Management Accounting Report: UCK Furniture - Cost Analysis Techniques

VerifiedAdded on 2020/06/04

|12

|2958

|36

Report

AI Summary

This report provides a detailed analysis of management accounting techniques, focusing on cost analysis and financial reporting within the context of UCK Furniture. It explores the application of marginal and absorption costing methods for income statement formulation, comparing their advantages and disadvantages. The report also examines budgetary control, outlining various planning tools and their effectiveness, along with the estimation of expenses based on activity levels and the preparation of a cash budget. Furthermore, it delves into the application of different management accounting systems to address financial issues, including Key Performance Indicators (KPIs), financial governance, and benchmarking. The report concludes with an assessment of how these systems contribute to improving financial performance, supported by financial ratios and performance metrics of UCK Furniture and UCK Woodwork's.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Application of cost analysis techniques for formulation of income statement.....................1

1.2 Application of management accounting techniques regarding financial reporting ..............3

1.3 Advantages and disadvantages of Marginal and Absorption costing...................................3

TASK 2............................................................................................................................................4

2.1 Advantages and disadvantages of different planning tools used for budgetary control.......4

2.2 Estimation of expenses if change in number of hours..........................................................5

2.3 Preparation of cash budget....................................................................................................5

TASK 3............................................................................................................................................6

3.1 Application of different management accounting systems to respond financial issues .......6

3.2 Contribution of management accounting to improve financial performance.......................8

3.3 Application of planning tools to reduce financial issues to achieve success........................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

.........................................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Application of cost analysis techniques for formulation of income statement.....................1

1.2 Application of management accounting techniques regarding financial reporting ..............3

1.3 Advantages and disadvantages of Marginal and Absorption costing...................................3

TASK 2............................................................................................................................................4

2.1 Advantages and disadvantages of different planning tools used for budgetary control.......4

2.2 Estimation of expenses if change in number of hours..........................................................5

2.3 Preparation of cash budget....................................................................................................5

TASK 3............................................................................................................................................6

3.1 Application of different management accounting systems to respond financial issues .......6

3.2 Contribution of management accounting to improve financial performance.......................8

3.3 Application of planning tools to reduce financial issues to achieve success........................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

.........................................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting includes the use of different cost techniques like Marginal and

Absorption for preparation of income statement. Marginal costing method helps in ascertainment

of cost which is considered most important for decision making. Absorption costing provides the

information regarding total manufacturing cost including fixed and variable. It is considered as

important profession which includes devise planning and performance management systems

which helps in control and formulation of organisational strategies. UCK Furniture deals in the

manufacturing of Table and Drawer division (Chiwamit, Modell and Yang, 2014).

In the present report explain about, advantages and disadvantage of planning tools used

for budgetary control, application of marginal and absorption costing for formulation of income

statement. Also, adaptation of different management accounting systems to respond financial

problems.

TASK 1

1.1 Application of cost analysis techniques for formulation of income statement

Cost: It is an amount which is given up by organisation to attain something new. It is an

monetary evaluation of efforts, resources, material, risk, time and utilities etc. It can be of

different kind which is defined below:

Fixed and variable costs: Fixed cost remains constant and never fluctuates with change

in level of output. But per unit fixed cost is diminished with the increase in level of production.

It includes rent and depreciation. On other hand, variable cost changes with the variation in level

of production. This cost has direct relation with production. It includes raw material, labour etc.

Opportunity and outlay costs: Outlay costs are also called as actual cost which is

incurred by organisation for machinery, material etc. Such costs are calculated on the basis of

accounting cost concept. Opportunity cost is the cost in terms of revenue which is foregone while

selecting next best alternative foregone.

Difference between Marginal and Absorption costing

Marginal costing: This method helps in calculation of increase in total cost due to

change in the level of output by one unit. This technique only consider variable cost while

calculating total cost of production. Important characteristics of marginal costing are mentioned

below:

1

Management accounting includes the use of different cost techniques like Marginal and

Absorption for preparation of income statement. Marginal costing method helps in ascertainment

of cost which is considered most important for decision making. Absorption costing provides the

information regarding total manufacturing cost including fixed and variable. It is considered as

important profession which includes devise planning and performance management systems

which helps in control and formulation of organisational strategies. UCK Furniture deals in the

manufacturing of Table and Drawer division (Chiwamit, Modell and Yang, 2014).

In the present report explain about, advantages and disadvantage of planning tools used

for budgetary control, application of marginal and absorption costing for formulation of income

statement. Also, adaptation of different management accounting systems to respond financial

problems.

TASK 1

1.1 Application of cost analysis techniques for formulation of income statement

Cost: It is an amount which is given up by organisation to attain something new. It is an

monetary evaluation of efforts, resources, material, risk, time and utilities etc. It can be of

different kind which is defined below:

Fixed and variable costs: Fixed cost remains constant and never fluctuates with change

in level of output. But per unit fixed cost is diminished with the increase in level of production.

It includes rent and depreciation. On other hand, variable cost changes with the variation in level

of production. This cost has direct relation with production. It includes raw material, labour etc.

Opportunity and outlay costs: Outlay costs are also called as actual cost which is

incurred by organisation for machinery, material etc. Such costs are calculated on the basis of

accounting cost concept. Opportunity cost is the cost in terms of revenue which is foregone while

selecting next best alternative foregone.

