Analysis of the UK Housing Market and Economic Determinants (BABS)

VerifiedAdded on 2023/01/10

|14

|3863

|55

Report

AI Summary

This report provides an analysis of the UK housing market, focusing on the period from 2009 to 2019. It examines the changes in average house prices during this time, highlighting regional variations and overall market trends. The report delves into the economic determinants influencing these changes, including real income growth, interest rates, housing supply, mortgage costs, and availability. It also explores the impact of government actions and policies on the housing market, as well as predictions on how the COVID-19 pandemic will affect the market. The analysis covers factors like the Brexit referendum, movements along the demand curve, speculation, supply constraints, and employment and earnings, providing a comprehensive overview of the forces shaping the UK housing landscape.

Contemporary

Business Environment

Business Environment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Average house prices in the UK changed over the period from 2009 – 2019........................3

Economic determinants of the changes outlined ...................................................................7

Government action over the period 2009-2019 affected the UK Housing market...............10

Impact of COVID-19 on Housing market of UK.................................................................10

CONCLUSION ...................................................................................................................13

REFERNCES.................................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Average house prices in the UK changed over the period from 2009 – 2019........................3

Economic determinants of the changes outlined ...................................................................7

Government action over the period 2009-2019 affected the UK Housing market...............10

Impact of COVID-19 on Housing market of UK.................................................................10

CONCLUSION ...................................................................................................................13

REFERNCES.................................................................................................................................14

INTRODUCTION

There has been lot of changes that are taking pale in the external environment of a

organisation and it consist of many different factors that are impacting the economy of a

organisation. Present report is based on the way average house prices have changes across these

years from 2009 to 2019 (Hwang, Cho and Shin, 2019). further there is discussion on the

economic determinants of the changes that have taken place all these years. There are certain

actions that have been taken by government in this period and has impacted the housing market

of UK. Further there is a prediction on the impact of COVID-19 pandemic is gong to impact the

housing market of UK in the coming future period of time. All these are economic determinants

that can poses a impact on the organisation and will have both positive & negative impact on its

functioning.

TASK

Average house prices in the UK changed over the period from 2009 – 2019

The office for statistic regulation designated the UK house price Index (HPI) as national

statistics on September 18.

House price inflation is defined as a rate according to residential properties that are

acquired in UK are rising of falling. The HPI of UK is a combined production by Registers of

Scotland, Property services northern Ireland, HM land registry and national statistics office. The

HPI of UK consist of all residential properties that are purchased from market and value in UK.

Sales only appearing in UK when purchases are registered and there can be a delay in

transactions feed in the index (Gong, Hu,and Boelhouwer, 2018).

The average housing prices have increased in UK by 0.9% in June 2019 and it was same

since may 2019. it can be seen that over past three years there has been a slowdown in housing

prices growth in UK and it is driven by a slowdown in east of England and South.

For example: Savills that is managing residential and commercial proprieties around world has

said that there are very few houses that have been sold in UK in the first part of six months of

year 2019 than any point in the first half of year 2009 the declines are observed in London where

the prices are falling after inflation. The normal prices of the homes that have been sold by

There has been lot of changes that are taking pale in the external environment of a

organisation and it consist of many different factors that are impacting the economy of a

organisation. Present report is based on the way average house prices have changes across these

years from 2009 to 2019 (Hwang, Cho and Shin, 2019). further there is discussion on the

economic determinants of the changes that have taken place all these years. There are certain

actions that have been taken by government in this period and has impacted the housing market

of UK. Further there is a prediction on the impact of COVID-19 pandemic is gong to impact the

housing market of UK in the coming future period of time. All these are economic determinants

that can poses a impact on the organisation and will have both positive & negative impact on its

functioning.

TASK

Average house prices in the UK changed over the period from 2009 – 2019

The office for statistic regulation designated the UK house price Index (HPI) as national

statistics on September 18.

