UGB 163 - Introduction to Accounting and Finance Assignment Analysis

VerifiedAdded on 2023/01/10

|14

|3931

|79

Homework Assignment

AI Summary

This assignment solution for UGB 163, Introduction to Accounting and Finance, addresses a series of financial and accounting problems. Part A focuses on the creation of an income statement and balance sheet for Racca Limited, providing insights into the company's financial performance and position. Part B delves into management accounting, calculating contribution, breakeven points, and margin of safety for Stockstone Ltd, alongside a strategic analysis of marketing expenditure. Part C explores investment appraisal techniques, including payback period, accounting rate of return, and net present value, to evaluate a machine purchase for Rockham Plc. The solution also discusses the merits and limitations of these techniques and the role of budgeting in strategic planning, providing a comprehensive overview of key accounting and finance concepts.

Introduction to Accounting and

Finance

1

Finance

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

1. Income statement of Racca Limited.....................................................................................3

2. Financial statement of Racca Limited..................................................................................3

PART B...........................................................................................................................................3

A) Calculation of contribution...............................................................................................3

B) Calculation of breakeven point and margin of safety if each electric kettle is sold for

£13 3

C) Calculation of the profit Stockstone Ltd. makes if it produces and sells 48,000 electric

kettles at £13 per kettle................................................................................................................3

D) Best strategy for Stockstone Ltd.......................................................................................3

E) Explanation of the underpinning assumptions attached to the break-even model

including analysing whether the model can successfully be utilised by a range of differing

businesses....................................................................................................................................3

PART C...........................................................................................................................................3

1. Calculation of the Payback Period, the Accounting Rate of Return, and the Net Present

Value of the machine, and provides recommendations as to whether Rockham Plc should buy

the machine..................................................................................................................................3

2. Explanation of the key merits and limitations of the differing investment appraisal

techniques....................................................................................................................................3

3. Explanation of advantages and disadvantages of using budget as tool of strategic planning

3

CONCLUSION................................................................................................................................3

REFRENCES...................................................................................................................................3

INTRODUCTION

2

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

1. Income statement of Racca Limited.....................................................................................3

2. Financial statement of Racca Limited..................................................................................3

PART B...........................................................................................................................................3

A) Calculation of contribution...............................................................................................3

B) Calculation of breakeven point and margin of safety if each electric kettle is sold for

£13 3

C) Calculation of the profit Stockstone Ltd. makes if it produces and sells 48,000 electric

kettles at £13 per kettle................................................................................................................3

D) Best strategy for Stockstone Ltd.......................................................................................3

E) Explanation of the underpinning assumptions attached to the break-even model

including analysing whether the model can successfully be utilised by a range of differing

businesses....................................................................................................................................3

PART C...........................................................................................................................................3

1. Calculation of the Payback Period, the Accounting Rate of Return, and the Net Present

Value of the machine, and provides recommendations as to whether Rockham Plc should buy

the machine..................................................................................................................................3

2. Explanation of the key merits and limitations of the differing investment appraisal

techniques....................................................................................................................................3

3. Explanation of advantages and disadvantages of using budget as tool of strategic planning

3

CONCLUSION................................................................................................................................3

REFRENCES...................................................................................................................................3

INTRODUCTION

2

INTRODUCTION

Account and finance theses two are part of business organization. Without theses mangers not

able to run business operation in effective way. This report is formulated to define importance of

financial and accounts by solving numerical case study. In includes the preparation of financial

report through which help in identifying the importance of systematic recording of transaction. In

the second part usefulness of BEP business organization decision making is define in effective

way. This report also includes the importance of budget as a tool of strategic planning.

