Finance Report: Capital Structure and Market Evaluation of TUI Group

VerifiedAdded on 2020/02/14

|32

|7114

|144

Report

AI Summary

This report provides a comprehensive analysis of TUI Group's financial strategies, focusing on its capital structure and market valuation. It explores the application of various corporate finance theories, including the trade-off theory, pecking order theory, and agency costs, to understand TUI's approach to debt and equity financing. The report delves into shareholder value analysis (SVA) to assess TUI's worth to shareholders, including the calculation of Weighted Average Cost of Capital (WACC) and the identification of value drivers. Furthermore, it examines the impact of modifying key assumptions in the financial models and discusses practical difficulties in applying the SVA model. The report provides a detailed examination of TUI Group's financial position, offering insights into its capital structure, market performance, and shareholder value, with the goal of informing management decisions and improving the company's overall financial health.

15058285_P58836_assignment 3

ACCOUNTING AND FINANCE

RESEARCH PROJECT

Student number: 15058285

Submission date: 30th September 2016

1

ACCOUNTING AND FINANCE

RESEARCH PROJECT

Student number: 15058285

Submission date: 30th September 2016

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

15058285_P58836_assignment 3

EXECUTIVE SUMMARY

After globalisation, companies carry out operations at international level as they operate in different countries across globe.

Thus, in order to sustain in the competitive age, they need huge amount of capital that is collected from debt and equity capital. The

composition of fixed and fluctuating capital that companies use is called capital structure. TUI Group is world’s leading tour company

that provides superior quality services to the global consumers to attain success. It is listed on London Stock Exchange (LSE) and

constutitents of FTSE index and regulated market of the Frankfurt Stock Exchange. This assignment report will lay emphasizes upon

the application of different corporate finance theories like capital structure theory in contxt to TUI Group. Moreover, shareholders

value analysis will be done in order to measures TUI Group’s worth to shareholders. Along with this, sensitivity analysis will be done

to assess the potential change in business performance with the market uncertainties.

1

EXECUTIVE SUMMARY

After globalisation, companies carry out operations at international level as they operate in different countries across globe.

Thus, in order to sustain in the competitive age, they need huge amount of capital that is collected from debt and equity capital. The

composition of fixed and fluctuating capital that companies use is called capital structure. TUI Group is world’s leading tour company

that provides superior quality services to the global consumers to attain success. It is listed on London Stock Exchange (LSE) and

constutitents of FTSE index and regulated market of the Frankfurt Stock Exchange. This assignment report will lay emphasizes upon

the application of different corporate finance theories like capital structure theory in contxt to TUI Group. Moreover, shareholders

value analysis will be done in order to measures TUI Group’s worth to shareholders. Along with this, sensitivity analysis will be done

to assess the potential change in business performance with the market uncertainties.

1

15058285_P58836_assignment 3

Table of Contents

INTRODUCTION........................................................................................................................................................................................3

1.TUI’s capital structure under the light of finance models.....................................................................................................................3

2. TUI’s market evaluation.....................................................................................................................................................................10

A. Weighted Average Cost of Capital for TUI.......................................................................................................................................10

B. Shareholder Value Analysis Model...................................................................................................................................................14

C. Value Drivers.....................................................................................................................................................................................17

D. Practically Application Difficulties of SVA......................................................................................................................................19

E. Market Value of TUI..........................................................................................................................................................................22

3. Impacts of modifications of key assumptions of the model...............................................................................................................23

CONCLUSION..........................................................................................................................................................................................26

REFERENCES...........................................................................................................................................................................................27

APPENDIX................................................................................................................................................................................................29

Appendix 1. DCF model.........................................................................................................................................................................29

2

Table of Contents

INTRODUCTION........................................................................................................................................................................................3

1.TUI’s capital structure under the light of finance models.....................................................................................................................3

2. TUI’s market evaluation.....................................................................................................................................................................10

A. Weighted Average Cost of Capital for TUI.......................................................................................................................................10

B. Shareholder Value Analysis Model...................................................................................................................................................14

