Analyzing the UK Housing Market: Economic Factors (2009-2019)

VerifiedAdded on 2023/01/11

|13

|3600

|21

Report

AI Summary

This report provides a detailed analysis of the UK housing market between 2009 and 2019, examining the changes in average house prices and the economic determinants behind these fluctuations. It explores the impact of the financial crisis, house price inflation rates, and mortgage approvals on the market. Furthermore, the report assesses the influence of government actions during this period and offers insights into the potential impact of COVID-19 on the UK housing market. The analysis includes graphical representations of house prices, inflation rates, and mortgage approvals to provide a comprehensive understanding of the market dynamics.

Evaluating Internal and

External Business

Environment

External Business

Environment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Average house prices in the UK changed over the period from 2009 to 2019............................1

Economic determinants of the changes in the UK housing prices from the year 2009 to 2019..5

Government action over the period 2009-2019 affected the UK Housing market......................8

Ascertainment of the potential impact of COVID-19 on UK Housing Market...........................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Average house prices in the UK changed over the period from 2009 to 2019............................1

Economic determinants of the changes in the UK housing prices from the year 2009 to 2019..5

Government action over the period 2009-2019 affected the UK Housing market......................8

Ascertainment of the potential impact of COVID-19 on UK Housing Market...........................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Internal and external business environment contains the factors that have direct and indirect

impact over organisational functions along with the whole market segment. Evaluation of both

markets is important because this will help in determination of the nature of factors that exist in

actual and have some kind of present and potential impact over business or market either in

positive or negative manner. Each different market and organisations exists under the market are

affecting differently from the factors. It is the duty over management that must study about these

and build the strategies through which optimum benefits can be taken out from the occurrence of

such factors (Baptista and et al., 2016). This further aid the organisations management to

formulate the mitigating measures through which they can secure the future transactions and able

to maintain the level of sustainability within business operations. The main of this report is also

to analyse the internal and external business environment for the purpose of ascertaining reason

behind the change in housing market of UK.

The aspects cover in this report includes average house prices in the UK changed over the

period from 2009 to 2019, economic determinants of the changes in the UK housing prices from

the year 2009 to 2019, government action over the period 2009-2019 affected the UK Housing

market and potential impact of COVID-19 on UK Housing Market.

MAIN BODY

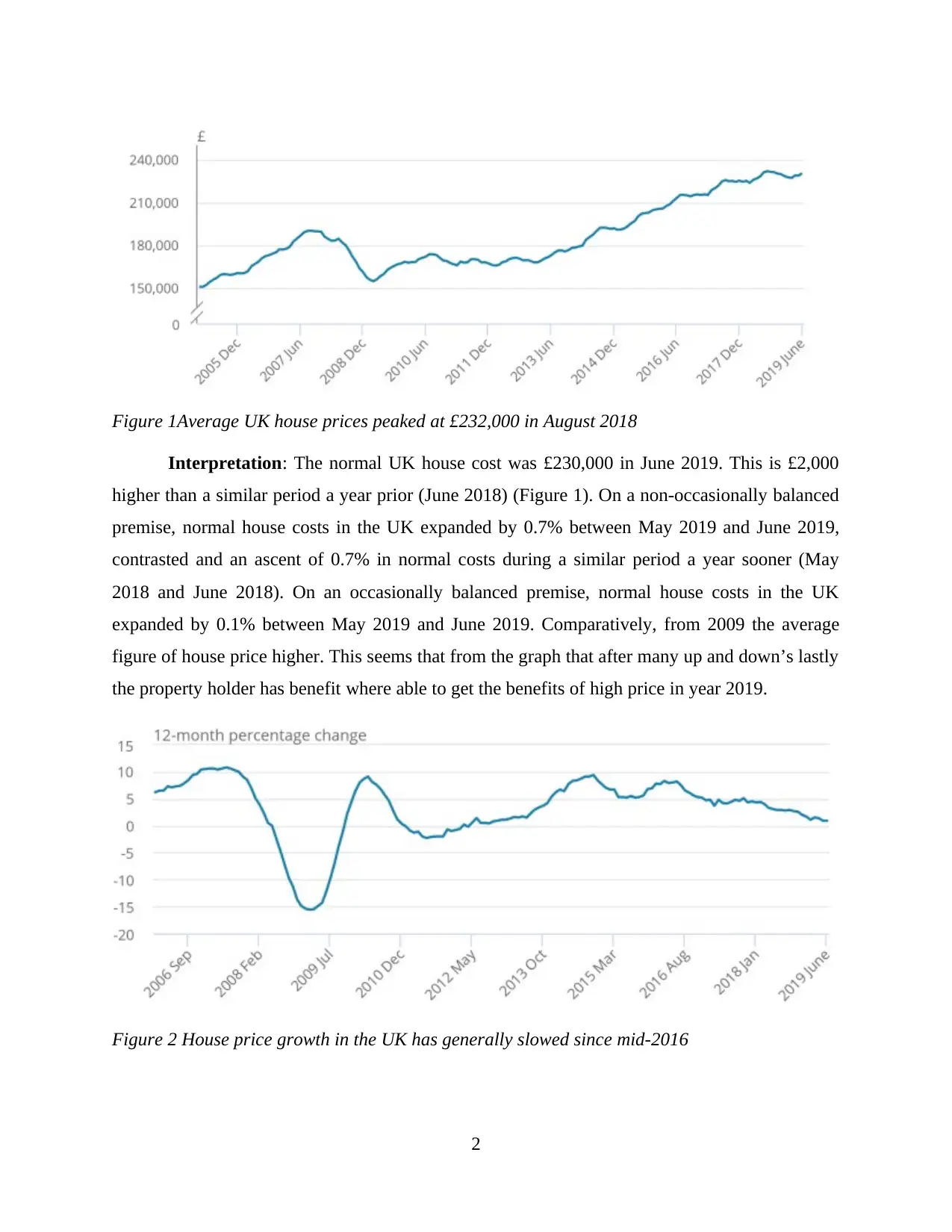

Average house prices in the UK changed over the period from 2009 to 2019

Average house price in UK is presented below with the aid of graph from 2009 to 2019.

There are many other aspects which are associated with housing market of UK that

simultaneously needed to study for better and deeper understanding (UK House Price Index,

2020). These are also presented below in graphical form along with proper interpretation.

1

Internal and external business environment contains the factors that have direct and indirect

impact over organisational functions along with the whole market segment. Evaluation of both

markets is important because this will help in determination of the nature of factors that exist in

actual and have some kind of present and potential impact over business or market either in

positive or negative manner. Each different market and organisations exists under the market are

affecting differently from the factors. It is the duty over management that must study about these

and build the strategies through which optimum benefits can be taken out from the occurrence of

such factors (Baptista and et al., 2016). This further aid the organisations management to

formulate the mitigating measures through which they can secure the future transactions and able

to maintain the level of sustainability within business operations. The main of this report is also

to analyse the internal and external business environment for the purpose of ascertaining reason

behind the change in housing market of UK.