House price inflation is defined as a rate according to residential properties that are

acquired in UK are rising of falling. The HPI of UK is a combined production by Registers of

Scotland, Property services northern Ireland, HM land registry and national statistics office. The

HPI of UK consist of all residential properties that are purchased from market and value in UK.

Sales only appearing in UK when purchases are registered and there can be a delay in

transactions feed in the index (Gong, Hu,and Boelhouwer, 2018).

The average housing prices have increased in UK by 0.9% in June 2019 and it was same

since may 2019. it can be seen that over past three years there has been a slowdown in housing

prices growth in UK and it is driven by a slowdown in east of England and South.

For example: Savills that is managing residential and commercial proprieties around world has

said that there are very few houses that have been sold in UK in the first part of six months of

year 2019 than any point in the first half of year 2009 the declines are observed in London where

the prices are falling after inflation. The normal prices of the homes that have been sold by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Savills fall by 32perdcent to 2.1 million pounds in initial six months 2019 as compared to year

2018.

The lowest growth can be seen in London where the prices have fallen by 2.7 percent in June

2019. and there was a less than 3.1 percent that was seen in the may 2019. the average housing

prices in London are also falling since since march 2018.

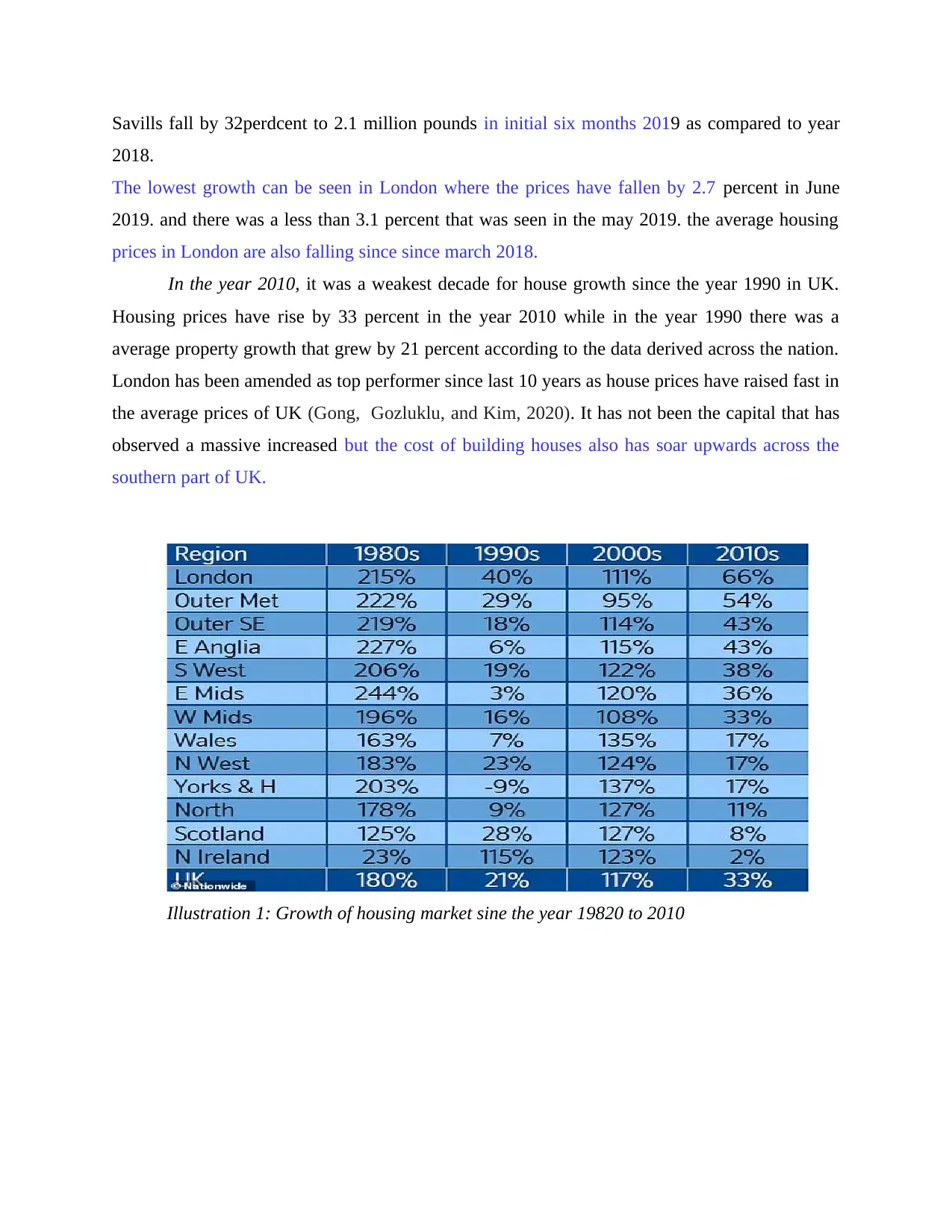

In the year 2010, it was a weakest decade for house growth since the year 1990 in UK.

Housing prices have rise by 33 percent in the year 2010 while in the year 1990 there was a

average property growth that grew by 21 percent according to the data derived across the nation.

London has been amended as top performer since last 10 years as house prices have raised fast in

the average prices of UK (Gong, Gozluklu, and Kim, 2020). It has not been the capital that has

observed a massive increased but the cost of building houses also has soar upwards across the

southern part of UK.

Illustration 1: Growth of housing market sine the year 19820 to 2010

2018.

The lowest growth can be seen in London where the prices have fallen by 2.7 percent in June

2019. and there was a less than 3.1 percent that was seen in the may 2019. the average housing

prices in London are also falling since since march 2018.

In the year 2010, it was a weakest decade for house growth since the year 1990 in UK.

Housing prices have rise by 33 percent in the year 2010 while in the year 1990 there was a

average property growth that grew by 21 percent according to the data derived across the nation.

London has been amended as top performer since last 10 years as house prices have raised fast in

the average prices of UK (Gong, Gozluklu, and Kim, 2020). It has not been the capital that has

observed a massive increased but the cost of building houses also has soar upwards across the

southern part of UK.

