Economics for Business: UK Housing Market Analysis and Policies

VerifiedAdded on 2021/04/21

|18

|3854

|454

Report

AI Summary

This report provides an in-depth analysis of the UK housing market, focusing on the period between 2006 and 2016. It examines various factors influencing housing prices, including GDP growth rate, unemployment rate, interest rates, consumer confidence, affordability, and demand. The report also investigates the impact of government schemes like 'Help to Buy,' 'Shared Ownership,' and 'Starter Homes' on the housing market. Through the analysis of these determinants, the report aims to provide a comprehensive understanding of the fluctuations in the UK housing market and the effectiveness of governmental policies in enhancing the welfare level of the country's residential sector. The report concludes by summarizing the key findings and offering insights into the complex interplay of economic factors and government interventions within the UK housing market.

Running head: ECONOMICS FOR BUSINESS

Economics for business

Name of the student:

Name of the university:

Author note

Economics for business

Name of the student:

Name of the university:

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMICS FOR BUSINESS

Executive summary:

United Kingdom is one of the developed nations in the world that has evolved itself through

considerable amount of market orientation in its economy since last two centuries. With raise

in the economic growth of the nation, christened through the industrial revolution of 18th

century, UK has faced enhanced pressure in its industrial sector. Rise in population through

backhand effect guided the economy to have better scope to withstand in the competitive

world. This report is aimed to discuss the various factors that have affected the UK housing

sector. In addition to this, this report is targeted to discuss the effect of the recent housing

policy initiatives by the UK government in order to enhance the welfare level of the country’s

residential. Through detailed analysis of the UK housing market it has been found that

various influential factors are there that has caused the fluctuation in the UK housing market.

One of the major factors that have caused the recent fluctuation in the UK housing market is

the rise in housing price in the country over the various regions. Amalgamation of the rise in

demand leading to price rise of the houses in the country has caused the fluctuation; however

several governmental policies have eased the situation. To conclude, it can be stated that over

the time there has been various fluctuation in the UK housing market, and it has to some

extent enhanced the welfare level through government housing policies; however whether it

has totally attained the desired outcome or not, it is subjective.

Executive summary:

United Kingdom is one of the developed nations in the world that has evolved itself through

considerable amount of market orientation in its economy since last two centuries. With raise

in the economic growth of the nation, christened through the industrial revolution of 18th

century, UK has faced enhanced pressure in its industrial sector. Rise in population through

backhand effect guided the economy to have better scope to withstand in the competitive

world. This report is aimed to discuss the various factors that have affected the UK housing

sector. In addition to this, this report is targeted to discuss the effect of the recent housing

policy initiatives by the UK government in order to enhance the welfare level of the country’s

residential. Through detailed analysis of the UK housing market it has been found that

various influential factors are there that has caused the fluctuation in the UK housing market.

One of the major factors that have caused the recent fluctuation in the UK housing market is

the rise in housing price in the country over the various regions. Amalgamation of the rise in

demand leading to price rise of the houses in the country has caused the fluctuation; however

several governmental policies have eased the situation. To conclude, it can be stated that over

the time there has been various fluctuation in the UK housing market, and it has to some

extent enhanced the welfare level through government housing policies; however whether it

has totally attained the desired outcome or not, it is subjective.

2ECONOMICS FOR BUSINESS

Table of Contents

Introduction:...............................................................................................................................3

Determinant factors of price of house in UK from 2006 to 2016:.............................................4

GDP growth rate:...................................................................................................................4

Unemployment rate:...............................................................................................................5

Interest rate:............................................................................................................................7

Consumer confidence:............................................................................................................8

Affordability range:................................................................................................................9

Demand of the houses:...........................................................................................................9

Impact of governmental schemes on housing market in UK:..................................................11

Help to Buy:.........................................................................................................................11

Shared ownership:................................................................................................................12

Starter Homes:......................................................................................................................12

Conclusion:..............................................................................................................................13

References:...............................................................................................................................15

Table of Contents

Introduction:...............................................................................................................................3

Determinant factors of price of house in UK from 2006 to 2016:.............................................4

GDP growth rate:...................................................................................................................4

Unemployment rate:...............................................................................................................5

Interest rate:............................................................................................................................7

Consumer confidence:............................................................................................................8

Affordability range:................................................................................................................9

Demand of the houses:...........................................................................................................9

Impact of governmental schemes on housing market in UK:..................................................11

Help to Buy:.........................................................................................................................11

Shared ownership:................................................................................................................12

Starter Homes:......................................................................................................................12

Conclusion:..............................................................................................................................13

References:...............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMICS FOR BUSINESS

Introduction:

United Kingdom is one of the developed nations in the world that has evolved itself

through considerable amount of market orientation in its economy since last two centuries.

According to the nominal GDP growth the country stands as the sixth largest economy and

when the Purchasing Power Parity is considered, then the economy is the ninth largest in the

world (Taylor 2016). Higher economic growth over the period of the nation has been

germinated through periodical development of the country’s infrastructural development

leading it towards the sustainability. Over the year the nation has faced immense

development leading it to become the second largest economy in the European Union (EU)

that has aided the UK to become where it is now. This immense growth in the UK economy

has helped the nation to curtail various macroeconomic variables, which has provided it

required sustainability and growth prospect (Spash 2014).

With raise in the economic growth of the nation, christened through the industrial

revolution of 18th century, UK has faced enhanced pressure in its industrial sector (Burawoy

2015). In addition to this economic prosperity of the country has provided it an upward rise in

the population of the country. Rise in population through backhand effect guided the

economy to have better scope to withstand in the competitive world. One of the major factors

that have aided the country to become where it is now is the changing dynamics in the

housing sector (Wilcox and Perry 2014). It has acted as the stimuli for the economic growth

of the country. Over the time, there has been immense amount of fluctuation in the housing

sector of the UK; however, a vast amount of fluctuation can be observed during the 2006 to

2016 session. Considering this scenario, this report is aimed to discuss the various factors that

have affected the UK housing sector. In addition to this, this report is targeted to discuss the

effect of the recent housing policy initiatives by the UK government in order to enhance the

welfare level of the country’s residential.

Introduction:

United Kingdom is one of the developed nations in the world that has evolved itself

through considerable amount of market orientation in its economy since last two centuries.