The aspects cover in this report includes average house prices in the UK changed over the

period from 2009 to 2019, economic determinants of the changes in the UK housing prices from

the year 2009 to 2019, government action over the period 2009-2019 affected the UK Housing

market and potential impact of COVID-19 on UK Housing Market.

MAIN BODY

Average house prices in the UK changed over the period from 2009 to 2019

Average house price in UK is presented below with the aid of graph from 2009 to 2019.

There are many other aspects which are associated with housing market of UK that

simultaneously needed to study for better and deeper understanding (UK House Price Index,

2020). These are also presented below in graphical form along with proper interpretation.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 1Average UK house prices peaked at £232,000 in August 2018

Interpretation: The normal UK house cost was £230,000 in June 2019. This is £2,000

higher than a similar period a year prior (June 2018) (Figure 1). On a non-occasionally balanced

premise, normal house costs in the UK expanded by 0.7% between May 2019 and June 2019,

contrasted and an ascent of 0.7% in normal costs during a similar period a year sooner (May

2018 and June 2018). On an occasionally balanced premise, normal house costs in the UK

expanded by 0.1% between May 2019 and June 2019. Comparatively, from 2009 the average

figure of house price higher. This seems that from the graph that after many up and down’s lastly

the property holder has benefit where able to get the benefits of high price in year 2019.

Figure 2 House price growth in the UK has generally slowed since mid-2016

2

Interpretation: The normal UK house cost was £230,000 in June 2019. This is £2,000

higher than a similar period a year prior (June 2018) (Figure 1). On a non-occasionally balanced

premise, normal house costs in the UK expanded by 0.7% between May 2019 and June 2019,

contrasted and an ascent of 0.7% in normal costs during a similar period a year sooner (May

2018 and June 2018). On an occasionally balanced premise, normal house costs in the UK

expanded by 0.1% between May 2019 and June 2019. Comparatively, from 2009 the average

figure of house price higher. This seems that from the graph that after many up and down’s lastly

the property holder has benefit where able to get the benefits of high price in year 2019.

Figure 2 House price growth in the UK has generally slowed since mid-2016

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: Normal house costs in the UK expanded by 0.9% in the year to June

2019, unaltered from May 2019 (Figure 2). In the course of recent years, there has been a general

log jam in UK house value development, driven mostly by a lull in the south and east of

England. The most minimal yearly development was in London, where costs fell by 2.7%

throughout the year to June 2019, not exactly the 3.1% fall in May 2019. Normal house costs in

London have now been falling throughout the year every month since Walk 2018.

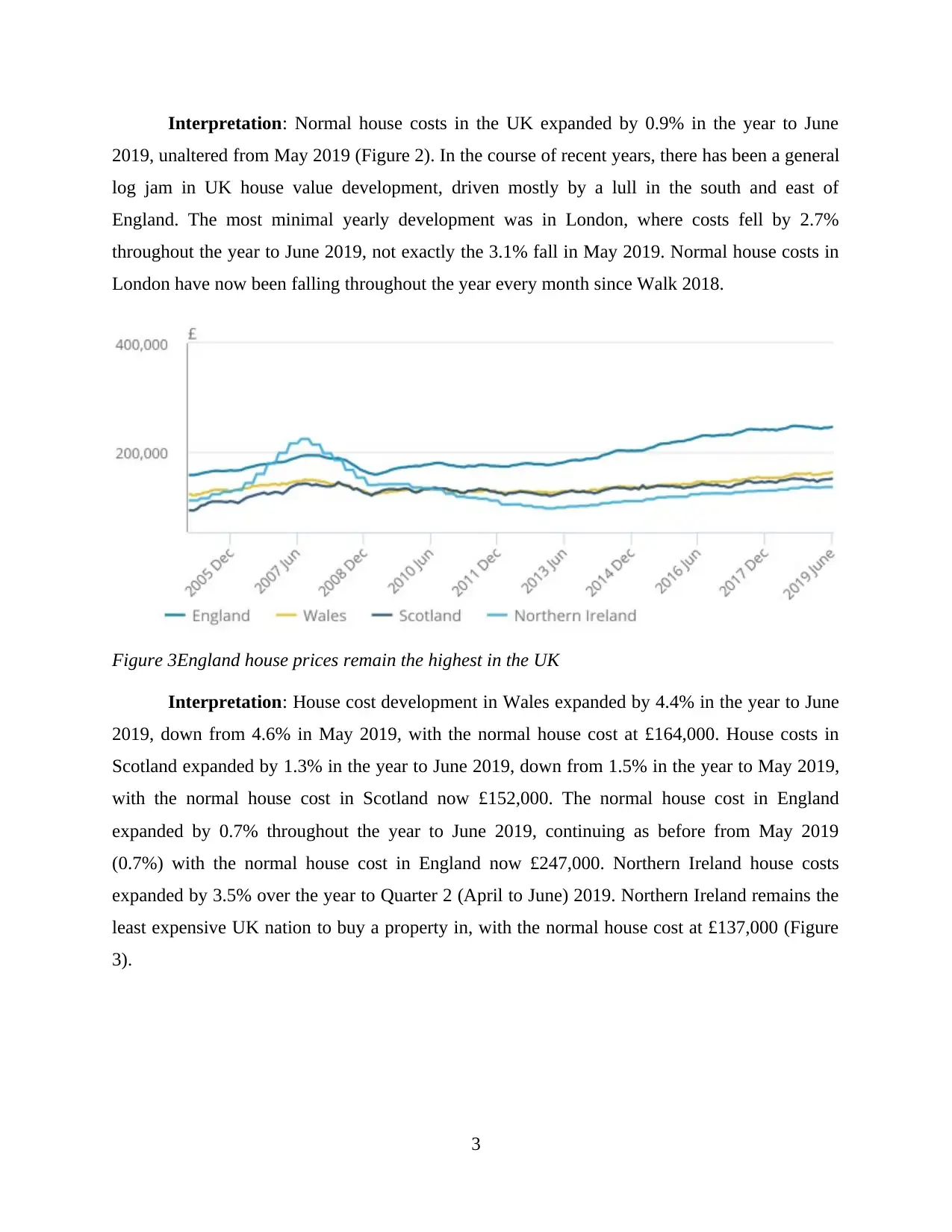

Figure 3England house prices remain the highest in the UK

Interpretation: House cost development in Wales expanded by 4.4% in the year to June

2019, down from 4.6% in May 2019, with the normal house cost at £164,000. House costs in

Scotland expanded by 1.3% in the year to June 2019, down from 1.5% in the year to May 2019,

with the normal house cost in Scotland now £152,000. The normal house cost in England

expanded by 0.7% throughout the year to June 2019, continuing as before from May 2019

(0.7%) with the normal house cost in England now £247,000. Northern Ireland house costs

expanded by 3.5% over the year to Quarter 2 (April to June) 2019. Northern Ireland remains the

least expensive UK nation to buy a property in, with the normal house cost at £137,000 (Figure

3).

