TSB Bank Performance: Asset, Liability, and Banking Sector Impact

VerifiedAdded on 2023/01/12

|11

|3750

|98

Report

AI Summary

This report provides a comprehensive analysis of TSB Bank's financial performance, examining its assets, liabilities, and income structure changes from 2018 to 2019. It includes a brief overview of TSB Bank's business activities and critically analyzes the bank's balance sheet, highlighting fluctuations in cash, debt securities, property, and loans. The report evaluates the bank's performance using profitability, efficiency, and liquidity ratios, such as operating margin, net profit margin, and current ratio, providing interpretations of each. Furthermore, it assesses the impact of banking sector changes, including digital transformation and Brexit, on TSB's performance, concluding with an evaluation of the bank's expected future performance and overall financial health. The analysis reveals insights into TSB Bank's operational efficiency and strategic positioning within the evolving banking landscape.

Modern Banking

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Brief overview of TSB bank in terms of nature or its business activities...................................3

Critically analyse the bank’s assets & liability or income structure changes over the time........3

Critically evaluate bank’s performance over the period by using ratio analysis.........................4

Critically evaluated that how banking sector changes impact the particular bank’s performance

.....................................................................................................................................................6

Assessment of an expected future performance of TSB bank.....................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

2

MAIN BODY..................................................................................................................................3

Brief overview of TSB bank in terms of nature or its business activities...................................3

Critically analyse the bank’s assets & liability or income structure changes over the time........3

Critically evaluate bank’s performance over the period by using ratio analysis.........................4

Critically evaluated that how banking sector changes impact the particular bank’s performance

.....................................................................................................................................................6

Assessment of an expected future performance of TSB bank.....................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

2

INTRODUCTION

Modern Banking Systems is a largest supplier for community banks with key banking tech

solutions. The main banking delivery system in real time allows everyone the

mobility, protection to pick and integrate apps that customers require such as internet, mobile

applications banking (Begenau and Landvoigt, 2018). For the better understanding of modern

banking systems, this assignment select TBS bank which is UK based and offer all the services

which is provided by any common bank. This report includes the several discussions such as

changes in bank’s assets, liability and income structure. Evaluate banks performance with the

help of ratio analysis. In addition, it also included that critically evaluated that how changes in

banks affect overall bank’s performance.

MAIN BODY

Brief overview of TSB bank in terms of nature or its business activities

TSB Bank plc is based UK retail and commercial bank which is Banco Sabadell affiliate. It

operated a network of 536 branches in England, Scotland and Wales but has had no presence in

Northern Ireland since 1991. TSB introduced in its original form on 9 September 2013. Its

headquarters are based in Edinburgh which has more than 5.2 million customers, with loans and

consumer deposits of over £20 billion (Bianco and Sardoni, 2018). The bank offers a wide range

of corporate and individual financial and banking services including deposit accounts, loans,

credit cards, investments, and savings. TSB Bank is approved by the Prudential Regulation

Authority and is governed by both the Financial Conduct Authority and Prudential Regulation

Authority.

Critically analyse the bank’s assets & liability or income structure changes over the time

Balance sheet is a representation of a Bank's financial position which outlines the assets,

liabilities and equity of the holder at a specific point in time. In certain words, the balance sheet

shows the net worth of your company. It might also include data from previous years, so that

they can make two years in a row back-to-back contrast. These data will help us monitor overall

success and find ways to improve the finances and see where they need to get better. In context

of TSB bank, overall assets or liability of the company for the period of 2018 was £ 41,138

million and in 2019, it was £ 39,535 million. It is observed that overall assets or liabilities value

3

Modern Banking Systems is a largest supplier for community banks with key banking tech

solutions. The main banking delivery system in real time allows everyone the

mobility, protection to pick and integrate apps that customers require such as internet, mobile

applications banking (Begenau and Landvoigt, 2018). For the better understanding of modern

banking systems, this assignment select TBS bank which is UK based and offer all the services

which is provided by any common bank. This report includes the several discussions such as

changes in bank’s assets, liability and income structure. Evaluate banks performance with the

help of ratio analysis. In addition, it also included that critically evaluated that how changes in

banks affect overall bank’s performance.

MAIN BODY

Brief overview of TSB bank in terms of nature or its business activities

TSB Bank plc is based UK retail and commercial bank which is Banco Sabadell affiliate. It

operated a network of 536 branches in England, Scotland and Wales but has had no presence in

Northern Ireland since 1991. TSB introduced in its original form on 9 September 2013. Its

headquarters are based in Edinburgh which has more than 5.2 million customers, with loans and

consumer deposits of over £20 billion (Bianco and Sardoni, 2018). The bank offers a wide range

of corporate and individual financial and banking services including deposit accounts, loans,

credit cards, investments, and savings. TSB Bank is approved by the Prudential Regulation

Authority and is governed by both the Financial Conduct Authority and Prudential Regulation

Authority.

Critically analyse the bank’s assets & liability or income structure changes over the time

Balance sheet is a representation of a Bank's financial position which outlines the assets,

liabilities and equity of the holder at a specific point in time. In certain words, the balance sheet

shows the net worth of your company. It might also include data from previous years, so that

they can make two years in a row back-to-back contrast. These data will help us monitor overall

success and find ways to improve the finances and see where they need to get better. In context

of TSB bank, overall assets or liability of the company for the period of 2018 was £ 41,138

million and in 2019, it was £ 39,535 million. It is observed that overall assets or liabilities value

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decreases. Through analysing annual report of the bank, it is also identifying that items of

balance sheet has fluctuation from the period of 2018 to 2019.

