UGB 163 Introduction to Accounting & Finance: Company Analysis

VerifiedAdded on 2022/11/29

|17

|3767

|152

Report

AI Summary

This report provides a comprehensive analysis of accounting and finance principles through the examination of three companies: Racca Limited, Stockstone Limited, and Rockham Plc. For Racca Limited, the report includes an income statement and balance sheet, revealing the company's financial performance and position. Stockstone Limited's analysis covers contribution margin, break-even point, margin of safety, and profitability under different scenarios, along with a strategic recommendation. The report also identifies the underlying assumptions of the break-even model. For Rockham Plc, the analysis focuses on investment appraisal techniques, including payback period, net present value (NPV), and accounting rate of return (ARR), offering a recommendation based on these metrics. The merits and limitations of these investment appraisal techniques are discussed, as well as the benefits and limitations of using budgets for strategic planning. The report concludes with an overall assessment of the financial health and investment potential of the companies analyzed.

Introduction to

Accounting and Finance

Accounting and Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

PART A - Racca Limited................................................................................................................................3

Income Statement...................................................................................................................................3

Balance sheet..........................................................................................................................................4

PART B – Stock stone Limited......................................................................................................................5

(a) Contribution.......................................................................................................................................6

(b) Break even point and margin of safety..............................................................................................7

(c) Calculate profit...................................................................................................................................7

(d) Good strategy for Stockstones Ltd.....................................................................................................8

(e) Identify and explain the underpinning assumptions attached to the break-even model...................8

PART C – Rockham Plc.................................................................................................................................9

Calculation...............................................................................................................................................9

(b) Merits and limitations of different Investment appraisal techniques-.............................................11

(C) Benefits and limitations of using budgets as a tool for strategic planning.......................................12

CONCLUSION.............................................................................................................................................14

REFERENCES..............................................................................................................................................15

INTRODUCTION...........................................................................................................................................3

PART A - Racca Limited................................................................................................................................3

Income Statement...................................................................................................................................3

Balance sheet..........................................................................................................................................4

PART B – Stock stone Limited......................................................................................................................5

(a) Contribution.......................................................................................................................................6

(b) Break even point and margin of safety..............................................................................................7

(c) Calculate profit...................................................................................................................................7

(d) Good strategy for Stockstones Ltd.....................................................................................................8

(e) Identify and explain the underpinning assumptions attached to the break-even model...................8

PART C – Rockham Plc.................................................................................................................................9

Calculation...............................................................................................................................................9

(b) Merits and limitations of different Investment appraisal techniques-.............................................11

(C) Benefits and limitations of using budgets as a tool for strategic planning.......................................12

CONCLUSION.............................................................................................................................................14

REFERENCES..............................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Accounting and finance both are important for any business entity to manage operations in

effective manner. The collection and analysis of company operations are referred to as finance

and accounting. Monitoring inbound and outbound network cash flow will help to avoid failures

by allowing creating better decisions. Finance is a wide phrase that encompasses bankers,

finance, finance, stock exchanges, currency, and securities, among other things. Money, banking,

loans, stocks, resources, and responsibilities are all part of financial systems, and finance is

responsible for overseeing, creating, and studying them. Accounting plays a crucial part in the

efficient operation of a corporate organisation by documenting company transactions in a

methodical manner (Li, Ying, Chen and Zhang, 2020). Through systematic preservation of

financial statement and accessibility towards these statements when and where necessary, it also

delivers additional thoughts to organisation and its clients including such borrowers, financiers,

financial regulators, investors, and providers. Accounting is essentially a data management

system. It is essentially intended to assist multiple stakeholders in various decision-making

processes with required, accurate and available details.

PART A - Racca Limited

Income Statement

A profit and loss statement is a statement of a company's taxes and expenditure over a

certain timeframe. A financial statement is also known as a P&L, an income statement, a

statement of comprehensive income, revenue and expense declaration, or a financial outcomes

declaration. The profit and loss statement (P&L) informs managers and shareholders if a firm

made a profit or lost money during the reporting period. The income statement's objective is to

forecast a company's overall condition over a particular time period. Control account, which is

provided by daily diary entries, is used to construct financial reports for a business. Profits,

losses, maintenance costs, variability, operational expenditures, and so on may all be calculated

using an income statement. It's being used to analyse a firm alongside the profit and loss account

statement. The analysis of the income statement allows a business and some other annual

financial readers to determine if the firm is able to market its current products (Wang, Yu and

Zhang, 2019).

Accounting and finance both are important for any business entity to manage operations in

effective manner. The collection and analysis of company operations are referred to as finance

and accounting. Monitoring inbound and outbound network cash flow will help to avoid failures

by allowing creating better decisions. Finance is a wide phrase that encompasses bankers,

finance, finance, stock exchanges, currency, and securities, among other things. Money, banking,

loans, stocks, resources, and responsibilities are all part of financial systems, and finance is

responsible for overseeing, creating, and studying them. Accounting plays a crucial part in the

efficient operation of a corporate organisation by documenting company transactions in a

methodical manner (Li, Ying, Chen and Zhang, 2020). Through systematic preservation of

financial statement and accessibility towards these statements when and where necessary, it also

delivers additional thoughts to organisation and its clients including such borrowers, financiers,

financial regulators, investors, and providers. Accounting is essentially a data management

system. It is essentially intended to assist multiple stakeholders in various decision-making

processes with required, accurate and available details.

PART A - Racca Limited

Income Statement

A profit and loss statement is a statement of a company's taxes and expenditure over a

certain timeframe. A financial statement is also known as a P&L, an income statement, a

statement of comprehensive income, revenue and expense declaration, or a financial outcomes

declaration. The profit and loss statement (P&L) informs managers and shareholders if a firm

made a profit or lost money during the reporting period. The income statement's objective is to

forecast a company's overall condition over a particular time period. Control account, which is

provided by daily diary entries, is used to construct financial reports for a business. Profits,

losses, maintenance costs, variability, operational expenditures, and so on may all be calculated

using an income statement. It's being used to analyse a firm alongside the profit and loss account

statement. The analysis of the income statement allows a business and some other annual

financial readers to determine if the firm is able to market its current products (Wang, Yu and

