Accounting Diploma: UK Corporation Tax, Capital Gains and Liabilities

VerifiedAdded on 2023/06/10

|12

|1371

|313

Report

AI Summary

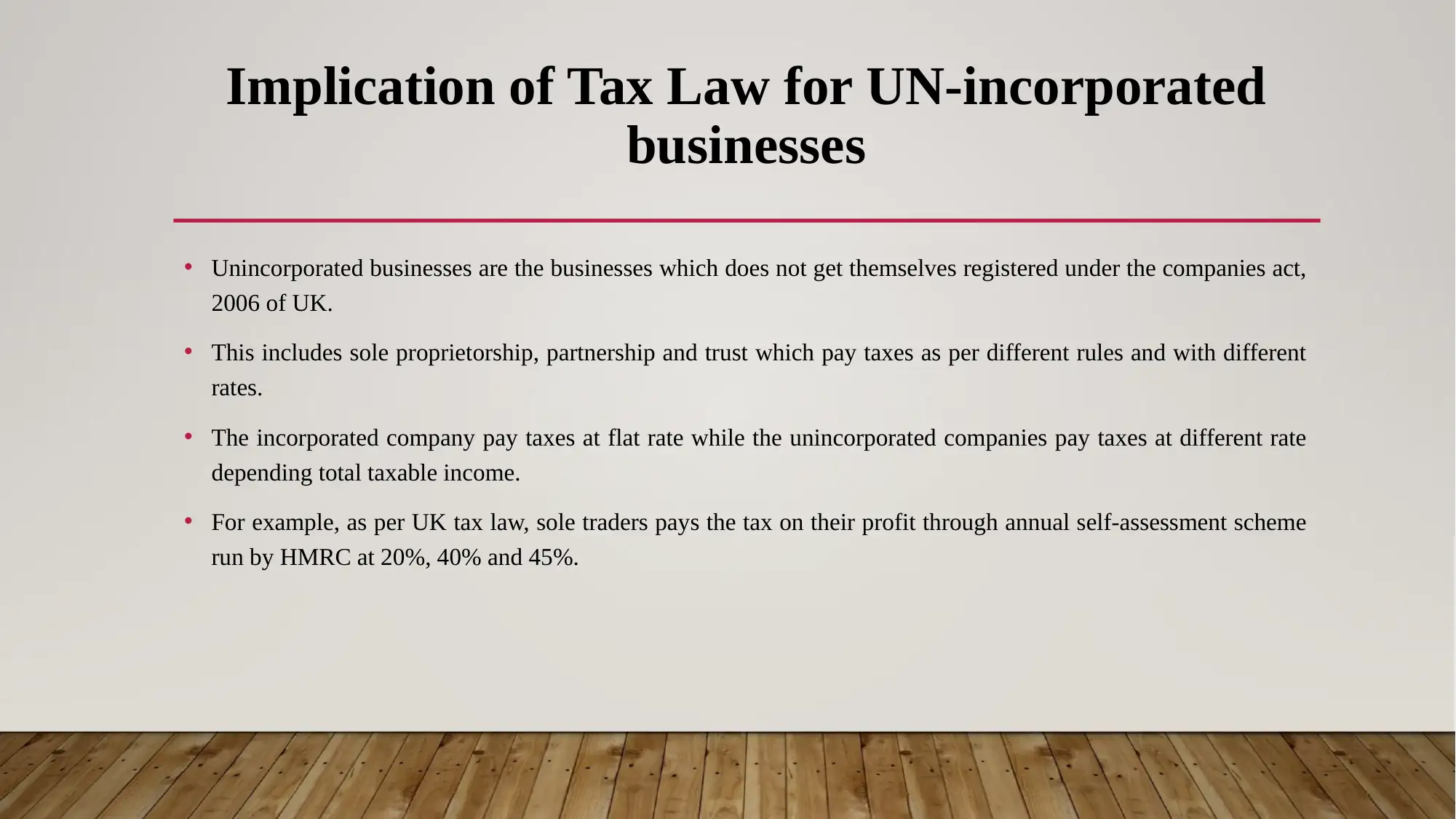

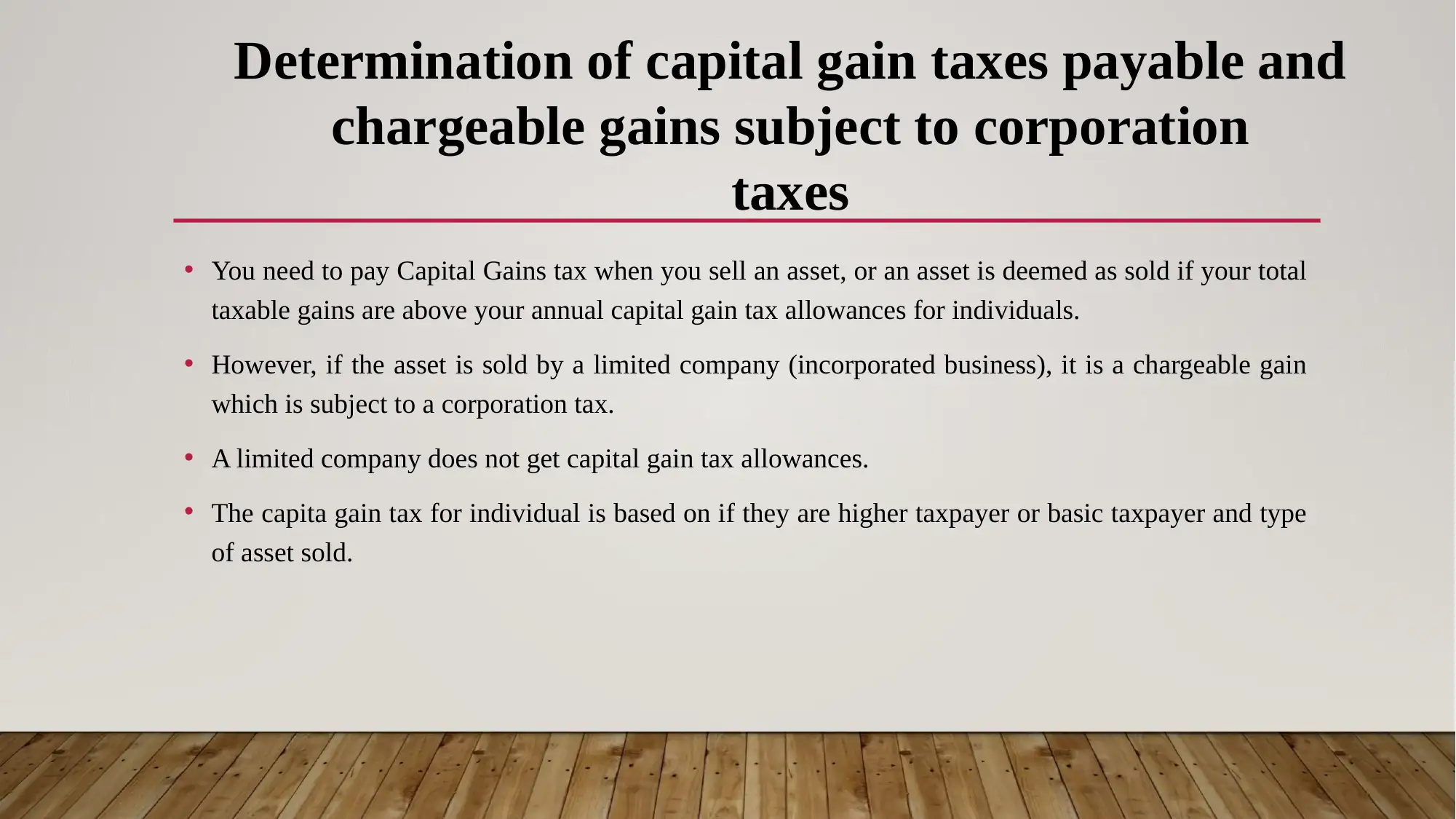