PART A

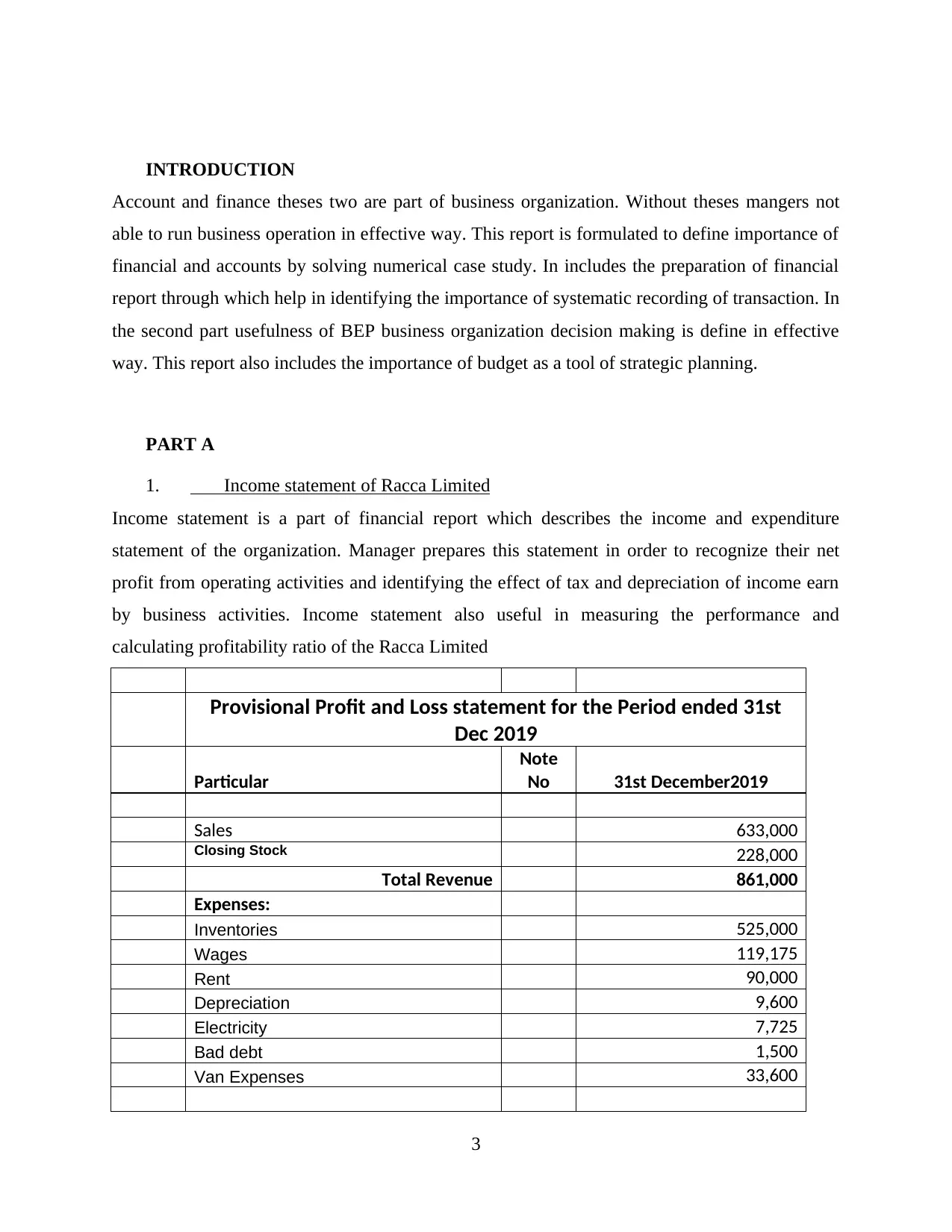

1. Income statement of Racca Limited

Income statement is a part of financial report which describes the income and expenditure

statement of the organization. Manager prepares this statement in order to recognize their net

profit from operating activities and identifying the effect of tax and depreciation of income earn

by business activities. Income statement also useful in measuring the performance and

calculating profitability ratio of the Racca Limited

Provisional Profit and Loss statement for the Period ended 31st

Dec 2019

Particular

Note

No 31st December2019

Sales 633,000

Closing Stock 228,000

Total Revenue 861,000

Expenses:

Inventories 525,000

Wages 119,175

Rent 90,000

Depreciation 9,600

Electricity 7,725

Bad debt 1,500

Van Expenses 33,600

3

Account and finance theses two are part of business organization. Without theses mangers not

able to run business operation in effective way. This report is formulated to define importance of

financial and accounts by solving numerical case study. In includes the preparation of financial

report through which help in identifying the importance of systematic recording of transaction. In

the second part usefulness of BEP business organization decision making is define in effective

way. This report also includes the importance of budget as a tool of strategic planning.

PART A

1. Income statement of Racca Limited

Income statement is a part of financial report which describes the income and expenditure

statement of the organization. Manager prepares this statement in order to recognize their net

profit from operating activities and identifying the effect of tax and depreciation of income earn

by business activities. Income statement also useful in measuring the performance and

calculating profitability ratio of the Racca Limited

Provisional Profit and Loss statement for the Period ended 31st

Dec 2019

Particular

Note

No 31st December2019

Sales 633,000

Closing Stock 228,000

Total Revenue 861,000

Expenses:

Inventories 525,000

Wages 119,175

Rent 90,000

Depreciation 9,600

Electricity 7,725

Bad debt 1,500

Van Expenses 33,600

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Expenses 786,600

Profit before tax (III - IV) 74,400

Tax expense: 5,775.00

Profit for the year (V - VI) 68,625

2. Financial statement of Racca Limited

Balance Sheet as at 31st December 2019

Note

No 31st December2019

I. EQUITY AND LIABILITIES

(1) Shareholders' Funds

(a) Share Capital 180,000

(b) Reserves and Surplus 68,625

(2) Non-Current Liabilities

(a) Long-term borrowings 0

(3) Current Liabilities

(a) Short-term borrowings 0

(b) Trade payables 393,000

(c) Other current liabilities 0

(d) Short Term Provision 0

Total 641,625

II. ASSETS

(1) Non-current assets

(a) Fixed assets

(i) Tangible assets 50,400

(ii) Capital Work - in - Progress

(b) Deferred tax Assets (Net)

(c) Long-term loans and advances

(d) Other non-current assets

(2) Current assets

(a) Inventories 228,000

(b) Trade receivables 436,500

(c) Cash and Bank Balance 90,000

4

Profit before tax (III - IV) 74,400

Tax expense: 5,775.00

Profit for the year (V - VI) 68,625

2. Financial statement of Racca Limited

Balance Sheet as at 31st December 2019

Note

No 31st December2019

I. EQUITY AND LIABILITIES

(1) Shareholders' Funds

(a) Share Capital 180,000

(b) Reserves and Surplus 68,625

(2) Non-Current Liabilities

(a) Long-term borrowings 0

(3) Current Liabilities

(a) Short-term borrowings 0

(b) Trade payables 393,000

(c) Other current liabilities 0

(d) Short Term Provision 0

Total 641,625

II. ASSETS

(1) Non-current assets

(a) Fixed assets

(i) Tangible assets 50,400

(ii) Capital Work - in - Progress

(b) Deferred tax Assets (Net)

(c) Long-term loans and advances

(d) Other non-current assets

(2) Current assets

(a) Inventories 228,000

(b) Trade receivables 436,500

(c) Cash and Bank Balance 90,000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

