Management Accounting Project: UCK Furniture Financial Analysis Report

VerifiedAdded on 2020/09/17

|13

|2925

|39

Report

AI Summary

This report delves into the application of management accounting principles within UCK Furniture, focusing on various costing methods and financial planning techniques. The report begins by examining marginal and absorption costing, comparing their advantages and disadvantages to determine the most effective method for cost analysis. It further explores the application of different planning tools, including budgetary control, forecasting tools, and scenario analysis tools, discussing their benefits and drawbacks. The analysis extends to the estimation of expenses based on activity levels and the preparation of a cash budget. Finally, the report addresses financial problems faced by UCK Furniture, such as profitability and cost efficiency, and suggests management accounting systems, including Key Performance Indicators (KPIs) and financial governance, to mitigate these issues. The report provides a comprehensive overview of management accounting practices, offering insights into cost analysis, budgeting, and financial problem-solving for the furniture company.

MANAGEMENT

ACCOUNTING

(PART 2)

ACCOUNTING

(PART 2)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PROJECT 2......................................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Few costing methods considered in management accounting..............................................3

1.2 Application of various techniques of management accounting............................................6

1.3 Advantages and disadvantages of Marginal and Absorption costing...................................6

TASK 2............................................................................................................................................7

2.1 Advantages and disadvantages of different type of planning tools......................................7

2.2 Estimation of expenses if change in number of hours..........................................................8

2.3 Preparation of cash budget....................................................................................................9

TASK 3............................................................................................................................................9

3.1 Enterprises are adapting management accounting systems to respond financial problems..9

3.2 Contribution of management accounting to improve financial performance.....................10

3.3 Planning tools for accounting respond to solve financial issues.........................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

PROJECT 2......................................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Few costing methods considered in management accounting..............................................3

1.2 Application of various techniques of management accounting............................................6

1.3 Advantages and disadvantages of Marginal and Absorption costing...................................6

TASK 2............................................................................................................................................7

2.1 Advantages and disadvantages of different type of planning tools......................................7

2.2 Estimation of expenses if change in number of hours..........................................................8

2.3 Preparation of cash budget....................................................................................................9

TASK 3............................................................................................................................................9

3.1 Enterprises are adapting management accounting systems to respond financial problems..9

3.2 Contribution of management accounting to improve financial performance.....................10

3.3 Planning tools for accounting respond to solve financial issues.........................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting can be defined as a procedure which is being carried out in

companies so as to efficiently manage all the finances of the company. It is very important for

every company to implement these kinds of processes inside the company so that their work can

be effectively managed and company can find various options to increase their funds as well

(Kotas, 2014). The company referred in this report is UCK Furniture who is starting a new

training course in order to train their employees. This part of the project will discuss about

various techniques of analysing the cost implemented by the company, advantages and

disadvantages of various types of planning tools and along with this various ways of adapting the

management accounting system in their financial statements.