Zhang, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

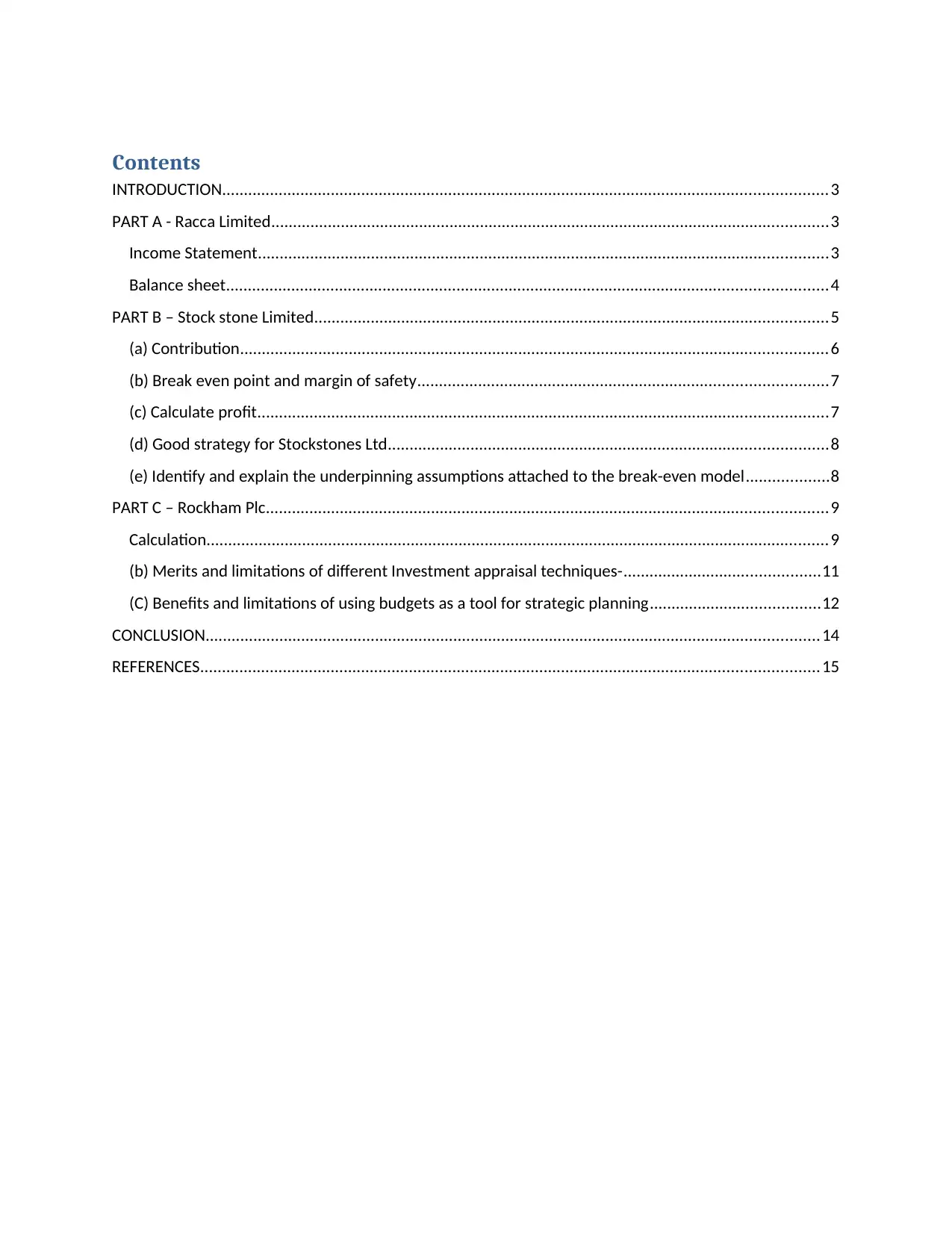

Income Statement for the year ended 31st December 2019

Particulars Amount Particulars Amount

To Opening Inventory 160000 By Sales 1400000

To Purchase 840000 By Closing Inventory 100000

To Wages 440000

Add: Outstanding 20000 460000

To Gross Profit 40000

1500000 1500000

To Heat and Light 80000 By Gross Profit 40000

Add: Outstanding gas

payment 8000 72000

To Sundry Expenses 170000

Less: Prepaid Rent 44000 126000

To Depreciation 96000

To Net Loss -254000

Total 40000 Total 4000

As per the above statement it has been analyzed that Racca Limited generate 40,000

gross profits after the set up all the costs and net loss of the company was 254000. It presents that

company has not good performance to survive in effective manner. There are required to manage

all the expenses in proper manner and take right decision in regard of the business activities.

Balance sheet

A report is a financial statement that shows the assets and liabilities of a corporation at a

certain point in time. That is one of the three fundamental accounting records used to assess

financial operations. A balance sheet is a document that shareholders and investors use to obtain

a sense of a company budgetary condition. It allows them to evaluate the pace wherein the firm

Particulars Amount Particulars Amount

To Opening Inventory 160000 By Sales 1400000

To Purchase 840000 By Closing Inventory 100000

To Wages 440000

Add: Outstanding 20000 460000

To Gross Profit 40000

1500000 1500000

To Heat and Light 80000 By Gross Profit 40000

Add: Outstanding gas

payment 8000 72000

To Sundry Expenses 170000

Less: Prepaid Rent 44000 126000

To Depreciation 96000

To Net Loss -254000

Total 40000 Total 4000

As per the above statement it has been analyzed that Racca Limited generate 40,000

gross profits after the set up all the costs and net loss of the company was 254000. It presents that

company has not good performance to survive in effective manner. There are required to manage

all the expenses in proper manner and take right decision in regard of the business activities.

Balance sheet

A report is a financial statement that shows the assets and liabilities of a corporation at a

certain point in time. That is one of the three fundamental accounting records used to assess

financial operations. A balance sheet is a document that shareholders and investors use to obtain

a sense of a company budgetary condition. It allows them to evaluate the pace wherein the firm

makes profits or compares income and expenses to estimate the corporation's viability.

Combining different or even more capital reserves from various periods of time might reveal

how a company has evolved. The balance sheet is an indication of a company's financial health

and wellbeing (Shen, 2021). This always employs the formula Assets = Liabilities + Equity to

list a company's assets, debts, and ownership. A balance sheet usually maintains a certain

structure, but based on the location of organization, it may have various payments. By examining

a company's financial statements across history, significant accounting reporting may be

uncovered.

