UGB106 Management Accounting: Costing, Budgeting, Variance Analysis

VerifiedAdded on 2023/06/18

|20

|4088

|226

Homework Assignment

AI Summary

This assignment provides solutions to management accounting problems, covering break-even analysis, margin of safety calculations, and profit estimations for Plaistead Plc. It also addresses cost allocation, overhead recovery rates, and product costing for Crawford Plc, alongside a discussion on absorption costing advantages and disadvantages. Furthermore, the assignment includes budget and variance analysis for Jayrod Plc, offering a comprehensive overview of key management accounting concepts and their practical application in business scenarios. The assignment adheres to the UGB106 Introduction to Management Accounting course requirements.

UGB 106 Introduction to

management accounting

management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents................................................................................................................................................2

Part 1.....................................................................................................................................................3

Question 2: Plaistead Plc..................................................................................................................3

Part 2.....................................................................................................................................................8

Question 3: Crawford Plc.................................................................................................................8

Part 3.....................................................................................................................................................3

Question 4:........................................................................................................................................3

REFERENCES...................................................................................................................................10

Contents................................................................................................................................................2

Part 1.....................................................................................................................................................3

Question 2: Plaistead Plc..................................................................................................................3

Part 2.....................................................................................................................................................8

Question 3: Crawford Plc.................................................................................................................8

Part 3.....................................................................................................................................................3

Question 4:........................................................................................................................................3

REFERENCES...................................................................................................................................10

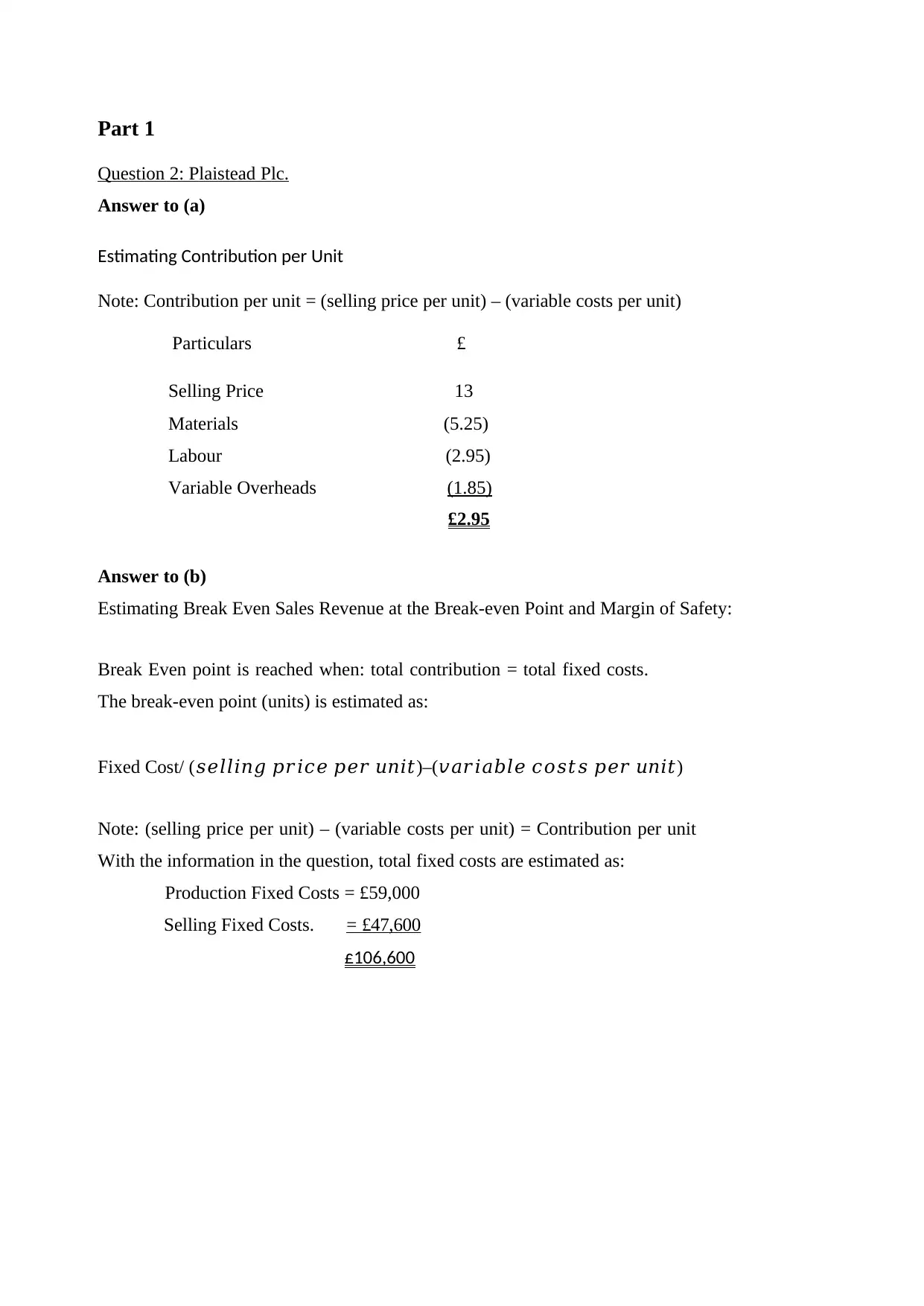

Part 1

Question 2: Plaistead Plc.

Answer to (a)

Estimating Contribution per Unit

Note: Contribution per unit = (selling price per unit) – (variable costs per unit)

Particulars £

Selling Price 13

Materials (5.25)

Labour (2.95)

Variable Overheads (1.85)

£2.95

Answer to (b)

Estimating Break Even Sales Revenue at the Break-even Point and Margin of Safety:

Break Even point is reached when: total contribution = total fixed costs.

The break-even point (units) is estimated as:

Fixed Cost/ (𝑠𝑒𝑙𝑙𝑖𝑛𝑔 𝑝𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡)–(𝑣𝑎𝑟𝑖𝑎𝑏𝑙𝑒 𝑐𝑜𝑠𝑡𝑠 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡)

Note: (selling price per unit) – (variable costs per unit) = Contribution per unit

With the information in the question, total fixed costs are estimated as:

Production Fixed Costs = £59,000

Selling Fixed Costs. = £47,600

£106,600

Question 2: Plaistead Plc.

Answer to (a)

Estimating Contribution per Unit

Note: Contribution per unit = (selling price per unit) – (variable costs per unit)

Particulars £

Selling Price 13

Materials (5.25)

Labour (2.95)

Variable Overheads (1.85)

£2.95

Answer to (b)

Estimating Break Even Sales Revenue at the Break-even Point and Margin of Safety:

Break Even point is reached when: total contribution = total fixed costs.