3

2019, unaltered from May 2019 (Figure 2). In the course of recent years, there has been a general

log jam in UK house value development, driven mostly by a lull in the south and east of

England. The most minimal yearly development was in London, where costs fell by 2.7%

throughout the year to June 2019, not exactly the 3.1% fall in May 2019. Normal house costs in

London have now been falling throughout the year every month since Walk 2018.

Figure 3England house prices remain the highest in the UK

Interpretation: House cost development in Wales expanded by 4.4% in the year to June

2019, down from 4.6% in May 2019, with the normal house cost at £164,000. House costs in

Scotland expanded by 1.3% in the year to June 2019, down from 1.5% in the year to May 2019,

with the normal house cost in Scotland now £152,000. The normal house cost in England

expanded by 0.7% throughout the year to June 2019, continuing as before from May 2019

(0.7%) with the normal house cost in England now £247,000. Northern Ireland house costs

expanded by 3.5% over the year to Quarter 2 (April to June) 2019. Northern Ireland remains the

least expensive UK nation to buy a property in, with the normal house cost at £137,000 (Figure

3).

3

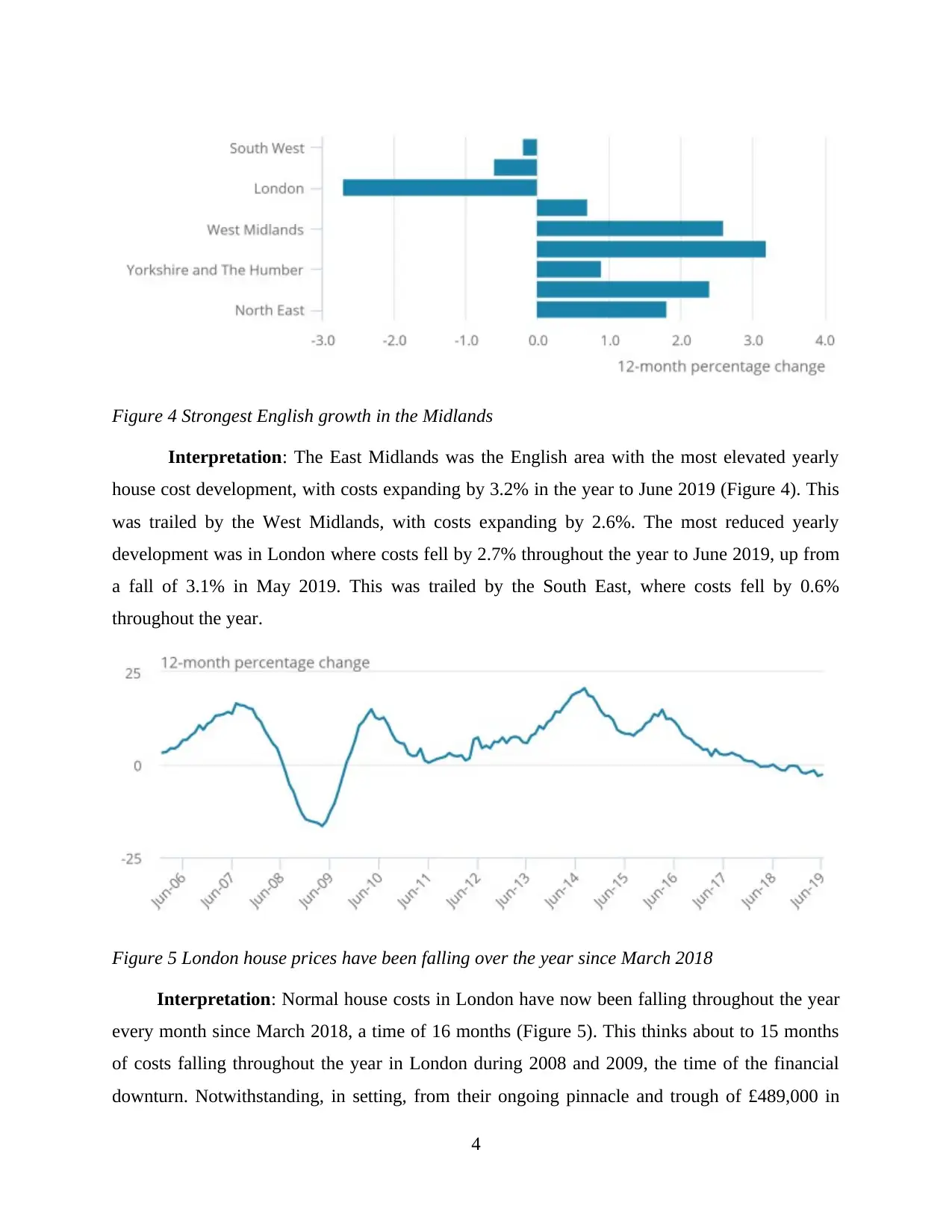

Figure 4 Strongest English growth in the Midlands

Interpretation: The East Midlands was the English area with the most elevated yearly

house cost development, with costs expanding by 3.2% in the year to June 2019 (Figure 4). This

was trailed by the West Midlands, with costs expanding by 2.6%. The most reduced yearly

development was in London where costs fell by 2.7% throughout the year to June 2019, up from

a fall of 3.1% in May 2019. This was trailed by the South East, where costs fell by 0.6%

throughout the year.