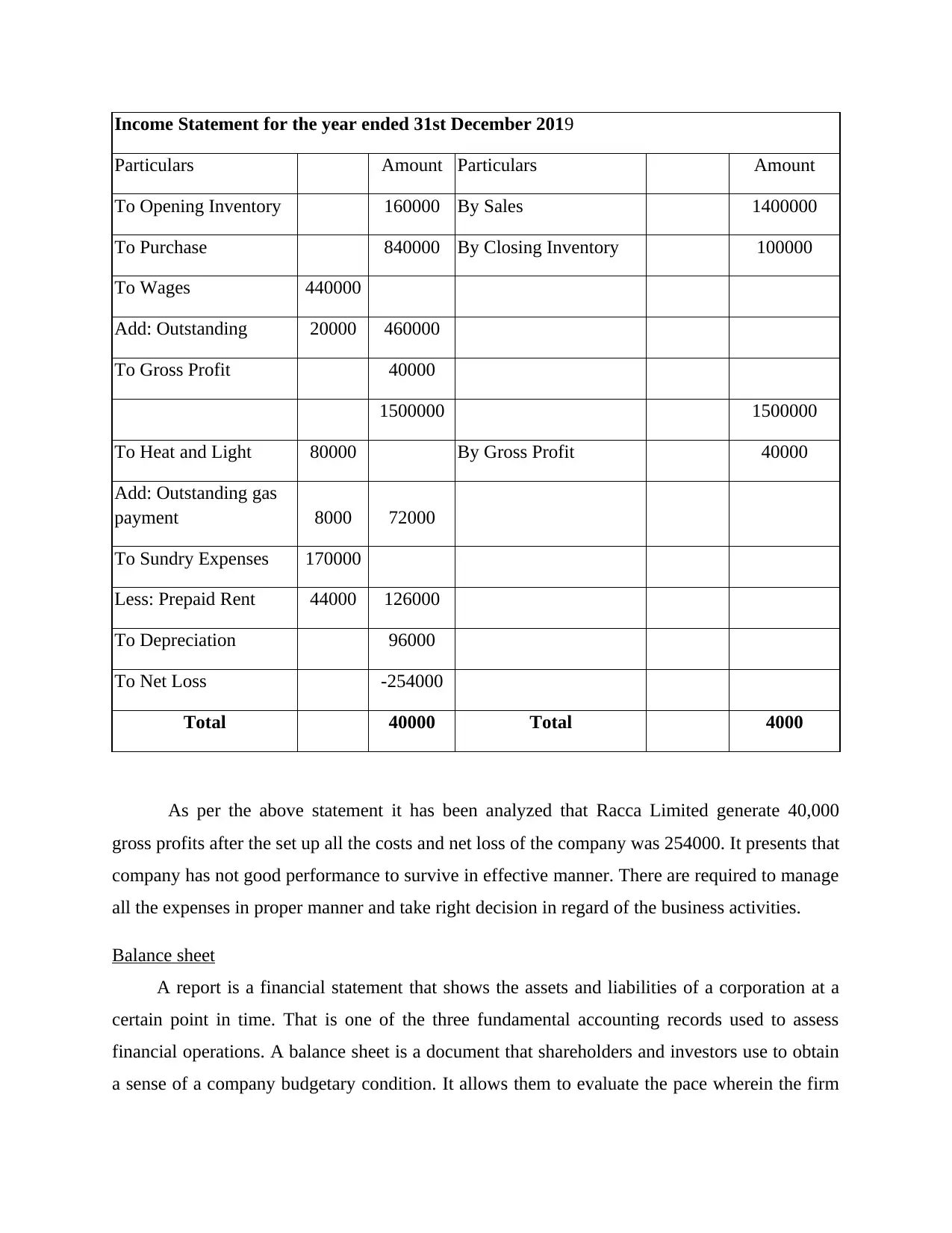

Balance Sheet as on 31st December, 2019

Liabilities Assets

Capital 960000 Furniture and Fittings 480000

Less: Drawings 110000 Less: Depreciation 96000 384000

Net Profit -254000 596000

Trade Receivables 160000

Bank Overdraft 80000 Inventory 100000

Outstanding Wages 20000 Prepaid Rent 44000

Outstanding Gas

payment 8000 Other Current Assets 16000

Total 704000 Total 704000

PART B – Stock stone Limited

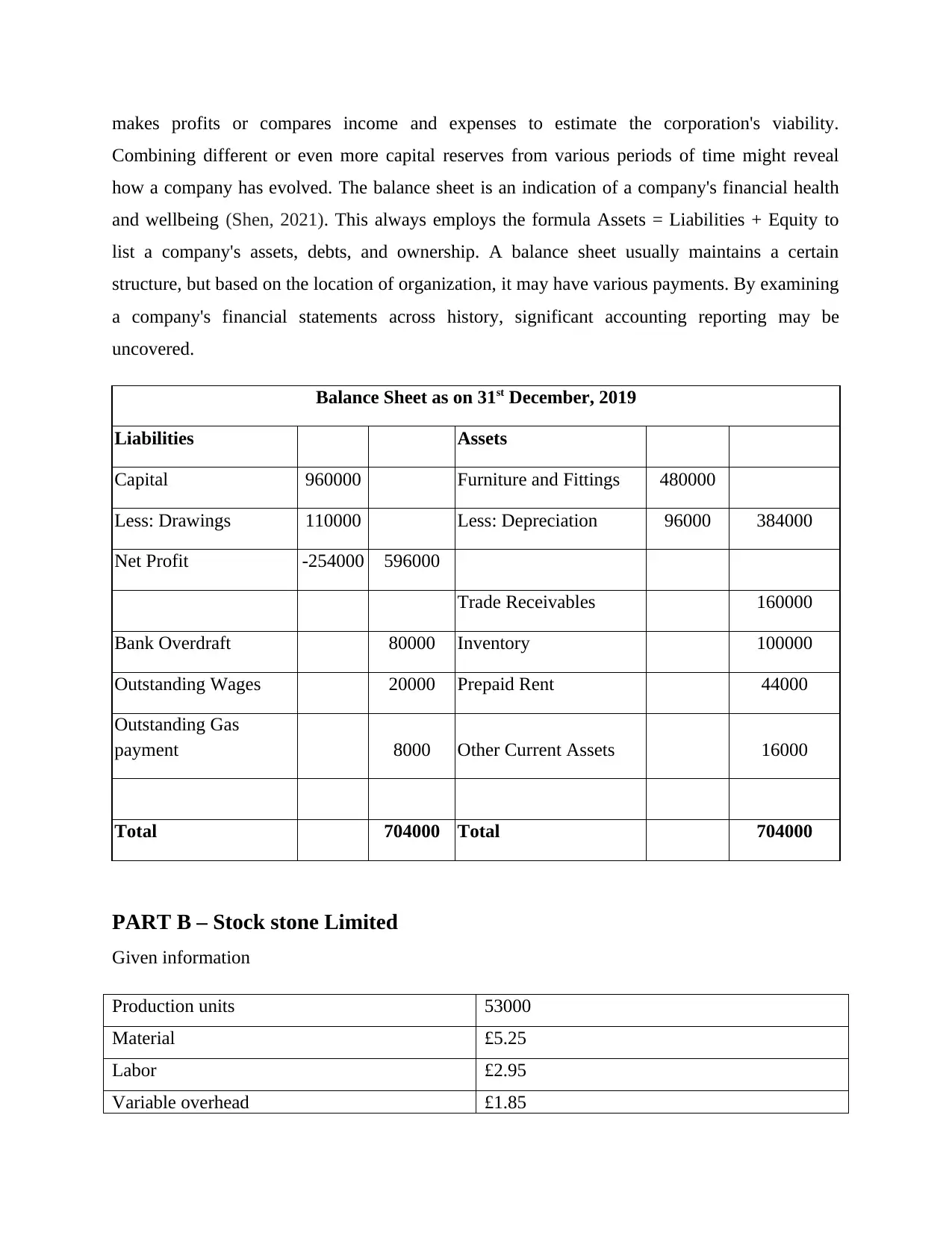

Given information

Production units 53000

Material £5.25

Labor £2.95

Variable overhead £1.85

Combining different or even more capital reserves from various periods of time might reveal