According to the nominal GDP growth the country stands as the sixth largest economy and

when the Purchasing Power Parity is considered, then the economy is the ninth largest in the

world (Taylor 2016). Higher economic growth over the period of the nation has been

germinated through periodical development of the country’s infrastructural development

leading it towards the sustainability. Over the year the nation has faced immense

development leading it to become the second largest economy in the European Union (EU)

that has aided the UK to become where it is now. This immense growth in the UK economy

has helped the nation to curtail various macroeconomic variables, which has provided it

required sustainability and growth prospect (Spash 2014).

With raise in the economic growth of the nation, christened through the industrial

revolution of 18th century, UK has faced enhanced pressure in its industrial sector (Burawoy

2015). In addition to this economic prosperity of the country has provided it an upward rise in

the population of the country. Rise in population through backhand effect guided the

economy to have better scope to withstand in the competitive world. One of the major factors

that have aided the country to become where it is now is the changing dynamics in the

housing sector (Wilcox and Perry 2014). It has acted as the stimuli for the economic growth

of the country. Over the time, there has been immense amount of fluctuation in the housing

sector of the UK; however, a vast amount of fluctuation can be observed during the 2006 to

2016 session. Considering this scenario, this report is aimed to discuss the various factors that

have affected the UK housing sector. In addition to this, this report is targeted to discuss the

effect of the recent housing policy initiatives by the UK government in order to enhance the

welfare level of the country’s residential.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMICS FOR BUSINESS

Determinant factors of price of house in UK from 2006 to 2016:

Various factors are there that has caused the fluctuation in the UK housing sector. For

instance, over the time factors like housing supply, housing demand, affordability, GDP

growth rate and income has been the major factors that caused fluctuation in the UK housing

sector (Sa 2015). Considering the given time scenario of 2006 to 2016 it can be stated that it

was one of the golden age of the UK housing sector. During this time the market has faced its

highest growth as well as faced highest amount of booking for the new houses too. Well,

moving forward this section will elaborate the various determinants of the factors of price of

the UK housing sector.

GDP growth rate:

One of the main factors that determine the UK housing price is the GDP growth rate.

According to the economic theories, if there is rise in economic growth rate, then it will lead

to rise in the national income too (Pigou 2017). With better national income it will be easy for

the citizen to buy new houses. One the other hand, if there is rise in national income, then it

will lead to rise in the demand, which ultimately cause in the rise in price too. Thus,

economic growth can lead the economy towards a social dilemma, where enhancing price and

rising demand take at same time and the price will be determined whether the supply demand

equilibrium takes place.

Determinant factors of price of house in UK from 2006 to 2016:

Various factors are there that has caused the fluctuation in the UK housing sector. For

instance, over the time factors like housing supply, housing demand, affordability, GDP

growth rate and income has been the major factors that caused fluctuation in the UK housing

sector (Sa 2015). Considering the given time scenario of 2006 to 2016 it can be stated that it

was one of the golden age of the UK housing sector. During this time the market has faced its

highest growth as well as faced highest amount of booking for the new houses too. Well,

moving forward this section will elaborate the various determinants of the factors of price of

the UK housing sector.

GDP growth rate:

One of the main factors that determine the UK housing price is the GDP growth rate.

According to the economic theories, if there is rise in economic growth rate, then it will lead

to rise in the national income too (Pigou 2017). With better national income it will be easy for

the citizen to buy new houses. One the other hand, if there is rise in national income, then it

will lead to rise in the demand, which ultimately cause in the rise in price too. Thus,

economic growth can lead the economy towards a social dilemma, where enhancing price and

rising demand take at same time and the price will be determined whether the supply demand

equilibrium takes place.

