was created at bargain value.

7

3. The third relation between them is if weighted average cost of capital is more than the

internal rate of return IRR<WACC then it shows that the investment in financial projects

is out from all the expectations of market competitors synergy or the projected

investment becomes too protective then the buyer more pays for the targets.

This relationship between the weighted average cost of capital and internal rate of return

shows about which method is more convenient to use so, it is concluded that the weighted

average cost of capital is best to use as compare to the internal rate of return because in

Weighted average cost of capital company provide returns according to the investment of

the investor and its easies to calculate but in internal rate of return it forecast the

profitability of the business for the potential investors.

Question no 3:

A) Price earnings ratio model for valuation:

This ratio is one of the most appropriate method to calculate the security of the company

through the formulation of price earnings ratio. It represents the firm actual share price

how much relative to its earning per share (EPS). This ratio also helps to analyse the

expansion capacity of the business. If P/E ratio is high, then its indicate the positive

future income of the firm and the investors are able to pay high but it also shows the

stocks are exceeded.

Price earnings ratio model used the following formula to conduct the valuation

= MPS / EPS

= 4.25 / .31

= 13.71.

Here the value of the Dragon plc has been arrived on the basis of competitor data that is

Kings Plc by using the below formula

= Earnings per share of competitors * PE ratio of the company

= 40.40 / 210 * 13.71

= .19 * 13.71

2.605

8

internal rate of return IRR<WACC then it shows that the investment in financial projects

is out from all the expectations of market competitors synergy or the projected

investment becomes too protective then the buyer more pays for the targets.

This relationship between the weighted average cost of capital and internal rate of return

shows about which method is more convenient to use so, it is concluded that the weighted

average cost of capital is best to use as compare to the internal rate of return because in

Weighted average cost of capital company provide returns according to the investment of

the investor and its easies to calculate but in internal rate of return it forecast the

profitability of the business for the potential investors.

Question no 3:

A) Price earnings ratio model for valuation:

This ratio is one of the most appropriate method to calculate the security of the company

through the formulation of price earnings ratio. It represents the firm actual share price

how much relative to its earning per share (EPS). This ratio also helps to analyse the

expansion capacity of the business. If P/E ratio is high, then its indicate the positive

future income of the firm and the investors are able to pay high but it also shows the

stocks are exceeded.

Price earnings ratio model used the following formula to conduct the valuation

= MPS / EPS

= 4.25 / .31

= 13.71.

Here the value of the Dragon plc has been arrived on the basis of competitor data that is

Kings Plc by using the below formula

= Earnings per share of competitors * PE ratio of the company

= 40.40 / 210 * 13.71

= .19 * 13.71

2.605

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

B) Discounted cash flow method:

This method shows to identify the rate of investment today and on the basis of project its

need to find out how much money it will create in future. Basically discounted cash flow

method is depending upon the time value of money and helps to formulate the how much

value a company invest in some asset and at which time it will create a future cash flows

of the company. For Example: If a company invest $1000 in some asset then what will

the value of $1000 after 1 year. Here is one formula to measure Discounted cash flow:

DCF = Cash flow / (1+r) ^t

This model used the following formula to calculate the values

= After tax annual profits / Cost of Capital

= (5.36 / 11 %)

= 48.73

C)Dividend valuation method:

This method is helps to forecast the value of company's stocks and bonds this is also

known quantitative method. It’s truly depends on the expectation that the current value of

stock is sum total of the firm’s future dividends. In this method there are three types of

dividend discounted model:

Constant rate of growth model: This method is one of the most commonly used

method. It is introducing by American economist Myron j. Gordon it helps to find

the intrinsic value of the stock. Here is the formula to calculate:

V0 = D1 / r-g

Dividend one- year discounted model: This model is less capable as compare to

the Gordon Growth model. It helps to identify the intrinsic value of the stocks

when he/she sell stock in a period of one year. Formula to calculate one period

model:

V0 = (D1 / 1+ r) + (P1 / 1+r)

Dividend numerous discounted model: This method is more capable as compare

to one- period discounted model. It helps to hold the stock for so many years. But

the main factor for this model is to predict dividend payment for every year is

required. Formula to calculate this model:

V0 = (D1 / 1+ r) ^1+ (D2 / 1+r) ^2+....Den / (1+r) ^n

9

This method shows to identify the rate of investment today and on the basis of project its

need to find out how much money it will create in future. Basically discounted cash flow

method is depending upon the time value of money and helps to formulate the how much

value a company invest in some asset and at which time it will create a future cash flows

of the company. For Example: If a company invest $1000 in some asset then what will

the value of $1000 after 1 year. Here is one formula to measure Discounted cash flow:

DCF = Cash flow / (1+r) ^t

This model used the following formula to calculate the values

= After tax annual profits / Cost of Capital

= (5.36 / 11 %)

= 48.73

C)Dividend valuation method:

This method is helps to forecast the value of company's stocks and bonds this is also

known quantitative method. It’s truly depends on the expectation that the current value of

stock is sum total of the firm’s future dividends. In this method there are three types of

dividend discounted model:

Constant rate of growth model: This method is one of the most commonly used

method. It is introducing by American economist Myron j. Gordon it helps to find

the intrinsic value of the stock. Here is the formula to calculate:

V0 = D1 / r-g

Dividend one- year discounted model: This model is less capable as compare to

the Gordon Growth model. It helps to identify the intrinsic value of the stocks

when he/she sell stock in a period of one year. Formula to calculate one period

model:

V0 = (D1 / 1+ r) + (P1 / 1+r)