how a company has evolved. The balance sheet is an indication of a company's financial health

and wellbeing (Shen, 2021). This always employs the formula Assets = Liabilities + Equity to

list a company's assets, debts, and ownership. A balance sheet usually maintains a certain

structure, but based on the location of organization, it may have various payments. By examining

a company's financial statements across history, significant accounting reporting may be

uncovered.

Balance Sheet as on 31st December, 2019

Liabilities Assets

Capital 960000 Furniture and Fittings 480000

Less: Drawings 110000 Less: Depreciation 96000 384000

Net Profit -254000 596000

Trade Receivables 160000

Bank Overdraft 80000 Inventory 100000

Outstanding Wages 20000 Prepaid Rent 44000

Outstanding Gas

payment 8000 Other Current Assets 16000

Total 704000 Total 704000

PART B – Stock stone Limited

Given information

Production units 53000

Material £5.25

Labor £2.95

Variable overhead £1.85

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

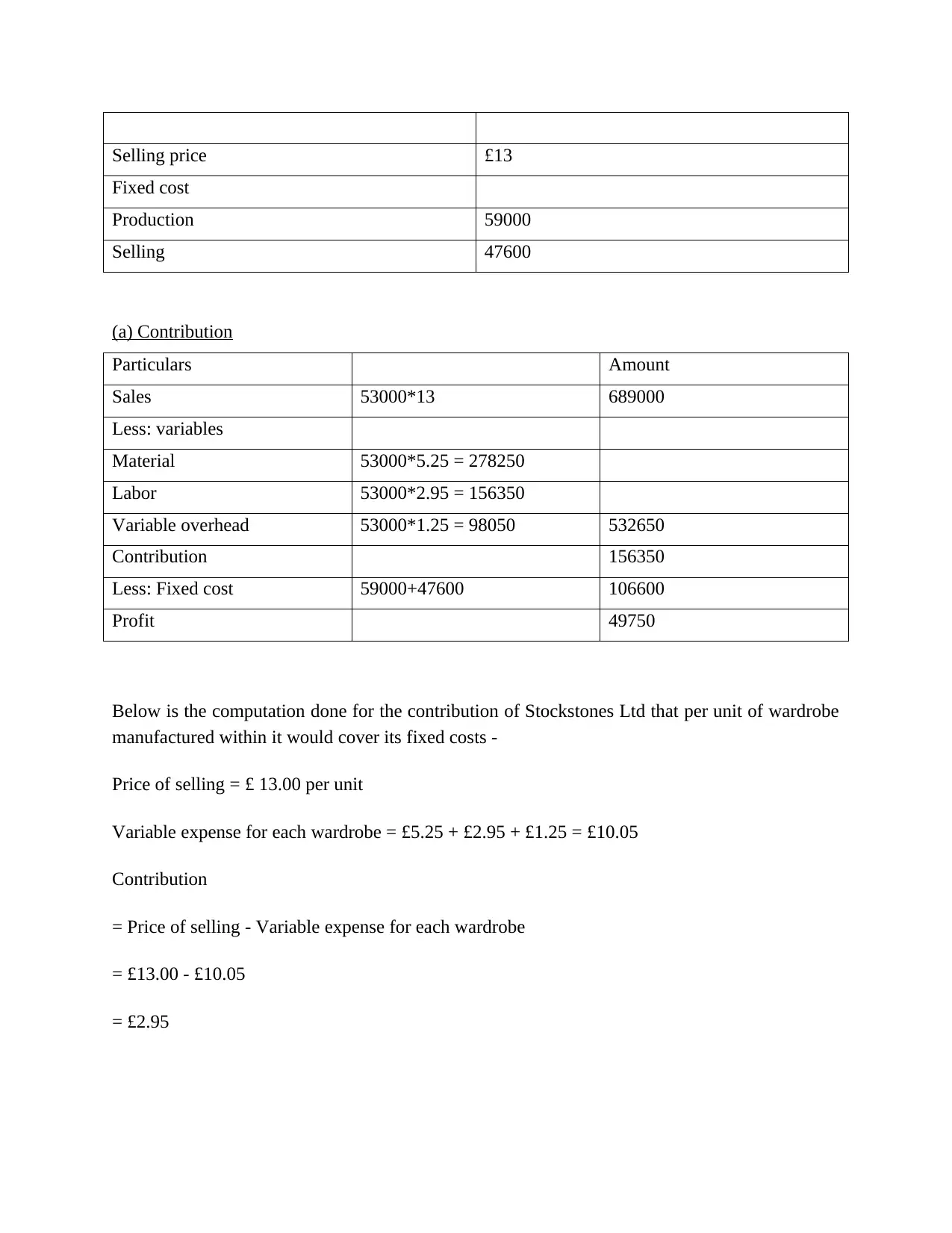

Selling price £13

Fixed cost

Production 59000

Selling 47600

(a) Contribution

Particulars Amount

Sales 53000*13 689000

Less: variables

Material 53000*5.25 = 278250

Labor 53000*2.95 = 156350

Variable overhead 53000*1.25 = 98050 532650

Contribution 156350

Less: Fixed cost 59000+47600 106600

Profit 49750

Below is the computation done for the contribution of Stockstones Ltd that per unit of wardrobe

manufactured within it would cover its fixed costs -

Price of selling = £ 13.00 per unit

Variable expense for each wardrobe = £5.25 + £2.95 + £1.25 = £10.05

Contribution

= Price of selling - Variable expense for each wardrobe

= £13.00 - £10.05

= £2.95

Fixed cost

Production 59000

Selling 47600

(a) Contribution

Particulars Amount

Sales 53000*13 689000

Less: variables

Material 53000*5.25 = 278250

Labor 53000*2.95 = 156350

Variable overhead 53000*1.25 = 98050 532650

Contribution 156350

Less: Fixed cost 59000+47600 106600

Profit 49750

Below is the computation done for the contribution of Stockstones Ltd that per unit of wardrobe

