UGB223 Finance Report: Project Evaluation, Rights Issue & Dividend

VerifiedAdded on 2023/06/10

|11

|2795

|495

Report

AI Summary

This report provides a comprehensive analysis of various financial concepts and their application to business decisions. It begins with a comparison of two projects using Net Present Value (NPV) and Internal Rate of Return (IRR) to determine the most viable investment, considering potential changes in the cost of capital. The report further explores the mechanics of a rights issue, calculating the theoretical ex-rights price, net cash raised, and the value of rights, while also discussing the advantages and disadvantages of this financing method. Additionally, it computes the Weighted Average Cost of Capital (WACC) using market weightings and critically assesses the company's capital structure. Finally, the report examines factors influencing dividend policy and calculates shareholder wealth under different dividend options. This assignment solution is available on Desklib, where students can find a wealth of academic resources, including past papers and solved assignments, to support their studies.

UGB 223 Business

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

QUESTION 2..................................................................................................................................3

a) Compute NPV and suggest which project should be accepted...............................................3

b) Calculate IRR and on the basis of this which project should be accepted..............................4

c) If the cost of capital increase to 20 % in year 5, then does the changes would be advisable..4

QUESTION 3..................................................................................................................................5

Calculate the following:...............................................................................................................5

a) the theoretical ex-rights price per share...................................................................................5

b) net cash raised.........................................................................................................................6

c) Value of rights.........................................................................................................................6

d) Discuss the pros and cons of right issue..................................................................................7

QUESTION 4..................................................................................................................................8

a) Compute the weighted average cost of capital (WACC) using the market weightings..........8

b) Critically discuss whether the company is integration a sensible level of capital structure

and can minimise the WACC......................................................................................................8

QUESTION 6..................................................................................................................................9

The size of the annual dividend to return to its shareholders for the factors which needs to be

considered....................................................................................................................................9

The practical issues that need to be considered when deciding on the size of the dividend

payment........................................................................................................................................9

b) Calculate the three options....................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

QUESTION 2..................................................................................................................................3

a) Compute NPV and suggest which project should be accepted...............................................3

b) Calculate IRR and on the basis of this which project should be accepted..............................4

c) If the cost of capital increase to 20 % in year 5, then does the changes would be advisable..4

QUESTION 3..................................................................................................................................5

Calculate the following:...............................................................................................................5

a) the theoretical ex-rights price per share...................................................................................5

b) net cash raised.........................................................................................................................6

c) Value of rights.........................................................................................................................6

d) Discuss the pros and cons of right issue..................................................................................7

QUESTION 4..................................................................................................................................8

a) Compute the weighted average cost of capital (WACC) using the market weightings..........8

b) Critically discuss whether the company is integration a sensible level of capital structure

and can minimise the WACC......................................................................................................8

QUESTION 6..................................................................................................................................9

The size of the annual dividend to return to its shareholders for the factors which needs to be

considered....................................................................................................................................9

The practical issues that need to be considered when deciding on the size of the dividend

payment........................................................................................................................................9

b) Calculate the three options....................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

