Analysis of UK Housing Market: 2009-2019 and COVID-19 Impact

VerifiedAdded on 2023/01/11

|13

|3757

|83

Report

AI Summary

This report provides a comprehensive analysis of the UK housing market, examining the changes in average house prices between 2009 and 2019. It delves into the economic determinants influencing these changes, including affordability, consumer confidence, interest rates, population growth, mortgage availability, and economic growth. The report further assesses the impact of government actions and policies on the UK housing market during this period. Finally, it offers predictions on the potential effects of the COVID-19 pandemic on the UK housing market, considering historical trends and the current economic climate. The report covers various factors like inflation, interest rates, population growth, and mortgage availability, offering a holistic view of the market dynamics. The analysis emphasizes the cyclical nature of the housing market and its sensitivity to economic fluctuations and government interventions. The report concludes by synthesizing the findings and offering insights into the future trajectory of the UK housing market.

Internal and external business

environment

environment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

How have average house prices in the UK changed over the period 2009-2019........................3

What are the economic determinants of the changes outlined in your own answer to Question

1...................................................................................................................................................5

How has the government action over the period 2009-2019 affected the UK housing market...7

Predict what would be the impact of COVID-19 on UK housing market...................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

How have average house prices in the UK changed over the period 2009-2019........................3

What are the economic determinants of the changes outlined in your own answer to Question

1...................................................................................................................................................5

How has the government action over the period 2009-2019 affected the UK housing market...7

Predict what would be the impact of COVID-19 on UK housing market...................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

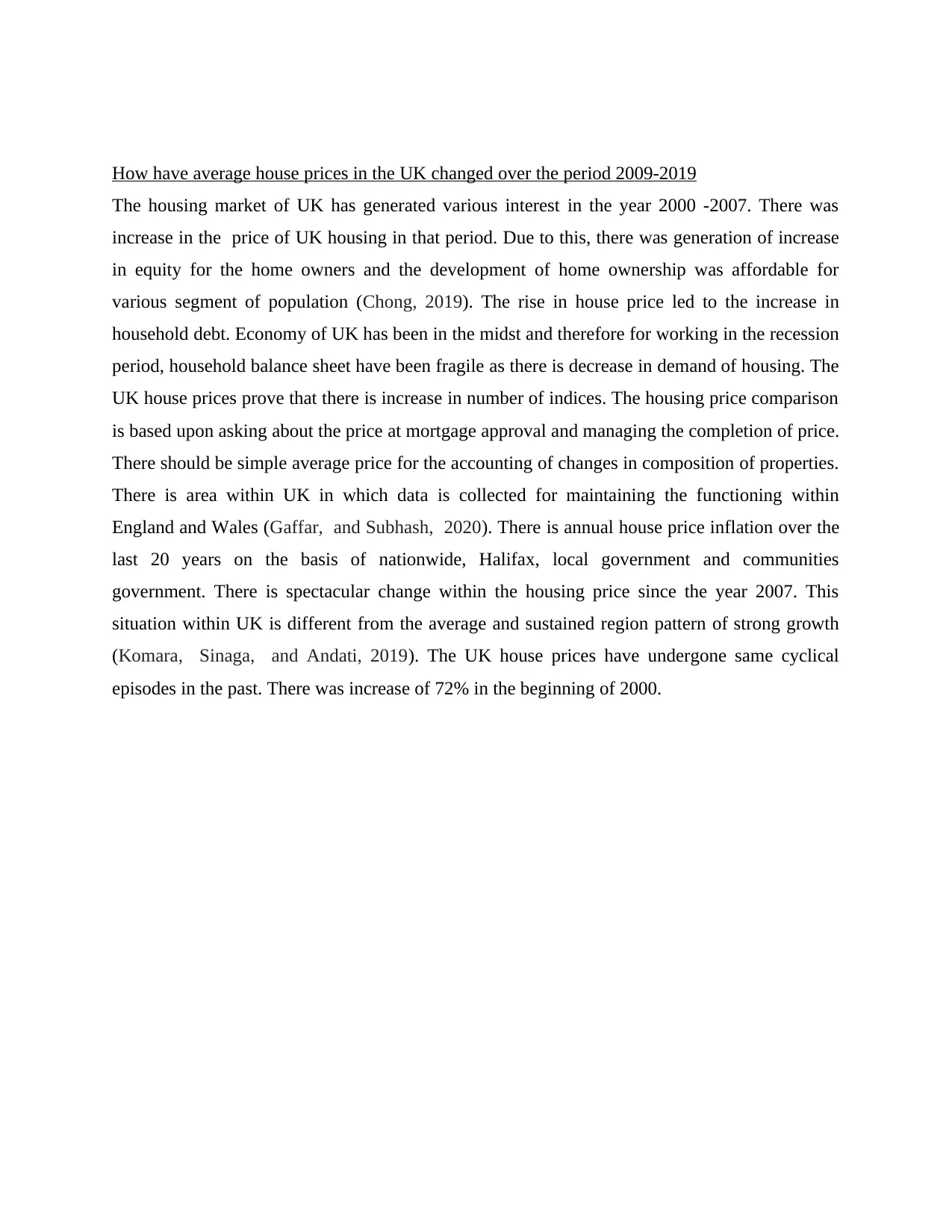

How have average house prices in the UK changed over the period 2009-2019

The housing market of UK has generated various interest in the year 2000 -2007. There was

increase in the price of UK housing in that period. Due to this, there was generation of increase

in equity for the home owners and the development of home ownership was affordable for

various segment of population (Chong, 2019). The rise in house price led to the increase in

household debt. Economy of UK has been in the midst and therefore for working in the recession

period, household balance sheet have been fragile as there is decrease in demand of housing. The

UK house prices prove that there is increase in number of indices. The housing price comparison

is based upon asking about the price at mortgage approval and managing the completion of price.