C. Value Drivers.....................................................................................................................................................................................17

D. Practically Application Difficulties of SVA......................................................................................................................................19

E. Market Value of TUI..........................................................................................................................................................................22

3. Impacts of modifications of key assumptions of the model...............................................................................................................23

CONCLUSION..........................................................................................................................................................................................26

REFERENCES...........................................................................................................................................................................................27

APPENDIX................................................................................................................................................................................................29

Appendix 1. DCF model.........................................................................................................................................................................29

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

15058285_P58836_assignment 3

INTRODUCTION

In the volatile market era and tough competitive age, companies are require to make evaluation of their performance and

market valuation as well. TUI Group is one of the top or leading tourism organization that has more than 1800 travel agencies, six

airlines, 130 aircraft, 300 hotels and 13 cruises around the globe.The present project report aims at developing an understanding of the

different capital structure theories in the light of finance models. Moreover, the report will also make market value analysis by

estimating weighted average cost of capital of TUI Group. Apart from this, Shareholders value analysis (SVA) refers to the process of

analysing that how operations of a firm affects the value of net present value (NPV) to the investors. In other words, it helps to

measure the ability of organizations to generate excessive earnings than the cost of capital. The assignment report will apply the SVA

model for TUI Group to analyse its earnings capability. Along with this, the report will also describe the difficulties associated with the

model in real corporate practice.This report will guide the management to take necessary steps and suitable and necessary decisions for

the better functioning, expansion and performance of the organization.

1.TUI’s capital structure under the light of finance models

For understanding the capital structure of the company, first of all an understanding is needed to be established for the ways of selecting their

capital structure and its formation by any of the organizations. There is a relationship exists between capital structure of the company and the

value of the firm (GmbH, 2016). The capital structure formations are different with respect to the nature of the organization and the region of

location of the organization. This basic theory by Modigliani and Miller (1958) was proposed in a seminal research paper which is named as

“The cost of capital, corporation finance, and the theory of investment”. This paper explained that the factors like taxation remedies on interest

payment and transaction cost are absent, credit of corporations and people takes place with similar rateand the value of the organization is

3

INTRODUCTION

In the volatile market era and tough competitive age, companies are require to make evaluation of their performance and

market valuation as well. TUI Group is one of the top or leading tourism organization that has more than 1800 travel agencies, six

airlines, 130 aircraft, 300 hotels and 13 cruises around the globe.The present project report aims at developing an understanding of the

different capital structure theories in the light of finance models. Moreover, the report will also make market value analysis by

estimating weighted average cost of capital of TUI Group. Apart from this, Shareholders value analysis (SVA) refers to the process of

analysing that how operations of a firm affects the value of net present value (NPV) to the investors. In other words, it helps to

measure the ability of organizations to generate excessive earnings than the cost of capital. The assignment report will apply the SVA

model for TUI Group to analyse its earnings capability. Along with this, the report will also describe the difficulties associated with the

model in real corporate practice.This report will guide the management to take necessary steps and suitable and necessary decisions for

the better functioning, expansion and performance of the organization.

1.TUI’s capital structure under the light of finance models

For understanding the capital structure of the company, first of all an understanding is needed to be established for the ways of selecting their

capital structure and its formation by any of the organizations. There is a relationship exists between capital structure of the company and the

value of the firm (GmbH, 2016). The capital structure formations are different with respect to the nature of the organization and the region of

location of the organization. This basic theory by Modigliani and Miller (1958) was proposed in a seminal research paper which is named as

“The cost of capital, corporation finance, and the theory of investment”. This paper explained that the factors like taxation remedies on interest

payment and transaction cost are absent, credit of corporations and people takes place with similar rateand the value of the organization is

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

15058285_P58836_assignment 3

termed as independent from its capital structure.This proposed prototype is ideal for the organizations which exist in the environment of perfect

competition and product markets.Apart from this basic model of capital structure, other three models for the structuring the base for theoretical

considerations for the organization are discussed subsequently (Hammes y.n.d).

