UGB 225 Business Taxation: Alternative Assessment Report 2020/21

VerifiedAdded on 2022/12/29

|13

|3940

|85

Report

AI Summary

This report, addressing the UGB 225 Business Taxation Alternative Assessment for 2020/21, delves into various aspects of business taxation. It begins with an analysis of Linda's trading profits, calculating the taxable income after adjustments for disallowed expenses and non-taxable income. The report then explores the criteria for employment versus self-employment, outlining the advantages of self-employment, including control, tax benefits, growth potential, and customer interactions, while also discussing the reasons behind IR35 cases. The discussion continues with an examination of the six badges of trade, providing insights into factors such as profit-seeking motive, the number of transactions, and changes to assets. Furthermore, the report covers different VAT schemes for VAT-registered companies and concludes with practical examples of inheritance tax and capital gains tax liabilities, providing a comprehensive overview of key business taxation concepts.

UGB 225 Business Taxation

Alternative Assessment 2020/21

Alternative Assessment 2020/21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1..................................................................................................................................3

Linda's trading profits for the year 31st march 2121:...................................................................3

QUESTION 2..................................................................................................................................4

Criteria for the use for employment for self employment, why people prefer self employment:

.....................................................................................................................................................4

Why prefer self-employment rather than being employed, resulting in so many IR 35 cases:...6

QUESTION 3..................................................................................................................................7

Discussion Six badges for trade:..................................................................................................7

Different VAT schemes for the various VAT registered companies:.........................................9

QUESTION 4................................................................................................................................11

Inheritance tax arising when the death:.....................................................................................11

Capital gain tax liability:...........................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

QUESTION 1..................................................................................................................................3

Linda's trading profits for the year 31st march 2121:...................................................................3

QUESTION 2..................................................................................................................................4

Criteria for the use for employment for self employment, why people prefer self employment:

.....................................................................................................................................................4

Why prefer self-employment rather than being employed, resulting in so many IR 35 cases:...6

QUESTION 3..................................................................................................................................7

Discussion Six badges for trade:..................................................................................................7

Different VAT schemes for the various VAT registered companies:.........................................9

QUESTION 4................................................................................................................................11

Inheritance tax arising when the death:.....................................................................................11

Capital gain tax liability:...........................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Business taxation corresponds to taxes which organizations are required to pay as

component of their regular business activities. If there is a single owner, a partner, limited

liability partnership or an organisation, every organization is accountable for compliance

with tax regulations. The study-report covers various aspects of business taxation (Blakeley,

2018). This report covers topics such as trading profits, six trade badges, different VAT schemes

for different VAT registered entities, etc. Besides this, it covers practical sum on inheritance tax

and capital benefit tax obligation.

QUESTION 1

Linda's trading profits for the year 31st march 2121:

In business, trading profit is equal to the overall profits gained of its operations. It does

not require the funding of associated profits, the cost of earnings for the properties. It aims to

have a higher predictor of the potential of firms to conduct key market operations in attempt to

improve their performance. The benefit that the purchaser produces for the acquisition, the

selling of securities. The trade returns are large for a customer who understands the risks

involved in business transactions. These gains are made from buying, selling for items, services.

This statement depicts not allowable trades with firms that display income from trade. Trading

gains are income-generating profits for the company, costs which are not allowed for the

enterprise. These benefits which enable companies to make profits through their operations,

which enable businesses to achieve their targets (d’Andria, Pontikakis and Skonieczna, 2018).

There are different concepts of accounting that allow administrators to make financial

decisions. Accounting department reports transactions that enable company to meet its goals.

The Accounting Team produces a number of financial reports to help them maintain track. These

documents allow them to make financial arrangements, manage finances for commercial

operations to meet goals.

Linda’s trading profit (before deduction of capital allowances) for year ended 31 Mar 2021

Particulars/details £ Amounts

Net profits per accounts 6,96 0

Business taxation corresponds to taxes which organizations are required to pay as

component of their regular business activities. If there is a single owner, a partner, limited

liability partnership or an organisation, every organization is accountable for compliance

with tax regulations. The study-report covers various aspects of business taxation (Blakeley,

2018). This report covers topics such as trading profits, six trade badges, different VAT schemes

for different VAT registered entities, etc. Besides this, it covers practical sum on inheritance tax

and capital benefit tax obligation.

QUESTION 1

Linda's trading profits for the year 31st march 2121:

In business, trading profit is equal to the overall profits gained of its operations. It does

not require the funding of associated profits, the cost of earnings for the properties. It aims to

have a higher predictor of the potential of firms to conduct key market operations in attempt to

improve their performance. The benefit that the purchaser produces for the acquisition, the

selling of securities. The trade returns are large for a customer who understands the risks

involved in business transactions. These gains are made from buying, selling for items, services.

This statement depicts not allowable trades with firms that display income from trade. Trading

gains are income-generating profits for the company, costs which are not allowed for the

enterprise. These benefits which enable companies to make profits through their operations,

which enable businesses to achieve their targets (d’Andria, Pontikakis and Skonieczna, 2018).

There are different concepts of accounting that allow administrators to make financial

decisions. Accounting department reports transactions that enable company to meet its goals.

The Accounting Team produces a number of financial reports to help them maintain track. These

documents allow them to make financial arrangements, manage finances for commercial

operations to meet goals.

Linda’s trading profit (before deduction of capital allowances) for year ended 31 Mar 2021

Particulars/details £ Amounts

Net profits per accounts 6,96 0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