Illustration 1: Growth of housing market sine the year 19820 to 2010

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

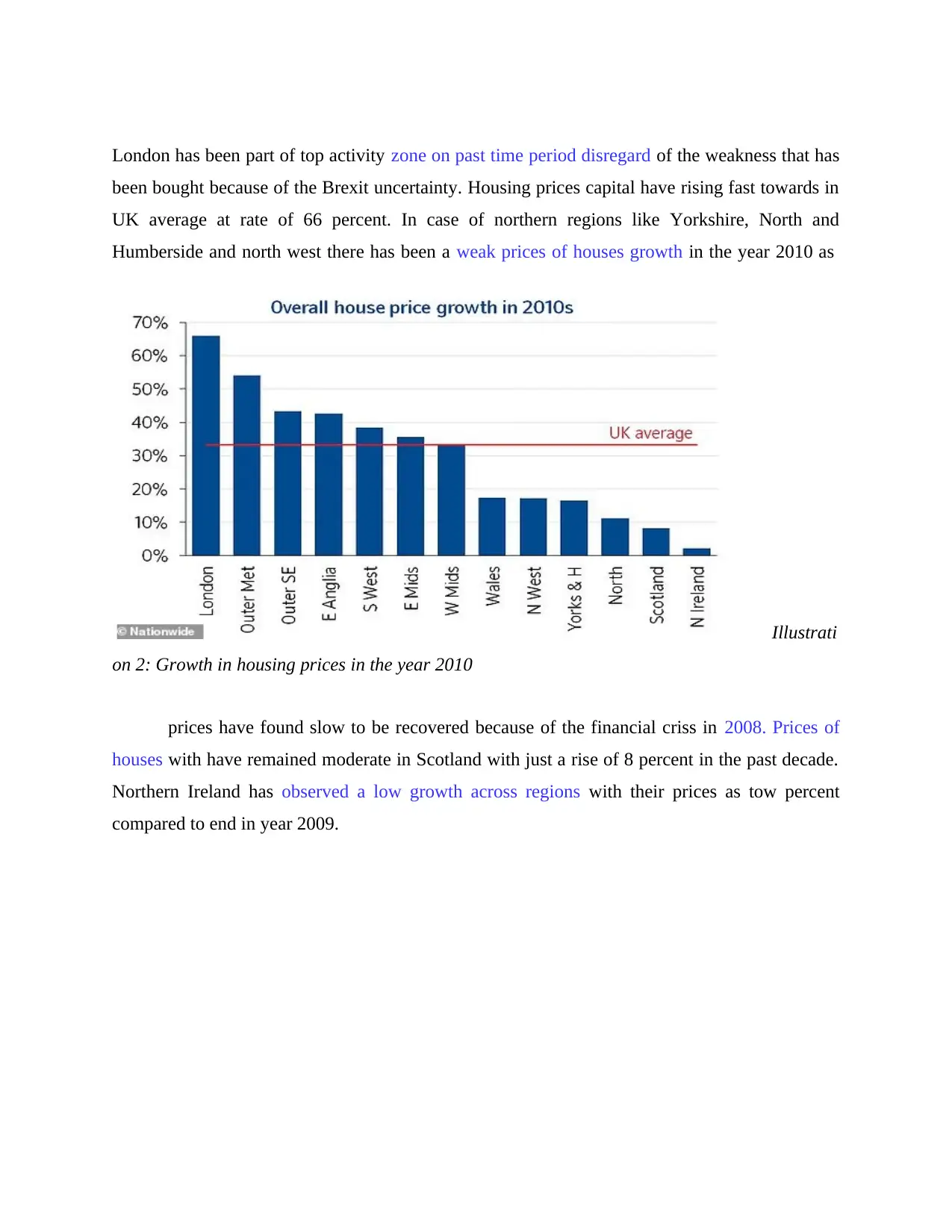

London has been part of top activity zone on past time period disregard of the weakness that has

been bought because of the Brexit uncertainty. Housing prices capital have rising fast towards in

UK average at rate of 66 percent. In case of northern regions like Yorkshire, North and

Humberside and north west there has been a weak prices of houses growth in the year 2010 as

prices have found slow to be recovered because of the financial criss in 2008. Prices of

houses with have remained moderate in Scotland with just a rise of 8 percent in the past decade.

Northern Ireland has observed a low growth across regions with their prices as tow percent

compared to end in year 2009.

Illustrati

on 2: Growth in housing prices in the year 2010

been bought because of the Brexit uncertainty. Housing prices capital have rising fast towards in

UK average at rate of 66 percent. In case of northern regions like Yorkshire, North and

Humberside and north west there has been a weak prices of houses growth in the year 2010 as

prices have found slow to be recovered because of the financial criss in 2008. Prices of

houses with have remained moderate in Scotland with just a rise of 8 percent in the past decade.

Northern Ireland has observed a low growth across regions with their prices as tow percent

compared to end in year 2009.