Difference between Marginal and Absorption costing

Marginal costing: This method helps in calculation of increase in total cost due to

change in the level of output by one unit. This technique only consider variable cost while

calculating total cost of production. Important characteristics of marginal costing are mentioned

below:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

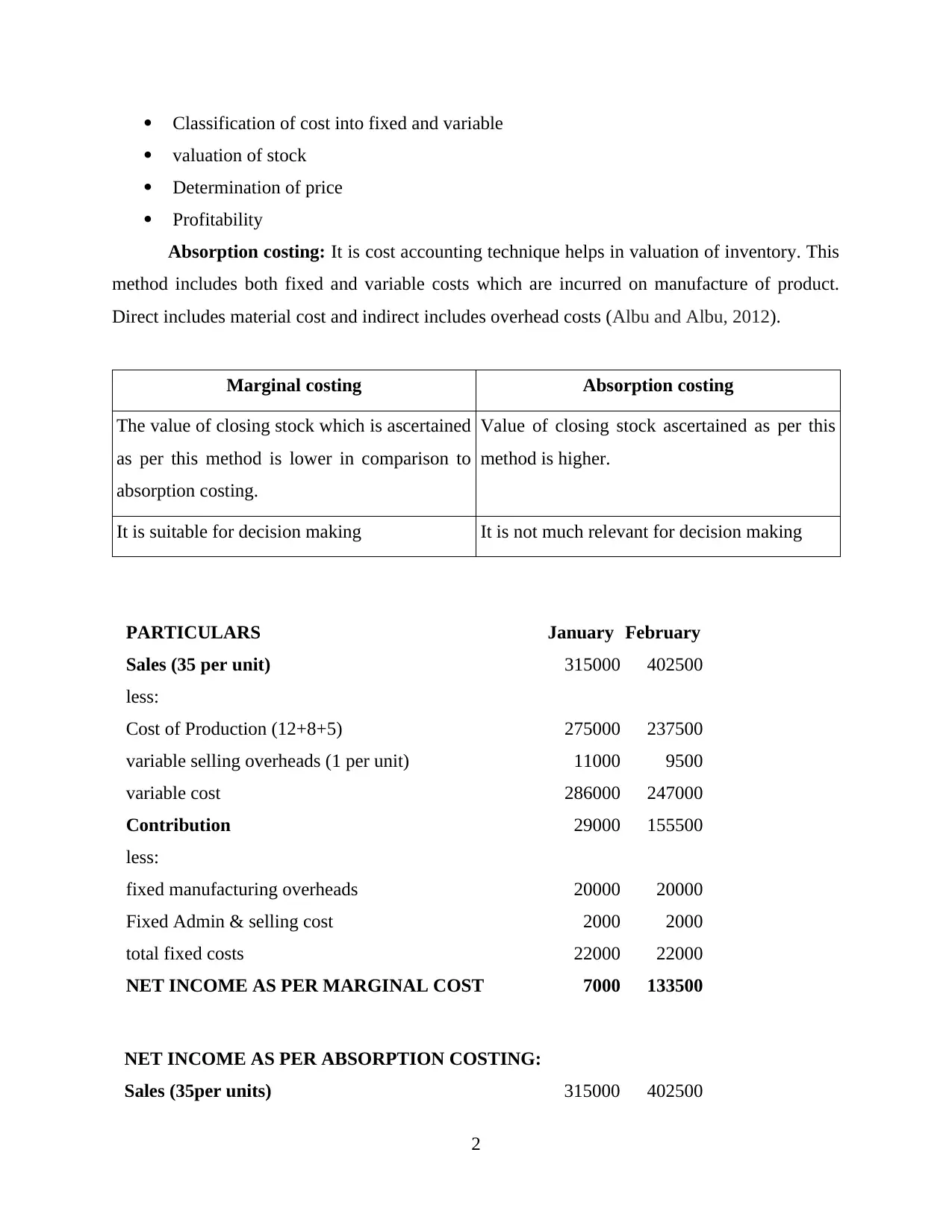

Classification of cost into fixed and variable

valuation of stock

Determination of price

Profitability

Absorption costing: It is cost accounting technique helps in valuation of inventory. This

method includes both fixed and variable costs which are incurred on manufacture of product.

Direct includes material cost and indirect includes overhead costs (Albu and Albu, 2012).

Marginal costing Absorption costing

The value of closing stock which is ascertained

as per this method is lower in comparison to

absorption costing.

Value of closing stock ascertained as per this

method is higher.

It is suitable for decision making It is not much relevant for decision making

PARTICULARS January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

less:

fixed manufacturing overheads 20000 20000

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

NET INCOME AS PER ABSORPTION COSTING:

Sales (35per units) 315000 402500

2

valuation of stock

Determination of price

Profitability

Absorption costing: It is cost accounting technique helps in valuation of inventory. This

method includes both fixed and variable costs which are incurred on manufacture of product.

Direct includes material cost and indirect includes overhead costs (Albu and Albu, 2012).

Marginal costing Absorption costing

The value of closing stock which is ascertained

as per this method is lower in comparison to

absorption costing.

Value of closing stock ascertained as per this

method is higher.

It is suitable for decision making It is not much relevant for decision making

PARTICULARS January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

less:

fixed manufacturing overheads 20000 20000

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

NET INCOME AS PER ABSORPTION COSTING:

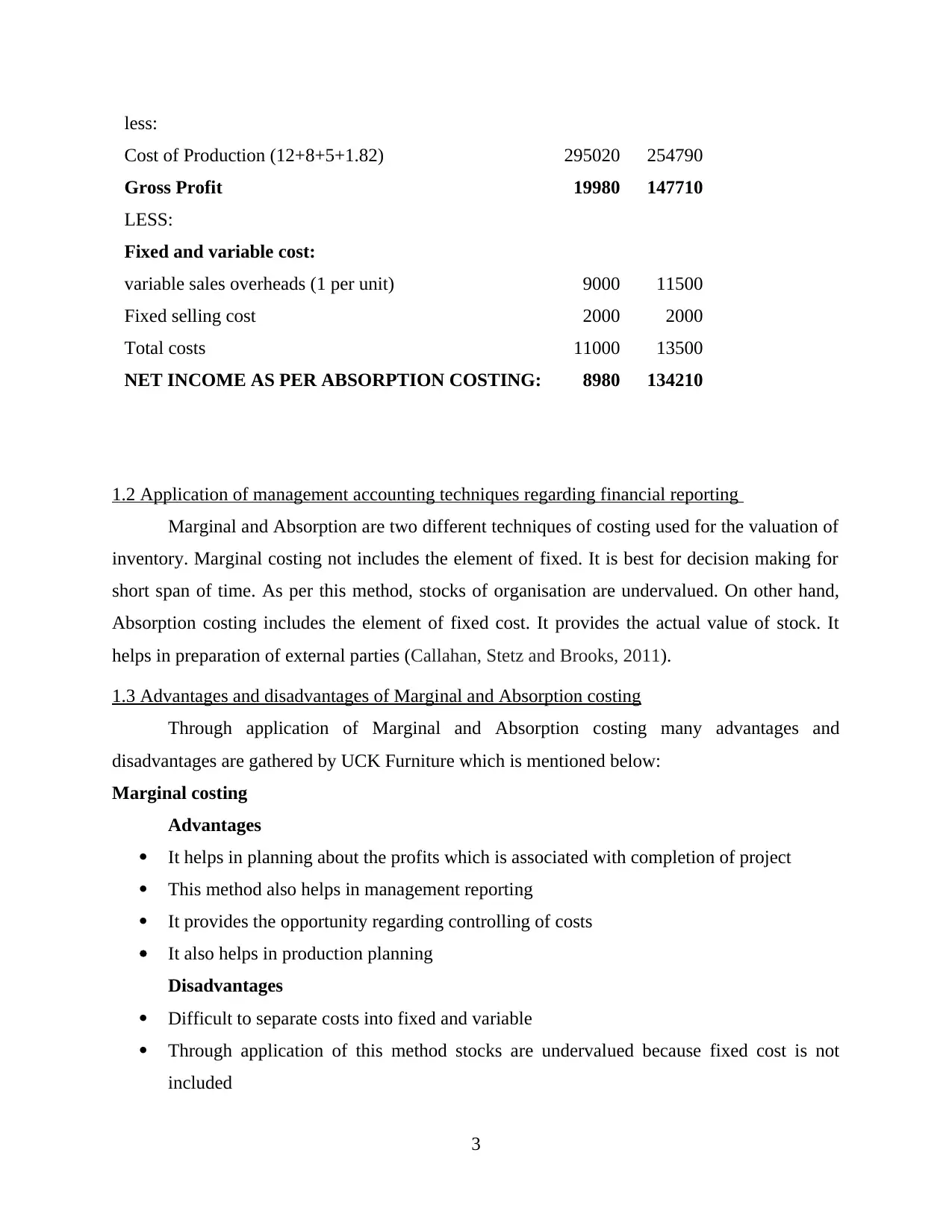

Sales (35per units) 315000 402500

2

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

NET INCOME AS PER ABSORPTION COSTING: 8980 134210

1.2 Application of management accounting techniques regarding financial reporting

Marginal and Absorption are two different techniques of costing used for the valuation of

inventory. Marginal costing not includes the element of fixed. It is best for decision making for

short span of time. As per this method, stocks of organisation are undervalued. On other hand,

Absorption costing includes the element of fixed cost. It provides the actual value of stock. It

helps in preparation of external parties (Callahan, Stetz and Brooks, 2011).

1.3 Advantages and disadvantages of Marginal and Absorption costing

Through application of Marginal and Absorption costing many advantages and

disadvantages are gathered by UCK Furniture which is mentioned below:

Marginal costing

Advantages

It helps in planning about the profits which is associated with completion of project

This method also helps in management reporting

It provides the opportunity regarding controlling of costs

It also helps in production planning

Disadvantages

Difficult to separate costs into fixed and variable

Through application of this method stocks are undervalued because fixed cost is not

included

3

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

NET INCOME AS PER ABSORPTION COSTING: 8980 134210

1.2 Application of management accounting techniques regarding financial reporting

Marginal and Absorption are two different techniques of costing used for the valuation of

inventory. Marginal costing not includes the element of fixed. It is best for decision making for

short span of time. As per this method, stocks of organisation are undervalued. On other hand,

Absorption costing includes the element of fixed cost. It provides the actual value of stock. It

helps in preparation of external parties (Callahan, Stetz and Brooks, 2011).

1.3 Advantages and disadvantages of Marginal and Absorption costing

Through application of Marginal and Absorption costing many advantages and

disadvantages are gathered by UCK Furniture which is mentioned below:

Marginal costing

Advantages

It helps in planning about the profits which is associated with completion of project

This method also helps in management reporting

It provides the opportunity regarding controlling of costs

It also helps in production planning

Disadvantages

Difficult to separate costs into fixed and variable

Through application of this method stocks are undervalued because fixed cost is not

included

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is true in short span of time

Absorption costing

Advantages

Not includes the process of separating the costs into fixed and variable.

It is useful in determination of price of products

It is helpful in preparation of external reports for stock valuation

Disadvantages

Profits of organisation is affected by production volumes

Difficult to calculate variations in cost which is occurred at various production level

Difficult to take good decisions regarding operational efficiency

TASK 2

2.1 Advantages and disadvantages of different planning tools used for budgetary control

Budget: Budget includes the forecasting of financial results and position of organisation

for future period of time. It can be used for two main purpose by the management of UCK

Furniture which are planning and performance measurement.

Budgetary control: It is management control system which helps in comparison of

actual income and expenses with planned income and expenses. UCK Furniture brings an

obligation upon their employees to adhere such standards in order to make large number of

profits (DRURY, 2013).

Steps of budgetary control

Establishment of plan: It is the prime function of manager of organisation to formulate

the plan. It provides the opportunity regarding improvement of the understanding between

different departments and bring coordination in their functions.

Record actual performance: It is the duty of manger to record actual performance

which is given by following such plans.

Comparison with budgeted: It includes comparison of actual with standards for

identification of deviation and reason behind them.

Calculation of variations: Under this step, reason and consequences of deviations are

identified.

4

Absorption costing

Advantages

Not includes the process of separating the costs into fixed and variable.

