Report: Profit Distribution and Performance of UK Food Manufacturers

VerifiedAdded on 2020/10/22

|13

|3636

|102

Report

AI Summary

This individual report provides a detailed analysis of the UK food manufacturing sector, examining various aspects of profitability and performance. The report begins with an introduction to data analysis and its application in understanding the food manufacturing sector. It analyzes profit distribution across organizations, comparing profit margins between SMEs and large companies, and evaluating return on shareholder funds. The study also explores the distribution of profit rates based on business activity, comparing food manufacturers with those engaged in other business activities. Furthermore, it investigates the relationship between the main activity of food manufacturers and business size using cross-tabulation. The analysis employs descriptive statistics, histograms, hypothesis tests, cross-tab analysis, correlation analysis, and bivariate regression to derive insights. The report concludes with a summary of findings and references used throughout the analysis.

INDIVIDUAL REPORT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A. Analysis of profit distribution across every organization..................................................1

B. Analysis of distribution of profit rate as compared to large and SME..............................2

C. Analysis of distribution of Return to shareholder funds as compared to large and SME food

manufacturers.........................................................................................................................3

D. Analysis of distribution of profit rate comparing with food manufacturers with type of

activity....................................................................................................................................5

E. Analysis of main activity of food manufacturer with reference to size of business..........6

F. Analysis of profit rate of all manufacturer associated with other quantitative variable....6

G. Analysing credit limit offered to UK food manufacturers with other quantitative variables.8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDICES...............................................................................................................................10

A...........................................................................................................................................10

E............................................................................................................................................10

G...........................................................................................................................................11

INTRODUCTION...........................................................................................................................1

A. Analysis of profit distribution across every organization..................................................1

B. Analysis of distribution of profit rate as compared to large and SME..............................2

C. Analysis of distribution of Return to shareholder funds as compared to large and SME food

manufacturers.........................................................................................................................3

D. Analysis of distribution of profit rate comparing with food manufacturers with type of

activity....................................................................................................................................5

E. Analysis of main activity of food manufacturer with reference to size of business..........6

F. Analysis of profit rate of all manufacturer associated with other quantitative variable....6

G. Analysing credit limit offered to UK food manufacturers with other quantitative variables.8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDICES...............................................................................................................................10

A...........................................................................................................................................10

E............................................................................................................................................10

G...........................................................................................................................................11

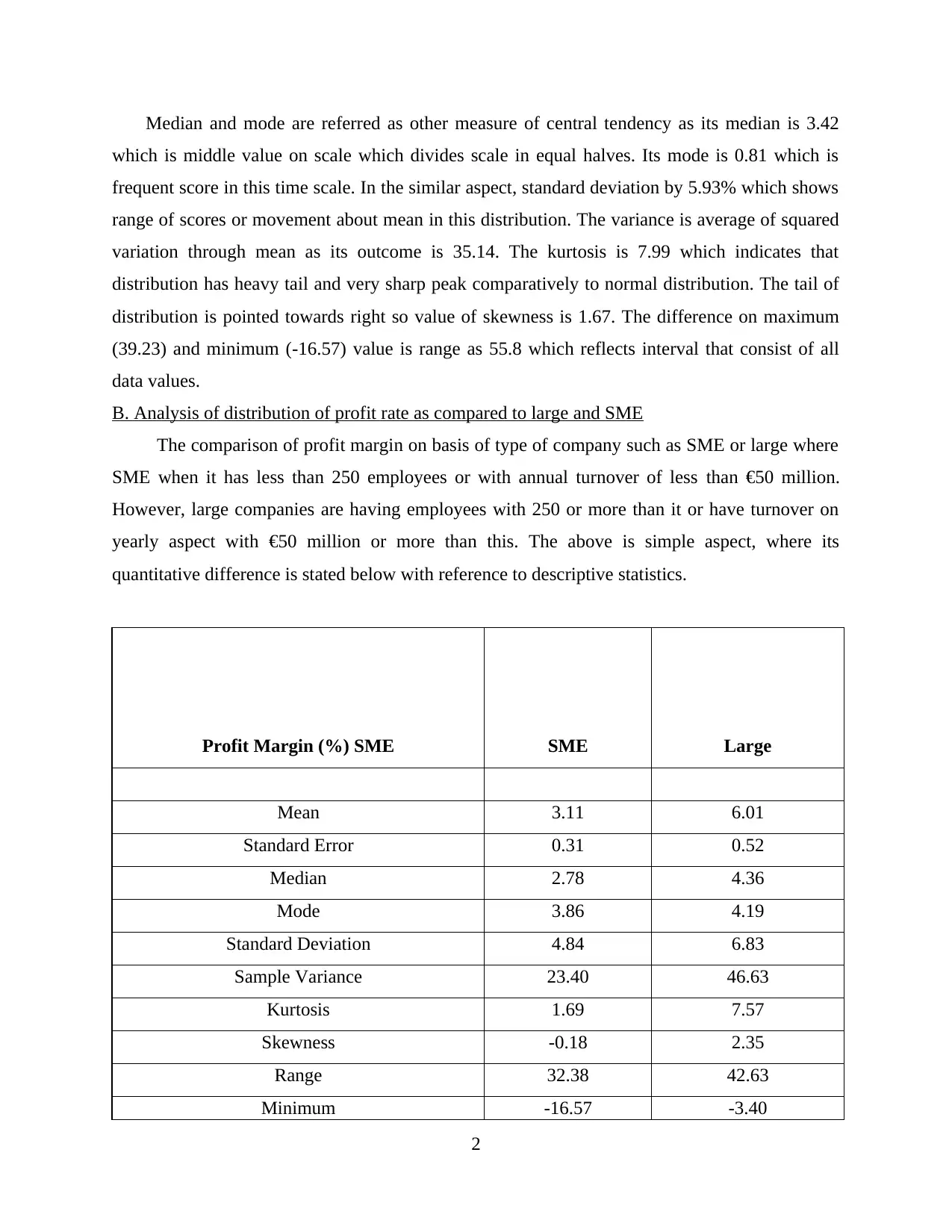

INTRODUCTION

Data analysis is considered as process of transforming, inspecting, modelling and cleansing

data with main objective for discovering important information, to support decision making

along with giving conclusion. The present report will discuss about food manufacturers who are

operating in United Kingdom along with consistent data on multiple variables. The main purpose

of this analysis is on basis of understanding food manufacturing sector to target future

investment. The variables of this data set are profit margin, number of employees, cost of

production, salaries as percentage turnover, credit limit, return on shareholders fund, business

activity, exporter and type of company. In this analysis, there will be implication of descriptive

statistics, histograms, hypothesis tests, cross tab analysis, correlation analysis and bivariate

regression with appropriate explanation.