There should be simple average price for the accounting of changes in composition of properties.

There is area within UK in which data is collected for maintaining the functioning within

England and Wales (Gaffar, and Subhash, 2020). There is annual house price inflation over the

last 20 years on the basis of nationwide, Halifax, local government and communities

government. There is spectacular change within the housing price since the year 2007. This

situation within UK is different from the average and sustained region pattern of strong growth

(Komara, Sinaga, and Andati, 2019). The UK house prices have undergone same cyclical

episodes in the past. There was increase of 72% in the beginning of 2000.

The housing market of UK has generated various interest in the year 2000 -2007. There was

increase in the price of UK housing in that period. Due to this, there was generation of increase

in equity for the home owners and the development of home ownership was affordable for

various segment of population (Chong, 2019). The rise in house price led to the increase in

household debt. Economy of UK has been in the midst and therefore for working in the recession

period, household balance sheet have been fragile as there is decrease in demand of housing. The

UK house prices prove that there is increase in number of indices. The housing price comparison

is based upon asking about the price at mortgage approval and managing the completion of price.

There should be simple average price for the accounting of changes in composition of properties.

There is area within UK in which data is collected for maintaining the functioning within

England and Wales (Gaffar, and Subhash, 2020). There is annual house price inflation over the

last 20 years on the basis of nationwide, Halifax, local government and communities

government. There is spectacular change within the housing price since the year 2007. This

situation within UK is different from the average and sustained region pattern of strong growth

(Komara, Sinaga, and Andati, 2019). The UK house prices have undergone same cyclical

episodes in the past. There was increase of 72% in the beginning of 2000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Periods in which nominal prices have arrived sharply and days have to be managed within the

small scale. Halifax and nationwide house price have to be worked in real terms and they have to

be managed effectively (Lund, and Måseidvåg, 2018). There was inflation rate which was

calculated by the analysis of difference between nominal and real house price inflation. This

must be close to the official retail price index as it will help in in analysing the relative long term

leverage ratio. This is related with long term ratio which is indicated for sustainable level of

house pricing. It is concluded that earning distribution has been differentiated from the higher

ratio as it will provide help in knowing about why house prices are increased. There is

relationship between earnings and house prices (Pearson, 2017). According to the statistics,

there is an equilibrium ratio between pricing of house and earning of people. This can be

explained with an example that if the relationship is changed due to structural shifts in credit

availability then the interest rate will resign.

small scale. Halifax and nationwide house price have to be worked in real terms and they have to

be managed effectively (Lund, and Måseidvåg, 2018). There was inflation rate which was

calculated by the analysis of difference between nominal and real house price inflation. This

must be close to the official retail price index as it will help in in analysing the relative long term

leverage ratio. This is related with long term ratio which is indicated for sustainable level of

house pricing. It is concluded that earning distribution has been differentiated from the higher

ratio as it will provide help in knowing about why house prices are increased. There is

relationship between earnings and house prices (Pearson, 2017). According to the statistics,

there is an equilibrium ratio between pricing of house and earning of people. This can be

explained with an example that if the relationship is changed due to structural shifts in credit

availability then the interest rate will resign.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