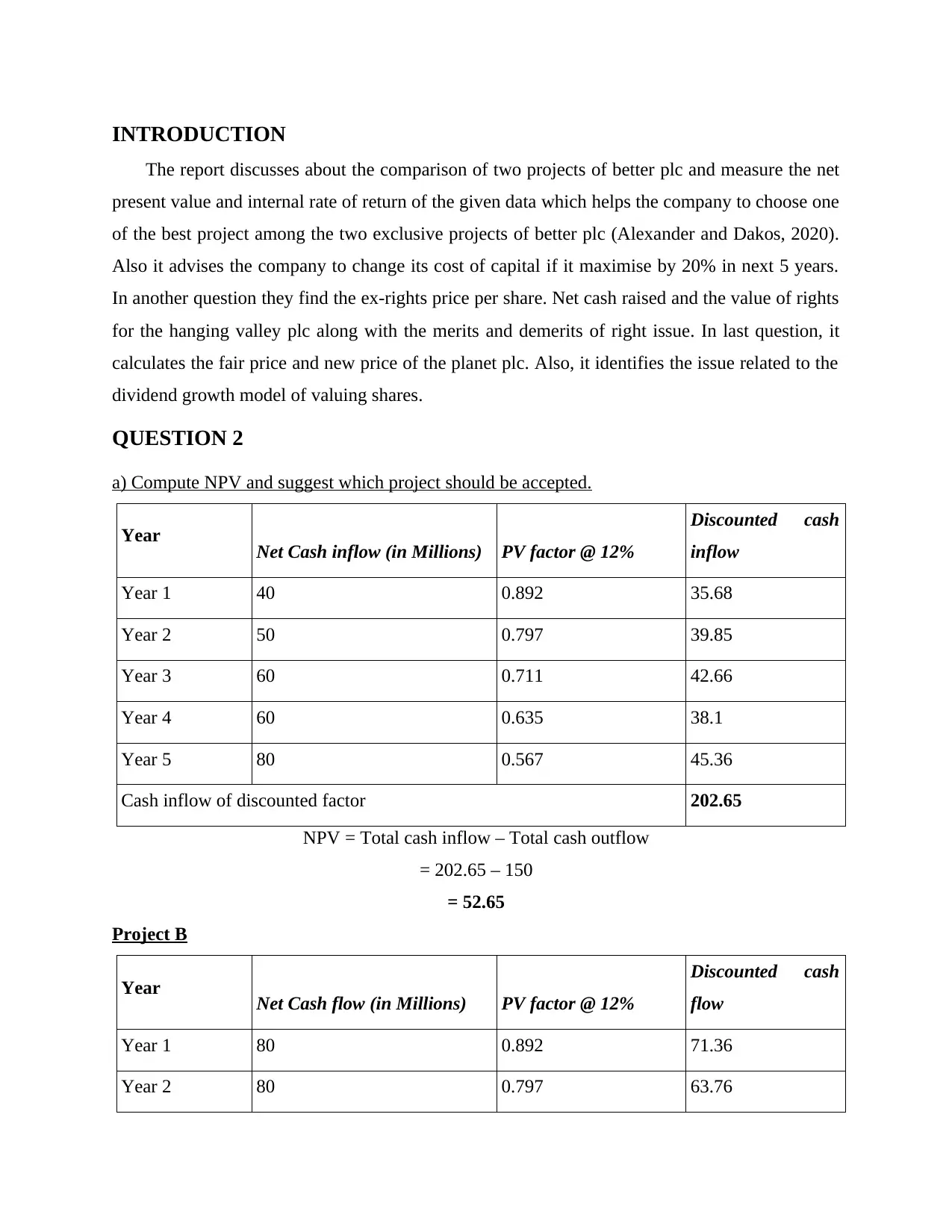

INTRODUCTION

The report discusses about the comparison of two projects of better plc and measure the net

present value and internal rate of return of the given data which helps the company to choose one

of the best project among the two exclusive projects of better plc (Alexander and Dakos, 2020).

Also it advises the company to change its cost of capital if it maximise by 20% in next 5 years.

In another question they find the ex-rights price per share. Net cash raised and the value of rights

for the hanging valley plc along with the merits and demerits of right issue. In last question, it

calculates the fair price and new price of the planet plc. Also, it identifies the issue related to the

dividend growth model of valuing shares.

QUESTION 2

a) Compute NPV and suggest which project should be accepted.

Year Net Cash inflow (in Millions) PV factor @ 12%

Discounted cash

inflow

Year 1 40 0.892 35.68

Year 2 50 0.797 39.85

Year 3 60 0.711 42.66

Year 4 60 0.635 38.1

Year 5 80 0.567 45.36

Cash inflow of discounted factor 202.65

NPV = Total cash inflow – Total cash outflow

= 202.65 – 150

= 52.65

Project B

Year Net Cash flow (in Millions) PV factor @ 12%

Discounted cash

flow

Year 1 80 0.892 71.36

Year 2 80 0.797 63.76

The report discusses about the comparison of two projects of better plc and measure the net

present value and internal rate of return of the given data which helps the company to choose one

of the best project among the two exclusive projects of better plc (Alexander and Dakos, 2020).

Also it advises the company to change its cost of capital if it maximise by 20% in next 5 years.

In another question they find the ex-rights price per share. Net cash raised and the value of rights

for the hanging valley plc along with the merits and demerits of right issue. In last question, it

calculates the fair price and new price of the planet plc. Also, it identifies the issue related to the

dividend growth model of valuing shares.

QUESTION 2

a) Compute NPV and suggest which project should be accepted.

Year Net Cash inflow (in Millions) PV factor @ 12%

Discounted cash

inflow

Year 1 40 0.892 35.68

Year 2 50 0.797 39.85

Year 3 60 0.711 42.66

Year 4 60 0.635 38.1

Year 5 80 0.567 45.36

Cash inflow of discounted factor 202.65

NPV = Total cash inflow – Total cash outflow

= 202.65 – 150

= 52.65

Project B

Year Net Cash flow (in Millions) PV factor @ 12%

Discounted cash

flow

Year 1 80 0.892 71.36

Year 2 80 0.797 63.76

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Year 3 50 0.711 35.55

Year 4 40 0.635 25.4

Year 5 30 0.567 17.01

Cash Flow 213.08

NPV = Total cash inflow – Total cash outflow

= 213.08 – 152

= 61.08

Analysis: According to the calculations, both projects are advantageous and deliver good returns

on investment. When the NPV approach is applied to both projects, it is discovered that project

A is more sustainable than project B because it provides a higher return for a lower investment.

b) Calculate IRR and on the basis of this which project should be accepted.