A. Analysis of profit distribution across every organization

The profit margin is traced in percentage format and best measure for performance of

organization. The criteria for calculating this is profit after tax as percentage of turnover is also

known as sales revenue. While analysing the profit margin of all companies, standard measure

has been extracted for centre of distribution of sample as average of 4.33% in 411 observations.

The average could be distorted is there is presence of outliers from mean of various score in this

group (Mooi, Sarstedt and Mooi-Reci, 2018). In the same series, its measure of dispersion which

is somewhat same to standard deviation as it provides information related to dispersion of values

in sampling distribution linked with interest of population through which sample is framed. In

simple words, it reflects accuracy with sample shows population and it is about 0.30.

Figure 1 Histogram: Profit margin

1

Data analysis is considered as process of transforming, inspecting, modelling and cleansing

data with main objective for discovering important information, to support decision making

along with giving conclusion. The present report will discuss about food manufacturers who are

operating in United Kingdom along with consistent data on multiple variables. The main purpose

of this analysis is on basis of understanding food manufacturing sector to target future

investment. The variables of this data set are profit margin, number of employees, cost of

production, salaries as percentage turnover, credit limit, return on shareholders fund, business

activity, exporter and type of company. In this analysis, there will be implication of descriptive

statistics, histograms, hypothesis tests, cross tab analysis, correlation analysis and bivariate

regression with appropriate explanation.

A. Analysis of profit distribution across every organization

The profit margin is traced in percentage format and best measure for performance of

organization. The criteria for calculating this is profit after tax as percentage of turnover is also

known as sales revenue. While analysing the profit margin of all companies, standard measure

has been extracted for centre of distribution of sample as average of 4.33% in 411 observations.

The average could be distorted is there is presence of outliers from mean of various score in this

group (Mooi, Sarstedt and Mooi-Reci, 2018). In the same series, its measure of dispersion which

is somewhat same to standard deviation as it provides information related to dispersion of values

in sampling distribution linked with interest of population through which sample is framed. In

simple words, it reflects accuracy with sample shows population and it is about 0.30.

Figure 1 Histogram: Profit margin

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Median and mode are referred as other measure of central tendency as its median is 3.42

which is middle value on scale which divides scale in equal halves. Its mode is 0.81 which is

frequent score in this time scale. In the similar aspect, standard deviation by 5.93% which shows

range of scores or movement about mean in this distribution. The variance is average of squared

variation through mean as its outcome is 35.14. The kurtosis is 7.99 which indicates that

distribution has heavy tail and very sharp peak comparatively to normal distribution. The tail of

distribution is pointed towards right so value of skewness is 1.67. The difference on maximum

(39.23) and minimum (-16.57) value is range as 55.8 which reflects interval that consist of all

data values.

B. Analysis of distribution of profit rate as compared to large and SME

The comparison of profit margin on basis of type of company such as SME or large where

SME when it has less than 250 employees or with annual turnover of less than €50 million.

However, large companies are having employees with 250 or more than it or have turnover on

yearly aspect with €50 million or more than this. The above is simple aspect, where its

quantitative difference is stated below with reference to descriptive statistics.

Profit Margin (%) SME SME Large

Mean 3.11 6.01

Standard Error 0.31 0.52

Median 2.78 4.36

Mode 3.86 4.19

Standard Deviation 4.84 6.83

Sample Variance 23.40 46.63

Kurtosis 1.69 7.57

Skewness -0.18 2.35

Range 32.38 42.63

Minimum -16.57 -3.40

2

which is middle value on scale which divides scale in equal halves. Its mode is 0.81 which is

frequent score in this time scale. In the similar aspect, standard deviation by 5.93% which shows

range of scores or movement about mean in this distribution. The variance is average of squared

variation through mean as its outcome is 35.14. The kurtosis is 7.99 which indicates that

distribution has heavy tail and very sharp peak comparatively to normal distribution. The tail of

distribution is pointed towards right so value of skewness is 1.67. The difference on maximum

(39.23) and minimum (-16.57) value is range as 55.8 which reflects interval that consist of all

data values.

B. Analysis of distribution of profit rate as compared to large and SME

The comparison of profit margin on basis of type of company such as SME or large where

SME when it has less than 250 employees or with annual turnover of less than €50 million.

However, large companies are having employees with 250 or more than it or have turnover on

yearly aspect with €50 million or more than this. The above is simple aspect, where its

quantitative difference is stated below with reference to descriptive statistics.