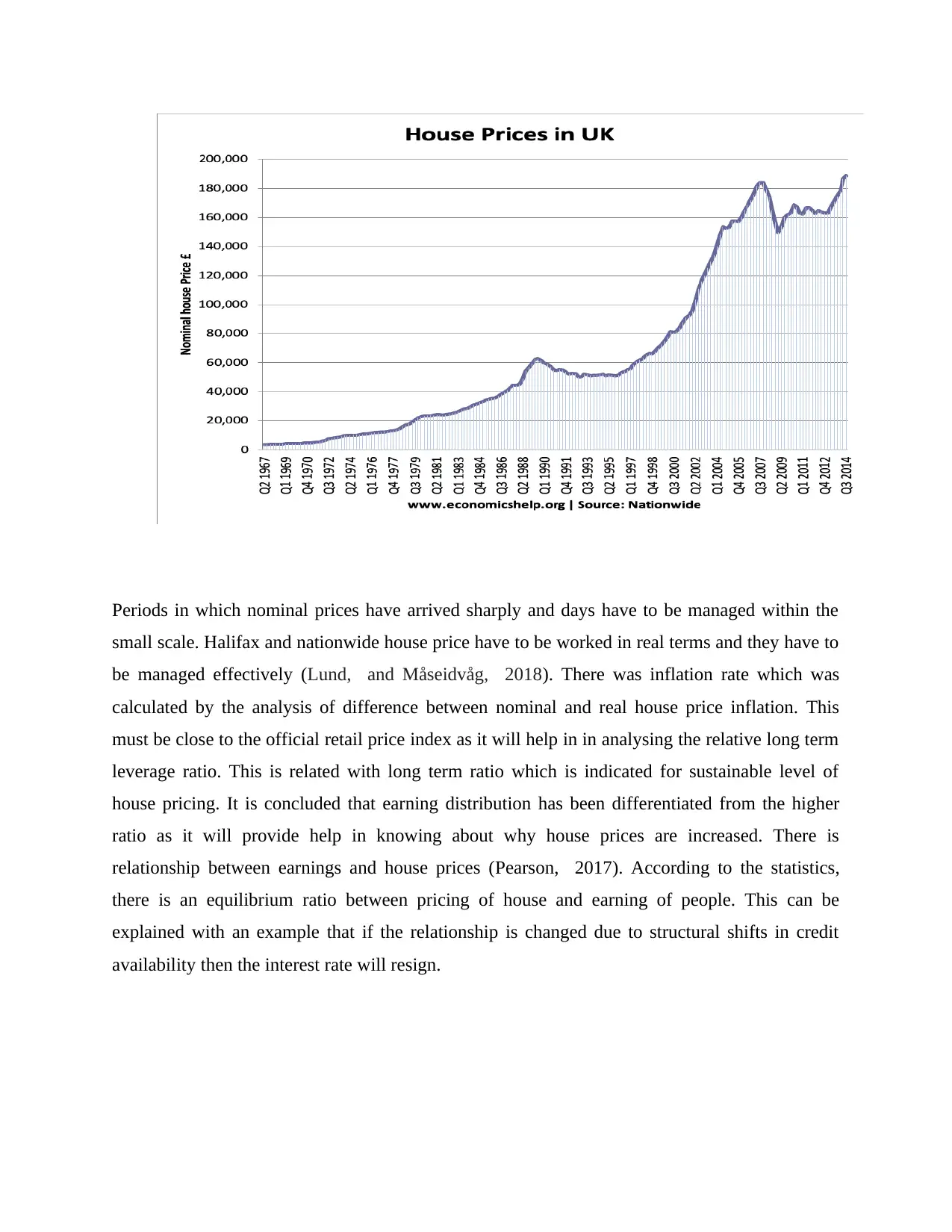

What are the economic determinants of the changes outlined in your own answer to Question 1

There are various factors related to economy which affects the average housing price within UK.

There are different elements related to supply and demand of housing which have to be

considered for analysing the condition of UK housing (Ren, and et. al., 2017). Some of the

factors are mentioned below-

Affordability – this is related with the rise in income of the people which has affected the

housing rent as well as house constructions directly. As there is economic growth and

development, the demand for house is also increased. There is also demand for housing

which bends towards the luxurious goods. When the earning of people is more, the

housing rent and allowances are also increased as they are in high demand. The house

There are various factors related to economy which affects the average housing price within UK.

There are different elements related to supply and demand of housing which have to be

considered for analysing the condition of UK housing (Ren, and et. al., 2017). Some of the

factors are mentioned below-

Affordability – this is related with the rise in income of the people which has affected the

housing rent as well as house constructions directly. As there is economic growth and

development, the demand for house is also increased. There is also demand for housing

which bends towards the luxurious goods. When the earning of people is more, the

housing rent and allowances are also increased as they are in high demand. The house

prices within UK have increased since 2009 at a faster rate as the growth of economy is

also increasing rapidly.

Confidence - consumers are they the most essential factor which affect the demand for

houses. It is very important for managing demand of house that is directly connected with

confidence of consumer. the future of economy is totally dependent upon confidence of

people and hence, it affects the rating of housing market. when consumers are expecting

that housing price will increase, there is gradual rise in demand that is helpful for these

companies to gain profit. The demand for house is board then the income of people

Hindi 2016 to 2019

Interest rates - these are defined as one of the biggest factor which are helpful in determining the

mortgage interest repayment cost. There are various home owners in UK which are shifting for

variable mortgage rates as they are very common in dealing. When there is any change within

the base rate by banks there is is shift in the mortgage interest payments. It is the element which

is useful for determining the housing affordability. The mortgage payments have to analyse high

percentage of personal disposable income so that it is easy to you manage the functioning (Rizal,

Suhadak, and Kholid, 2017). This can be explained with an example that if a person has to

mortgage 150000 euros then and it has to pay. 5% change in base rate on monthly basis. This

proves that if there is a small change in interest rate then the decision making of people is

affected. The interest rates were 15% in the year 1992. At that time demand for housing

collapsed. Moreover, the housing rates in the year 2009 to 2014 work cut 20.5 percent. Interest

rates provided by bank were also decreased but the demand for housing remained low. the reason

behind minimised housing demand was like recession and unemployment (Morioka, Evans, and

de Carvalho, 2016).

Population of England - there is gradual growth in in population within UK over 60

million within 2019. there is gradual increase of 6 million in UK population since 2012.

This is a very important factor that affects the housing demand. number of people does

not affect the housing rates but as there is change in demographic like the growth of

single people which has led to increase in housing demand. The rates of housing depend

upon average housing price. The housing demand does not depend upon the population

but it is dependent upon average size of household. There are some demographic as well

also increasing rapidly.

