Advanced Financial Accounting Assignment: Tutt Bryant Group Analysis

VerifiedAdded on 2020/05/16

|17

|2908

|51

Report

AI Summary

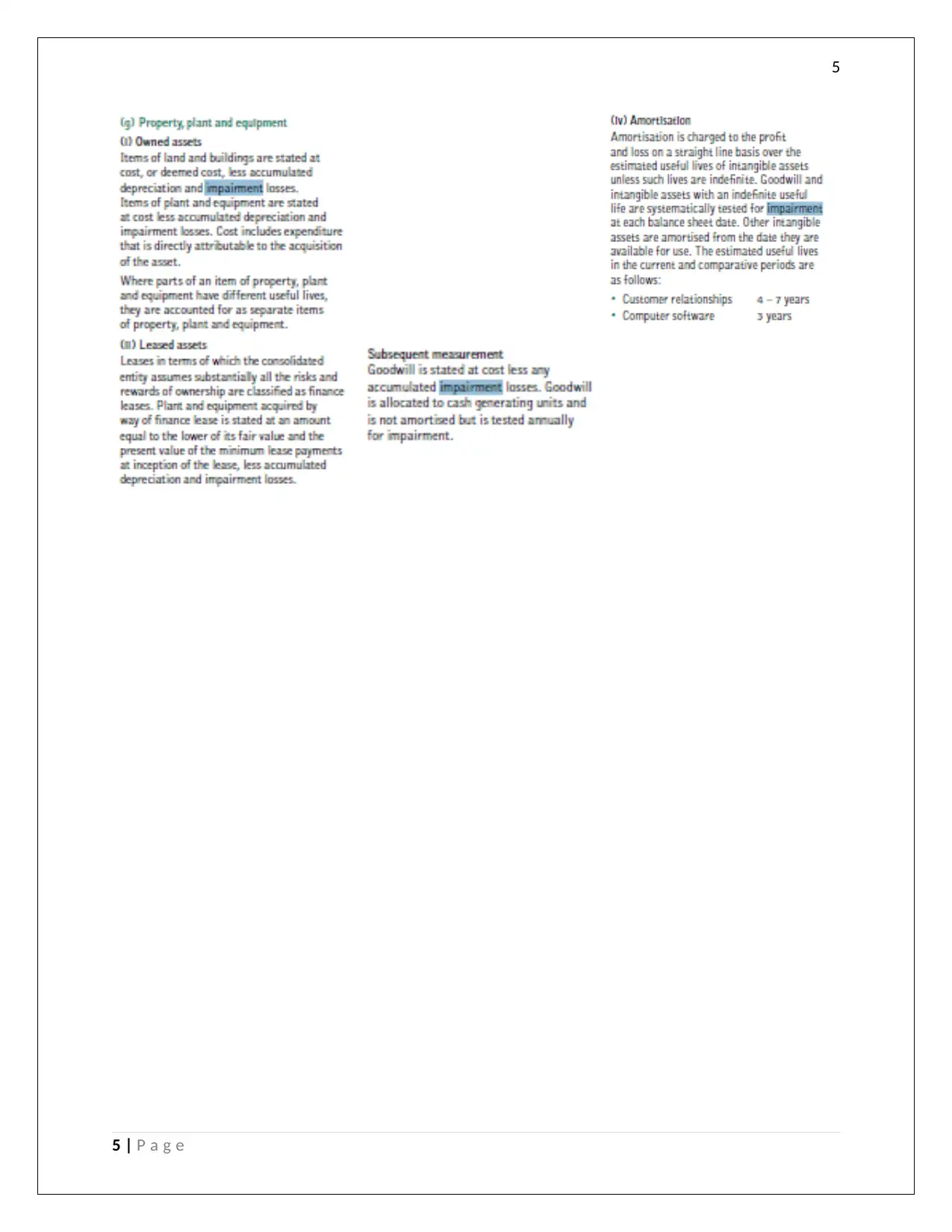

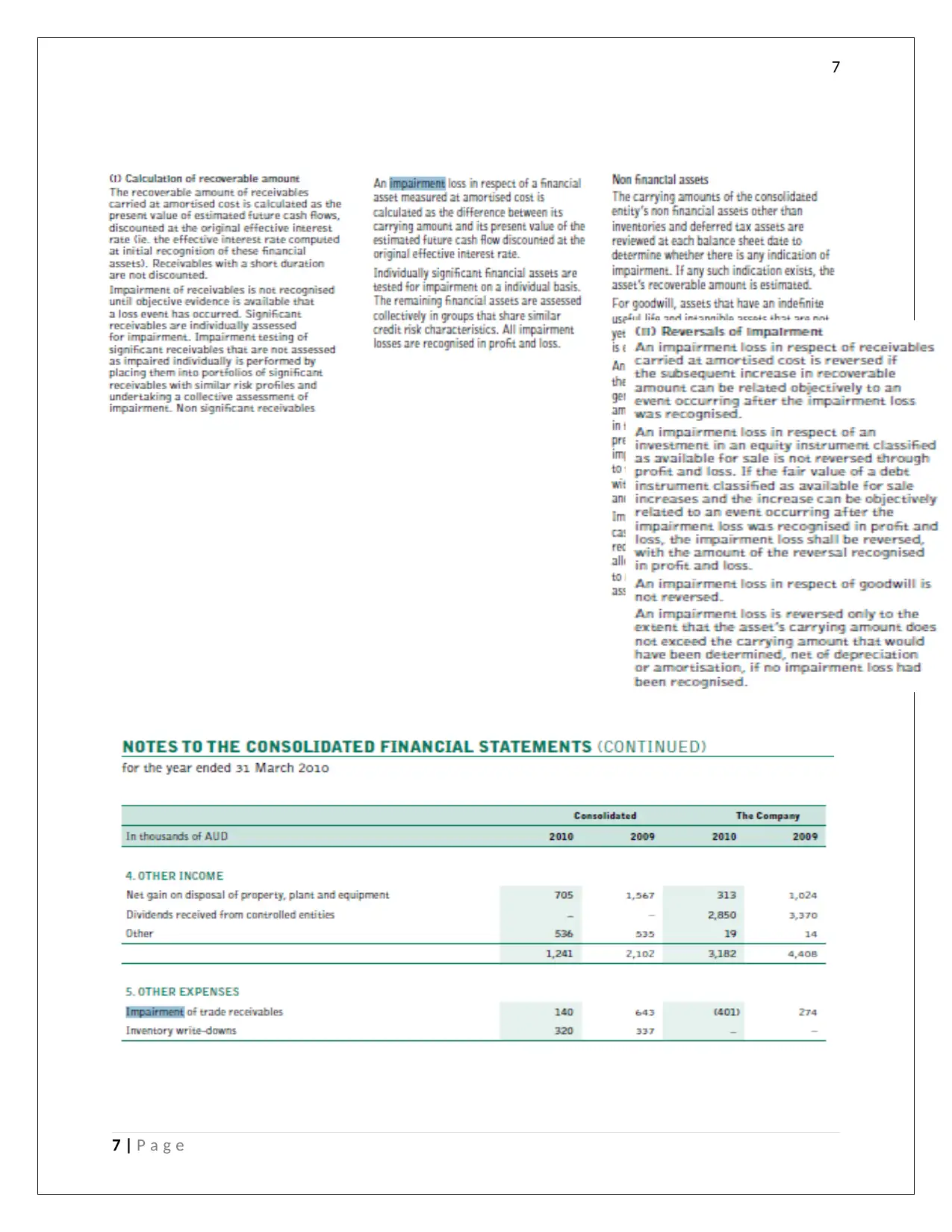

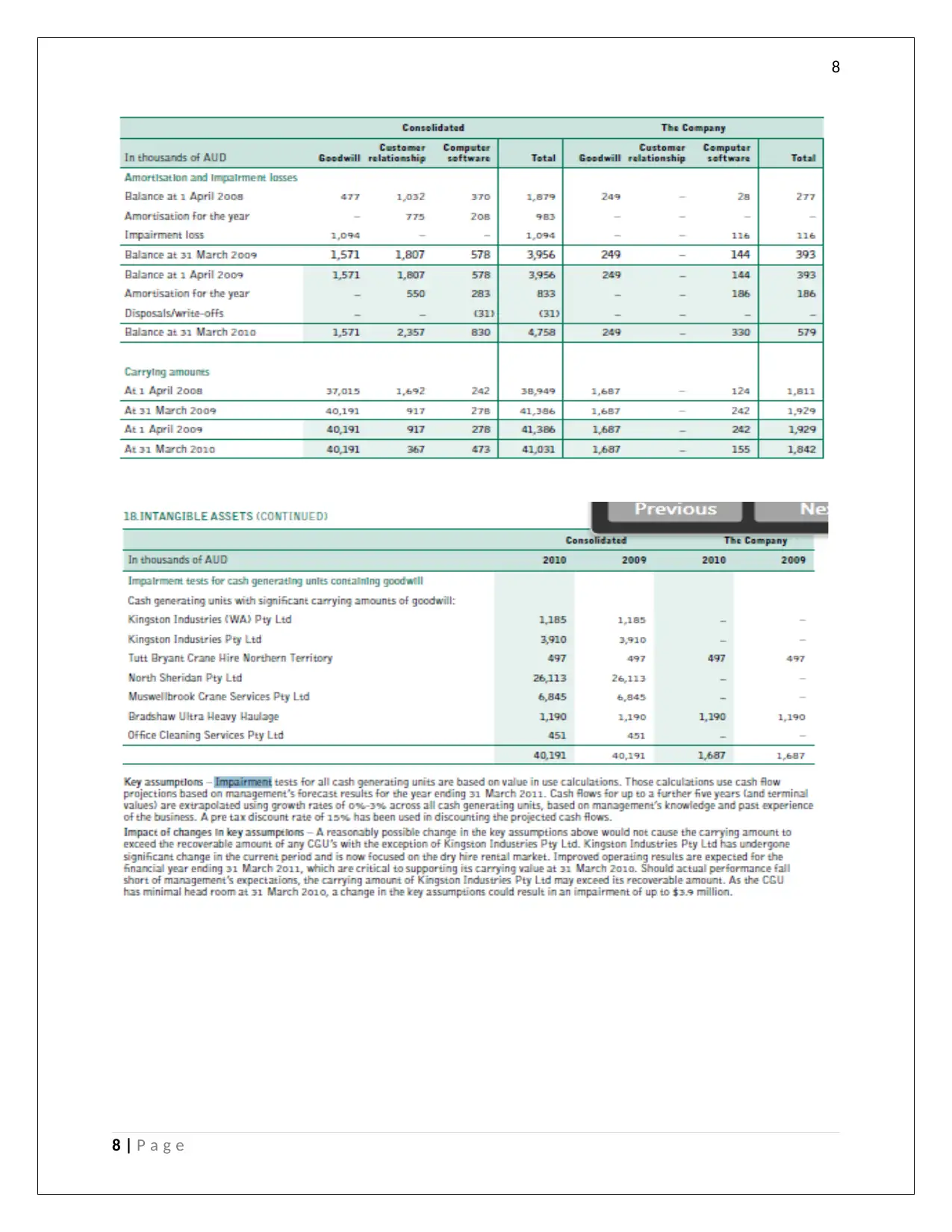

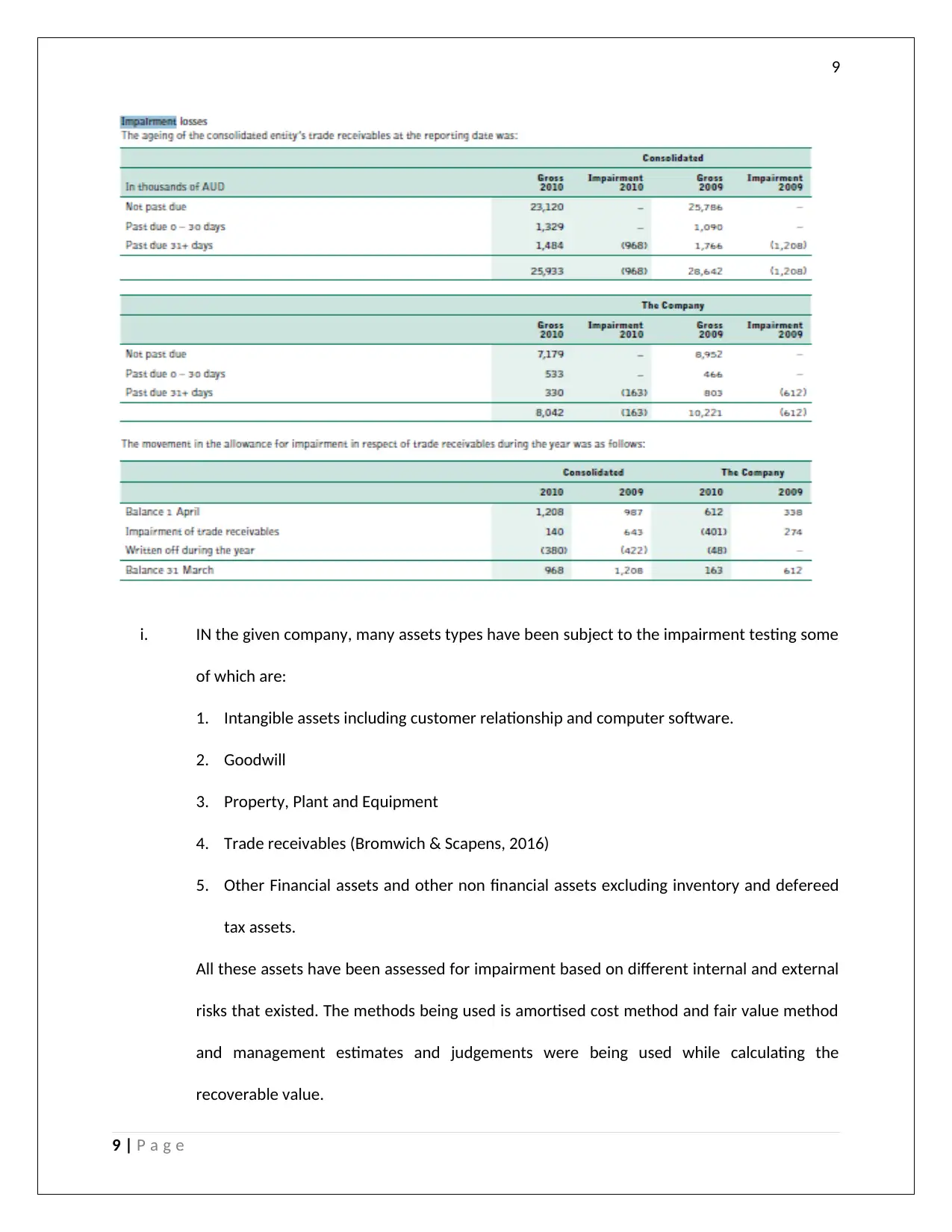

This report provides a comprehensive analysis of the 2010 financial statements of Tutt Bryant Group Limited, focusing on impairment disclosures and accounting practices. The report examines the company's approach to impairment testing, including the methods used, such as amortized cost and fair value, and the various internal and external factors considered. It also delves into the subjectivity involved in management's estimates and assumptions, particularly concerning intangible assets and the application of IAS 36. Furthermore, the report compares the old and new leasing standards, highlighting how the new standard addresses the shortcomings of the previous one by increasing transparency and providing a more accurate reflection of a company's liabilities, especially regarding operating leases. The analysis also discusses the benefits of the new standard for investors and the impact on financial statement comparability.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.