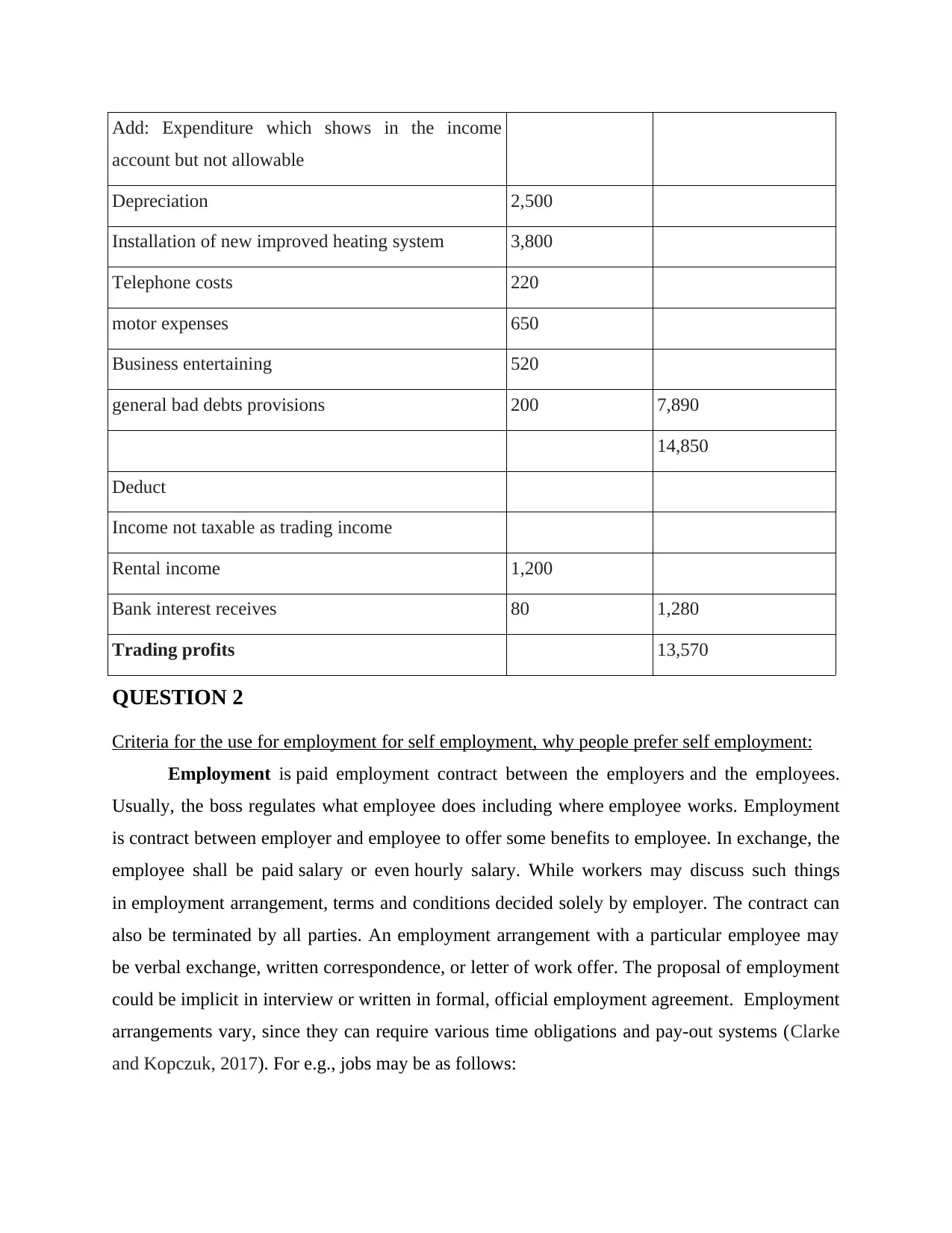

Add: Expenditure which shows in the income

account but not allowable

Depreciation 2,500

Installation of new improved heating system 3,800

Telephone costs 220

motor expenses 650

Business entertaining 520

general bad debts provisions 200 7,890

14,850

Deduct

Income not taxable as trading income

Rental income 1,200

Bank interest receives 80 1,280

Trading profits 13,570

QUESTION 2

Criteria for the use for employment for self employment, why people prefer self employment:

Employment is paid employment contract between the employers and the employees.

Usually, the boss regulates what employee does including where employee works. Employment

is contract between employer and employee to offer some benefits to employee. In exchange, the

employee shall be paid salary or even hourly salary. While workers may discuss such things

in employment arrangement, terms and conditions decided solely by employer. The contract can

also be terminated by all parties. An employment arrangement with a particular employee may

be verbal exchange, written correspondence, or letter of work offer. The proposal of employment

could be implicit in interview or written in formal, official employment agreement. Employment

arrangements vary, since they can require various time obligations and pay-out systems (Clarke

and Kopczuk, 2017). For e.g., jobs may be as follows:

account but not allowable

Depreciation 2,500

Installation of new improved heating system 3,800

Telephone costs 220

motor expenses 650

Business entertaining 520

general bad debts provisions 200 7,890

14,850

Deduct

Income not taxable as trading income

Rental income 1,200

Bank interest receives 80 1,280

Trading profits 13,570

QUESTION 2

Criteria for the use for employment for self employment, why people prefer self employment:

Employment is paid employment contract between the employers and the employees.

Usually, the boss regulates what employee does including where employee works. Employment

is contract between employer and employee to offer some benefits to employee. In exchange, the

employee shall be paid salary or even hourly salary. While workers may discuss such things

in employment arrangement, terms and conditions decided solely by employer. The contract can

also be terminated by all parties. An employment arrangement with a particular employee may

be verbal exchange, written correspondence, or letter of work offer. The proposal of employment

could be implicit in interview or written in formal, official employment agreement. Employment

arrangements vary, since they can require various time obligations and pay-out systems (Clarke

and Kopczuk, 2017). For e.g., jobs may be as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hourly part-time jobs that are charged a fixed sum figure for every hour working. Full-time jobs

wherein the employee earns a wage and rewards from employer for the completion of the duties

needed by a specific role

A fixed schedule forcing workers to serve 40-hour week with hour for lunch including two 15-

minute rests, one in morning and one in afternoon, as mandated by state statute.

So as long as company retains its arrangement to pay off employee—and pay on time-limited

basis—and the employee wants to keep working with employer, employment generally

continues. Most of the working relationship among employer and employee is controlled

by employer's requirements, viability and theory of management. The work relationship is often

influenced by availability and desires of employees (Blakeley, 2018).

The meaning of self-employment is 'beginning and operating a profitable firm or social

organization Many successful corporations started this way when innovative males and females

invented an invention, set up a business or registered a trademark. While an outstanding business

concept plays a vital role in overall success/results of business, the execution of idea will

inevitably determine its destiny. Self-employment is often the only choice if choose to follow a

particular career choice. Journalism, some legal or medical occupations and the artistic and

creative artists are all fields of which self-employment or self-employed practise is a common

style of activity. Self-employed people are citizen who make livelihood by functioning for

himself or herself, not as employee of anyone else as well as not with the owners (shareholders)

of a company. However, there are different interpretations of 'self-employed' which vary slightly.