5ECONOMICS FOR BUSINESS

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

-5

-4

-3

-2

-1

0

1

2

3

4

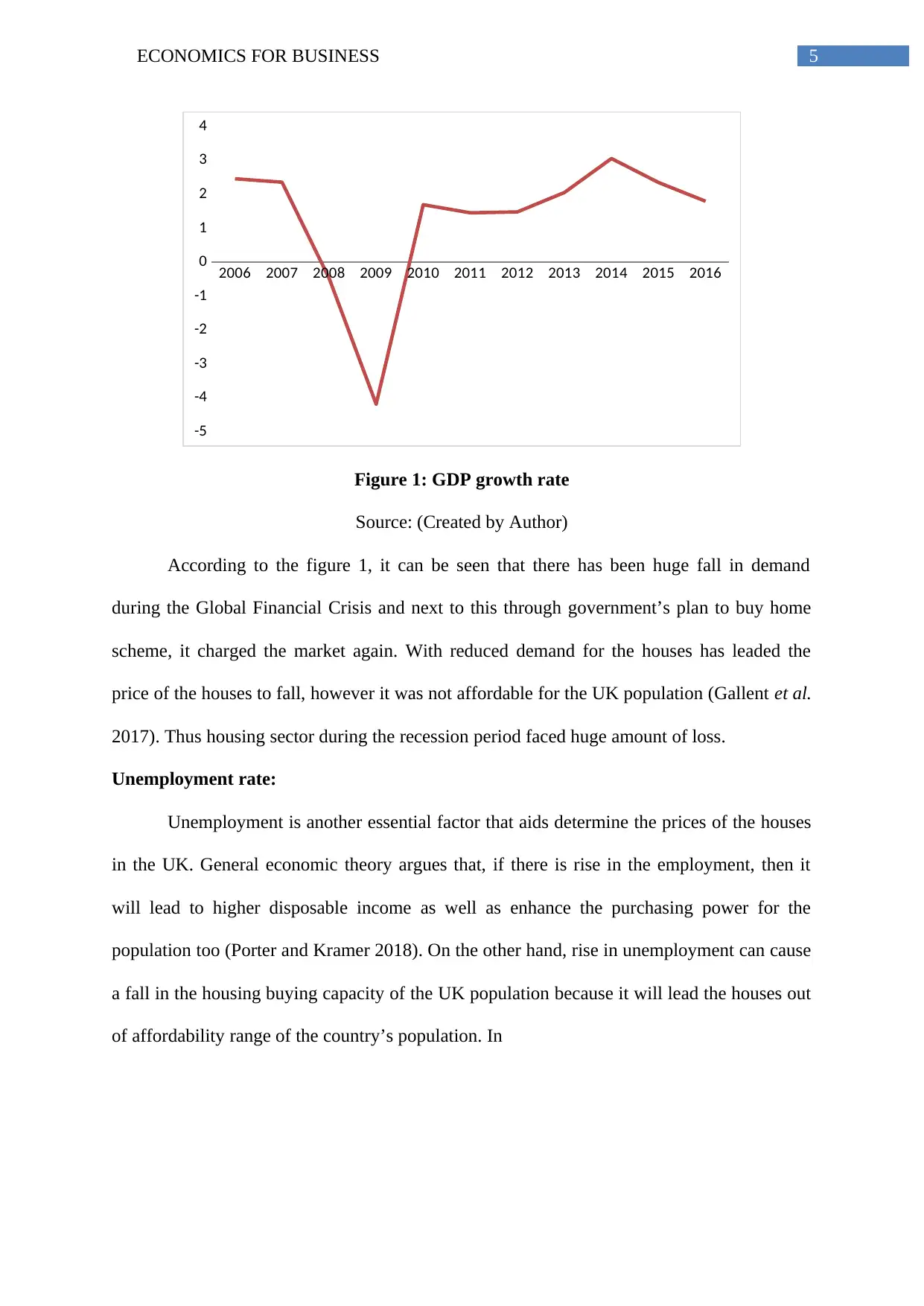

Figure 1: GDP growth rate

Source: (Created by Author)

According to the figure 1, it can be seen that there has been huge fall in demand

during the Global Financial Crisis and next to this through government’s plan to buy home

scheme, it charged the market again. With reduced demand for the houses has leaded the

price of the houses to fall, however it was not affordable for the UK population (Gallent et al.

2017). Thus housing sector during the recession period faced huge amount of loss.

Unemployment rate:

Unemployment is another essential factor that aids determine the prices of the houses

in the UK. General economic theory argues that, if there is rise in the employment, then it

will lead to higher disposable income as well as enhance the purchasing power for the

population too (Porter and Kramer 2018). On the other hand, rise in unemployment can cause

a fall in the housing buying capacity of the UK population because it will lead the houses out

of affordability range of the country’s population. In

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

-5

-4

-3

-2

-1

0

1

2

3

4

Figure 1: GDP growth rate

Source: (Created by Author)

According to the figure 1, it can be seen that there has been huge fall in demand

during the Global Financial Crisis and next to this through government’s plan to buy home

scheme, it charged the market again. With reduced demand for the houses has leaded the

price of the houses to fall, however it was not affordable for the UK population (Gallent et al.

2017). Thus housing sector during the recession period faced huge amount of loss.

Unemployment rate:

Unemployment is another essential factor that aids determine the prices of the houses

in the UK. General economic theory argues that, if there is rise in the employment, then it

will lead to higher disposable income as well as enhance the purchasing power for the

population too (Porter and Kramer 2018). On the other hand, rise in unemployment can cause

a fall in the housing buying capacity of the UK population because it will lead the houses out

of affordability range of the country’s population. In

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ECONOMICS FOR BUSINESS

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

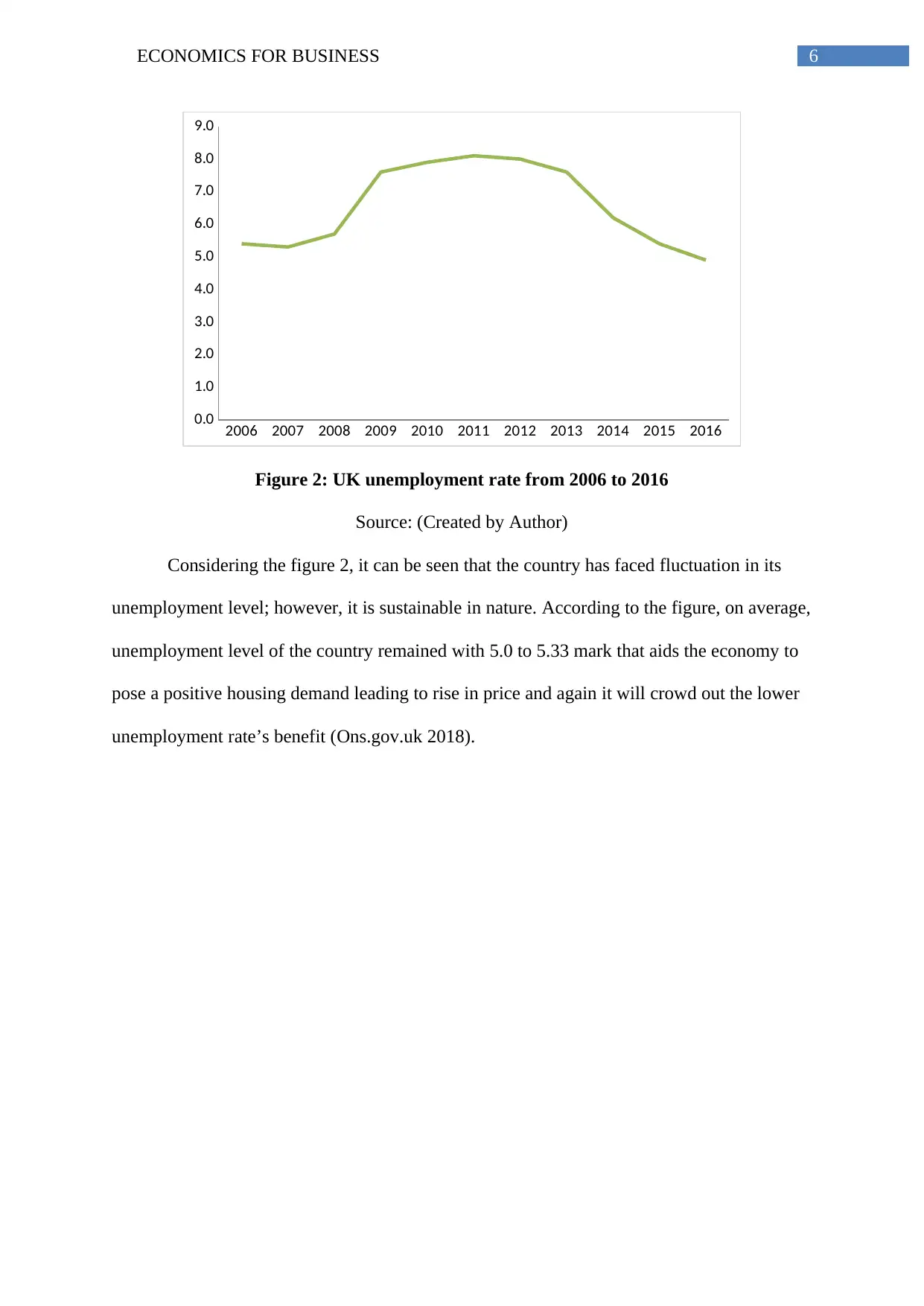

Figure 2: UK unemployment rate from 2006 to 2016

Source: (Created by Author)

Considering the figure 2, it can be seen that the country has faced fluctuation in its

unemployment level; however, it is sustainable in nature. According to the figure, on average,

unemployment level of the country remained with 5.0 to 5.33 mark that aids the economy to

pose a positive housing demand leading to rise in price and again it will crowd out the lower

unemployment rate’s benefit (Ons.gov.uk 2018).