It is useful in determination of price of products

It is helpful in preparation of external reports for stock valuation

Disadvantages

Profits of organisation is affected by production volumes

Difficult to calculate variations in cost which is occurred at various production level

Difficult to take good decisions regarding operational efficiency

TASK 2

2.1 Advantages and disadvantages of different planning tools used for budgetary control

Budget: Budget includes the forecasting of financial results and position of organisation

for future period of time. It can be used for two main purpose by the management of UCK

Furniture which are planning and performance measurement.

Budgetary control: It is management control system which helps in comparison of

actual income and expenses with planned income and expenses. UCK Furniture brings an

obligation upon their employees to adhere such standards in order to make large number of

profits (DRURY, 2013).

Steps of budgetary control

Establishment of plan: It is the prime function of manager of organisation to formulate

the plan. It provides the opportunity regarding improvement of the understanding between

different departments and bring coordination in their functions.

Record actual performance: It is the duty of manger to record actual performance

which is given by following such plans.

Comparison with budgeted: It includes comparison of actual with standards for

identification of deviation and reason behind them.

Calculation of variations: Under this step, reason and consequences of deviations are

identified.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Remedy of situation: Providing of appropriate solutions which helps in achievement of

targets.

Planning tools: It is a tool which provides the direction to different organisational

actions which helps in effective implementation of program. Advantages and Disadvantages of

different tools are mentioned below:

Forecasting tools: This tools helps in determination of the internal and external factors

which impact the business activities. It is useful for growth prospect of company.

Advantages: It provides visualisation of the future models and actions. It is effective risk

management tool.

Disadvantage: Forecast are based on assumptions as per their personal knowledge. So,

large number of chances of failure.

Scenario analysis tool: This tool brings identification of the fears in open and

application of rational and professional framework which helps in exploring their capabilities

regarding completion of tasks. Process of using this tool includes certain steps like define issues,

collection of data, separation of certainties from uncertainties, development of sceneries and

planning about actions (Fourie and et. al., 2015).

Advantages: Helps in preparation of strategies and identification of uncertainties. It

provides the opportunity regarding development of contingency plan.

Disadvantage: Wrong identification of situations provides negative results.

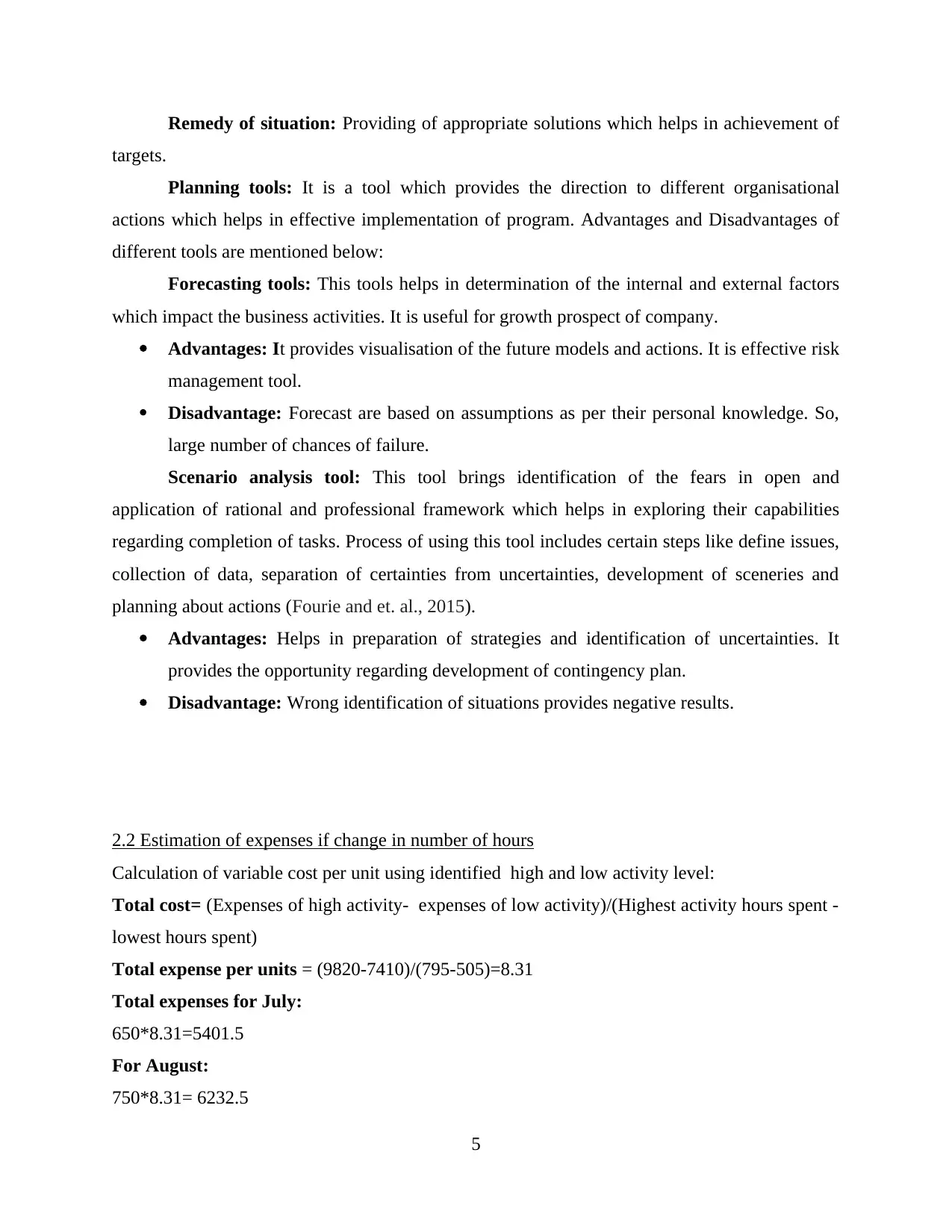

2.2 Estimation of expenses if change in number of hours

Calculation of variable cost per unit using identified high and low activity level:

Total cost= (Expenses of high activity- expenses of low activity)/(Highest activity hours spent -

lowest hours spent)

Total expense per units = (9820-7410)/(795-505)=8.31

Total expenses for July:

650*8.31=5401.5

For August:

750*8.31= 6232.5

5

targets.