Confidence - consumers are they the most essential factor which affect the demand for

houses. It is very important for managing demand of house that is directly connected with

confidence of consumer. the future of economy is totally dependent upon confidence of

people and hence, it affects the rating of housing market. when consumers are expecting

that housing price will increase, there is gradual rise in demand that is helpful for these

companies to gain profit. The demand for house is board then the income of people

Hindi 2016 to 2019

Interest rates - these are defined as one of the biggest factor which are helpful in determining the

mortgage interest repayment cost. There are various home owners in UK which are shifting for

variable mortgage rates as they are very common in dealing. When there is any change within

the base rate by banks there is is shift in the mortgage interest payments. It is the element which

is useful for determining the housing affordability. The mortgage payments have to analyse high

percentage of personal disposable income so that it is easy to you manage the functioning (Rizal,

Suhadak, and Kholid, 2017). This can be explained with an example that if a person has to

mortgage 150000 euros then and it has to pay. 5% change in base rate on monthly basis. This

proves that if there is a small change in interest rate then the decision making of people is

affected. The interest rates were 15% in the year 1992. At that time demand for housing

collapsed. Moreover, the housing rates in the year 2009 to 2014 work cut 20.5 percent. Interest

rates provided by bank were also decreased but the demand for housing remained low. the reason

behind minimised housing demand was like recession and unemployment (Morioka, Evans, and

de Carvalho, 2016).

Population of England - there is gradual growth in in population within UK over 60

million within 2019. there is gradual increase of 6 million in UK population since 2012.

This is a very important factor that affects the housing demand. number of people does

not affect the housing rates but as there is change in demographic like the growth of

single people which has led to increase in housing demand. The rates of housing depend

upon average housing price. The housing demand does not depend upon the population

but it is dependent upon average size of household. There are some demographic as well

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as social elements which are reason for increase in household number. Some of the

demographic changes include age of people who are living homes because of increased

life expectancy. This has led to increase in number of old people. Divorce rates are

increasing and hence, the number of single parent families is increasing. Due to this,

there is high increase in price of housing in UK.

Mortgage availability - this is known as element which determines effectiveness of demand for

houses. There is demand of housing because of the willingness of banks to lend mortgages.

When banks are giving mortgages with bigger income multiplies there is increase in demand for

housing. The finance mod gauging can depend upon strength of interbank which is affected by

land sector. Due to credit crisis within 2009, there is increase in cost of inter- bank lending. This

has decreased the availability of mortgage finance. There are various mortgage products which

have been withdrawn for making it difficult to manage the property (Levytska, and Vovk,

2017). There are different mod gauges like 100% as well as 1 25% which have been withdrawn

in the bank of England. there is increase in demand of bank due to high deposit of the lending

mortgage.

Economic growth and retail incomes – there is rise in income which has encouraged and

motivated demand for housing. In time of increased demand the housing prices are also

increased rapidly due to the index of renting. According to the statistics, there is increase

of 22% in cost of renting. There was financial crisis and housing crash but it has helped

for causing UK house price for continuing rising after 2011. The UK housing market is

has to do the work properly by analysing the expensive renting cost and motivating the

lenders to buy the household by stretching the budget and housing ladder.

There are various increase within new houses which are built in UK. Great Britain is a

city which has experienced increased within new houses since past century (Luqmani,

Leach, and Jesson, 2017). There was increased after 2000 at a higher rate.

There is restriction on planning and using the land properly. There is big problem within

UK for managing the limitations as well as restrictions on building houses on green belt

land.

There is local opposition which restricts the building of new houses and homes. It effects

pricing of houses.

demographic changes include age of people who are living homes because of increased

life expectancy. This has led to increase in number of old people. Divorce rates are

increasing and hence, the number of single parent families is increasing. Due to this,

there is high increase in price of housing in UK.

Mortgage availability - this is known as element which determines effectiveness of demand for

houses. There is demand of housing because of the willingness of banks to lend mortgages.

When banks are giving mortgages with bigger income multiplies there is increase in demand for

housing. The finance mod gauging can depend upon strength of interbank which is affected by

land sector. Due to credit crisis within 2009, there is increase in cost of inter- bank lending. This

has decreased the availability of mortgage finance. There are various mortgage products which

have been withdrawn for making it difficult to manage the property (Levytska, and Vovk,

2017). There are different mod gauges like 100% as well as 1 25% which have been withdrawn

in the bank of England. there is increase in demand of bank due to high deposit of the lending

mortgage.

Economic growth and retail incomes – there is rise in income which has encouraged and

motivated demand for housing. In time of increased demand the housing prices are also

increased rapidly due to the index of renting. According to the statistics, there is increase

of 22% in cost of renting. There was financial crisis and housing crash but it has helped

for causing UK house price for continuing rising after 2011. The UK housing market is

has to do the work properly by analysing the expensive renting cost and motivating the

lenders to buy the household by stretching the budget and housing ladder.

There are various increase within new houses which are built in UK. Great Britain is a

city which has experienced increased within new houses since past century (Luqmani,

Leach, and Jesson, 2017). There was increased after 2000 at a higher rate.

There is restriction on planning and using the land properly. There is big problem within

UK for managing the limitations as well as restrictions on building houses on green belt

land.

