Management Accounting Project: UCK Group Financial Analysis

VerifiedAdded on 2020/07/22

|12

|2559

|69

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on the financial performance of the UCK group. It begins with an introduction to management accounting and its role in effective business operations. The report then delves into diverse costing methods, including historical, absorption, and marginal costing, and their application in income statement preparation. A comparative analysis of marginal and absorption costing is presented, highlighting their respective advantages and disadvantages. The report further explores budgetary control, outlining the merits and demerits of planning tools like forecasting, scenario analysis, and contingency planning. High-low method forecasting is applied to estimate variable costs for specific months, followed by a cash flow estimation. Finally, the report examines the adoption of various accounting systems to determine financial problems, including the use of financial ratios such as ROCE and operating profit margin, to assess the financial health of UCK woodworks and UCK furnitures.

MANAGEMENT

ACCOUNTING

PROJECT - 2

ACCOUNTING

PROJECT - 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Diverse cost and tools use while implementing income statements:....................................1

1.2: Different range of management accounting techniques:......................................................3

1.3 Interpretation of both costing methods used to assess net profits:........................................3

TASK 2............................................................................................................................................4

2.1: Merits and demerits of implementing planning tools implemented in the budgetary

control:........................................................................................................................................4

2.2 High and low method forecasting needed for July and August:...........................................5

2.3: Cash flow estimation............................................................................................................5

TASK 3............................................................................................................................................6

3.1: Adoption of various accounting system in order to determine financial problems:............6

3.2: Making analysis to overcome financial issues:....................................................................7

CONCLUSION................................................................................................................................7

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Diverse cost and tools use while implementing income statements:....................................1

1.2: Different range of management accounting techniques:......................................................3

1.3 Interpretation of both costing methods used to assess net profits:........................................3

TASK 2............................................................................................................................................4

2.1: Merits and demerits of implementing planning tools implemented in the budgetary

control:........................................................................................................................................4

2.2 High and low method forecasting needed for July and August:...........................................5

2.3: Cash flow estimation............................................................................................................5

TASK 3............................................................................................................................................6

3.1: Adoption of various accounting system in order to determine financial problems:............6

3.2: Making analysis to overcome financial issues:....................................................................7

CONCLUSION................................................................................................................................7

INTRODUCTION

Management accounting is the tool which is used by the company's management

accountant who are keen to make the operations in an effective manner. However, this is the best

part via which the company can make an effective efforts. Here, various tools are used by the

management accountant for gaining the decisions in order to gain an effective strategy. Various

strategies are used by the organisation for gaining sustainability (Zang, 2011). By taking help of

management accounting tools, manager are not only required to record cost of transaction but all

those influence and direction which is mostly affect on the business activities.

In this report, there is a short discussion about diverse costing methods that were helpful

in assessing total profits for UCK group of the organisation. In addition to this, this report is

totally delivered vast information related to the financial constraints and their respective

measures in order to overcome them henceforth, effective results can be identified.

TASK 1

1.1 Diverse cost and tools use while implementing income statements:

In each producing business, they required to handle their work in higher and in an

efficient manner for gaining desired outcomes. This is an efficient recording of each costs that

which is covered in a organisation so that they could be used in order to form valuable changes

in the operational department of a company. Cost is a kind of value of amount through which

manager can gather something. These are those costs that are directly or indirectly linked up with

the manufacturing process. Cost accounting is a kind of recording, classifying and assessing and

diverse alternative course of action for gaining control on a entire costs.

This is an accounting tools which would render aims for gathering an organisation's

entire costs of production via evaluating input costs of each of the process for producing sectors.

This is implemented to calculate and assess total costs that is linked with the manufacturing

projects. This is implemented to calculate and assess total costs which is going to the linked with

the manufacturing of goods. Henceforth, higher reliability outcomes will be produced for more

quick time (Setthasakko, 2010). There are diverse kinds of costs that would be charged at the

time of production process like direct, indirect, fixed and operating costs. Apart from that, there

are few other costs which are likewise implemented at the process. Some of them are discussed

as under:

1

Management accounting is the tool which is used by the company's management

accountant who are keen to make the operations in an effective manner. However, this is the best

part via which the company can make an effective efforts. Here, various tools are used by the

management accountant for gaining the decisions in order to gain an effective strategy. Various

strategies are used by the organisation for gaining sustainability (Zang, 2011). By taking help of

management accounting tools, manager are not only required to record cost of transaction but all

those influence and direction which is mostly affect on the business activities.