Profit Margin (%) SME SME Large

Mean 3.11 6.01

Standard Error 0.31 0.52

Median 2.78 4.36

Mode 3.86 4.19

Standard Deviation 4.84 6.83

Sample Variance 23.40 46.63

Kurtosis 1.69 7.57

Skewness -0.18 2.35

Range 32.38 42.63

Minimum -16.57 -3.40

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

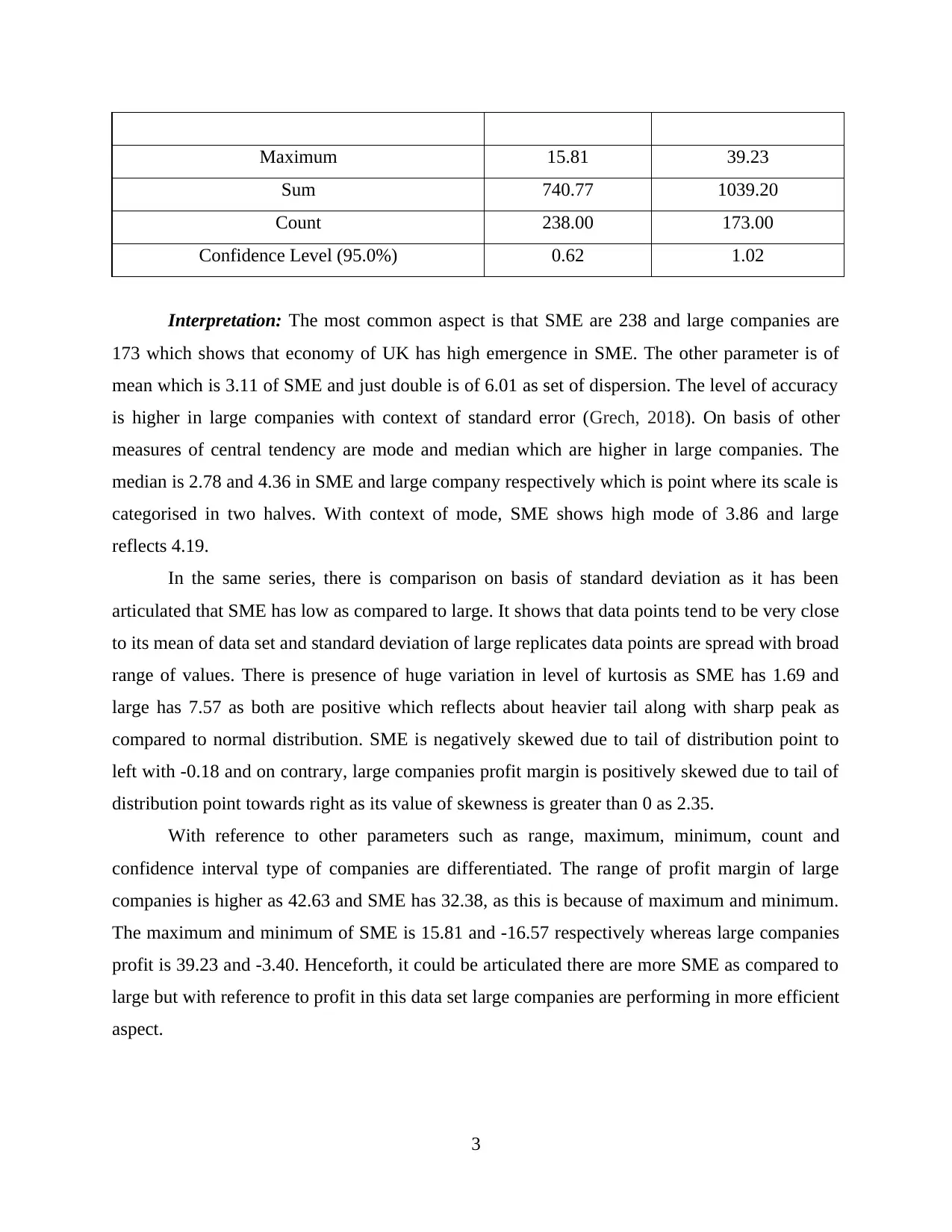

Maximum 15.81 39.23

Sum 740.77 1039.20

Count 238.00 173.00

Confidence Level (95.0%) 0.62 1.02

Interpretation: The most common aspect is that SME are 238 and large companies are

173 which shows that economy of UK has high emergence in SME. The other parameter is of

mean which is 3.11 of SME and just double is of 6.01 as set of dispersion. The level of accuracy

is higher in large companies with context of standard error (Grech, 2018). On basis of other

measures of central tendency are mode and median which are higher in large companies. The

median is 2.78 and 4.36 in SME and large company respectively which is point where its scale is

categorised in two halves. With context of mode, SME shows high mode of 3.86 and large

reflects 4.19.

In the same series, there is comparison on basis of standard deviation as it has been

articulated that SME has low as compared to large. It shows that data points tend to be very close

to its mean of data set and standard deviation of large replicates data points are spread with broad

range of values. There is presence of huge variation in level of kurtosis as SME has 1.69 and

large has 7.57 as both are positive which reflects about heavier tail along with sharp peak as

compared to normal distribution. SME is negatively skewed due to tail of distribution point to

left with -0.18 and on contrary, large companies profit margin is positively skewed due to tail of

distribution point towards right as its value of skewness is greater than 0 as 2.35.

With reference to other parameters such as range, maximum, minimum, count and

confidence interval type of companies are differentiated. The range of profit margin of large

companies is higher as 42.63 and SME has 32.38, as this is because of maximum and minimum.

The maximum and minimum of SME is 15.81 and -16.57 respectively whereas large companies

profit is 39.23 and -3.40. Henceforth, it could be articulated there are more SME as compared to

large but with reference to profit in this data set large companies are performing in more efficient

aspect.

3

Sum 740.77 1039.20

Count 238.00 173.00

Confidence Level (95.0%) 0.62 1.02

Interpretation: The most common aspect is that SME are 238 and large companies are

173 which shows that economy of UK has high emergence in SME. The other parameter is of

mean which is 3.11 of SME and just double is of 6.01 as set of dispersion. The level of accuracy

is higher in large companies with context of standard error (Grech, 2018). On basis of other

measures of central tendency are mode and median which are higher in large companies. The

median is 2.78 and 4.36 in SME and large company respectively which is point where its scale is

categorised in two halves. With context of mode, SME shows high mode of 3.86 and large

reflects 4.19.

In the same series, there is comparison on basis of standard deviation as it has been

articulated that SME has low as compared to large. It shows that data points tend to be very close

to its mean of data set and standard deviation of large replicates data points are spread with broad

range of values. There is presence of huge variation in level of kurtosis as SME has 1.69 and

large has 7.57 as both are positive which reflects about heavier tail along with sharp peak as

compared to normal distribution. SME is negatively skewed due to tail of distribution point to

left with -0.18 and on contrary, large companies profit margin is positively skewed due to tail of

distribution point towards right as its value of skewness is greater than 0 as 2.35.

With reference to other parameters such as range, maximum, minimum, count and

confidence interval type of companies are differentiated. The range of profit margin of large

companies is higher as 42.63 and SME has 32.38, as this is because of maximum and minimum.

The maximum and minimum of SME is 15.81 and -16.57 respectively whereas large companies

profit is 39.23 and -3.40. Henceforth, it could be articulated there are more SME as compared to

large but with reference to profit in this data set large companies are performing in more efficient

aspect.