The break-even point (units) is estimated as:

Fixed Cost/ (𝑠𝑒𝑙𝑙𝑖𝑛𝑔 𝑝𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡)–(𝑣𝑎𝑟𝑖𝑎𝑏𝑙𝑒 𝑐𝑜𝑠𝑡𝑠 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡)

Note: (selling price per unit) – (variable costs per unit) = Contribution per unit

With the information in the question, total fixed costs are estimated as:

Production Fixed Costs = £59,000

Selling Fixed Costs. = £47,600

£106,600

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

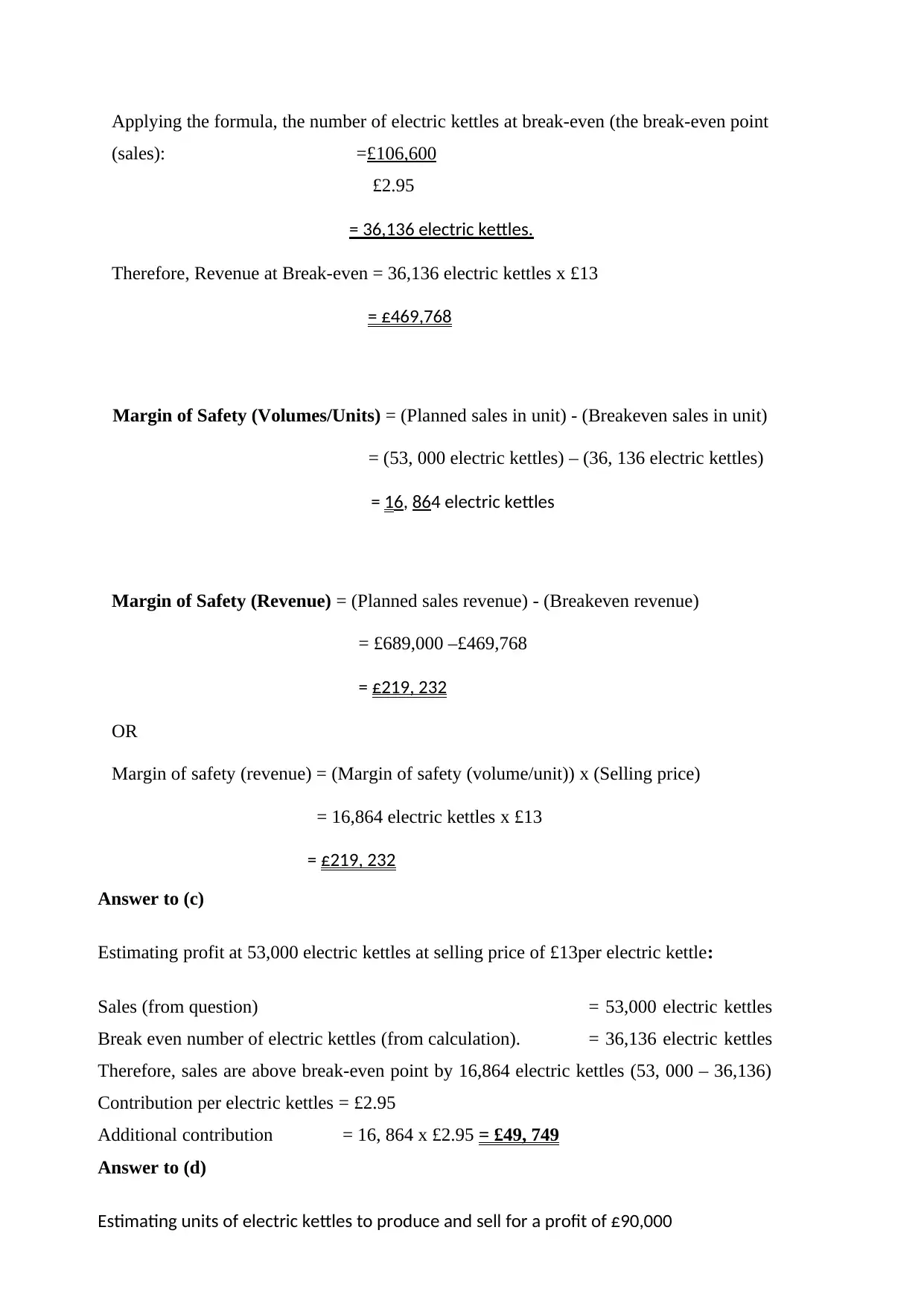

Applying the formula, the number of electric kettles at break-even (the break-even point

(sales): =£106,600

£2.95

= 36,136 electric kettles.

Therefore, Revenue at Break-even = 36,136 electric kettles x £13

= £469,768

Margin of Safety (Volumes/Units) = (Planned sales in unit) - (Breakeven sales in unit)

= (53, 000 electric kettles) – (36, 136 electric kettles)

= 16, 864 electric kettles

Margin of Safety (Revenue) = (Planned sales revenue) - (Breakeven revenue)

= £689,000 –£469,768

= £219, 232

OR

Margin of safety (revenue) = (Margin of safety (volume/unit)) x (Selling price)

= 16,864 electric kettles x £13

= £219, 232

Answer to (c)

Estimating profit at 53,000 electric kettles at selling price of £13per electric kettle:

Sales (from question) = 53,000 electric kettles

Break even number of electric kettles (from calculation). = 36,136 electric kettles

Therefore, sales are above break-even point by 16,864 electric kettles (53, 000 – 36,136)

Contribution per electric kettles = £2.95

Additional contribution = 16, 864 x £2.95 = £49, 749

Answer to (d)

Estimating units of electric kettles to produce and sell for a profit of £90,000

(sales): =£106,600

£2.95

= 36,136 electric kettles.

Therefore, Revenue at Break-even = 36,136 electric kettles x £13

= £469,768

Margin of Safety (Volumes/Units) = (Planned sales in unit) - (Breakeven sales in unit)

= (53, 000 electric kettles) – (36, 136 electric kettles)

= 16, 864 electric kettles

Margin of Safety (Revenue) = (Planned sales revenue) - (Breakeven revenue)

= £689,000 –£469,768

= £219, 232

OR

Margin of safety (revenue) = (Margin of safety (volume/unit)) x (Selling price)

= 16,864 electric kettles x £13

= £219, 232

Answer to (c)

Estimating profit at 53,000 electric kettles at selling price of £13per electric kettle:

Sales (from question) = 53,000 electric kettles

Break even number of electric kettles (from calculation). = 36,136 electric kettles

Therefore, sales are above break-even point by 16,864 electric kettles (53, 000 – 36,136)

Contribution per electric kettles = £2.95

Additional contribution = 16, 864 x £2.95 = £49, 749

Answer to (d)

Estimating units of electric kettles to produce and sell for a profit of £90,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