In this report, there is a short discussion about diverse costing methods that were helpful

in assessing total profits for UCK group of the organisation. In addition to this, this report is

totally delivered vast information related to the financial constraints and their respective

measures in order to overcome them henceforth, effective results can be identified.

TASK 1

1.1 Diverse cost and tools use while implementing income statements:

In each producing business, they required to handle their work in higher and in an

efficient manner for gaining desired outcomes. This is an efficient recording of each costs that

which is covered in a organisation so that they could be used in order to form valuable changes

in the operational department of a company. Cost is a kind of value of amount through which

manager can gather something. These are those costs that are directly or indirectly linked up with

the manufacturing process. Cost accounting is a kind of recording, classifying and assessing and

diverse alternative course of action for gaining control on a entire costs.

This is an accounting tools which would render aims for gathering an organisation's

entire costs of production via evaluating input costs of each of the process for producing sectors.

This is implemented to calculate and assess total costs that is linked with the manufacturing

projects. This is implemented to calculate and assess total costs which is going to the linked with

the manufacturing of goods. Henceforth, higher reliability outcomes will be produced for more

quick time (Setthasakko, 2010). There are diverse kinds of costs that would be charged at the

time of production process like direct, indirect, fixed and operating costs. Apart from that, there

are few other costs which are likewise implemented at the process. Some of them are discussed

as under:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Historical costs: This is the costs which are associated to the historical facts and figure.

This simply refers to the most effective value measuring process which is usable in accounting

under which the price of an assets on the balance sheet. This is normally relied upon its nominal

or genuine costs which is required to be achieved at the time of total manufacturing process. This

is the fixed measurement units assumptions.

Absorption costing: This is required to be known as the costs which is incurred on an

entire production of the services. Under this, all the costs which are related to the cost of

production considered. Fixed and variable costs are considered to be known as directly forming

impacts in the performance if a company. As entire costs are to be known as the identifying as

entire costing. Products costs is more than the costs which is known measure according to the

variable costing.

Marginal costing: This simply means to those costs which includes with an extra

manufacturing of products and services. This simply means to be the considered only variable

costs and fixed costs are ignored while calculating contribution. This kinds of costs are required

to be known as the period costs. The entire costs is much lower than those calculated as per the

absorption costs. Valuation of closing stock is lowering in marginal costing as compare to

absorption. This is highly reliable for intention of forming an effective decisions (Salehi,

Rostami and Mogadam, 2010).

Computing Net gain by preparing incomes statements though using marginal costing

PARTICULARS January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

less:

fixed manufacturing overheads 20000 20000

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

2

This simply refers to the most effective value measuring process which is usable in accounting

under which the price of an assets on the balance sheet. This is normally relied upon its nominal

or genuine costs which is required to be achieved at the time of total manufacturing process. This

is the fixed measurement units assumptions.

Absorption costing: This is required to be known as the costs which is incurred on an

entire production of the services. Under this, all the costs which are related to the cost of

production considered. Fixed and variable costs are considered to be known as directly forming

impacts in the performance if a company. As entire costs are to be known as the identifying as

entire costing. Products costs is more than the costs which is known measure according to the

variable costing.

Marginal costing: This simply means to those costs which includes with an extra

manufacturing of products and services. This simply means to be the considered only variable

costs and fixed costs are ignored while calculating contribution. This kinds of costs are required

to be known as the period costs. The entire costs is much lower than those calculated as per the

absorption costs. Valuation of closing stock is lowering in marginal costing as compare to

absorption. This is highly reliable for intention of forming an effective decisions (Salehi,

Rostami and Mogadam, 2010).