Illustrati

on 2: Growth in housing prices in the year 2010

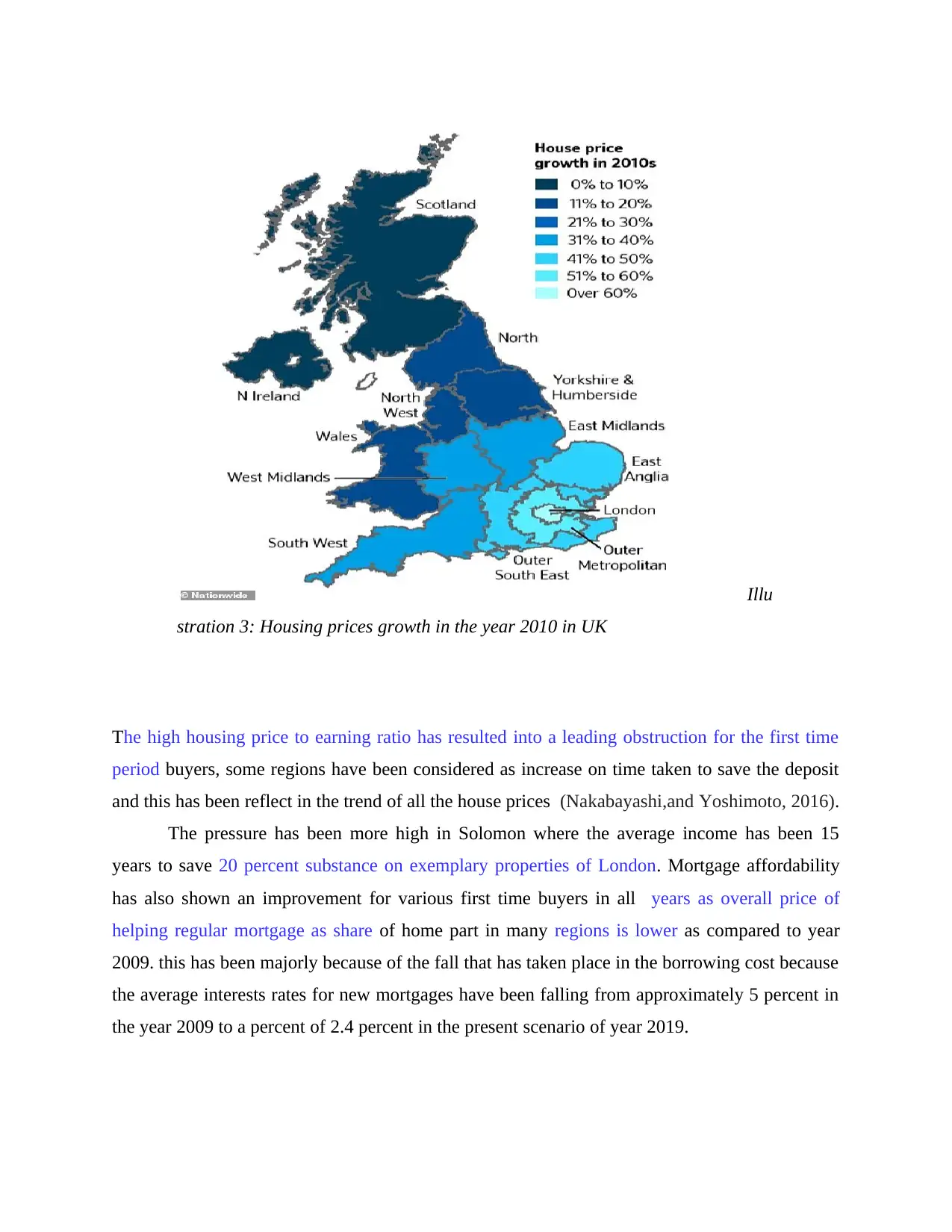

The high housing price to earning ratio has resulted into a leading obstruction for the first time

period buyers, some regions have been considered as increase on time taken to save the deposit

and this has been reflect in the trend of all the house prices (Nakabayashi,and Yoshimoto, 2016).

The pressure has been more high in Solomon where the average income has been 15

years to save 20 percent substance on exemplary properties of London. Mortgage affordability

has also shown an improvement for various first time buyers in all years as overall price of

helping regular mortgage as share of home part in many regions is lower as compared to year

2009. this has been majorly because of the fall that has taken place in the borrowing cost because

the average interests rates for new mortgages have been falling from approximately 5 percent in

the year 2009 to a percent of 2.4 percent in the present scenario of year 2019.

Illu

stration 3: Housing prices growth in the year 2010 in UK

period buyers, some regions have been considered as increase on time taken to save the deposit

and this has been reflect in the trend of all the house prices (Nakabayashi,and Yoshimoto, 2016).