In the assets side of balance sheet, cash and other demand deposits reduce that is £ 7,135

million in 2018 and £ 4,592 in 2019 (Annual Report of TSB Bank, 2019). Debt security increases

from 2018 to 2019 because previously it was £ 96.2 million and latest year it was £ 548.6 million

that is huge change in the numbers. Property and equipment increases, £ 163.1 million in 2018

and £ 293.2 million in 2019 that means company spend their money buy properties for its

operational expansion. An intangible asset also increases where it was £ 18.4 million in 2018 and

in 2019 it was £ 20.3 million. In 2018, loan and advances to customers is £ 30,008 million and in

2019 it was £ 31,075 million. Other assets of TBS bank are £ 197.1 million in 2018 and it was

reduces and remain at £ 146.5 million in 2019. Basically, an overall asset of value of bank from

2018 to 2019 decreases and it has several reasons. Further discussion is all about the changes in

liabilities side from the period of 2018 to 2019.

In the liability side of balance sheet, borrowings from central banks reduce from £ 6,482

million to £ 4,483 million for the period of 2018 to 2019. Customer deposits increase from 2018

to 2019 where the value was £ 29,094 million to £ 30,182 million. In 2018, debt securities in

issues were £ 1,122 million and £ 1,676 million in 2019. Portfolio hedged risk heavily increases

such as in 2018 it was £ 9.4 million and on 2019 it was £ 52.2 million (Carruthers, 2018)

(Danyali, 2018). Provisions of the banks are 51.8 million in 2019 and 63.6 million in 2018. In

the TSB bank, share capital is same for both years that are 79.4 million. Share premium for the

period was 195.6 million and merger reserves are 412.8 million for the duration of 2018 to 2019.

Overall shareholder’s equity increases from the period of 2018 it was 1,878 million and in 2019

it was 1,900 million.

According to income statement of TSB bank for the period of 2018 to 2019, it was

critically evaluated that interest income from 2018 to 2019 duration decreases with £ 22 million.

So, net interest income for the period of 2018 was £ 884.8 million and in 2019 it was £ 841.1

which shows the decline around £ 43.7 million. In result, total income also reduces from

£1,295.3 million to £ 987.2 million. It was also found that, operating expenses in 2019 of TSB

bank decreases in comparison to previous year that was £ 881.3 million. At the end,

comprehensive income for the duration of 2018 was £ (60.1) million which was a loss and in

2019 bank generate profit of £ 21.9 million.

4

balance sheet has fluctuation from the period of 2018 to 2019.

In the assets side of balance sheet, cash and other demand deposits reduce that is £ 7,135

million in 2018 and £ 4,592 in 2019 (Annual Report of TSB Bank, 2019). Debt security increases

from 2018 to 2019 because previously it was £ 96.2 million and latest year it was £ 548.6 million

that is huge change in the numbers. Property and equipment increases, £ 163.1 million in 2018

and £ 293.2 million in 2019 that means company spend their money buy properties for its

operational expansion. An intangible asset also increases where it was £ 18.4 million in 2018 and

in 2019 it was £ 20.3 million. In 2018, loan and advances to customers is £ 30,008 million and in

2019 it was £ 31,075 million. Other assets of TBS bank are £ 197.1 million in 2018 and it was

reduces and remain at £ 146.5 million in 2019. Basically, an overall asset of value of bank from

2018 to 2019 decreases and it has several reasons. Further discussion is all about the changes in

liabilities side from the period of 2018 to 2019.

In the liability side of balance sheet, borrowings from central banks reduce from £ 6,482

million to £ 4,483 million for the period of 2018 to 2019. Customer deposits increase from 2018

to 2019 where the value was £ 29,094 million to £ 30,182 million. In 2018, debt securities in

issues were £ 1,122 million and £ 1,676 million in 2019. Portfolio hedged risk heavily increases

such as in 2018 it was £ 9.4 million and on 2019 it was £ 52.2 million (Carruthers, 2018)

(Danyali, 2018). Provisions of the banks are 51.8 million in 2019 and 63.6 million in 2018. In

the TSB bank, share capital is same for both years that are 79.4 million. Share premium for the

period was 195.6 million and merger reserves are 412.8 million for the duration of 2018 to 2019.

Overall shareholder’s equity increases from the period of 2018 it was 1,878 million and in 2019

it was 1,900 million.

According to income statement of TSB bank for the period of 2018 to 2019, it was

critically evaluated that interest income from 2018 to 2019 duration decreases with £ 22 million.

So, net interest income for the period of 2018 was £ 884.8 million and in 2019 it was £ 841.1

which shows the decline around £ 43.7 million. In result, total income also reduces from

£1,295.3 million to £ 987.2 million. It was also found that, operating expenses in 2019 of TSB

bank decreases in comparison to previous year that was £ 881.3 million. At the end,

comprehensive income for the duration of 2018 was £ (60.1) million which was a loss and in

2019 bank generate profit of £ 21.9 million.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