Computing Net gain by preparing incomes statements though using marginal costing

PARTICULARS January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

less:

fixed manufacturing overheads 20000 20000

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

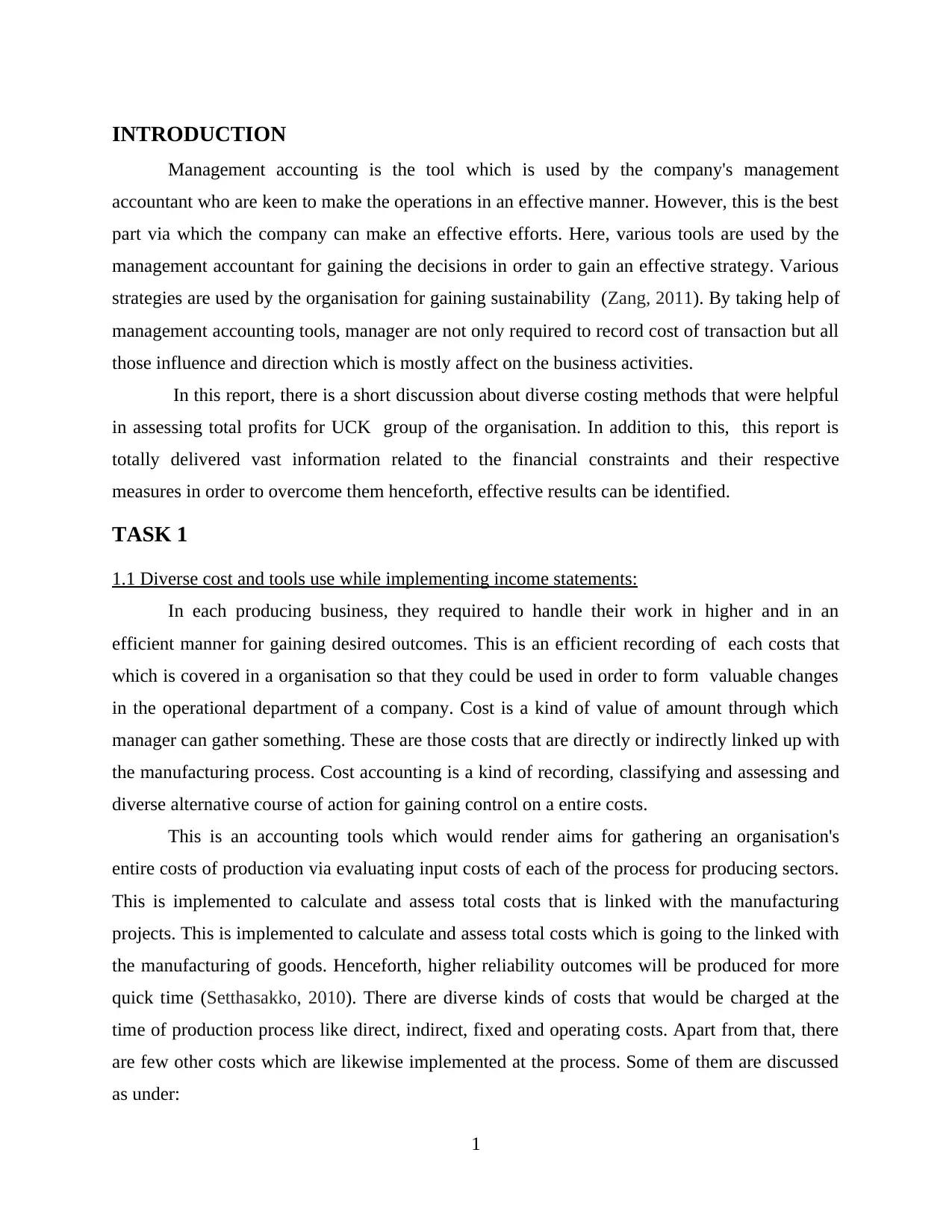

NET INCOME AS PER ABSORPTION

COSTING: January February

Sales (35per units) 315000 402500

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

NET INCOME AS PER ABSORPTION

COSTING: 8980 134210

1.2: Different range of management accounting techniques:

This is required to be known as the each business organisation, this can be said that

financial transaction is required to be done in highly systematic manner (Bromwich and

Bhimani, 2005). Management accounting is the one of the important aspects for UCK group of

organisation to assess their data by implementing valuable outcomes produced at the time. In

addition to this, this is mostly difficult in order to form assess nature of accounting tools.

