UGB222 Management Accounting: Financial Analysis and Decisions

VerifiedAdded on 2023/06/18

|10

|1204

|444

Homework Assignment

AI Summary

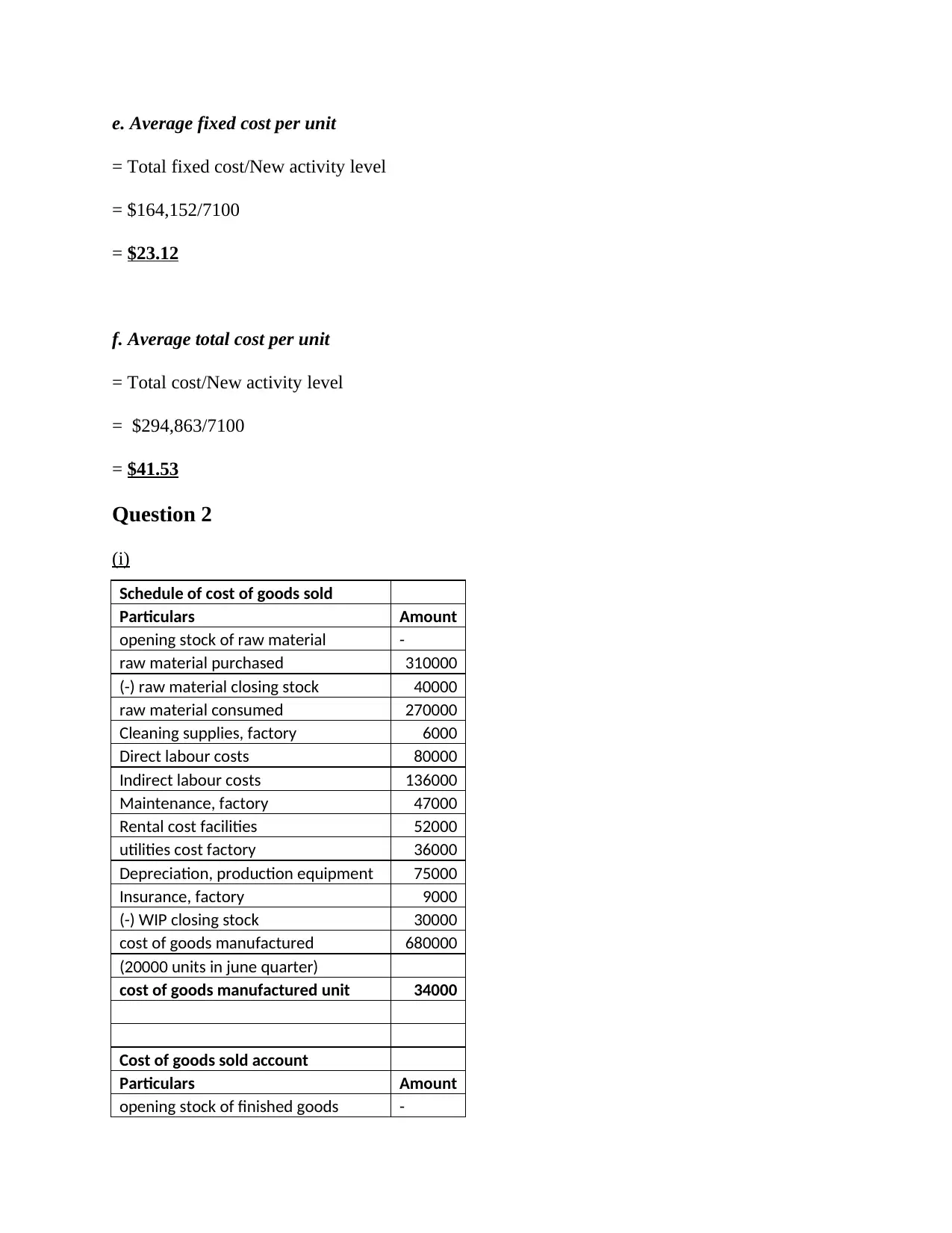

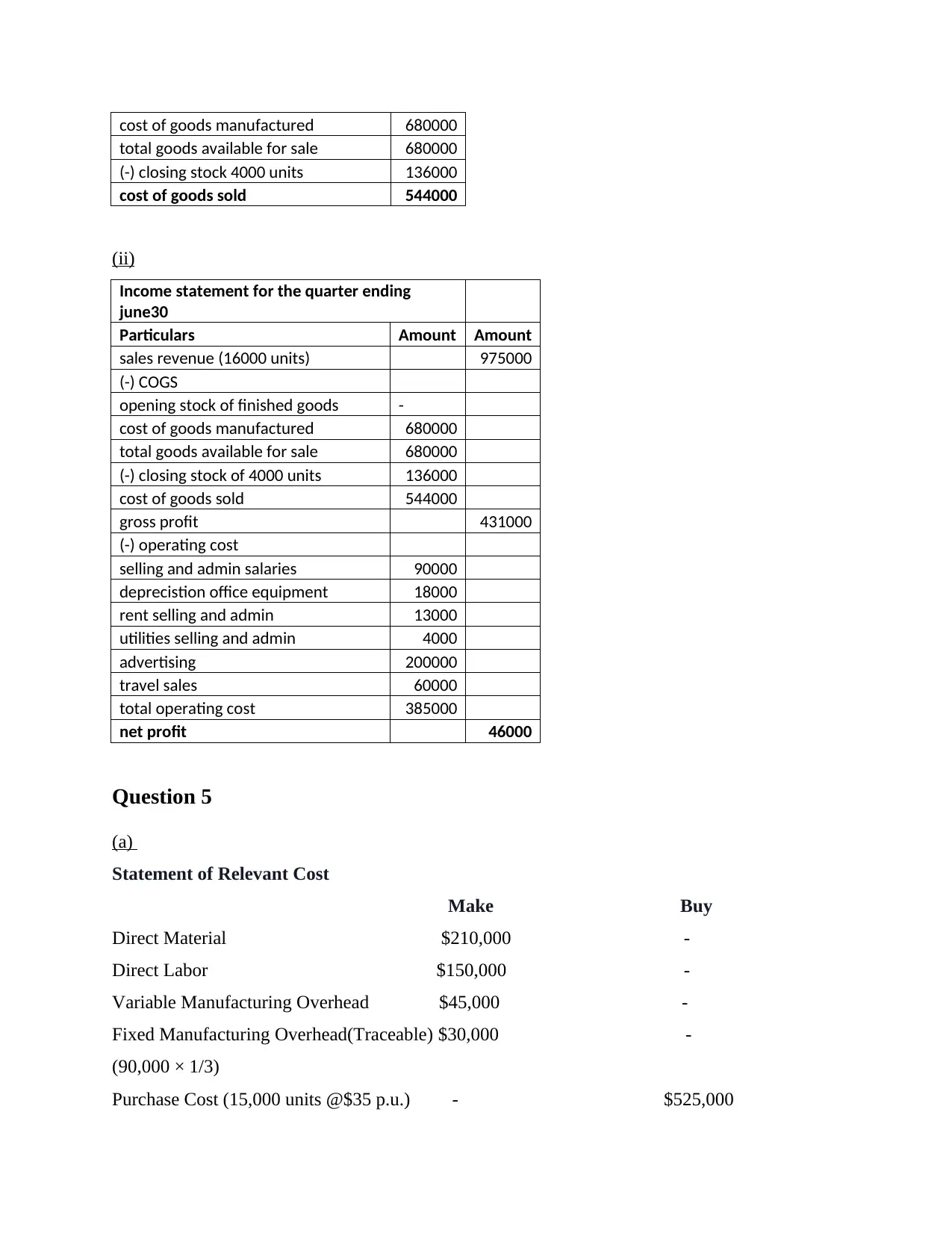