3

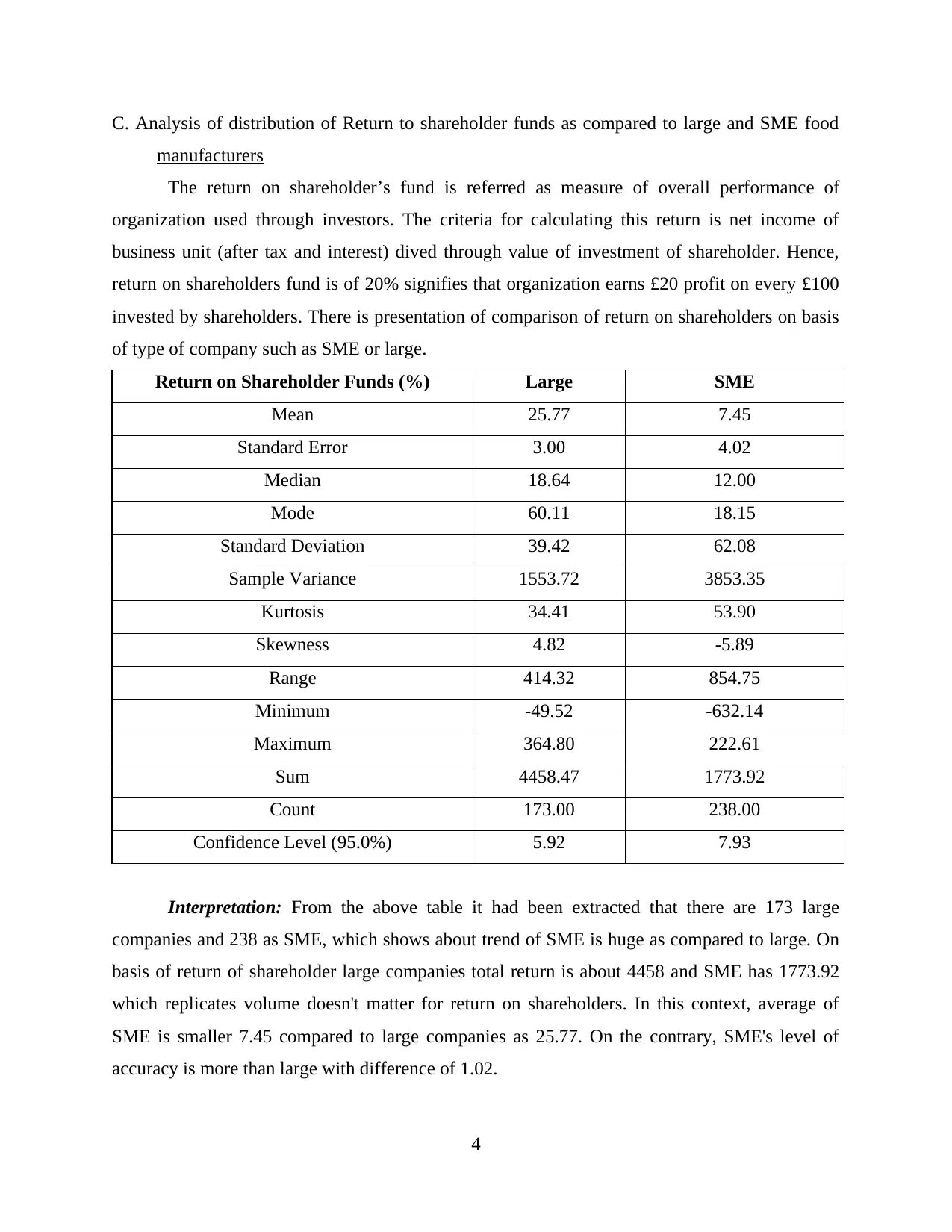

C. Analysis of distribution of Return to shareholder funds as compared to large and SME food

manufacturers

The return on shareholder’s fund is referred as measure of overall performance of

organization used through investors. The criteria for calculating this return is net income of

business unit (after tax and interest) dived through value of investment of shareholder. Hence,

return on shareholders fund is of 20% signifies that organization earns £20 profit on every £100

invested by shareholders. There is presentation of comparison of return on shareholders on basis

of type of company such as SME or large.

Return on Shareholder Funds (%) Large SME

Mean 25.77 7.45

Standard Error 3.00 4.02

Median 18.64 12.00

Mode 60.11 18.15

Standard Deviation 39.42 62.08

Sample Variance 1553.72 3853.35

Kurtosis 34.41 53.90

Skewness 4.82 -5.89

Range 414.32 854.75

Minimum -49.52 -632.14

Maximum 364.80 222.61

Sum 4458.47 1773.92

Count 173.00 238.00

Confidence Level (95.0%) 5.92 7.93

Interpretation: From the above table it had been extracted that there are 173 large

companies and 238 as SME, which shows about trend of SME is huge as compared to large. On

basis of return of shareholder large companies total return is about 4458 and SME has 1773.92

which replicates volume doesn't matter for return on shareholders. In this context, average of

SME is smaller 7.45 compared to large companies as 25.77. On the contrary, SME's level of

accuracy is more than large with difference of 1.02.

4

manufacturers

The return on shareholder’s fund is referred as measure of overall performance of

organization used through investors. The criteria for calculating this return is net income of

business unit (after tax and interest) dived through value of investment of shareholder. Hence,

return on shareholders fund is of 20% signifies that organization earns £20 profit on every £100

invested by shareholders. There is presentation of comparison of return on shareholders on basis

of type of company such as SME or large.

Return on Shareholder Funds (%) Large SME

Mean 25.77 7.45

Standard Error 3.00 4.02

Median 18.64 12.00

Mode 60.11 18.15

Standard Deviation 39.42 62.08

Sample Variance 1553.72 3853.35

Kurtosis 34.41 53.90

Skewness 4.82 -5.89

Range 414.32 854.75

Minimum -49.52 -632.14

Maximum 364.80 222.61

Sum 4458.47 1773.92

Count 173.00 238.00

Confidence Level (95.0%) 5.92 7.93

Interpretation: From the above table it had been extracted that there are 173 large

companies and 238 as SME, which shows about trend of SME is huge as compared to large. On

basis of return of shareholder large companies total return is about 4458 and SME has 1773.92

which replicates volume doesn't matter for return on shareholders. In this context, average of

SME is smaller 7.45 compared to large companies as 25.77. On the contrary, SME's level of

accuracy is more than large with difference of 1.02.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As mean, mode and median and referred as measure of central tendency as in these types

of companies as far variation among both as 60.11 is of large and 18.15 is of SME. Furthermore,

standard deviation helps in quantifying amount of variation or dispersion of set of multiple data

values (Popoola and et.al., 2018). In this aspect, large companies have risk of movement of 39.42

and SME has 62.08 far from the mean of dataset related to return on shareholders fund. While

measuring kurtosis, peakedness of distribution is measured of both SME and large where both

type of companies has positive outcome with heavier tail and sharp peak to normal distribution.

The value of skewness could be positive or negative where SME's return is negatively

skewed whose mean is left to the peak and large company's return is positively skewed as with

right skewed distribution. On basis of maximum and minimum, range is based with large and

SME of maximum and minimum return of shareholder and this all information is based on 95%

confidence interval of 5.92 in large and 7.93 in SME.

