UGB105 Financial Accounting: Financial Statement Analysis and Prep

VerifiedAdded on 2022/11/29

|19

|3306

|171

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial accounting assignment, focusing on the preparation and analysis of financial statements for Bob Peterson's fabric shop. It includes the preparation of a trading account, profit and loss account, and balance sheet as of April 30, 2020. The solution also analyzes six key features of financial statement information, such as reliability, comparability, and timeliness, highlighting their benefits and importance to various stakeholders. Furthermore, the assignment involves calculating and interpreting financial ratios for Danaye Ltd, including gross profit margin, return on capital employed, current ratio, trade receivable days, and trade payable days. Finally, the document provides bank account statements, loan accounts, rent accounts, and advertisement accounts, culminating in a trial balance as of April 30, 2020, and a comparison of straight-line and reducing balance depreciation methods.

UGB105- INTRODUCTION

TO FINANCIAL

ACCOUNTING

TO FINANCIAL

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1..............................................................................................................................................3

1a)...............................................................................................................................................................3

a) Trading account for the year ended 30th April 2020........................................................................3

b) Profit and Loss Account (P&L A/c) for the year ended 30th April 2020.........................................3

c) Statement of financial position as at the 30th April 2020..................................................................4

1b)...............................................................................................................................................................5

Analyzing six features of information presented by financial statement for users as well benefits &

importance...............................................................................................................................................5

QUESTION 2..............................................................................................................................................8

2a)...............................................................................................................................................................8

Calculating ratios for Danaye Ltd............................................................................................................8

2b).............................................................................................................................................................10

a) Bank Account for two months.......................................................................................................10

b) Other accounts are as follows:.......................................................................................................11

c) Trial Balance as at the 30th April 2020..........................................................................................14

2c).............................................................................................................................................................15

i. Straight Line Methods...................................................................................................................15

ii. Reducing Balance method.............................................................................................................16

iii. Explaining the following concepts............................................................................................17

QUESTION 1..............................................................................................................................................3

1a)...............................................................................................................................................................3

a) Trading account for the year ended 30th April 2020........................................................................3

b) Profit and Loss Account (P&L A/c) for the year ended 30th April 2020.........................................3

c) Statement of financial position as at the 30th April 2020..................................................................4

1b)...............................................................................................................................................................5

Analyzing six features of information presented by financial statement for users as well benefits &

importance...............................................................................................................................................5

QUESTION 2..............................................................................................................................................8

2a)...............................................................................................................................................................8

Calculating ratios for Danaye Ltd............................................................................................................8

2b).............................................................................................................................................................10

a) Bank Account for two months.......................................................................................................10

b) Other accounts are as follows:.......................................................................................................11

c) Trial Balance as at the 30th April 2020..........................................................................................14

2c).............................................................................................................................................................15

i. Straight Line Methods...................................................................................................................15

ii. Reducing Balance method.............................................................................................................16

iii. Explaining the following concepts............................................................................................17

QUESTION 1

1a)