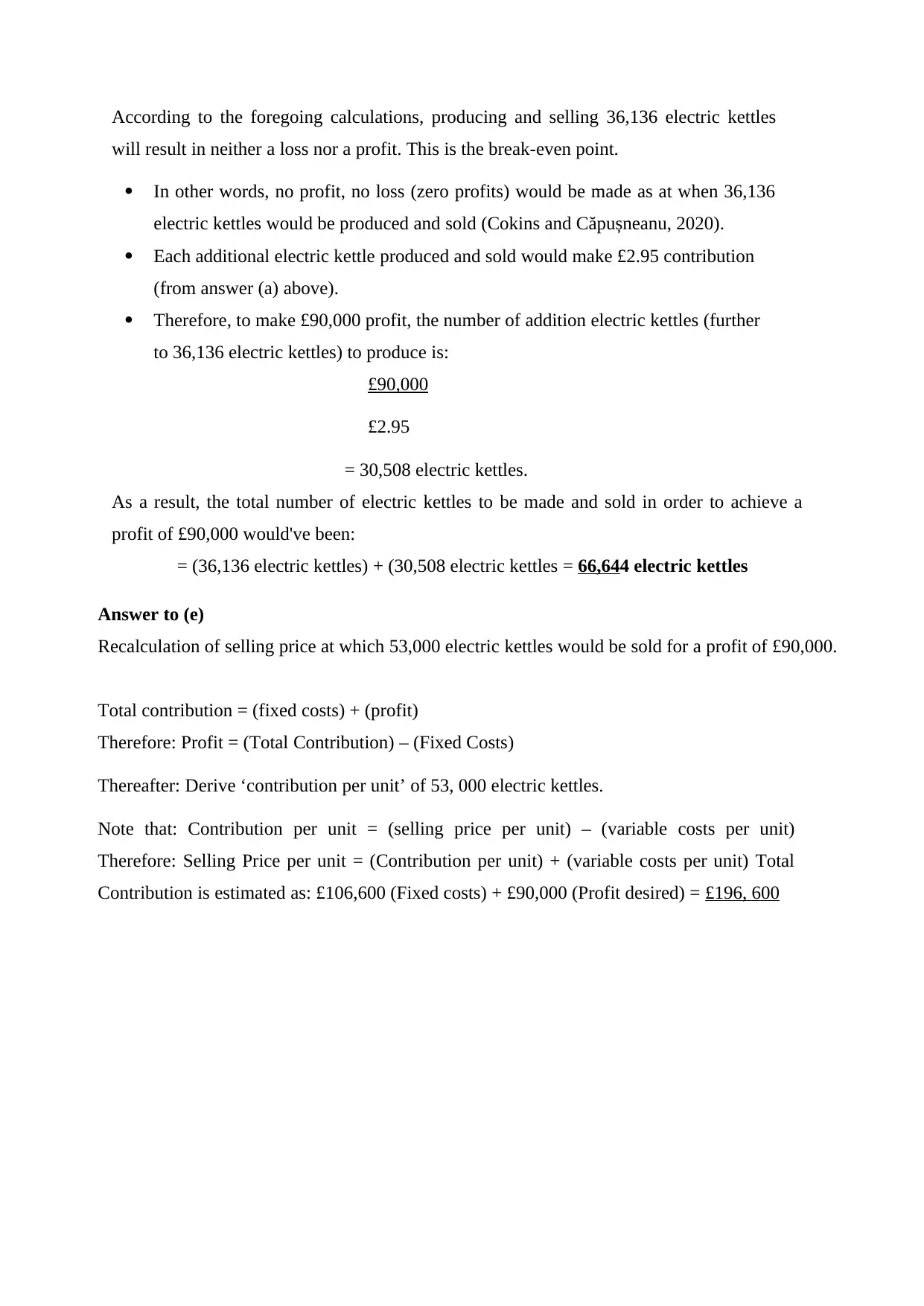

According to the foregoing calculations, producing and selling 36,136 electric kettles

will result in neither a loss nor a profit. This is the break-even point.

In other words, no profit, no loss (zero profits) would be made as at when 36,136

electric kettles would be produced and sold (Cokins and Căpușneanu, 2020).

Each additional electric kettle produced and sold would make £2.95 contribution

(from answer (a) above).

Therefore, to make £90,000 profit, the number of addition electric kettles (further

to 36,136 electric kettles) to produce is:

£90,000

£2.95

= 30,508 electric kettles.

As a result, the total number of electric kettles to be made and sold in order to achieve a

profit of £90,000 would've been:

= (36,136 electric kettles) + (30,508 electric kettles = 66,644 electric kettles

Answer to (e)

Recalculation of selling price at which 53,000 electric kettles would be sold for a profit of £90,000.

Total contribution = (fixed costs) + (profit)

Therefore: Profit = (Total Contribution) – (Fixed Costs)

Thereafter: Derive ‘contribution per unit’ of 53, 000 electric kettles.

Note that: Contribution per unit = (selling price per unit) – (variable costs per unit)

Therefore: Selling Price per unit = (Contribution per unit) + (variable costs per unit) Total

Contribution is estimated as: £106,600 (Fixed costs) + £90,000 (Profit desired) = £196, 600

will result in neither a loss nor a profit. This is the break-even point.

In other words, no profit, no loss (zero profits) would be made as at when 36,136

electric kettles would be produced and sold (Cokins and Căpușneanu, 2020).

Each additional electric kettle produced and sold would make £2.95 contribution

(from answer (a) above).

Therefore, to make £90,000 profit, the number of addition electric kettles (further

to 36,136 electric kettles) to produce is:

£90,000

£2.95

= 30,508 electric kettles.

As a result, the total number of electric kettles to be made and sold in order to achieve a

profit of £90,000 would've been:

= (36,136 electric kettles) + (30,508 electric kettles = 66,644 electric kettles

Answer to (e)

Recalculation of selling price at which 53,000 electric kettles would be sold for a profit of £90,000.

Total contribution = (fixed costs) + (profit)

Therefore: Profit = (Total Contribution) – (Fixed Costs)

Thereafter: Derive ‘contribution per unit’ of 53, 000 electric kettles.

Note that: Contribution per unit = (selling price per unit) – (variable costs per unit)

Therefore: Selling Price per unit = (Contribution per unit) + (variable costs per unit) Total

Contribution is estimated as: £106,600 (Fixed costs) + £90,000 (Profit desired) = £196, 600

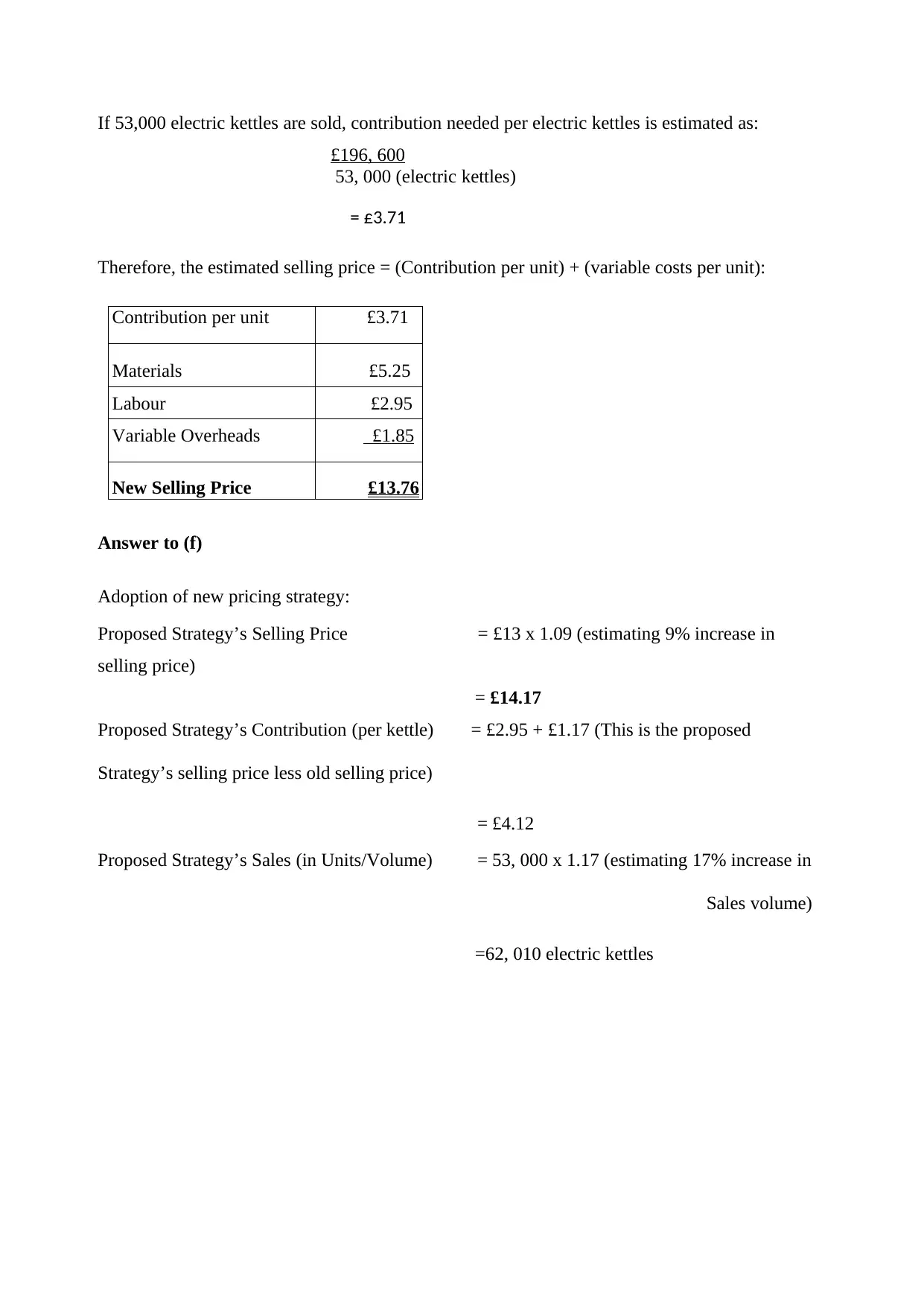

If 53,000 electric kettles are sold, contribution needed per electric kettles is estimated as:

£196, 600

53, 000 (electric kettles)

= £3.71

Therefore, the estimated selling price = (Contribution per unit) + (variable costs per unit):

Contribution per unit £3.71

Materials £5.25

Labour £2.95

Variable Overheads £1.85

New Selling Price £13.76

Answer to (f)

Adoption of new pricing strategy:

Proposed Strategy’s Selling Price = £13 x 1.09 (estimating 9% increase in

selling price)

= £14.17

Proposed Strategy’s Contribution (per kettle) = £2.95 + £1.17 (This is the proposed

Strategy’s selling price less old selling price)

= £4.12

Proposed Strategy’s Sales (in Units/Volume) = 53, 000 x 1.17 (estimating 17% increase in

Sales volume)

=62, 010 electric kettles

£196, 600

53, 000 (electric kettles)

= £3.71

Therefore, the estimated selling price = (Contribution per unit) + (variable costs per unit):

Contribution per unit £3.71

Materials £5.25

Labour £2.95

Variable Overheads £1.85

New Selling Price £13.76

Answer to (f)

Adoption of new pricing strategy:

Proposed Strategy’s Selling Price = £13 x 1.09 (estimating 9% increase in

selling price)

= £14.17

Proposed Strategy’s Contribution (per kettle) = £2.95 + £1.17 (This is the proposed

Strategy’s selling price less old selling price)

= £4.12

Proposed Strategy’s Sales (in Units/Volume) = 53, 000 x 1.17 (estimating 17% increase in

Sales volume)

=62, 010 electric kettles

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

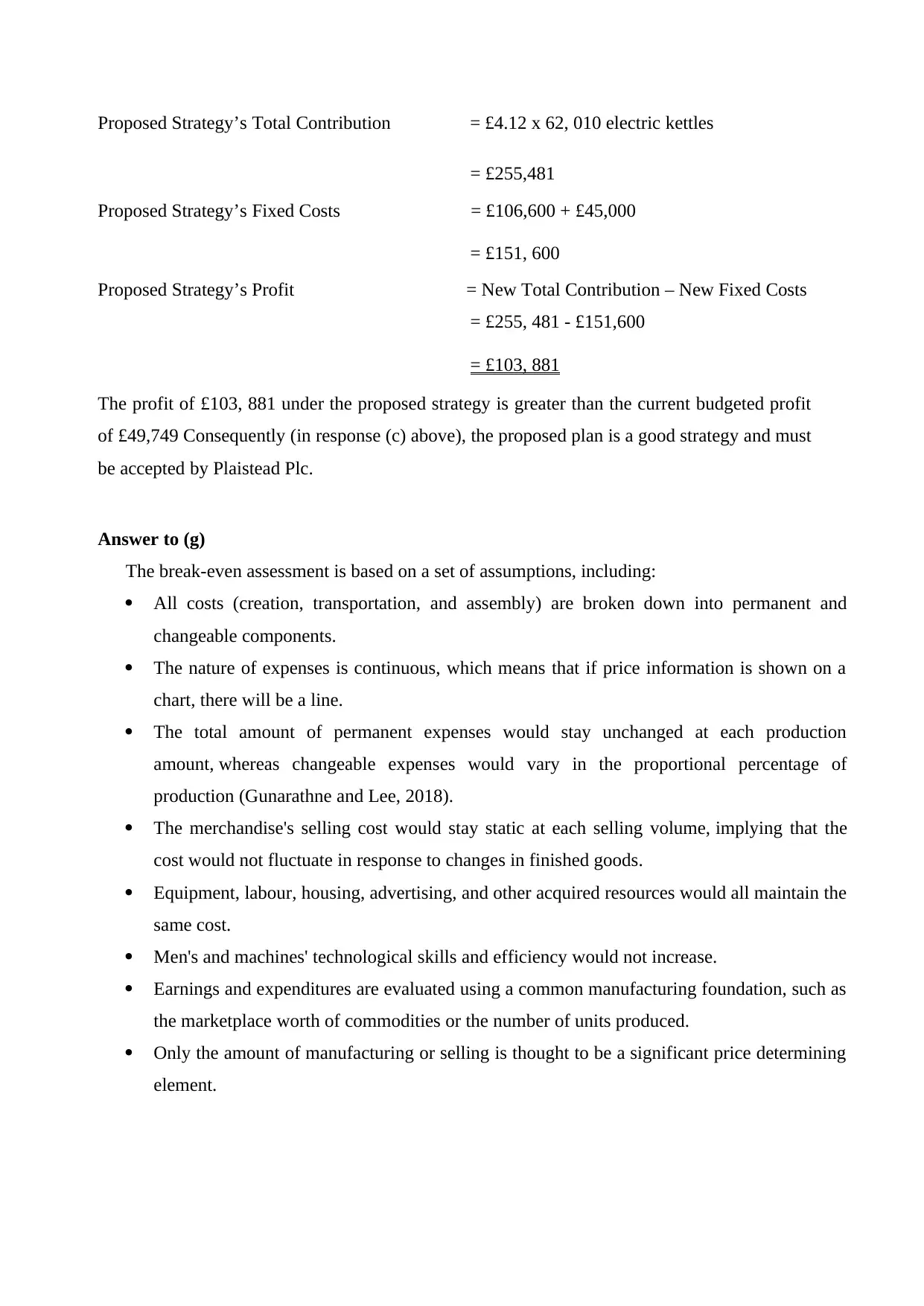

Proposed Strategy’s Total Contribution = £4.12 x 62, 010 electric kettles

= £255,481

Proposed Strategy’s Fixed Costs = £106,600 + £45,000

= £151, 600

Proposed Strategy’s Profit = New Total Contribution – New Fixed Costs

= £255, 481 - £151,600

= £103, 881

The profit of £103, 881 under the proposed strategy is greater than the current budgeted profit

of £49,749 Consequently (in response (c) above), the proposed plan is a good strategy and must

be accepted by Plaistead Plc.

Answer to (g)

The break-even assessment is based on a set of assumptions, including:

All costs (creation, transportation, and assembly) are broken down into permanent and

changeable components.

The nature of expenses is continuous, which means that if price information is shown on a

chart, there will be a line.

The total amount of permanent expenses would stay unchanged at each production

amount, whereas changeable expenses would vary in the proportional percentage of

production (Gunarathne and Lee, 2018).

The merchandise's selling cost would stay static at each selling volume, implying that the

cost would not fluctuate in response to changes in finished goods.

Equipment, labour, housing, advertising, and other acquired resources would all maintain the

same cost.

Men's and machines' technological skills and efficiency would not increase.

Earnings and expenditures are evaluated using a common manufacturing foundation, such as

the marketplace worth of commodities or the number of units produced.

Only the amount of manufacturing or selling is thought to be a significant price determining

element.

= £255,481

Proposed Strategy’s Fixed Costs = £106,600 + £45,000

= £151, 600

Proposed Strategy’s Profit = New Total Contribution – New Fixed Costs

= £255, 481 - £151,600

= £103, 881

The profit of £103, 881 under the proposed strategy is greater than the current budgeted profit

of £49,749 Consequently (in response (c) above), the proposed plan is a good strategy and must

be accepted by Plaistead Plc.

Answer to (g)

The break-even assessment is based on a set of assumptions, including:

All costs (creation, transportation, and assembly) are broken down into permanent and

changeable components.