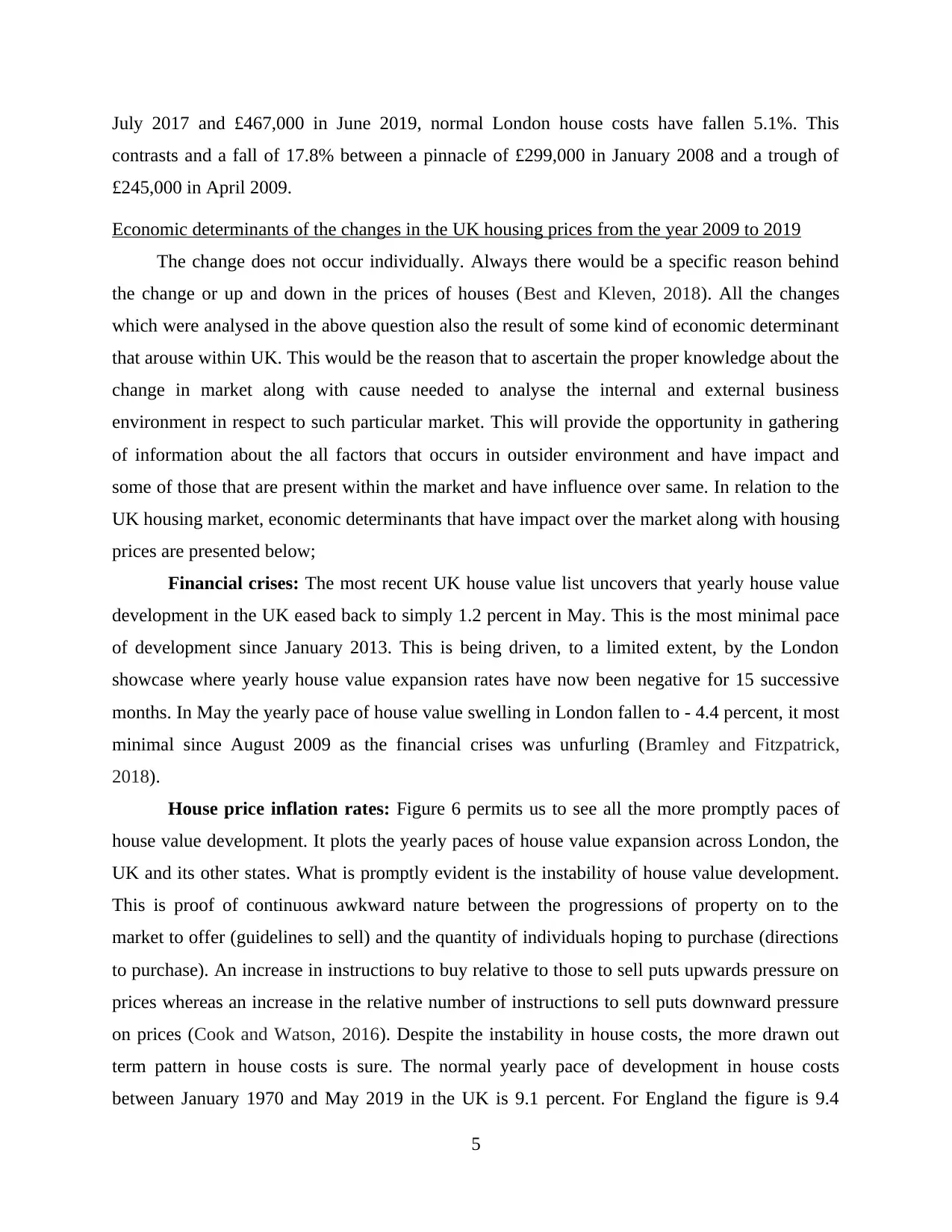

Figure 5 London house prices have been falling over the year since March 2018

Interpretation: Normal house costs in London have now been falling throughout the year

every month since March 2018, a time of 16 months (Figure 5). This thinks about to 15 months

of costs falling throughout the year in London during 2008 and 2009, the time of the financial

downturn. Notwithstanding, in setting, from their ongoing pinnacle and trough of £489,000 in

4

Interpretation: The East Midlands was the English area with the most elevated yearly

house cost development, with costs expanding by 3.2% in the year to June 2019 (Figure 4). This

was trailed by the West Midlands, with costs expanding by 2.6%. The most reduced yearly

development was in London where costs fell by 2.7% throughout the year to June 2019, up from

a fall of 3.1% in May 2019. This was trailed by the South East, where costs fell by 0.6%

throughout the year.

Figure 5 London house prices have been falling over the year since March 2018

Interpretation: Normal house costs in London have now been falling throughout the year

every month since March 2018, a time of 16 months (Figure 5). This thinks about to 15 months

of costs falling throughout the year in London during 2008 and 2009, the time of the financial

downturn. Notwithstanding, in setting, from their ongoing pinnacle and trough of £489,000 in

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

July 2017 and £467,000 in June 2019, normal London house costs have fallen 5.1%. This

contrasts and a fall of 17.8% between a pinnacle of £299,000 in January 2008 and a trough of

£245,000 in April 2009.

Economic determinants of the changes in the UK housing prices from the year 2009 to 2019

The change does not occur individually. Always there would be a specific reason behind

the change or up and down in the prices of houses (Best and Kleven, 2018). All the changes

which were analysed in the above question also the result of some kind of economic determinant

that arouse within UK. This would be the reason that to ascertain the proper knowledge about the

change in market along with cause needed to analyse the internal and external business

environment in respect to such particular market. This will provide the opportunity in gathering

of information about the all factors that occurs in outsider environment and have impact and

some of those that are present within the market and have influence over same. In relation to the

UK housing market, economic determinants that have impact over the market along with housing

prices are presented below;

Financial crises: The most recent UK house value list uncovers that yearly house value

development in the UK eased back to simply 1.2 percent in May. This is the most minimal pace

of development since January 2013. This is being driven, to a limited extent, by the London

showcase where yearly house value expansion rates have now been negative for 15 successive

months. In May the yearly pace of house value swelling in London fallen to - 4.4 percent, it most

minimal since August 2009 as the financial crises was unfurling (Bramley and Fitzpatrick,

2018).