There is local opposition which restricts the building of new houses and homes. It effects

pricing of houses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

How has the government action over the period 2009-2019 affected the UK housing market

The Government of UK has affected suspended the property market and housing market of the

country since last 20 years. The estate agents have stopped from marketing new homes and

banning visits to the areas where there is sale done already. Government affects the housing

industry in one way or the other. When there is any e economic decline, then the housing prices

are increased as a result (Schaltegger, Hansen, and Lüdeke-Freund, 2016). There are various

ministers and lenders who have invested their money within Bank for managing the valuations

regarding the housing price. They have also granted several credit due to the downfall in

economy. It is concluded that it is not possible for survey for properties and various people al2

analyse the discussion on working of housing industry. Government policies and regulations

affect the buying and selling of housing. This can be explained with an example that as there is

lock down within UK due to the covid-19 epidemic. Hence, government has started lockdown

and there is no access to any individual to visit any place. Due to this, there are several houses

which are sold but now There are no people who have visited that place and transactions are not

taken due to the current situation within market. Barclays and Lloyds banking group which are

the UK biggest lenders are not providing any type of mortgage investment. Lords banking

service has stopped offering mod cages for remote gauges by this is only possible if 40% of the

value of properties (Sztangret, 2016). This is only possible if 40% of the value of property is

provided by the customer. The mortgage offers are valid for 3 months and customers have to

exchange their contacts on the extension of mortgage offer.

The Government of UK has affected suspended the property market and housing market of the

country since last 20 years. The estate agents have stopped from marketing new homes and

banning visits to the areas where there is sale done already. Government affects the housing

industry in one way or the other. When there is any e economic decline, then the housing prices

are increased as a result (Schaltegger, Hansen, and Lüdeke-Freund, 2016). There are various

ministers and lenders who have invested their money within Bank for managing the valuations

regarding the housing price. They have also granted several credit due to the downfall in

economy. It is concluded that it is not possible for survey for properties and various people al2

analyse the discussion on working of housing industry. Government policies and regulations

affect the buying and selling of housing. This can be explained with an example that as there is

lock down within UK due to the covid-19 epidemic. Hence, government has started lockdown

and there is no access to any individual to visit any place. Due to this, there are several houses

which are sold but now There are no people who have visited that place and transactions are not

taken due to the current situation within market. Barclays and Lloyds banking group which are

the UK biggest lenders are not providing any type of mortgage investment. Lords banking

service has stopped offering mod cages for remote gauges by this is only possible if 40% of the

value of properties (Sztangret, 2016). This is only possible if 40% of the value of property is

provided by the customer. The mortgage offers are valid for 3 months and customers have to

exchange their contacts on the extension of mortgage offer.