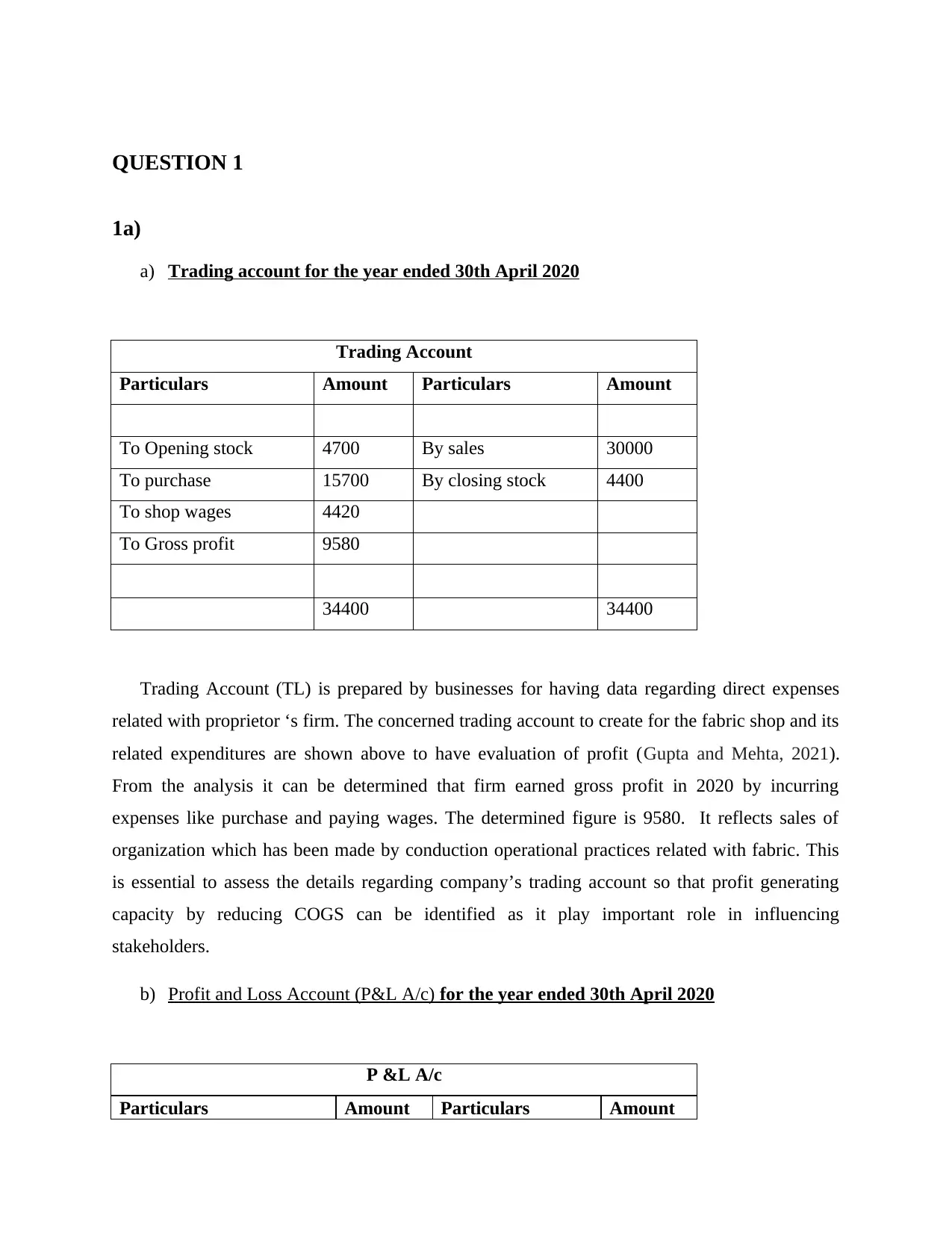

a) Trading account for the year ended 30th April 2020

Trading Account

Particulars Amount Particulars Amount

To Opening stock 4700 By sales 30000

To purchase 15700 By closing stock 4400

To shop wages 4420

To Gross profit 9580

34400 34400

Trading Account (TL) is prepared by businesses for having data regarding direct expenses

related with proprietor ‘s firm. The concerned trading account to create for the fabric shop and its

related expenditures are shown above to have evaluation of profit (Gupta and Mehta, 2021).

From the analysis it can be determined that firm earned gross profit in 2020 by incurring

expenses like purchase and paying wages. The determined figure is 9580. It reflects sales of

organization which has been made by conduction operational practices related with fabric. This

is essential to assess the details regarding company’s trading account so that profit generating

capacity by reducing COGS can be identified as it play important role in influencing

stakeholders.

b) Profit and Loss Account (P&L A/c) for the year ended 30th April 2020

P &L A/c

Particulars Amount Particulars Amount

1a)

a) Trading account for the year ended 30th April 2020

Trading Account

Particulars Amount Particulars Amount

To Opening stock 4700 By sales 30000

To purchase 15700 By closing stock 4400

To shop wages 4420

To Gross profit 9580

34400 34400

Trading Account (TL) is prepared by businesses for having data regarding direct expenses

related with proprietor ‘s firm. The concerned trading account to create for the fabric shop and its

related expenditures are shown above to have evaluation of profit (Gupta and Mehta, 2021).

From the analysis it can be determined that firm earned gross profit in 2020 by incurring

expenses like purchase and paying wages. The determined figure is 9580. It reflects sales of

organization which has been made by conduction operational practices related with fabric. This

is essential to assess the details regarding company’s trading account so that profit generating

capacity by reducing COGS can be identified as it play important role in influencing

stakeholders.

b) Profit and Loss Account (P&L A/c) for the year ended 30th April 2020

P &L A/c

Particulars Amount Particulars Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To lighting and heat 260 By Gross profit 9580

To rent 4500

To insurance 120

To net profit 4700

9580 9580

Profit and Loss account contributes in gaining knowledge of factors which highly

influences organization’s efforts for attaining desirable profits. In addition to this, fabric shop’s

indirect expenditures and earnings are shown in above illustrated tabular format. It is considered

to be important to have such type of income statement for giving stakeholders deep insights of

operational practices by segregating indirect overheads such as operational expenses, etc. By

analyzing the above mentioned net profit margin which is 4700 for the financial year of 2020. It

can be used to give positive impact on stakeholders so that better sustainability and profitability

can be derived.