Period Inflows PV @ 14% Cash Flow PV @ 18% Cash Flow

0 275,000 1 -275,000 1 -275,000

1 72,500 0.88 63,800 0.85 61,625

2 72,500 0.77 55,825 0.72 52,200

3 72,500 0.68 49,300 0.61 44,225

4 72,500 0.61 44,225 0.52 37,700

5 72,500 0.54 39,150 0.44 31,900

6 72,500 0.48 34,800 0.37 26,825

Residual value

at the end 41,250 0.48 19,800 0.37 15,263

Net Present Value 31,900 -5,262

c) If the cost of capital increase to 20 % in year 5, then does the changes would be advisable.

Years Inflows PV @ 12% Discounted Cash

Flow

Year 4 40 0.635 25.4

Year 5 30 0.567 17.01

Cash Flow 213.08

NPV = Total cash inflow – Total cash outflow

= 213.08 – 152

= 61.08

Analysis: According to the calculations, both projects are advantageous and deliver good returns

on investment. When the NPV approach is applied to both projects, it is discovered that project

A is more sustainable than project B because it provides a higher return for a lower investment.

b) Calculate IRR and on the basis of this which project should be accepted.

Period Inflows PV @ 14% Cash Flow PV @ 18% Cash Flow

0 275,000 1 -275,000 1 -275,000

1 72,500 0.88 63,800 0.85 61,625

2 72,500 0.77 55,825 0.72 52,200

3 72,500 0.68 49,300 0.61 44,225

4 72,500 0.61 44,225 0.52 37,700

5 72,500 0.54 39,150 0.44 31,900

6 72,500 0.48 34,800 0.37 26,825

Residual value

at the end 41,250 0.48 19,800 0.37 15,263

Net Present Value 31,900 -5,262

c) If the cost of capital increase to 20 % in year 5, then does the changes would be advisable.

Years Inflows PV @ 12% Discounted Cash

Flow

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0 275000 1 -275,000

1 72,500 0.89 64,525

2 72,500 0.80 58,000

3 72,500 0.71 51,475

4 72,500 0.64 46,400

5 72,500 0.57 41,325

6 72,500 0.51 36,975

Residual value at

the end

41,250 0.51 20,138

Net Present Value 48,838

The cost of capital is increase to 20% in the 5th year, so from that it is advised to select

project A for the purpose of investment.

QUESTION 3

Calculate the following:

Issue shares = 2 m

Nominal Value = £ 1

Issue price for market = 80%

Current market price = £ 2.75

Issue Costs = £ 50000

a) the theoretical ex-rights price per share

= (New Shares * Issue Price) + (Old Share * Market Price) / (New Shares + Old Shares)

Particulars Condition 1 Condition 2 Condition 3

Recommended prices to issue shares £ 1.80 £ 1.60 £ 1.40

Fund to be increased £ 180,000 £ 180,000 £ 180,000

Number of shares required to issue £ 100,000 £ 112,500 £ 128,571

1 72,500 0.89 64,525

2 72,500 0.80 58,000

3 72,500 0.71 51,475

4 72,500 0.64 46,400

5 72,500 0.57 41,325

6 72,500 0.51 36,975

Residual value at

the end

41,250 0.51 20,138

Net Present Value 48,838

The cost of capital is increase to 20% in the 5th year, so from that it is advised to select

project A for the purpose of investment.

QUESTION 3

Calculate the following:

Issue shares = 2 m

Nominal Value = £ 1

Issue price for market = 80%

Current market price = £ 2.75

Issue Costs = £ 50000

a) the theoretical ex-rights price per share

= (New Shares * Issue Price) + (Old Share * Market Price) / (New Shares + Old Shares)