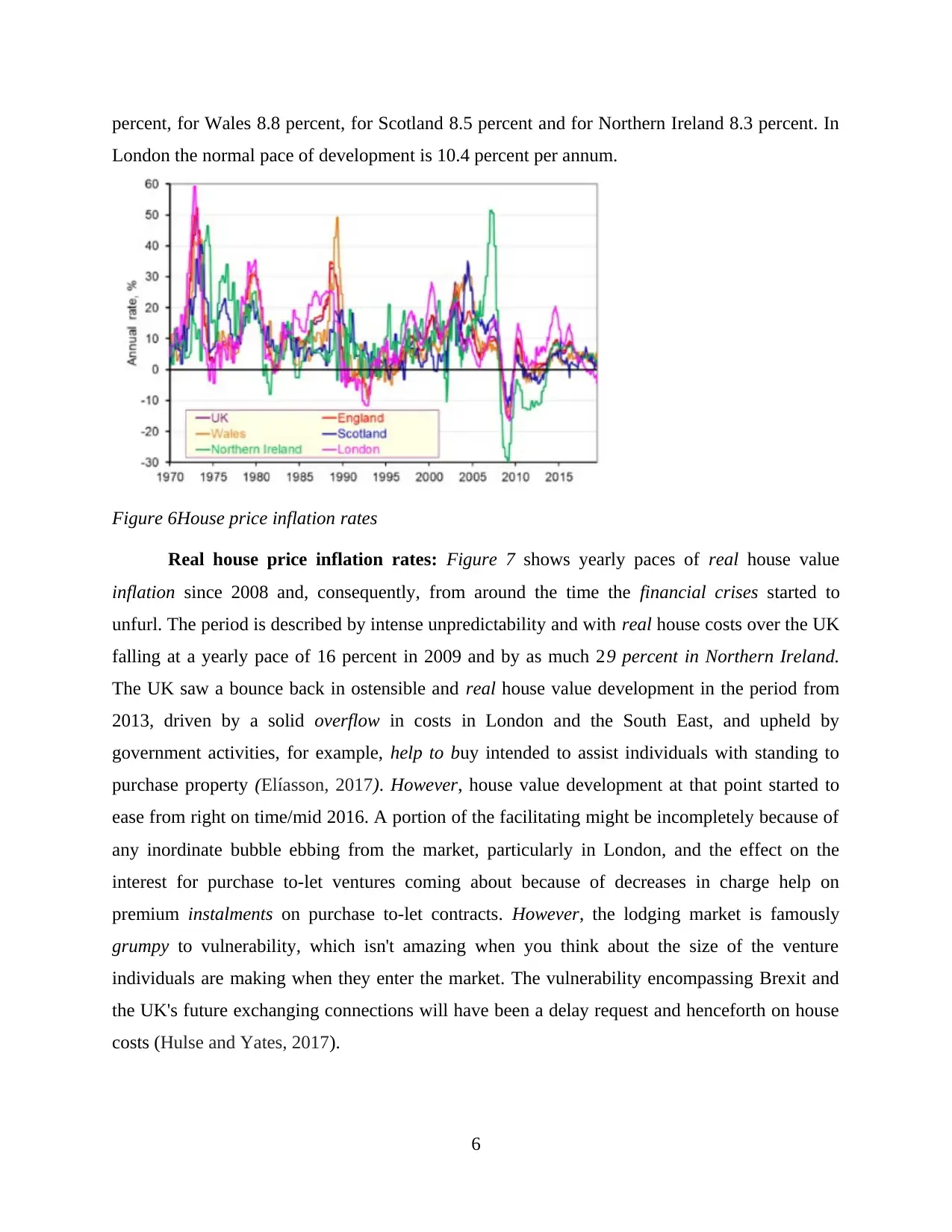

House price inflation rates: Figure 6 permits us to see all the more promptly paces of

house value development. It plots the yearly paces of house value expansion across London, the

UK and its other states. What is promptly evident is the instability of house value development.

This is proof of continuous awkward nature between the progressions of property on to the

market to offer (guidelines to sell) and the quantity of individuals hoping to purchase (directions

to purchase). An increase in instructions to buy relative to those to sell puts upwards pressure on

prices whereas an increase in the relative number of instructions to sell puts downward pressure

on prices (Cook and Watson, 2016). Despite the instability in house costs, the more drawn out

term pattern in house costs is sure. The normal yearly pace of development in house costs

between January 1970 and May 2019 in the UK is 9.1 percent. For England the figure is 9.4

5

contrasts and a fall of 17.8% between a pinnacle of £299,000 in January 2008 and a trough of

£245,000 in April 2009.

Economic determinants of the changes in the UK housing prices from the year 2009 to 2019

The change does not occur individually. Always there would be a specific reason behind

the change or up and down in the prices of houses (Best and Kleven, 2018). All the changes

which were analysed in the above question also the result of some kind of economic determinant

that arouse within UK. This would be the reason that to ascertain the proper knowledge about the

change in market along with cause needed to analyse the internal and external business

environment in respect to such particular market. This will provide the opportunity in gathering

of information about the all factors that occurs in outsider environment and have impact and

some of those that are present within the market and have influence over same. In relation to the

UK housing market, economic determinants that have impact over the market along with housing

prices are presented below;

Financial crises: The most recent UK house value list uncovers that yearly house value

development in the UK eased back to simply 1.2 percent in May. This is the most minimal pace

of development since January 2013. This is being driven, to a limited extent, by the London

showcase where yearly house value expansion rates have now been negative for 15 successive

months. In May the yearly pace of house value swelling in London fallen to - 4.4 percent, it most

minimal since August 2009 as the financial crises was unfurling (Bramley and Fitzpatrick,

2018).

House price inflation rates: Figure 6 permits us to see all the more promptly paces of

house value development. It plots the yearly paces of house value expansion across London, the

UK and its other states. What is promptly evident is the instability of house value development.

This is proof of continuous awkward nature between the progressions of property on to the

market to offer (guidelines to sell) and the quantity of individuals hoping to purchase (directions

to purchase). An increase in instructions to buy relative to those to sell puts upwards pressure on

prices whereas an increase in the relative number of instructions to sell puts downward pressure

on prices (Cook and Watson, 2016). Despite the instability in house costs, the more drawn out

term pattern in house costs is sure. The normal yearly pace of development in house costs

between January 1970 and May 2019 in the UK is 9.1 percent. For England the figure is 9.4

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

percent, for Wales 8.8 percent, for Scotland 8.5 percent and for Northern Ireland 8.3 percent. In

London the normal pace of development is 10.4 percent per annum.