manufactured within it would cover its fixed costs -

Price of selling = £ 13.00 per unit

Variable expense for each wardrobe = £5.25 + £2.95 + £1.25 = £10.05

Contribution

= Price of selling - Variable expense for each wardrobe

= £13.00 - £10.05

= £2.95

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

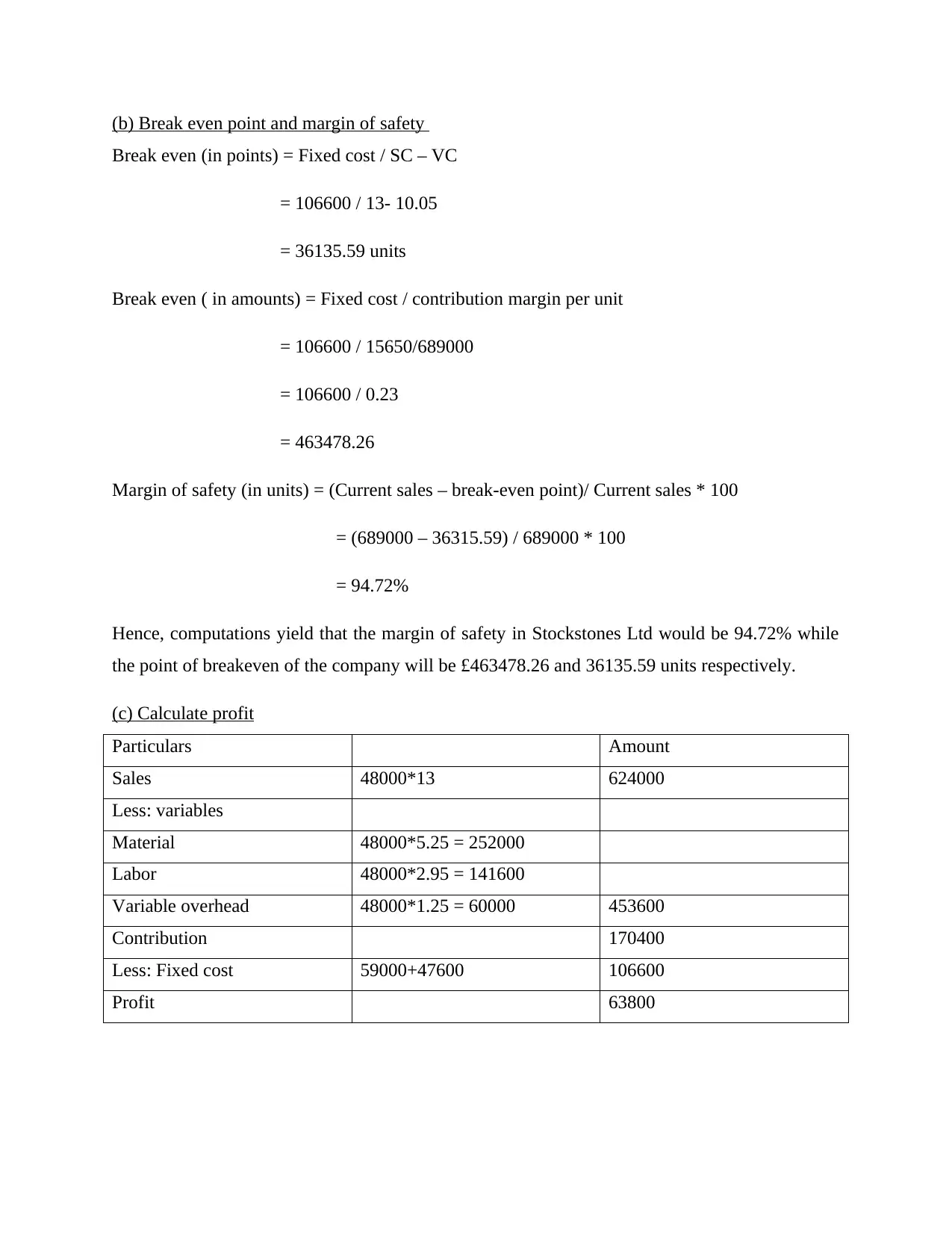

(b) Break even point and margin of safety

Break even (in points) = Fixed cost / SC – VC

= 106600 / 13- 10.05

= 36135.59 units

Break even ( in amounts) = Fixed cost / contribution margin per unit

= 106600 / 15650/689000

= 106600 / 0.23

= 463478.26

Margin of safety (in units) = (Current sales – break-even point)/ Current sales * 100

= (689000 – 36315.59) / 689000 * 100

= 94.72%

Hence, computations yield that the margin of safety in Stockstones Ltd would be 94.72% while

the point of breakeven of the company will be £463478.26 and 36135.59 units respectively.

(c) Calculate profit

Particulars Amount

Sales 48000*13 624000

Less: variables

Material 48000*5.25 = 252000

Labor 48000*2.95 = 141600

Variable overhead 48000*1.25 = 60000 453600

Contribution 170400

Less: Fixed cost 59000+47600 106600

Profit 63800

Break even (in points) = Fixed cost / SC – VC

= 106600 / 13- 10.05

= 36135.59 units

Break even ( in amounts) = Fixed cost / contribution margin per unit

= 106600 / 15650/689000

= 106600 / 0.23

= 463478.26

Margin of safety (in units) = (Current sales – break-even point)/ Current sales * 100

= (689000 – 36315.59) / 689000 * 100

= 94.72%

Hence, computations yield that the margin of safety in Stockstones Ltd would be 94.72% while

the point of breakeven of the company will be £463478.26 and 36135.59 units respectively.