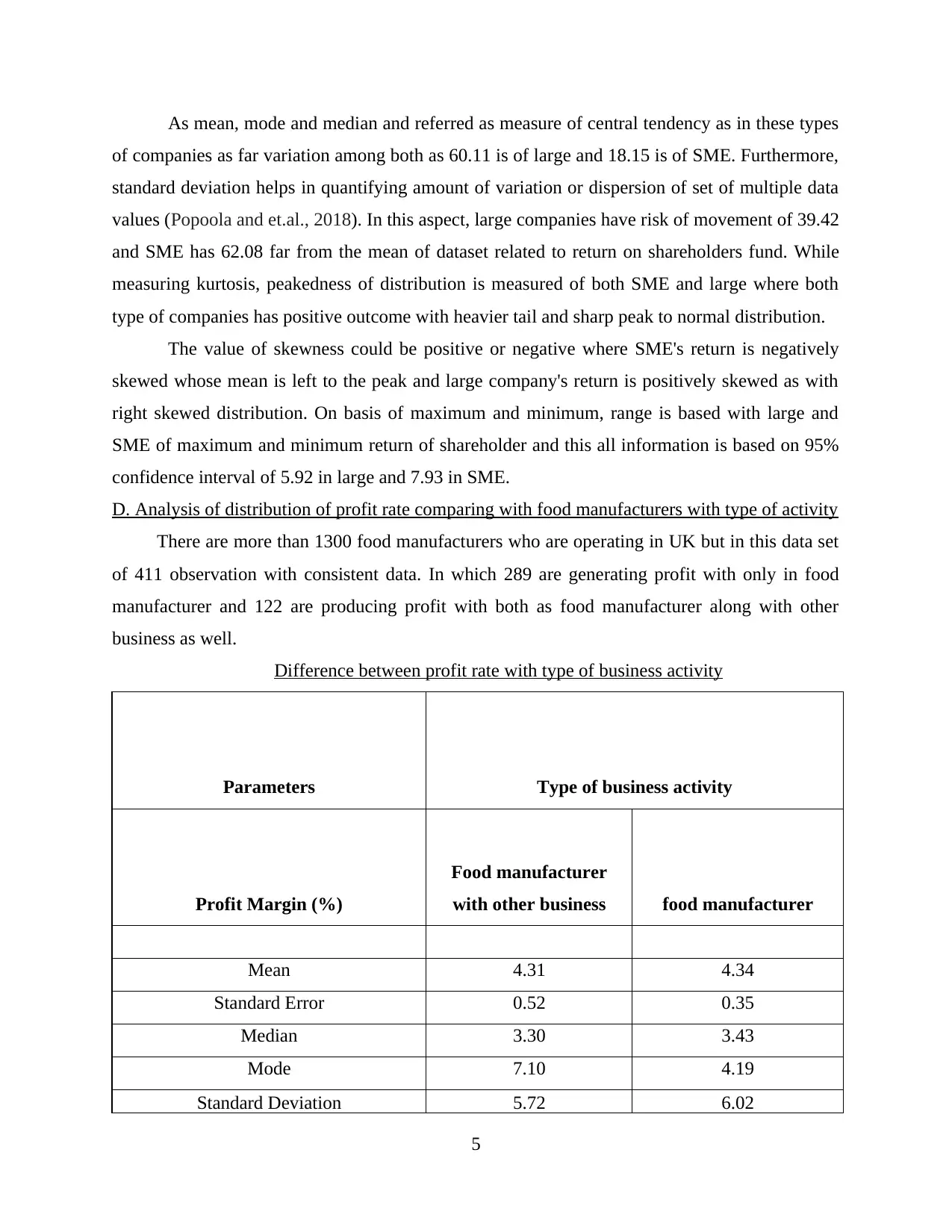

D. Analysis of distribution of profit rate comparing with food manufacturers with type of activity

There are more than 1300 food manufacturers who are operating in UK but in this data set

of 411 observation with consistent data. In which 289 are generating profit with only in food

manufacturer and 122 are producing profit with both as food manufacturer along with other

business as well.

Difference between profit rate with type of business activity

Parameters Type of business activity

Profit Margin (%)

Food manufacturer

with other business food manufacturer

Mean 4.31 4.34

Standard Error 0.52 0.35

Median 3.30 3.43

Mode 7.10 4.19

Standard Deviation 5.72 6.02

5

of companies as far variation among both as 60.11 is of large and 18.15 is of SME. Furthermore,

standard deviation helps in quantifying amount of variation or dispersion of set of multiple data

values (Popoola and et.al., 2018). In this aspect, large companies have risk of movement of 39.42

and SME has 62.08 far from the mean of dataset related to return on shareholders fund. While

measuring kurtosis, peakedness of distribution is measured of both SME and large where both

type of companies has positive outcome with heavier tail and sharp peak to normal distribution.

The value of skewness could be positive or negative where SME's return is negatively

skewed whose mean is left to the peak and large company's return is positively skewed as with

right skewed distribution. On basis of maximum and minimum, range is based with large and

SME of maximum and minimum return of shareholder and this all information is based on 95%

confidence interval of 5.92 in large and 7.93 in SME.

D. Analysis of distribution of profit rate comparing with food manufacturers with type of activity

There are more than 1300 food manufacturers who are operating in UK but in this data set

of 411 observation with consistent data. In which 289 are generating profit with only in food

manufacturer and 122 are producing profit with both as food manufacturer along with other

business as well.

Difference between profit rate with type of business activity

Parameters Type of business activity

Profit Margin (%)

Food manufacturer

with other business food manufacturer

Mean 4.31 4.34

Standard Error 0.52 0.35

Median 3.30 3.43

Mode 7.10 4.19

Standard Deviation 5.72 6.02

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sample Variance 32.71 36.28

Kurtosis 11.44 6.96

Skewness 2.56 1.37

Range 44.26 55.80

Minimum -5.92 -16.57

Maximum 38.34 39.23

Sum 525.30 1254.67

Count 122.00 289.00

Confidence Level (95.0%) 1.03 0.70

From the above analysis, it had been articulated that average of profit rate of both type of

business activity is similar to each other. By estimating level of accuracy with context to

standard error as only with food manufacturer is 0.35 which is lower than combination with other

business as 0.52. Undertaking other measure of central tendency is mode and median where

median is similar to both business activity. With reference to mode, profit rate percentage is

higher with mix of other business activity as 7.10 and food manufacturer with 4.19.

By considering sample variance and standard deviation, only food manufacturer has the

highest risk or amount far from mean. The kurtosis measure of both business activities is positive

will have sharp peak and heavy tail for distribution along with positive skewness or right skewed

distribution (Odukoya and et.al., 2018). In the same series, range of business activities are

dependent on maximum and minimum as highest is approx. similar but lowest of food

manufacturer is -16.57 and mix of other business has -5.92. Henceforth, it could be evaluated

that food manufacturer has total profit 1254.67 and combination has 525.30 so, they should

provide special focus on their core activity because its confidence level is also higher 1.03

against 0.70.