Standard costing is implementing in highly operating situation and form comparison of actual

along with the budgeted outcomes. Budgetary control tools is the other crucial tools which is

helpful in analysing diverse activities of UCK business.

1.3 Interpretation of both costing methods used to assess net profits:

From the above mentioned calculation, this can be done that both marginal and

absorption costing, this can be found that the results are incorporated and these are different from

each other. The net profits addition from implementing marginal costing is 7000 for January and

133500 for February months. Whereas, by taking help of absorption costing would be 8980 and

134210 for similar months.

3

COSTING: January February

Sales (35per units) 315000 402500

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

NET INCOME AS PER ABSORPTION

COSTING: 8980 134210

1.2: Different range of management accounting techniques:

This is required to be known as the each business organisation, this can be said that

financial transaction is required to be done in highly systematic manner (Bromwich and

Bhimani, 2005). Management accounting is the one of the important aspects for UCK group of

organisation to assess their data by implementing valuable outcomes produced at the time. In

addition to this, this is mostly difficult in order to form assess nature of accounting tools.

Standard costing is implementing in highly operating situation and form comparison of actual

along with the budgeted outcomes. Budgetary control tools is the other crucial tools which is

helpful in analysing diverse activities of UCK business.

1.3 Interpretation of both costing methods used to assess net profits:

From the above mentioned calculation, this can be done that both marginal and

absorption costing, this can be found that the results are incorporated and these are different from

each other. The net profits addition from implementing marginal costing is 7000 for January and

133500 for February months. Whereas, by taking help of absorption costing would be 8980 and

134210 for similar months.

3

Advantages of marginal costing: This is required to be one of the most important

costing method which would assist for assessing total profits for the year. This is known

as the best suitable method for future decision making. The main part of costing is that

both variable and fixed costs are considered for making into consideration.

Disadvantages: To form a segregation of total costs into diverse variable is highly

difficult task (Horngren and et.al. 2002).

Advantages of absorption costing: As per the variable costing, absorption costing is

delivered effectively representation of a product cost via fixed manufacturing overhead

costs.

Demerits: There are various investors who presumes that this would be not effectively

reliable for future decision-making.

TASK 2

2.1: Merits and demerits of implementing planning tools implemented in the budgetary control:

In each organisation, planning is a foremost aspects that would incorporate vast impacts

for enhancing goodwill of the organisation. They are needed to have much effective system

which would help out for enhancing profitability for a company. The main aim of the UCK

group is to form that expenditure would not reverse its total income incurred during the time.

Budgets is a forecasting of future costs which would going to invest by the organisation for the

manufacturing of furniture, desk (Chapman and et.al. 2006). This is a most effective financial

plan which is implemented at the time of efficient period of the time which are formed for one

year. This covers of planned sales, volume and total revenue. The total forecasting is

incorporated for a particular period of time in order to form sales estimation for the entire

working capital needs. For managing them, managers are mostly implemented for the aim of

incorporating entire assessment of producing optimum return for the organisation for a particular

period of time (Horngren and et.al. 2005). There are various planning tools which are used for

budgetary control. Some of them are as follows:

Forecasting tools: This is the most effective planning tools which assist the management

for addressing the uncertainties that could arise in the near future. These are started with diverse

assumptions which is relied upon the management experience, knowledge and assessment.

4

costing method which would assist for assessing total profits for the year. This is known

as the best suitable method for future decision making. The main part of costing is that

both variable and fixed costs are considered for making into consideration.

Disadvantages: To form a segregation of total costs into diverse variable is highly

difficult task (Horngren and et.al. 2002).

Advantages of absorption costing: As per the variable costing, absorption costing is

delivered effectively representation of a product cost via fixed manufacturing overhead

costs.

Demerits: There are various investors who presumes that this would be not effectively

reliable for future decision-making.

TASK 2

2.1: Merits and demerits of implementing planning tools implemented in the budgetary control:

In each organisation, planning is a foremost aspects that would incorporate vast impacts

for enhancing goodwill of the organisation. They are needed to have much effective system

which would help out for enhancing profitability for a company. The main aim of the UCK

group is to form that expenditure would not reverse its total income incurred during the time.