PROJECT 2

TASK 1

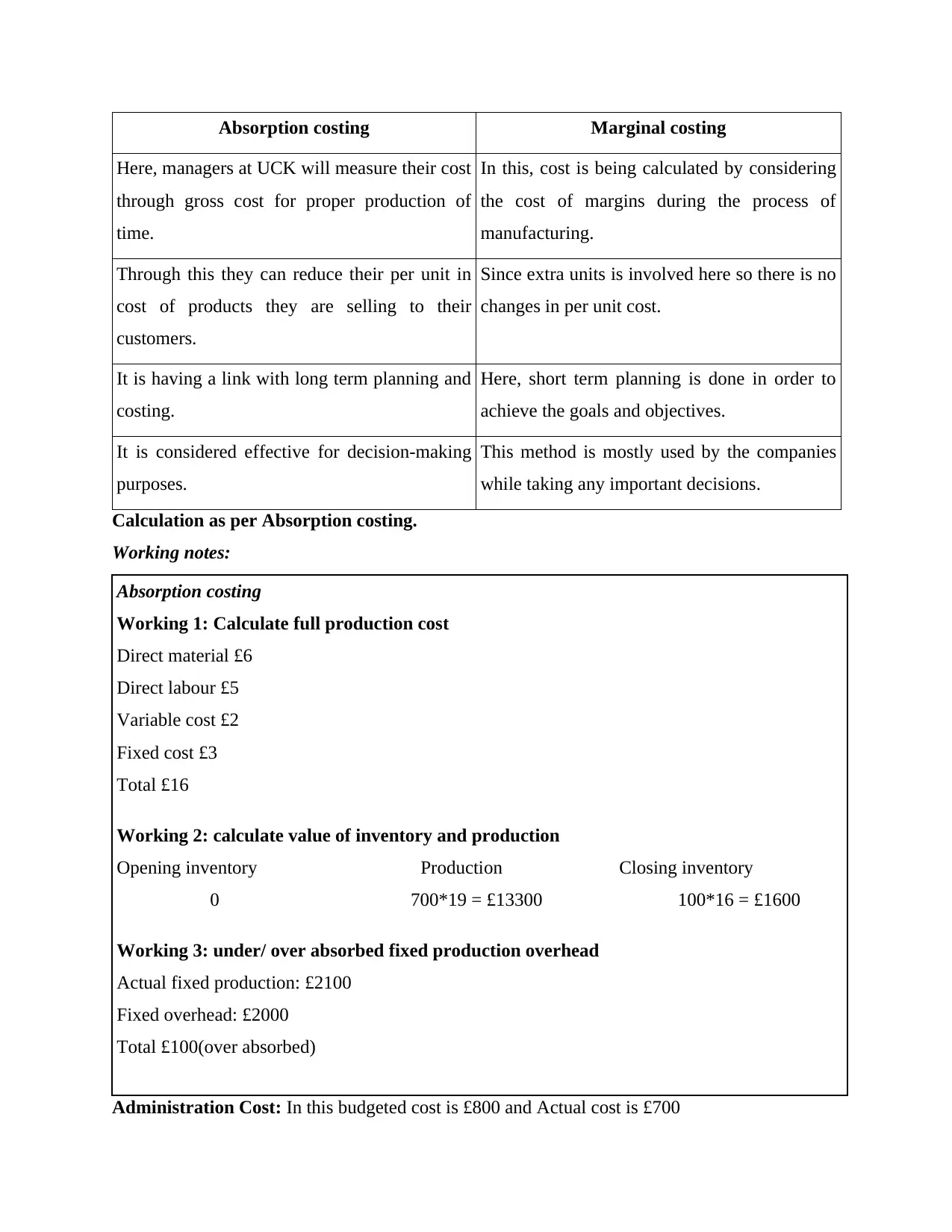

1.1 Few costing methods considered in management accounting

It is very important for every company to analyse their cost time to time so that they can

come to know that whether they are selling their products at correct price or not. It is really need

to be taken care of while manufacturing the products and services. So companies have to choose

a technique of management accounting while preparing their income statements. The main

techniques involved in this type of accounting is Marginal costing and absorption costing. Both

these are very effective but the latter one is more used. These methods are discussed as under:-

Marginal Costing – In this type of costing , cost of manufacturing and production

process is being used. Here both fixed as well as variable cost is being used together so as

to calculate the cost correctly. This technique will be used to calculate the cost of

products and services by taking in concern direct cost and overheads as well (Laudon and

Laudon, 2016).

Absorption Costing – It is called as the cost of one extra unit of production and it is

being used by companies like UCK Furniture. If the company will charge extra per unit

of the product then this will be very effective for the company as they will be able to

manufacture the units more.

Comparison of Marginal Costing and Absorption Costing is done as follows:-

Management accounting can be defined as a procedure which is being carried out in

companies so as to efficiently manage all the finances of the company. It is very important for

every company to implement these kinds of processes inside the company so that their work can

be effectively managed and company can find various options to increase their funds as well

(Kotas, 2014). The company referred in this report is UCK Furniture who is starting a new

training course in order to train their employees. This part of the project will discuss about

various techniques of analysing the cost implemented by the company, advantages and

disadvantages of various types of planning tools and along with this various ways of adapting the

management accounting system in their financial statements.

PROJECT 2

TASK 1

1.1 Few costing methods considered in management accounting

It is very important for every company to analyse their cost time to time so that they can

come to know that whether they are selling their products at correct price or not. It is really need

to be taken care of while manufacturing the products and services. So companies have to choose

a technique of management accounting while preparing their income statements. The main

techniques involved in this type of accounting is Marginal costing and absorption costing. Both

these are very effective but the latter one is more used. These methods are discussed as under:-

Marginal Costing – In this type of costing , cost of manufacturing and production

process is being used. Here both fixed as well as variable cost is being used together so as

to calculate the cost correctly. This technique will be used to calculate the cost of

products and services by taking in concern direct cost and overheads as well (Laudon and

Laudon, 2016).

Absorption Costing – It is called as the cost of one extra unit of production and it is

being used by companies like UCK Furniture. If the company will charge extra per unit

of the product then this will be very effective for the company as they will be able to

manufacture the units more.

Comparison of Marginal Costing and Absorption Costing is done as follows:-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Absorption costing Marginal costing

Here, managers at UCK will measure their cost

through gross cost for proper production of

time.

In this, cost is being calculated by considering

the cost of margins during the process of

manufacturing.

Through this they can reduce their per unit in

cost of products they are selling to their

customers.

Since extra units is involved here so there is no

changes in per unit cost.

It is having a link with long term planning and

costing.

Here, short term planning is done in order to

achieve the goals and objectives.

It is considered effective for decision-making

purposes.

This method is mostly used by the companies

while taking any important decisions.

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Here, managers at UCK will measure their cost

through gross cost for proper production of

time.

In this, cost is being calculated by considering

the cost of margins during the process of

manufacturing.

Through this they can reduce their per unit in

cost of products they are selling to their

customers.

Since extra units is involved here so there is no

changes in per unit cost.

It is having a link with long term planning and

costing.

Here, short term planning is done in order to

achieve the goals and objectives.

It is considered effective for decision-making

purposes.

This method is mostly used by the companies

while taking any important decisions.