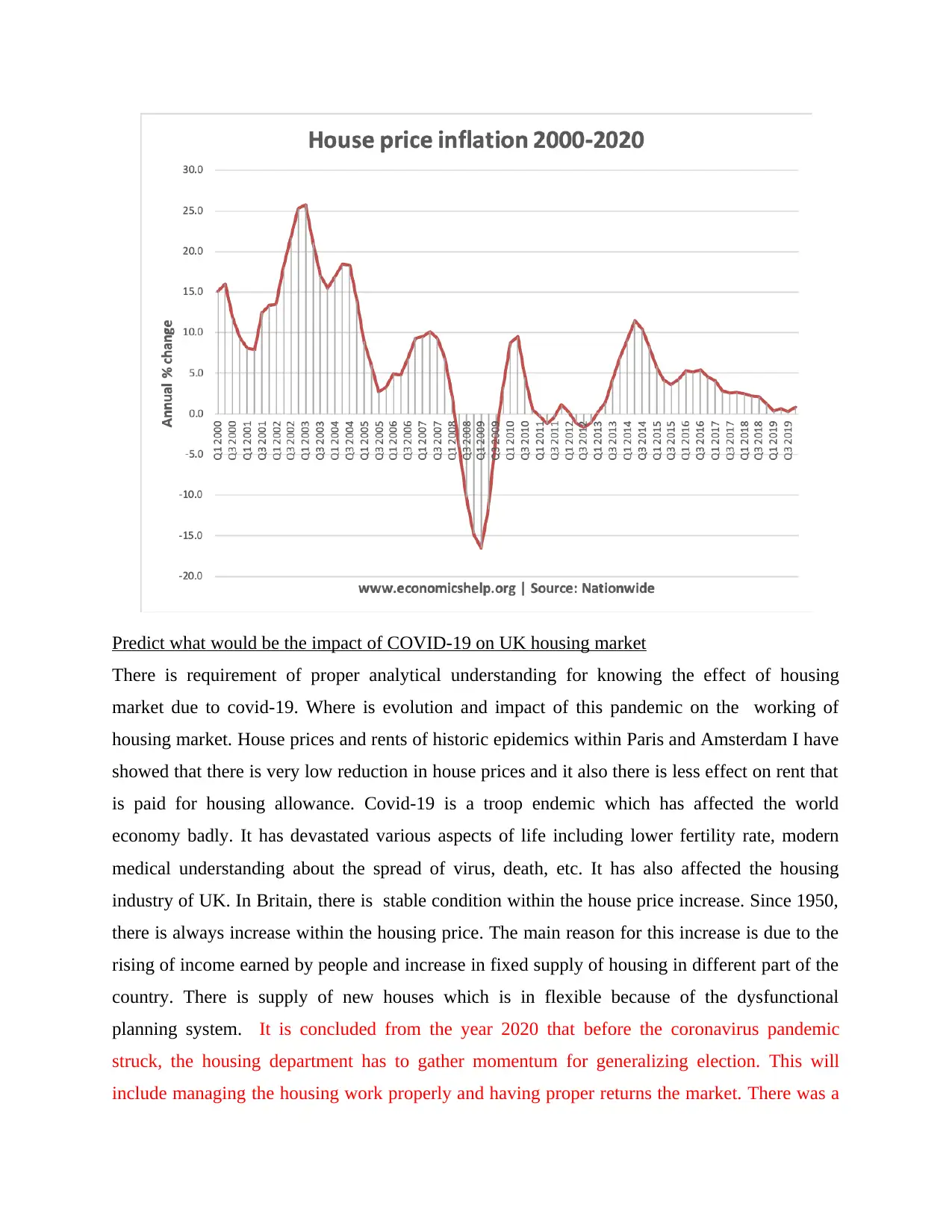

Predict what would be the impact of COVID-19 on UK housing market

There is requirement of proper analytical understanding for knowing the effect of housing

market due to covid-19. Where is evolution and impact of this pandemic on the working of

housing market. House prices and rents of historic epidemics within Paris and Amsterdam I have

showed that there is very low reduction in house prices and it also there is less effect on rent that

is paid for housing allowance. Covid-19 is a troop endemic which has affected the world

economy badly. It has devastated various aspects of life including lower fertility rate, modern

medical understanding about the spread of virus, death, etc. It has also affected the housing

industry of UK. In Britain, there is stable condition within the house price increase. Since 1950,

there is always increase within the housing price. The main reason for this increase is due to the

rising of income earned by people and increase in fixed supply of housing in different part of the

country. There is supply of new houses which is in flexible because of the dysfunctional

planning system. It is concluded from the year 2020 that before the coronavirus pandemic

struck, the housing department has to gather momentum for generalizing election. This will

include managing the housing work properly and having proper returns the market. There was a

There is requirement of proper analytical understanding for knowing the effect of housing

market due to covid-19. Where is evolution and impact of this pandemic on the working of

housing market. House prices and rents of historic epidemics within Paris and Amsterdam I have

showed that there is very low reduction in house prices and it also there is less effect on rent that

is paid for housing allowance. Covid-19 is a troop endemic which has affected the world

economy badly. It has devastated various aspects of life including lower fertility rate, modern

medical understanding about the spread of virus, death, etc. It has also affected the housing

industry of UK. In Britain, there is stable condition within the house price increase. Since 1950,

there is always increase within the housing price. The main reason for this increase is due to the

rising of income earned by people and increase in fixed supply of housing in different part of the

country. There is supply of new houses which is in flexible because of the dysfunctional

planning system. It is concluded from the year 2020 that before the coronavirus pandemic

struck, the housing department has to gather momentum for generalizing election. This will

include managing the housing work properly and having proper returns the market. There was a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

great decline due to the corona virus pandemic in sales of the houses. The Brexit has also

affected the situation and also it was seen that work was disturbed at that time too and now

Corona crisis has also affected the sales of houses within UK (Shahzadi, Toor, and ul Haq,

2018). The nationwide lockdown imposed by the government on 23 March to contain the Covid-

19 pandemic. There is affect on housing department of UK and there is problem in managing the

economic growth. There was need for managing the working of the housing department so that

sales will be increased. There are opportunities for providing various promotions and offers to

the housing. The house hunters were only allowed to conduct virtual viewings. The Data from

HMRC showed residential property transactions were down 53% in April compared with the

same month in 2019.. There are potential buyers within market who are planning for waiting in

order to buy house. There are various lenders who provided the information that approximately

15% of people were considering moving as a result of life in lockdown, with a third stating they

thought differently about their home. They focused upon indoor space and garden. There are

22% individuals who think that people were considering improving their home instead. It is

concluded from The EY Item Club economic forecasting group that house prices must be

managed properly for managing the condition with house prices. This is concluded from the

views of chief economic adviser, Howard Archer that housing market activity is likely to be

limited because this pandemic. Many people have already lost their jobs, despite the supportive

government measures, while others will be worried that they may still end up losing theirs once

the furlough scheme ends. The local government and was not able to provide incentives to the

local authorities and format the development plans. This has resulted in in managing the supply

of houses and driving the price. Due to the covid-19, there is no buying and selling of housing.

This has affected the housing industry in the manner that there is no loss and no profit. After the

lockdown is over and market and phrases, there will be low transactions regarding the housing

allowance. There is probable ongoing economic destruction which has affected the economy and

hence, it is not easy to focus upon t housing business. there is construction of new houses which

is strictly restricted as new home will be contributing to small fraction of total stock. This will

affect total supply and hence there will be fall in house prices. The income of many people has

been affected. Consumer confidence is currently at or near record low levels and many people

are likely to remain cautious for some time to come when making major spending decisions such

as buying or moving house. The house-price growth was forecasted zero for 2020 before the

affected the situation and also it was seen that work was disturbed at that time too and now

Corona crisis has also affected the sales of houses within UK (Shahzadi, Toor, and ul Haq,

2018). The nationwide lockdown imposed by the government on 23 March to contain the Covid-

19 pandemic. There is affect on housing department of UK and there is problem in managing the

economic growth. There was need for managing the working of the housing department so that

sales will be increased. There are opportunities for providing various promotions and offers to

the housing. The house hunters were only allowed to conduct virtual viewings. The Data from