Dividend numerous discounted model: This method is more capable as compare

to one- period discounted model. It helps to hold the stock for so many years. But

the main factor for this model is to predict dividend payment for every year is

required. Formula to calculate this model:

V0 = (D1 / 1+ r) ^1+ (D2 / 1+r) ^2+....Den / (1+r) ^n

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In this model the formula which has been used will be

P0 = D1 / Ke – G

Here D1 is expected dividend per share, ke is cost of equity capital, and G stands for

growth rate

Valuation of Dragon Plc has been made as under:

= No of shares * MPS

= 210 * 3.33

= Pound 699.33

Working Notes: -

Cost of Equity has been calculated using the Capital Asset pricing model whose

formula is:

Ke = Rf + B (Rm – Rf)

= 5.50 + 1.05 (11 – 5.50)

= 5.55 + .58

= 6.13 %

The Expected dividend per share has been calculated as under: -

= (Last Dividend Paid + Growth Rate)

= 12 +2.50 %

= 12.30p

D) Problems associated with usage of the above techniques along with recommendation that

which technique is viable along with justification to board of Kings Plc:

Problems associated with the models has been listed below: -

Price earnings ratio method: The main problem associated with this method is that it does

not account for the growth rate. Further many entities have debt related issues that are

high in number but this model considers only the equity share price of the enterprise and

not the debt hold by the organisation. Further the results derived from this model is

sometimes misleading as the entity report positive earning but in actual they have

negative cash flows.

10

P0 = D1 / Ke – G

Here D1 is expected dividend per share, ke is cost of equity capital, and G stands for

growth rate

Valuation of Dragon Plc has been made as under:

= No of shares * MPS

= 210 * 3.33

= Pound 699.33

Working Notes: -

Cost of Equity has been calculated using the Capital Asset pricing model whose

formula is:

Ke = Rf + B (Rm – Rf)

= 5.50 + 1.05 (11 – 5.50)

= 5.55 + .58

= 6.13 %

The Expected dividend per share has been calculated as under: -

= (Last Dividend Paid + Growth Rate)

= 12 +2.50 %

= 12.30p

D) Problems associated with usage of the above techniques along with recommendation that

which technique is viable along with justification to board of Kings Plc:

Problems associated with the models has been listed below: -

Price earnings ratio method: The main problem associated with this method is that it does

not account for the growth rate. Further many entities have debt related issues that are

high in number but this model considers only the equity share price of the enterprise and

not the debt hold by the organisation. Further the results derived from this model is

sometimes misleading as the entity report positive earning but in actual they have

negative cash flows.

10

Discounted cash flow method: The major drawback of this method is that it is easily

prone to errors, having wrong assumptions, overconfidence towards the net worth of the

organisation. The major drawback with this system is that it does not consider time value

of money and not only this it also ignores the depreciation. In order to apply this method

on a particular investment appraisal a lot of assumption has to be taken with which makes

the result not fruitful. Further this method is over complex and very sensitive to changes

in assumptions depending the case under consideration.

Dividend valuation method: This method is very simple which does not provide accurate

justification to the results obtained thereunder. Further this method works only on those

shares which are regularly paying the dividend to its shareholders. There are some other

non-monetary factors too that affect the valuation of the entity such as customer

retention, loyalty towards brand etc. This model only values payment in the form of

dividend as the return on investment. This model is also very sensitive to the quality of

information involved because if the information is not correct then valuation will differ

completely.

Recommendation on which techniques must be followed by Kings Plc:

It is recommended to kings Plc is that to use dividend valuation method as their capital structure

cover both equity and debt and they are readily paying the dividend to its holders of security.

Therefore, from the above method they must consider dividend model to make valuation of their

company.

CONCLUSION

The above report consists of two different set of question relating to financial management that

has been addressed accordingly. The first question deals with capital structure of the organisation

which consist of equity, debt and reserves and surplus. Them after the weighted average cost of

capital has been calculated using book value and market value debts. In the next question the

valuation of Kings plc has been made using different models such as price earnings ratio method,

discounted cash flow method, dividend valuation method and recommendation has been made to

them that which models they must follow to carry out their valuation.

11

prone to errors, having wrong assumptions, overconfidence towards the net worth of the

organisation. The major drawback with this system is that it does not consider time value

of money and not only this it also ignores the depreciation. In order to apply this method

on a particular investment appraisal a lot of assumption has to be taken with which makes

the result not fruitful. Further this method is over complex and very sensitive to changes

in assumptions depending the case under consideration.

Dividend valuation method: This method is very simple which does not provide accurate

justification to the results obtained thereunder. Further this method works only on those

shares which are regularly paying the dividend to its shareholders. There are some other

non-monetary factors too that affect the valuation of the entity such as customer

retention, loyalty towards brand etc. This model only values payment in the form of

dividend as the return on investment. This model is also very sensitive to the quality of

information involved because if the information is not correct then valuation will differ

completely.

Recommendation on which techniques must be followed by Kings Plc:

It is recommended to kings Plc is that to use dividend valuation method as their capital structure

cover both equity and debt and they are readily paying the dividend to its holders of security.

Therefore, from the above method they must consider dividend model to make valuation of their

company.

CONCLUSION

The above report consists of two different set of question relating to financial management that

has been addressed accordingly. The first question deals with capital structure of the organisation

which consist of equity, debt and reserves and surplus. Them after the weighted average cost of

capital has been calculated using book value and market value debts. In the next question the

valuation of Kings plc has been made using different models such as price earnings ratio method,

discounted cash flow method, dividend valuation method and recommendation has been made to

them that which models they must follow to carry out their valuation.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.