Self-employment is act of producing one's revenue directly from customer rather than becoming

a company job. Usually, tax officials will deem an individual for being self-employed when the

person wishes to be known as such or earns revenue in such manner that person is expected to

submit tax return in compliance with the law in effect in the applicable jurisdiction. In real

world, the main problem for taxation officials is not that of an individual selling, but that

of person making profit. In other terms, the practise of trade is expected to be overlooked where

there is zero profit. Consequently, sporadic and hobby-or enthusiast-based commercial activity is

usually neglected by the authorities. Self-employed individuals usually pursue jobs on their

choice instead of being hired by employer, gaining money from trade or a sector in which they

reside. In certain countries, policymakers put more focus on specifying whether a person is self-

employed either involved in disguised jobs, often defined as a pretence of intra-business

wherein the employee earns a wage and rewards from employer for the completion of the duties

needed by a specific role

A fixed schedule forcing workers to serve 40-hour week with hour for lunch including two 15-

minute rests, one in morning and one in afternoon, as mandated by state statute.

So as long as company retains its arrangement to pay off employee—and pay on time-limited

basis—and the employee wants to keep working with employer, employment generally

continues. Most of the working relationship among employer and employee is controlled

by employer's requirements, viability and theory of management. The work relationship is often

influenced by availability and desires of employees (Blakeley, 2018).

The meaning of self-employment is 'beginning and operating a profitable firm or social

organization Many successful corporations started this way when innovative males and females

invented an invention, set up a business or registered a trademark. While an outstanding business

concept plays a vital role in overall success/results of business, the execution of idea will

inevitably determine its destiny. Self-employment is often the only choice if choose to follow a

particular career choice. Journalism, some legal or medical occupations and the artistic and

creative artists are all fields of which self-employment or self-employed practise is a common

style of activity. Self-employed people are citizen who make livelihood by functioning for

himself or herself, not as employee of anyone else as well as not with the owners (shareholders)

of a company. However, there are different interpretations of 'self-employed' which vary slightly.

Self-employment is act of producing one's revenue directly from customer rather than becoming

a company job. Usually, tax officials will deem an individual for being self-employed when the

person wishes to be known as such or earns revenue in such manner that person is expected to

submit tax return in compliance with the law in effect in the applicable jurisdiction. In real

world, the main problem for taxation officials is not that of an individual selling, but that

of person making profit. In other terms, the practise of trade is expected to be overlooked where

there is zero profit. Consequently, sporadic and hobby-or enthusiast-based commercial activity is

usually neglected by the authorities. Self-employed individuals usually pursue jobs on their

choice instead of being hired by employer, gaining money from trade or a sector in which they

reside. In certain countries, policymakers put more focus on specifying whether a person is self-

employed either involved in disguised jobs, often defined as a pretence of intra-business

contractual arrangement to mask what is otherwise straightforward employer-employee

arrangement. There are, even then, certain personnel whose position is really not that clear. For

eg, one may operate from home as well as and using own computer, but report to an agency in

which someone monitors and manages their work. In both situations, a decision must be taken as

to if they are employee or self-employed individual (Carton, Corugedo and Hunt, 2017). This is

not sufficient for the individual paying to decide their classification; sometimes, payers are

biased, since they do not wish to share financial expenses and obligations of getting employee

(explained below). Even so, if one in doubt regarding your ranking, it is useful to reply the

following queries:

Whether individual have power of how work is performed, that is do they work

independently without someone observing the work?

Will they have upwards of one customer?

Are individuals permitted to take clients with you anytime they choose?

Could they delegate their work?

Would they fail to do task?

Will they have their own resources and equipment Example, When anything fails, do you

have their private computer, are they liable for charging for programme subscriptions, are

they responsible for fixing or upgrading their working tools?

Are you selling yourself?

Would they hire somebody else to perform work without somebody else's permission?

Do they bear the burden and accountability for work done — for example if this is not

accomplished well, will they still be charged?

Is there formal contract specifying the standards and requirements of work?

Will they have their client invoiced?

Have you been recruited to do a particular job?

Why prefer self-employment rather than being employed, resulting in so many IR 35 cases:

Control across all areas of business: The best benefit of self-employment is management

control of every part of the business. Individuals decide what to do with their

business. individual can pick targeted audience. They chose the marketing features that

make their business distinctive. Being self-employed sometimes ensures that one can set their

own targets, business mission and values. They are responsible for quality of the products or

arrangement. There are, even then, certain personnel whose position is really not that clear. For

eg, one may operate from home as well as and using own computer, but report to an agency in

which someone monitors and manages their work. In both situations, a decision must be taken as

to if they are employee or self-employed individual (Carton, Corugedo and Hunt, 2017). This is

not sufficient for the individual paying to decide their classification; sometimes, payers are

biased, since they do not wish to share financial expenses and obligations of getting employee

(explained below). Even so, if one in doubt regarding your ranking, it is useful to reply the

following queries:

Whether individual have power of how work is performed, that is do they work

independently without someone observing the work?

Will they have upwards of one customer?

Are individuals permitted to take clients with you anytime they choose?

Could they delegate their work?

Would they fail to do task?

Will they have their own resources and equipment Example, When anything fails, do you

have their private computer, are they liable for charging for programme subscriptions, are

they responsible for fixing or upgrading their working tools?

Are you selling yourself?

Would they hire somebody else to perform work without somebody else's permission?

Do they bear the burden and accountability for work done — for example if this is not

accomplished well, will they still be charged?

Is there formal contract specifying the standards and requirements of work?

Will they have their client invoiced?

Have you been recruited to do a particular job?

Why prefer self-employment rather than being employed, resulting in so many IR 35 cases:

Control across all areas of business: The best benefit of self-employment is management

control of every part of the business. Individuals decide what to do with their

business. individual can pick targeted audience. They chose the marketing features that

make their business distinctive. Being self-employed sometimes ensures that one can set their

own targets, business mission and values. They are responsible for quality of the products or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

services you sell. They chose all the employers they recruit, but instead of being stuck with co-

workers can't bear, they get to select the ones deal with each day.

Tax Benefits: Individuals may deduct certain costs related to running the company. Online,

mobile and fax charges are covered If individual use same mobile and internet within business as

they do for their personal usage, will only be entitled to subtract a part of bill. Travel and

corporate use of the vehicle are eligible for tax cuts. They will also exclude food and

entertainment expenses as they are relevant to work. When individual go back to education and

otherwise broaden their business-related skills, one will be eligible to deduct these expenditures

(Beckers, 2018).