Figure 6House price inflation rates

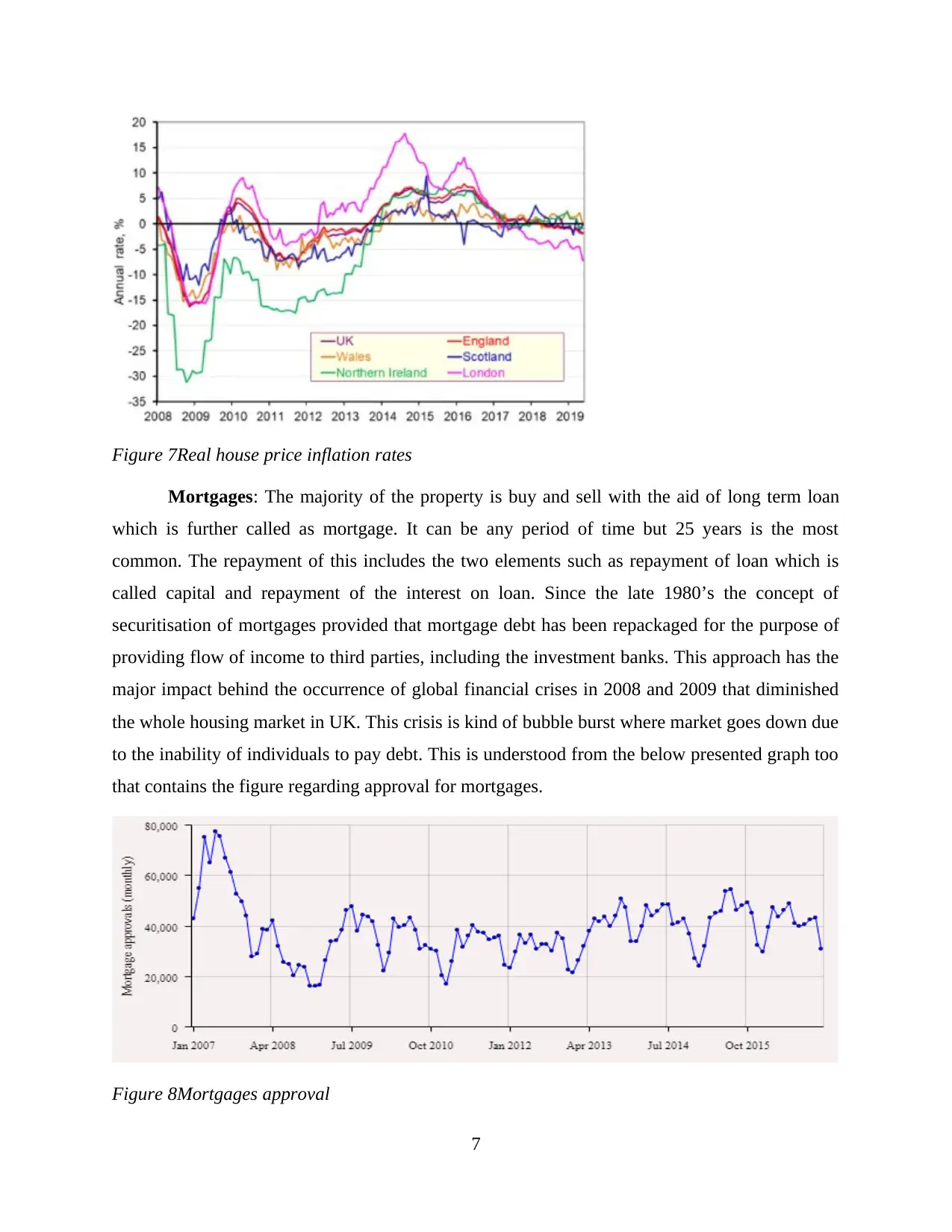

Real house price inflation rates: Figure 7 shows yearly paces of real house value

inflation since 2008 and, consequently, from around the time the financial crises started to

unfurl. The period is described by intense unpredictability and with real house costs over the UK

falling at a yearly pace of 16 percent in 2009 and by as much 29 percent in Northern Ireland.

The UK saw a bounce back in ostensible and real house value development in the period from

2013, driven by a solid overflow in costs in London and the South East, and upheld by

government activities, for example, help to buy intended to assist individuals with standing to

purchase property (Elíasson, 2017). However, house value development at that point started to

ease from right on time/mid 2016. A portion of the facilitating might be incompletely because of

any inordinate bubble ebbing from the market, particularly in London, and the effect on the

interest for purchase to-let ventures coming about because of decreases in charge help on

premium instalments on purchase to-let contracts. However, the lodging market is famously

grumpy to vulnerability, which isn't amazing when you think about the size of the venture

individuals are making when they enter the market. The vulnerability encompassing Brexit and

the UK's future exchanging connections will have been a delay request and henceforth on house

costs (Hulse and Yates, 2017).

6

London the normal pace of development is 10.4 percent per annum.

Figure 6House price inflation rates

Real house price inflation rates: Figure 7 shows yearly paces of real house value

inflation since 2008 and, consequently, from around the time the financial crises started to

unfurl. The period is described by intense unpredictability and with real house costs over the UK

falling at a yearly pace of 16 percent in 2009 and by as much 29 percent in Northern Ireland.

The UK saw a bounce back in ostensible and real house value development in the period from

2013, driven by a solid overflow in costs in London and the South East, and upheld by

government activities, for example, help to buy intended to assist individuals with standing to

purchase property (Elíasson, 2017). However, house value development at that point started to

ease from right on time/mid 2016. A portion of the facilitating might be incompletely because of

any inordinate bubble ebbing from the market, particularly in London, and the effect on the

interest for purchase to-let ventures coming about because of decreases in charge help on

premium instalments on purchase to-let contracts. However, the lodging market is famously

grumpy to vulnerability, which isn't amazing when you think about the size of the venture

individuals are making when they enter the market. The vulnerability encompassing Brexit and

the UK's future exchanging connections will have been a delay request and henceforth on house

costs (Hulse and Yates, 2017).