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Figure 2: UK unemployment rate from 2006 to 2016

Source: (Created by Author)

Considering the figure 2, it can be seen that the country has faced fluctuation in its

unemployment level; however, it is sustainable in nature. According to the figure, on average,

unemployment level of the country remained with 5.0 to 5.33 mark that aids the economy to

pose a positive housing demand leading to rise in price and again it will crowd out the lower

unemployment rate’s benefit (Ons.gov.uk 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS FOR BUSINESS

2006 Q1

2006 Q3

2007 Q1

2007 Q3

2008 Q1

2008 Q3

2009 Q1

2009 Q3

2010 Q1

2010 Q3

2011 Q1

2011 Q3

2012 Q1

2012 Q3

2013 Q1

2013 Q3

2014 Q1

2014 Q3

2015 Q1

2015 Q3

2016 Q1

2016 Q3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

UK North London Wales

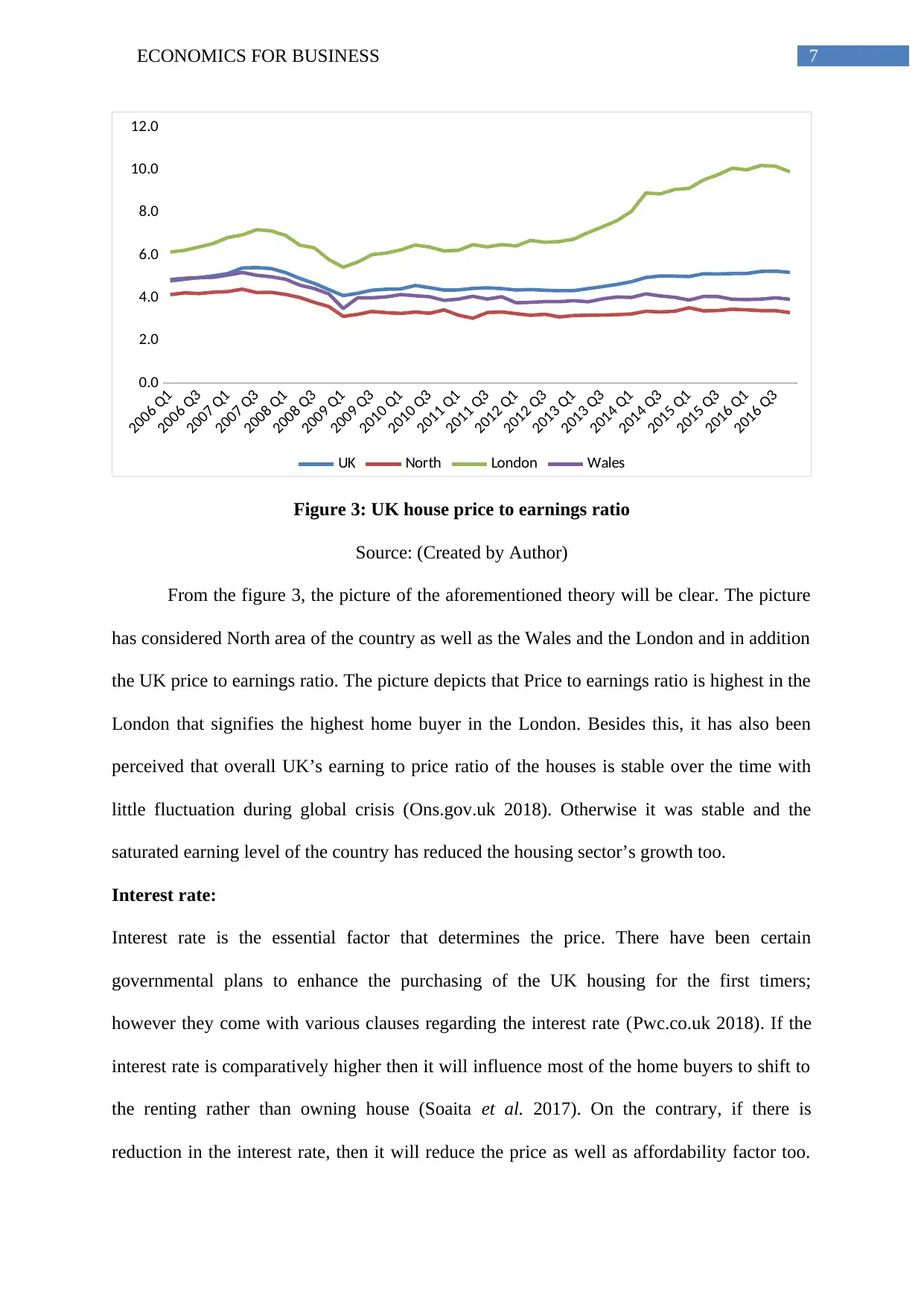

Figure 3: UK house price to earnings ratio

Source: (Created by Author)

From the figure 3, the picture of the aforementioned theory will be clear. The picture

has considered North area of the country as well as the Wales and the London and in addition

the UK price to earnings ratio. The picture depicts that Price to earnings ratio is highest in the

London that signifies the highest home buyer in the London. Besides this, it has also been

perceived that overall UK’s earning to price ratio of the houses is stable over the time with

little fluctuation during global crisis (Ons.gov.uk 2018). Otherwise it was stable and the

saturated earning level of the country has reduced the housing sector’s growth too.

Interest rate:

Interest rate is the essential factor that determines the price. There have been certain

governmental plans to enhance the purchasing of the UK housing for the first timers;

however they come with various clauses regarding the interest rate (Pwc.co.uk 2018). If the

interest rate is comparatively higher then it will influence most of the home buyers to shift to

the renting rather than owning house (Soaita et al. 2017). On the contrary, if there is

reduction in the interest rate, then it will reduce the price as well as affordability factor too.