Miller and Modigliani(1958), developed two prepositions to describe the capital structure one is in the absence of capital structure and another

is with the absence of taxation liabilities that are enumerated underneath:

Preposition: 1. In the absence of taxation

In this preposition, it has been believed that changes in capital structure do not influence net value and weighted average cost of capital of

the firm. In other words, change in leverage and mix of debt and equity will not have any effect on firm’s value and cost of capital, thus, capital

structure is irrelevant. As per the theory, TUI can gathered funds either from the use of debt or equity capital each has different benefits and

shortcoming as well and each of the investors in the market have a same access to buy or sell their holdings.

Preposition: 2. With the presence of taxation (Trade-off theory)

The earlier preposition believe that there are no taxes, however, in the real corporate world, companies are require to pay taxes on their

earnings. This theory is termed as trade-off theory, in which, it has been discovered that debt is a cheaper financial source relatively to the cost

of equity. The reason behind this is interest paid on borrowed money is tax deductible, therefore, it provides tax benefits to the TUI Group.

However, such kind of benefits will not be available on equity financing as dividend on equity capital will not give tax advantage to the

4

termed as independent from its capital structure.This proposed prototype is ideal for the organizations which exist in the environment of perfect

competition and product markets.Apart from this basic model of capital structure, other three models for the structuring the base for theoretical

considerations for the organization are discussed subsequently (Hammes y.n.d).

Miller and Modigliani(1958), developed two prepositions to describe the capital structure one is in the absence of capital structure and another

is with the absence of taxation liabilities that are enumerated underneath:

Preposition: 1. In the absence of taxation

In this preposition, it has been believed that changes in capital structure do not influence net value and weighted average cost of capital of

the firm. In other words, change in leverage and mix of debt and equity will not have any effect on firm’s value and cost of capital, thus, capital

structure is irrelevant. As per the theory, TUI can gathered funds either from the use of debt or equity capital each has different benefits and

shortcoming as well and each of the investors in the market have a same access to buy or sell their holdings.

Preposition: 2. With the presence of taxation (Trade-off theory)

The earlier preposition believe that there are no taxes, however, in the real corporate world, companies are require to pay taxes on their

earnings. This theory is termed as trade-off theory, in which, it has been discovered that debt is a cheaper financial source relatively to the cost

of equity. The reason behind this is interest paid on borrowed money is tax deductible, therefore, it provides tax benefits to the TUI Group.

However, such kind of benefits will not be available on equity financing as dividend on equity capital will not give tax advantage to the

4

15058285_P58836_assignment 3

company. Thus, on the basis of this theory, TUI Group must make use of debt capital to a threshold point in their capital structure so as to

reduce the overall cost of capital and rise firm’s value. However, beyond a threshold point, if debt are increase then it gives rises to the equity

capital risk, which in turn, result in higher cost. Therefore, in accordance with the theory, TUI Group must makes use of debt capital to a

specified point in order to reduce WACC and maximize value.

The mode of debt financing is not a straight forward process but annexed with a lot of costs along with the benefits.The firm needs to make a

fine balance between costs and benefits by equalizing both the debt and capital sources through the application of trade off method. Something

is forgone to achieve other thing but the thing that is permitted to forgo should not be in higher value than the benefits so the marginal

difference is the profit that is enjoyed by the company. Hence for the purpose of effective capital structure through the suitable mix of debt and

equity financing, a cost and benefit analysis is also required to maintain for trading off the costs for the benefits and to determine the level of

credit that is manageable by the firm for maximizing the value. If factors like rate of corporate tax, rate of personal tax on equity earning, if

mark-up rates on debt are under level, positive sentiments of market towards debt financing, knowledge from signs of quality of firm, signs

from aggressive competition, accessibility to capital markets at fair value, expense of excess financing, costs of transaction, rights of the

financers, the control mechanism and better skills of negotiations are signals of the benefits of the debt and these factors take the debt to higher

best possible stage. There are other factors which work in opposite direction like personal rate of tax on net revenue, direct financial distress

cost and otherwise, the high rate of mark up on debt, negative sentiments of market toward debt financing, flexibility in knowledge,

accessibility to capital markets at fair price, costs of underfinancing, transaction costs, rights of creditor and competitiveness of the market.

