Alternative Exam Assignment: UGB222 Management Accounting

VerifiedAdded on 2023/06/10

|9

|1215

|417

Homework Assignment

AI Summary

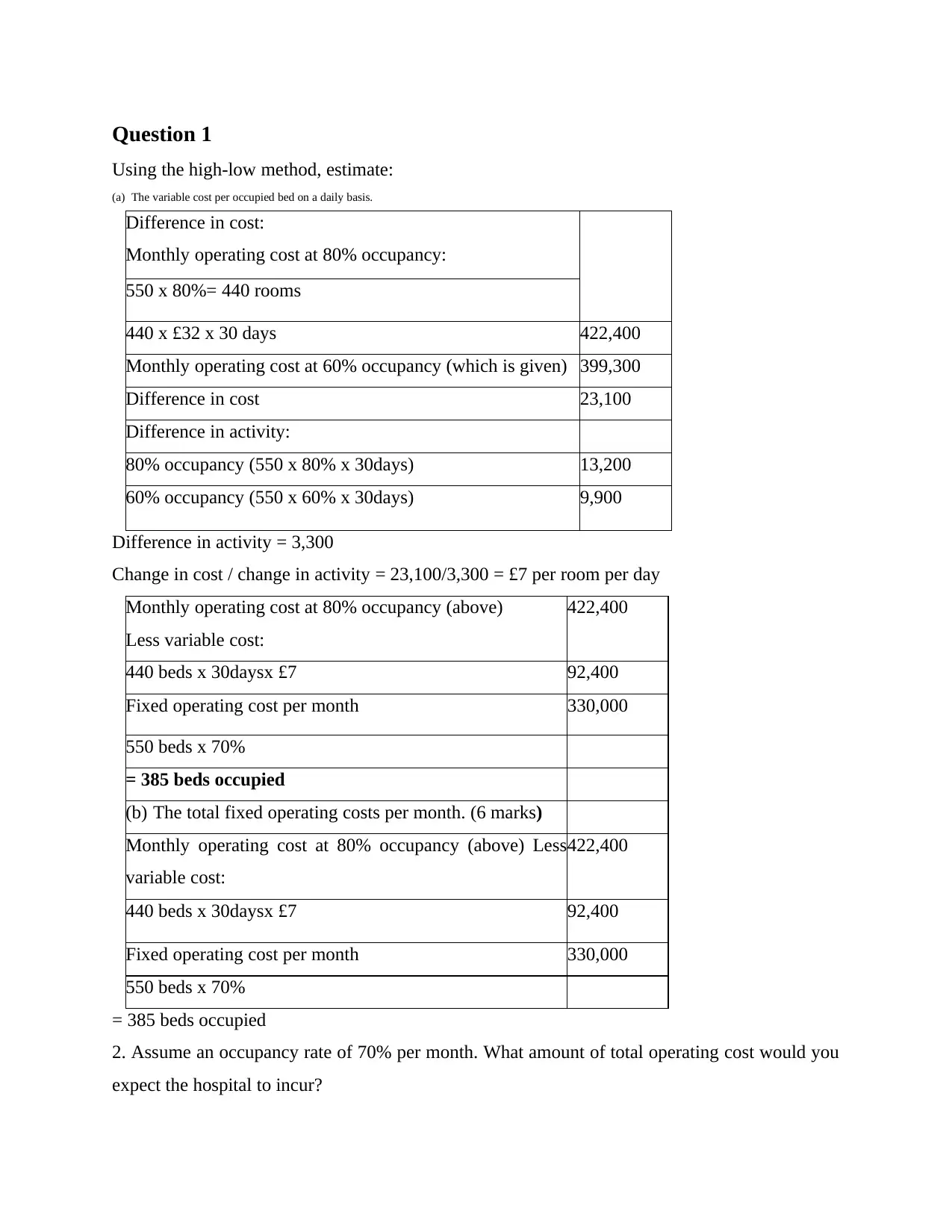

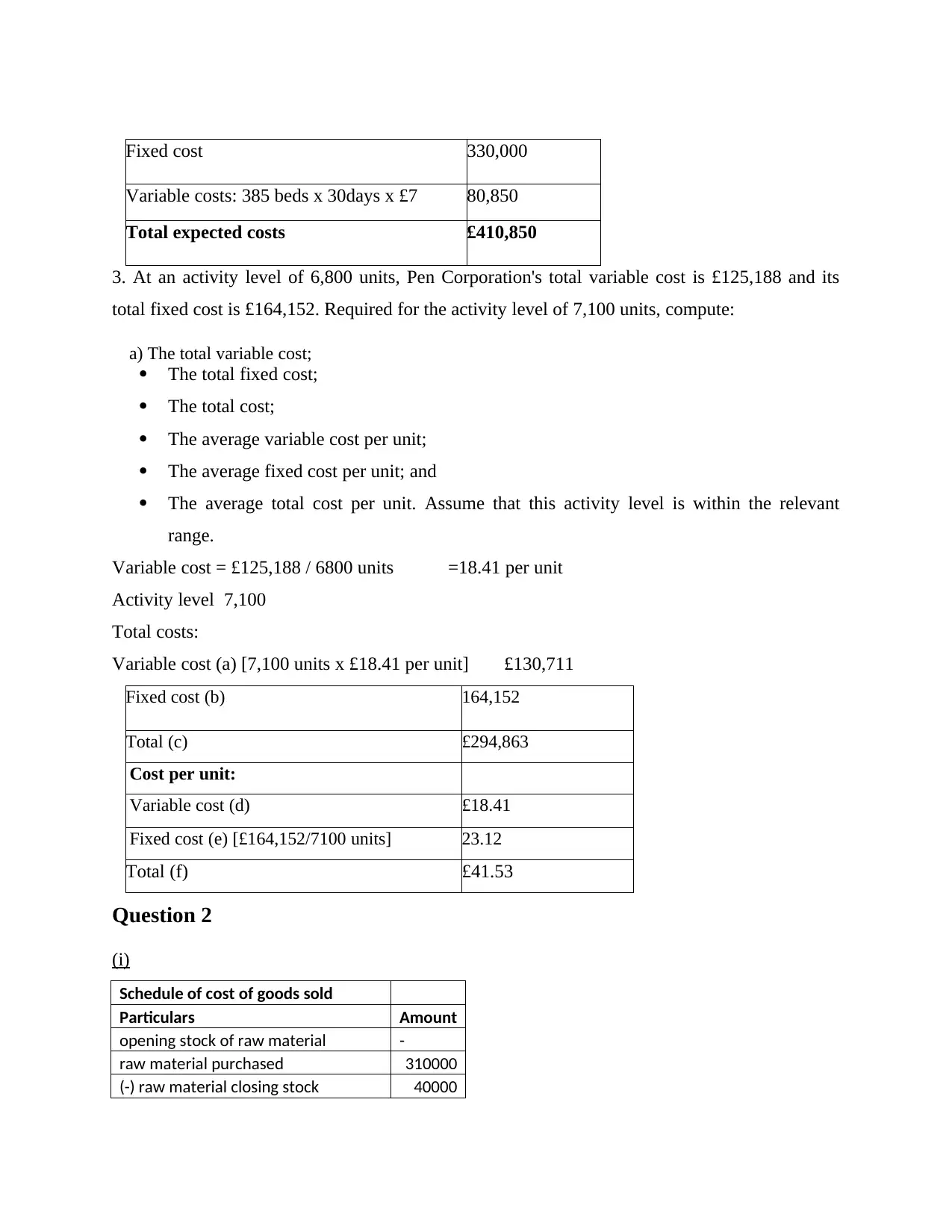