Potential for Growth: Self-employment offers everyone practical experience throughout all facets

of operating business Working for oneself needs one to be efficient and can entail doing lots of

researches on various facets of their business. This covers such aspects as buying products,

handling employees, marketing and accounting. These skills stick with them as they expand that

business launch new business, and even plan to head back to working with somebody else.

Customer Interactions: When individuals are self-employed, individuals always do all the

working, particularly at the beginning. This ensures that you can develop good partnerships with

their clients They deal directly with any individual who utilizes their services or purchases their

goods. They get rare chance to continue to understand the clients, which offers them insights in

with what they desire. This connection will also help create customer loyalty and help hold them

returning to their business in future

QUESTION 3

Discussion Six badges for trade:

In year 1955, report of Royal Commission on Taxation of Profit sums as well as Income

evaluated case law and established 6 trade badges. It was starting point and, as one might

understand, several changes have taken place in the field complemented by case-law. Here are

key six trade badges, as discussed below:

1. Profit Seeking Motive: it is obvious that having desire to make profit may imply a

trading operation, but that's not sufficient on its own. In the scenario of the Salt v

Chamberlain – Ch D 1979, 53 TC 143; [1979] STC 750, research consultant suffered

damages on stock exchange after attempting to foresee market. The loss happened after

workers can't bear, they get to select the ones deal with each day.

Tax Benefits: Individuals may deduct certain costs related to running the company. Online,

mobile and fax charges are covered If individual use same mobile and internet within business as

they do for their personal usage, will only be entitled to subtract a part of bill. Travel and

corporate use of the vehicle are eligible for tax cuts. They will also exclude food and

entertainment expenses as they are relevant to work. When individual go back to education and

otherwise broaden their business-related skills, one will be eligible to deduct these expenditures

(Beckers, 2018).

Potential for Growth: Self-employment offers everyone practical experience throughout all facets

of operating business Working for oneself needs one to be efficient and can entail doing lots of

researches on various facets of their business. This covers such aspects as buying products,

handling employees, marketing and accounting. These skills stick with them as they expand that

business launch new business, and even plan to head back to working with somebody else.

Customer Interactions: When individuals are self-employed, individuals always do all the

working, particularly at the beginning. This ensures that you can develop good partnerships with

their clients They deal directly with any individual who utilizes their services or purchases their

goods. They get rare chance to continue to understand the clients, which offers them insights in

with what they desire. This connection will also help create customer loyalty and help hold them

returning to their business in future

QUESTION 3

Discussion Six badges for trade:

In year 1955, report of Royal Commission on Taxation of Profit sums as well as Income

evaluated case law and established 6 trade badges. It was starting point and, as one might

understand, several changes have taken place in the field complemented by case-law. Here are

key six trade badges, as discussed below:

1. Profit Seeking Motive: it is obvious that having desire to make profit may imply a

trading operation, but that's not sufficient on its own. In the scenario of the Salt v

Chamberlain – Ch D 1979, 53 TC 143; [1979] STC 750, research consultant suffered

damages on stock exchange after attempting to foresee market. The loss happened after

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

several cycles more than 200 transactions. It isn't seen as question of commerce and

money in existence. This was established that the selling of shares by private person

should never have exchange badges attached to them. Both sales are subjected to capital-

gains taxes.

2. Number of transactions: A sole transaction may be a commercial operation, which is

more representative if they are frequent and regular transactions. It was specifically seen

in the Pickford v Quirke – CA 1927, 13 TC 251. The union acquired a cotton-spinning

factory with the intention of utilizing it in exchange, but on the acquisition of mill it was

in poorer condition than was originally expected. The union then voted to strip mill of its

riches and selling it piecemeal, producing a profit. It's been replicated a lot of times

for number of mills. Owing to the recurring existence of the sales, it was stated

that profits were trade profits and taxed even so (Kaledin, Barkhatov, Kapkaev and

Shestakova, 2018).

3. Changes to the asset: It is necessary to acknowledge any improvements or adjustments

introduced to asset that can make it much more valuable. In case of Cape Brandy

Syndicate v CIR – CA 1921, 12 TC 358; [1921] members of wine syndicate entered a

new trade union to buy brandy in the South Africa. Some were sent to East, the rest have

been sent to the London to be mixed with French brandy, re-engineered and sold for

profit. The taxpayer sought to contend that the deal was of financial disposition as a result

of the selling of investment. This was held that trade or a company had been carried out

and could be calculated as trading benefit.

4. Way sale was carried out: In its advice, HMRC notes that this is always pointer if deal

follows those of 'undisputed trades.' Scenario CIR v Livingston and Others included three

unconnected people who, together, had acquired cargo vessel. That vessel was turned

into steam drifter then sold at profit. The acquisition was first vessel acquired by the three

persons. An evaluation was made of the benefit, which was identified as trading profit. In

the ruling, the judge mentioned that the measure to be followed to assess whether or

not undertaking as are now examining is of "trade" type is whether transactions

concerned are of same type and carry out in same manner as that are typical of ordinary

dealing in line of business wherein the endeavour was carried out.

money in existence. This was established that the selling of shares by private person

should never have exchange badges attached to them. Both sales are subjected to capital-

gains taxes.

2. Number of transactions: A sole transaction may be a commercial operation, which is

more representative if they are frequent and regular transactions. It was specifically seen

in the Pickford v Quirke – CA 1927, 13 TC 251. The union acquired a cotton-spinning

factory with the intention of utilizing it in exchange, but on the acquisition of mill it was

in poorer condition than was originally expected. The union then voted to strip mill of its

riches and selling it piecemeal, producing a profit. It's been replicated a lot of times

for number of mills. Owing to the recurring existence of the sales, it was stated

that profits were trade profits and taxed even so (Kaledin, Barkhatov, Kapkaev and

Shestakova, 2018).

3. Changes to the asset: It is necessary to acknowledge any improvements or adjustments

introduced to asset that can make it much more valuable. In case of Cape Brandy

Syndicate v CIR – CA 1921, 12 TC 358; [1921] members of wine syndicate entered a

new trade union to buy brandy in the South Africa. Some were sent to East, the rest have

been sent to the London to be mixed with French brandy, re-engineered and sold for

profit. The taxpayer sought to contend that the deal was of financial disposition as a result

of the selling of investment. This was held that trade or a company had been carried out

and could be calculated as trading benefit.