The pressure has been more high in Solomon where the average income has been 15

years to save 20 percent substance on exemplary properties of London. Mortgage affordability

has also shown an improvement for various first time buyers in all years as overall price of

helping regular mortgage as share of home part in many regions is lower as compared to year

2009. this has been majorly because of the fall that has taken place in the borrowing cost because

the average interests rates for new mortgages have been falling from approximately 5 percent in

the year 2009 to a percent of 2.4 percent in the present scenario of year 2019.

Illu

stration 3: Housing prices growth in the year 2010 in UK

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Economic determinants of the changes outlined

There are certain economic determinants that are related to the changes that are taking

place in the housing market of UK. That has resulted into the changes that have occurred

between the year 2009 to 2019. some of these economic determinants are mentioned below:

Real income growth: In the year 1991, the aggregate income of household was

approximately 754 billion pounds. In the year 2016 aggregate disposable income was

approx 1,320 billion pounds. This has shown that there has been a real terms of increase

of 75%. this has lead to addition in the construction prices to be increased by 150 percent

between the year 1991 & 2016 (Analysis of the determinants of house price changes,

2018).

Interest rate reduction: There has been a scenario of falling Interest rates between year

1991 & 2016. this has estimated relationships between the level of interest rates that has

changed in the market and there are many crucial changes that have been in the observed

market in the mortgage market that consist of mortgage regulation and there exists a

relationship between interest rates and mortgage rates (Adams, 2020). These are some

of the changes that are part of scale and denotes that a model is estimated for earlier time

period that has affected the housing market of UK. Interest rates are crucial determination

of housing prices and it must be anticipated that there will be a decrease in the Interest

rates that have been experienced over the time period from 1991 to the year 2016. other

things are among constant this has lead to enhancement in demand for hosing and lead a

pressure on the prices of houses (Analysis of the determinants of house price changes,

2018)

Housing supply: In the year 2016 the housing stock or the dwelling stock in England

was approx 23.7 million. There has been a enhancement of housing stick between these

years that has estimated to be approximately 4.1 million and is 200.6 percent. The

increase in the housing supply is expected to lead the housing prices to be reduce by 40

% when all other aspects are constant (Analysis of the determinants of house price

changes, 2018) .

Mortgages cost: In period of 1990 mortgages rates were very low. People used to afford

larger mortgages & they were able to purchase costly houses. In year 2009 mortgages

There are certain economic determinants that are related to the changes that are taking

place in the housing market of UK. That has resulted into the changes that have occurred

between the year 2009 to 2019. some of these economic determinants are mentioned below:

Real income growth: In the year 1991, the aggregate income of household was

approximately 754 billion pounds. In the year 2016 aggregate disposable income was

approx 1,320 billion pounds. This has shown that there has been a real terms of increase

of 75%. this has lead to addition in the construction prices to be increased by 150 percent

between the year 1991 & 2016 (Analysis of the determinants of house price changes,

2018).

Interest rate reduction: There has been a scenario of falling Interest rates between year

1991 & 2016. this has estimated relationships between the level of interest rates that has

changed in the market and there are many crucial changes that have been in the observed

market in the mortgage market that consist of mortgage regulation and there exists a

relationship between interest rates and mortgage rates (Adams, 2020). These are some

of the changes that are part of scale and denotes that a model is estimated for earlier time

period that has affected the housing market of UK. Interest rates are crucial determination

of housing prices and it must be anticipated that there will be a decrease in the Interest

rates that have been experienced over the time period from 1991 to the year 2016. other

things are among constant this has lead to enhancement in demand for hosing and lead a

pressure on the prices of houses (Analysis of the determinants of house price changes,

2018)

Housing supply: In the year 2016 the housing stock or the dwelling stock in England

was approx 23.7 million. There has been a enhancement of housing stick between these

years that has estimated to be approximately 4.1 million and is 200.6 percent. The

increase in the housing supply is expected to lead the housing prices to be reduce by 40

% when all other aspects are constant (Analysis of the determinants of house price

changes, 2018) .