(c) Calculate profit

Particulars Amount

Sales 48000*13 624000

Less: variables

Material 48000*5.25 = 252000

Labor 48000*2.95 = 141600

Variable overhead 48000*1.25 = 60000 453600

Contribution 170400

Less: Fixed cost 59000+47600 106600

Profit 63800

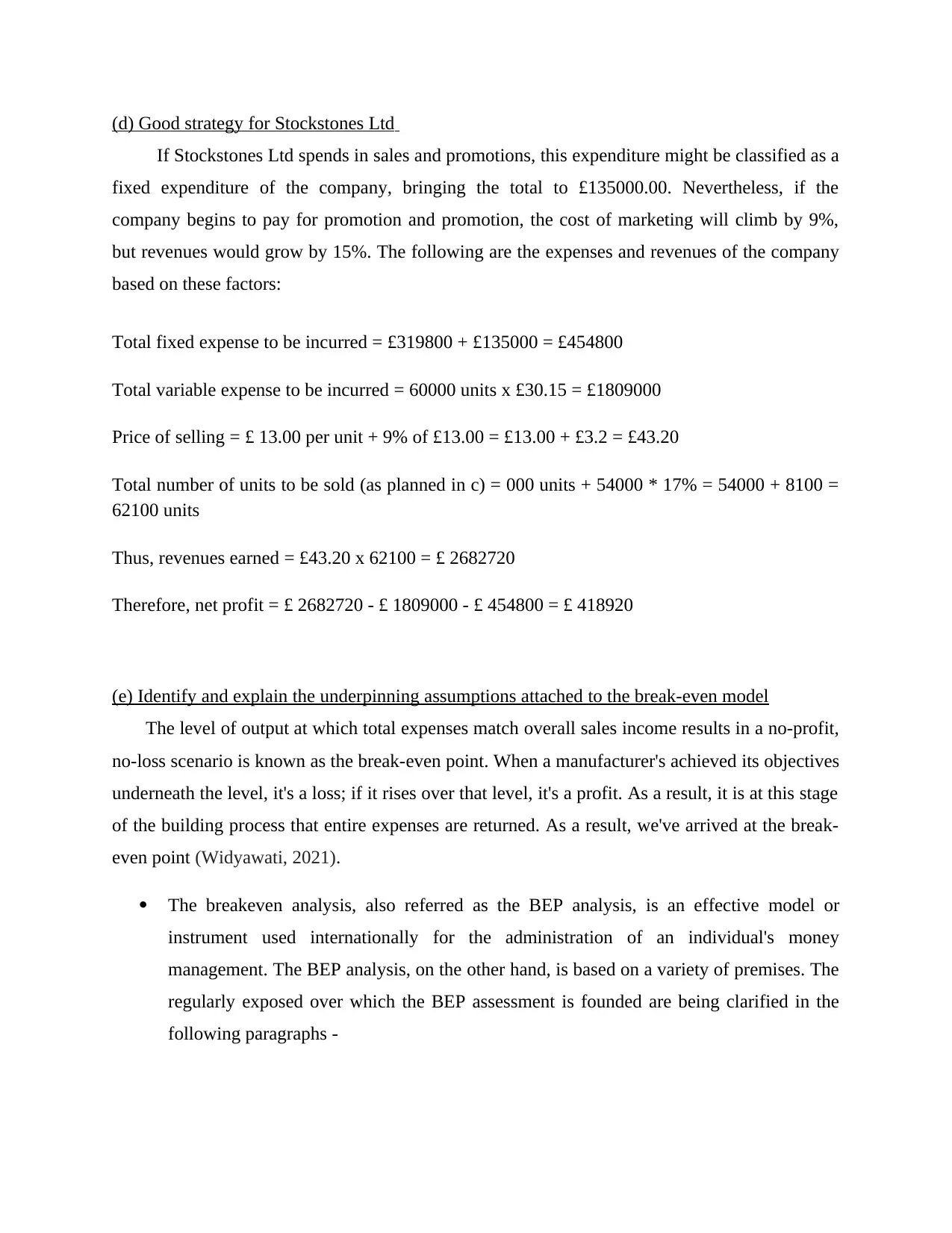

(d) Good strategy for Stockstones Ltd

If Stockstones Ltd spends in sales and promotions, this expenditure might be classified as a

fixed expenditure of the company, bringing the total to £135000.00. Nevertheless, if the

company begins to pay for promotion and promotion, the cost of marketing will climb by 9%,

but revenues would grow by 15%. The following are the expenses and revenues of the company

based on these factors:

Total fixed expense to be incurred = £319800 + £135000 = £454800

Total variable expense to be incurred = 60000 units x £30.15 = £1809000

Price of selling = £ 13.00 per unit + 9% of £13.00 = £13.00 + £3.2 = £43.20

Total number of units to be sold (as planned in c) = 000 units + 54000 * 17% = 54000 + 8100 =

62100 units

Thus, revenues earned = £43.20 x 62100 = £ 2682720

Therefore, net profit = £ 2682720 - £ 1809000 - £ 454800 = £ 418920

(e) Identify and explain the underpinning assumptions attached to the break-even model

The level of output at which total expenses match overall sales income results in a no-profit,

no-loss scenario is known as the break-even point. When a manufacturer's achieved its objectives

underneath the level, it's a loss; if it rises over that level, it's a profit. As a result, it is at this stage

of the building process that entire expenses are returned. As a result, we've arrived at the break-

even point (Widyawati, 2021).

The breakeven analysis, also referred as the BEP analysis, is an effective model or

instrument used internationally for the administration of an individual's money

management. The BEP analysis, on the other hand, is based on a variety of premises. The

regularly exposed over which the BEP assessment is founded are being clarified in the

following paragraphs -

If Stockstones Ltd spends in sales and promotions, this expenditure might be classified as a

fixed expenditure of the company, bringing the total to £135000.00. Nevertheless, if the

company begins to pay for promotion and promotion, the cost of marketing will climb by 9%,

but revenues would grow by 15%. The following are the expenses and revenues of the company

based on these factors:

Total fixed expense to be incurred = £319800 + £135000 = £454800

Total variable expense to be incurred = 60000 units x £30.15 = £1809000

Price of selling = £ 13.00 per unit + 9% of £13.00 = £13.00 + £3.2 = £43.20

Total number of units to be sold (as planned in c) = 000 units + 54000 * 17% = 54000 + 8100 =

62100 units

Thus, revenues earned = £43.20 x 62100 = £ 2682720

Therefore, net profit = £ 2682720 - £ 1809000 - £ 454800 = £ 418920

(e) Identify and explain the underpinning assumptions attached to the break-even model

The level of output at which total expenses match overall sales income results in a no-profit,

no-loss scenario is known as the break-even point. When a manufacturer's achieved its objectives

underneath the level, it's a loss; if it rises over that level, it's a profit. As a result, it is at this stage

of the building process that entire expenses are returned. As a result, we've arrived at the break-

even point (Widyawati, 2021).

The breakeven analysis, also referred as the BEP analysis, is an effective model or

instrument used internationally for the administration of an individual's money

management. The BEP analysis, on the other hand, is based on a variety of premises. The

regularly exposed over which the BEP assessment is founded are being clarified in the