4. Way sale was carried out: In its advice, HMRC notes that this is always pointer if deal

follows those of 'undisputed trades.' Scenario CIR v Livingston and Others included three

unconnected people who, together, had acquired cargo vessel. That vessel was turned

into steam drifter then sold at profit. The acquisition was first vessel acquired by the three

persons. An evaluation was made of the benefit, which was identified as trading profit. In

the ruling, the judge mentioned that the measure to be followed to assess whether or

not undertaking as are now examining is of "trade" type is whether transactions

concerned are of same type and carry out in same manner as that are typical of ordinary

dealing in line of business wherein the endeavour was carried out.

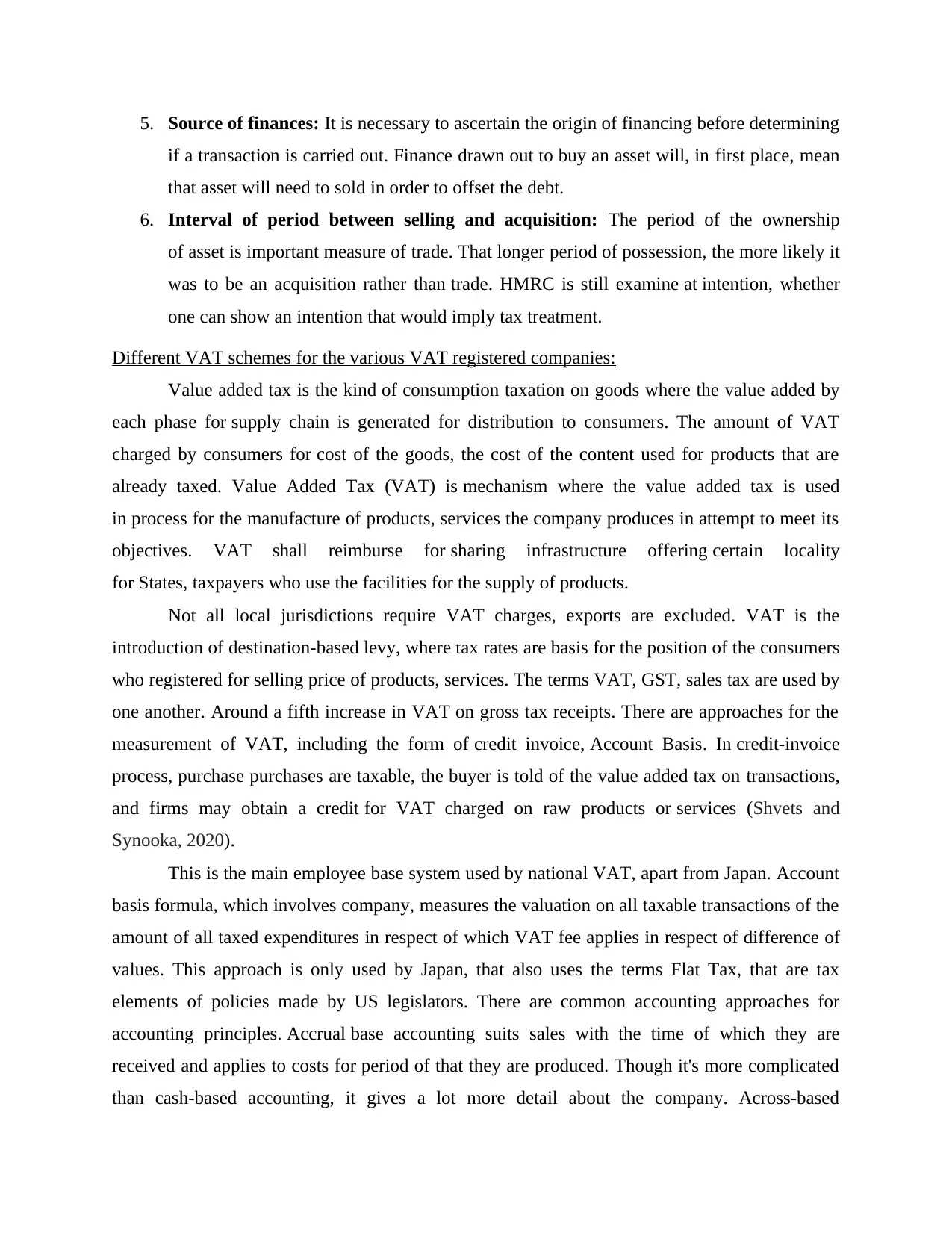

5. Source of finances: It is necessary to ascertain the origin of financing before determining

if a transaction is carried out. Finance drawn out to buy an asset will, in first place, mean

that asset will need to sold in order to offset the debt.

6. Interval of period between selling and acquisition: The period of the ownership

of asset is important measure of trade. That longer period of possession, the more likely it

was to be an acquisition rather than trade. HMRC is still examine at intention, whether

one can show an intention that would imply tax treatment.

Different VAT schemes for the various VAT registered companies:

Value added tax is the kind of consumption taxation on goods where the value added by

each phase for supply chain is generated for distribution to consumers. The amount of VAT

charged by consumers for cost of the goods, the cost of the content used for products that are

already taxed. Value Added Tax (VAT) is mechanism where the value added tax is used

in process for the manufacture of products, services the company produces in attempt to meet its

objectives. VAT shall reimburse for sharing infrastructure offering certain locality

for States, taxpayers who use the facilities for the supply of products.

Not all local jurisdictions require VAT charges, exports are excluded. VAT is the

introduction of destination-based levy, where tax rates are basis for the position of the consumers

who registered for selling price of products, services. The terms VAT, GST, sales tax are used by

one another. Around a fifth increase in VAT on gross tax receipts. There are approaches for the

measurement of VAT, including the form of credit invoice, Account Basis. In credit-invoice

process, purchase purchases are taxable, the buyer is told of the value added tax on transactions,

and firms may obtain a credit for VAT charged on raw products or services (Shvets and

Synooka, 2020).

This is the main employee base system used by national VAT, apart from Japan. Account

basis formula, which involves company, measures the valuation on all taxable transactions of the

amount of all taxed expenditures in respect of which VAT fee applies in respect of difference of

values. This approach is only used by Japan, that also uses the terms Flat Tax, that are tax

elements of policies made by US legislators. There are common accounting approaches for

accounting principles. Accrual base accounting suits sales with the time of which they are

received and applies to costs for period of that they are produced. Though it's more complicated

than cash-based accounting, it gives a lot more detail about the company. Across-based

if a transaction is carried out. Finance drawn out to buy an asset will, in first place, mean

that asset will need to sold in order to offset the debt.