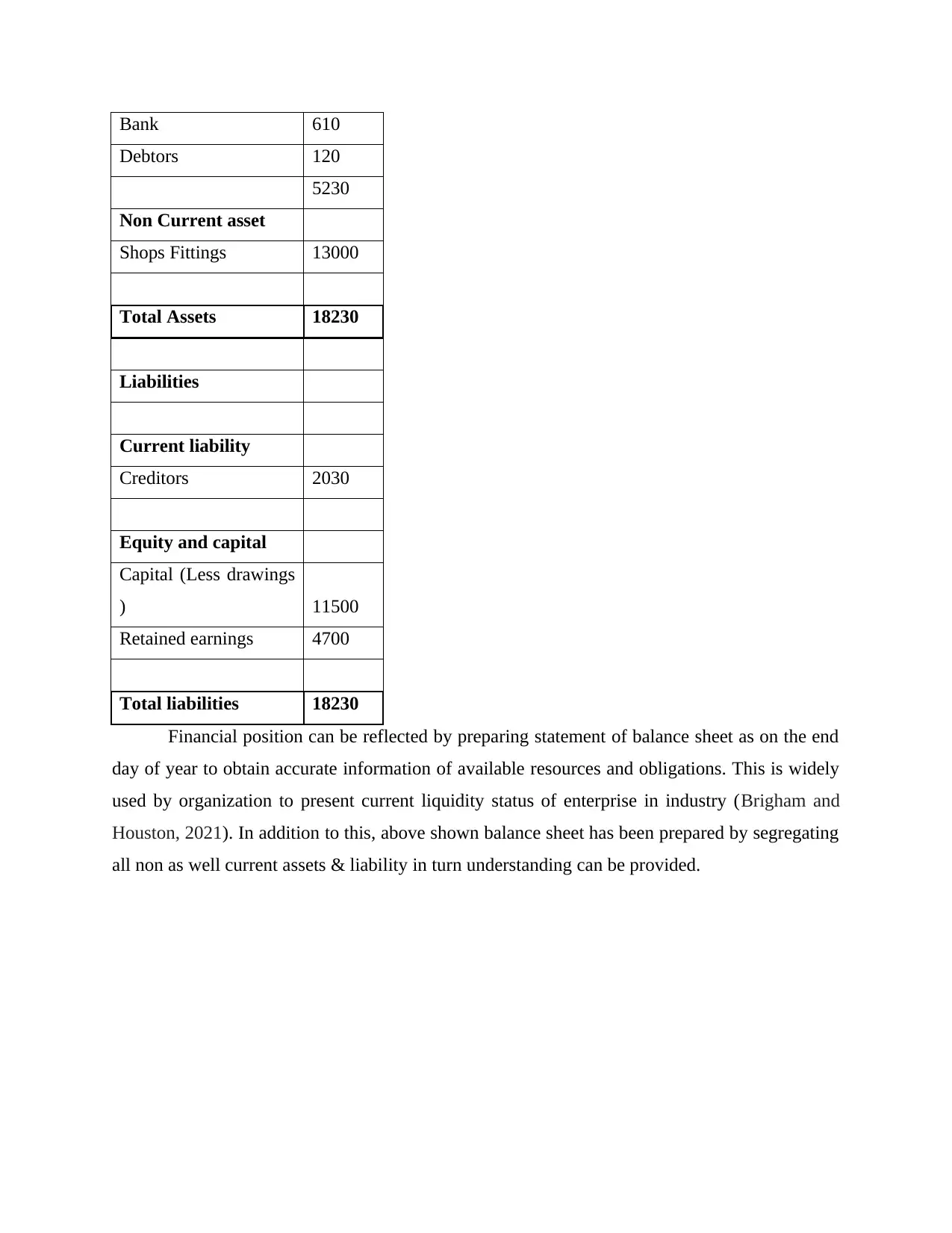

c) Statement of financial position as at the 30th April 2020

Balance sheet as at 30 April

2020

Particulars

Amoun

t

Current assets

closing stock 4400

Cash 100

To rent 4500

To insurance 120

To net profit 4700

9580 9580

Profit and Loss account contributes in gaining knowledge of factors which highly

influences organization’s efforts for attaining desirable profits. In addition to this, fabric shop’s

indirect expenditures and earnings are shown in above illustrated tabular format. It is considered

to be important to have such type of income statement for giving stakeholders deep insights of

operational practices by segregating indirect overheads such as operational expenses, etc. By

analyzing the above mentioned net profit margin which is 4700 for the financial year of 2020. It

can be used to give positive impact on stakeholders so that better sustainability and profitability

can be derived.

c) Statement of financial position as at the 30th April 2020

Balance sheet as at 30 April

2020

Particulars

Amoun

t

Current assets

closing stock 4400

Cash 100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bank 610

Debtors 120

5230

Non Current asset

Shops Fittings 13000

Total Assets 18230

Liabilities

Current liability

Creditors 2030

Equity and capital

Capital (Less drawings

) 11500

Retained earnings 4700

Total liabilities 18230

Financial position can be reflected by preparing statement of balance sheet as on the end

day of year to obtain accurate information of available resources and obligations. This is widely

used by organization to present current liquidity status of enterprise in industry (Brigham and

Houston, 2021). In addition to this, above shown balance sheet has been prepared by segregating

all non as well current assets & liability in turn understanding can be provided.

Debtors 120

5230

Non Current asset

Shops Fittings 13000

Total Assets 18230

Liabilities

Current liability

Creditors 2030

Equity and capital

Capital (Less drawings

) 11500

Retained earnings 4700

Total liabilities 18230

Financial position can be reflected by preparing statement of balance sheet as on the end

day of year to obtain accurate information of available resources and obligations. This is widely

used by organization to present current liquidity status of enterprise in industry (Brigham and

Houston, 2021). In addition to this, above shown balance sheet has been prepared by segregating

all non as well current assets & liability in turn understanding can be provided.

1b)

Analyzing six features of information presented by financial statement for users as well benefits

& importance

There are different types of financial statement which provides varying aspect knowledge to

viewers. The reason to look into company's information is related with having significant data

for accomplishing decision making process (Robinson. 2020). Company presents different

financial statements which reflect information which is helpful for firm's suppliers, competitors,

lenders and other stakeholders (Williams and Dobelman, 2017). The six main features of

information for users of financial statements are as mentioned below:

The one of the most important characteristic of information shown by Financial

Statement (FS) is that it should be reliable so that fair decision can be taken by users

through referring such accounting data. It is responsibility of concerned organization to

share reliable information in turn trustworthiness can be gained among stakeholders.

Comparability is as well crucial feature of data shared through FS as economic decision

requires to implement ranking among course of action (Legrand, 2017). In addition to

this, it is significant for users like suppliers, customers, competitors, etc to make

comparison so that better end outcome can be derived from the available platforms.

Every users go through these information so that their purpose of maximizing

profitability can be achieved by identifying strengths and weakness.

Timeliness is how quickly is information is available to users as the less timely lower

would be usefulness in respect to decision making procedure. Stakeholders usually

depend on financials statements details for having structural decision making process.

Relevance is considered to be crucial component so that users can rely on such

information (Prihartono and Asandimitra, 2018). With respect to this, different types of

stakeholders want to have details of internal processes in order to know actual

circumstances prevailing to reach certain action therefore it is information should be

relevant. Possible future events & past related data should be included.

Consistency should be there while sharing data with users so that their purpose of

making judgments on company’s performance can be exerted by having this feature in

financial statements.

Analyzing six features of information presented by financial statement for users as well benefits

& importance

There are different types of financial statement which provides varying aspect knowledge to

viewers. The reason to look into company's information is related with having significant data

for accomplishing decision making process (Robinson. 2020). Company presents different

financial statements which reflect information which is helpful for firm's suppliers, competitors,

lenders and other stakeholders (Williams and Dobelman, 2017). The six main features of

information for users of financial statements are as mentioned below:

The one of the most important characteristic of information shown by Financial

Statement (FS) is that it should be reliable so that fair decision can be taken by users

through referring such accounting data. It is responsibility of concerned organization to

share reliable information in turn trustworthiness can be gained among stakeholders.