6

Figure 7Real house price inflation rates

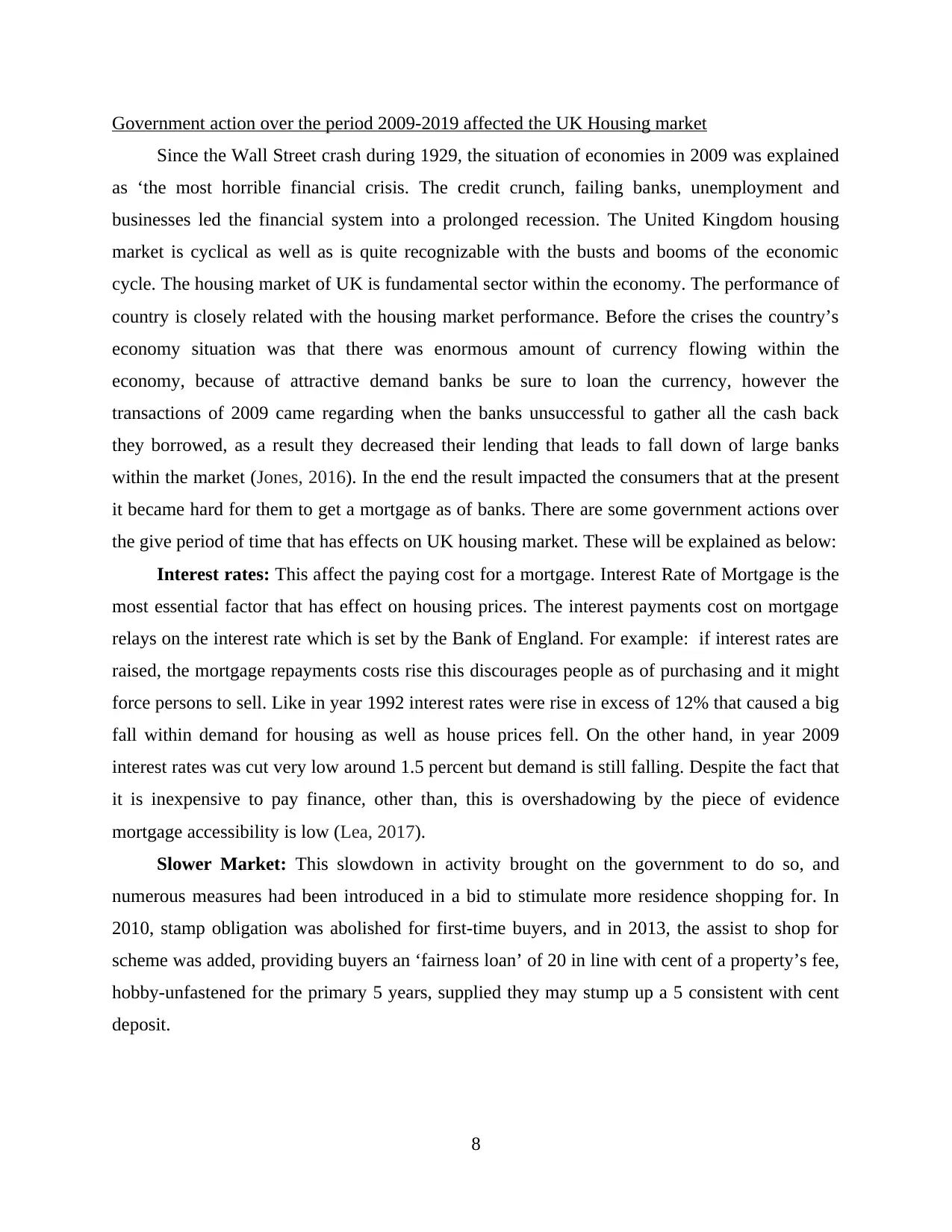

Mortgages: The majority of the property is buy and sell with the aid of long term loan

which is further called as mortgage. It can be any period of time but 25 years is the most

common. The repayment of this includes the two elements such as repayment of loan which is

called capital and repayment of the interest on loan. Since the late 1980’s the concept of

securitisation of mortgages provided that mortgage debt has been repackaged for the purpose of

providing flow of income to third parties, including the investment banks. This approach has the

major impact behind the occurrence of global financial crises in 2008 and 2009 that diminished

the whole housing market in UK. This crisis is kind of bubble burst where market goes down due

to the inability of individuals to pay debt. This is understood from the below presented graph too

that contains the figure regarding approval for mortgages.

Figure 8Mortgages approval

7

Mortgages: The majority of the property is buy and sell with the aid of long term loan

which is further called as mortgage. It can be any period of time but 25 years is the most

common. The repayment of this includes the two elements such as repayment of loan which is

called capital and repayment of the interest on loan. Since the late 1980’s the concept of

securitisation of mortgages provided that mortgage debt has been repackaged for the purpose of

providing flow of income to third parties, including the investment banks. This approach has the

major impact behind the occurrence of global financial crises in 2008 and 2009 that diminished

the whole housing market in UK. This crisis is kind of bubble burst where market goes down due

to the inability of individuals to pay debt. This is understood from the below presented graph too

that contains the figure regarding approval for mortgages.

Figure 8Mortgages approval

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Government action over the period 2009-2019 affected the UK Housing market

Since the Wall Street crash during 1929, the situation of economies in 2009 was explained

as ‘the most horrible financial crisis. The credit crunch, failing banks, unemployment and

businesses led the financial system into a prolonged recession. The United Kingdom housing

market is cyclical as well as is quite recognizable with the busts and booms of the economic

cycle. The housing market of UK is fundamental sector within the economy. The performance of

country is closely related with the housing market performance. Before the crises the country’s

economy situation was that there was enormous amount of currency flowing within the

economy, because of attractive demand banks be sure to loan the currency, however the

transactions of 2009 came regarding when the banks unsuccessful to gather all the cash back

they borrowed, as a result they decreased their lending that leads to fall down of large banks

within the market (Jones, 2016). In the end the result impacted the consumers that at the present

it became hard for them to get a mortgage as of banks. There are some government actions over

the give period of time that has effects on UK housing market. These will be explained as below:

Interest rates: This affect the paying cost for a mortgage. Interest Rate of Mortgage is the

most essential factor that has effect on housing prices. The interest payments cost on mortgage

relays on the interest rate which is set by the Bank of England. For example: if interest rates are

raised, the mortgage repayments costs rise this discourages people as of purchasing and it might

force persons to sell. Like in year 1992 interest rates were rise in excess of 12% that caused a big

fall within demand for housing as well as house prices fell. On the other hand, in year 2009

interest rates was cut very low around 1.5 percent but demand is still falling. Despite the fact that

it is inexpensive to pay finance, other than, this is overshadowing by the piece of evidence

mortgage accessibility is low (Lea, 2017).

Slower Market: This slowdown in activity brought on the government to do so, and

numerous measures had been introduced in a bid to stimulate more residence shopping for. In

2010, stamp obligation was abolished for first-time buyers, and in 2013, the assist to shop for

scheme was added, providing buyers an ‘fairness loan’ of 20 in line with cent of a property’s fee,

hobby-unfastened for the primary 5 years, supplied they may stump up a 5 consistent with cent

deposit.

8

Since the Wall Street crash during 1929, the situation of economies in 2009 was explained

as ‘the most horrible financial crisis. The credit crunch, failing banks, unemployment and

businesses led the financial system into a prolonged recession. The United Kingdom housing

market is cyclical as well as is quite recognizable with the busts and booms of the economic

cycle. The housing market of UK is fundamental sector within the economy. The performance of

country is closely related with the housing market performance. Before the crises the country’s

economy situation was that there was enormous amount of currency flowing within the

economy, because of attractive demand banks be sure to loan the currency, however the

transactions of 2009 came regarding when the banks unsuccessful to gather all the cash back

they borrowed, as a result they decreased their lending that leads to fall down of large banks

within the market (Jones, 2016). In the end the result impacted the consumers that at the present

it became hard for them to get a mortgage as of banks. There are some government actions over

the give period of time that has effects on UK housing market. These will be explained as below:

Interest rates: This affect the paying cost for a mortgage. Interest Rate of Mortgage is the

most essential factor that has effect on housing prices. The interest payments cost on mortgage

relays on the interest rate which is set by the Bank of England. For example: if interest rates are

raised, the mortgage repayments costs rise this discourages people as of purchasing and it might

force persons to sell. Like in year 1992 interest rates were rise in excess of 12% that caused a big

fall within demand for housing as well as house prices fell. On the other hand, in year 2009

interest rates was cut very low around 1.5 percent but demand is still falling. Despite the fact that

it is inexpensive to pay finance, other than, this is overshadowing by the piece of evidence

mortgage accessibility is low (Lea, 2017).