2006 Q1

2006 Q3

2007 Q1

2007 Q3

2008 Q1

2008 Q3

2009 Q1

2009 Q3

2010 Q1

2010 Q3

2011 Q1

2011 Q3

2012 Q1

2012 Q3

2013 Q1

2013 Q3

2014 Q1

2014 Q3

2015 Q1

2015 Q3

2016 Q1

2016 Q3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

UK North London Wales

Figure 3: UK house price to earnings ratio

Source: (Created by Author)

From the figure 3, the picture of the aforementioned theory will be clear. The picture

has considered North area of the country as well as the Wales and the London and in addition

the UK price to earnings ratio. The picture depicts that Price to earnings ratio is highest in the

London that signifies the highest home buyer in the London. Besides this, it has also been

perceived that overall UK’s earning to price ratio of the houses is stable over the time with

little fluctuation during global crisis (Ons.gov.uk 2018). Otherwise it was stable and the

saturated earning level of the country has reduced the housing sector’s growth too.

Interest rate:

Interest rate is the essential factor that determines the price. There have been certain

governmental plans to enhance the purchasing of the UK housing for the first timers;

however they come with various clauses regarding the interest rate (Pwc.co.uk 2018). If the

interest rate is comparatively higher then it will influence most of the home buyers to shift to

the renting rather than owning house (Soaita et al. 2017). On the contrary, if there is

reduction in the interest rate, then it will reduce the price as well as affordability factor too.

8ECONOMICS FOR BUSINESS

With enhanced scope for reduced interest rate, the housing sector can attract higher number

of buyers.

Consumer confidence:

Over the time during the selected time frame there have been various price changes in

the UK housing sector. Fluctuation in the price range can affect the consumer confidence

through direct relation and thus with the fluctuation in the UK housing market, consumer

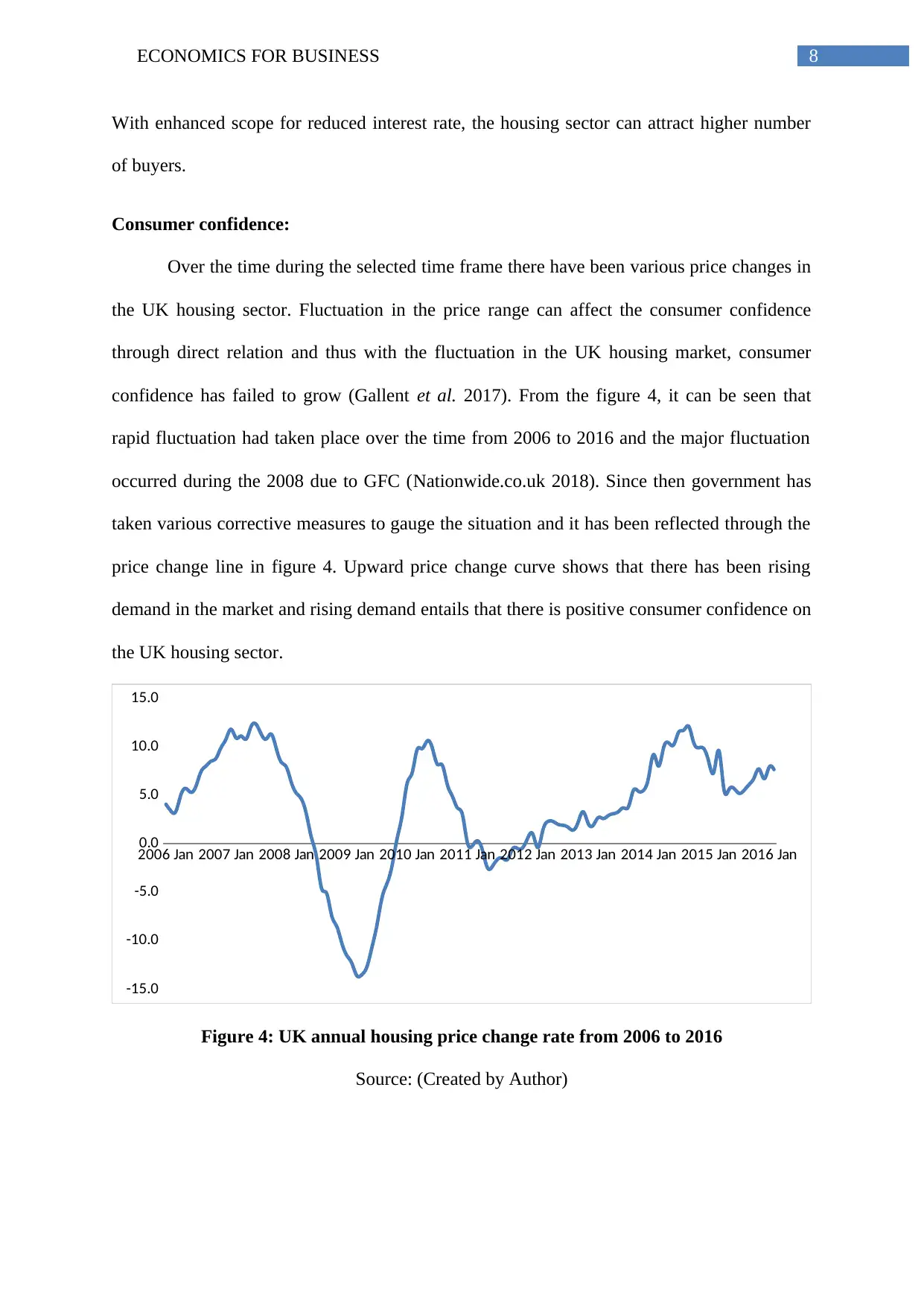

confidence has failed to grow (Gallent et al. 2017). From the figure 4, it can be seen that

rapid fluctuation had taken place over the time from 2006 to 2016 and the major fluctuation

occurred during the 2008 due to GFC (Nationwide.co.uk 2018). Since then government has

taken various corrective measures to gauge the situation and it has been reflected through the

price change line in figure 4. Upward price change curve shows that there has been rising

demand in the market and rising demand entails that there is positive consumer confidence on

the UK housing sector.

2006 Jan 2007 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012 Jan 2013 Jan 2014 Jan 2015 Jan 2016 Jan

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

Figure 4: UK annual housing price change rate from 2006 to 2016

Source: (Created by Author)

With enhanced scope for reduced interest rate, the housing sector can attract higher number

of buyers.