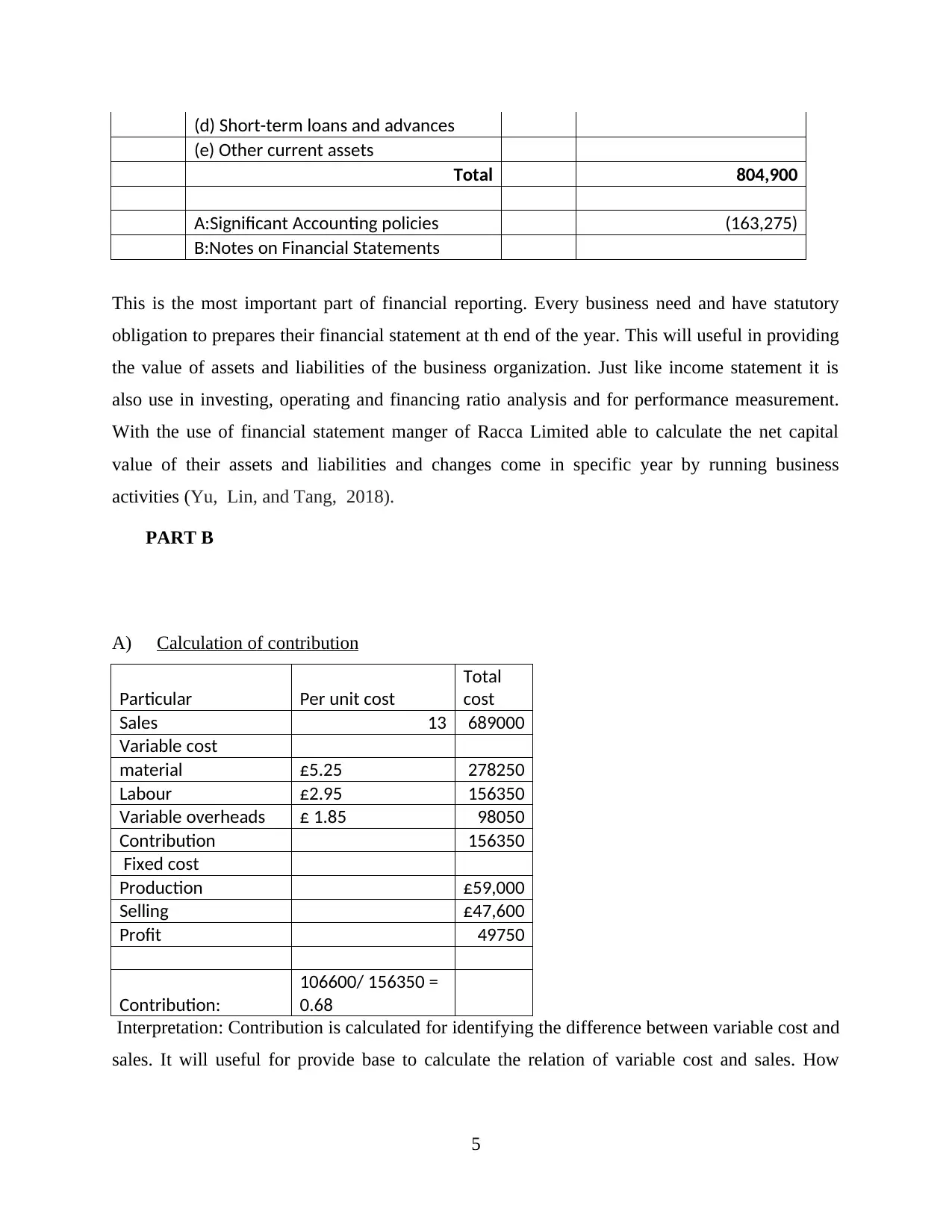

(d) Short-term loans and advances

(e) Other current assets

Total 804,900

163,275.00

A:Significant Accounting policies (163,275)

B:Notes on Financial Statements

This is the most important part of financial reporting. Every business need and have statutory

obligation to prepares their financial statement at th end of the year. This will useful in providing

the value of assets and liabilities of the business organization. Just like income statement it is

also use in investing, operating and financing ratio analysis and for performance measurement.

With the use of financial statement manger of Racca Limited able to calculate the net capital

value of their assets and liabilities and changes come in specific year by running business

activities (Yu, Lin, and Tang, 2018).