E. Analysis of main activity of food manufacturer with reference to size of business

The main activity of food manufacturer against business size has been categorised with

application of cross tabulation. Cross tabulation is referred as tool used for comparing

relationship among two variables. In this dataset there are two variables size as large and SME

6

Kurtosis 11.44 6.96

Skewness 2.56 1.37

Range 44.26 55.80

Minimum -5.92 -16.57

Maximum 38.34 39.23

Sum 525.30 1254.67

Count 122.00 289.00

Confidence Level (95.0%) 1.03 0.70

From the above analysis, it had been articulated that average of profit rate of both type of

business activity is similar to each other. By estimating level of accuracy with context to

standard error as only with food manufacturer is 0.35 which is lower than combination with other

business as 0.52. Undertaking other measure of central tendency is mode and median where

median is similar to both business activity. With reference to mode, profit rate percentage is

higher with mix of other business activity as 7.10 and food manufacturer with 4.19.

By considering sample variance and standard deviation, only food manufacturer has the

highest risk or amount far from mean. The kurtosis measure of both business activities is positive

will have sharp peak and heavy tail for distribution along with positive skewness or right skewed

distribution (Odukoya and et.al., 2018). In the same series, range of business activities are

dependent on maximum and minimum as highest is approx. similar but lowest of food

manufacturer is -16.57 and mix of other business has -5.92. Henceforth, it could be evaluated

that food manufacturer has total profit 1254.67 and combination has 525.30 so, they should

provide special focus on their core activity because its confidence level is also higher 1.03

against 0.70.

E. Analysis of main activity of food manufacturer with reference to size of business

The main activity of food manufacturer against business size has been categorised with

application of cross tabulation. Cross tabulation is referred as tool used for comparing

relationship among two variables. In this dataset there are two variables size as large and SME

6

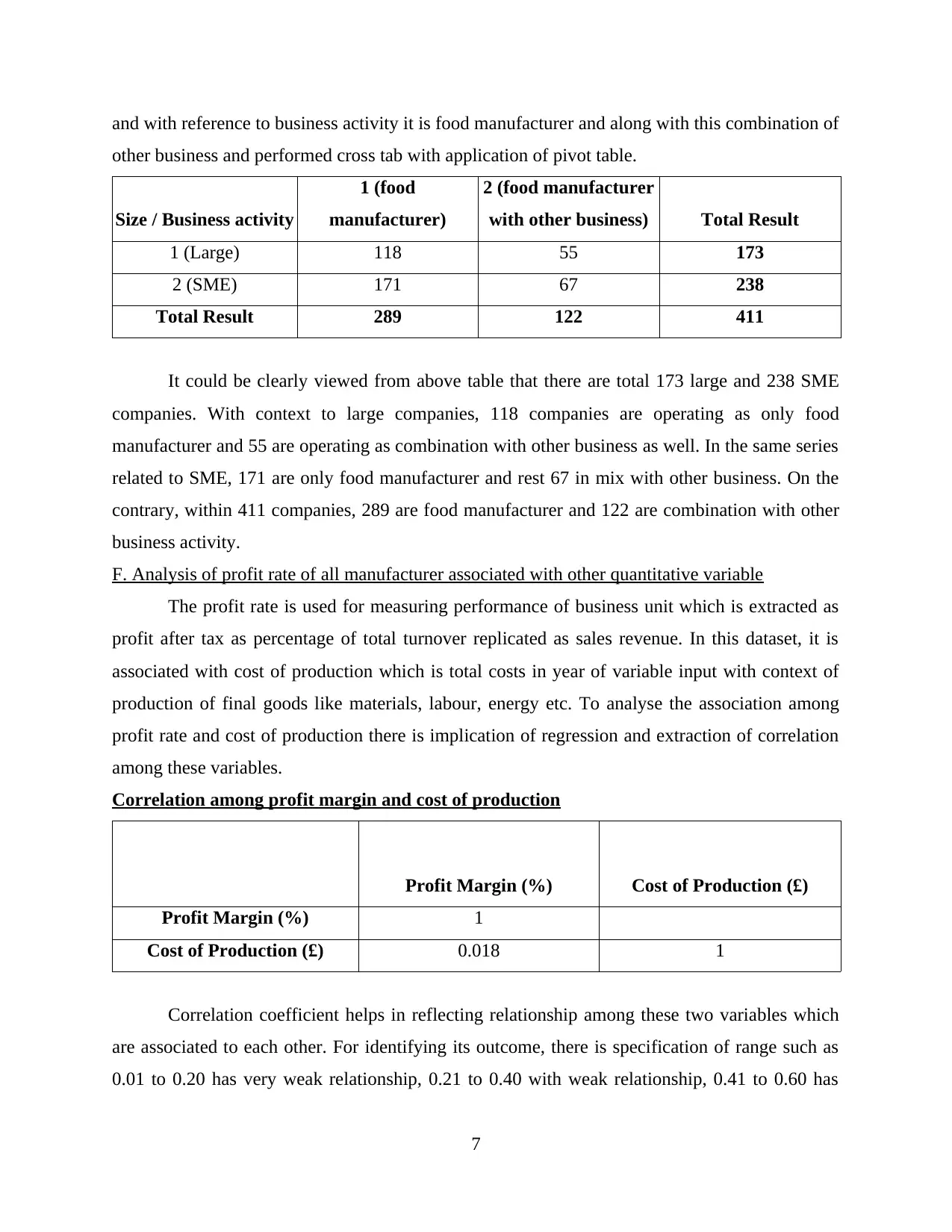

and with reference to business activity it is food manufacturer and along with this combination of

other business and performed cross tab with application of pivot table.

Size / Business activity

1 (food

manufacturer)

2 (food manufacturer

with other business) Total Result

1 (Large) 118 55 173

2 (SME) 171 67 238

Total Result 289 122 411

It could be clearly viewed from above table that there are total 173 large and 238 SME

companies. With context to large companies, 118 companies are operating as only food

manufacturer and 55 are operating as combination with other business as well. In the same series

related to SME, 171 are only food manufacturer and rest 67 in mix with other business. On the

contrary, within 411 companies, 289 are food manufacturer and 122 are combination with other

business activity.