Particulars Condition 1 Condition 2 Condition 3

Recommended prices to issue shares £ 1.80 £ 1.60 £ 1.40

Fund to be increased £ 180,000 £ 180,000 £ 180,000

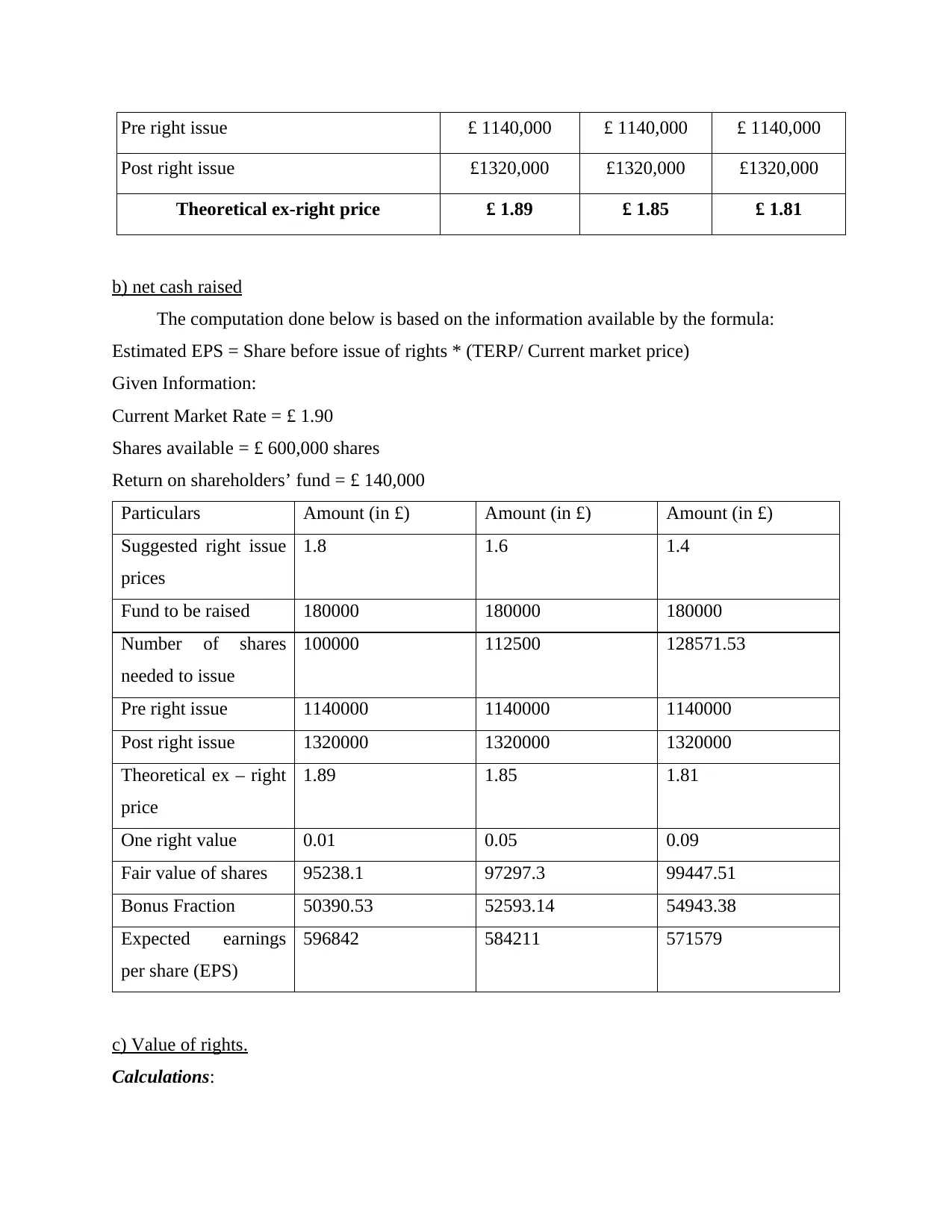

Number of shares required to issue £ 100,000 £ 112,500 £ 128,571

Pre right issue £ 1140,000 £ 1140,000 £ 1140,000

Post right issue £1320,000 £1320,000 £1320,000

Theoretical ex-right price £ 1.89 £ 1.85 £ 1.81

b) net cash raised

The computation done below is based on the information available by the formula:

Estimated EPS = Share before issue of rights * (TERP/ Current market price)

Given Information:

Current Market Rate = £ 1.90

Shares available = £ 600,000 shares

Return on shareholders’ fund = £ 140,000

Particulars Amount (in £) Amount (in £) Amount (in £)

Suggested right issue

prices

1.8 1.6 1.4

Fund to be raised 180000 180000 180000

Number of shares

needed to issue

100000 112500 128571.53

Pre right issue 1140000 1140000 1140000

Post right issue 1320000 1320000 1320000

Theoretical ex – right

price

1.89 1.85 1.81

One right value 0.01 0.05 0.09

Fair value of shares 95238.1 97297.3 99447.51

Bonus Fraction 50390.53 52593.14 54943.38

Expected earnings

per share (EPS)

596842 584211 571579

c) Value of rights.

Calculations:

Post right issue £1320,000 £1320,000 £1320,000

Theoretical ex-right price £ 1.89 £ 1.85 £ 1.81

b) net cash raised

The computation done below is based on the information available by the formula:

Estimated EPS = Share before issue of rights * (TERP/ Current market price)

Given Information:

Current Market Rate = £ 1.90

Shares available = £ 600,000 shares

Return on shareholders’ fund = £ 140,000

Particulars Amount (in £) Amount (in £) Amount (in £)

Suggested right issue

prices

1.8 1.6 1.4

Fund to be raised 180000 180000 180000

Number of shares

needed to issue

100000 112500 128571.53

Pre right issue 1140000 1140000 1140000

Post right issue 1320000 1320000 1320000

Theoretical ex – right

price

1.89 1.85 1.81

One right value 0.01 0.05 0.09

Fair value of shares 95238.1 97297.3 99447.51

Bonus Fraction 50390.53 52593.14 54943.38

Expected earnings

per share (EPS)

596842 584211 571579

c) Value of rights.