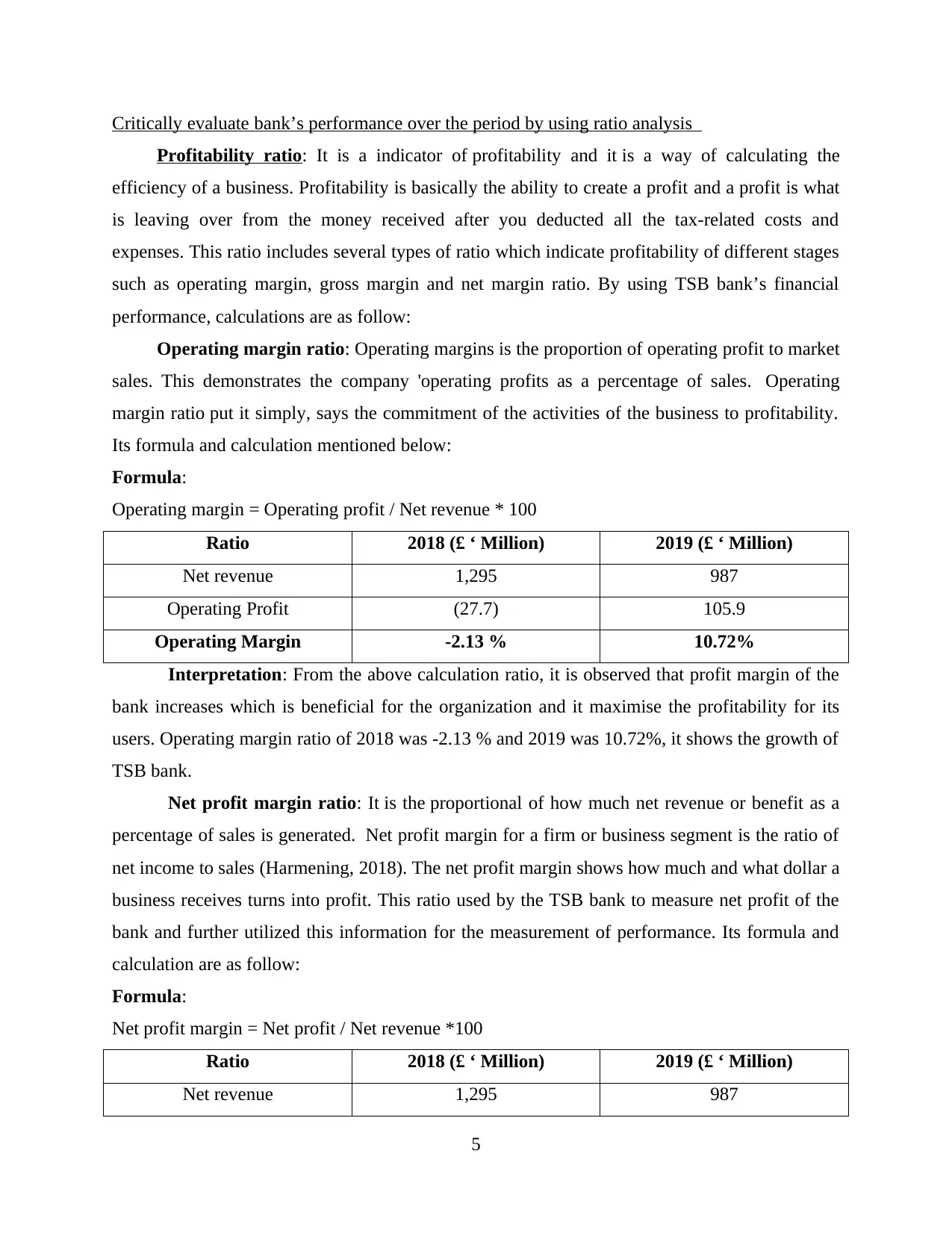

Critically evaluate bank’s performance over the period by using ratio analysis

Profitability ratio: It is a indicator of profitability and it is a way of calculating the

efficiency of a business. Profitability is basically the ability to create a profit and a profit is what

is leaving over from the money received after you deducted all the tax-related costs and

expenses. This ratio includes several types of ratio which indicate profitability of different stages

such as operating margin, gross margin and net margin ratio. By using TSB bank’s financial

performance, calculations are as follow:

Operating margin ratio: Operating margins is the proportion of operating profit to market

sales. This demonstrates the company 'operating profits as a percentage of sales. Operating

margin ratio put it simply, says the commitment of the activities of the business to profitability.

Its formula and calculation mentioned below:

Formula:

Operating margin = Operating profit / Net revenue * 100

Ratio 2018 (£ ‘ Million) 2019 (£ ‘ Million)

Net revenue 1,295 987

Operating Profit (27.7) 105.9

Operating Margin -2.13 % 10.72%

Interpretation: From the above calculation ratio, it is observed that profit margin of the

bank increases which is beneficial for the organization and it maximise the profitability for its

users. Operating margin ratio of 2018 was -2.13 % and 2019 was 10.72%, it shows the growth of

TSB bank.

Net profit margin ratio: It is the proportional of how much net revenue or benefit as a

percentage of sales is generated. Net profit margin for a firm or business segment is the ratio of

net income to sales (Harmening, 2018). The net profit margin shows how much and what dollar a

business receives turns into profit. This ratio used by the TSB bank to measure net profit of the

bank and further utilized this information for the measurement of performance. Its formula and

calculation are as follow:

Formula:

Net profit margin = Net profit / Net revenue *100

Ratio 2018 (£ ‘ Million) 2019 (£ ‘ Million)

Net revenue 1,295 987

5

Profitability ratio: It is a indicator of profitability and it is a way of calculating the

efficiency of a business. Profitability is basically the ability to create a profit and a profit is what

is leaving over from the money received after you deducted all the tax-related costs and

expenses. This ratio includes several types of ratio which indicate profitability of different stages

such as operating margin, gross margin and net margin ratio. By using TSB bank’s financial

performance, calculations are as follow:

Operating margin ratio: Operating margins is the proportion of operating profit to market

sales. This demonstrates the company 'operating profits as a percentage of sales. Operating

margin ratio put it simply, says the commitment of the activities of the business to profitability.

Its formula and calculation mentioned below:

Formula:

Operating margin = Operating profit / Net revenue * 100

Ratio 2018 (£ ‘ Million) 2019 (£ ‘ Million)

Net revenue 1,295 987

Operating Profit (27.7) 105.9

Operating Margin -2.13 % 10.72%

Interpretation: From the above calculation ratio, it is observed that profit margin of the

bank increases which is beneficial for the organization and it maximise the profitability for its

users. Operating margin ratio of 2018 was -2.13 % and 2019 was 10.72%, it shows the growth of

TSB bank.