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

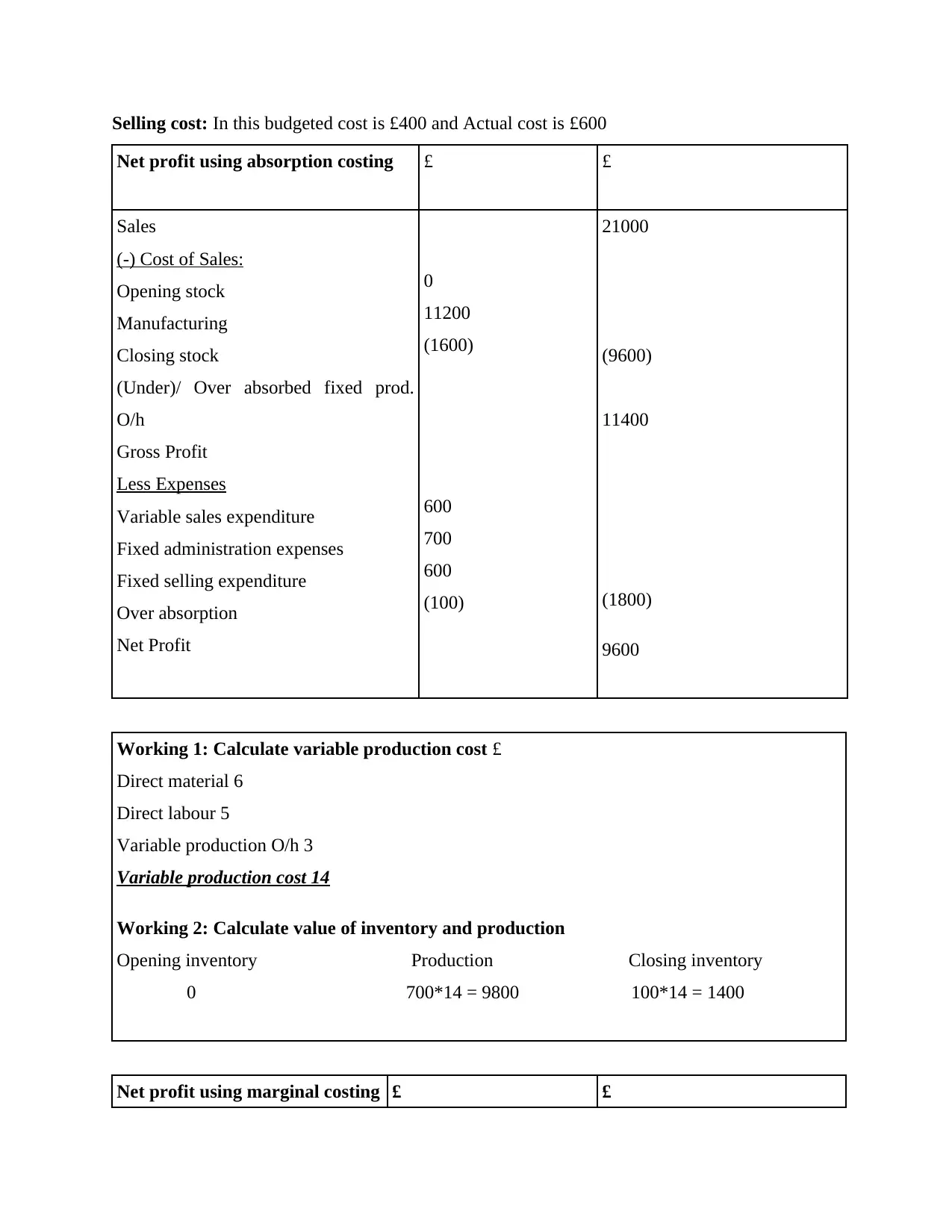

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

0

11200

(1600)

600

700

600

(100)

21000

(9600)

11400

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

0

11200

(1600)

600

700

600

(100)

21000

(9600)

11400

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9100

(1300)

2000

1300

600

21000

(7800)

13200

3900

9300

From the above calculation it gets cleared that they should make use of absorption

costing method while doing their cost analysis. This decision is taken because it is giving the

company the net profit of £9600 whereas through marginal costing profits will be around £9300

only. The another influence in this treatments is linked with the closing stock.

1.2 Application of various techniques of management accounting

Both Marginal costing and absorption costing are two different techniques which is

helping in finding out the valuation of inventory (Liao, Chu and Hsiao, 2012). Marginal cost is

not including any elements of fixed cost and it is considered as one of the best method for taking

important decisions of the company within short duration of time. It has also been assessed that

stock of the organisation is undervalued whereas in Absorption costing elements of foxed cost is

available. They are also providing the correct value of stock.

1.3 Advantages and disadvantages of Marginal and Absorption costing

After applying the marginal and absorption costing, the advantages and disadvantages of

UCK furniture is being mentioned here:-

Advantages and disadvantages of Marginal costing

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9100

(1300)

2000

1300

600

21000

(7800)

13200

3900

9300

From the above calculation it gets cleared that they should make use of absorption

costing method while doing their cost analysis. This decision is taken because it is giving the

company the net profit of £9600 whereas through marginal costing profits will be around £9300

only. The another influence in this treatments is linked with the closing stock.