The nature of expenses is continuous, which means that if price information is shown on a

chart, there will be a line.

The total amount of permanent expenses would stay unchanged at each production

amount, whereas changeable expenses would vary in the proportional percentage of

production (Gunarathne and Lee, 2018).

The merchandise's selling cost would stay static at each selling volume, implying that the

cost would not fluctuate in response to changes in finished goods.

Equipment, labour, housing, advertising, and other acquired resources would all maintain the

same cost.

Men's and machines' technological skills and efficiency would not increase.

Earnings and expenditures are evaluated using a common manufacturing foundation, such as

the marketplace worth of commodities or the number of units produced.

Only the amount of manufacturing or selling is thought to be a significant price determining

element.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

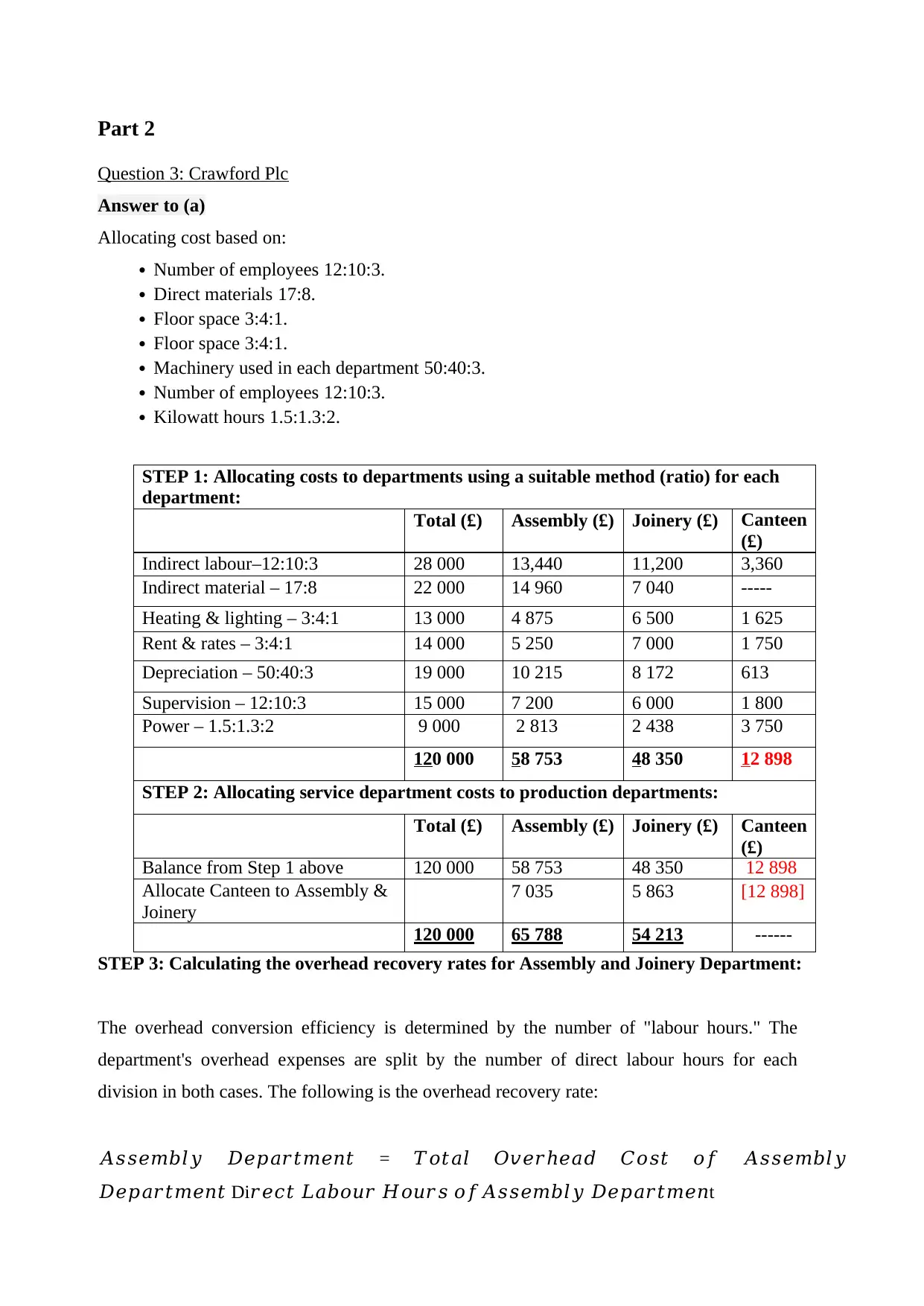

Part 2

Question 3: Crawford Plc

Answer to (a)

Allocating cost based on:

Number of employees 12:10:3.

Direct materials 17:8.

Floor space 3:4:1.

Floor space 3:4:1.

Machinery used in each department 50:40:3.

Number of employees 12:10:3.

Kilowatt hours 1.5:1.3:2.

STEP 1: Allocating costs to departments using a suitable method (ratio) for each

department:

Total (£) Assembly (£) Joinery (£) Canteen

(£)

Indirect labour–12:10:3 28 000 13,440 11,200 3,360

Indirect material – 17:8 22 000 14 960 7 040 -----

Heating & lighting – 3:4:1 13 000 4 875 6 500 1 625

Rent & rates – 3:4:1 14 000 5 250 7 000 1 750

Depreciation – 50:40:3 19 000 10 215 8 172 613

Supervision – 12:10:3 15 000 7 200 6 000 1 800

Power – 1.5:1.3:2 9 000 2 813 2 438 3 750

120 000 58 753 48 350 12 898

STEP 2: Allocating service department costs to production departments:

Total (£) Assembly (£) Joinery (£) Canteen

(£)

Balance from Step 1 above 120 000 58 753 48 350 12 898

Allocate Canteen to Assembly &

Joinery

7 035 5 863 [12 898]

120 000 65 788 54 213 ------

STEP 3: Calculating the overhead recovery rates for Assembly and Joinery Department:

The overhead conversion efficiency is determined by the number of "labour hours." The

department's overhead expenses are split by the number of direct labour hours for each

division in both cases. The following is the overhead recovery rate:

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 = 𝑇𝑜𝑡𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦

𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 Di𝑟𝑒𝑐𝑡 𝐿𝑎𝑏𝑜𝑢𝑟 𝐻𝑜𝑢𝑟𝑠 𝑜𝑓𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛t

Question 3: Crawford Plc

Answer to (a)

Allocating cost based on:

Number of employees 12:10:3.

Direct materials 17:8.

Floor space 3:4:1.

Floor space 3:4:1.

Machinery used in each department 50:40:3.

Number of employees 12:10:3.

Kilowatt hours 1.5:1.3:2.