Consumer confidence:

Over the time during the selected time frame there have been various price changes in

the UK housing sector. Fluctuation in the price range can affect the consumer confidence

through direct relation and thus with the fluctuation in the UK housing market, consumer

confidence has failed to grow (Gallent et al. 2017). From the figure 4, it can be seen that

rapid fluctuation had taken place over the time from 2006 to 2016 and the major fluctuation

occurred during the 2008 due to GFC (Nationwide.co.uk 2018). Since then government has

taken various corrective measures to gauge the situation and it has been reflected through the

price change line in figure 4. Upward price change curve shows that there has been rising

demand in the market and rising demand entails that there is positive consumer confidence on

the UK housing sector.

2006 Jan 2007 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012 Jan 2013 Jan 2014 Jan 2015 Jan 2016 Jan

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

Figure 4: UK annual housing price change rate from 2006 to 2016

Source: (Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMICS FOR BUSINESS

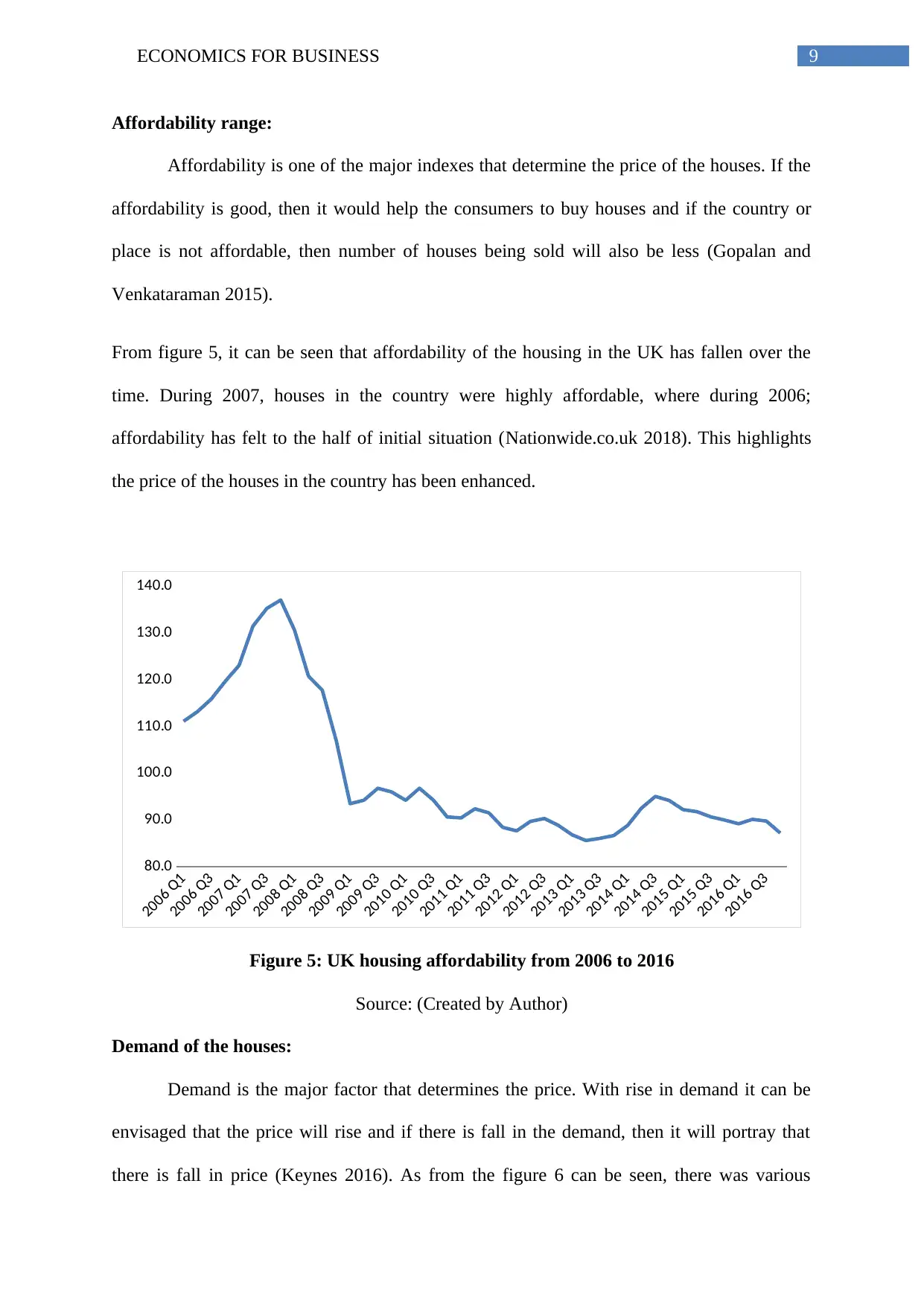

Affordability range:

Affordability is one of the major indexes that determine the price of the houses. If the

affordability is good, then it would help the consumers to buy houses and if the country or

place is not affordable, then number of houses being sold will also be less (Gopalan and

Venkataraman 2015).

From figure 5, it can be seen that affordability of the housing in the UK has fallen over the

time. During 2007, houses in the country were highly affordable, where during 2006;

affordability has felt to the half of initial situation (Nationwide.co.uk 2018). This highlights

the price of the houses in the country has been enhanced.

2006 Q1

2006 Q3

2007 Q1

2007 Q3

2008 Q1

2008 Q3

2009 Q1

2009 Q3

2010 Q1

2010 Q3

2011 Q1

2011 Q3

2012 Q1

2012 Q3

2013 Q1

2013 Q3

2014 Q1

2014 Q3

2015 Q1

2015 Q3

2016 Q1

2016 Q3

80.0

90.0

100.0

110.0

120.0

130.0

140.0

Figure 5: UK housing affordability from 2006 to 2016

Source: (Created by Author)