PART B

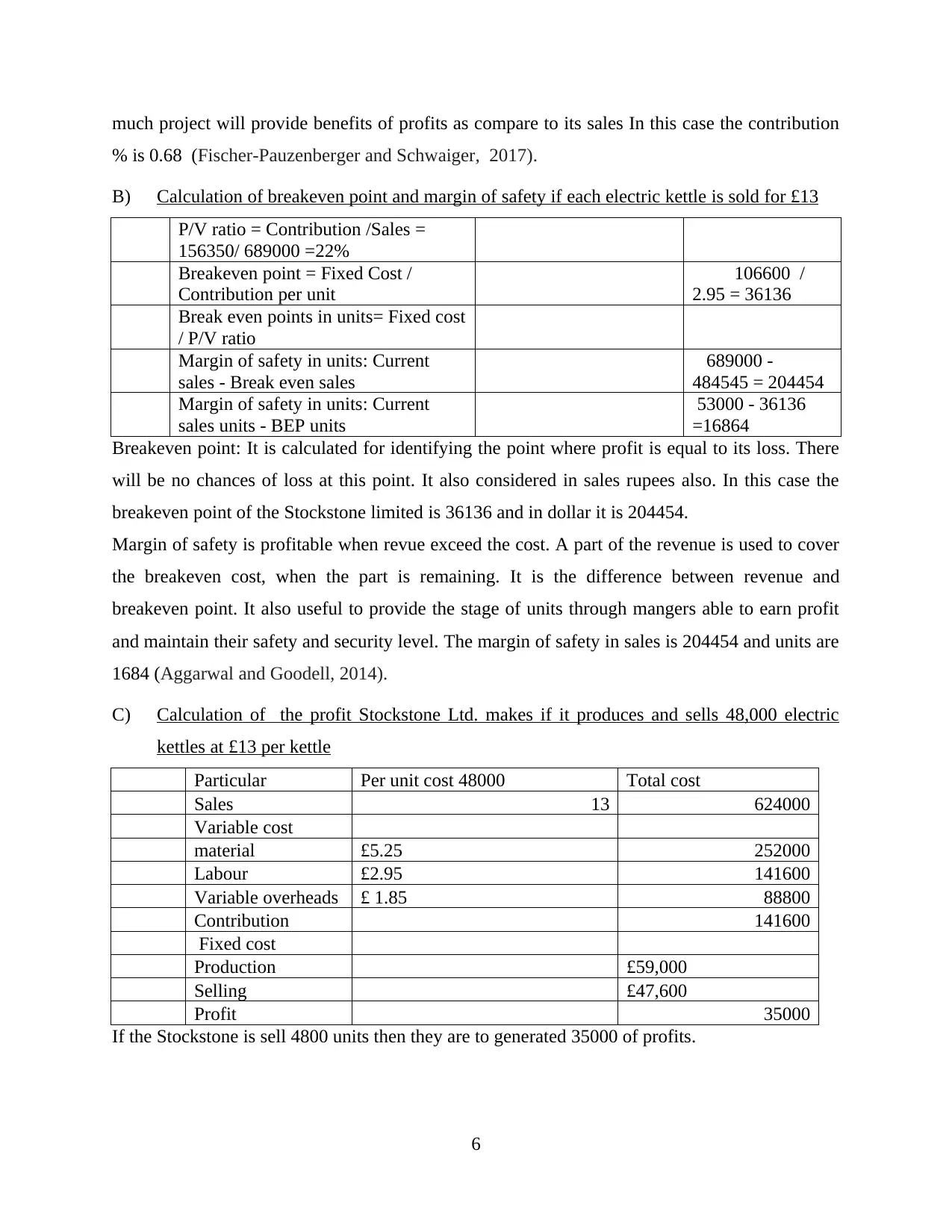

A) Calculation of contribution

Particular Per unit cost

Total

cost

Sales 13 689000

Variable cost

material £5.25 278250

Labour £2.95 156350

Variable overheads £ 1.85 98050

Contribution 156350

Fixed cost

Production £59,000

Selling £47,600

Profit 49750

Contribution:

106600/ 156350 =

0.68

Interpretation: Contribution is calculated for identifying the difference between variable cost and

sales. It will useful for provide base to calculate the relation of variable cost and sales. How

5

(e) Other current assets

Total 804,900

163,275.00

A:Significant Accounting policies (163,275)

B:Notes on Financial Statements

This is the most important part of financial reporting. Every business need and have statutory

obligation to prepares their financial statement at th end of the year. This will useful in providing

the value of assets and liabilities of the business organization. Just like income statement it is

also use in investing, operating and financing ratio analysis and for performance measurement.

With the use of financial statement manger of Racca Limited able to calculate the net capital

value of their assets and liabilities and changes come in specific year by running business

activities (Yu, Lin, and Tang, 2018).

PART B

A) Calculation of contribution

Particular Per unit cost

Total

cost

Sales 13 689000

Variable cost

material £5.25 278250

Labour £2.95 156350

Variable overheads £ 1.85 98050

Contribution 156350

Fixed cost

Production £59,000

Selling £47,600

Profit 49750

Contribution:

106600/ 156350 =

0.68

Interpretation: Contribution is calculated for identifying the difference between variable cost and

sales. It will useful for provide base to calculate the relation of variable cost and sales. How

5

much project will provide benefits of profits as compare to its sales In this case the contribution

% is 0.68 (Fischer-Pauzenberger and Schwaiger, 2017).

B) Calculation of breakeven point and margin of safety if each electric kettle is sold for £13

P/V ratio = Contribution /Sales =

156350/ 689000 =22%

Breakeven point = Fixed Cost /

Contribution per unit

106600 /

2.95 = 36136

Break even points in units= Fixed cost

/ P/V ratio

Margin of safety in units: Current

sales - Break even sales

689000 -

484545 = 204454

Margin of safety in units: Current

sales units - BEP units

53000 - 36136

=16864

Breakeven point: It is calculated for identifying the point where profit is equal to its loss. There

will be no chances of loss at this point. It also considered in sales rupees also. In this case the

breakeven point of the Stockstone limited is 36136 and in dollar it is 204454.

Margin of safety is profitable when revue exceed the cost. A part of the revenue is used to cover

the breakeven cost, when the part is remaining. It is the difference between revenue and

breakeven point. It also useful to provide the stage of units through mangers able to earn profit

and maintain their safety and security level. The margin of safety in sales is 204454 and units are

1684 (Aggarwal and Goodell, 2014).

C) Calculation of the profit Stockstone Ltd. makes if it produces and sells 48,000 electric

kettles at £13 per kettle

Particular Per unit cost 48000 Total cost

Sales 13 624000

Variable cost

material £5.25 252000

Labour £2.95 141600

Variable overheads £ 1.85 88800

Contribution 141600

Fixed cost

Production £59,000

Selling £47,600

Profit 35000

If the Stockstone is sell 4800 units then they are to generated 35000 of profits.

6

% is 0.68 (Fischer-Pauzenberger and Schwaiger, 2017).

B) Calculation of breakeven point and margin of safety if each electric kettle is sold for £13

P/V ratio = Contribution /Sales =

156350/ 689000 =22%

Breakeven point = Fixed Cost /

Contribution per unit

106600 /

2.95 = 36136

Break even points in units= Fixed cost

/ P/V ratio

Margin of safety in units: Current

sales - Break even sales

689000 -

484545 = 204454

Margin of safety in units: Current

sales units - BEP units

53000 - 36136

=16864

Breakeven point: It is calculated for identifying the point where profit is equal to its loss. There

will be no chances of loss at this point. It also considered in sales rupees also. In this case the

breakeven point of the Stockstone limited is 36136 and in dollar it is 204454.