Calculations:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

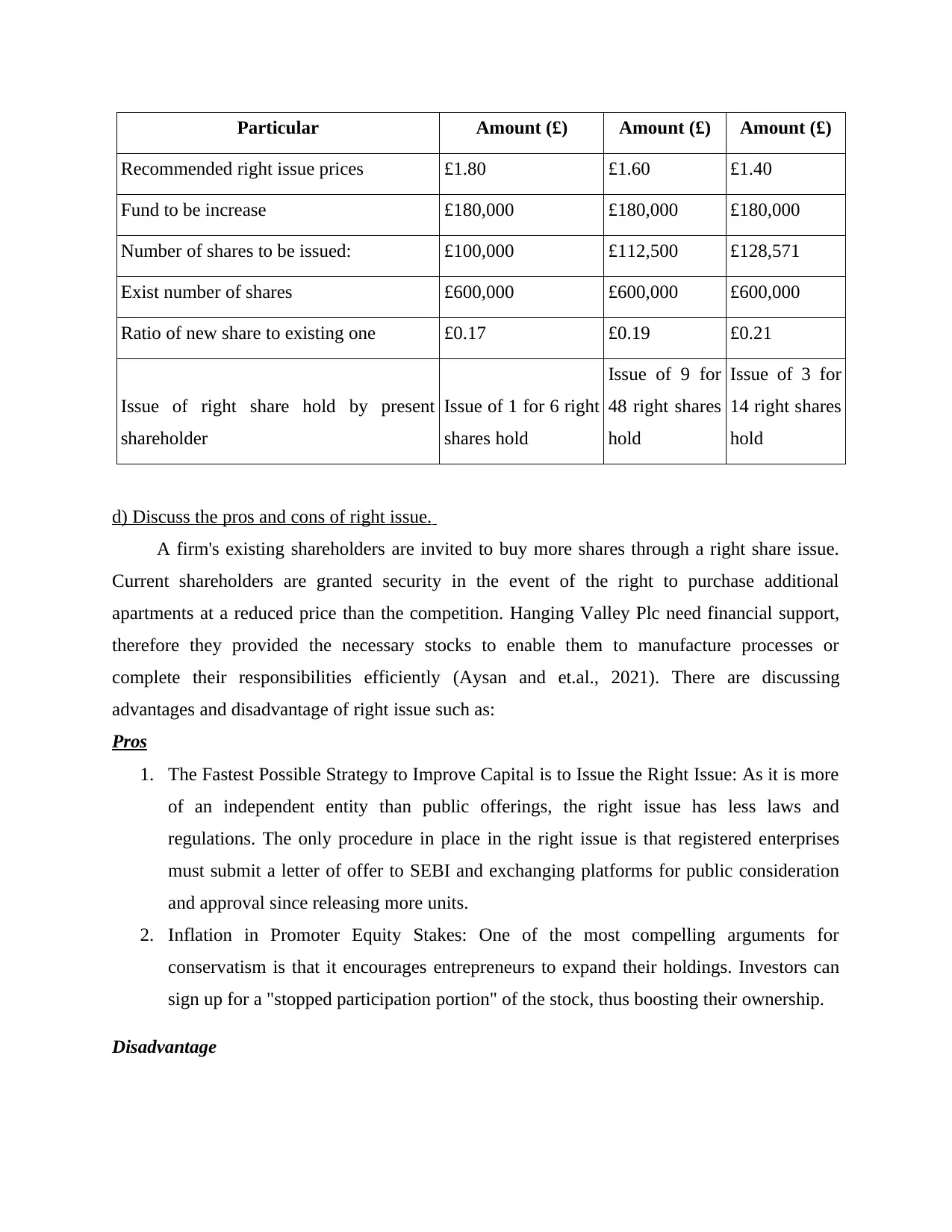

Particular Amount (£) Amount (£) Amount (£)

Recommended right issue prices £1.80 £1.60 £1.40

Fund to be increase £180,000 £180,000 £180,000

Number of shares to be issued: £100,000 £112,500 £128,571

Exist number of shares £600,000 £600,000 £600,000

Ratio of new share to existing one £0.17 £0.19 £0.21

Issue of right share hold by present

shareholder

Issue of 1 for 6 right

shares hold

Issue of 9 for

48 right shares

hold

Issue of 3 for

14 right shares

hold

d) Discuss the pros and cons of right issue.

A firm's existing shareholders are invited to buy more shares through a right share issue.

Current shareholders are granted security in the event of the right to purchase additional

apartments at a reduced price than the competition. Hanging Valley Plc need financial support,

therefore they provided the necessary stocks to enable them to manufacture processes or

complete their responsibilities efficiently (Aysan and et.al., 2021). There are discussing

advantages and disadvantage of right issue such as:

Pros

1. The Fastest Possible Strategy to Improve Capital is to Issue the Right Issue: As it is more

of an independent entity than public offerings, the right issue has less laws and

regulations. The only procedure in place in the right issue is that registered enterprises

must submit a letter of offer to SEBI and exchanging platforms for public consideration

and approval since releasing more units.

2. Inflation in Promoter Equity Stakes: One of the most compelling arguments for

conservatism is that it encourages entrepreneurs to expand their holdings. Investors can

sign up for a "stopped participation portion" of the stock, thus boosting their ownership.