Net profit margin ratio: It is the proportional of how much net revenue or benefit as a

percentage of sales is generated. Net profit margin for a firm or business segment is the ratio of

net income to sales (Harmening, 2018). The net profit margin shows how much and what dollar a

business receives turns into profit. This ratio used by the TSB bank to measure net profit of the

bank and further utilized this information for the measurement of performance. Its formula and

calculation are as follow:

Formula:

Net profit margin = Net profit / Net revenue *100

Ratio 2018 (£ ‘ Million) 2019 (£ ‘ Million)

Net revenue 1,295 987

5

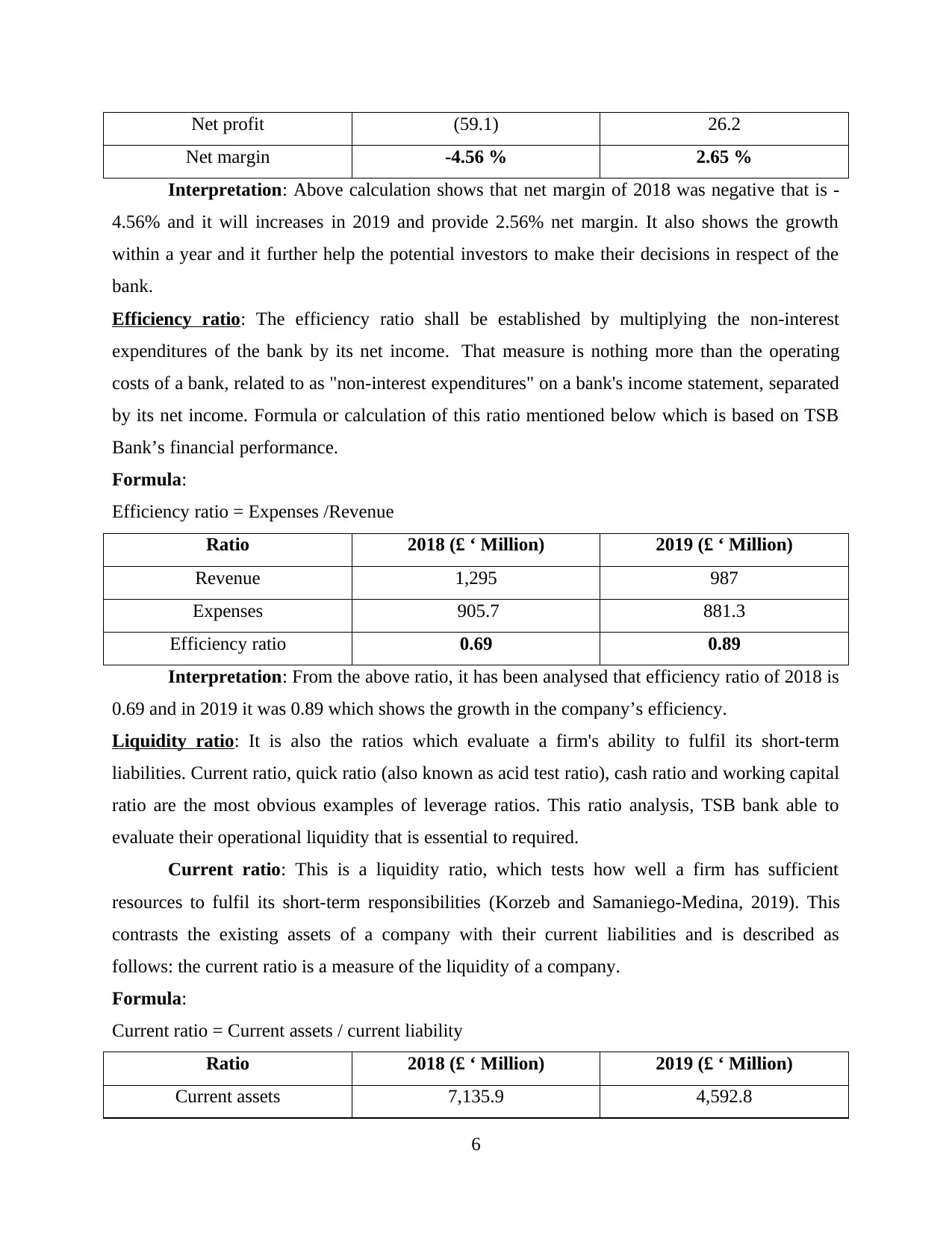

Net profit (59.1) 26.2

Net margin -4.56 % 2.65 %

Interpretation: Above calculation shows that net margin of 2018 was negative that is -

4.56% and it will increases in 2019 and provide 2.56% net margin. It also shows the growth

within a year and it further help the potential investors to make their decisions in respect of the

bank.

Efficiency ratio: The efficiency ratio shall be established by multiplying the non-interest

expenditures of the bank by its net income. That measure is nothing more than the operating

costs of a bank, related to as "non-interest expenditures" on a bank's income statement, separated

by its net income. Formula or calculation of this ratio mentioned below which is based on TSB

Bank’s financial performance.

Formula:

Efficiency ratio = Expenses /Revenue

Ratio 2018 (£ ‘ Million) 2019 (£ ‘ Million)

Revenue 1,295 987

Expenses 905.7 881.3

Efficiency ratio 0.69 0.89

Interpretation: From the above ratio, it has been analysed that efficiency ratio of 2018 is

0.69 and in 2019 it was 0.89 which shows the growth in the company’s efficiency.

Liquidity ratio: It is also the ratios which evaluate a firm's ability to fulfil its short-term

liabilities. Current ratio, quick ratio (also known as acid test ratio), cash ratio and working capital

ratio are the most obvious examples of leverage ratios. This ratio analysis, TSB bank able to

evaluate their operational liquidity that is essential to required.

Current ratio: This is a liquidity ratio, which tests how well a firm has sufficient

resources to fulfil its short-term responsibilities (Korzeb and Samaniego-Medina, 2019). This

contrasts the existing assets of a company with their current liabilities and is described as

follows: the current ratio is a measure of the liquidity of a company.