Margin of safety is profitable when revue exceed the cost. A part of the revenue is used to cover

the breakeven cost, when the part is remaining. It is the difference between revenue and

breakeven point. It also useful to provide the stage of units through mangers able to earn profit

and maintain their safety and security level. The margin of safety in sales is 204454 and units are

1684 (Aggarwal and Goodell, 2014).

C) Calculation of the profit Stockstone Ltd. makes if it produces and sells 48,000 electric

kettles at £13 per kettle

Particular Per unit cost 48000 Total cost

Sales 13 624000

Variable cost

material £5.25 252000

Labour £2.95 141600

Variable overheads £ 1.85 88800

Contribution 141600

Fixed cost

Production £59,000

Selling £47,600

Profit 35000

If the Stockstone is sell 4800 units then they are to generated 35000 of profits.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

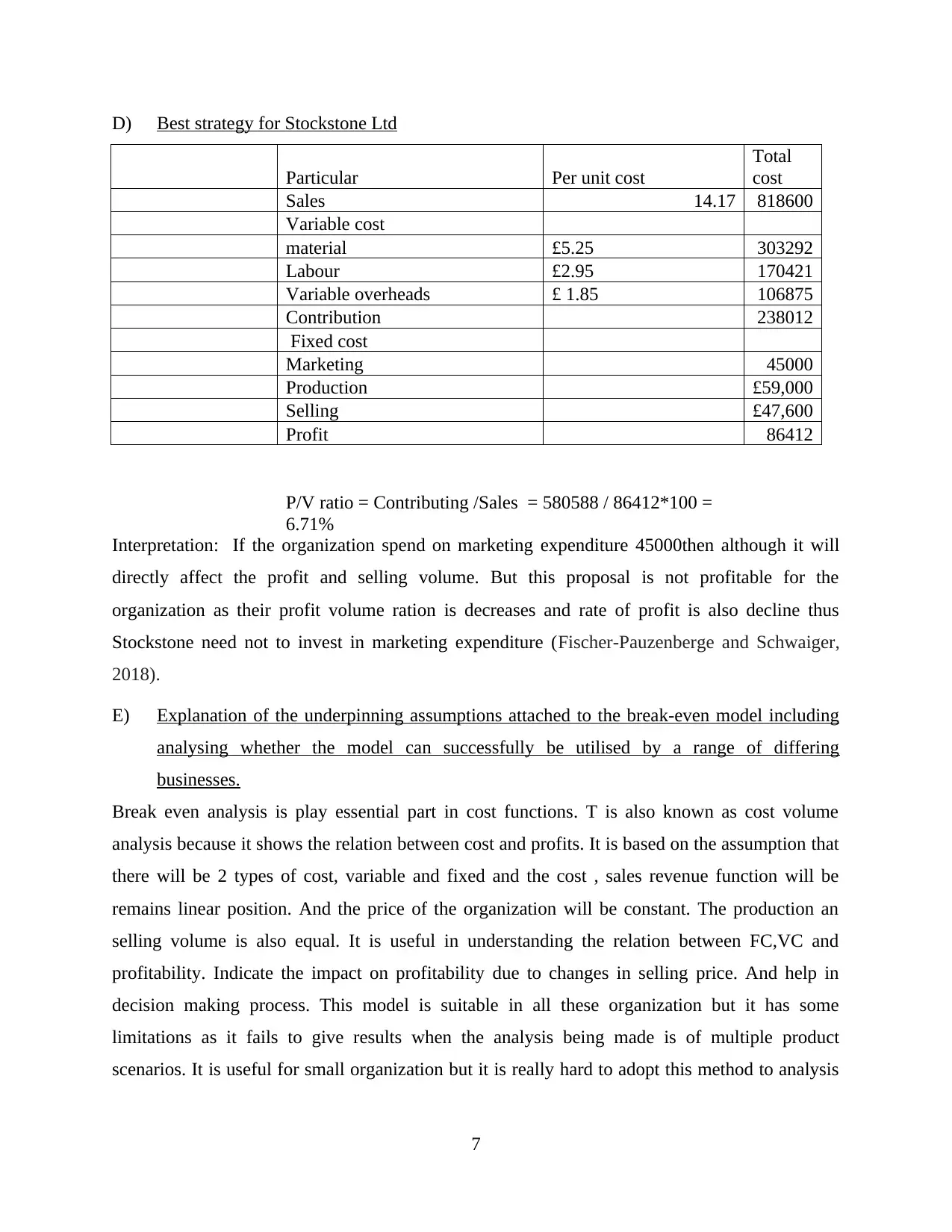

D) Best strategy for Stockstone Ltd

Particular Per unit cost

Total

cost

Sales 14.17 818600

Variable cost

material £5.25 303292

Labour £2.95 170421

Variable overheads £ 1.85 106875

Contribution 238012

Fixed cost

Marketing 45000

Production £59,000

Selling £47,600

Profit 86412

P/V ratio = Contributing /Sales = 580588 / 86412*100 =

6.71%

Interpretation: If the organization spend on marketing expenditure 45000then although it will

directly affect the profit and selling volume. But this proposal is not profitable for the

organization as their profit volume ration is decreases and rate of profit is also decline thus

Stockstone need not to invest in marketing expenditure (Fischer-Pauzenberge and Schwaiger,

2018).

E) Explanation of the underpinning assumptions attached to the break-even model including

analysing whether the model can successfully be utilised by a range of differing

businesses.