following paragraphs -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

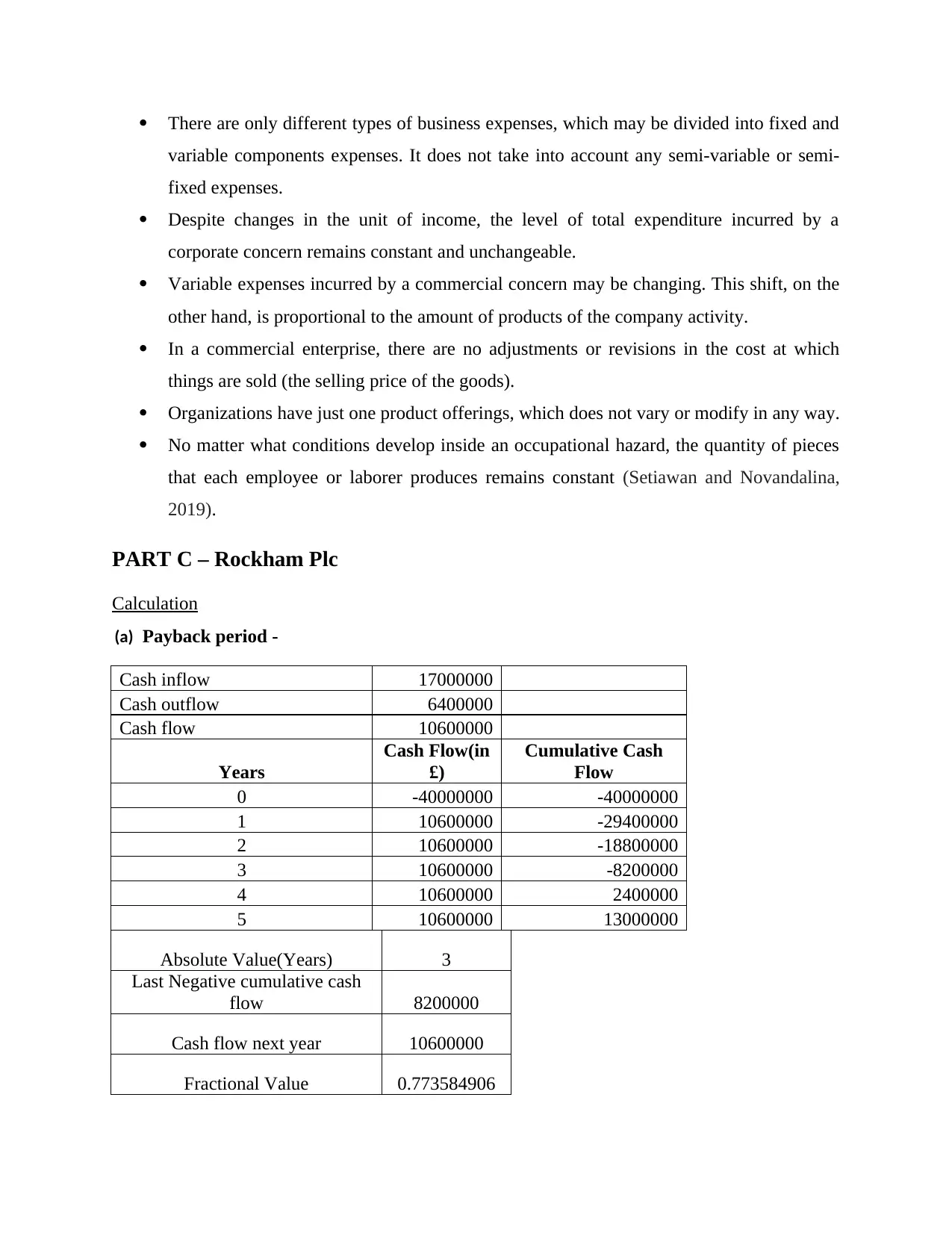

There are only different types of business expenses, which may be divided into fixed and

variable components expenses. It does not take into account any semi-variable or semi-

fixed expenses.

Despite changes in the unit of income, the level of total expenditure incurred by a

corporate concern remains constant and unchangeable.

Variable expenses incurred by a commercial concern may be changing. This shift, on the

other hand, is proportional to the amount of products of the company activity.

In a commercial enterprise, there are no adjustments or revisions in the cost at which

things are sold (the selling price of the goods).

Organizations have just one product offerings, which does not vary or modify in any way.

No matter what conditions develop inside an occupational hazard, the quantity of pieces

that each employee or laborer produces remains constant (Setiawan and Novandalina,

2019).

PART C – Rockham Plc

Calculation

(a) Payback period -

Cash inflow 17000000

Cash outflow 6400000

Cash flow 10600000

Years

Cash Flow(in

£)

Cumulative Cash

Flow

0 -40000000 -40000000

1 10600000 -29400000

2 10600000 -18800000

3 10600000 -8200000

4 10600000 2400000

5 10600000 13000000

Absolute Value(Years) 3

Last Negative cumulative cash

flow 8200000

Cash flow next year 10600000

Fractional Value 0.773584906

variable components expenses. It does not take into account any semi-variable or semi-

fixed expenses.

Despite changes in the unit of income, the level of total expenditure incurred by a

corporate concern remains constant and unchangeable.

Variable expenses incurred by a commercial concern may be changing. This shift, on the

other hand, is proportional to the amount of products of the company activity.

In a commercial enterprise, there are no adjustments or revisions in the cost at which

things are sold (the selling price of the goods).

Organizations have just one product offerings, which does not vary or modify in any way.

No matter what conditions develop inside an occupational hazard, the quantity of pieces

that each employee or laborer produces remains constant (Setiawan and Novandalina,

2019).

PART C – Rockham Plc

Calculation

(a) Payback period -

Cash inflow 17000000

Cash outflow 6400000

Cash flow 10600000

Years

Cash Flow(in

£)