5

company. Thus, on the basis of this theory, TUI Group must make use of debt capital to a threshold point in their capital structure so as to

reduce the overall cost of capital and rise firm’s value. However, beyond a threshold point, if debt are increase then it gives rises to the equity

capital risk, which in turn, result in higher cost. Therefore, in accordance with the theory, TUI Group must makes use of debt capital to a

specified point in order to reduce WACC and maximize value.

The mode of debt financing is not a straight forward process but annexed with a lot of costs along with the benefits.The firm needs to make a

fine balance between costs and benefits by equalizing both the debt and capital sources through the application of trade off method. Something

is forgone to achieve other thing but the thing that is permitted to forgo should not be in higher value than the benefits so the marginal

difference is the profit that is enjoyed by the company. Hence for the purpose of effective capital structure through the suitable mix of debt and

equity financing, a cost and benefit analysis is also required to maintain for trading off the costs for the benefits and to determine the level of

credit that is manageable by the firm for maximizing the value. If factors like rate of corporate tax, rate of personal tax on equity earning, if

mark-up rates on debt are under level, positive sentiments of market towards debt financing, knowledge from signs of quality of firm, signs

from aggressive competition, accessibility to capital markets at fair value, expense of excess financing, costs of transaction, rights of the

financers, the control mechanism and better skills of negotiations are signals of the benefits of the debt and these factors take the debt to higher

best possible stage. There are other factors which work in opposite direction like personal rate of tax on net revenue, direct financial distress

cost and otherwise, the high rate of mark up on debt, negative sentiments of market toward debt financing, flexibility in knowledge,

accessibility to capital markets at fair price, costs of underfinancing, transaction costs, rights of creditor and competitiveness of the market.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

15058285_P58836_assignment 3

These factors show themselves as the cost of debt and they are contributing factor in declining the best possible stage (Serveas and Tofano

2006)

Pecking Order Theory

According to this theory, the organization does not set any particular amount of debt in conscious but relies solely on the outcome of

profitability of the organization. This theory suggests that companies can raise money from three sources, that are retained profit, equity

financing and debt financing (Serveas and Tofano 2006). It is one of the most influential theory of corporate leverage that demonstrates that

availability of asymmetric information to the managers affects the selection of internal and external financing. It believes that retained earnings

is the most effective source of finance because it is available at nil financial cost and have no adverse impact. While, if they need to raise money

through external finance, then debt gains preference over equity because share capital is more riskier and costlier because of higher premium.

The reason behind this is debt interest is fixed and also give tax benefits, whereas, external investors need higher return in return for the risk

undertaken. Thus, it can be said that firms often prefer internal financing, if require more funds, then debt will be issued first and then rest of the

funds will be collected by equity capital (Serveas and Tofano 2006).

Agency costs

Agency costs theories of finance takes their origination from basic principle of partnership and agent-principal relation. Principal under this

scenario is shareholder and members of management work as agents of the principal to function in the favour of shareholder and organization

6

These factors show themselves as the cost of debt and they are contributing factor in declining the best possible stage (Serveas and Tofano

2006)

Pecking Order Theory

According to this theory, the organization does not set any particular amount of debt in conscious but relies solely on the outcome of

profitability of the organization. This theory suggests that companies can raise money from three sources, that are retained profit, equity

financing and debt financing (Serveas and Tofano 2006). It is one of the most influential theory of corporate leverage that demonstrates that

availability of asymmetric information to the managers affects the selection of internal and external financing. It believes that retained earnings

is the most effective source of finance because it is available at nil financial cost and have no adverse impact. While, if they need to raise money

through external finance, then debt gains preference over equity because share capital is more riskier and costlier because of higher premium.