1.2 Application of various techniques of management accounting

Both Marginal costing and absorption costing are two different techniques which is

helping in finding out the valuation of inventory (Liao, Chu and Hsiao, 2012). Marginal cost is

not including any elements of fixed cost and it is considered as one of the best method for taking

important decisions of the company within short duration of time. It has also been assessed that

stock of the organisation is undervalued whereas in Absorption costing elements of foxed cost is

available. They are also providing the correct value of stock.

1.3 Advantages and disadvantages of Marginal and Absorption costing

After applying the marginal and absorption costing, the advantages and disadvantages of

UCK furniture is being mentioned here:-

Advantages and disadvantages of Marginal costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

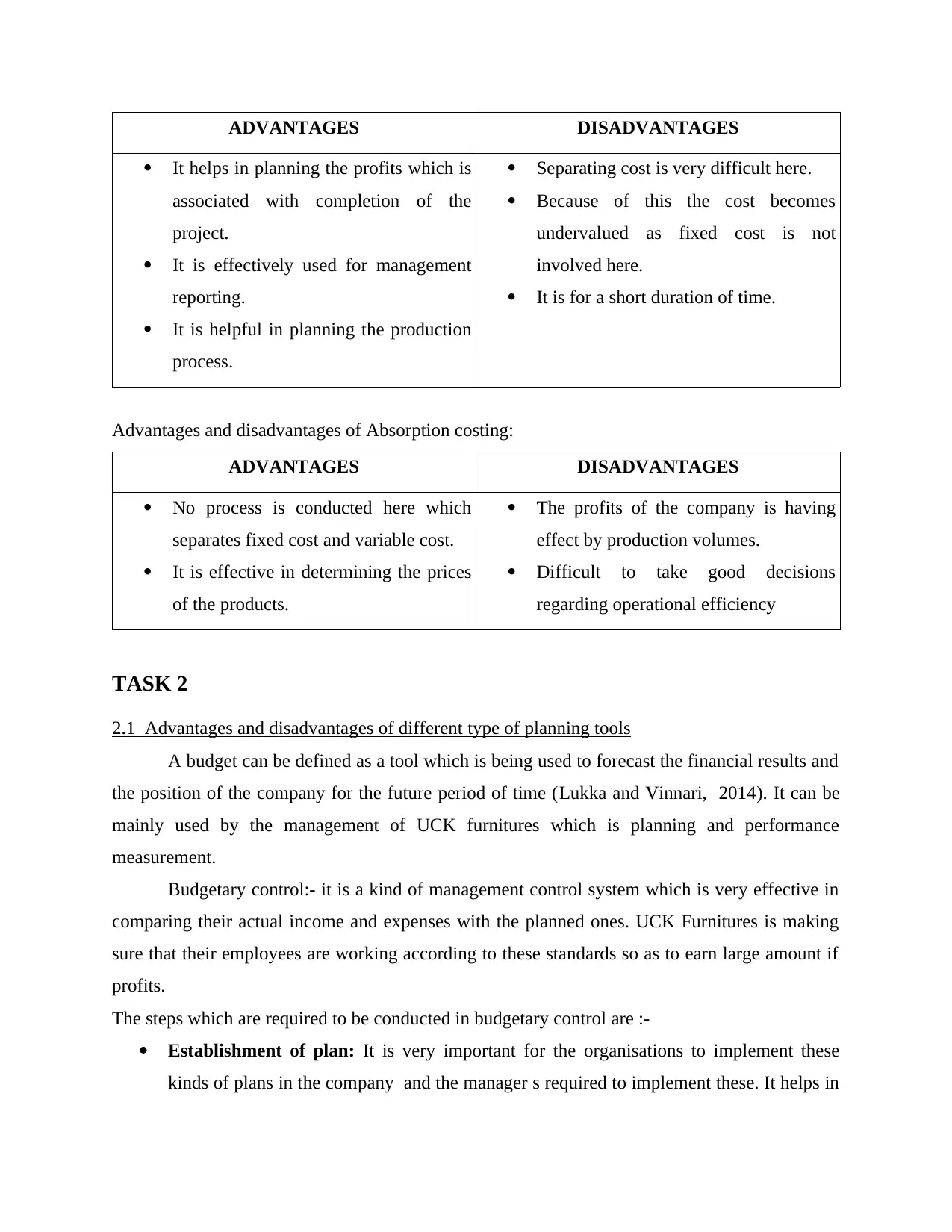

ADVANTAGES DISADVANTAGES

It helps in planning the profits which is

associated with completion of the

project.

It is effectively used for management

reporting.

It is helpful in planning the production

process.

Separating cost is very difficult here.

Because of this the cost becomes

undervalued as fixed cost is not

involved here.

It is for a short duration of time.

Advantages and disadvantages of Absorption costing:

ADVANTAGES DISADVANTAGES

No process is conducted here which

separates fixed cost and variable cost.

It is effective in determining the prices

of the products.

The profits of the company is having

effect by production volumes.

Difficult to take good decisions

regarding operational efficiency

TASK 2

2.1 Advantages and disadvantages of different type of planning tools

A budget can be defined as a tool which is being used to forecast the financial results and

the position of the company for the future period of time (Lukka and Vinnari, 2014). It can be

mainly used by the management of UCK furnitures which is planning and performance

measurement.