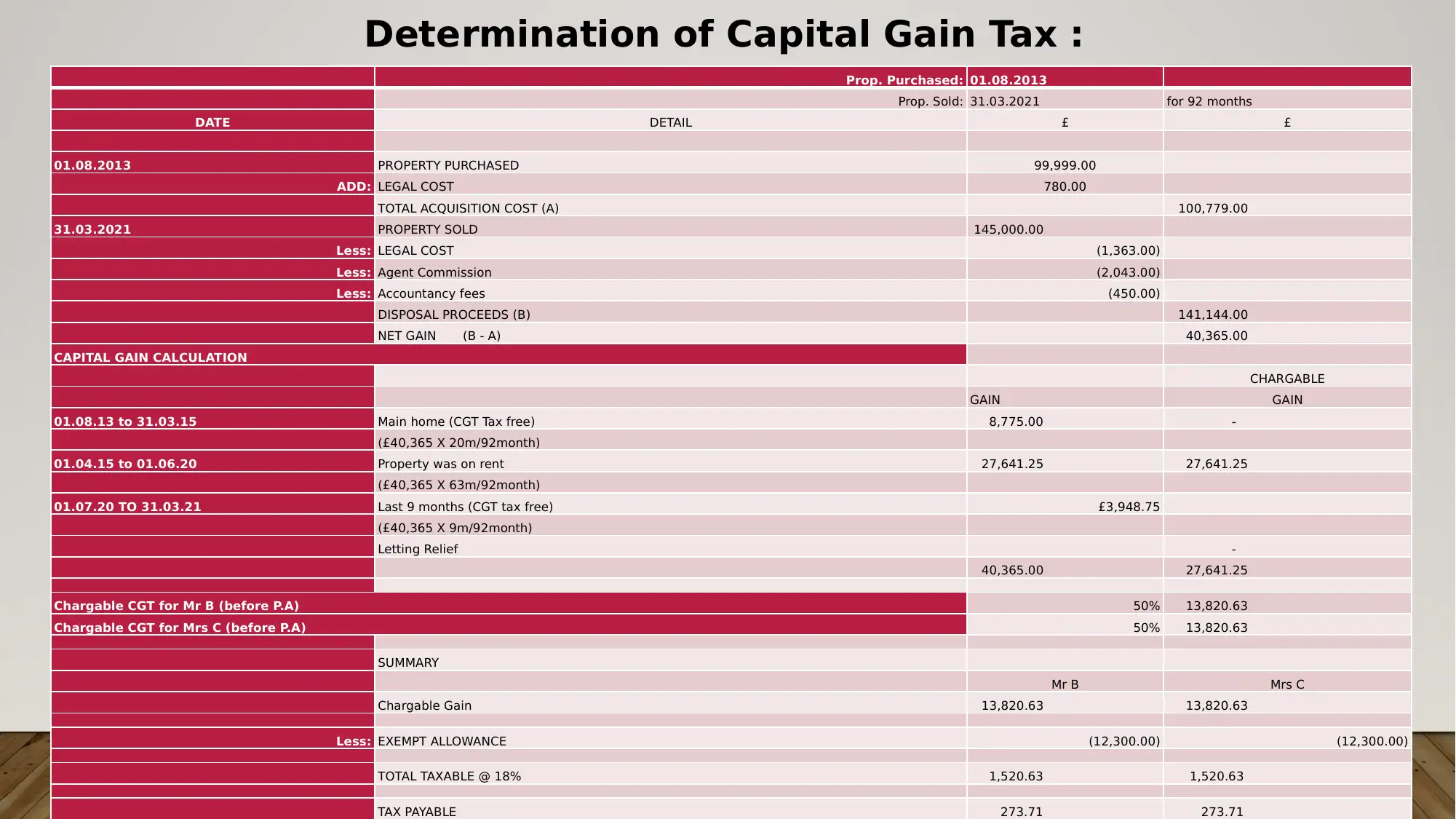

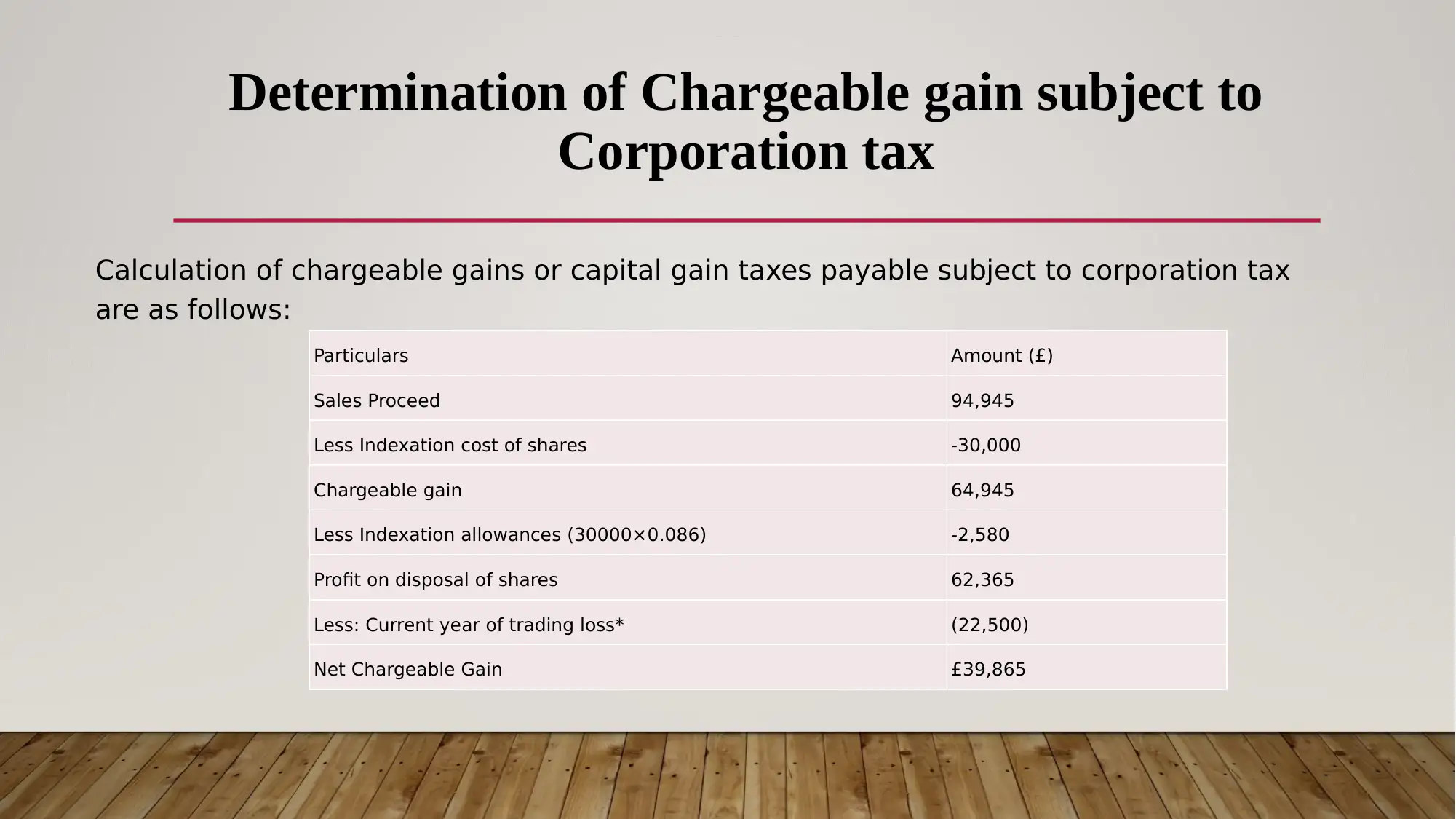

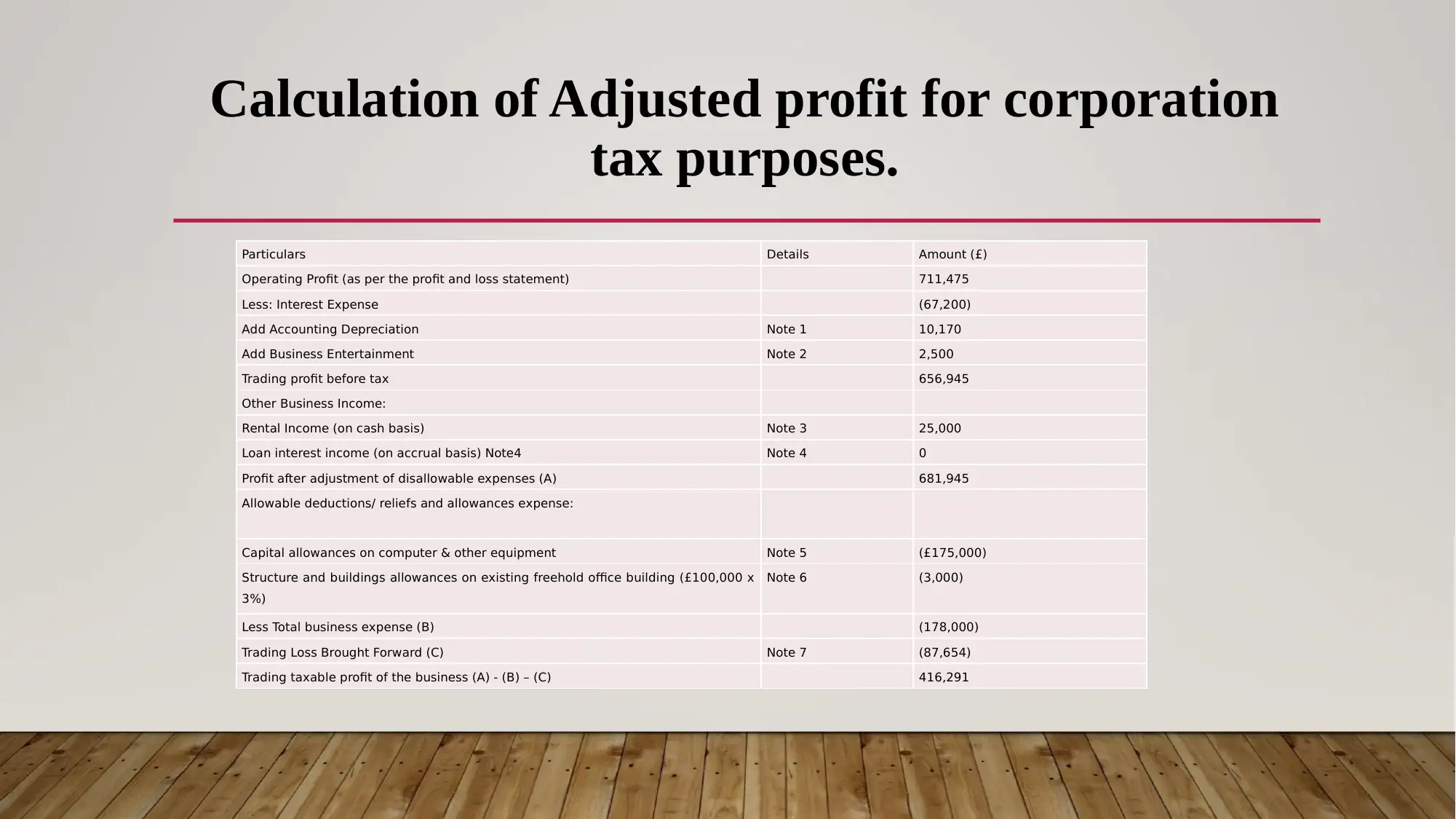

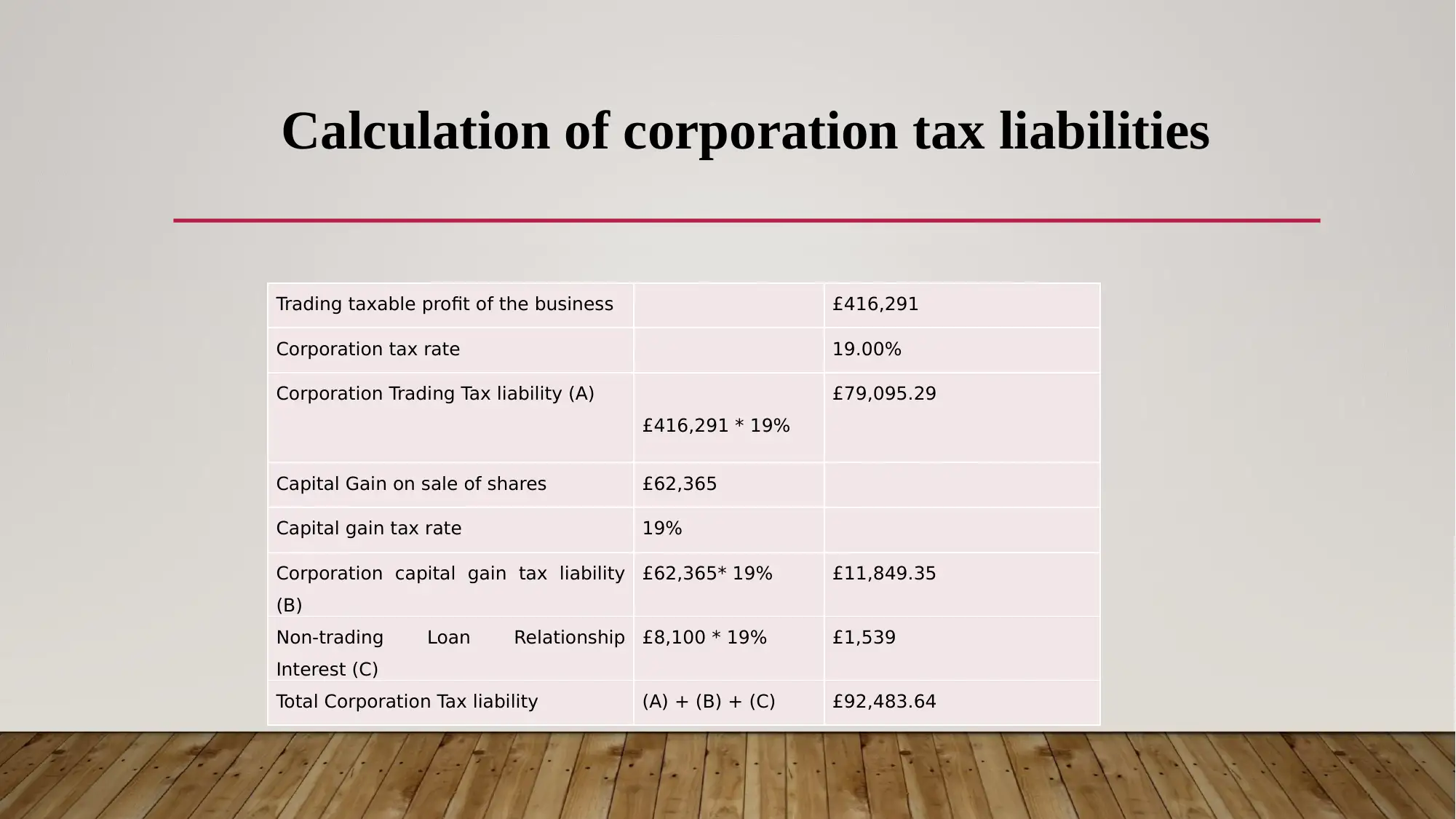

This report provides a detailed analysis of UK tax law and its implications for both unincorporated and incorporated businesses, focusing on corporation tax. It discusses the roles of HM Revenue and Customs (HMRC) and the various sources of tax revenue in the UK. The report highlights the differences in tax treatment between incorporated and unincorporated businesses, including corporation tax rates and self-assessment schemes. Furthermore, it delves into the determination of capital gains taxes payable, chargeable gains subject to corporation taxes, and the calculation of adjusted profit for corporation tax purposes. The document provides a comprehensive calculation of corporation tax liabilities, including trading taxable profit, capital gains, and non-trading loan relationships, offering a complete overview of corporate tax obligations in the UK. Desklib offers more solved assignments and resources for students.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.