Budgets is a forecasting of future costs which would going to invest by the organisation for the

manufacturing of furniture, desk (Chapman and et.al. 2006). This is a most effective financial

plan which is implemented at the time of efficient period of the time which are formed for one

year. This covers of planned sales, volume and total revenue. The total forecasting is

incorporated for a particular period of time in order to form sales estimation for the entire

working capital needs. For managing them, managers are mostly implemented for the aim of

incorporating entire assessment of producing optimum return for the organisation for a particular

period of time (Horngren and et.al. 2005). There are various planning tools which are used for

budgetary control. Some of them are as follows:

Forecasting tools: This is the most effective planning tools which assist the management

for addressing the uncertainties that could arise in the near future. These are started with diverse

assumptions which is relied upon the management experience, knowledge and assessment.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages: The crucial advantages of implementing forecasting tools which is used to

incorporate decision related to the safeguarding future losses of the organisation.

Disadvantages: This is much difficult to form forecasting of future in a most appropriate

manner due to of their qualitative nature of forecasting.

Scenario tools: This is the most effective tool which is totally based on the scenario for

forming analysis of future. A group of executive fix in order to incorporate a small number of

scenario that will help out for dealing with diverse problems. This tool refers to their capability

to gather a vast range of possibilities in a great extent. This will help out for assessing current

trends and uncertainty.

Advantages: This will help out in getting higher level of production by avoiding all

those aspects which influence the performance of a company. Excess line of code could be easily

remove by addressing with major problems that can arise.

Disadvantages: These tools are much costs expensive tools of testing total costs for the

organisation. This is highly complex in order to maintain growth and uncertainties of UCK group

of organisation.

Contingencies tools: This will render a large funds, time and resources that could help

out for using them to unavoidable risk events. This risk is evaluating for each element during

introducing of budgeting process (Hoque, 2002).

Advantages: This is perfect tools for incorporating risk evaluating in order to have much

efficient outcomes for the organisation.

Disadvantages: Contingencies tools suffers from inappropriately of literature. This can

not be done higher efficiently tools as risk can't calculate accordingly (Ezzamel and et.al. 2003).

2.2 High and low method forecasting needed for July and August:

For aiming of assessing high and low activities level of variable costs are assessed by

measuring total costs of organisation.

(Total expenditure of high activity – Expenditure from low activity)

Total cost=

(Highest activity per hour spend – Lower hour spend)

Total Expenditure: (9820-7410) / (795-505)=8.31 Per units

5

incorporate decision related to the safeguarding future losses of the organisation.

Disadvantages: This is much difficult to form forecasting of future in a most appropriate

manner due to of their qualitative nature of forecasting.

Scenario tools: This is the most effective tool which is totally based on the scenario for

forming analysis of future. A group of executive fix in order to incorporate a small number of

scenario that will help out for dealing with diverse problems. This tool refers to their capability

to gather a vast range of possibilities in a great extent. This will help out for assessing current

trends and uncertainty.

Advantages: This will help out in getting higher level of production by avoiding all

those aspects which influence the performance of a company. Excess line of code could be easily

remove by addressing with major problems that can arise.

Disadvantages: These tools are much costs expensive tools of testing total costs for the

organisation. This is highly complex in order to maintain growth and uncertainties of UCK group

of organisation.

Contingencies tools: This will render a large funds, time and resources that could help

out for using them to unavoidable risk events. This risk is evaluating for each element during

introducing of budgeting process (Hoque, 2002).

Advantages: This is perfect tools for incorporating risk evaluating in order to have much

efficient outcomes for the organisation.

Disadvantages: Contingencies tools suffers from inappropriately of literature. This can

not be done higher efficiently tools as risk can't calculate accordingly (Ezzamel and et.al. 2003).

2.2 High and low method forecasting needed for July and August:

For aiming of assessing high and low activities level of variable costs are assessed by

measuring total costs of organisation.