Formula:

Current ratio = Current assets / current liability

Ratio 2018 (£ ‘ Million) 2019 (£ ‘ Million)

Current assets 7,135.9 4,592.8

6

Net margin -4.56 % 2.65 %

Interpretation: Above calculation shows that net margin of 2018 was negative that is -

4.56% and it will increases in 2019 and provide 2.56% net margin. It also shows the growth

within a year and it further help the potential investors to make their decisions in respect of the

bank.

Efficiency ratio: The efficiency ratio shall be established by multiplying the non-interest

expenditures of the bank by its net income. That measure is nothing more than the operating

costs of a bank, related to as "non-interest expenditures" on a bank's income statement, separated

by its net income. Formula or calculation of this ratio mentioned below which is based on TSB

Bank’s financial performance.

Formula:

Efficiency ratio = Expenses /Revenue

Ratio 2018 (£ ‘ Million) 2019 (£ ‘ Million)

Revenue 1,295 987

Expenses 905.7 881.3

Efficiency ratio 0.69 0.89

Interpretation: From the above ratio, it has been analysed that efficiency ratio of 2018 is

0.69 and in 2019 it was 0.89 which shows the growth in the company’s efficiency.

Liquidity ratio: It is also the ratios which evaluate a firm's ability to fulfil its short-term

liabilities. Current ratio, quick ratio (also known as acid test ratio), cash ratio and working capital

ratio are the most obvious examples of leverage ratios. This ratio analysis, TSB bank able to

evaluate their operational liquidity that is essential to required.

Current ratio: This is a liquidity ratio, which tests how well a firm has sufficient

resources to fulfil its short-term responsibilities (Korzeb and Samaniego-Medina, 2019). This

contrasts the existing assets of a company with their current liabilities and is described as

follows: the current ratio is a measure of the liquidity of a company.

Formula:

Current ratio = Current assets / current liability

Ratio 2018 (£ ‘ Million) 2019 (£ ‘ Million)

Current assets 7,135.9 4,592.8

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

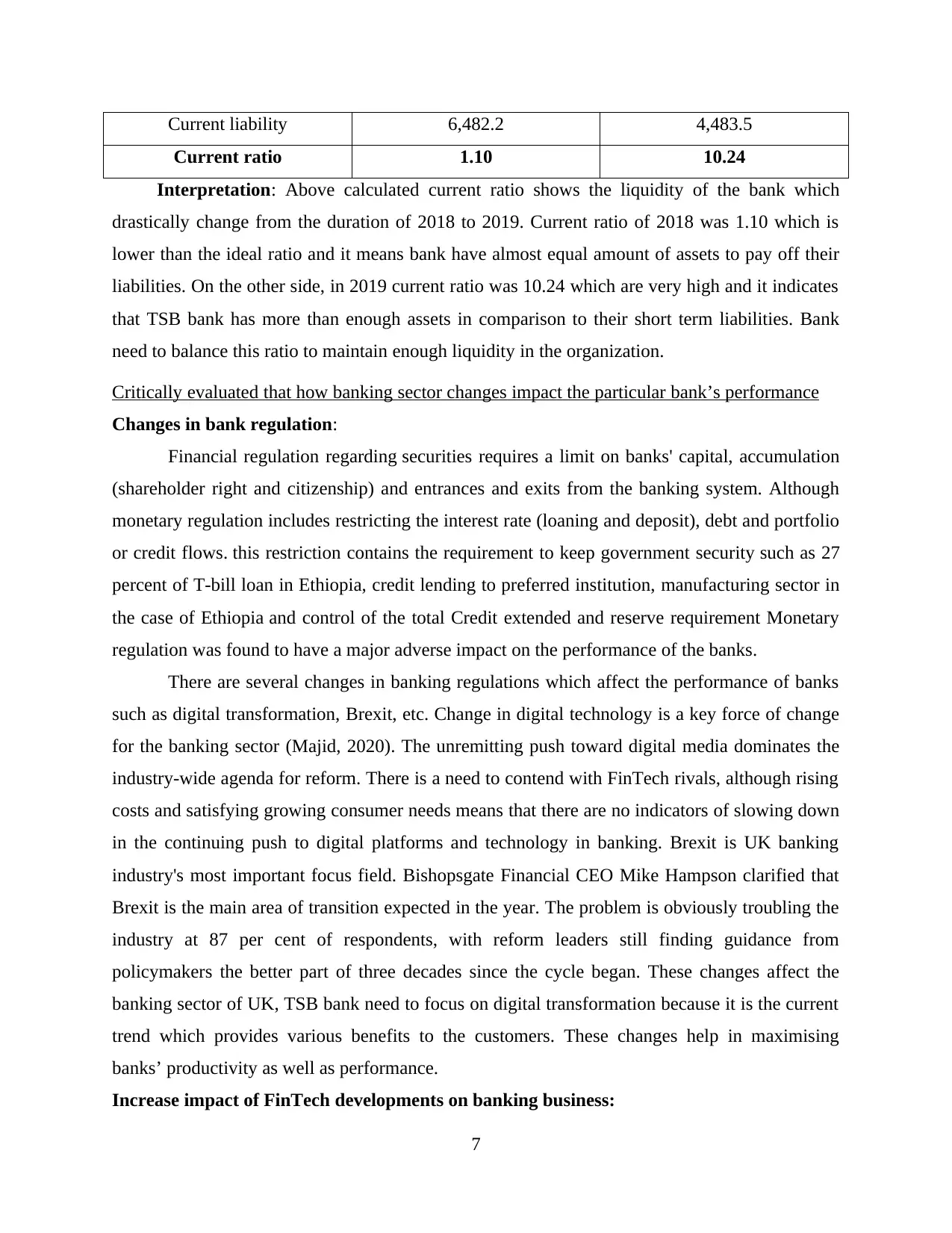

Current liability 6,482.2 4,483.5

Current ratio 1.10 10.24

Interpretation: Above calculated current ratio shows the liquidity of the bank which

drastically change from the duration of 2018 to 2019. Current ratio of 2018 was 1.10 which is

lower than the ideal ratio and it means bank have almost equal amount of assets to pay off their

liabilities. On the other side, in 2019 current ratio was 10.24 which are very high and it indicates

that TSB bank has more than enough assets in comparison to their short term liabilities. Bank

need to balance this ratio to maintain enough liquidity in the organization.