Budgetary control:- it is a kind of management control system which is very effective in

comparing their actual income and expenses with the planned ones. UCK Furnitures is making

sure that their employees are working according to these standards so as to earn large amount if

profits.

The steps which are required to be conducted in budgetary control are :-

Establishment of plan: It is very important for the organisations to implement these

kinds of plans in the company and the manager s required to implement these. It helps in

It helps in planning the profits which is

associated with completion of the

project.

It is effectively used for management

reporting.

It is helpful in planning the production

process.

Separating cost is very difficult here.

Because of this the cost becomes

undervalued as fixed cost is not

involved here.

It is for a short duration of time.

Advantages and disadvantages of Absorption costing:

ADVANTAGES DISADVANTAGES

No process is conducted here which

separates fixed cost and variable cost.

It is effective in determining the prices

of the products.

The profits of the company is having

effect by production volumes.

Difficult to take good decisions

regarding operational efficiency

TASK 2

2.1 Advantages and disadvantages of different type of planning tools

A budget can be defined as a tool which is being used to forecast the financial results and

the position of the company for the future period of time (Lukka and Vinnari, 2014). It can be

mainly used by the management of UCK furnitures which is planning and performance

measurement.

Budgetary control:- it is a kind of management control system which is very effective in

comparing their actual income and expenses with the planned ones. UCK Furnitures is making

sure that their employees are working according to these standards so as to earn large amount if

profits.

The steps which are required to be conducted in budgetary control are :-

Establishment of plan: It is very important for the organisations to implement these

kinds of plans in the company and the manager s required to implement these. It helps in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

developing the opportunities for understanding various departments and bringing

coordination in them as well.

Record actual performance: It is the duty of the managers of the company to record the

actual performance of the employees which is following these plans (Macintosh and

Quattrone, 2010).

Comparison with budgeted: Here, the actual budget is being compared with the planned

one and then in case of any errors corrective actions is required to be taken.

Calculation of variations: Under this, reason and consequences of deviations are

identified (Otley and Emmanuel, 2013). Remedy of situation: In this appropriate actions is being provided so as to achieve their

targets more easily.

Planning tools: It will help in conducting right actions which will help the company in

implementing their targets in an effective manner.

Forecasting tools: It is very effective determination of internal and external factors

which is having a bad impact on the business activities and is also very effective in

growing the company across the market.

Advantages: It is very effective in managing the risk of the company.

Disadvantage: There is large no. of chances of failure.

Scenario analysis tool: This tool helps in identifying the fear in open and application of

logical and professional model through which capabilities can be known about

completing the task of the company.

Advantages: Helps in planning of schemes and finding of uncertainties. It gives the opportunity

regarding development of contingency plan.

Disadvantage: Incorrect recognition of situations often results in negative results.

2.2 Estimation of expenses if change in number of hours

Calculation of variable cost per unit using identified high and low activity level:

Total cost= (Expenses of high activity- expenses of low activity)/(Highest activity hours

spent -lowest hours spent)

Total expense per units = (9820-7410)/(795-505)=8.31

Total expenses for July: 650*8.31=5401.5

For August:750*8.31= 6232.5

coordination in them as well.

Record actual performance: It is the duty of the managers of the company to record the

actual performance of the employees which is following these plans (Macintosh and

Quattrone, 2010).

Comparison with budgeted: Here, the actual budget is being compared with the planned

one and then in case of any errors corrective actions is required to be taken.

Calculation of variations: Under this, reason and consequences of deviations are

identified (Otley and Emmanuel, 2013). Remedy of situation: In this appropriate actions is being provided so as to achieve their

targets more easily.

Planning tools: It will help in conducting right actions which will help the company in

implementing their targets in an effective manner.

Forecasting tools: It is very effective determination of internal and external factors

which is having a bad impact on the business activities and is also very effective in

growing the company across the market.

Advantages: It is very effective in managing the risk of the company.

Disadvantage: There is large no. of chances of failure.

Scenario analysis tool: This tool helps in identifying the fear in open and application of

logical and professional model through which capabilities can be known about

completing the task of the company.

Advantages: Helps in planning of schemes and finding of uncertainties. It gives the opportunity

regarding development of contingency plan.

Disadvantage: Incorrect recognition of situations often results in negative results.

2.2 Estimation of expenses if change in number of hours

Calculation of variable cost per unit using identified high and low activity level:

Total cost= (Expenses of high activity- expenses of low activity)/(Highest activity hours

spent -lowest hours spent)