(Total expenditure of high activity – Expenditure from low activity)

Total cost=

(Highest activity per hour spend – Lower hour spend)

Total Expenditure: (9820-7410) / (795-505)=8.31 Per units

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

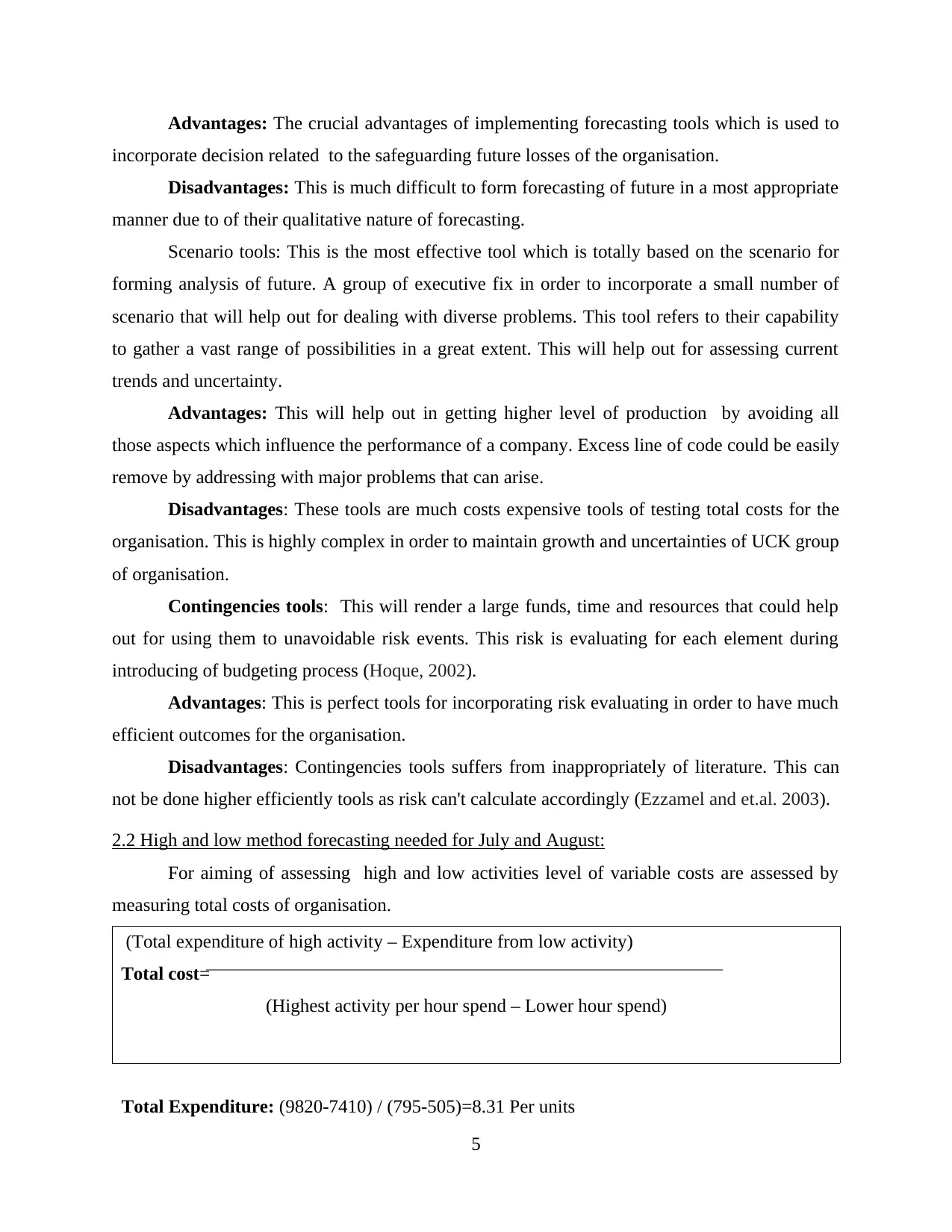

Total expense for the month of July:

= 650*8.31=5401.5

For August:

= 750*8.31= 6232.5

2.3: Cash flow estimation

Cash budget Amount

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Less:

Purchase -16800

Selling and administration

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash at the end of

September month 6848

TASK 3

3.1: Adoption of various accounting system in order to determine financial problems:

In case of production of business like UCK group of organisation covers of UCK furnitures and

Woodwork (Kotas, 2014). They are known as the working for assessing diverse financial issues

which could lead to form vast affects on the earnings position of the organisation.