Disadvantage

Recommended right issue prices £1.80 £1.60 £1.40

Fund to be increase £180,000 £180,000 £180,000

Number of shares to be issued: £100,000 £112,500 £128,571

Exist number of shares £600,000 £600,000 £600,000

Ratio of new share to existing one £0.17 £0.19 £0.21

Issue of right share hold by present

shareholder

Issue of 1 for 6 right

shares hold

Issue of 9 for

48 right shares

hold

Issue of 3 for

14 right shares

hold

d) Discuss the pros and cons of right issue.

A firm's existing shareholders are invited to buy more shares through a right share issue.

Current shareholders are granted security in the event of the right to purchase additional

apartments at a reduced price than the competition. Hanging Valley Plc need financial support,

therefore they provided the necessary stocks to enable them to manufacture processes or

complete their responsibilities efficiently (Aysan and et.al., 2021). There are discussing

advantages and disadvantage of right issue such as:

Pros

1. The Fastest Possible Strategy to Improve Capital is to Issue the Right Issue: As it is more

of an independent entity than public offerings, the right issue has less laws and

regulations. The only procedure in place in the right issue is that registered enterprises

must submit a letter of offer to SEBI and exchanging platforms for public consideration

and approval since releasing more units.

2. Inflation in Promoter Equity Stakes: One of the most compelling arguments for

conservatism is that it encourages entrepreneurs to expand their holdings. Investors can

sign up for a "stopped participation portion" of the stock, thus boosting their ownership.

Disadvantage

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Raise revenue up to a certain amount- An obvious downside is that a company cannot

acquire a specific quantity in the event of a crisis (IPO). The amount of money a

company can raise through a core issue is usually limited by stock markets (Babich and

Birge, 2020).

2. The value of each unit could be diluted- When a corporation issues equity shares to raise

capital, the stakes of current investors may be lowered. When the proportion of stock

holdings decreases due to the entrance of stock holders, property investors face a tough

situation.

QUESTION 4

a) Compute the weighted average cost of capital (WACC) using the market weightings.

Particular Amount Weights Cost of Capital WACC

Equity Share capital 200 0.10752688 18% 1.95%

Preference Share Capital 300 0.16129032 7% 1.13%

Reserves and surplus 150 0.08064516 24% 1.94%

Bonds 650 0.34946237 9% 3.15%

Bank Notes 560 0.30107527 9% 2.71%

Total 1860 1

WACC 10.87

%

Cost of equity = Rf + Beta * (Rm – Rf)

= 7% + 1.21 * 9.1% = 0.18 = 18.11%

b) Critically discuss whether the company is integration a sensible level of capital structure and

can minimise the WACC.

Even without the actual wording, an overall capital value is assessed at 18.11%. These

indicate that WACC will be reduced by 10.87% due to the completion of each valid capital

change, thus helping the company to reduce possible uses. Jordan Plc will be prepared to spend

these funds and assets to deliver potential outcomes for the planned businesses and operations

acquire a specific quantity in the event of a crisis (IPO). The amount of money a

company can raise through a core issue is usually limited by stock markets (Babich and

Birge, 2020).

2. The value of each unit could be diluted- When a corporation issues equity shares to raise

capital, the stakes of current investors may be lowered. When the proportion of stock

holdings decreases due to the entrance of stock holders, property investors face a tough

situation.

QUESTION 4

a) Compute the weighted average cost of capital (WACC) using the market weightings.

Particular Amount Weights Cost of Capital WACC

Equity Share capital 200 0.10752688 18% 1.95%

Preference Share Capital 300 0.16129032 7% 1.13%

Reserves and surplus 150 0.08064516 24% 1.94%

Bonds 650 0.34946237 9% 3.15%

Bank Notes 560 0.30107527 9% 2.71%

Total 1860 1

WACC 10.87

%

Cost of equity = Rf + Beta * (Rm – Rf)

= 7% + 1.21 * 9.1% = 0.18 = 18.11%

b) Critically discuss whether the company is integration a sensible level of capital structure and

can minimise the WACC.

Even without the actual wording, an overall capital value is assessed at 18.11%. These

indicate that WACC will be reduced by 10.87% due to the completion of each valid capital

change, thus helping the company to reduce possible uses. Jordan Plc will be prepared to spend

these funds and assets to deliver potential outcomes for the planned businesses and operations

(Blackwell and Kohl, 2018). Chiefs may choose to acquire new equipment that can be used more

from time to time to increase the efficiency of the guild and enable hierarchies.

The gearing features a link between the promise of the party and the financial exchange.

Organizations like Jordan Plc would be well suited to maintain a balance between domestic and

global resources, provided they tap into that degree.

Weighted normal capital expense: This can be described as a financing cost or instalment

and should be imposed on an element's financial backers, especially the owner. It is not entirely

characterized by overall communication, nor by directors. Variable values, propensity tools, and

commitments are listed when inspected (Hassan and Mollah, 2018).