F. Analysis of profit rate of all manufacturer associated with other quantitative variable

The profit rate is used for measuring performance of business unit which is extracted as

profit after tax as percentage of total turnover replicated as sales revenue. In this dataset, it is

associated with cost of production which is total costs in year of variable input with context of

production of final goods like materials, labour, energy etc. To analyse the association among

profit rate and cost of production there is implication of regression and extraction of correlation

among these variables.

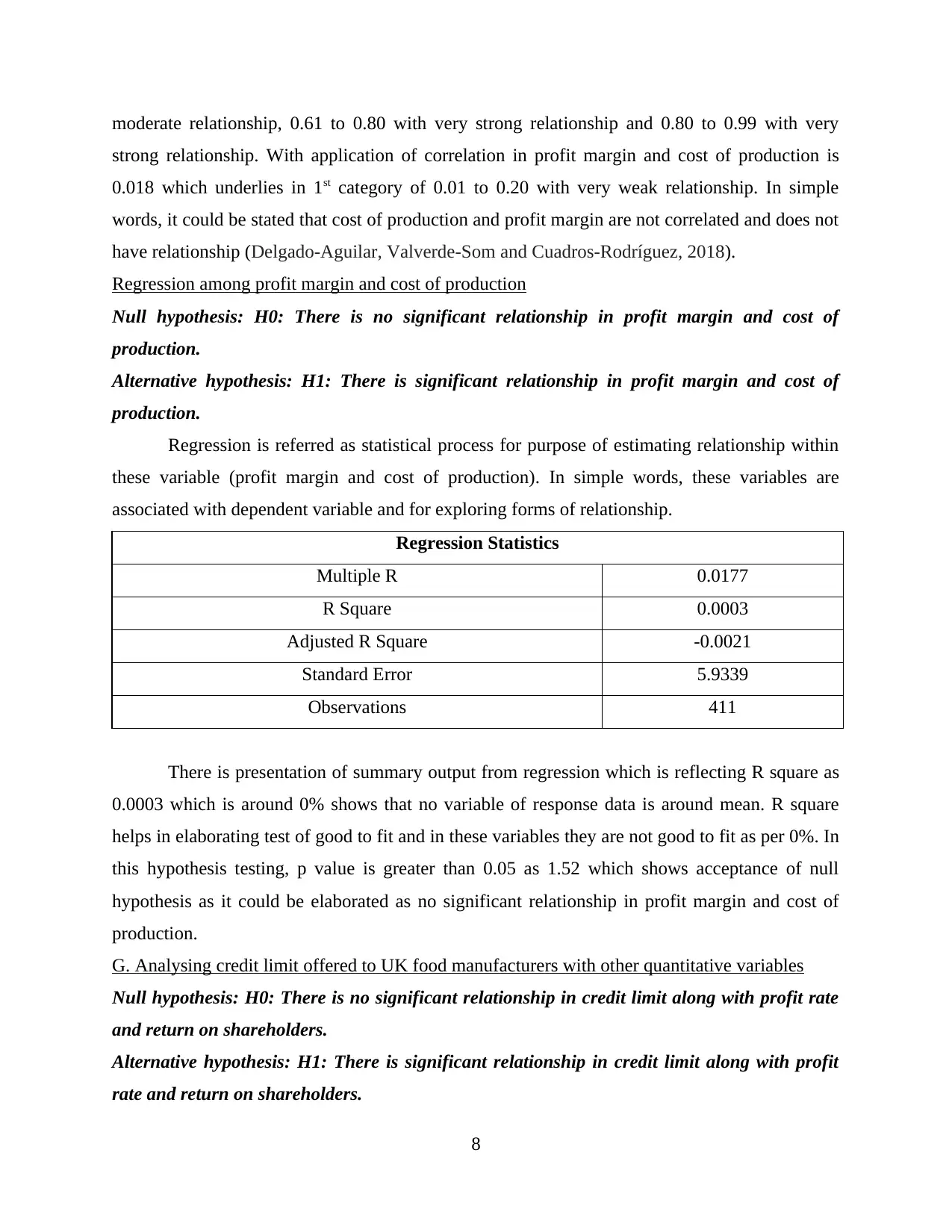

Correlation among profit margin and cost of production

Profit Margin (%) Cost of Production (£)

Profit Margin (%) 1

Cost of Production (£) 0.018 1

Correlation coefficient helps in reflecting relationship among these two variables which

are associated to each other. For identifying its outcome, there is specification of range such as

0.01 to 0.20 has very weak relationship, 0.21 to 0.40 with weak relationship, 0.41 to 0.60 has

7

other business and performed cross tab with application of pivot table.

Size / Business activity

1 (food

manufacturer)

2 (food manufacturer

with other business) Total Result

1 (Large) 118 55 173

2 (SME) 171 67 238

Total Result 289 122 411

It could be clearly viewed from above table that there are total 173 large and 238 SME

companies. With context to large companies, 118 companies are operating as only food

manufacturer and 55 are operating as combination with other business as well. In the same series

related to SME, 171 are only food manufacturer and rest 67 in mix with other business. On the

contrary, within 411 companies, 289 are food manufacturer and 122 are combination with other

business activity.

F. Analysis of profit rate of all manufacturer associated with other quantitative variable

The profit rate is used for measuring performance of business unit which is extracted as

profit after tax as percentage of total turnover replicated as sales revenue. In this dataset, it is

associated with cost of production which is total costs in year of variable input with context of

production of final goods like materials, labour, energy etc. To analyse the association among

profit rate and cost of production there is implication of regression and extraction of correlation

among these variables.

Correlation among profit margin and cost of production

Profit Margin (%) Cost of Production (£)

Profit Margin (%) 1

Cost of Production (£) 0.018 1

Correlation coefficient helps in reflecting relationship among these two variables which

are associated to each other. For identifying its outcome, there is specification of range such as

0.01 to 0.20 has very weak relationship, 0.21 to 0.40 with weak relationship, 0.41 to 0.60 has

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

moderate relationship, 0.61 to 0.80 with very strong relationship and 0.80 to 0.99 with very

strong relationship. With application of correlation in profit margin and cost of production is

0.018 which underlies in 1st category of 0.01 to 0.20 with very weak relationship. In simple

words, it could be stated that cost of production and profit margin are not correlated and does not

have relationship (Delgado-Aguilar, Valverde-Som and Cuadros-Rodríguez, 2018).

Regression among profit margin and cost of production

Null hypothesis: H0: There is no significant relationship in profit margin and cost of

production.

Alternative hypothesis: H1: There is significant relationship in profit margin and cost of

production.