HMRC showed residential property transactions were down 53% in April compared with the

same month in 2019.. There are potential buyers within market who are planning for waiting in

order to buy house. There are various lenders who provided the information that approximately

15% of people were considering moving as a result of life in lockdown, with a third stating they

thought differently about their home. They focused upon indoor space and garden. There are

22% individuals who think that people were considering improving their home instead. It is

concluded from The EY Item Club economic forecasting group that house prices must be

managed properly for managing the condition with house prices. This is concluded from the

views of chief economic adviser, Howard Archer that housing market activity is likely to be

limited because this pandemic. Many people have already lost their jobs, despite the supportive

government measures, while others will be worried that they may still end up losing theirs once

the furlough scheme ends. The local government and was not able to provide incentives to the

local authorities and format the development plans. This has resulted in in managing the supply

of houses and driving the price. Due to the covid-19, there is no buying and selling of housing.

This has affected the housing industry in the manner that there is no loss and no profit. After the

lockdown is over and market and phrases, there will be low transactions regarding the housing

allowance. There is probable ongoing economic destruction which has affected the economy and

hence, it is not easy to focus upon t housing business. there is construction of new houses which

is strictly restricted as new home will be contributing to small fraction of total stock. This will

affect total supply and hence there will be fall in house prices. The income of many people has

been affected. Consumer confidence is currently at or near record low levels and many people

are likely to remain cautious for some time to come when making major spending decisions such

as buying or moving house. The house-price growth was forecasted zero for 2020 before the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

pandemic struck. The forecasting of the long-term effects of the outbreak on the economy and

house prices cannot be said clear. Moreover there will be high price in the induced death

because of covid-19 and as there are more elder people who have died, there are various houses

which can be e sold to new people. There is no professional forecast which can tell the

information about how long this epidemic or lockdown will last. According to the statistics, it

can be said that longer dialogue down last, slower will be the recovery in housing industry. The

economy is in free fall and the official data provides information that the sales of housing has

been decreased negatively since the rise of this epidemic. When the earning of people will start

to recover after the open of lock down then there are many people who have used their fixed

deposits or savings to survive in the lockdown period. Hence, there are many people who have

saved their money to buy a house and due to this epidemic, they have to use that money for

surviving in the lockdown period. Raft of policies which have been adopted for supporting the

economy is going to help ensuring the impact on the housing market. This will provide help in

associated with the economic magnitude. The ability for generating the house price index was

unaffected so far as sample sizes remained sufficiently large to generate robust results. There

was low transaction levels may make gauging price trends difficult in the coming months,

especially for regional indices. The Office for National Statistics has suspended its official house

price index because of insufficient data. In this case, they have to postpone the time for buying a

new house. there is economic downturn due to the covid-19 and it has created depression for

housing industry.

CONCLUSION

From the above discussion, it can be said that there are various policies and regulations of

bank which have fostered the shift from secure and dependable assets like bonds into square and

less dependent assets like real estate and stocks. It is analysed from researches that there is yield

and higher returns due to the investor demand for housing. the demand and pricing dynamics of

housing have been increased rapidly due to the sale inventory of the market. Due to the covid-19

pandemic, there is increase in the housing prices at higher rate as individuals will shift from

affected areas to good and safe environment.

house prices cannot be said clear. Moreover there will be high price in the induced death

because of covid-19 and as there are more elder people who have died, there are various houses

which can be e sold to new people. There is no professional forecast which can tell the

information about how long this epidemic or lockdown will last. According to the statistics, it

can be said that longer dialogue down last, slower will be the recovery in housing industry. The

economy is in free fall and the official data provides information that the sales of housing has

been decreased negatively since the rise of this epidemic. When the earning of people will start

to recover after the open of lock down then there are many people who have used their fixed

deposits or savings to survive in the lockdown period. Hence, there are many people who have

saved their money to buy a house and due to this epidemic, they have to use that money for

surviving in the lockdown period. Raft of policies which have been adopted for supporting the

economy is going to help ensuring the impact on the housing market. This will provide help in

associated with the economic magnitude. The ability for generating the house price index was

unaffected so far as sample sizes remained sufficiently large to generate robust results. There

was low transaction levels may make gauging price trends difficult in the coming months,

especially for regional indices. The Office for National Statistics has suspended its official house

price index because of insufficient data. In this case, they have to postpone the time for buying a

new house. there is economic downturn due to the covid-19 and it has created depression for

housing industry.

CONCLUSION

From the above discussion, it can be said that there are various policies and regulations of

bank which have fostered the shift from secure and dependable assets like bonds into square and

less dependent assets like real estate and stocks. It is analysed from researches that there is yield

and higher returns due to the investor demand for housing. the demand and pricing dynamics of

housing have been increased rapidly due to the sale inventory of the market. Due to the covid-19

pandemic, there is increase in the housing prices at higher rate as individuals will shift from

affected areas to good and safe environment.

REFERENCES

Books and Journals

Chong, S.C., 2019. An Analysis of the External and Internal Factors Affecting Honda Motor

Company’s Performance.

Gaffar, M.R. and Subhash, K.B., 2020. External and internal factors of mobile games adoption in

Indonesia.

Komara, A.A., Sinaga, B.M. and Andati, T., 2019. The Impact of Changes in External and

Internal Factors on Financial Performance and Stock Returns of Coal Companies. Jurnal

Aplikasi Bisnis dan Manajemen (JABM), 5(3).