Infrastructure is the system that an association needs to control its obligations and securities

transactions through representational commitments. This helps companies identify assets that are

expected to scale and fulfil layered tasks. In different aspects, the time frame spent on

commitments, financial exchanges and different protections may be considered.

QUESTION 6

The size of the annual dividend to return to its shareholders for the factors which needs to be

considered.

Profitability and expansion: The higher the expected growth and productivity, the lower

the dividend should be, because the financial investors of funds will misjudge the return

on capital of the organization, so the speculative value will increase with the value of the

organization itself (Hassan, Khan and Paltrinieri, 2019).

Liquidity: Assuming that the organization needs reserves, it prefers the lower profit scale

because the holding is a source of funding and does not need to be acquired externally at

a fixed cost.

The practical issues that need to be considered when deciding on the size of the dividend

payment.

i) Before declaring profits, the profit shifting criteria set out in the Companies Act

should be met. The size is subject to the conditions set out in the company law

ii) Deadline for profit instalments - the company needs to assess whether it has too much

assets to deliver profits. Productivity does not equal mobility. Subsequently, the

available reserves limit the size of the dividend (Kong and et.al., 2021).

from time to time to increase the efficiency of the guild and enable hierarchies.

The gearing features a link between the promise of the party and the financial exchange.

Organizations like Jordan Plc would be well suited to maintain a balance between domestic and

global resources, provided they tap into that degree.

Weighted normal capital expense: This can be described as a financing cost or instalment

and should be imposed on an element's financial backers, especially the owner. It is not entirely

characterized by overall communication, nor by directors. Variable values, propensity tools, and

commitments are listed when inspected (Hassan and Mollah, 2018).

Infrastructure is the system that an association needs to control its obligations and securities

transactions through representational commitments. This helps companies identify assets that are

expected to scale and fulfil layered tasks. In different aspects, the time frame spent on

commitments, financial exchanges and different protections may be considered.

QUESTION 6

The size of the annual dividend to return to its shareholders for the factors which needs to be

considered.

Profitability and expansion: The higher the expected growth and productivity, the lower

the dividend should be, because the financial investors of funds will misjudge the return

on capital of the organization, so the speculative value will increase with the value of the

organization itself (Hassan, Khan and Paltrinieri, 2019).

Liquidity: Assuming that the organization needs reserves, it prefers the lower profit scale

because the holding is a source of funding and does not need to be acquired externally at

a fixed cost.

The practical issues that need to be considered when deciding on the size of the dividend

payment.

i) Before declaring profits, the profit shifting criteria set out in the Companies Act

should be met. The size is subject to the conditions set out in the company law

ii) Deadline for profit instalments - the company needs to assess whether it has too much

assets to deliver profits. Productivity does not equal mobility. Subsequently, the

available reserves limit the size of the dividend (Kong and et.al., 2021).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

iii) Set the correct market assumptions - If an organization declares abnormally high

profits in a particular year, the market may expect that it should keep up with the size

of the profits. Subsequently, forgiving the size of the dividend is crucial

b) Calculate the three options.

Wealth of Shareholder = Market value of Shares held + Dividend received + Market value

of Shares newly allotted - Loss in value of shares due to dividend / scrip dividend

In all 3 cases, since there is no value creation, wealth of shareholder will remain same. Existing

wealth

= 432 * 1250 = 540,000

i) cash dividend payment A cash dividend payment of 15p per share = 15 * 1250 + (432

- 15) * 1250 = 18,750 + 521,250 = 540,000

(Cash per share * shares held) + (shares held * new market value per share)

ii) A 5% scrip dividend = 1250 * 105% * (540,000 / (1250 * 105%) = 540,000

(new total shares * new Market value per share)

iii) A repurchase of 15 % of ordinary share capital at the current market price = 187.5 *

432 + 1062.5 * 432 = 540,000

(Cash for 187.5 shares + Market value of remaining shares)

CONCLUSION

As it is concluded from the above report, it analyses that which project is more suitable for

the company better plc. It finds out through the calculation of internal rate of return and net

present value. Afterwards it suggests the company to change in cost of capital of next 5 years if

its above 20%. In another step, it determines the price per share, value of rights and net cash

raise of the hanging plc company along with the advantages and disadvantage so right issue. At

last it determines fair and new price of the planet plc company and find the problems which arise

with the dividend growth model.

profits in a particular year, the market may expect that it should keep up with the size

of the profits. Subsequently, forgiving the size of the dividend is crucial

b) Calculate the three options.