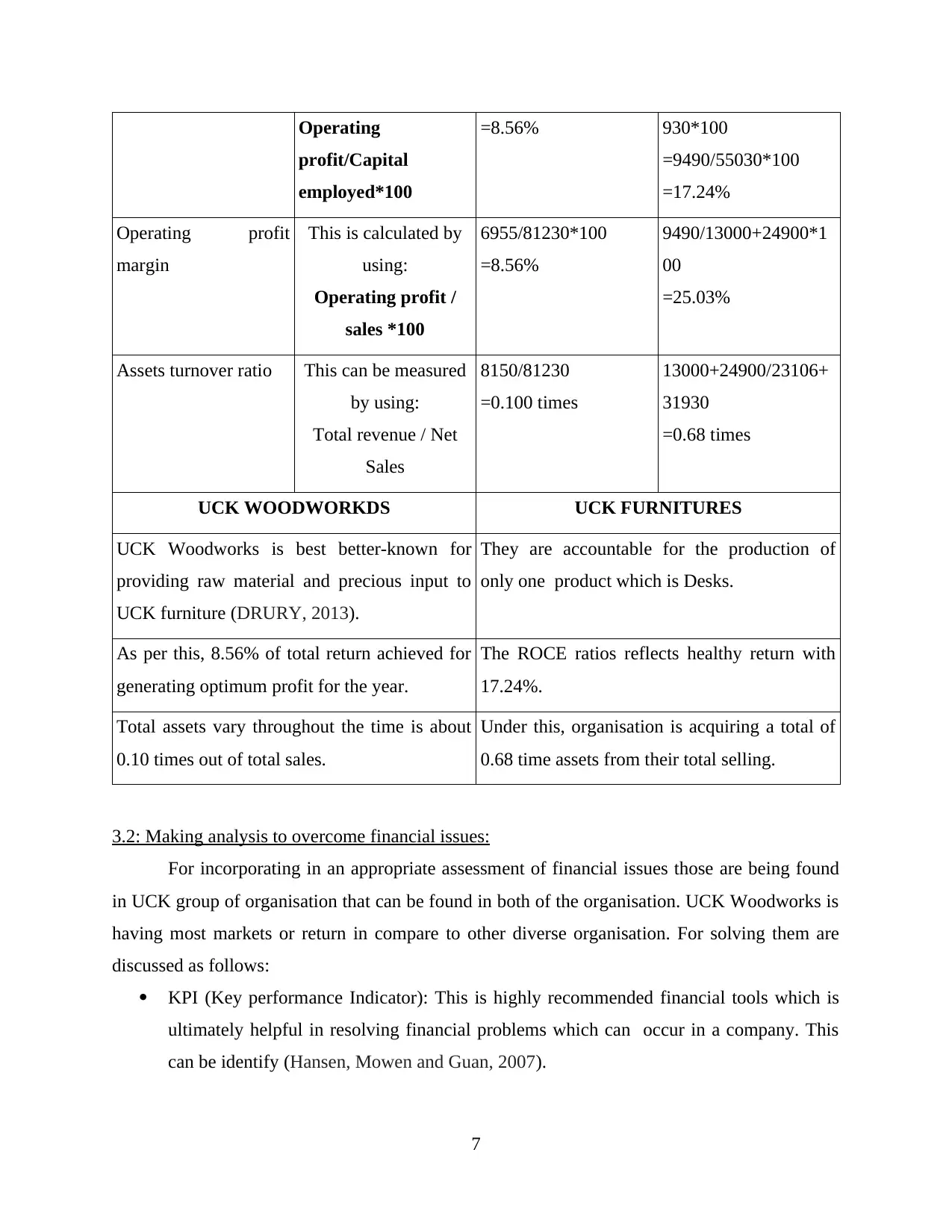

Various ratio's Formula UCK woodworks UCK furnitures

ROCE This is calculated by

using formula:

6955/81230*100 5890+3600/23100+31

6

= 650*8.31=5401.5

For August:

= 750*8.31= 6232.5

2.3: Cash flow estimation

Cash budget Amount

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Less:

Purchase -16800

Selling and administration

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash at the end of

September month 6848

TASK 3

3.1: Adoption of various accounting system in order to determine financial problems:

In case of production of business like UCK group of organisation covers of UCK furnitures and

Woodwork (Kotas, 2014). They are known as the working for assessing diverse financial issues

which could lead to form vast affects on the earnings position of the organisation.