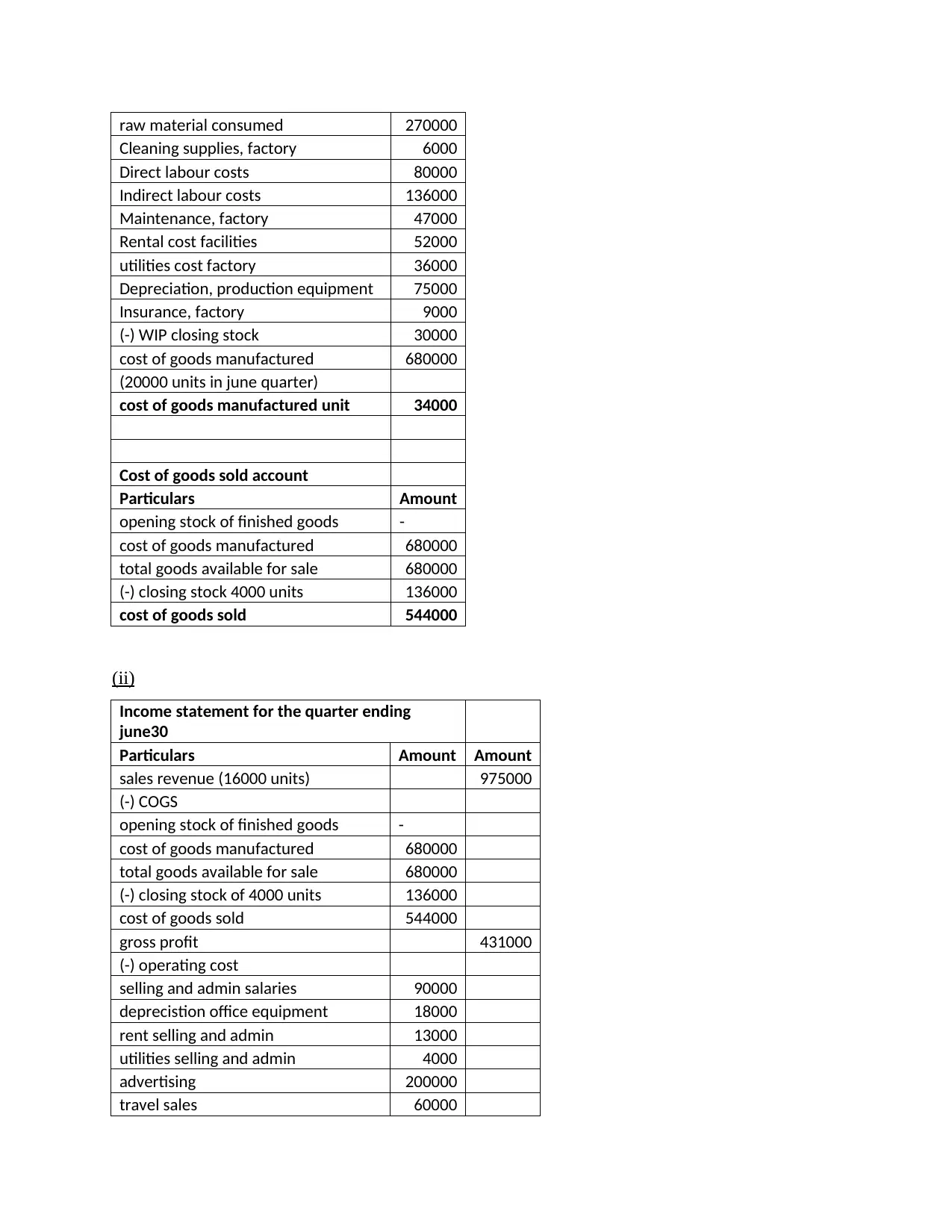

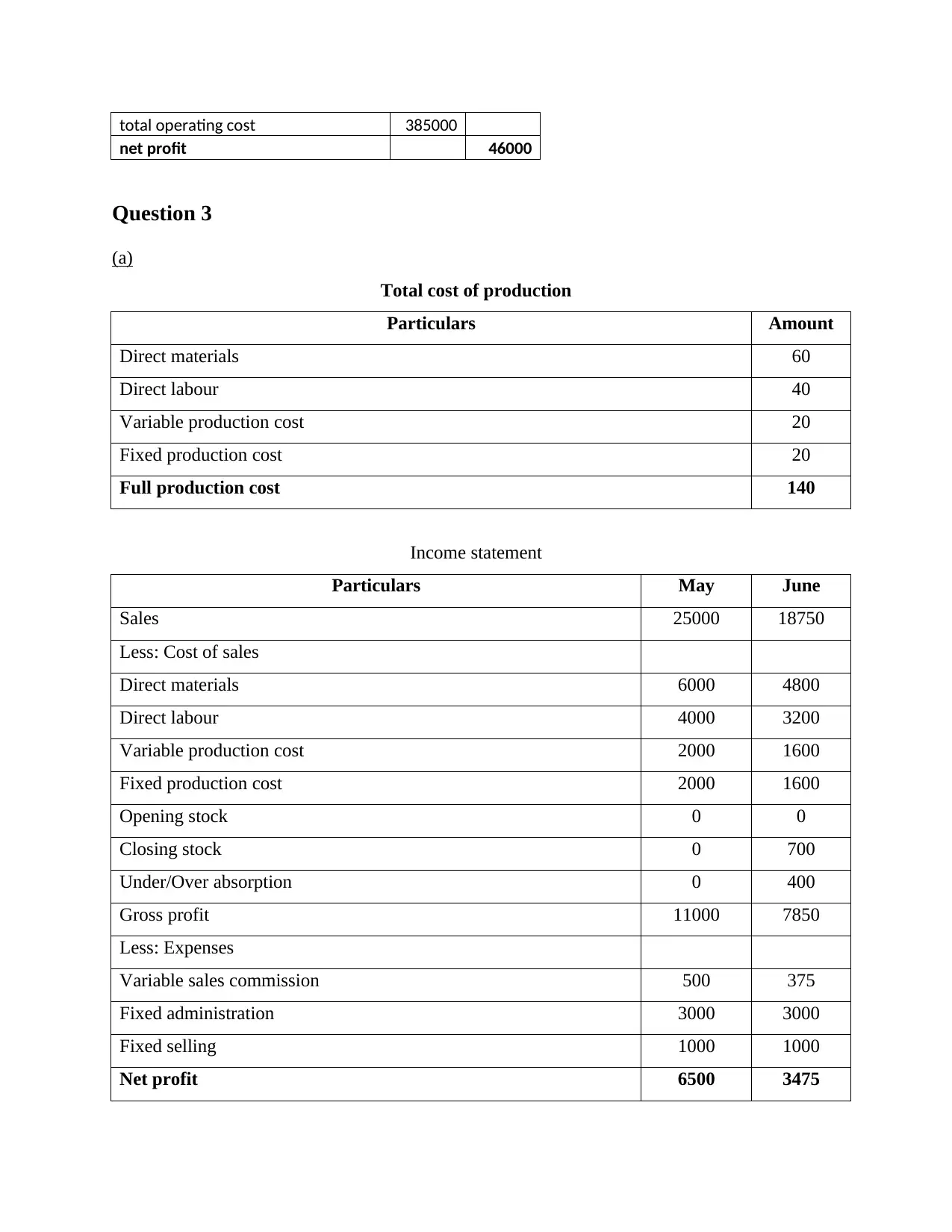

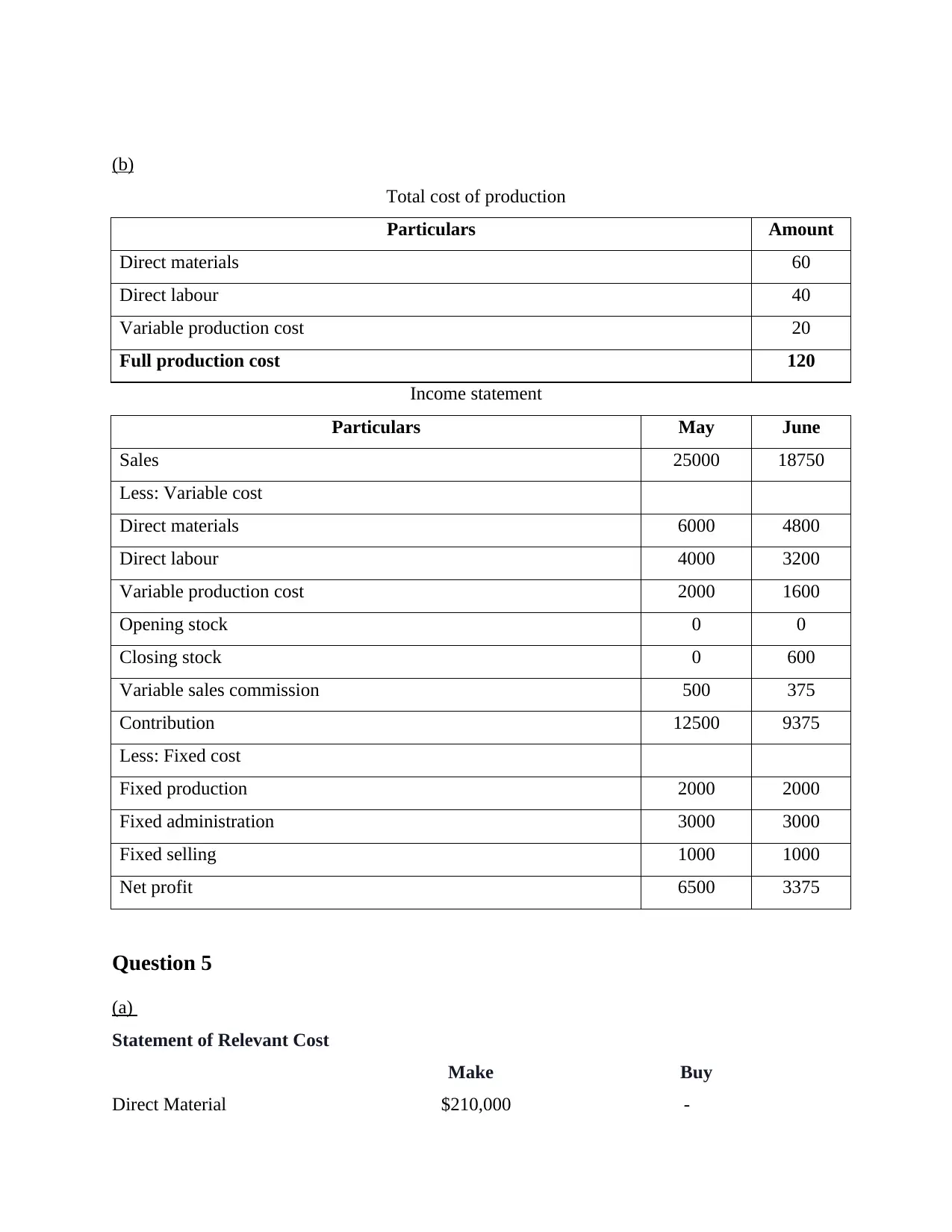

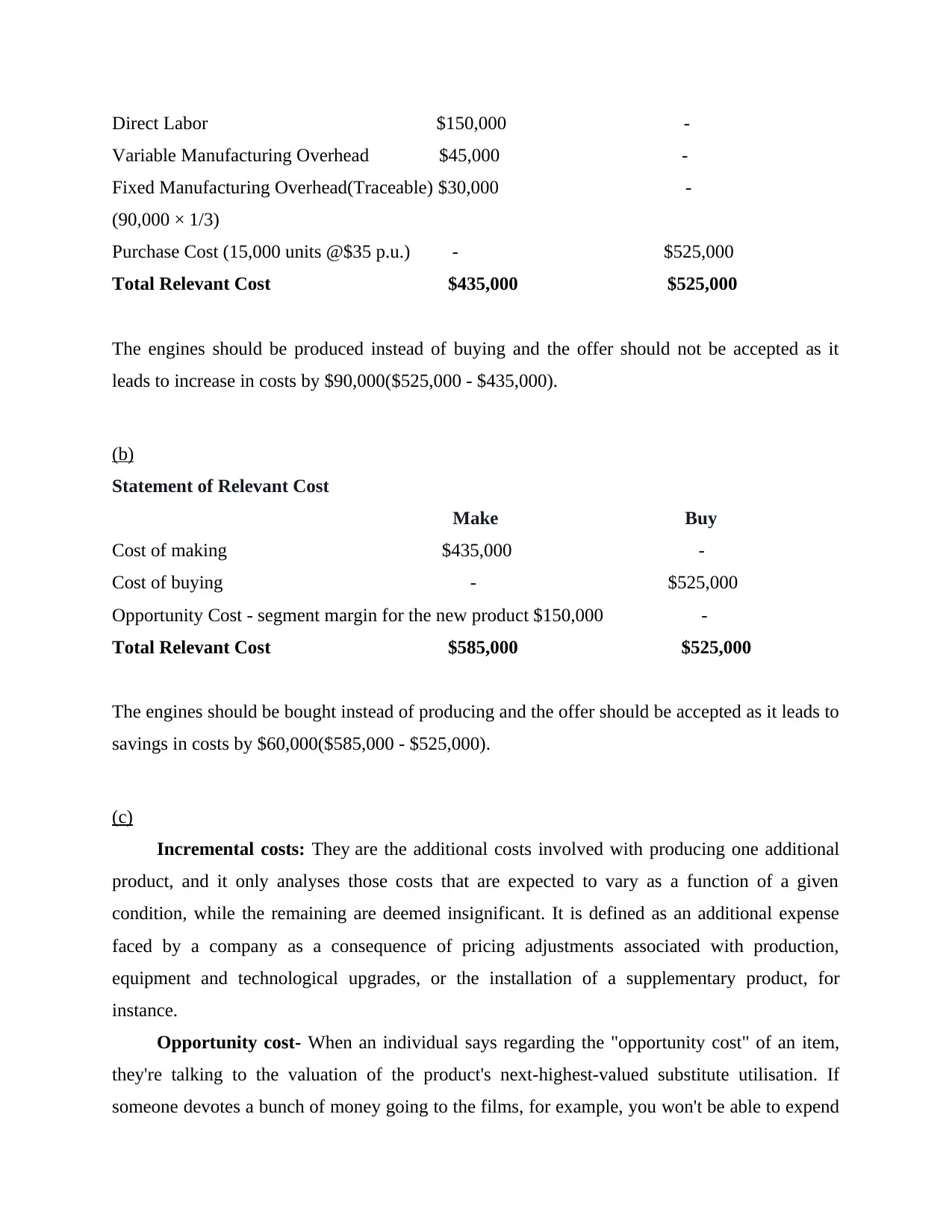

This document presents a comprehensive solution to an alternative exam assignment in Management Accounting (UGB222) from the Faculty of Business, Law & Tourism. The solution addresses four questions, each worth 25 marks, covering key concepts such as the high-low method for cost estimation, calculating fixed and variable costs, preparing cost of goods sold schedules and income statements, and performing relevant cost analysis for make-or-buy decisions. Detailed calculations and explanations are provided for each part of the questions, including the application of relevant cost principles, the analysis of different cost structures, and the impact of various scenarios on profitability. The assignment requires students to demonstrate their understanding of cost accounting principles and their ability to apply them to practical business situations. The document is designed to aid students in understanding the concepts and preparing for similar assessments.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.