The reason behind this is debt interest is fixed and also give tax benefits, whereas, external investors need higher return in return for the risk

undertaken. Thus, it can be said that firms often prefer internal financing, if require more funds, then debt will be issued first and then rest of the

funds will be collected by equity capital (Serveas and Tofano 2006).

Agency costs

Agency costs theories of finance takes their origination from basic principle of partnership and agent-principal relation. Principal under this

scenario is shareholder and members of management work as agents of the principal to function in the favour of shareholder and organization

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

15058285_P58836_assignment 3

by conduct of best practices. However, due to occurrence of asymmetric and imperfect level of comprehension and medium of transfer that

knowledge, the control of outcome and resultant factors are beyond the capacity of the management sometimes same is the case with decisions

which are taken by the management. As per agency cost theory, shareholders do not necessarily desire a high level of variation and hence they

raise the debt level of the company. Therefore, they reduce the FCFF (Free cash flow for the firm) which is available to managers who are self-

motivatedfor fund provision in variation programs which are not profitable(Jstor.org, 2016).

This theory says that agency costs arises when managers of the firm owns a proportion of total share capital. As a result, they can work in

the interest of stakeholders. This theory proposes that indebtedness can be considered as a way to resolve conflicts between both the managers

and shareholders. The theory indicates that indebtedness gives rises to three type of costs that are control and justification, higher risk and

bankruptcy as well. Thus optimal capital structure gives huge assistance to the firm to minimize agency cost and to appeal for external funds to

meet out long-term capital requirement.

TUI’s Structure of Capital

The capital structure of TUI is dependent on several factors namely size of the firm, CVA, earnings volatility, profitability, growth

opportunities, energy extremity, framework of ownership, rated vs. non-rated, less cost against service and leasing characteristics. With respect

to size of the firm, TUI is considered as one of the greatest because of the widespread huge size and number of employees as well as area of

management. The greater the size, theless capacities and abilities ofearnings due to meeting up the mass administrative and operational cost. As

per Wessel and Titman (1988) the size of the company stimulates the revenue capacity of that company. TUI Group follows trade-off theory, in

7

by conduct of best practices. However, due to occurrence of asymmetric and imperfect level of comprehension and medium of transfer that

knowledge, the control of outcome and resultant factors are beyond the capacity of the management sometimes same is the case with decisions

which are taken by the management. As per agency cost theory, shareholders do not necessarily desire a high level of variation and hence they

raise the debt level of the company. Therefore, they reduce the FCFF (Free cash flow for the firm) which is available to managers who are self-

motivatedfor fund provision in variation programs which are not profitable(Jstor.org, 2016).

This theory says that agency costs arises when managers of the firm owns a proportion of total share capital. As a result, they can work in

the interest of stakeholders. This theory proposes that indebtedness can be considered as a way to resolve conflicts between both the managers

and shareholders. The theory indicates that indebtedness gives rises to three type of costs that are control and justification, higher risk and

bankruptcy as well. Thus optimal capital structure gives huge assistance to the firm to minimize agency cost and to appeal for external funds to

meet out long-term capital requirement.

TUI’s Structure of Capital

The capital structure of TUI is dependent on several factors namely size of the firm, CVA, earnings volatility, profitability, growth

opportunities, energy extremity, framework of ownership, rated vs. non-rated, less cost against service and leasing characteristics. With respect

to size of the firm, TUI is considered as one of the greatest because of the widespread huge size and number of employees as well as area of

management. The greater the size, theless capacities and abilities ofearnings due to meeting up the mass administrative and operational cost. As

per Wessel and Titman (1988) the size of the company stimulates the revenue capacity of that company. TUI Group follows trade-off theory, in

7

15058285_P58836_assignment 3

which, it makes use of both equity as well as debt capital to meet out their long-term capital. Debt is utilized by the firm to get taxation benefits

and trading on equity so as to maximize their return for the investors (TUI’s annual financial reports, 2015)

). Moreover, another reason for debt utilization is it does not transfer rights to the debt holders, however, equity holders have right to control

decisions. On the basis of it, it can be said that Trade off theory is following by TUI Company. But still, it must be noted that the proportion of

debt in TUI’s long-term capital is still less than equity because it brings excessive financial burden to the firm as they are legally liable to pay

fixed interest obligations as per debt covenants. Optimum mix of debt and equity assists TUI group to manage their financial risk and solvency

position as well to repay long-term liabilities on right time.