Planning tools: It is a tool which provides the direction to different organisational

actions which helps in effective implementation of program. Advantages and Disadvantages of

different tools are mentioned below:

Forecasting tools: This tools helps in determination of the internal and external factors

which impact the business activities. It is useful for growth prospect of company.

Advantages: It provides visualisation of the future models and actions. It is effective risk

management tool.

Disadvantage: Forecast are based on assumptions as per their personal knowledge. So,

large number of chances of failure.

Scenario analysis tool: This tool brings identification of the fears in open and

application of rational and professional framework which helps in exploring their capabilities

regarding completion of tasks. Process of using this tool includes certain steps like define issues,

collection of data, separation of certainties from uncertainties, development of sceneries and

planning about actions (Fourie and et. al., 2015).

Advantages: Helps in preparation of strategies and identification of uncertainties. It

provides the opportunity regarding development of contingency plan.

Disadvantage: Wrong identification of situations provides negative results.

2.2 Estimation of expenses if change in number of hours

Calculation of variable cost per unit using identified high and low activity level:

Total cost= (Expenses of high activity- expenses of low activity)/(Highest activity hours spent -

lowest hours spent)

Total expense per units = (9820-7410)/(795-505)=8.31

Total expenses for July:

650*8.31=5401.5

For August:

750*8.31= 6232.5

5

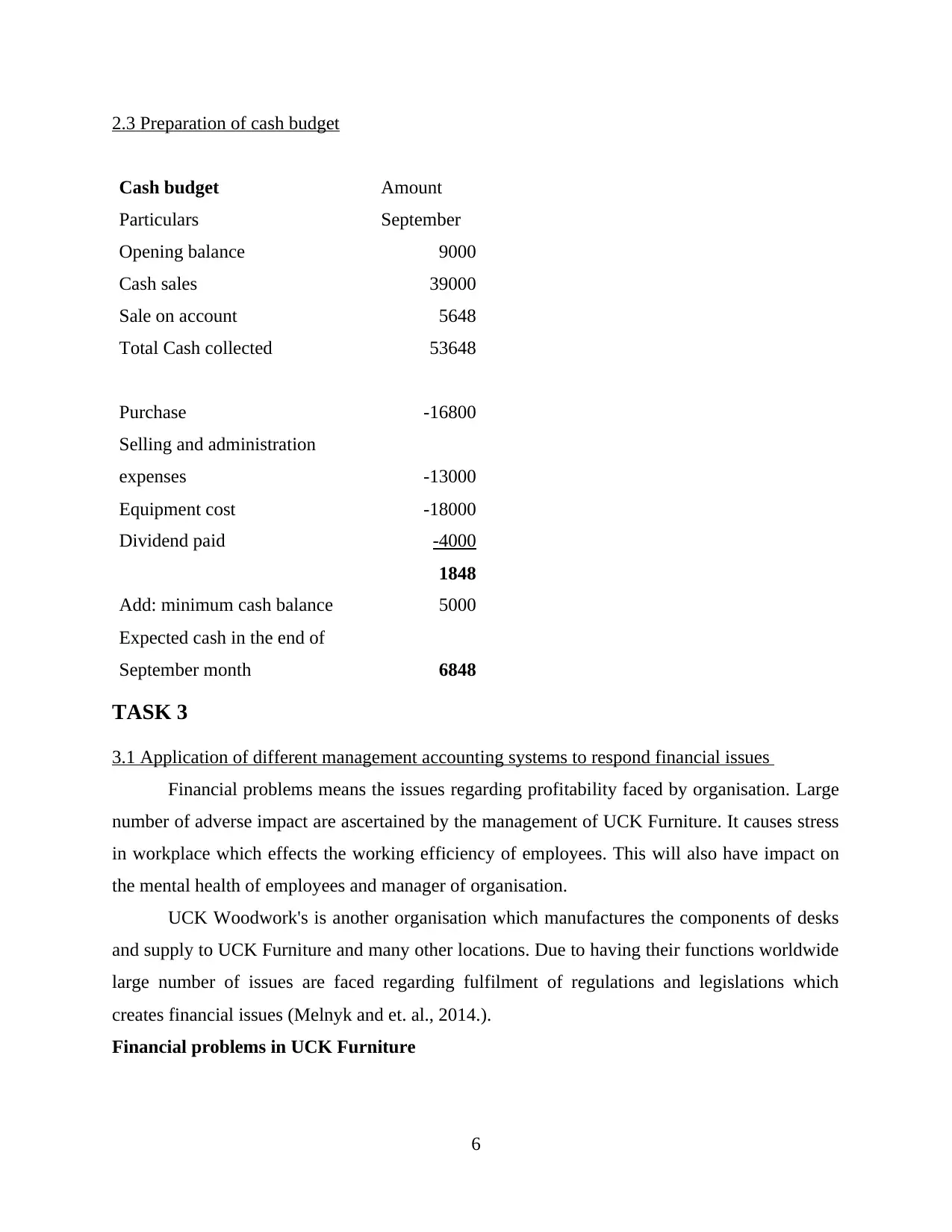

2.3 Preparation of cash budget

Cash budget Amount

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Purchase -16800

Selling and administration

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash in the end of

September month 6848

TASK 3

3.1 Application of different management accounting systems to respond financial issues

Financial problems means the issues regarding profitability faced by organisation. Large

number of adverse impact are ascertained by the management of UCK Furniture. It causes stress

in workplace which effects the working efficiency of employees. This will also have impact on

the mental health of employees and manager of organisation.