STEP 1: Allocating costs to departments using a suitable method (ratio) for each

department:

Total (£) Assembly (£) Joinery (£) Canteen

(£)

Indirect labour–12:10:3 28 000 13,440 11,200 3,360

Indirect material – 17:8 22 000 14 960 7 040 -----

Heating & lighting – 3:4:1 13 000 4 875 6 500 1 625

Rent & rates – 3:4:1 14 000 5 250 7 000 1 750

Depreciation – 50:40:3 19 000 10 215 8 172 613

Supervision – 12:10:3 15 000 7 200 6 000 1 800

Power – 1.5:1.3:2 9 000 2 813 2 438 3 750

120 000 58 753 48 350 12 898

STEP 2: Allocating service department costs to production departments:

Total (£) Assembly (£) Joinery (£) Canteen

(£)

Balance from Step 1 above 120 000 58 753 48 350 12 898

Allocate Canteen to Assembly &

Joinery

7 035 5 863 [12 898]

120 000 65 788 54 213 ------

STEP 3: Calculating the overhead recovery rates for Assembly and Joinery Department:

The overhead conversion efficiency is determined by the number of "labour hours." The

department's overhead expenses are split by the number of direct labour hours for each

division in both cases. The following is the overhead recovery rate:

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 = 𝑇𝑜𝑡𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦

𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 Di𝑟𝑒𝑐𝑡 𝐿𝑎𝑏𝑜𝑢𝑟 𝐻𝑜𝑢𝑟𝑠 𝑜𝑓𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛t

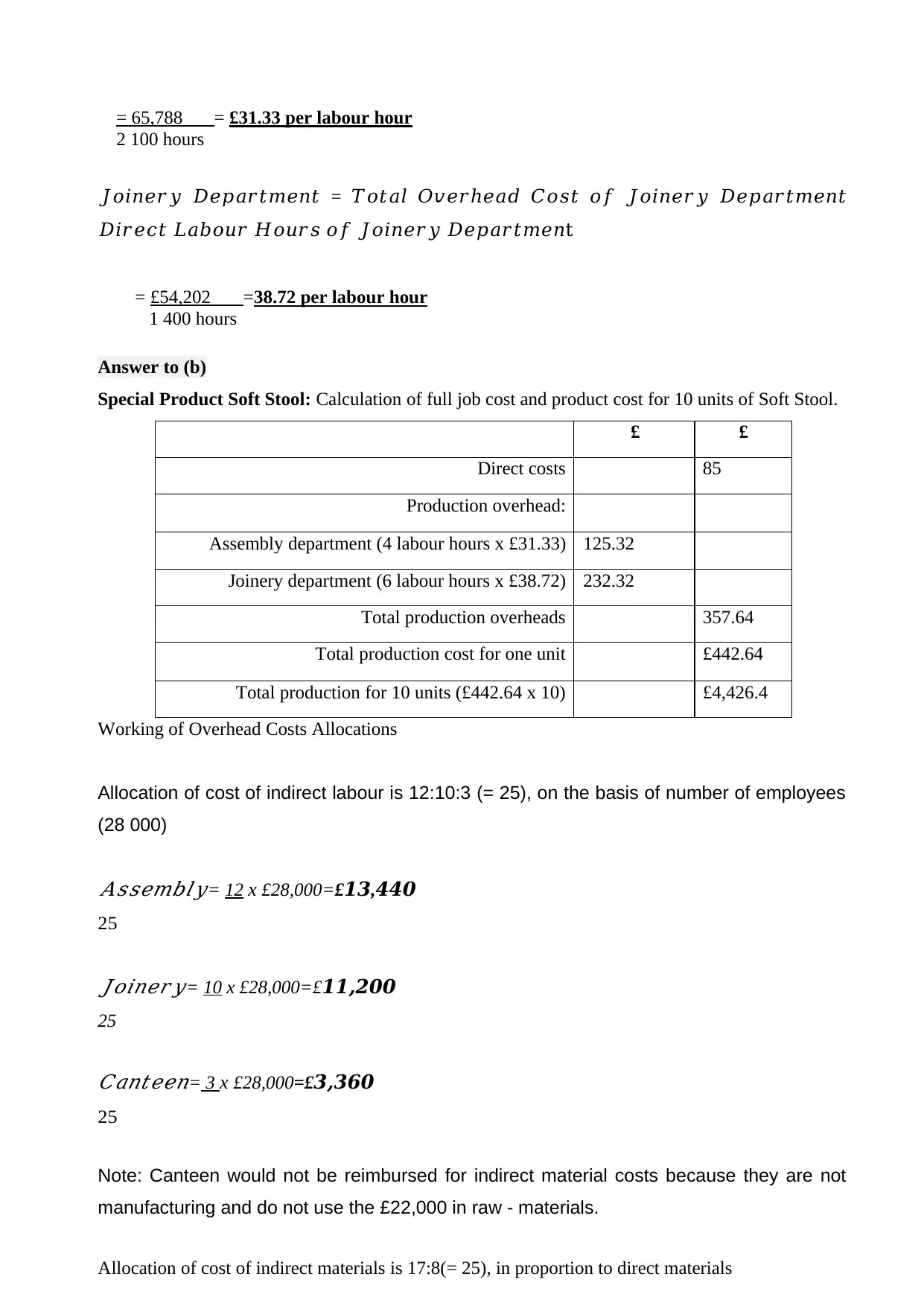

= 65,788 = £31.33 per labour hour

2 100 hours

𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 = 𝑇𝑜𝑡𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡

𝐷𝑖𝑟𝑒𝑐𝑡 𝐿𝑎𝑏𝑜𝑢𝑟 𝐻𝑜𝑢𝑟𝑠 𝑜𝑓 𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛t

= £54,202 =38.72 per labour hour

1 400 hours

Answer to (b)

Special Product Soft Stool: Calculation of full job cost and product cost for 10 units of Soft Stool.

£ £

Direct costs 85

Production overhead:

Assembly department (4 labour hours x £31.33) 125.32

Joinery department (6 labour hours x £38.72) 232.32

Total production overheads 357.64

Total production cost for one unit £442.64

Total production for 10 units (£442.64 x 10) £4,426.4

Working of Overhead Costs Allocations

Allocation of cost of indirect labour is 12:10:3 (= 25), on the basis of number of employees

(28 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦= 12 x £28,000=£13,440

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 10 x £28,000=£11,200

25

𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 3 x £28,000=£3,360

25

Note: Canteen would not be reimbursed for indirect material costs because they are not

manufacturing and do not use the £22,000 in raw - materials.

Allocation of cost of indirect materials is 17:8(= 25), in proportion to direct materials

2 100 hours

𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 = 𝑇𝑜𝑡𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡

𝐷𝑖𝑟𝑒𝑐𝑡 𝐿𝑎𝑏𝑜𝑢𝑟 𝐻𝑜𝑢𝑟𝑠 𝑜𝑓 𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛t

= £54,202 =38.72 per labour hour

1 400 hours

Answer to (b)

Special Product Soft Stool: Calculation of full job cost and product cost for 10 units of Soft Stool.

£ £

Direct costs 85

Production overhead:

Assembly department (4 labour hours x £31.33) 125.32

Joinery department (6 labour hours x £38.72) 232.32

Total production overheads 357.64

Total production cost for one unit £442.64

Total production for 10 units (£442.64 x 10) £4,426.4

Working of Overhead Costs Allocations

Allocation of cost of indirect labour is 12:10:3 (= 25), on the basis of number of employees

(28 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦= 12 x £28,000=£13,440

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 10 x £28,000=£11,200

25

𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 3 x £28,000=£3,360

25

Note: Canteen would not be reimbursed for indirect material costs because they are not

manufacturing and do not use the £22,000 in raw - materials.