Cumulative Cash

Flow

0 -40000000 -40000000

1 10600000 -29400000

2 10600000 -18800000

3 10600000 -8200000

4 10600000 2400000

5 10600000 13000000

Absolute Value(Years) 3

Last Negative cumulative cash

flow 8200000

Cash flow next year 10600000

Fractional Value 0.773584906

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

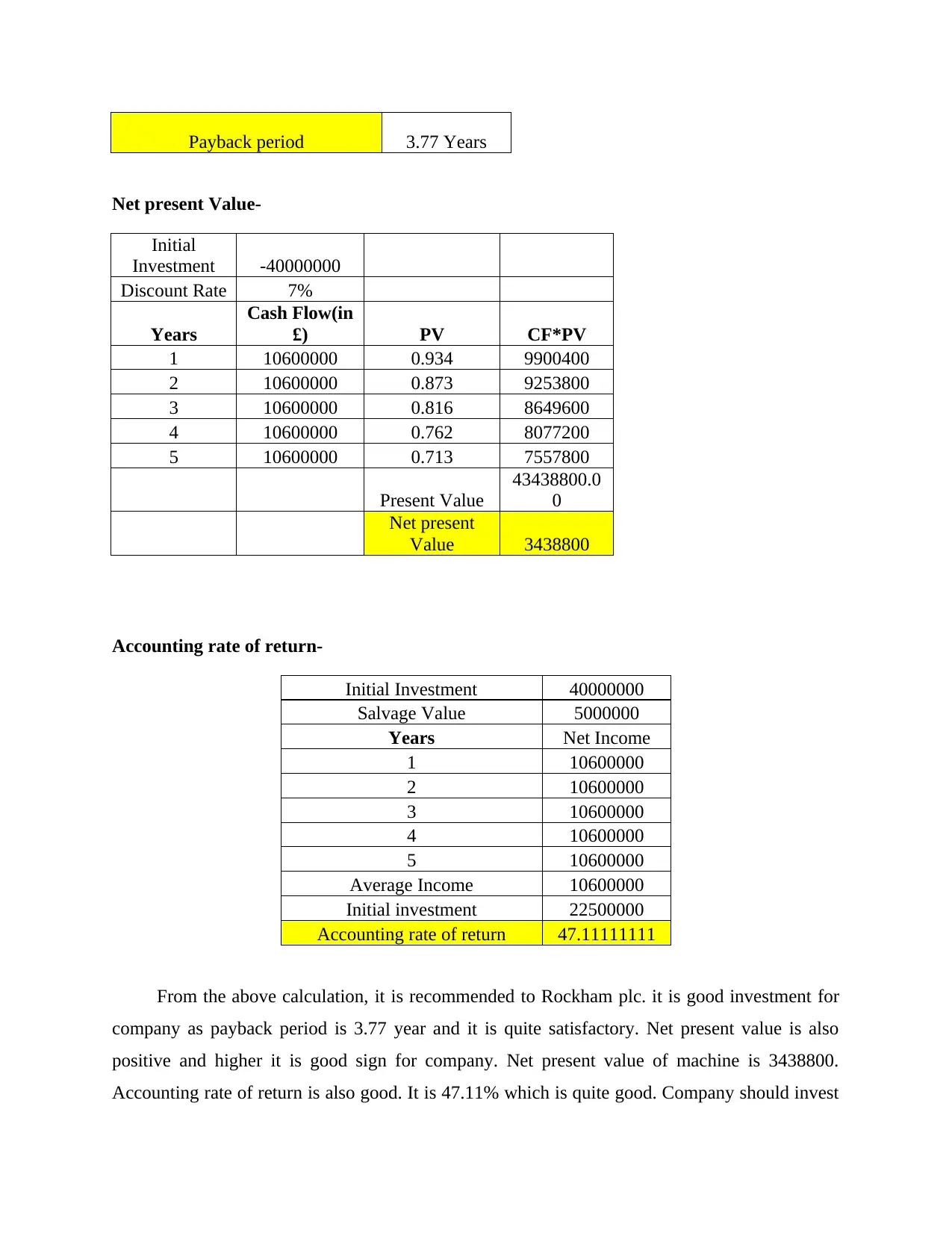

Payback period 3.77 Years

Net present Value-

Initial

Investment -40000000

Discount Rate 7%

Years

Cash Flow(in

£) PV CF*PV

1 10600000 0.934 9900400

2 10600000 0.873 9253800

3 10600000 0.816 8649600

4 10600000 0.762 8077200

5 10600000 0.713 7557800

Present Value

43438800.0

0

Net present

Value 3438800

Accounting rate of return-

Initial Investment 40000000

Salvage Value 5000000

Years Net Income

1 10600000

2 10600000

3 10600000

4 10600000

5 10600000

Average Income 10600000

Initial investment 22500000

Accounting rate of return 47.11111111

From the above calculation, it is recommended to Rockham plc. it is good investment for

company as payback period is 3.77 year and it is quite satisfactory. Net present value is also

positive and higher it is good sign for company. Net present value of machine is 3438800.

Accounting rate of return is also good. It is 47.11% which is quite good. Company should invest

Net present Value-

Initial

Investment -40000000

Discount Rate 7%

Years

Cash Flow(in

£) PV CF*PV

1 10600000 0.934 9900400

2 10600000 0.873 9253800

3 10600000 0.816 8649600

4 10600000 0.762 8077200

5 10600000 0.713 7557800

Present Value

43438800.0

0

Net present

Value 3438800

Accounting rate of return-

Initial Investment 40000000

Salvage Value 5000000

Years Net Income

1 10600000

2 10600000

3 10600000

4 10600000

5 10600000

Average Income 10600000

Initial investment 22500000

Accounting rate of return 47.11111111

From the above calculation, it is recommended to Rockham plc. it is good investment for

company as payback period is 3.77 year and it is quite satisfactory. Net present value is also

positive and higher it is good sign for company. Net present value of machine is 3438800.

Accounting rate of return is also good. It is 47.11% which is quite good. Company should invest

in this machinery as it is providing good return in future. It means purchase of new machine is

profitable for the company (Luo, 2019). Likewise, the NPV guidelines stipulate that investments

with a positive net present value (NPV) are permitted since they indicate success. In the situation

of the provides incentives that Rockham plc is considering, it is possible to discover that the

expenditure is not only suitable, but also very viable. This is due to the fact that this machine has

a short payback period and its ARR is substantially larger than its return on capital. The

machine's NPV, on the other hand, is rather high. As a result of evaluating all of these strategies

and considerations, Rockham plc has received excellent ratings and is stated to be embracing the

financing.

(b) Merits and limitations of different Investment appraisal techniques-

Investment appraisal techniques are Payback period, accounting rate of return and

discounting cash flow techniques such as NPV and IRR. Advantages and disadvantages are as

follows-

Payback Period:

Advantage-

It is very easy to calculate and understand.

It has less uncertainty.

It is very quick to identify when cash flow becomes positive.

Disadvantages-

Main disadvantage is after payback period it ignores all the cash flows.

Time value of money is avoided in this technique.

Accounting rate of return-

Advantages-

Calculation is very easy and also easy to understand.

It is popular among businesses because of its simplicity.

It undertakes all the cash flows till the end of life of project.

Main focus is on profitability.

profitable for the company (Luo, 2019). Likewise, the NPV guidelines stipulate that investments

with a positive net present value (NPV) are permitted since they indicate success. In the situation

of the provides incentives that Rockham plc is considering, it is possible to discover that the

expenditure is not only suitable, but also very viable. This is due to the fact that this machine has

a short payback period and its ARR is substantially larger than its return on capital. The

machine's NPV, on the other hand, is rather high. As a result of evaluating all of these strategies

and considerations, Rockham plc has received excellent ratings and is stated to be embracing the

financing.

(b) Merits and limitations of different Investment appraisal techniques-

Investment appraisal techniques are Payback period, accounting rate of return and

discounting cash flow techniques such as NPV and IRR. Advantages and disadvantages are as

follows-

Payback Period:

Advantage-

It is very easy to calculate and understand.

It has less uncertainty.

It is very quick to identify when cash flow becomes positive.

Disadvantages-

Main disadvantage is after payback period it ignores all the cash flows.

Time value of money is avoided in this technique.

Accounting rate of return-

Advantages-

Calculation is very easy and also easy to understand.

It is popular among businesses because of its simplicity.

It undertakes all the cash flows till the end of life of project.

Main focus is on profitability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.