Critically evaluated that how banking sector changes impact the particular bank’s performance

Changes in bank regulation:

Financial regulation regarding securities requires a limit on banks' capital, accumulation

(shareholder right and citizenship) and entrances and exits from the banking system. Although

monetary regulation includes restricting the interest rate (loaning and deposit), debt and portfolio

or credit flows. this restriction contains the requirement to keep government security such as 27

percent of T-bill loan in Ethiopia, credit lending to preferred institution, manufacturing sector in

the case of Ethiopia and control of the total Credit extended and reserve requirement Monetary

regulation was found to have a major adverse impact on the performance of the banks.

There are several changes in banking regulations which affect the performance of banks

such as digital transformation, Brexit, etc. Change in digital technology is a key force of change

for the banking sector (Majid, 2020). The unremitting push toward digital media dominates the

industry-wide agenda for reform. There is a need to contend with FinTech rivals, although rising

costs and satisfying growing consumer needs means that there are no indicators of slowing down

in the continuing push to digital platforms and technology in banking. Brexit is UK banking

industry's most important focus field. Bishopsgate Financial CEO Mike Hampson clarified that

Brexit is the main area of transition expected in the year. The problem is obviously troubling the

industry at 87 per cent of respondents, with reform leaders still finding guidance from

policymakers the better part of three decades since the cycle began. These changes affect the

banking sector of UK, TSB bank need to focus on digital transformation because it is the current

trend which provides various benefits to the customers. These changes help in maximising

banks’ productivity as well as performance.

Increase impact of FinTech developments on banking business:

7

Current ratio 1.10 10.24

Interpretation: Above calculated current ratio shows the liquidity of the bank which

drastically change from the duration of 2018 to 2019. Current ratio of 2018 was 1.10 which is

lower than the ideal ratio and it means bank have almost equal amount of assets to pay off their

liabilities. On the other side, in 2019 current ratio was 10.24 which are very high and it indicates

that TSB bank has more than enough assets in comparison to their short term liabilities. Bank

need to balance this ratio to maintain enough liquidity in the organization.

Critically evaluated that how banking sector changes impact the particular bank’s performance

Changes in bank regulation:

Financial regulation regarding securities requires a limit on banks' capital, accumulation

(shareholder right and citizenship) and entrances and exits from the banking system. Although

monetary regulation includes restricting the interest rate (loaning and deposit), debt and portfolio

or credit flows. this restriction contains the requirement to keep government security such as 27

percent of T-bill loan in Ethiopia, credit lending to preferred institution, manufacturing sector in

the case of Ethiopia and control of the total Credit extended and reserve requirement Monetary

regulation was found to have a major adverse impact on the performance of the banks.

There are several changes in banking regulations which affect the performance of banks

such as digital transformation, Brexit, etc. Change in digital technology is a key force of change

for the banking sector (Majid, 2020). The unremitting push toward digital media dominates the

industry-wide agenda for reform. There is a need to contend with FinTech rivals, although rising

costs and satisfying growing consumer needs means that there are no indicators of slowing down

in the continuing push to digital platforms and technology in banking. Brexit is UK banking

industry's most important focus field. Bishopsgate Financial CEO Mike Hampson clarified that

Brexit is the main area of transition expected in the year. The problem is obviously troubling the

industry at 87 per cent of respondents, with reform leaders still finding guidance from

policymakers the better part of three decades since the cycle began. These changes affect the

banking sector of UK, TSB bank need to focus on digital transformation because it is the current

trend which provides various benefits to the customers. These changes help in maximising

banks’ productivity as well as performance.

Increase impact of FinTech developments on banking business:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fintech rivals are disrupting the conventional banking market, given the fact that

institutions adapt to the digital world. New entrants may use hard (codifiable) data to erode the

conventional banking-customer relationship on the basis of soft information. Banks have

historically concentrated on goods, although there are more than 55 new entrants. Fintech rivals

put competition to bear on banks' conventional business model. Fintech outlets benefit from the

circumstance but depend on government assurances that are both explicit and implied. This fact

indicates that the entry into the traditional banking market with new technology would depend

greatly on how regulations and government guarantees are implemented.

Fintech can be interpreted as using advanced information and mechanized farming in

financial services. New digital technology automates a diverse range of business activities and

can offer fresh and more price-effective solutions in parts of the financial sector. From lending to

wealth management and from investment, it was advised for payment system (Pilnik, Radionov

and Yazykov, 2018). Throughout these sectors, the influence of fintech rivals is starting to be

noticed in the banking and capital markets. Furthermore, in comparison with the scale of

financial intermediated assets and markets, the fintech field is low and lagging behind in Europe,

both in terms of level and development rate, relative to the US or China.

Consolidation in the banking sector of the particular country:

Small and medium-sized banks throughout the UK are preparing themselves for a

massive wave of consolidation as price increases, competitive pressures and a shrinking

economy are generating new obstacles for groups seeking to take on big five lenders. Senior

managers at many small lenders and existing high streets banks said they were anticipating a

pick-up in M&A activity. After Shawbrook's £850m acquisition last year and Aldermore's

£1.1bn purchase of FirstRand placed the market on alert for a switch to deal making.

After the financial crisis, legislation designed to encourage competition in the banking

sector have facilitated a proliferation of different "challenger" banks and professional lenders.

But Paul Lynam, board member responsible for competitors at the UK Finance industry lobby

group and chief executive of Safe Trust Bank, said it's "nearly unavoidable" that many of them

will be merging.