Allocation of cost of indirect materials is 17:8(= 25), in proportion to direct materials

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

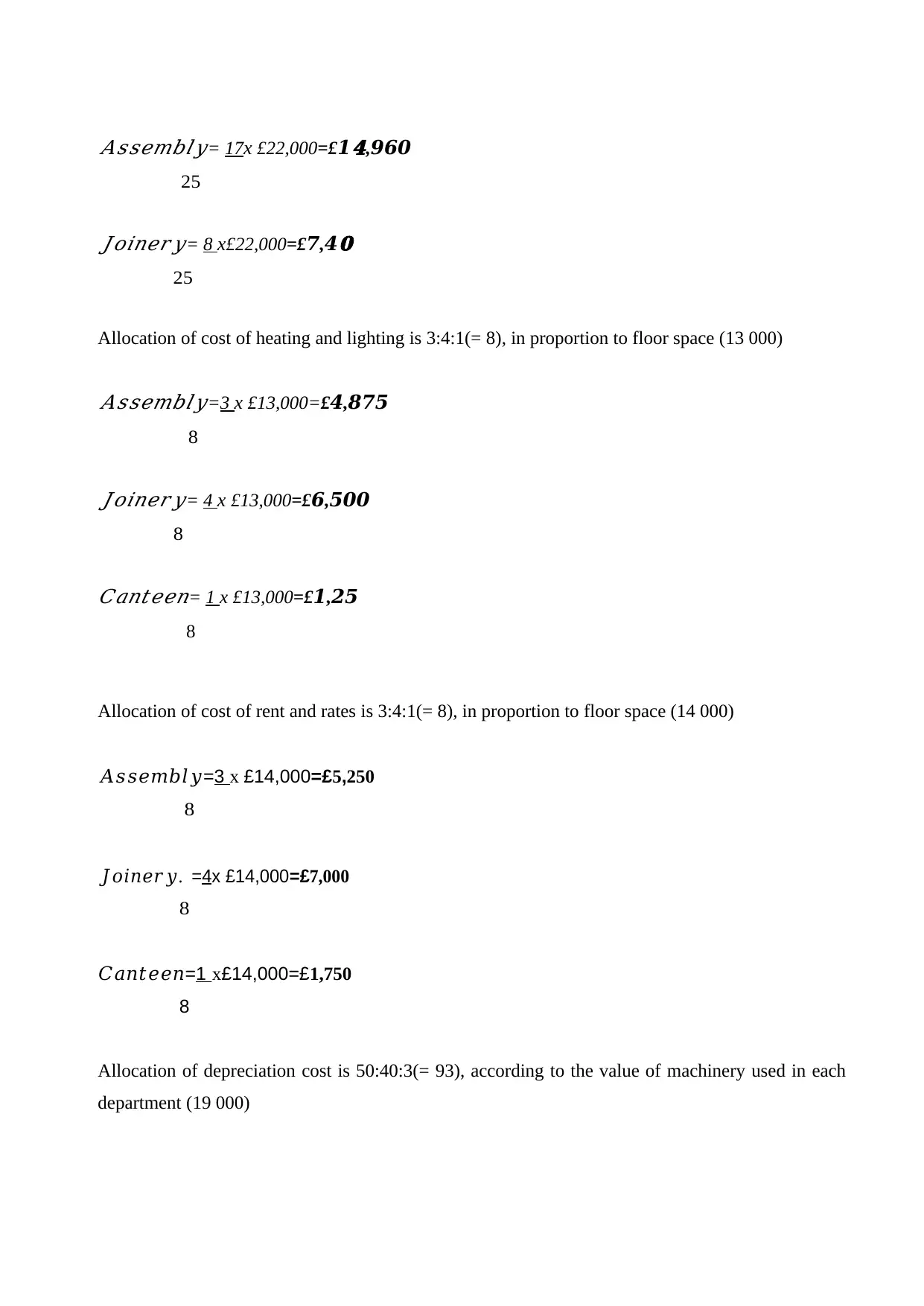

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦= 17x £22,000=£1

𝟒,960

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 8 x£22,000=£7,4

𝟎

25

Allocation of cost of heating and lighting is 3:4:1(= 8), in proportion to floor space (13 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=3 x £13,000=£4,875

8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 4 x £13,000=£6,500

8𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 1 x £13,000=£1,25

8

Allocation of cost of rent and rates is 3:4:1(= 8), in proportion to floor space (14 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=3 x £14,000=£5,250

8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦. =4x £14,000=£7,000

8

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=1 x£14,000=£1,750

8

Allocation of depreciation cost is 50:40:3(= 93), according to the value of machinery used in each

department (19 000)

𝟒,960

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 8 x£22,000=£7,4

𝟎

25

Allocation of cost of heating and lighting is 3:4:1(= 8), in proportion to floor space (13 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=3 x £13,000=£4,875

8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 4 x £13,000=£6,500

8𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 1 x £13,000=£1,25

8

Allocation of cost of rent and rates is 3:4:1(= 8), in proportion to floor space (14 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=3 x £14,000=£5,250

8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦. =4x £14,000=£7,000

8

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=1 x£14,000=£1,750

8

Allocation of depreciation cost is 50:40:3(= 93), according to the value of machinery used in each

department (19 000)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

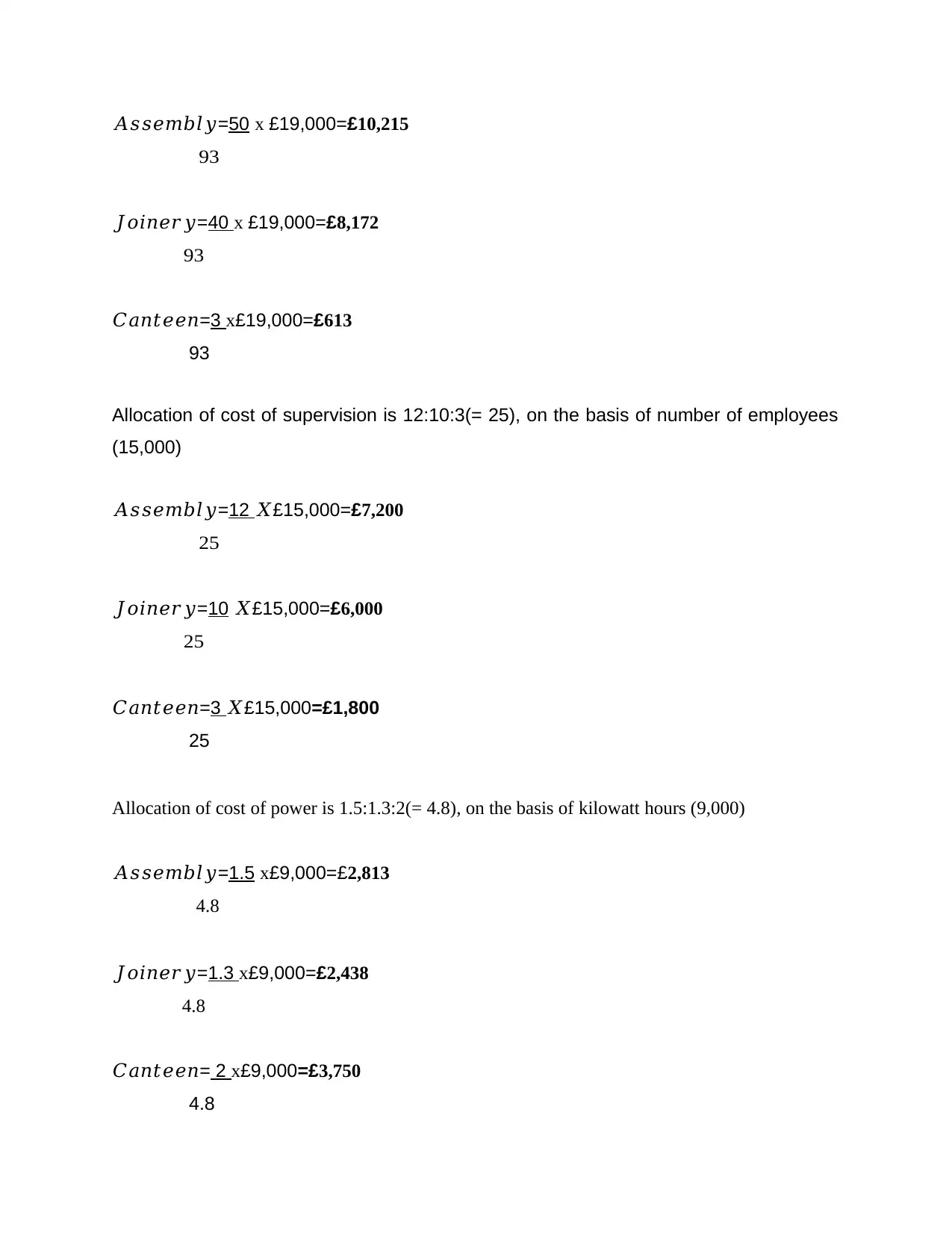

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=50 x £19,000=£10,215

93

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=40 x £19,000=£8,172

93

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=3 x£19,000=£613

93

Allocation of cost of supervision is 12:10:3(= 25), on the basis of number of employees