Total expense per units = (9820-7410)/(795-505)=8.31

Total expenses for July: 650*8.31=5401.5

For August:750*8.31= 6232.5

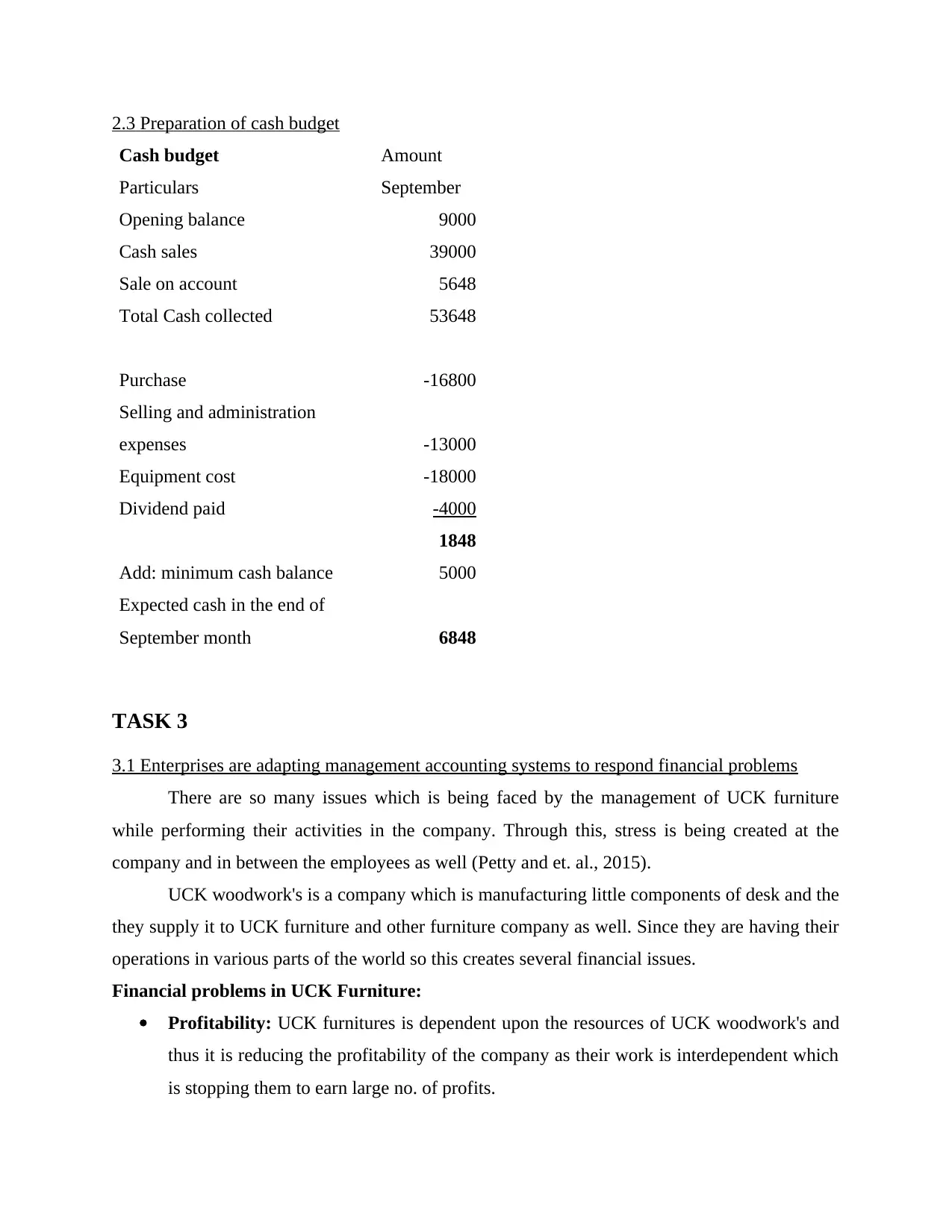

2.3 Preparation of cash budget

Cash budget Amount

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Purchase -16800

Selling and administration

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash in the end of

September month 6848

TASK 3

3.1 Enterprises are adapting management accounting systems to respond financial problems

There are so many issues which is being faced by the management of UCK furniture

while performing their activities in the company. Through this, stress is being created at the

company and in between the employees as well (Petty and et. al., 2015).

UCK woodwork's is a company which is manufacturing little components of desk and the

they supply it to UCK furniture and other furniture company as well. Since they are having their

operations in various parts of the world so this creates several financial issues.

Financial problems in UCK Furniture:

Profitability: UCK furnitures is dependent upon the resources of UCK woodwork's and

thus it is reducing the profitability of the company as their work is interdependent which

is stopping them to earn large no. of profits.

Cash budget Amount

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Purchase -16800

Selling and administration

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash in the end of

September month 6848

TASK 3

3.1 Enterprises are adapting management accounting systems to respond financial problems

There are so many issues which is being faced by the management of UCK furniture

while performing their activities in the company. Through this, stress is being created at the

company and in between the employees as well (Petty and et. al., 2015).

UCK woodwork's is a company which is manufacturing little components of desk and the

they supply it to UCK furniture and other furniture company as well. Since they are having their

operations in various parts of the world so this creates several financial issues.