Consolidation may help reduce cost incompetence if the management of the purchasing

company becomes more effective at reducing costs than the leadership of the goal, and is willing

to remove excessive costs after the combination occurs. In the future, the restructuring process

8

institutions adapt to the digital world. New entrants may use hard (codifiable) data to erode the

conventional banking-customer relationship on the basis of soft information. Banks have

historically concentrated on goods, although there are more than 55 new entrants. Fintech rivals

put competition to bear on banks' conventional business model. Fintech outlets benefit from the

circumstance but depend on government assurances that are both explicit and implied. This fact

indicates that the entry into the traditional banking market with new technology would depend

greatly on how regulations and government guarantees are implemented.

Fintech can be interpreted as using advanced information and mechanized farming in

financial services. New digital technology automates a diverse range of business activities and

can offer fresh and more price-effective solutions in parts of the financial sector. From lending to

wealth management and from investment, it was advised for payment system (Pilnik, Radionov

and Yazykov, 2018). Throughout these sectors, the influence of fintech rivals is starting to be

noticed in the banking and capital markets. Furthermore, in comparison with the scale of

financial intermediated assets and markets, the fintech field is low and lagging behind in Europe,

both in terms of level and development rate, relative to the US or China.

Consolidation in the banking sector of the particular country:

Small and medium-sized banks throughout the UK are preparing themselves for a

massive wave of consolidation as price increases, competitive pressures and a shrinking

economy are generating new obstacles for groups seeking to take on big five lenders. Senior

managers at many small lenders and existing high streets banks said they were anticipating a

pick-up in M&A activity. After Shawbrook's £850m acquisition last year and Aldermore's

£1.1bn purchase of FirstRand placed the market on alert for a switch to deal making.

After the financial crisis, legislation designed to encourage competition in the banking

sector have facilitated a proliferation of different "challenger" banks and professional lenders.

But Paul Lynam, board member responsible for competitors at the UK Finance industry lobby

group and chief executive of Safe Trust Bank, said it's "nearly unavoidable" that many of them

will be merging.

Consolidation may help reduce cost incompetence if the management of the purchasing

company becomes more effective at reducing costs than the leadership of the goal, and is willing

to remove excessive costs after the combination occurs. In the future, the restructuring process

8

will vary by country and from segment to segment, based on the various reference points about

the number of companies and the variety of operations carried out within the organization

concerned. In Europe, the speed of restructuring could increase, provided that the euro's

stimulating effect is not yet running its course, although impediments can be reduced as

integration advances in areas such as taxation and regulation.

Issues relevant to the changes observed in the global banking markets or particular

country’s banking markets:

In all over the banking sector, there are several issues faced by the banks in the global

market. These challenges affect the performance as well as profitability of the banks. Some of

them are as follow:

Customer retention: Customers of financial services expect customized and meaningful

interactions via simple and straightforward interfaces on any computer, anywhere and at any

point. While consumer experience can be difficult to measure, customer satisfaction is

measurable and customer loyalty is increasingly becoming a term in trouble. Customer loyalty is

a result of a wealth of customer relationships that begin with understanding the customer and

their needs and adopting a continuous customer-cantered approach.

Outdated mobile application: Banking or financial group has its own customized mobile

application but because an company has an internet banking plan doesn't mean it's diversified as

best as possible (Popova and Butakova, 2019). To keep customers happy, a bank's mobile

experience requires being smooth, easy to use, feature packed, safe, and updated regularly. Many

banks have also started to re-imagine what a banking app might be by adding mobile payment

technology that enables consumers to view their cell phones as protected digital wallets and send

money to other countries and friends instantly.

Assessment of an expected future performance of TSB bank

From the above financial analysis of TSB bank, it has been analysed that bank need to

improve their performance there is growth between two consecutive years but not according to

the entire industry growth. Profitability ratio was is favourable condition but they need to

improve liquidity that is 10.24 in 2019 that is not according to ideal ratio. Ideal ratio should be

2:1 which means company have sufficient assets to meet their obligations. But in 2019, this ratio

indicates that banks have more than required current assets that are not beneficial at all.

9

the number of companies and the variety of operations carried out within the organization

concerned. In Europe, the speed of restructuring could increase, provided that the euro's

stimulating effect is not yet running its course, although impediments can be reduced as

integration advances in areas such as taxation and regulation.

Issues relevant to the changes observed in the global banking markets or particular

country’s banking markets:

In all over the banking sector, there are several issues faced by the banks in the global

market. These challenges affect the performance as well as profitability of the banks. Some of

them are as follow:

Customer retention: Customers of financial services expect customized and meaningful

interactions via simple and straightforward interfaces on any computer, anywhere and at any

point. While consumer experience can be difficult to measure, customer satisfaction is

measurable and customer loyalty is increasingly becoming a term in trouble. Customer loyalty is

a result of a wealth of customer relationships that begin with understanding the customer and

their needs and adopting a continuous customer-cantered approach.

Outdated mobile application: Banking or financial group has its own customized mobile

application but because an company has an internet banking plan doesn't mean it's diversified as

best as possible (Popova and Butakova, 2019). To keep customers happy, a bank's mobile

experience requires being smooth, easy to use, feature packed, safe, and updated regularly. Many

banks have also started to re-imagine what a banking app might be by adding mobile payment

technology that enables consumers to view their cell phones as protected digital wallets and send

money to other countries and friends instantly.

Assessment of an expected future performance of TSB bank

From the above financial analysis of TSB bank, it has been analysed that bank need to

improve their performance there is growth between two consecutive years but not according to

the entire industry growth. Profitability ratio was is favourable condition but they need to

improve liquidity that is 10.24 in 2019 that is not according to ideal ratio. Ideal ratio should be

2:1 which means company have sufficient assets to meet their obligations. But in 2019, this ratio

indicates that banks have more than required current assets that are not beneficial at all.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TSB bank should focus on changes in the banking sector such as digital transformation to

eliminate the issues which they currently face. TSB Bank introduces three latest strategies for

future growth and it should be achieved by 2022. They focus on three aspects to enhance their

performance and all are discussed below:

Customer focus: Because of its target section the "Aspiring Middle" made up of working

people, money converters and variable income customer groups. TSB will provide wonderful

banking basics and convincing differences. Such clients have a variety of unmet needs and

clearly pose resources where TSB can really make a big difference.