Comparability is as well crucial feature of data shared through FS as economic decision

requires to implement ranking among course of action (Legrand, 2017). In addition to

this, it is significant for users like suppliers, customers, competitors, etc to make

comparison so that better end outcome can be derived from the available platforms.

Every users go through these information so that their purpose of maximizing

profitability can be achieved by identifying strengths and weakness.

Timeliness is how quickly is information is available to users as the less timely lower

would be usefulness in respect to decision making procedure. Stakeholders usually

depend on financials statements details for having structural decision making process.

Relevance is considered to be crucial component so that users can rely on such

information (Prihartono and Asandimitra, 2018). With respect to this, different types of

stakeholders want to have details of internal processes in order to know actual

circumstances prevailing to reach certain action therefore it is information should be

relevant. Possible future events & past related data should be included.

Consistency should be there while sharing data with users so that their purpose of

making judgments on company’s performance can be exerted by having this feature in

financial statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Understability refers to providing information in such form that stakeholders can easily

interpret and understand actual meaning of it. The reason behind publishing data is to

give significant information which is completely understable so that users can take

positive decisions.

Significance and advantages related to data of FS to Users

There are various types of users who rely on financial statements for fulfilling their

objectives of taking decision regarding lending, investing, supplying, etc. in addition to this,

these information is widely significance for stakeholders as these are part of published

sources which provides trustworthiness of proper utilization, allocation and controlling of

resources (Yuniningsih Pertiwi and Purwanto, 2019). Users comprises suppliers, investors,

lenders, financial institutions, customers, competitors, etc they all play some different role in

company’s progress. The available data helps stakeholders to understand what form of

strategies, plans, etc are reason for shown expenditures. It helps users to get insights in way

of spending particular amount of capital. This can also be identified by users that how much

debt is taken & reason behind this. Financial health can be judged by giving emphasis on

performance, operations and cash flow.

Stakeholders get benefited from financial statements as it play important role in

providing information related to expenses, debt, revenue and profitability. Users like

financial institutions, lenders, creditors can assess how provided funds are allocated and

sued to know its efficiency of paying back. Company’s pricing strategy, cost structure,

revenue generating sources, fund raising method, etc helps in understanding company’s

ability to continue business with ensuring smooth functioning. The recorded data reflects all

mentioned aspects to derive meaningful conclusion in turn accurate judgments can be made

with respect to solvency insolvency. Operational efficiency can be evaluated by identifying

various factors which are current assets & liabilities, inventory, debtor, creditor turnover,

etc. as these contribute heavily in influencing stakeholders decision making process.

Various tools followed by company for choosing course for choosing course of

action aids users to determine direction of growth of business. In addition to this, trend lien

can be judged by comparing previous data with actual to evaluate deviation derived. The

interpret and understand actual meaning of it. The reason behind publishing data is to

give significant information which is completely understable so that users can take

positive decisions.

Significance and advantages related to data of FS to Users

There are various types of users who rely on financial statements for fulfilling their

objectives of taking decision regarding lending, investing, supplying, etc. in addition to this,

these information is widely significance for stakeholders as these are part of published

sources which provides trustworthiness of proper utilization, allocation and controlling of

resources (Yuniningsih Pertiwi and Purwanto, 2019). Users comprises suppliers, investors,

lenders, financial institutions, customers, competitors, etc they all play some different role in

company’s progress. The available data helps stakeholders to understand what form of

strategies, plans, etc are reason for shown expenditures. It helps users to get insights in way

of spending particular amount of capital. This can also be identified by users that how much

debt is taken & reason behind this. Financial health can be judged by giving emphasis on

performance, operations and cash flow.

Stakeholders get benefited from financial statements as it play important role in

providing information related to expenses, debt, revenue and profitability. Users like

financial institutions, lenders, creditors can assess how provided funds are allocated and

sued to know its efficiency of paying back. Company’s pricing strategy, cost structure,

revenue generating sources, fund raising method, etc helps in understanding company’s

ability to continue business with ensuring smooth functioning. The recorded data reflects all

mentioned aspects to derive meaningful conclusion in turn accurate judgments can be made

with respect to solvency insolvency. Operational efficiency can be evaluated by identifying

various factors which are current assets & liabilities, inventory, debtor, creditor turnover,

etc. as these contribute heavily in influencing stakeholders decision making process.

Various tools followed by company for choosing course for choosing course of

action aids users to determine direction of growth of business. In addition to this, trend lien

can be judged by comparing previous data with actual to evaluate deviation derived. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

users get benefited from financial statements as company’s ability to cooperate with

changing circumstances can be recognized by having variance details. Stakeholders can get

assistance in identifying efficiency in order to manage its obligations, etc. There are various

benefits which serves importance to users for having fair and systematic decision making

process. Company should pay attention on providing such benefits through publishing

appropriate information through balance sheet, equity shareholders , income, cash flow

statements, etc in turn stakeholders can reach positive decision making procedure.