6. Interval of period between selling and acquisition: The period of the ownership

of asset is important measure of trade. That longer period of possession, the more likely it

was to be an acquisition rather than trade. HMRC is still examine at intention, whether

one can show an intention that would imply tax treatment.

Different VAT schemes for the various VAT registered companies:

Value added tax is the kind of consumption taxation on goods where the value added by

each phase for supply chain is generated for distribution to consumers. The amount of VAT

charged by consumers for cost of the goods, the cost of the content used for products that are

already taxed. Value Added Tax (VAT) is mechanism where the value added tax is used

in process for the manufacture of products, services the company produces in attempt to meet its

objectives. VAT shall reimburse for sharing infrastructure offering certain locality

for States, taxpayers who use the facilities for the supply of products.

Not all local jurisdictions require VAT charges, exports are excluded. VAT is the

introduction of destination-based levy, where tax rates are basis for the position of the consumers

who registered for selling price of products, services. The terms VAT, GST, sales tax are used by

one another. Around a fifth increase in VAT on gross tax receipts. There are approaches for the

measurement of VAT, including the form of credit invoice, Account Basis. In credit-invoice

process, purchase purchases are taxable, the buyer is told of the value added tax on transactions,

and firms may obtain a credit for VAT charged on raw products or services (Shvets and

Synooka, 2020).

This is the main employee base system used by national VAT, apart from Japan. Account

basis formula, which involves company, measures the valuation on all taxable transactions of the

amount of all taxed expenditures in respect of which VAT fee applies in respect of difference of

values. This approach is only used by Japan, that also uses the terms Flat Tax, that are tax

elements of policies made by US legislators. There are common accounting approaches for

accounting principles. Accrual base accounting suits sales with the time of which they are

received and applies to costs for period of that they are produced. Though it's more complicated

than cash-based accounting, it gives a lot more detail about the company. Across-based

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

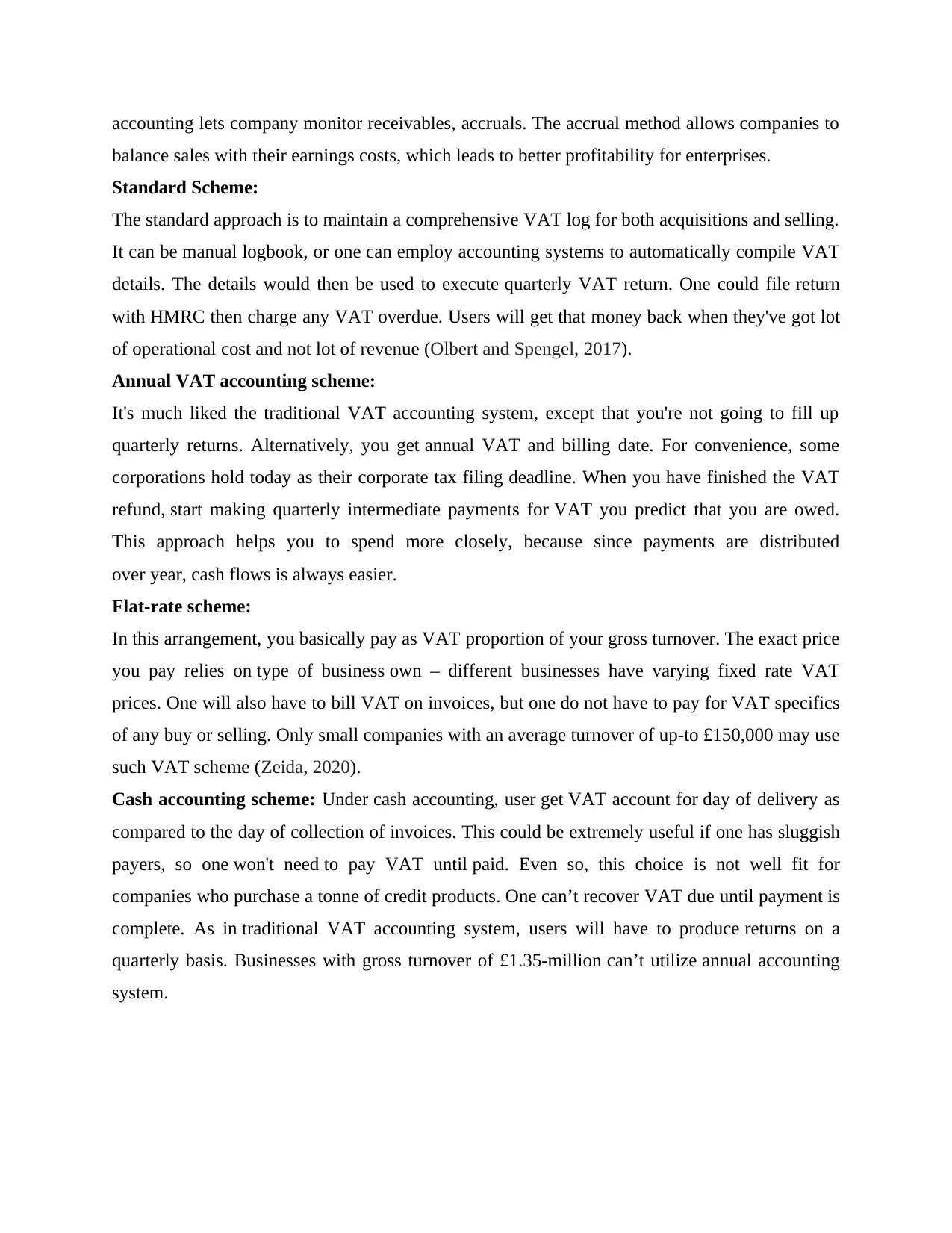

accounting lets company monitor receivables, accruals. The accrual method allows companies to

balance sales with their earnings costs, which leads to better profitability for enterprises.

Standard Scheme:

The standard approach is to maintain a comprehensive VAT log for both acquisitions and selling.

It can be manual logbook, or one can employ accounting systems to automatically compile VAT

details. The details would then be used to execute quarterly VAT return. One could file return

with HMRC then charge any VAT overdue. Users will get that money back when they've got lot

of operational cost and not lot of revenue (Olbert and Spengel, 2017).