Regression is referred as statistical process for purpose of estimating relationship within

these variable (profit margin and cost of production). In simple words, these variables are

associated with dependent variable and for exploring forms of relationship.

Regression Statistics

Multiple R 0.0177

R Square 0.0003

Adjusted R Square -0.0021

Standard Error 5.9339

Observations 411

There is presentation of summary output from regression which is reflecting R square as

0.0003 which is around 0% shows that no variable of response data is around mean. R square

helps in elaborating test of good to fit and in these variables they are not good to fit as per 0%. In

this hypothesis testing, p value is greater than 0.05 as 1.52 which shows acceptance of null

hypothesis as it could be elaborated as no significant relationship in profit margin and cost of

production.

G. Analysing credit limit offered to UK food manufacturers with other quantitative variables

Null hypothesis: H0: There is no significant relationship in credit limit along with profit rate

and return on shareholders.

Alternative hypothesis: H1: There is significant relationship in credit limit along with profit

rate and return on shareholders.

8

strong relationship. With application of correlation in profit margin and cost of production is

0.018 which underlies in 1st category of 0.01 to 0.20 with very weak relationship. In simple

words, it could be stated that cost of production and profit margin are not correlated and does not

have relationship (Delgado-Aguilar, Valverde-Som and Cuadros-Rodríguez, 2018).

Regression among profit margin and cost of production

Null hypothesis: H0: There is no significant relationship in profit margin and cost of

production.

Alternative hypothesis: H1: There is significant relationship in profit margin and cost of

production.

Regression is referred as statistical process for purpose of estimating relationship within

these variable (profit margin and cost of production). In simple words, these variables are

associated with dependent variable and for exploring forms of relationship.

Regression Statistics

Multiple R 0.0177

R Square 0.0003

Adjusted R Square -0.0021

Standard Error 5.9339

Observations 411

There is presentation of summary output from regression which is reflecting R square as

0.0003 which is around 0% shows that no variable of response data is around mean. R square

helps in elaborating test of good to fit and in these variables they are not good to fit as per 0%. In

this hypothesis testing, p value is greater than 0.05 as 1.52 which shows acceptance of null

hypothesis as it could be elaborated as no significant relationship in profit margin and cost of

production.

G. Analysing credit limit offered to UK food manufacturers with other quantitative variables

Null hypothesis: H0: There is no significant relationship in credit limit along with profit rate

and return on shareholders.

Alternative hypothesis: H1: There is significant relationship in credit limit along with profit

rate and return on shareholders.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.2738

R Square 0.0749

Adjusted R Square 0.0704

Standard Error 4881964.13

Observations 411

The credit limit is referred as predicted estimate of total amount of outstanding credit on

organization which is derived through market data, financial status and likelihood insolvency

over next 1 year (Martin and et.al, 2018). While observing predicted credit limit is associated

with profit margin and return on shareholders fund. In the above analysis, it had extracted about

positive relationship as good to fit test is about 7.50%. Here P value is 0.01 which shows it is

smaller than 0.05 then alternative hypothesis is accepted. It could be elaborated that there is

significant relationship in credit limit along with profit rate and return on shareholders.

CONCLUSION

On basis of above report, it could be concluded that food industry is attaining huge profit as

per dataset of year 2017. With reference to performance, it had attained best position by

comparing it from other business activities. In this total companies are 411 with average profit

percentage is 4.33 which is acceptable in which large companies are performing in efficient

aspect with 0.62 of 95% confidence interval.

REFERENCES

Books and Journals

Delgado-Aguilar, M., Valverde-Som, L. and Cuadros-Rodríguez, L., 2018. Solver, an Excel

application to solve the difficulty in applying different univariate linear regression

methods. Chemometrics and Intelligent Laboratory Systems. 178. pp.39-46.

Grech, V., 2018. WASP (Write a Scientific Paper) using Excel–6: Standard error and confidence

interval. Early human development. 118. pp.61-63.

Martin, C. B., and et.al, 2018. Performing data mining operations within a columnar database

management system. U.S. Patent Application 15/714,358.

9

Regression Statistics

Multiple R 0.2738

R Square 0.0749

Adjusted R Square 0.0704

Standard Error 4881964.13

Observations 411

The credit limit is referred as predicted estimate of total amount of outstanding credit on

organization which is derived through market data, financial status and likelihood insolvency

over next 1 year (Martin and et.al, 2018). While observing predicted credit limit is associated

with profit margin and return on shareholders fund. In the above analysis, it had extracted about

positive relationship as good to fit test is about 7.50%. Here P value is 0.01 which shows it is

smaller than 0.05 then alternative hypothesis is accepted. It could be elaborated that there is

significant relationship in credit limit along with profit rate and return on shareholders.

CONCLUSION

On basis of above report, it could be concluded that food industry is attaining huge profit as

per dataset of year 2017. With reference to performance, it had attained best position by

comparing it from other business activities. In this total companies are 411 with average profit

percentage is 4.33 which is acceptable in which large companies are performing in efficient

aspect with 0.62 of 95% confidence interval.

REFERENCES

Books and Journals

Delgado-Aguilar, M., Valverde-Som, L. and Cuadros-Rodríguez, L., 2018. Solver, an Excel

application to solve the difficulty in applying different univariate linear regression

methods. Chemometrics and Intelligent Laboratory Systems. 178. pp.39-46.

Grech, V., 2018. WASP (Write a Scientific Paper) using Excel–6: Standard error and confidence

interval. Early human development. 118. pp.61-63.

Martin, C. B., and et.al, 2018. Performing data mining operations within a columnar database

management system. U.S. Patent Application 15/714,358.

9

Mooi, E., Sarstedt, M. and Mooi-Reci, I., 2018. Descriptive Statistics. In Market Research (pp.

95-152). Springer, Singapore.

Odukoya, J. A. and et.al., 2018. Learning analytics: Dataset for empirical evaluation of entry

requirements into engineering undergraduate programs in a Nigerian university. Data in

brief. 17. pp.998-1014.

Popoola, S. I. and et.al., 2018. Learning analytics for smart campus: data on academic

performances of engineering undergraduates in Nigerian private university. Data in

brief. 17. pp.76-94.

10

95-152). Springer, Singapore.

Odukoya, J. A. and et.al., 2018. Learning analytics: Dataset for empirical evaluation of entry

requirements into engineering undergraduate programs in a Nigerian university. Data in

brief. 17. pp.998-1014.

Popoola, S. I. and et.al., 2018. Learning analytics for smart campus: data on academic

performances of engineering undergraduates in Nigerian private university. Data in

brief. 17. pp.76-94.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.