QUESTION 2

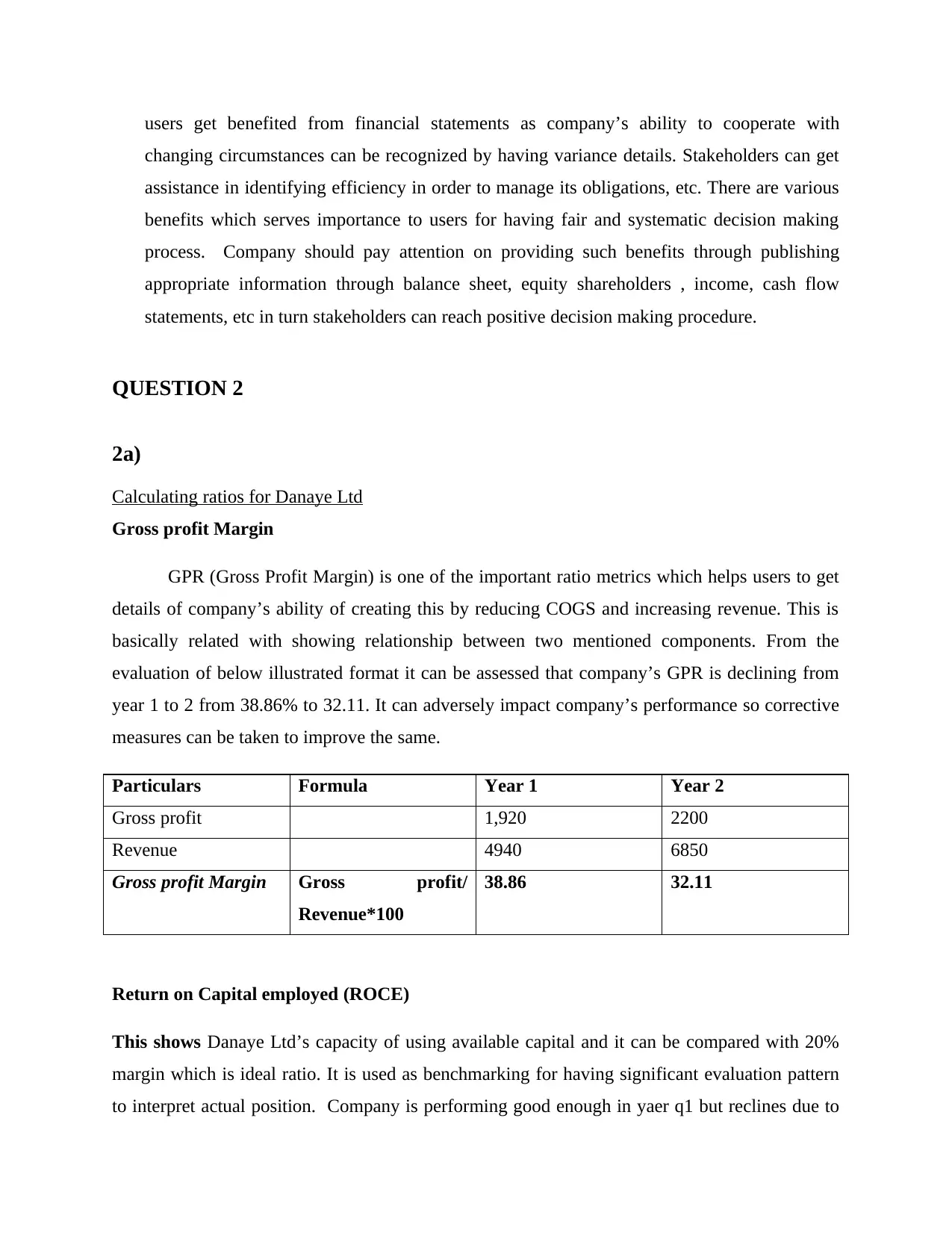

2a)

Calculating ratios for Danaye Ltd

Gross profit Margin

GPR (Gross Profit Margin) is one of the important ratio metrics which helps users to get

details of company’s ability of creating this by reducing COGS and increasing revenue. This is

basically related with showing relationship between two mentioned components. From the

evaluation of below illustrated format it can be assessed that company’s GPR is declining from

year 1 to 2 from 38.86% to 32.11. It can adversely impact company’s performance so corrective

measures can be taken to improve the same.