Slower Market: This slowdown in activity brought on the government to do so, and

numerous measures had been introduced in a bid to stimulate more residence shopping for. In

2010, stamp obligation was abolished for first-time buyers, and in 2013, the assist to shop for

scheme was added, providing buyers an ‘fairness loan’ of 20 in line with cent of a property’s fee,

hobby-unfastened for the primary 5 years, supplied they may stump up a 5 consistent with cent

deposit.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ascertainment of the potential impact of COVID-19 on UK Housing Market

Housing Market introduces to the demand and supply for houses, mainly within a specific

region or country. A key component of housing market of United Kingdom is the average house

prices as well as trend in houses prices. Along with this, COVID-19 is a financial crisis that has

negative impact on business, industry and an individual. This also have impact on UK housing

market by decreasing prices and rents of house. While British people within the middle of

purchasing a house can still turn, property screenings have been halted as well as estate agents'

offices have stopped up to the public as component of wide-ranging measures to decrease

COVID-19 infections. Prices of House across the United Kingdom fell at the highest rate

recently since the financial crisis or corona virus. The average price of a house dropped by 1.7

percent in May as of the earlier, to £218,902, as per the Nationwide, one of the United

Kingdom’s largest finance lenders. This comes after April’s increase of 0.9 percent and is the

largest monthly drop since February 2009, whilst the average cost of a house was around

£147,746. The annual increase charge slowed to at least one.8%, down from three.7% in April

and the slowest due to the fact December (Panagiotidis and Printzis, 2016).

The COVID-19 has halted the residential property market WITHIN United Kingdom.

After the government of the specific nation stopped house viewings as well as prevented real

estate agents as of promoting innovative properties, as a main part of broader moves to have the

pandemic’s spread. Amidst all of the uncertainty, both within the U.S. And round the world, we

felt it was extra vital than ever a good way to share our insights as it pertains to the global

housing financial system. COVID-19: Housing Market Updates will explore topics related to the

intersection of the corona virus pandemic and the economic system, housing marketplace and

danger.

There is vast uncertainty or issue surrounding the corona virus crisis. It is probable to have

long-lasting impacts on both Britain’s housing markets as well as housing policies. Prices and

rents of real house may fall within the medium and short term with no making housing less high-

priced. It will stay mainly excessive for the individual and those on lower incomes, particularly

in South East and the London, and for many people and industry hardest-hit by corona virus.

After it comes in the direction of housing policies, policymakers would be sensible not to skip on

the populist band-wagon. Along with this, COVID-19 has direct impact over housing market (Sá,

2016).

9

Housing Market introduces to the demand and supply for houses, mainly within a specific

region or country. A key component of housing market of United Kingdom is the average house

prices as well as trend in houses prices. Along with this, COVID-19 is a financial crisis that has

negative impact on business, industry and an individual. This also have impact on UK housing

market by decreasing prices and rents of house. While British people within the middle of

purchasing a house can still turn, property screenings have been halted as well as estate agents'

offices have stopped up to the public as component of wide-ranging measures to decrease

COVID-19 infections. Prices of House across the United Kingdom fell at the highest rate

recently since the financial crisis or corona virus. The average price of a house dropped by 1.7

percent in May as of the earlier, to £218,902, as per the Nationwide, one of the United

Kingdom’s largest finance lenders. This comes after April’s increase of 0.9 percent and is the

largest monthly drop since February 2009, whilst the average cost of a house was around

£147,746. The annual increase charge slowed to at least one.8%, down from three.7% in April

and the slowest due to the fact December (Panagiotidis and Printzis, 2016).

The COVID-19 has halted the residential property market WITHIN United Kingdom.

After the government of the specific nation stopped house viewings as well as prevented real

estate agents as of promoting innovative properties, as a main part of broader moves to have the

pandemic’s spread. Amidst all of the uncertainty, both within the U.S. And round the world, we

felt it was extra vital than ever a good way to share our insights as it pertains to the global

housing financial system. COVID-19: Housing Market Updates will explore topics related to the

intersection of the corona virus pandemic and the economic system, housing marketplace and

danger.

There is vast uncertainty or issue surrounding the corona virus crisis. It is probable to have

long-lasting impacts on both Britain’s housing markets as well as housing policies. Prices and

rents of real house may fall within the medium and short term with no making housing less high-

priced. It will stay mainly excessive for the individual and those on lower incomes, particularly

in South East and the London, and for many people and industry hardest-hit by corona virus.

After it comes in the direction of housing policies, policymakers would be sensible not to skip on

the populist band-wagon. Along with this, COVID-19 has direct impact over housing market (Sá,

2016).

9

CONCLUSION

It has been concluded from the above report that there is huge need of internal and

external business environment analysis for the purpose of ascertaining information about the

factors that have impact over organisations along with the market. This will provide the

opportunity to management that build the strategies through which they able to grab the growth

in market. The UK housing market is greatly impacted by the different internal external factors.

The average price of houses in UK is increases in between the time period of 2009 to 2019.

There are many external aspects that have impact over the UK housing market includes inflation,

financial crises, interest rate, mortgage and slower market growth. The role of government is also

very impactful regarding creating of external factors along with their simultaneous impact over

different markets. The government decision in respect of the mortgage and interest rates has the

direct impact over the UK housing market. It is also the duty over government that take such

measures that help in maintain the balance in the market so nobody gets unnecessary benefit of

some particular situation. The recent incident of Covid-19 also has the negative impact over UK

housing market where demand decreases. To overcome from this situation, government has to

intervene with the aid of effective measures trough which able to provide consistency to market.

10

It has been concluded from the above report that there is huge need of internal and

external business environment analysis for the purpose of ascertaining information about the

factors that have impact over organisations along with the market. This will provide the

opportunity to management that build the strategies through which they able to grab the growth

in market. The UK housing market is greatly impacted by the different internal external factors.

The average price of houses in UK is increases in between the time period of 2009 to 2019.

There are many external aspects that have impact over the UK housing market includes inflation,

financial crises, interest rate, mortgage and slower market growth. The role of government is also

very impactful regarding creating of external factors along with their simultaneous impact over

different markets. The government decision in respect of the mortgage and interest rates has the

direct impact over the UK housing market. It is also the duty over government that take such

measures that help in maintain the balance in the market so nobody gets unnecessary benefit of

some particular situation. The recent incident of Covid-19 also has the negative impact over UK

housing market where demand decreases. To overcome from this situation, government has to

intervene with the aid of effective measures trough which able to provide consistency to market.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.