Uber Valuation: Financial Analysis for FN 4535 Module

VerifiedAdded on 2022/09/11

|11

|669

|13

Project

AI Summary

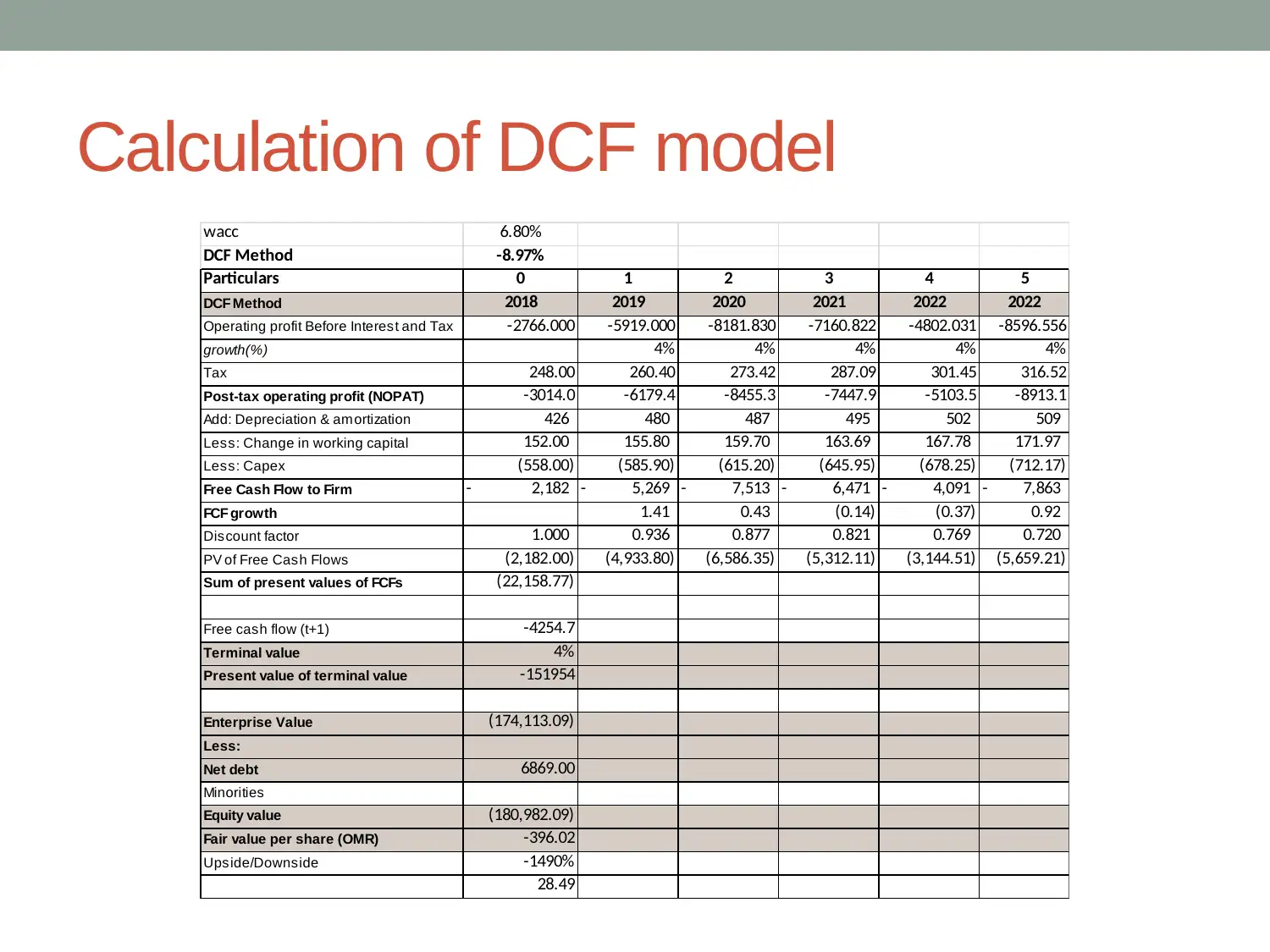

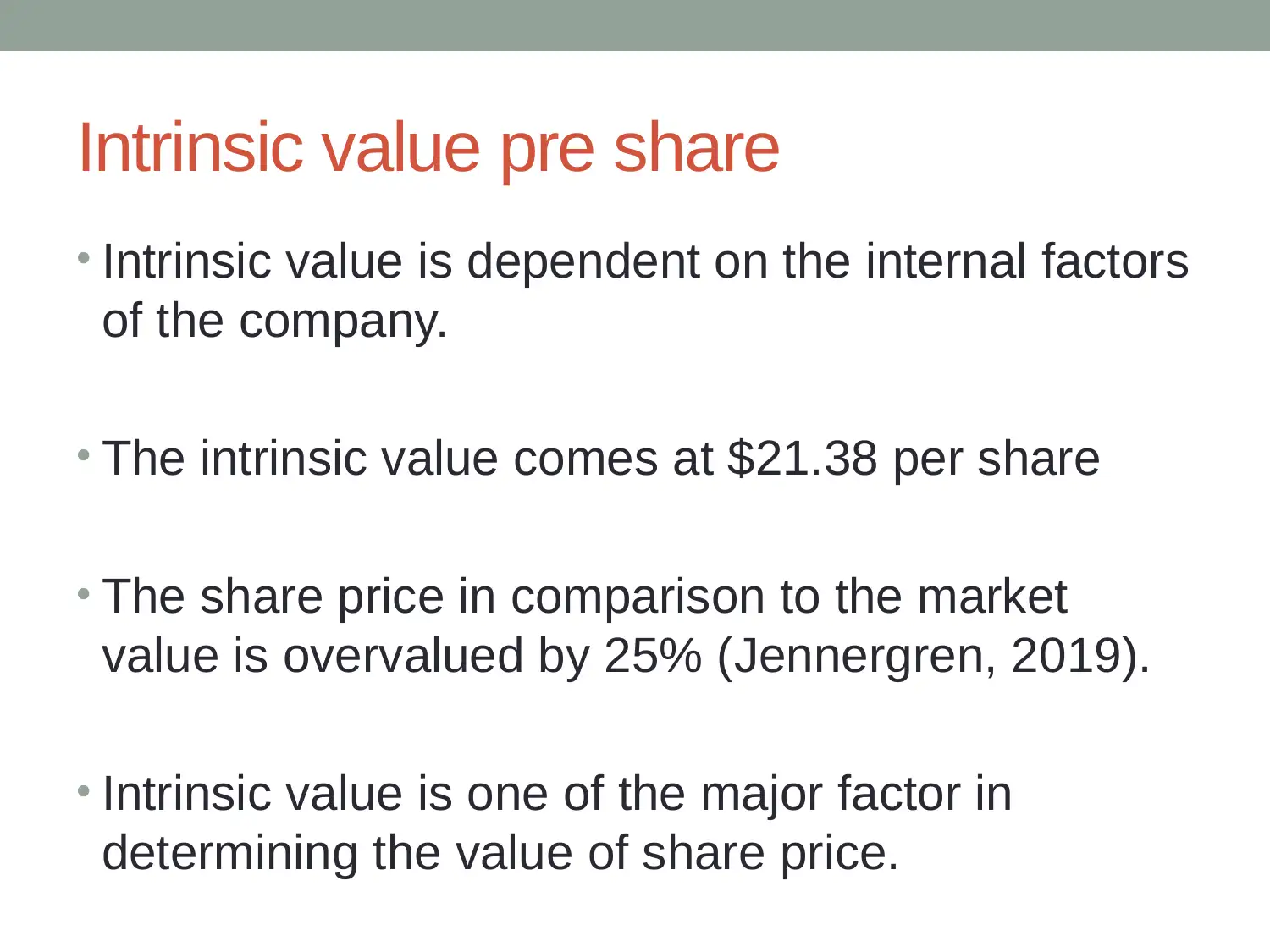

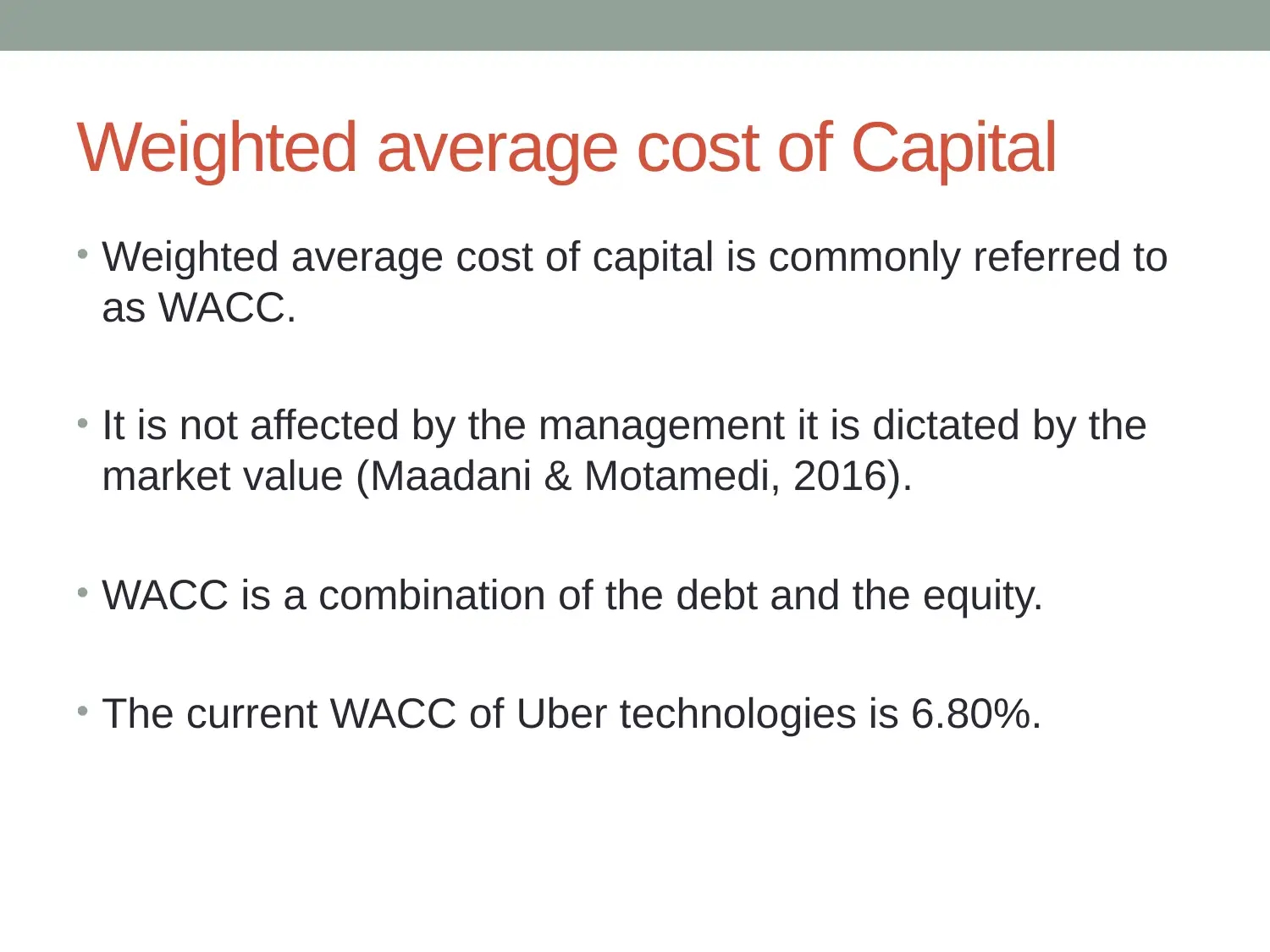

This project provides a comprehensive valuation analysis of Uber Technologies, employing a Discounted Cash Flow (DCF) model to determine its intrinsic value. The analysis utilizes historical data from Bloomberg to forecast future growth and profitability, including a 4% growth rate and adjustments for depreciation and capital expenditures. The DCF model calculates the present value and terminal value to arrive at free cash flows. The rationale behind using DCF is its effectiveness in valuing large, established firms and verifying share price characteristics, as other methods are deemed less reliable. The project calculates an intrinsic value of $21.38 per share, which is then compared to the market value, revealing a 25% overvaluation. The project also examines the historical beta coefficient as a risk measure and the Weighted Average Cost of Capital (WACC), which is calculated to be 6.80%. Sensitivity analysis is conducted using growth rate and WACC as variables. The conclusion suggests the DCF model is effective in identifying the intrinsic value but indicates that Uber's shares are overvalued based on the analysis. The project includes references to relevant academic papers and financial data sources to support its findings.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.