Particulars Formula Year 1 Year 2

Gross profit 1,920 2200

Revenue 4940 6850

Gross profit Margin Gross profit/

Revenue*100

38.86 32.11

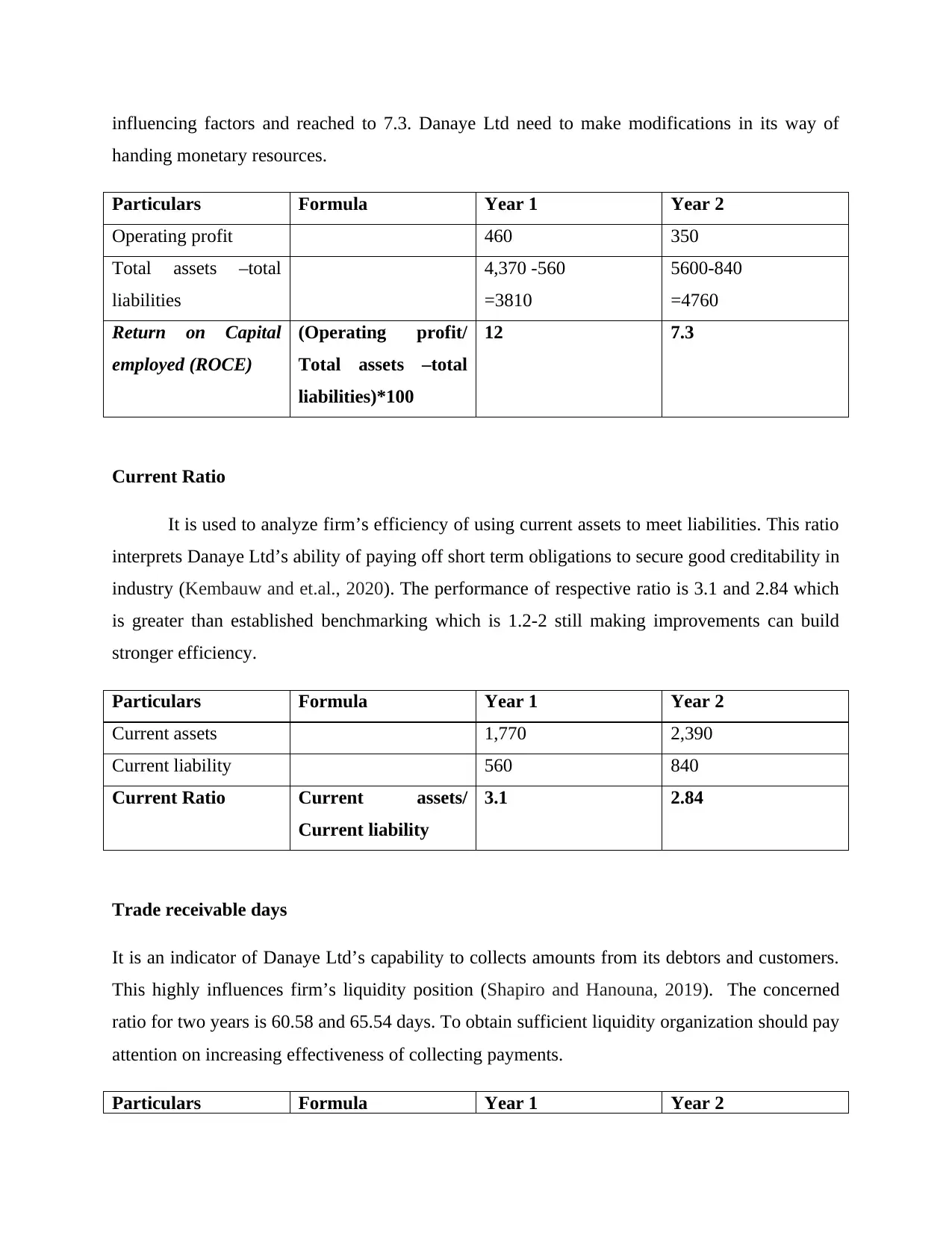

Return on Capital employed (ROCE)

This shows Danaye Ltd’s capacity of using available capital and it can be compared with 20%

margin which is ideal ratio. It is used as benchmarking for having significant evaluation pattern

to interpret actual position. Company is performing good enough in yaer q1 but reclines due to

changing circumstances can be recognized by having variance details. Stakeholders can get

assistance in identifying efficiency in order to manage its obligations, etc. There are various

benefits which serves importance to users for having fair and systematic decision making

process. Company should pay attention on providing such benefits through publishing

appropriate information through balance sheet, equity shareholders , income, cash flow

statements, etc in turn stakeholders can reach positive decision making procedure.

QUESTION 2

2a)

Calculating ratios for Danaye Ltd

Gross profit Margin

GPR (Gross Profit Margin) is one of the important ratio metrics which helps users to get

details of company’s ability of creating this by reducing COGS and increasing revenue. This is

basically related with showing relationship between two mentioned components. From the

evaluation of below illustrated format it can be assessed that company’s GPR is declining from

year 1 to 2 from 38.86% to 32.11. It can adversely impact company’s performance so corrective

measures can be taken to improve the same.

Particulars Formula Year 1 Year 2

Gross profit 1,920 2200

Revenue 4940 6850

Gross profit Margin Gross profit/

Revenue*100

38.86 32.11

Return on Capital employed (ROCE)

This shows Danaye Ltd’s capacity of using available capital and it can be compared with 20%

margin which is ideal ratio. It is used as benchmarking for having significant evaluation pattern

to interpret actual position. Company is performing good enough in yaer q1 but reclines due to

influencing factors and reached to 7.3. Danaye Ltd need to make modifications in its way of

handing monetary resources.

Particulars Formula Year 1 Year 2

Operating profit 460 350

Total assets –total

liabilities

4,370 -560

=3810

5600-840

=4760

Return on Capital

employed (ROCE)

(Operating profit/

Total assets –total

liabilities)*100

12 7.3

Current Ratio

It is used to analyze firm’s efficiency of using current assets to meet liabilities. This ratio

interprets Danaye Ltd’s ability of paying off short term obligations to secure good creditability in

industry (Kembauw and et.al., 2020). The performance of respective ratio is 3.1 and 2.84 which

is greater than established benchmarking which is 1.2-2 still making improvements can build

stronger efficiency.

Particulars Formula Year 1 Year 2

Current assets 1,770 2,390

Current liability 560 840

Current Ratio Current assets/

Current liability

3.1 2.84

Trade receivable days

It is an indicator of Danaye Ltd’s capability to collects amounts from its debtors and customers.

This highly influences firm’s liquidity position (Shapiro and Hanouna, 2019). The concerned

ratio for two years is 60.58 and 65.54 days. To obtain sufficient liquidity organization should pay

attention on increasing effectiveness of collecting payments.

Particulars Formula Year 1 Year 2

handing monetary resources.

Particulars Formula Year 1 Year 2

Operating profit 460 350

Total assets –total

liabilities

4,370 -560

=3810

5600-840

=4760

Return on Capital

employed (ROCE)

(Operating profit/

Total assets –total

liabilities)*100

12 7.3

Current Ratio

It is used to analyze firm’s efficiency of using current assets to meet liabilities. This ratio

interprets Danaye Ltd’s ability of paying off short term obligations to secure good creditability in

industry (Kembauw and et.al., 2020). The performance of respective ratio is 3.1 and 2.84 which

is greater than established benchmarking which is 1.2-2 still making improvements can build

stronger efficiency.

Particulars Formula Year 1 Year 2

Current assets 1,770 2,390

Current liability 560 840

Current Ratio Current assets/

Current liability

3.1 2.84

Trade receivable days

It is an indicator of Danaye Ltd’s capability to collects amounts from its debtors and customers.

This highly influences firm’s liquidity position (Shapiro and Hanouna, 2019). The concerned

ratio for two years is 60.58 and 65.54 days. To obtain sufficient liquidity organization should pay

attention on increasing effectiveness of collecting payments.

Particulars Formula Year 1 Year 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Trade receivables 820 1,230

Revenue 4940 6850

Trade receivable

days

Trade receivables/

Revenue*365

60.58 65.54

Trade payable days

There are different type of users who pay attention on trade payable days which involves

creditors, lenders, suppliers, etc. they expect it to be low in turn their funds can be paid by

organization easily. The performance of Danaye Ltd in respect to this ratio is 21645 &2116 days

which highly need improvements to gain trustworthiness among stakeholders.