Break even analysis is play essential part in cost functions. T is also known as cost volume

analysis because it shows the relation between cost and profits. It is based on the assumption that

there will be 2 types of cost, variable and fixed and the cost , sales revenue function will be

remains linear position. And the price of the organization will be constant. The production an

selling volume is also equal. It is useful in understanding the relation between FC,VC and

profitability. Indicate the impact on profitability due to changes in selling price. And help in

decision making process. This model is suitable in all these organization but it has some

limitations as it fails to give results when the analysis being made is of multiple product

scenarios. It is useful for small organization but it is really hard to adopt this method to analysis

7

Particular Per unit cost

Total

cost

Sales 14.17 818600

Variable cost

material £5.25 303292

Labour £2.95 170421

Variable overheads £ 1.85 106875

Contribution 238012

Fixed cost

Marketing 45000

Production £59,000

Selling £47,600

Profit 86412

P/V ratio = Contributing /Sales = 580588 / 86412*100 =

6.71%

Interpretation: If the organization spend on marketing expenditure 45000then although it will

directly affect the profit and selling volume. But this proposal is not profitable for the

organization as their profit volume ration is decreases and rate of profit is also decline thus

Stockstone need not to invest in marketing expenditure (Fischer-Pauzenberge and Schwaiger,

2018).

E) Explanation of the underpinning assumptions attached to the break-even model including

analysing whether the model can successfully be utilised by a range of differing

businesses.

Break even analysis is play essential part in cost functions. T is also known as cost volume

analysis because it shows the relation between cost and profits. It is based on the assumption that

there will be 2 types of cost, variable and fixed and the cost , sales revenue function will be

remains linear position. And the price of the organization will be constant. The production an

selling volume is also equal. It is useful in understanding the relation between FC,VC and

profitability. Indicate the impact on profitability due to changes in selling price. And help in

decision making process. This model is suitable in all these organization but it has some

limitations as it fails to give results when the analysis being made is of multiple product

scenarios. It is useful for small organization but it is really hard to adopt this method to analysis

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the relation at large scale organization as they have different department which deal in unique

products and services (Stent, Bradbury and Hooks, 2017).

PART C

1. Calculation of the Payback Period, the Accounting Rate of Return, and the Net Present

Pay back period

Year Particular Depreciation

Cash

outflow

Net cash

inflow

Depreciation

Add

Cash

inflow

C

I

1 17000000 7000000 6400000 3600000 7000000 4300000

2 17000000 7000000 6400000 3600000 7000000 4300000

3 17000000 7000000 6400000 3600000 7000000 4300000

4 17000000 7000000 6400000 3600000 7000000 4300000

5 17000000 7000000 6400000 3600000 7000000 4300000

Pay back period when even cash inflows

Initial outlay of the project / Annual Cash inflow 35000000/4300000 = 8.13 years

ARR = Average Annual Profit after tax/ Average initial investment*100

Average investment: Initial investment - Salvage Value/2 = 4000000-500000/2 = 17500000

Average profit = 3600000

ARR 17500000/3600000 = 4.86

Year

Cash

inflow

Discounted factor

7 %

Present

value

1 10600000 0.588 6232800

2 10600000 0.346 3667600

3 10600000 0.203 2151800

4 10600000 0.119 1261400

5 10600000 0.07 742000

6 5000000 0.041 205000

14260600

Net present value = Initial investment – Total present value of cash inflow = 20739400

2. Value of the machine, and provides recommendations as to whether Rockham Plc

should buy the machine.

From the calculation of the investment appraisal techniques, it has been analyse that buying

chine for Rockham Plc is better option as according to the concept of the payback period, an

8

products and services (Stent, Bradbury and Hooks, 2017).

PART C

1. Calculation of the Payback Period, the Accounting Rate of Return, and the Net Present

Pay back period

Year Particular Depreciation

Cash

outflow

Net cash

inflow

Depreciation

Add

Cash

inflow

C

I

1 17000000 7000000 6400000 3600000 7000000 4300000

2 17000000 7000000 6400000 3600000 7000000 4300000

3 17000000 7000000 6400000 3600000 7000000 4300000

4 17000000 7000000 6400000 3600000 7000000 4300000

5 17000000 7000000 6400000 3600000 7000000 4300000

Pay back period when even cash inflows

Initial outlay of the project / Annual Cash inflow 35000000/4300000 = 8.13 years

ARR = Average Annual Profit after tax/ Average initial investment*100

Average investment: Initial investment - Salvage Value/2 = 4000000-500000/2 = 17500000

Average profit = 3600000

ARR 17500000/3600000 = 4.86

Year

Cash

inflow

Discounted factor

7 %

Present

value

1 10600000 0.588 6232800

2 10600000 0.346 3667600

3 10600000 0.203 2151800

4 10600000 0.119 1261400

5 10600000 0.07 742000

6 5000000 0.041 205000

14260600

Net present value = Initial investment – Total present value of cash inflow = 20739400

2. Value of the machine, and provides recommendations as to whether Rockham Plc

should buy the machine.

From the calculation of the investment appraisal techniques, it has been analyse that buying

chine for Rockham Plc is better option as according to the concept of the payback period, an

8

investment is considered to be best choice or accept for purchasing when the payback period is

lower and in this case the payback period required more than 8 years for cover up their initial

cost of capital. It requires long time which how the lower rate of profitability. On the other side

organization will be able to earn only 4 % average rate of return which is not a better return for

investment purpose. The value of net present value is lower then initial cost of investment and

the cash inflow is not higher their present value is either not higher thus organization only able to

accept the proposal when the net present value is higher as compare to their cash outflow. In this

case the net present value is not so high thus manager of Rockham need not to accept the

proposal or invest in purchasing of machine to expand their investment (Adler, and Stringer

2018).

3. Explanation of the key merits and limitations of the differing investment appraisal

techniques.

Investment appraisal techniques: It is a method used by business organizations to choose

the best proposal of investment by suing capital budgeting and finical techniques of

management. For business managers it is a way of fundamental analysis. It is mechanism of long

term preparation for creation and economic projected capital outlay.