UCK Woodwork's is another organisation which manufactures the components of desks

and supply to UCK Furniture and many other locations. Due to having their functions worldwide

large number of issues are faced regarding fulfilment of regulations and legislations which

creates financial issues (Melnyk and et. al., 2014.).

Financial problems in UCK Furniture

6

Cash budget Amount

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Purchase -16800

Selling and administration

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash in the end of

September month 6848

TASK 3

3.1 Application of different management accounting systems to respond financial issues

Financial problems means the issues regarding profitability faced by organisation. Large

number of adverse impact are ascertained by the management of UCK Furniture. It causes stress

in workplace which effects the working efficiency of employees. This will also have impact on

the mental health of employees and manager of organisation.

UCK Woodwork's is another organisation which manufactures the components of desks

and supply to UCK Furniture and many other locations. Due to having their functions worldwide

large number of issues are faced regarding fulfilment of regulations and legislations which

creates financial issues (Melnyk and et. al., 2014.).

Financial problems in UCK Furniture

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

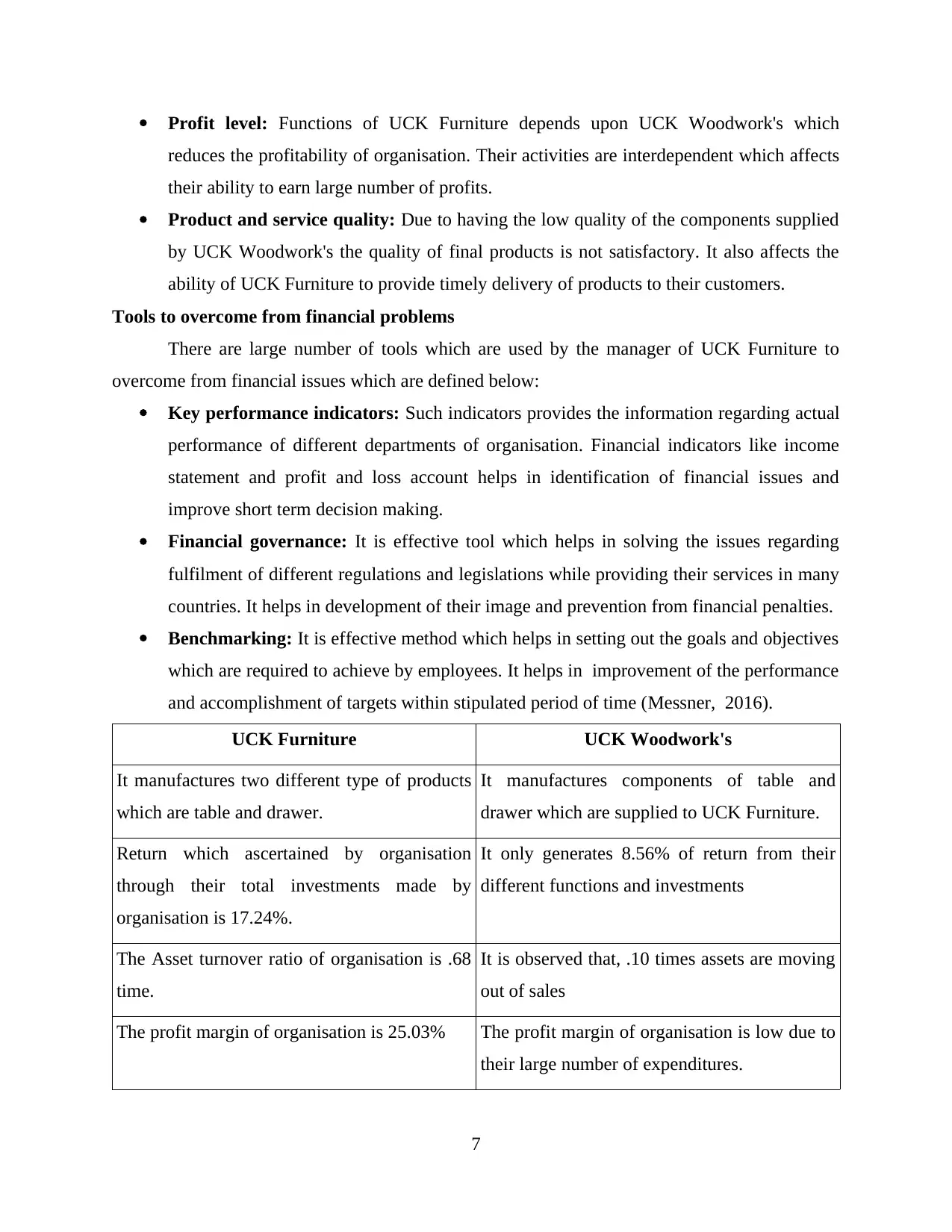

Profit level: Functions of UCK Furniture depends upon UCK Woodwork's which

reduces the profitability of organisation. Their activities are interdependent which affects

their ability to earn large number of profits.

Product and service quality: Due to having the low quality of the components supplied

by UCK Woodwork's the quality of final products is not satisfactory. It also affects the

ability of UCK Furniture to provide timely delivery of products to their customers.

Tools to overcome from financial problems

There are large number of tools which are used by the manager of UCK Furniture to

overcome from financial issues which are defined below:

Key performance indicators: Such indicators provides the information regarding actual

performance of different departments of organisation. Financial indicators like income

statement and profit and loss account helps in identification of financial issues and

improve short term decision making.

Financial governance: It is effective tool which helps in solving the issues regarding

fulfilment of different regulations and legislations while providing their services in many

countries. It helps in development of their image and prevention from financial penalties.

Benchmarking: It is effective method which helps in setting out the goals and objectives

which are required to achieve by employees. It helps in improvement of the performance

and accomplishment of targets within stipulated period of time (Messner, 2016).

UCK Furniture UCK Woodwork's

It manufactures two different type of products

which are table and drawer.