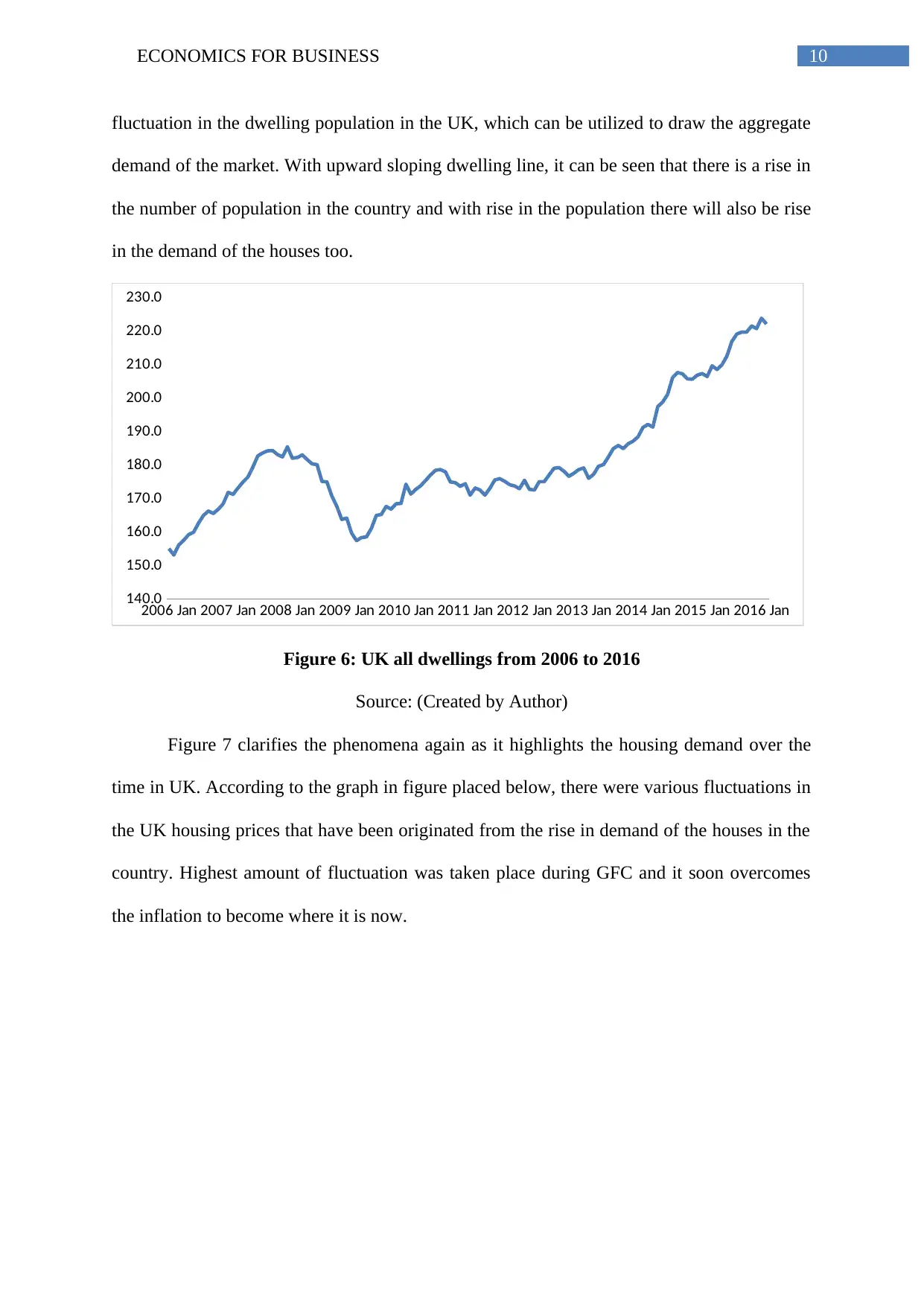

Demand of the houses:

Demand is the major factor that determines the price. With rise in demand it can be

envisaged that the price will rise and if there is fall in the demand, then it will portray that

there is fall in price (Keynes 2016). As from the figure 6 can be seen, there was various

Affordability range:

Affordability is one of the major indexes that determine the price of the houses. If the

affordability is good, then it would help the consumers to buy houses and if the country or

place is not affordable, then number of houses being sold will also be less (Gopalan and

Venkataraman 2015).

From figure 5, it can be seen that affordability of the housing in the UK has fallen over the

time. During 2007, houses in the country were highly affordable, where during 2006;

affordability has felt to the half of initial situation (Nationwide.co.uk 2018). This highlights

the price of the houses in the country has been enhanced.

2006 Q1

2006 Q3

2007 Q1

2007 Q3

2008 Q1

2008 Q3

2009 Q1

2009 Q3

2010 Q1

2010 Q3

2011 Q1

2011 Q3

2012 Q1

2012 Q3

2013 Q1

2013 Q3

2014 Q1

2014 Q3

2015 Q1

2015 Q3

2016 Q1

2016 Q3

80.0

90.0

100.0

110.0

120.0

130.0

140.0

Figure 5: UK housing affordability from 2006 to 2016

Source: (Created by Author)

Demand of the houses:

Demand is the major factor that determines the price. With rise in demand it can be

envisaged that the price will rise and if there is fall in the demand, then it will portray that

there is fall in price (Keynes 2016). As from the figure 6 can be seen, there was various

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMICS FOR BUSINESS

fluctuation in the dwelling population in the UK, which can be utilized to draw the aggregate

demand of the market. With upward sloping dwelling line, it can be seen that there is a rise in

the number of population in the country and with rise in the population there will also be rise

in the demand of the houses too.

2006 Jan 2007 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012 Jan 2013 Jan 2014 Jan 2015 Jan 2016 Jan

140.0

150.0

160.0

170.0

180.0

190.0

200.0

210.0

220.0

230.0

Figure 6: UK all dwellings from 2006 to 2016

Source: (Created by Author)