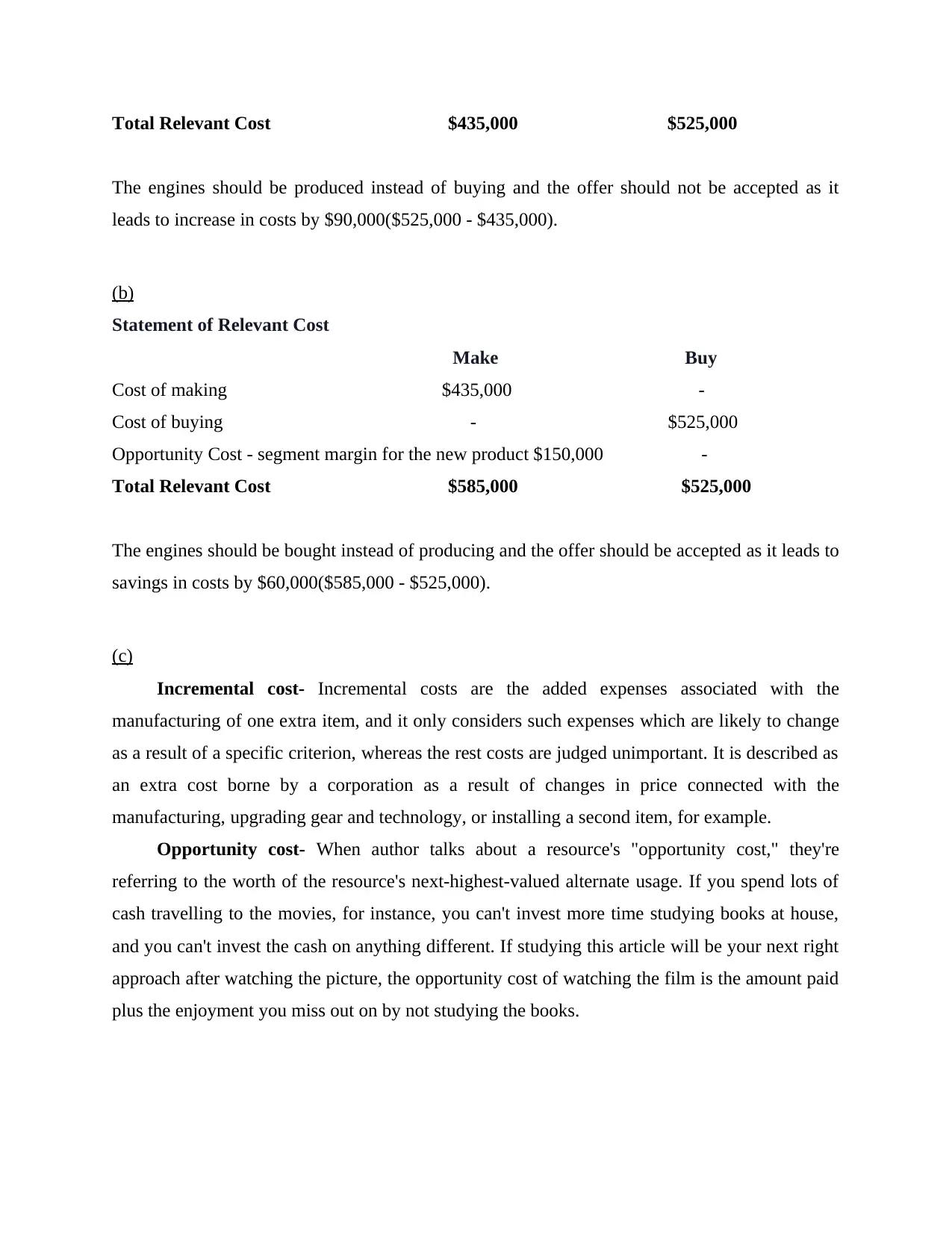

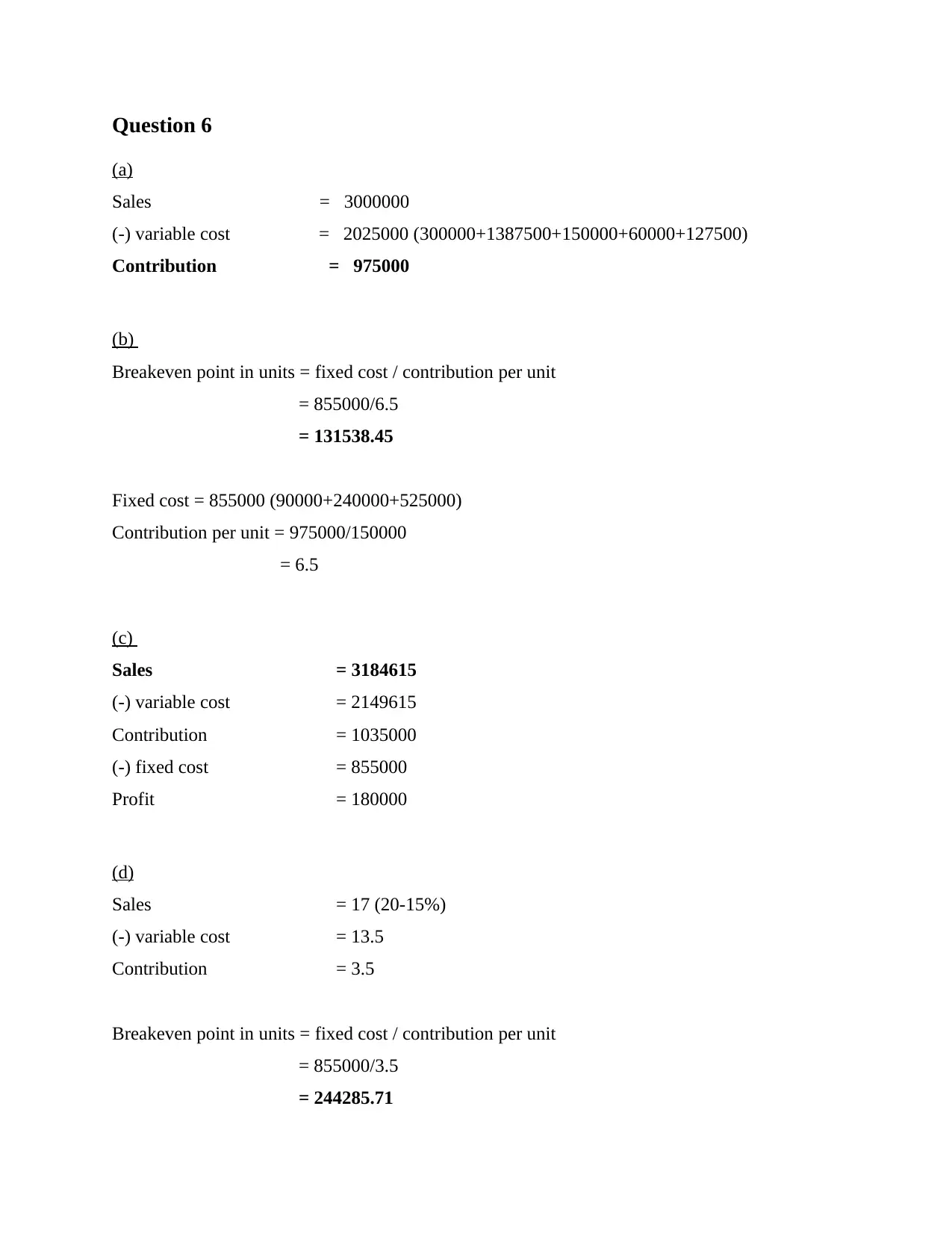

This assignment solution provides detailed answers to several management accounting questions. It includes a high-low method analysis to estimate variable and fixed costs for St James Hospital, a schedule of cost of goods sold and an income statement, and a relevant cost analysis for make-or-buy decisions. Furthermore, it covers break-even point calculations and contribution margin analysis, offering a comprehensive overview of essential management accounting concepts and their practical application. Desklib is your go-to resource for more solved assignments and past papers.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.