Simplification and efficiency: Becoming a company that is more tech-enabled and creative

means turning it to be easier and more efficient (Smolyansky, 2019). With dual-cloud and data

technologies, TSB's latest IT framework has a solid foundation to build on for the future,

leveraging data-driven knowledge and analytics to optimize user experiences because of its

target market.

Operational excellence: TSB seeks to build a robust and profitable organization that

provides operational excellence. Clear governance structure and monitoring are behind the plan,

supported by an accomplished management team.

CONCLUSION

From the above discussion, it has been observed that banking sector need to update their

operational activities according to business environment otherwise it affects the overall

performance. Ratio analysis is the most suitable method of analysing performance which further

beneficial for management to make decisions.

10

eliminate the issues which they currently face. TSB Bank introduces three latest strategies for

future growth and it should be achieved by 2022. They focus on three aspects to enhance their

performance and all are discussed below:

Customer focus: Because of its target section the "Aspiring Middle" made up of working

people, money converters and variable income customer groups. TSB will provide wonderful

banking basics and convincing differences. Such clients have a variety of unmet needs and

clearly pose resources where TSB can really make a big difference.

Simplification and efficiency: Becoming a company that is more tech-enabled and creative

means turning it to be easier and more efficient (Smolyansky, 2019). With dual-cloud and data

technologies, TSB's latest IT framework has a solid foundation to build on for the future,

leveraging data-driven knowledge and analytics to optimize user experiences because of its

target market.

Operational excellence: TSB seeks to build a robust and profitable organization that

provides operational excellence. Clear governance structure and monitoring are behind the plan,

supported by an accomplished management team.

CONCLUSION

From the above discussion, it has been observed that banking sector need to update their

operational activities according to business environment otherwise it affects the overall

performance. Ratio analysis is the most suitable method of analysing performance which further

beneficial for management to make decisions.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books & Journals

Begenau, J., & Landvoigt, T. (2018). Financial regulation in a quantitative model of the modern

banking system. Available at SSRN 2748206.

Bianco, A., & Sardoni, C. (2018). Banking theories and macroeconomics. Journal of Post

Keynesian Economics. 41(2). 165-184.

Carruthers, B. G. (2018). What Is Sociological About Banks and Banking?. In The sociology of

economic life (pp. 242-263). Routledge.

Danyali, A. A. (2018). Factors influencing customers’ change of behaviors from online banking

to mobile banking in Tejarat Bank, Iran. Journal of Organizational Change Management.

Harmening, D. M. (2018). Modern blood banking & transfusion practices. FA Davis.

Korzeb, Z., & Samaniego-Medina, R. (2019). Sustainability Performance. A Comparative

Analysis in the Polish Banking Sector. Sustainability. 11(3). 653.

Majid, M. A. (2020). The Input Requirements of Conventional and Shariahcompliant

Banking. International Journal of Banking and Finance. 7(1). 51-78.

Pilnik, N., Radionov, S., & Yazykov, A. (2018). The Optimal Behavior Model of the Modern

Russian Banking System. HSE Economic Journal. 22(3). 418-447.

Popova, N. A., & Butakova, N. G. (2019, January). Research of a possibility of using blockchain

technology without tokens to protect banking transactions. In 2019 IEEE Conference of

Russian Young Researchers in Electrical and Electronic Engineering (EIConRus) (pp.

1764-1768). IEEE.

Smolyansky, M. (2019). Policy externalities and banking integration. Journal of Financial

Economics. 132(3). 118-139.

Online

Annual Report of TSB Bank. 2019. [Online]. Available Through:

< https://www.tsb.co.uk/tsb-bank-ara-2019.pdf >

11

Books & Journals

Begenau, J., & Landvoigt, T. (2018). Financial regulation in a quantitative model of the modern

banking system. Available at SSRN 2748206.

Bianco, A., & Sardoni, C. (2018). Banking theories and macroeconomics. Journal of Post

Keynesian Economics. 41(2). 165-184.

Carruthers, B. G. (2018). What Is Sociological About Banks and Banking?. In The sociology of

economic life (pp. 242-263). Routledge.

Danyali, A. A. (2018). Factors influencing customers’ change of behaviors from online banking

to mobile banking in Tejarat Bank, Iran. Journal of Organizational Change Management.

Harmening, D. M. (2018). Modern blood banking & transfusion practices. FA Davis.

Korzeb, Z., & Samaniego-Medina, R. (2019). Sustainability Performance. A Comparative

Analysis in the Polish Banking Sector. Sustainability. 11(3). 653.

Majid, M. A. (2020). The Input Requirements of Conventional and Shariahcompliant

Banking. International Journal of Banking and Finance. 7(1). 51-78.

Pilnik, N., Radionov, S., & Yazykov, A. (2018). The Optimal Behavior Model of the Modern

Russian Banking System. HSE Economic Journal. 22(3). 418-447.

Popova, N. A., & Butakova, N. G. (2019, January). Research of a possibility of using blockchain

technology without tokens to protect banking transactions. In 2019 IEEE Conference of

Russian Young Researchers in Electrical and Electronic Engineering (EIConRus) (pp.

1764-1768). IEEE.

Smolyansky, M. (2019). Policy externalities and banking integration. Journal of Financial

Economics. 132(3). 118-139.

Online

Annual Report of TSB Bank. 2019. [Online]. Available Through:

< https://www.tsb.co.uk/tsb-bank-ara-2019.pdf >

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.