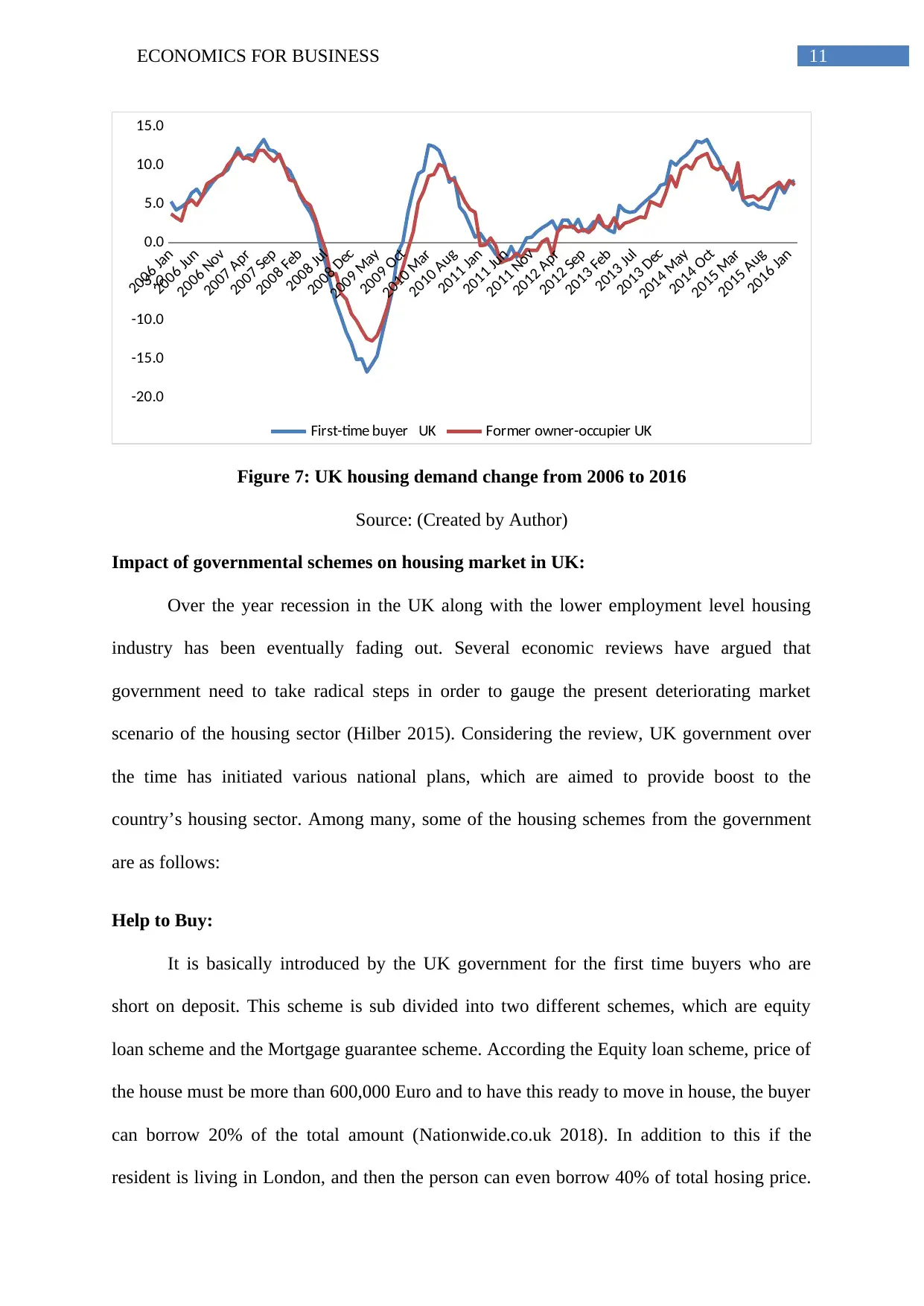

Figure 7 clarifies the phenomena again as it highlights the housing demand over the

time in UK. According to the graph in figure placed below, there were various fluctuations in

the UK housing prices that have been originated from the rise in demand of the houses in the

country. Highest amount of fluctuation was taken place during GFC and it soon overcomes

the inflation to become where it is now.

fluctuation in the dwelling population in the UK, which can be utilized to draw the aggregate

demand of the market. With upward sloping dwelling line, it can be seen that there is a rise in

the number of population in the country and with rise in the population there will also be rise

in the demand of the houses too.

2006 Jan 2007 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012 Jan 2013 Jan 2014 Jan 2015 Jan 2016 Jan

140.0

150.0

160.0

170.0

180.0

190.0

200.0

210.0

220.0

230.0

Figure 6: UK all dwellings from 2006 to 2016

Source: (Created by Author)

Figure 7 clarifies the phenomena again as it highlights the housing demand over the

time in UK. According to the graph in figure placed below, there were various fluctuations in

the UK housing prices that have been originated from the rise in demand of the houses in the

country. Highest amount of fluctuation was taken place during GFC and it soon overcomes

the inflation to become where it is now.

11ECONOMICS FOR BUSINESS

2006 Jan

2006 Jun

2006 Nov

2007 Apr

2007 Sep

2008 Feb

2008 Jul

2008 Dec

2009 May

2009 Oct

2010 Mar

2010 Aug

2011 Jan

2011 Jun

2011 Nov

2012 Apr

2012 Sep

2013 Feb

2013 Jul

2013 Dec

2014 May

2014 Oct

2015 Mar

2015 Aug

2016 Jan

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

First-time buyer UK Former owner-occupier UK

Figure 7: UK housing demand change from 2006 to 2016

Source: (Created by Author)

Impact of governmental schemes on housing market in UK:

Over the year recession in the UK along with the lower employment level housing

industry has been eventually fading out. Several economic reviews have argued that

government need to take radical steps in order to gauge the present deteriorating market

scenario of the housing sector (Hilber 2015). Considering the review, UK government over

the time has initiated various national plans, which are aimed to provide boost to the

country’s housing sector. Among many, some of the housing schemes from the government

are as follows:

Help to Buy:

It is basically introduced by the UK government for the first time buyers who are

short on deposit. This scheme is sub divided into two different schemes, which are equity

loan scheme and the Mortgage guarantee scheme. According the Equity loan scheme, price of

the house must be more than 600,000 Euro and to have this ready to move in house, the buyer

can borrow 20% of the total amount (Nationwide.co.uk 2018). In addition to this if the

resident is living in London, and then the person can even borrow 40% of total hosing price.

2006 Jan

2006 Jun

2006 Nov

2007 Apr

2007 Sep

2008 Feb

2008 Jul

2008 Dec

2009 May

2009 Oct

2010 Mar

2010 Aug

2011 Jan

2011 Jun

2011 Nov

2012 Apr

2012 Sep

2013 Feb

2013 Jul

2013 Dec

2014 May

2014 Oct

2015 Mar

2015 Aug

2016 Jan

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

First-time buyer UK Former owner-occupier UK

Figure 7: UK housing demand change from 2006 to 2016

Source: (Created by Author)

Impact of governmental schemes on housing market in UK:

Over the year recession in the UK along with the lower employment level housing

industry has been eventually fading out. Several economic reviews have argued that

government need to take radical steps in order to gauge the present deteriorating market

scenario of the housing sector (Hilber 2015). Considering the review, UK government over

the time has initiated various national plans, which are aimed to provide boost to the

country’s housing sector. Among many, some of the housing schemes from the government

are as follows:

Help to Buy:

It is basically introduced by the UK government for the first time buyers who are

short on deposit. This scheme is sub divided into two different schemes, which are equity

loan scheme and the Mortgage guarantee scheme. According the Equity loan scheme, price of

the house must be more than 600,000 Euro and to have this ready to move in house, the buyer

can borrow 20% of the total amount (Nationwide.co.uk 2018). In addition to this if the

resident is living in London, and then the person can even borrow 40% of total hosing price.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.