Annual VAT accounting scheme:

It's much liked the traditional VAT accounting system, except that you're not going to fill up

quarterly returns. Alternatively, you get annual VAT and billing date. For convenience, some

corporations hold today as their corporate tax filing deadline. When you have finished the VAT

refund, start making quarterly intermediate payments for VAT you predict that you are owed.

This approach helps you to spend more closely, because since payments are distributed

over year, cash flows is always easier.

Flat-rate scheme:

In this arrangement, you basically pay as VAT proportion of your gross turnover. The exact price

you pay relies on type of business own – different businesses have varying fixed rate VAT

prices. One will also have to bill VAT on invoices, but one do not have to pay for VAT specifics

of any buy or selling. Only small companies with an average turnover of up-to £150,000 may use

such VAT scheme (Zeida, 2020).

Cash accounting scheme: Under cash accounting, user get VAT account for day of delivery as

compared to the day of collection of invoices. This could be extremely useful if one has sluggish

payers, so one won't need to pay VAT until paid. Even so, this choice is not well fit for

companies who purchase a tonne of credit products. One can’t recover VAT due until payment is

complete. As in traditional VAT accounting system, users will have to produce returns on a

quarterly basis. Businesses with gross turnover of £1.35-million can’t utilize annual accounting

system.

balance sales with their earnings costs, which leads to better profitability for enterprises.

Standard Scheme:

The standard approach is to maintain a comprehensive VAT log for both acquisitions and selling.

It can be manual logbook, or one can employ accounting systems to automatically compile VAT

details. The details would then be used to execute quarterly VAT return. One could file return

with HMRC then charge any VAT overdue. Users will get that money back when they've got lot

of operational cost and not lot of revenue (Olbert and Spengel, 2017).

Annual VAT accounting scheme:

It's much liked the traditional VAT accounting system, except that you're not going to fill up

quarterly returns. Alternatively, you get annual VAT and billing date. For convenience, some

corporations hold today as their corporate tax filing deadline. When you have finished the VAT

refund, start making quarterly intermediate payments for VAT you predict that you are owed.

This approach helps you to spend more closely, because since payments are distributed

over year, cash flows is always easier.

Flat-rate scheme:

In this arrangement, you basically pay as VAT proportion of your gross turnover. The exact price

you pay relies on type of business own – different businesses have varying fixed rate VAT

prices. One will also have to bill VAT on invoices, but one do not have to pay for VAT specifics

of any buy or selling. Only small companies with an average turnover of up-to £150,000 may use

such VAT scheme (Zeida, 2020).

Cash accounting scheme: Under cash accounting, user get VAT account for day of delivery as

compared to the day of collection of invoices. This could be extremely useful if one has sluggish

payers, so one won't need to pay VAT until paid. Even so, this choice is not well fit for

companies who purchase a tonne of credit products. One can’t recover VAT due until payment is

complete. As in traditional VAT accounting system, users will have to produce returns on a

quarterly basis. Businesses with gross turnover of £1.35-million can’t utilize annual accounting

system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

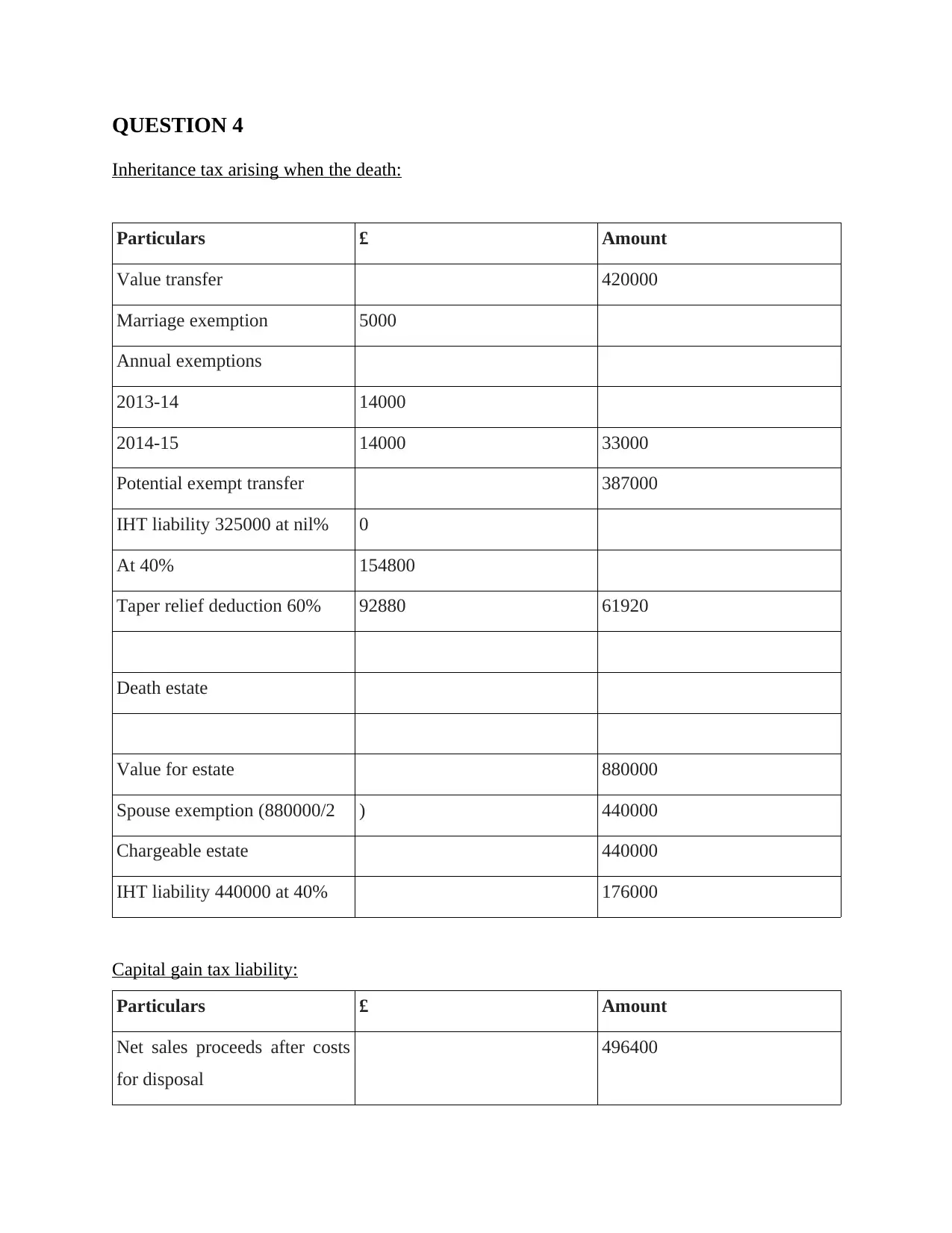

QUESTION 4

Inheritance tax arising when the death:

Particulars £ Amount

Value transfer 420000

Marriage exemption 5000

Annual exemptions

2013-14 14000

2014-15 14000 33000

Potential exempt transfer 387000

IHT liability 325000 at nil% 0

At 40% 154800

Taper relief deduction 60% 92880 61920

Death estate

Value for estate 880000

Spouse exemption (880000/2 ) 440000

Chargeable estate 440000

IHT liability 440000 at 40% 176000

Capital gain tax liability:

Particulars £ Amount

Net sales proceeds after costs

for disposal

496400

Inheritance tax arising when the death:

Particulars £ Amount

Value transfer 420000

Marriage exemption 5000

Annual exemptions

2013-14 14000

2014-15 14000 33000

Potential exempt transfer 387000

IHT liability 325000 at nil% 0

At 40% 154800

Taper relief deduction 60% 92880 61920

Death estate

Value for estate 880000

Spouse exemption (880000/2 ) 440000

Chargeable estate 440000

IHT liability 440000 at 40% 176000

Capital gain tax liability:

Particulars £ Amount

Net sales proceeds after costs

for disposal

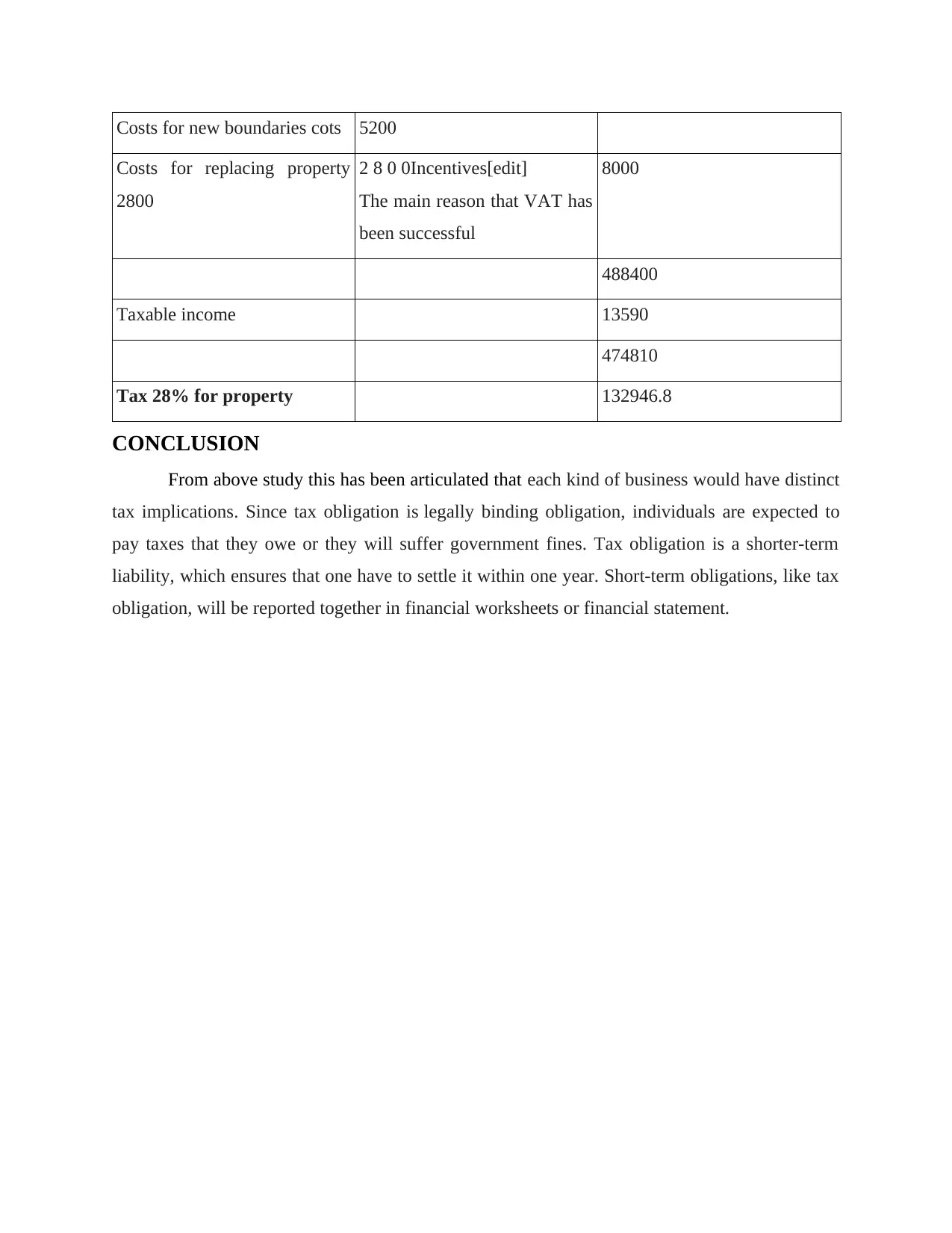

496400

Costs for new boundaries cots 5200

Costs for replacing property

2800

2 8 0 0Incentives[edit]

The main reason that VAT has

been successful

8000

488400

Taxable income 13590

474810

Tax 28% for property 132946.8

CONCLUSION

From above study this has been articulated that each kind of business would have distinct

tax implications. Since tax obligation is legally binding obligation, individuals are expected to

pay taxes that they owe or they will suffer government fines. Tax obligation is a shorter-term

liability, which ensures that one have to settle it within one year. Short-term obligations, like tax

obligation, will be reported together in financial worksheets or financial statement.

Costs for replacing property

2800

2 8 0 0Incentives[edit]

The main reason that VAT has

been successful

8000

488400

Taxable income 13590

474810

Tax 28% for property 132946.8

CONCLUSION

From above study this has been articulated that each kind of business would have distinct

tax implications. Since tax obligation is legally binding obligation, individuals are expected to

pay taxes that they owe or they will suffer government fines. Tax obligation is a shorter-term

liability, which ensures that one have to settle it within one year. Short-term obligations, like tax

obligation, will be reported together in financial worksheets or financial statement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.