Lund, M.R. and Måseidvåg, S., 2018. Brand Portfolio Management in the Norwegian Brewing

Industry-An assessment of external and internal factors influencing the brand portfolio

management of large established breweries in Norway (Master's thesis, NTNU).

Oraman, Y., Unakitan, G., Konyali, S., Basaran, B. and Abdikoglu, D.I., 2018. WHAT

EXTERNAL AND INTERNAL FACTORS AFFECT ORGANIC FOOD

SECTOR?. New knowledge Journal of science, 7(2), pp.33-44.

Pearson, R., 2017. Business ethics as communication ethics: Public relations practice and the

idea of dialogue. In Public relations theory (pp. 111-131). Routledge.

Ren, S. and et. al., 2017. Modelling quality dynamics, business value and firm performance in a

big data analytics environment. International Journal of Production Research. 55(17).

pp.5011-5026.pp.23-34.

Rizal, O., Suhadak, M. and Kholid, M., 2017. Analysis of the influence of external and internal

environmental factors on business performance: A study on micro small and medium

enterprises (MSMES) of food and beverage. Russian Journal of Agricultural and Socio-

Economic Sciences, 66(6).

Morioka, S.N., Evans, S. and de Carvalho, M.M., 2016. Sustainable business model innovation:

Exploring evidences in sustainability reporting. Procedia CIRP, 40, pp.659-667.

Levytska, S. and Vovk, V., 2017. Variability of information support for the results of enterprise

business activity. Zeszyty Naukowe PWSZ w Płocku. Nauki Ekonomiczne.

Luqmani, A., Leach, M. and Jesson, D., 2017. Factors behind sustainable business innovation:

The case of a global carpet manufacturing company. Environmental innovation and

societal transitions, 24, pp.94-105.

Schaltegger, S., Hansen, E. G. and Lüdeke-Freund, F., 2016. Business models for sustainability:

Origins, present research, and future avenues.

Sztangret, I., 2016. The Competence Centres in IT business ecosystem. Case study. Journal of

Economics & Management, 24, pp.99-110.

Shahzadi, S., Khan, R., Toor, M. and ul Haq, A., 2018. Impact of external and internal factors on

management accounting practices: a study of Pakistan. Asian Journal of Accounting

Research.

Vidović, A.B., 2015. Growth and development of companies in the function mergers and

acquisitions. Tehnika, 70(5), pp.866-869.

Books and Journals

Chong, S.C., 2019. An Analysis of the External and Internal Factors Affecting Honda Motor

Company’s Performance.

Gaffar, M.R. and Subhash, K.B., 2020. External and internal factors of mobile games adoption in

Indonesia.

Komara, A.A., Sinaga, B.M. and Andati, T., 2019. The Impact of Changes in External and

Internal Factors on Financial Performance and Stock Returns of Coal Companies. Jurnal

Aplikasi Bisnis dan Manajemen (JABM), 5(3).

Lund, M.R. and Måseidvåg, S., 2018. Brand Portfolio Management in the Norwegian Brewing

Industry-An assessment of external and internal factors influencing the brand portfolio

management of large established breweries in Norway (Master's thesis, NTNU).

Oraman, Y., Unakitan, G., Konyali, S., Basaran, B. and Abdikoglu, D.I., 2018. WHAT

EXTERNAL AND INTERNAL FACTORS AFFECT ORGANIC FOOD

SECTOR?. New knowledge Journal of science, 7(2), pp.33-44.

Pearson, R., 2017. Business ethics as communication ethics: Public relations practice and the

idea of dialogue. In Public relations theory (pp. 111-131). Routledge.

Ren, S. and et. al., 2017. Modelling quality dynamics, business value and firm performance in a

big data analytics environment. International Journal of Production Research. 55(17).

pp.5011-5026.pp.23-34.

Rizal, O., Suhadak, M. and Kholid, M., 2017. Analysis of the influence of external and internal

environmental factors on business performance: A study on micro small and medium

enterprises (MSMES) of food and beverage. Russian Journal of Agricultural and Socio-

Economic Sciences, 66(6).

Morioka, S.N., Evans, S. and de Carvalho, M.M., 2016. Sustainable business model innovation:

Exploring evidences in sustainability reporting. Procedia CIRP, 40, pp.659-667.

Levytska, S. and Vovk, V., 2017. Variability of information support for the results of enterprise

business activity. Zeszyty Naukowe PWSZ w Płocku. Nauki Ekonomiczne.

Luqmani, A., Leach, M. and Jesson, D., 2017. Factors behind sustainable business innovation:

The case of a global carpet manufacturing company. Environmental innovation and

societal transitions, 24, pp.94-105.

Schaltegger, S., Hansen, E. G. and Lüdeke-Freund, F., 2016. Business models for sustainability:

Origins, present research, and future avenues.

Sztangret, I., 2016. The Competence Centres in IT business ecosystem. Case study. Journal of

Economics & Management, 24, pp.99-110.

Shahzadi, S., Khan, R., Toor, M. and ul Haq, A., 2018. Impact of external and internal factors on

management accounting practices: a study of Pakistan. Asian Journal of Accounting

Research.

Vidović, A.B., 2015. Growth and development of companies in the function mergers and

acquisitions. Tehnika, 70(5), pp.866-869.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.