Manager of Rockham Plc used investment appraisal techniques as these techniques helps

in defining risk and uncertainty, provide information regarding cash inflow and cash outflow and

help in taking the best decision for business organizations. There will be 2 types of investment

appraisal techniques has been used to analysis the best alternative for business organization.

Manager can se tradition method or discounted cash flow method for their capital budgeting.

Both methods have their own advantages and disadvantages. It depends on the size, skills of

personals they choose technique for taking decision of long term investments which they can ale

to earn future profits. Following are the techniques of investment appraisal

Payback period: It is the method investment appraisal which is the part of capital

budgeting method. Payback period is defining the time required by projects to fulfil their initial

cost. It can be define in different terms; it is the length of time period which is requires to cover

up the initial cost of project. There will be different rules and formula used by manger regarding

this technique when investment cash inflow are uneven. Following are the advantage and

disadvantages of this method

9

lower and in this case the payback period required more than 8 years for cover up their initial

cost of capital. It requires long time which how the lower rate of profitability. On the other side

organization will be able to earn only 4 % average rate of return which is not a better return for

investment purpose. The value of net present value is lower then initial cost of investment and

the cash inflow is not higher their present value is either not higher thus organization only able to

accept the proposal when the net present value is higher as compare to their cash outflow. In this

case the net present value is not so high thus manager of Rockham need not to accept the

proposal or invest in purchasing of machine to expand their investment (Adler, and Stringer

2018).

3. Explanation of the key merits and limitations of the differing investment appraisal

techniques.

Investment appraisal techniques: It is a method used by business organizations to choose

the best proposal of investment by suing capital budgeting and finical techniques of

management. For business managers it is a way of fundamental analysis. It is mechanism of long

term preparation for creation and economic projected capital outlay.

Manager of Rockham Plc used investment appraisal techniques as these techniques helps

in defining risk and uncertainty, provide information regarding cash inflow and cash outflow and

help in taking the best decision for business organizations. There will be 2 types of investment

appraisal techniques has been used to analysis the best alternative for business organization.

Manager can se tradition method or discounted cash flow method for their capital budgeting.

Both methods have their own advantages and disadvantages. It depends on the size, skills of

personals they choose technique for taking decision of long term investments which they can ale

to earn future profits. Following are the techniques of investment appraisal

Payback period: It is the method investment appraisal which is the part of capital

budgeting method. Payback period is defining the time required by projects to fulfil their initial

cost. It can be define in different terms; it is the length of time period which is requires to cover

up the initial cost of project. There will be different rules and formula used by manger regarding

this technique when investment cash inflow are uneven. Following are the advantage and

disadvantages of this method

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Easy to operate: It is the easiest and simple concept and application of the investment

appraisal. This method is useful for basically small business organizations which are not require

skills manpower for taking decision.

Liquidity indicator: It business entities suffers from any issue are related with the

liquidity then it is the best method to indication of liquidity (Hamilton, 2020).

Time: It is time consuming method as mangers will easily calculate the best alternative

and period time required to cover-up cost in short time period.

Disadvantage:

Ignore cash inflows: Under this method manger does not considers those cash inflow

which organization generate cover up the project initial cost.

Ignore salvage value: It also neglect timing of the occurrence of the cash flows .They

did not take salvage cost during calculation of the payback period.

Method of capital recovery: It is not perfect method of identifying profitability rather it

is the techniques of capital recovery.

Risk: This method is not reliable as it is too hard to find the accurate investment

information.

Accounting rate of return: It also known as average rate of return method. With the

uses of this method mangers able to recognise the average rate .

Advantage

Easy to calculate: It is one of the simplest methods as in this method accounting

information is used.

Consider entire cash flow: With the uses of accounting rate of return, mangers able to

use entire cash inflows during calculating of cost of investment.

Based on financial data: Chances of errors are less as compare to pay back period method

because this technique utilized financial data.

Disadvantage

Ignore time value: This method also not considers the value of time money. During

calculation of the average return

Problem of comparability: There are two ways of calculate the accounting rate of return

which cases a problem of comparability.

10

appraisal. This method is useful for basically small business organizations which are not require

skills manpower for taking decision.

Liquidity indicator: It business entities suffers from any issue are related with the

liquidity then it is the best method to indication of liquidity (Hamilton, 2020).

Time: It is time consuming method as mangers will easily calculate the best alternative

and period time required to cover-up cost in short time period.

Disadvantage:

Ignore cash inflows: Under this method manger does not considers those cash inflow

which organization generate cover up the project initial cost.

Ignore salvage value: It also neglect timing of the occurrence of the cash flows .They

did not take salvage cost during calculation of the payback period.

Method of capital recovery: It is not perfect method of identifying profitability rather it

is the techniques of capital recovery.

Risk: This method is not reliable as it is too hard to find the accurate investment

information.

Accounting rate of return: It also known as average rate of return method. With the

uses of this method mangers able to recognise the average rate .

Advantage

Easy to calculate: It is one of the simplest methods as in this method accounting

information is used.

Consider entire cash flow: With the uses of accounting rate of return, mangers able to

use entire cash inflows during calculating of cost of investment.

Based on financial data: Chances of errors are less as compare to pay back period method

because this technique utilized financial data.

Disadvantage

Ignore time value: This method also not considers the value of time money. During

calculation of the average return

Problem of comparability: There are two ways of calculate the accounting rate of return

which cases a problem of comparability.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Use only accounting figure: In this method on investee appraisal manger only

considered accounting data (Vann, 2016).

Net present value: This method of capital budgeting is considered in modern methods of

capital budgeting. In this technique time value is considered and present value are calculated.

Higher net present value shows future profitably of the proposals.