Various ratio's Formula UCK woodworks UCK furnitures

ROCE This is calculated by

using formula:

6955/81230*100 5890+3600/23100+31

6

Operating

profit/Capital

employed*100

=8.56% 930*100

=9490/55030*100

=17.24%

Operating profit

margin

This is calculated by

using:

Operating profit /

sales *100

6955/81230*100

=8.56%

9490/13000+24900*1

00

=25.03%

Assets turnover ratio This can be measured

by using:

Total revenue / Net

Sales

8150/81230

=0.100 times

13000+24900/23106+

31930

=0.68 times

UCK WOODWORKDS UCK FURNITURES

UCK Woodworks is best better-known for

providing raw material and precious input to

UCK furniture (DRURY, 2013).

They are accountable for the production of

only one product which is Desks.

As per this, 8.56% of total return achieved for

generating optimum profit for the year.

The ROCE ratios reflects healthy return with

17.24%.

Total assets vary throughout the time is about

0.10 times out of total sales.

Under this, organisation is acquiring a total of

0.68 time assets from their total selling.

3.2: Making analysis to overcome financial issues:

For incorporating in an appropriate assessment of financial issues those are being found

in UCK group of organisation that can be found in both of the organisation. UCK Woodworks is

having most markets or return in compare to other diverse organisation. For solving them are

discussed as follows:

KPI (Key performance Indicator): This is highly recommended financial tools which is

ultimately helpful in resolving financial problems which can occur in a company. This

can be identify (Hansen, Mowen and Guan, 2007).

7

profit/Capital

employed*100

=8.56% 930*100

=9490/55030*100

=17.24%

Operating profit

margin

This is calculated by

using:

Operating profit /

sales *100

6955/81230*100

=8.56%

9490/13000+24900*1

00

=25.03%

Assets turnover ratio This can be measured

by using:

Total revenue / Net

Sales

8150/81230

=0.100 times

13000+24900/23106+

31930

=0.68 times

UCK WOODWORKDS UCK FURNITURES

UCK Woodworks is best better-known for

providing raw material and precious input to

UCK furniture (DRURY, 2013).

They are accountable for the production of

only one product which is Desks.

As per this, 8.56% of total return achieved for

generating optimum profit for the year.

The ROCE ratios reflects healthy return with

17.24%.

Total assets vary throughout the time is about

0.10 times out of total sales.

Under this, organisation is acquiring a total of

0.68 time assets from their total selling.

3.2: Making analysis to overcome financial issues:

For incorporating in an appropriate assessment of financial issues those are being found

in UCK group of organisation that can be found in both of the organisation. UCK Woodworks is

having most markets or return in compare to other diverse organisation. For solving them are

discussed as follows:

KPI (Key performance Indicator): This is highly recommended financial tools which is

ultimately helpful in resolving financial problems which can occur in a company. This

can be identify (Hansen, Mowen and Guan, 2007).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

From the above document this has been concluded that management accounting is an

effective tool that assist in keeping records of financial data in an appropriate manner. It assist in

controlling the inflow and outflow of cash which further assist in achieving the targets of a

particular financial year. Apart from this the concept of budget was also discussed in detail

which shows how they help in maintaining balance in the expense of different departments.

8

From the above document this has been concluded that management accounting is an

effective tool that assist in keeping records of financial data in an appropriate manner. It assist in

controlling the inflow and outflow of cash which further assist in achieving the targets of a

particular financial year. Apart from this the concept of budget was also discussed in detail

which shows how they help in maintaining balance in the expense of different departments.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

9

Books and Journals

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.