Financial problems in UCK Furniture:

Profitability: UCK furnitures is dependent upon the resources of UCK woodwork's and

thus it is reducing the profitability of the company as their work is interdependent which

is stopping them to earn large no. of profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

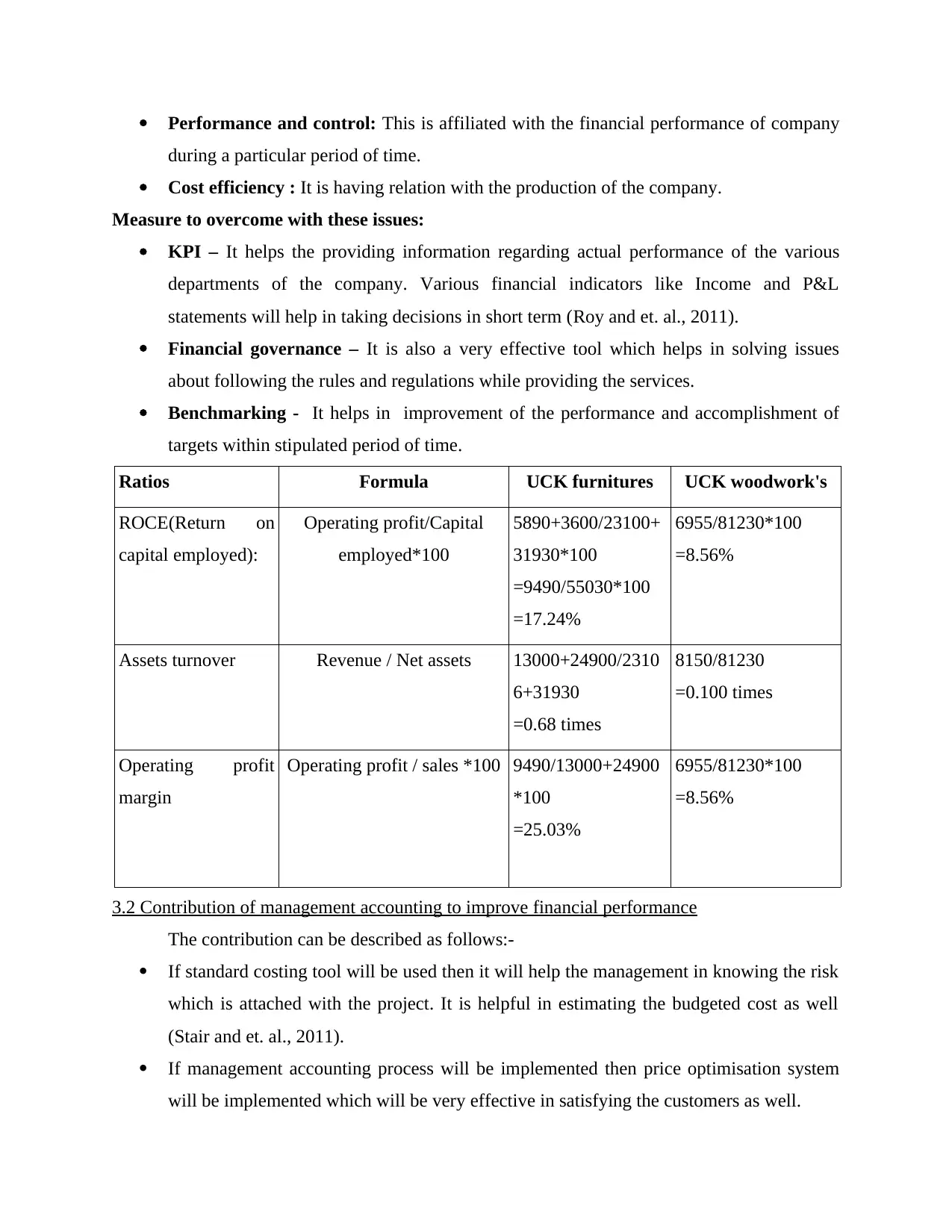

Performance and control: This is affiliated with the financial performance of company

during a particular period of time.

Cost efficiency : It is having relation with the production of the company.

Measure to overcome with these issues:

KPI – It helps the providing information regarding actual performance of the various

departments of the company. Various financial indicators like Income and P&L

statements will help in taking decisions in short term (Roy and et. al., 2011).

Financial governance – It is also a very effective tool which helps in solving issues

about following the rules and regulations while providing the services.

Benchmarking - It helps in improvement of the performance and accomplishment of

targets within stipulated period of time.

Ratios Formula UCK furnitures UCK woodwork's

ROCE(Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+

31930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/2310

6+31930

=0.68 times

8150/81230

=0.100 times

Operating profit

margin

Operating profit / sales *100 9490/13000+24900

*100

=25.03%

6955/81230*100

=8.56%

3.2 Contribution of management accounting to improve financial performance

The contribution can be described as follows:-

If standard costing tool will be used then it will help the management in knowing the risk

which is attached with the project. It is helpful in estimating the budgeted cost as well

(Stair and et. al., 2011).

If management accounting process will be implemented then price optimisation system

will be implemented which will be very effective in satisfying the customers as well.

during a particular period of time.

Cost efficiency : It is having relation with the production of the company.

Measure to overcome with these issues:

KPI – It helps the providing information regarding actual performance of the various

departments of the company. Various financial indicators like Income and P&L

statements will help in taking decisions in short term (Roy and et. al., 2011).

Financial governance – It is also a very effective tool which helps in solving issues

about following the rules and regulations while providing the services.

Benchmarking - It helps in improvement of the performance and accomplishment of

targets within stipulated period of time.