Wealth of Shareholder = Market value of Shares held + Dividend received + Market value

of Shares newly allotted - Loss in value of shares due to dividend / scrip dividend

In all 3 cases, since there is no value creation, wealth of shareholder will remain same. Existing

wealth

= 432 * 1250 = 540,000

i) cash dividend payment A cash dividend payment of 15p per share = 15 * 1250 + (432

- 15) * 1250 = 18,750 + 521,250 = 540,000

(Cash per share * shares held) + (shares held * new market value per share)

ii) A 5% scrip dividend = 1250 * 105% * (540,000 / (1250 * 105%) = 540,000

(new total shares * new Market value per share)

iii) A repurchase of 15 % of ordinary share capital at the current market price = 187.5 *

432 + 1062.5 * 432 = 540,000

(Cash for 187.5 shares + Market value of remaining shares)

CONCLUSION

As it is concluded from the above report, it analyses that which project is more suitable for

the company better plc. It finds out through the calculation of internal rate of return and net

present value. Afterwards it suggests the company to change in cost of capital of next 5 years if

its above 20%. In another step, it determines the price per share, value of rights and net cash

raise of the hanging plc company along with the advantages and disadvantage so right issue. At

last it determines fair and new price of the planet plc company and find the problems which arise

with the dividend growth model.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Alexander, C. and Dakos, M., 2020. A critical investigation of cryptocurrency data and

analysis. Quantitative Finance. 20(2). pp.173-188.

Aysan, A.F and et.al., 2021. In search of safe haven assets during COVID-19 pandemic: An

empirical analysis of different investor types. Research in International Business and

Finance. 58.

Babich, V. and Birge, J.R., 2020. Foundations and trends at the interface of finance, operations,

and risk management. Operations, and Risk Management (December 28, 2020).

Blackwell, T. and Kohl, S., 2018. The origins of national housing finance systems: a

comparative investigation into historical variations in mortgage finance

regimes. Review of International Political Economy. 25(1). pp.49-74.

Hassan, A. and Mollah, S., 2018. Islamic Finance: A Global Alternative. In Islamic Finance (pp.

19-30). Palgrave Macmillan, Cham.

Hassan, M.K., Khan, A. and Paltrinieri, A., 2019. Liquidity risk, credit risk and stability in

Islamic and conventional banks. Research in International Business and Finance. 48.

17–31.

Kong, Q and et.al., 2021. High-speed railway opening and urban green productivity in the post-

COVID-19: Evidence from green finance. Global Finance Journal. 49. p.100645.

Moreale, J. and Zaynutdinova, G.R., 2018. A Bloomberg terminal application in an intermediate

finance course. Journal of Financial Education. 44(2). pp.262-283.

Rod Koch, C.M.A. and CSCA, P., 2019. Can RPA Improve Agility?. Strategic Finance. 100(9).

pp.68-69.

Romano, A.A and et.al., 2018. Climate Finance as an Instrument to Promote the Green Growth

in Developing Countries. Springer International Publishing.

Sison, A.J.G and et.al., 2018. Virtues and the common good in finance. In Business Ethics (pp.

51-81). Routledge.

Xia, X. and Gan, L., 2020. SME financing with new credit guarantee contracts over the business

cycle. International Review of Economics & Finance. 69. pp.515-538.

Yan, N and et.al., 2021. Online finance with dual channels and bidirectional free-riding

effect. International Journal of Production Economics. 231. p.107834.

Books and Journals

Alexander, C. and Dakos, M., 2020. A critical investigation of cryptocurrency data and

analysis. Quantitative Finance. 20(2). pp.173-188.

Aysan, A.F and et.al., 2021. In search of safe haven assets during COVID-19 pandemic: An

empirical analysis of different investor types. Research in International Business and

Finance. 58.

Babich, V. and Birge, J.R., 2020. Foundations and trends at the interface of finance, operations,

and risk management. Operations, and Risk Management (December 28, 2020).

Blackwell, T. and Kohl, S., 2018. The origins of national housing finance systems: a

comparative investigation into historical variations in mortgage finance

regimes. Review of International Political Economy. 25(1). pp.49-74.

Hassan, A. and Mollah, S., 2018. Islamic Finance: A Global Alternative. In Islamic Finance (pp.

19-30). Palgrave Macmillan, Cham.

Hassan, M.K., Khan, A. and Paltrinieri, A., 2019. Liquidity risk, credit risk and stability in

Islamic and conventional banks. Research in International Business and Finance. 48.

17–31.

Kong, Q and et.al., 2021. High-speed railway opening and urban green productivity in the post-

COVID-19: Evidence from green finance. Global Finance Journal. 49. p.100645.

Moreale, J. and Zaynutdinova, G.R., 2018. A Bloomberg terminal application in an intermediate

finance course. Journal of Financial Education. 44(2). pp.262-283.

Rod Koch, C.M.A. and CSCA, P., 2019. Can RPA Improve Agility?. Strategic Finance. 100(9).

pp.68-69.

Romano, A.A and et.al., 2018. Climate Finance as an Instrument to Promote the Green Growth

in Developing Countries. Springer International Publishing.

Sison, A.J.G and et.al., 2018. Virtues and the common good in finance. In Business Ethics (pp.

51-81). Routledge.

Xia, X. and Gan, L., 2020. SME financing with new credit guarantee contracts over the business

cycle. International Review of Economics & Finance. 69. pp.515-538.

Yan, N and et.al., 2021. Online finance with dual channels and bidirectional free-riding

effect. International Journal of Production Economics. 231. p.107834.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.