It manufactures components of table and

drawer which are supplied to UCK Furniture.

Return which ascertained by organisation

through their total investments made by

organisation is 17.24%.

It only generates 8.56% of return from their

different functions and investments

The Asset turnover ratio of organisation is .68

time.

It is observed that, .10 times assets are moving

out of sales

The profit margin of organisation is 25.03% The profit margin of organisation is low due to

their large number of expenditures.

7

reduces the profitability of organisation. Their activities are interdependent which affects

their ability to earn large number of profits.

Product and service quality: Due to having the low quality of the components supplied

by UCK Woodwork's the quality of final products is not satisfactory. It also affects the

ability of UCK Furniture to provide timely delivery of products to their customers.

Tools to overcome from financial problems

There are large number of tools which are used by the manager of UCK Furniture to

overcome from financial issues which are defined below:

Key performance indicators: Such indicators provides the information regarding actual

performance of different departments of organisation. Financial indicators like income

statement and profit and loss account helps in identification of financial issues and

improve short term decision making.

Financial governance: It is effective tool which helps in solving the issues regarding

fulfilment of different regulations and legislations while providing their services in many

countries. It helps in development of their image and prevention from financial penalties.

Benchmarking: It is effective method which helps in setting out the goals and objectives

which are required to achieve by employees. It helps in improvement of the performance

and accomplishment of targets within stipulated period of time (Messner, 2016).

UCK Furniture UCK Woodwork's

It manufactures two different type of products

which are table and drawer.

It manufactures components of table and

drawer which are supplied to UCK Furniture.

Return which ascertained by organisation

through their total investments made by

organisation is 17.24%.

It only generates 8.56% of return from their

different functions and investments

The Asset turnover ratio of organisation is .68

time.

It is observed that, .10 times assets are moving

out of sales

The profit margin of organisation is 25.03% The profit margin of organisation is low due to

their large number of expenditures.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

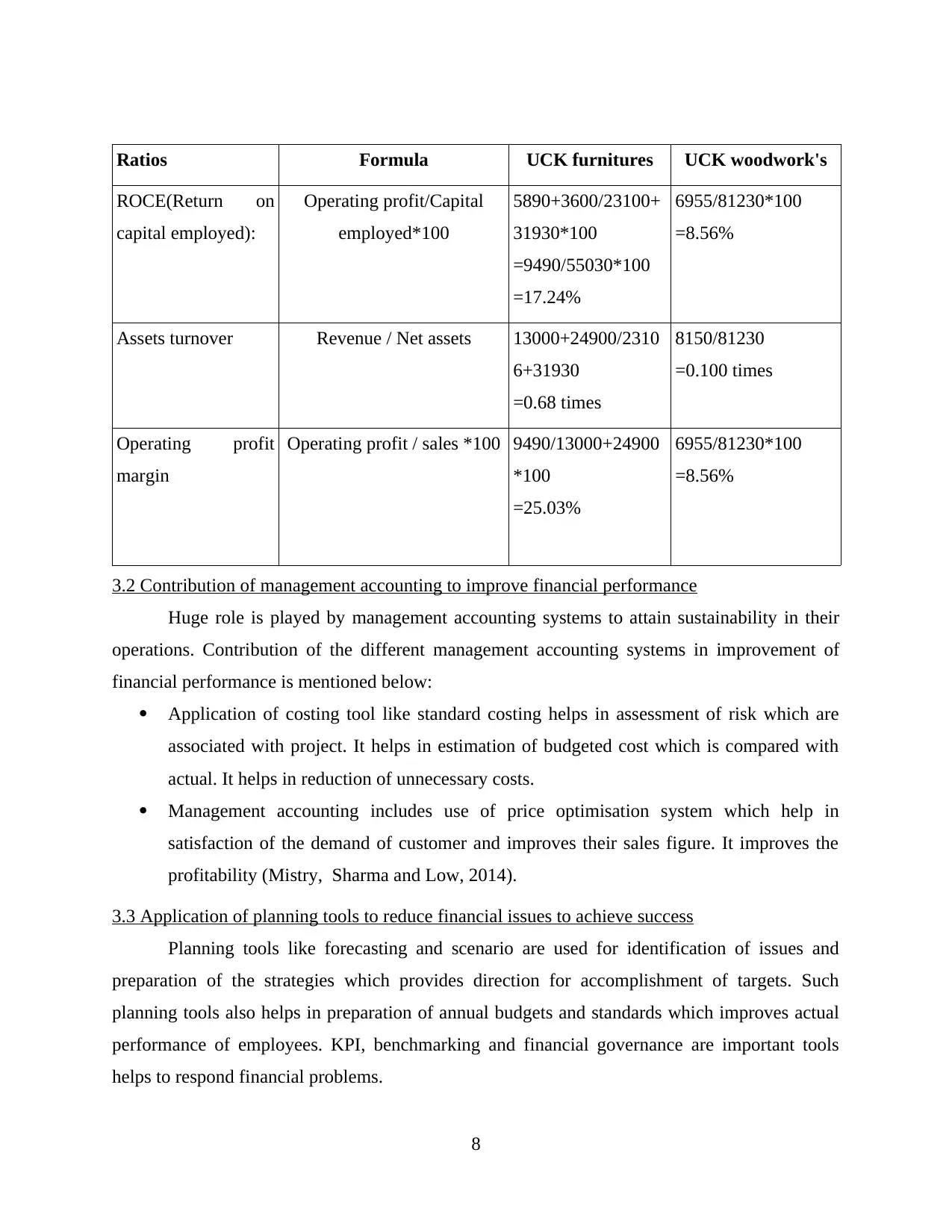

Ratios Formula UCK furnitures UCK woodwork's

ROCE(Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+

31930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/2310

6+31930

=0.68 times

8150/81230

=0.100 times

Operating profit

margin

Operating profit / sales *100 9490/13000+24900

*100

=25.03%

6955/81230*100

=8.56%

3.2 Contribution of management accounting to improve financial performance

Huge role is played by management accounting systems to attain sustainability in their

operations. Contribution of the different management accounting systems in improvement of

financial performance is mentioned below:

Application of costing tool like standard costing helps in assessment of risk which are

associated with project. It helps in estimation of budgeted cost which is compared with

actual. It helps in reduction of unnecessary costs.