Ratios Formula UCK furnitures UCK woodwork's

ROCE(Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+

31930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/2310

6+31930

=0.68 times

8150/81230

=0.100 times

Operating profit

margin

Operating profit / sales *100 9490/13000+24900

*100

=25.03%

6955/81230*100

=8.56%

3.2 Contribution of management accounting to improve financial performance

The contribution can be described as follows:-

If standard costing tool will be used then it will help the management in knowing the risk

which is attached with the project. It is helpful in estimating the budgeted cost as well

(Stair and et. al., 2011).

If management accounting process will be implemented then price optimisation system

will be implemented which will be very effective in satisfying the customers as well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.3 Planning tools for accounting respond to solve financial issues

The various planning tools like forecasting and scenario are being used by the financial

managers for recognising the issues and making strategies which will be helpful in completing

the targets of the company. Planning tools also helps in formulation of annual budgets and

standards which improves existent performance of worker (Wagner, Moll and Newell, 2011).

KPI, benchmarking and financial governance are important tools helps to respond financial

problems.

CONCLUSION

From the above report, it can be concluded that management accounting is one of the

most effective process which is being implemented by the finance managers of the company.

Through this, various business operations of the company is being managed in an effective

manner which helps the company in achieving their goals and objectives in a fast manner. In this

report as well UCK furniture's managers is also making use of various methods so as to analyse

the cost of their efficiency which will later on help them in performing nicely. In this

report,various methods of cost analysis is also been discussed here and various planning tools

along with its merits and demerits are also discussed.

The various planning tools like forecasting and scenario are being used by the financial

managers for recognising the issues and making strategies which will be helpful in completing

the targets of the company. Planning tools also helps in formulation of annual budgets and

standards which improves existent performance of worker (Wagner, Moll and Newell, 2011).

KPI, benchmarking and financial governance are important tools helps to respond financial

problems.

CONCLUSION

From the above report, it can be concluded that management accounting is one of the

most effective process which is being implemented by the finance managers of the company.

Through this, various business operations of the company is being managed in an effective

manner which helps the company in achieving their goals and objectives in a fast manner. In this

report as well UCK furniture's managers is also making use of various methods so as to analyse

the cost of their efficiency which will later on help them in performing nicely. In this

report,various methods of cost analysis is also been discussed here and various planning tools

along with its merits and demerits are also discussed.

REFERENCES

Books and Journals

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Laudon, K. C. and Laudon, J. P., 2016. Management information system. Pearson Education

India.

Liao, S. H., Chu, P. H. and Hsiao, P. Y., 2012. Data mining techniques and applications–A

decade review from 2000 to 2011. Expert systems with applications. 39(12). pp.11303-

11311.

Lukka, K. and Vinnari, E., 2014. Domain theory and method theory in management accounting

research. Accounting, Auditing & Accountability Journal. 27(8). pp.1308-1338.

Macintosh, N. B and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Otley, D and Emmanuel, K. M. C., 2013. Readings in accounting for management control.

Springer.

Petty, J. W. and et. al., 2015. Financial management: Principles and applications. Pearson

Higher Education AU.

Roy, A. and et. al., 2011, April. Energy management in mobile devices with the cinder operating

system. In Proceedings of the sixth conference on Computer systems (pp. 139-152).

ACM.

Stair, R. and et. al., 2011. Principles of information systems. Cengage Learning Australia.

Wagner, E. L., Moll, J. and Newell, S., 2011. Accounting logics, reconfiguration of ERP systems

and the emergence of new accounting practices: A sociomaterial perspective.

Management Accounting Research. 22(3). pp.181-197.

Online:

What is absorption costing? 2017. [Online]. Available through

:<https://www.accountingcoach.com/blog/absorption-costing>.

Budgetary control, 2017. [Online]. Available

through<http://www.fao.org/docrep/w4343e/w4343e05.htm>.

Books and Journals

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Laudon, K. C. and Laudon, J. P., 2016. Management information system. Pearson Education

India.

Liao, S. H., Chu, P. H. and Hsiao, P. Y., 2012. Data mining techniques and applications–A

decade review from 2000 to 2011. Expert systems with applications. 39(12). pp.11303-

11311.

Lukka, K. and Vinnari, E., 2014. Domain theory and method theory in management accounting

research. Accounting, Auditing & Accountability Journal. 27(8). pp.1308-1338.

Macintosh, N. B and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Otley, D and Emmanuel, K. M. C., 2013. Readings in accounting for management control.

Springer.

Petty, J. W. and et. al., 2015. Financial management: Principles and applications. Pearson

Higher Education AU.

Roy, A. and et. al., 2011, April. Energy management in mobile devices with the cinder operating

system. In Proceedings of the sixth conference on Computer systems (pp. 139-152).

ACM.

Stair, R. and et. al., 2011. Principles of information systems. Cengage Learning Australia.

Wagner, E. L., Moll, J. and Newell, S., 2011. Accounting logics, reconfiguration of ERP systems

and the emergence of new accounting practices: A sociomaterial perspective.

Management Accounting Research. 22(3). pp.181-197.

Online:

What is absorption costing? 2017. [Online]. Available through

:<https://www.accountingcoach.com/blog/absorption-costing>.

Budgetary control, 2017. [Online]. Available

through<http://www.fao.org/docrep/w4343e/w4343e05.htm>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.