The All other variables by keeping under consideration can be stated the Trade-off theory is appropriate for application and development

the capital structure of TUI Company. trade-off theory is applicable here because the size has played a significant role in the development and

expansion of the company worldwide. If we evaluate other afore mentioned factors as well under the light of trade off theory, we get results as

positive relationship with CVA, positive relationship with level of profitability, negative relationship with revenue volatility, negative

relationship with growth opportunities, negative relationship with energy extremity, positive relationship with structure of ownership, positive

relationship with rated vs. non-rated, positive as well as negative relationship with less cost vs. service and positive relationship with leasing.

The same connections and states of relationships have been observed in the case of TUI Company

TUI Group’s capital structure or gearing

8

which, it makes use of both equity as well as debt capital to meet out their long-term capital. Debt is utilized by the firm to get taxation benefits

and trading on equity so as to maximize their return for the investors (TUI’s annual financial reports, 2015)

). Moreover, another reason for debt utilization is it does not transfer rights to the debt holders, however, equity holders have right to control

decisions. On the basis of it, it can be said that Trade off theory is following by TUI Company. But still, it must be noted that the proportion of

debt in TUI’s long-term capital is still less than equity because it brings excessive financial burden to the firm as they are legally liable to pay

fixed interest obligations as per debt covenants. Optimum mix of debt and equity assists TUI group to manage their financial risk and solvency

position as well to repay long-term liabilities on right time.

The All other variables by keeping under consideration can be stated the Trade-off theory is appropriate for application and development

the capital structure of TUI Company. trade-off theory is applicable here because the size has played a significant role in the development and

expansion of the company worldwide. If we evaluate other afore mentioned factors as well under the light of trade off theory, we get results as

positive relationship with CVA, positive relationship with level of profitability, negative relationship with revenue volatility, negative

relationship with growth opportunities, negative relationship with energy extremity, positive relationship with structure of ownership, positive

relationship with rated vs. non-rated, positive as well as negative relationship with less cost vs. service and positive relationship with leasing.

The same connections and states of relationships have been observed in the case of TUI Company