(15,000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=12 𝑋£15,000=£7,200

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=10 𝑋£15,000=£6,000

25

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=3 𝑋£15,000=£1,800

25

Allocation of cost of power is 1.5:1.3:2(= 4.8), on the basis of kilowatt hours (9,000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=1.5 x£9,000=£2,813

4.8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=1.3 x£9,000=£2,438

4.8

𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 2 x£9,000=£3,750

4.8

93

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=40 x £19,000=£8,172

93

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=3 x£19,000=£613

93

Allocation of cost of supervision is 12:10:3(= 25), on the basis of number of employees

(15,000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=12 𝑋£15,000=£7,200

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=10 𝑋£15,000=£6,000

25

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=3 𝑋£15,000=£1,800

25

Allocation of cost of power is 1.5:1.3:2(= 4.8), on the basis of kilowatt hours (9,000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=1.5 x£9,000=£2,813

4.8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=1.3 x£9,000=£2,438

4.8

𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 2 x£9,000=£3,750

4.8

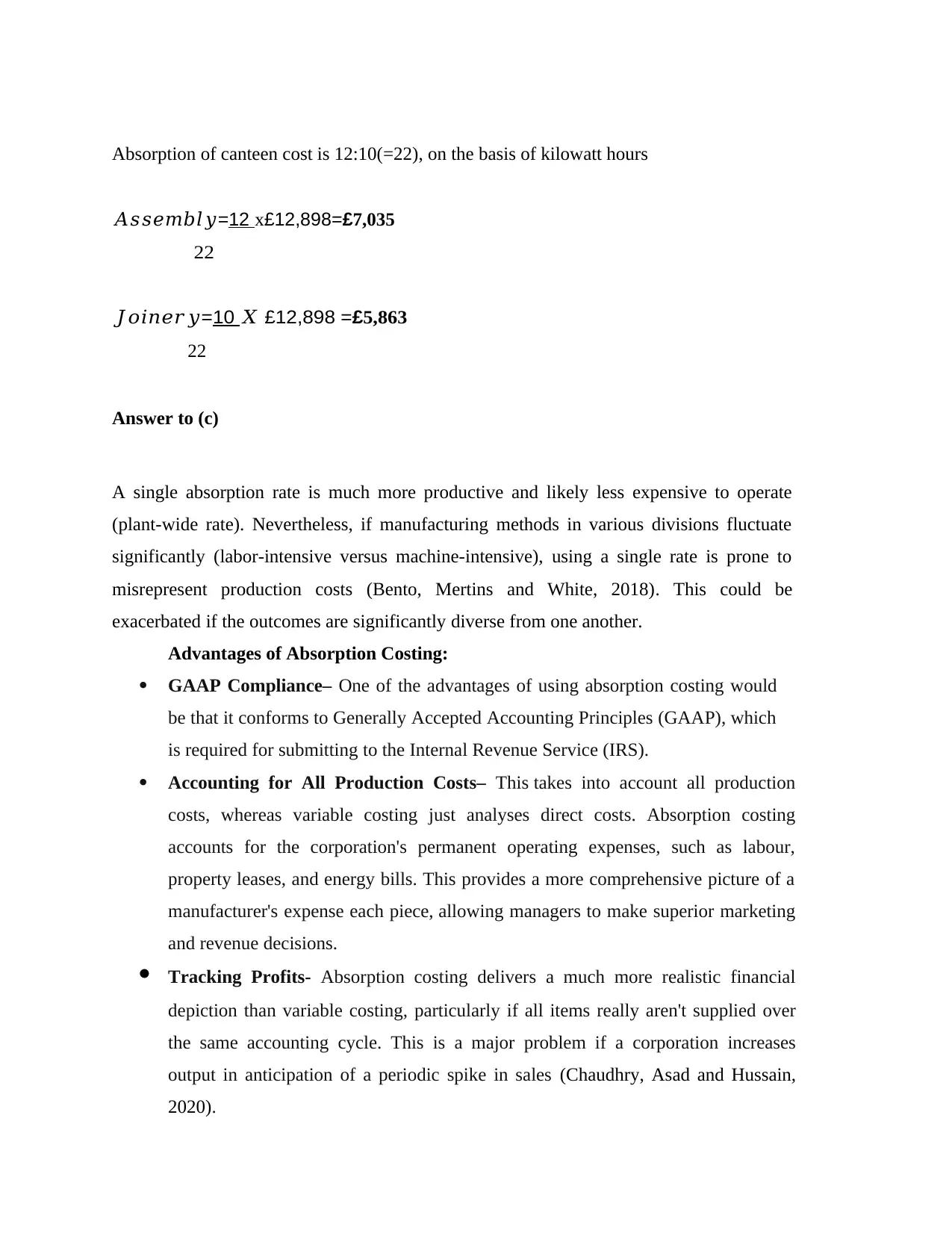

Absorption of canteen cost is 12:10(=22), on the basis of kilowatt hours

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=12 x£12,898=£7,035

22

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=10 𝑋 £12,898 =£5,863

22

Answer to (c)

A single absorption rate is much more productive and likely less expensive to operate

(plant-wide rate). Nevertheless, if manufacturing methods in various divisions fluctuate

significantly (labor-intensive versus machine-intensive), using a single rate is prone to

misrepresent production costs (Bento, Mertins and White, 2018). This could be

exacerbated if the outcomes are significantly diverse from one another.

Advantages of Absorption Costing:

GAAP Compliance– One of the advantages of using absorption costing would

be that it conforms to Generally Accepted Accounting Principles (GAAP), which

is required for submitting to the Internal Revenue Service (IRS).

Accounting for All Production Costs– This takes into account all production

costs, whereas variable costing just analyses direct costs. Absorption costing

accounts for the corporation's permanent operating expenses, such as labour,

property leases, and energy bills. This provides a more comprehensive picture of a

manufacturer's expense each piece, allowing managers to make superior marketing

and revenue decisions.

Tracking Profits- Absorption costing delivers a much more realistic financial

depiction than variable costing, particularly if all items really aren't supplied over

the same accounting cycle. This is a major problem if a corporation increases

output in anticipation of a periodic spike in sales (Chaudhry, Asad and Hussain,

2020).

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=12 x£12,898=£7,035

22

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=10 𝑋 £12,898 =£5,863

22

Answer to (c)

A single absorption rate is much more productive and likely less expensive to operate

(plant-wide rate). Nevertheless, if manufacturing methods in various divisions fluctuate

significantly (labor-intensive versus machine-intensive), using a single rate is prone to

misrepresent production costs (Bento, Mertins and White, 2018). This could be

exacerbated if the outcomes are significantly diverse from one another.

Advantages of Absorption Costing:

GAAP Compliance– One of the advantages of using absorption costing would

be that it conforms to Generally Accepted Accounting Principles (GAAP), which

is required for submitting to the Internal Revenue Service (IRS).

Accounting for All Production Costs– This takes into account all production

costs, whereas variable costing just analyses direct costs. Absorption costing

accounts for the corporation's permanent operating expenses, such as labour,

property leases, and energy bills. This provides a more comprehensive picture of a

manufacturer's expense each piece, allowing managers to make superior marketing

and revenue decisions.

Tracking Profits- Absorption costing delivers a much more realistic financial

depiction than variable costing, particularly if all items really aren't supplied over

the same accounting cycle. This is a major problem if a corporation increases

output in anticipation of a periodic spike in sales (Chaudhry, Asad and Hussain,

2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.