Advantages:

Considered time value: By applying this modern method s that it is considered time

value during calculation of the best investment proposals. It is considered time value which

means if 2 machines are equal but the net present value are different because of different pattern

of cash stream .

Sound method of appraisal: With the use of this technique manger able to recognize the

benefits from project business organization able to generate.

Maximization of shareholders worth: It is theoretically correct method of selection of

investment proposal. With the use of these methods manage able to take right decision regarding

their investment; it will help in increasing the worth of their shareholders.

Disadvantage

Hard to understand: The concept f the net present value method is very hard as it is

required higher skilled personals which have knowledge regarding every aspect of finance.

Accurate decision: This method is not provide accreted and reliable decision if

investments of mutually exclusive projects are not same.

Calculation: It is very hard to calcite the new present value of projects as, it considered,

deprecation and salvage values.

Internal rate of return: It is also known as second discounted cash flow and time

adjusting mechanism of capital investment. In this method the net pres value, the discounted rate

is required rate of return and being a predetermined rate. This method of investment appraisal is

based on the internal rate of return.

Advantage:

Recognize the value: This method is also useful because it considered the value of time.

Accurate result: It is most useful technique as it provides reliable result oriented to

investment of proposals (Benson, Faff and Smith, 2014).

Indicate profitability: It use internal rate of return which shoe the sign of profitability.

11

considered accounting data (Vann, 2016).

Net present value: This method of capital budgeting is considered in modern methods of

capital budgeting. In this technique time value is considered and present value are calculated.

Higher net present value shows future profitably of the proposals.

Advantages:

Considered time value: By applying this modern method s that it is considered time

value during calculation of the best investment proposals. It is considered time value which

means if 2 machines are equal but the net present value are different because of different pattern

of cash stream .

Sound method of appraisal: With the use of this technique manger able to recognize the

benefits from project business organization able to generate.

Maximization of shareholders worth: It is theoretically correct method of selection of

investment proposal. With the use of these methods manage able to take right decision regarding

their investment; it will help in increasing the worth of their shareholders.

Disadvantage

Hard to understand: The concept f the net present value method is very hard as it is

required higher skilled personals which have knowledge regarding every aspect of finance.

Accurate decision: This method is not provide accreted and reliable decision if

investments of mutually exclusive projects are not same.

Calculation: It is very hard to calcite the new present value of projects as, it considered,

deprecation and salvage values.

Internal rate of return: It is also known as second discounted cash flow and time

adjusting mechanism of capital investment. In this method the net pres value, the discounted rate

is required rate of return and being a predetermined rate. This method of investment appraisal is

based on the internal rate of return.

Advantage:

Recognize the value: This method is also useful because it considered the value of time.

Accurate result: It is most useful technique as it provides reliable result oriented to

investment of proposals (Benson, Faff and Smith, 2014).

Indicate profitability: It use internal rate of return which shoe the sign of profitability.

11

Disadvantage: Tedious calculation” It involves tedious calculation and generated

involves competitive computations.

Confusing in multiple rules: It is nit useful for small organizations it require skills

personals who has the knowledge of all principles regarding these technique.

Time: It required high time to identify the best alternative.

Every investment appraisal method has their own benefits and drawback and these apply

by mangers according to their suitability of the organization operations.

4. Explanation of advantages and disadvantages of using budget as tool of strategic

planning

Budget: It is a statement or format which is prepared by the managers of the organizations in

order to recognize the future position and future performance rate of the business. In other words

budget is a numerical statement which is used for identifying the value of profit and expenses in

specific time period. It is the most useful tool of management accounting. It is help in strategic

planning as it provides base for mangers through which they are able to formulate policies and

strategies for future business activities. Following are the advantages of the budget as tool of

strategic planning

Provide base for planning: Budget are the base for formulating planning. It provides data on the

basis of which manages formulated strategies.

Help in environment scanning: With the uses of budget statement managers able to identify

future risk and measure their strengths, weakness, and opportunities. It will also help in

determining the effect of political, legal and environment factors on organization with their data.

Provide information regarding resources: Financial budget help in determine the resource

required for running business activities in future. They also use manufacturing reports, operating,

purchase and sales budget to determine the requirement of other then human resource for the

organization.

Help in running organization activities: Budget help in allocation of resource in effective , it

also proved base and mangers distribute work and responsibilities on the basis of the budget it

will help in managing coordination among team members of the business entities.

12

involves competitive computations.

Confusing in multiple rules: It is nit useful for small organizations it require skills

personals who has the knowledge of all principles regarding these technique.

Time: It required high time to identify the best alternative.

Every investment appraisal method has their own benefits and drawback and these apply

by mangers according to their suitability of the organization operations.

4. Explanation of advantages and disadvantages of using budget as tool of strategic

planning

Budget: It is a statement or format which is prepared by the managers of the organizations in

order to recognize the future position and future performance rate of the business. In other words

budget is a numerical statement which is used for identifying the value of profit and expenses in

specific time period. It is the most useful tool of management accounting. It is help in strategic

planning as it provides base for mangers through which they are able to formulate policies and

strategies for future business activities. Following are the advantages of the budget as tool of

strategic planning

Provide base for planning: Budget are the base for formulating planning. It provides data on the

basis of which manages formulated strategies.

Help in environment scanning: With the uses of budget statement managers able to identify

future risk and measure their strengths, weakness, and opportunities. It will also help in

determining the effect of political, legal and environment factors on organization with their data.

Provide information regarding resources: Financial budget help in determine the resource

required for running business activities in future. They also use manufacturing reports, operating,

purchase and sales budget to determine the requirement of other then human resource for the

organization.

Help in running organization activities: Budget help in allocation of resource in effective , it

also proved base and mangers distribute work and responsibilities on the basis of the budget it

will help in managing coordination among team members of the business entities.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.