TUI Group’s capital structure or gearing

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

15058285_P58836_assignment 3

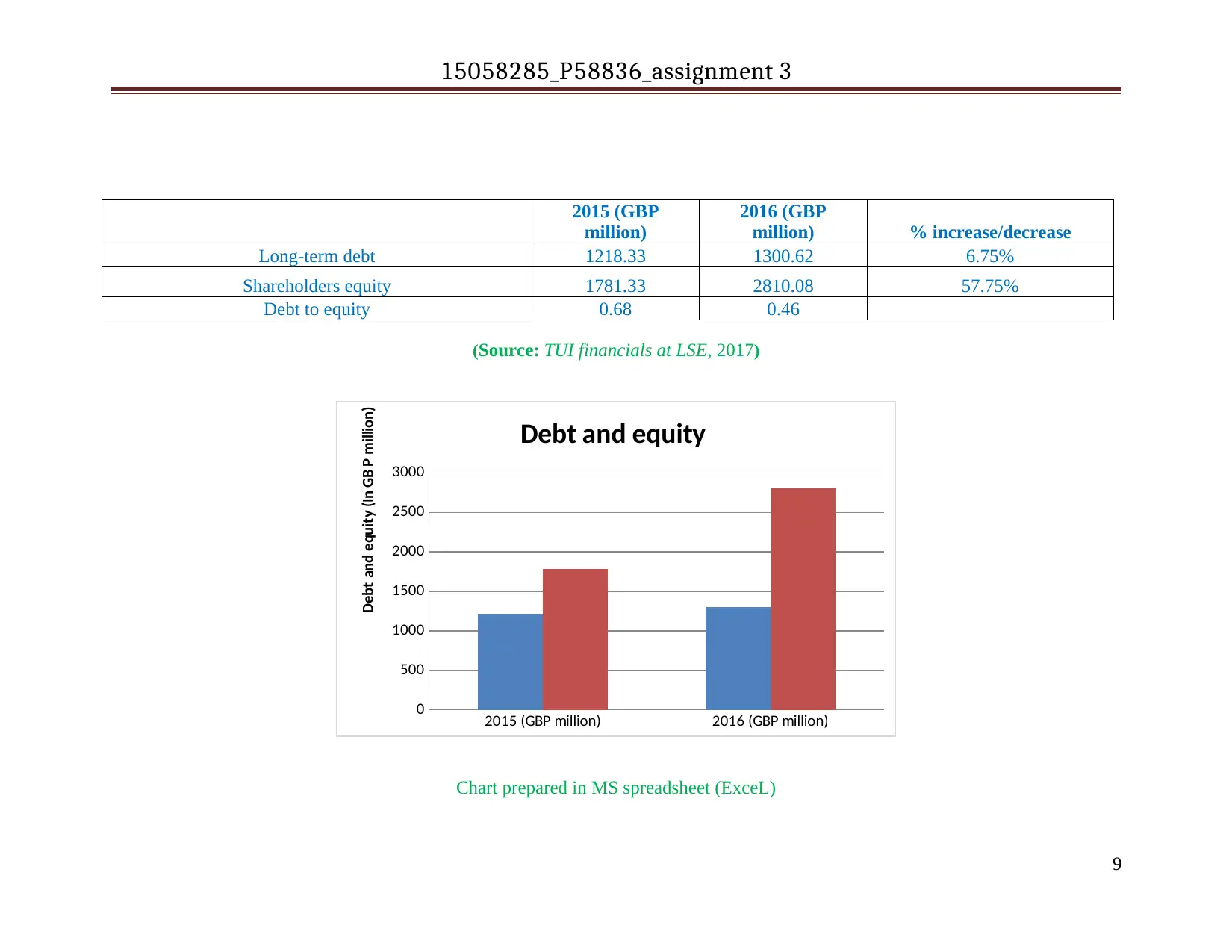

2015 (GBP

million)

2016 (GBP

million) % increase/decrease

Long-term debt 1218.33 1300.62 6.75%

Shareholders equity 1781.33 2810.08 57.75%

Debt to equity 0.68 0.46

(Source: TUI financials at LSE, 2017)

2015 (GBP million) 2016 (GBP million)

0

500

1000

1500

2000

2500

3000

Debt and equity

Debt and equity (In GB P million)

Chart prepared in MS spreadsheet (ExceL)

9

2015 (GBP

million)

2016 (GBP

million) % increase/decrease

Long-term debt 1218.33 1300.62 6.75%

Shareholders equity 1781.33 2810.08 57.75%

Debt to equity 0.68 0.46

(Source: TUI financials at LSE, 2017)

2015 (GBP million) 2016 (GBP million)

0

500

1000

1500

2000

2500

3000

Debt and equity

Debt and equity (In GB P million)

Chart prepared in MS spreadsheet (ExceL)

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

15058285_P58836_assignment 3

Important highlights:

Taking into consideration the results, it can be seen that in 2016, TUI Group enhanced its debt from 1218.33 to 1300.62 GBP million

by 6.75%. However, excessive additional capital requirement has been fulfilled by issuing more share capital. As in 2016, it has been increased

from 1781.33 to 2810.08 by 57.75% resulted in declined gearing or leverage from 0.68:1 to 0.46:1 indicates lower financial risk. But still, it is

a little bit far away from the ideal ratio of debt to equity of 0.5:1 (TUI financials at LSE, 2017). Thus, on the basis of this, it can be suggested

to the firm to raise additional money through taking external borrowings via debt capital to get more tax benefits and improved solvency.