Management accounting includes use of price optimisation system which help in

satisfaction of the demand of customer and improves their sales figure. It improves the

profitability (Mistry, Sharma and Low, 2014).

3.3 Application of planning tools to reduce financial issues to achieve success

Planning tools like forecasting and scenario are used for identification of issues and

preparation of the strategies which provides direction for accomplishment of targets. Such

planning tools also helps in preparation of annual budgets and standards which improves actual

performance of employees. KPI, benchmarking and financial governance are important tools

helps to respond financial problems.

8

ROCE(Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+

31930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/2310

6+31930

=0.68 times

8150/81230

=0.100 times

Operating profit

margin

Operating profit / sales *100 9490/13000+24900

*100

=25.03%

6955/81230*100

=8.56%

3.2 Contribution of management accounting to improve financial performance

Huge role is played by management accounting systems to attain sustainability in their

operations. Contribution of the different management accounting systems in improvement of

financial performance is mentioned below:

Application of costing tool like standard costing helps in assessment of risk which are

associated with project. It helps in estimation of budgeted cost which is compared with

actual. It helps in reduction of unnecessary costs.

Management accounting includes use of price optimisation system which help in

satisfaction of the demand of customer and improves their sales figure. It improves the

profitability (Mistry, Sharma and Low, 2014).

3.3 Application of planning tools to reduce financial issues to achieve success

Planning tools like forecasting and scenario are used for identification of issues and

preparation of the strategies which provides direction for accomplishment of targets. Such

planning tools also helps in preparation of annual budgets and standards which improves actual

performance of employees. KPI, benchmarking and financial governance are important tools

helps to respond financial problems.

8

CONCLUSION

It has been concluded from the above report that, due to the use of planning tools large

number of benefits are achieved by UCK Furniture. Scenario tools helps in identification of

uncertainties and preparation of provisions regarding contingencies. Forecasting tool helps in

planning of future actions. Adoption of management accounting system provides financial and

non financial KPI like Financial governance, benchmarking to overcome from financial issues

and improve their profitability. Preparation of cash budget helps in determination of availability

of cash and operation of functions effectively.

REFERENCES

Books and Journals

Chiwamit, P., Modell, S. and Yang, C. L., 2014. The societal relevance of management

accounting innovations: economic value added and institutional work in the fields of

Chinese and Thai state-owned enterprises. Accounting and Business Research. 44(2).

pp.144-180.

Albu, N. and Albu, C. N., 2012. Factors associated with the adoption and use of management

accounting techniques in developing countries: The case of Romania. Journal of

International Financial Management & Accounting. 23(3). pp.245-276.

Callahan, K. R., Stetz, G. S. and Brooks, L. M., 2011. Project Management Accounting, with

Website: Budgeting, Tracking, and Reporting Costs and Profitability (Vol. 565). John

Wiley & Sons.

DRURY, C. M., 2013. Management and cost accounting. Springer.

Fourie, M. L. and et. al., 2015. Municipal finance and accounting. Van Schaik Publishers.

Melnyk, S. A. and et. al., 2014. Is performance measurement and management fit for the future?.

Management Accounting Research. 25(2). pp.173-186.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Mistry, V., Sharma, U. and Low, M., 2014. Management accountants' perception of their role in

accounting for sustainable development: An exploratory study. Pacific Accounting

Review. 26(1/2). pp.112-133.

Renz, D. O. and Herman, R. D. Eds., 2016. The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

Robalo, R., 2014. Explanations for the gap between management accounting rules and routines:

An institutional approach. Revista de Contabilidad. 17(1). pp.88-97.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

9

It has been concluded from the above report that, due to the use of planning tools large

number of benefits are achieved by UCK Furniture. Scenario tools helps in identification of

uncertainties and preparation of provisions regarding contingencies. Forecasting tool helps in

planning of future actions. Adoption of management accounting system provides financial and

non financial KPI like Financial governance, benchmarking to overcome from financial issues

and improve their profitability. Preparation of cash budget helps in determination of availability

of cash and operation of functions effectively.

REFERENCES

Books and Journals

Chiwamit, P., Modell, S. and Yang, C. L., 2014. The societal relevance of management

accounting innovations: economic value added and institutional work in the fields of

Chinese and Thai state-owned enterprises. Accounting and Business Research. 44(2).

pp.144-180.

Albu, N. and Albu, C. N., 2012. Factors associated with the adoption and use of management

accounting techniques in developing countries: The case of Romania. Journal of

International Financial Management & Accounting. 23(3). pp.245-276.

Callahan, K. R., Stetz, G. S. and Brooks, L. M., 2011. Project Management Accounting, with

Website: Budgeting, Tracking, and Reporting Costs and Profitability (Vol. 565). John

Wiley & Sons.

DRURY, C. M., 2013. Management and cost accounting. Springer.

Fourie, M. L. and et. al., 2015. Municipal finance and accounting. Van Schaik Publishers.

Melnyk, S. A. and et. al., 2014. Is performance measurement and management fit for the future?.

Management Accounting Research. 25(2). pp.173-186.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Mistry, V., Sharma, U. and Low, M., 2014. Management accountants' perception of their role in

accounting for sustainable development: An exploratory study. Pacific Accounting

Review. 26(1/2). pp.112-133.

Renz, D. O. and Herman, R. D. Eds., 2016. The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

Robalo, R., 2014. Explanations for the gap between management accounting rules and routines:

An institutional approach. Revista de Contabilidad. 17(1). pp.88-97.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.