Particulars Formula Year 1 Year 2

Purchase 3,320 4870

Trade payables 560 840

Trade payable days Purchase/ Trade

payables*365

21645 2116

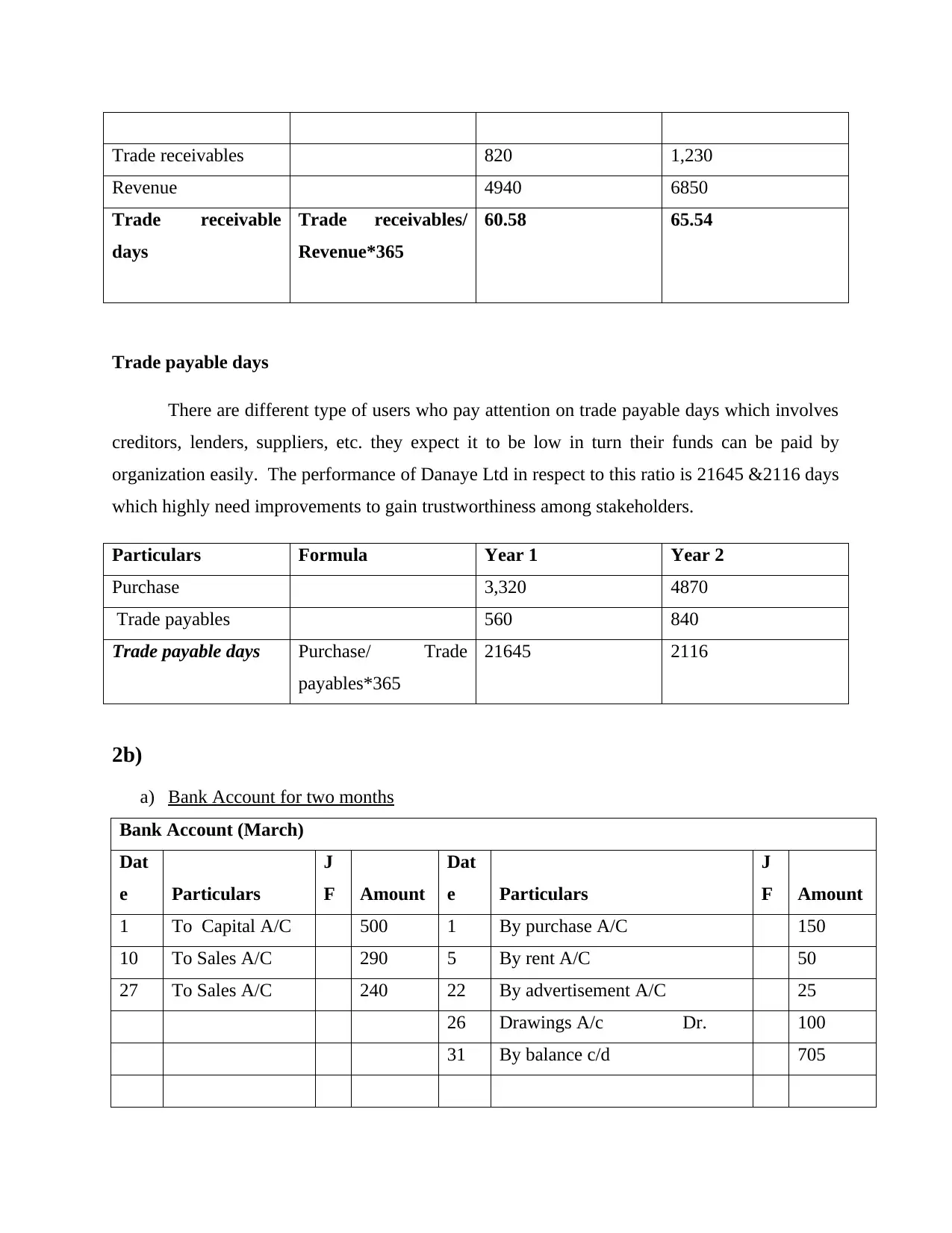

2b)

a) Bank Account for two months

Bank Account (March)

Dat

e Particulars

J

F Amount

Dat

e Particulars

J

F Amount

1 To Capital A/C 500 1 By purchase A/C 150

10 To Sales A/C 290 5 By rent A/C 50

27 To Sales A/C 240 22 By advertisement A/C 25

26 Drawings A/c Dr. 100

31 By balance c/d 705

Revenue 4940 6850

Trade receivable

days

Trade receivables/

Revenue*365

60.58 65.54

Trade payable days

There are different type of users who pay attention on trade payable days which involves

creditors, lenders, suppliers, etc. they expect it to be low in turn their funds can be paid by

organization easily. The performance of Danaye Ltd in respect to this ratio is 21645 &2116 days

which highly need improvements to gain trustworthiness among stakeholders.

Particulars Formula Year 1 Year 2

Purchase 3,320 4870

Trade payables 560 840

Trade payable days Purchase/ Trade

payables*365

21645 2116

2b)

a) Bank Account for two months

Bank Account (March)

Dat

e Particulars

J

F Amount

Dat

e Particulars

J

F Amount

1 To Capital A/C 500 1 By purchase A/C 150

10 To Sales A/C 290 5 By rent A/C 50

27 To Sales A/C 240 22 By advertisement A/C 25

26 Drawings A/c Dr. 100

31 By balance c/d 705

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1030 1030

Bank Account (April )

Dat

e Particulars

J

F

Amoun

t

Dat

e Particulars

J

F

Amoun

t

2 By purchase A/C 100

1 By balance b/d 705 5 By rent A/C 50

14 To Loan (L lock) A/c 450 23 Drawings A/c Dr. 75

16 To Sales A/C 330 29 By advertisement A/C 30

26 To Sales A/C 180 30 by balance c/d 1410

1665 1665

b) Other accounts are as follows:

Loan A/C (L Lock )