Moreover, it will also drive benefits of Trading On Equity (TOE), under this TUI Group can use debt to raise earnings for the equity

shareholders and satisfy them.

2. TUI’s market evaluation

A. Weighted Average Cost of Capital for TUI

The economic goal of the company as a market driven securities based organization is to make certain a sustainable and balanced

rise in the worth of the group as a whole.The standardized and benchmark level administration system has been formulated for

implementation of value- recognized management over the venture as a complete as well as separate sectors of the ventures. WACC

refers to the rate which TUI Group will be require to pay to their fund providers to finance their assets, also termed as cost of capital

(Tripathi, 2017). It is calculated by taking into account both the cost of debt as well as equity capital by using following formulas:

10

Important highlights:

Taking into consideration the results, it can be seen that in 2016, TUI Group enhanced its debt from 1218.33 to 1300.62 GBP million

by 6.75%. However, excessive additional capital requirement has been fulfilled by issuing more share capital. As in 2016, it has been increased

from 1781.33 to 2810.08 by 57.75% resulted in declined gearing or leverage from 0.68:1 to 0.46:1 indicates lower financial risk. But still, it is

a little bit far away from the ideal ratio of debt to equity of 0.5:1 (TUI financials at LSE, 2017). Thus, on the basis of this, it can be suggested

to the firm to raise additional money through taking external borrowings via debt capital to get more tax benefits and improved solvency.

Moreover, it will also drive benefits of Trading On Equity (TOE), under this TUI Group can use debt to raise earnings for the equity

shareholders and satisfy them.

2. TUI’s market evaluation

A. Weighted Average Cost of Capital for TUI

The economic goal of the company as a market driven securities based organization is to make certain a sustainable and balanced

rise in the worth of the group as a whole.The standardized and benchmark level administration system has been formulated for

implementation of value- recognized management over the venture as a complete as well as separate sectors of the ventures. WACC

refers to the rate which TUI Group will be require to pay to their fund providers to finance their assets, also termed as cost of capital

(Tripathi, 2017). It is calculated by taking into account both the cost of debt as well as equity capital by using following formulas:

10

15058285_P58836_assignment 3

WACC = (equity/value*Ke) + [Debt/value*Kd(1-Tax rates)

Higher the WACC gives rises to the risk and decrease in corporate value or vice-versa.

The company uses ROIC and absolute value added approaches for value analysis of the project. The company compares

ROIC with sector specific cost of capital. The company applies EBITA approach for monitor of the economic performance along

with various variables of the Group. The company has achieved a sustainability in fuel consumption and carbon emission as far as

their air craft segment of the venture is considered.

Calculation of cost of equity as per dividend growth model:

Cost of equity is the required rate of return that TUI Trvael group will be require to pay to their equity investors as a monetary

return for the risk borne. As per dividend growth model, cost of equity can be computed by taking into accont the dividend rate and

market price of the share plus expected rate of growth in dividend (Heinrichs and et.al., 2013). Henceforth, it can be writeen as

follows:

Cost of equity (Ke) = (Current dividend/market price)+Growth rate in dividend

Where;

11

WACC = (equity/value*Ke) + [Debt/value*Kd(1-Tax rates)

Higher the WACC gives rises to the risk and decrease in corporate value or vice-versa.

The company uses ROIC and absolute value added approaches for value analysis of the project. The company compares

ROIC with sector specific cost of capital. The company applies EBITA approach for monitor of the economic performance along

with various variables of the Group. The company has achieved a sustainability in fuel consumption and carbon emission as far as

their air craft segment of the venture is considered.

Calculation of cost of equity as per dividend growth model:

Cost of equity is the required rate of return that TUI Trvael group will be require to pay to their equity investors as a monetary

return for the risk borne. As per dividend growth model, cost of equity can be computed by taking into accont the dividend rate and

market price of the share plus expected rate of growth in dividend (Heinrichs and et.al., 2013). Henceforth, it can be writeen as

follows:

Cost of equity (Ke) = (Current dividend/market price)+Growth rate in dividend

Where;

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 32

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.