Date Particulars

J

F Amount Date Particulars

J

F Amount

30 To balance c/d 450 14 By bank A/c 450

450 450

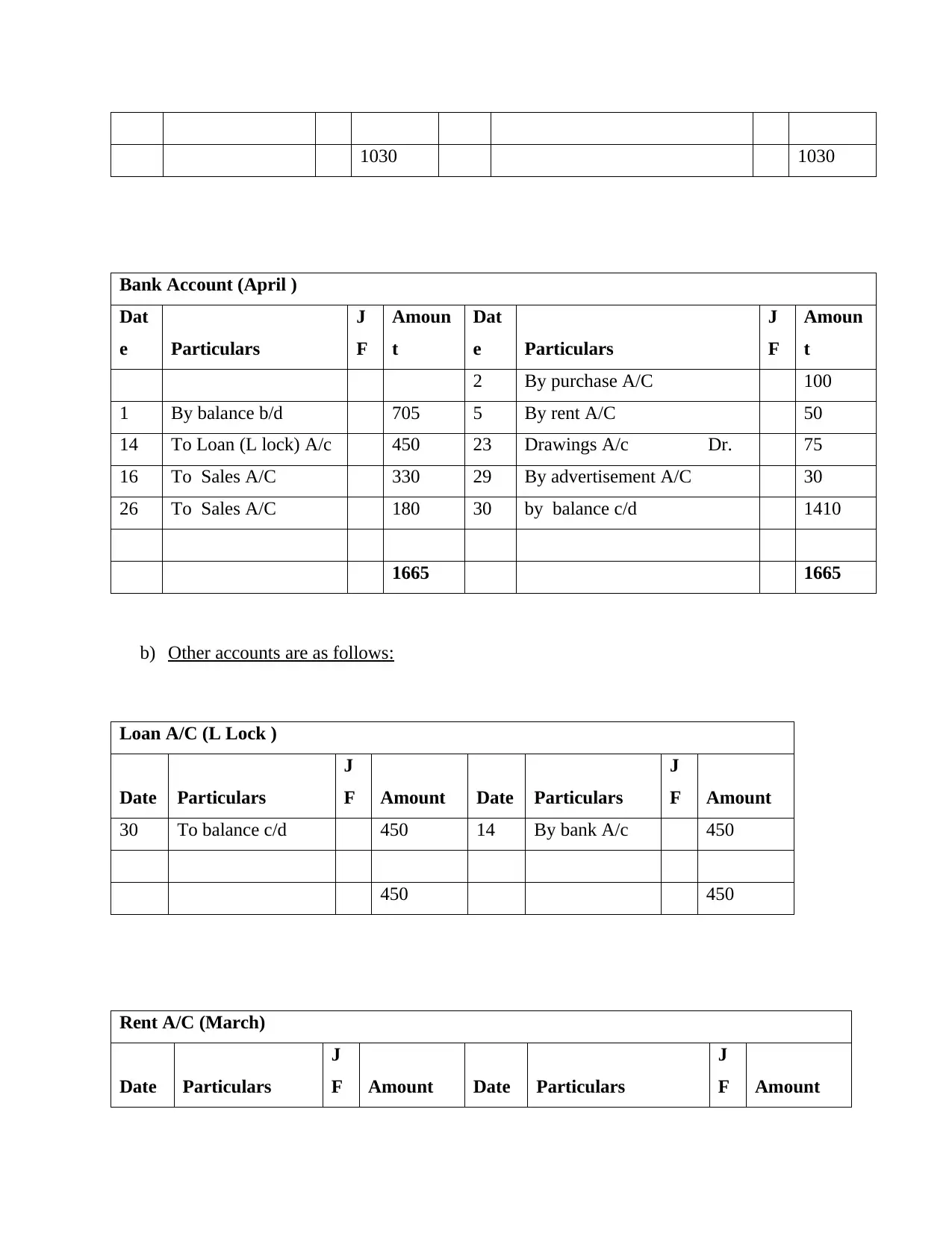

Rent A/C (March)

Date Particulars

J

F Amount Date Particulars

J

F Amount

Bank Account (April )

Dat

e Particulars

J

F

Amoun

t

Dat

e Particulars

J

F

Amoun

t

2 By purchase A/C 100

1 By balance b/d 705 5 By rent A/C 50

14 To Loan (L lock) A/c 450 23 Drawings A/c Dr. 75

16 To Sales A/C 330 29 By advertisement A/C 30

26 To Sales A/C 180 30 by balance c/d 1410

1665 1665

b) Other accounts are as follows:

Loan A/C (L Lock )

Date Particulars

J

F Amount Date Particulars

J

F Amount

30 To balance c/d 450 14 By bank A/c 450

450 450

Rent A/C (March)

Date Particulars

J

F Amount Date Particulars

J

F Amount

5 To bank A/c 50 31 By balance c/d 50

50 50

Rent A/C (April)

Date Particulars

J

F Amount Date Particulars

J

F Amount

1 To balance b/d 50 30 By balance c/d 100

5 To Bank A/c 50

Purchase A/C (March )

Date Particulars

J

F Amount Date Particulars

J

F Amount

1 To bank A/c 150 31 By balance c/d 150

150 150

Purchase A/C (April )

Date Particulars

J

F Amount Date Particulars

J

F Amount

1 To balance b/d 150 30 By balance c/d 250

2 To Bank A/c 100

250 250

50 50

Rent A/C (April)

Date Particulars

J

F Amount Date Particulars

J

F Amount

1 To balance b/d 50 30 By balance c/d 100

5 To Bank A/c 50

Purchase A/C (March )

Date Particulars

J

F Amount Date Particulars

J

F Amount

1 To bank A/c 150 31 By balance c/d 150

150 150

Purchase A/C (April )

Date Particulars

J

F Amount Date Particulars

J

F Amount

1 To balance b/d 150 30 By balance c/d 250

2 To Bank A/c 100

250 250

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.