Mortgages cost: In period of 1990 mortgages rates were very low. People used to afford

larger mortgages & they were able to purchase costly houses. In year 2009 mortgages

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

rate have shown a very high rise and many people have faced difficulty in maintaining

their existing payments system. In 2003 mortgages rate were again reduced and this lead

to more fuelling demand for houses. Interest rates rise in the period 2004-2007 but in the

year 2008-2009 there were higher mortgage rates that lead to a scenario of people not

able to a national statistics supply mortgaged and this lead to a situation of initial

downturn in the housing industry of UK (The Different Determinants Of House Prices

Economics Essay, 2020).).

Mortgage availability: In the scenario of housing boom between year 2003-2007

mortgages were promptly accessible. House rising price, building & bank societies were

ready to accept small deposits & lend a larger double people income. Borrowers to

default and lenders had a very good chances of getting money back. In year 2008

building societies and banks were more cautious for granting mortgages. As they alert

that falling housing prices, growing situations of negative equity, rising unemployment

lead to a high danger that borrowers might default their payment. In the year 2008-2009

this problem was related to credit crunch and banks had less amount to lend (The

Different Determinants Of House Prices Economics Essay, 2020).

Brexit referendum: In UK both commercial and sales of residential property have

faded since June 2016 because of Brexit referendum. Prices are still rising on average

across different parts of UK and has rise by 1.2 percent in may year 2019 as compared to

1.5 percent in April in 2019. there has been a move to online purchases that has lead to

shoppers diverting away from various local streets that has resulted in sales outlet

closures (UK housing market at its weakest point in a decade, says Savills, 2020).

Movements along the demand curve: If there is alteration in demand determinants apart

from the price changes that there is a effect on price change that is depicted by the

movement taking place across the economic process curve. If there is change in any of

determinants that new demand curve has to be created. If change is part of a determinant

than it can leads to rise in price raise and whole curve can also shift towards right

(Morley, and Thomas, 2018). This clearly shown that price are more than there will be

high demand. In the housing market of UK the price rise has lead to shifting of the

demand curve towards right in last few years since 2009-2015 and the fall of housing

prices have lead to curve shift towards left.

their existing payments system. In 2003 mortgages rate were again reduced and this lead

to more fuelling demand for houses. Interest rates rise in the period 2004-2007 but in the

year 2008-2009 there were higher mortgage rates that lead to a scenario of people not

able to a national statistics supply mortgaged and this lead to a situation of initial

downturn in the housing industry of UK (The Different Determinants Of House Prices

Economics Essay, 2020).).

Mortgage availability: In the scenario of housing boom between year 2003-2007

mortgages were promptly accessible. House rising price, building & bank societies were

ready to accept small deposits & lend a larger double people income. Borrowers to

default and lenders had a very good chances of getting money back. In year 2008

building societies and banks were more cautious for granting mortgages. As they alert

that falling housing prices, growing situations of negative equity, rising unemployment

lead to a high danger that borrowers might default their payment. In the year 2008-2009

this problem was related to credit crunch and banks had less amount to lend (The

Different Determinants Of House Prices Economics Essay, 2020).

Brexit referendum: In UK both commercial and sales of residential property have

faded since June 2016 because of Brexit referendum. Prices are still rising on average

across different parts of UK and has rise by 1.2 percent in may year 2019 as compared to

1.5 percent in April in 2019. there has been a move to online purchases that has lead to

shoppers diverting away from various local streets that has resulted in sales outlet

closures (UK housing market at its weakest point in a decade, says Savills, 2020).

Movements along the demand curve: If there is alteration in demand determinants apart

from the price changes that there is a effect on price change that is depicted by the

movement taking place across the economic process curve. If there is change in any of

determinants that new demand curve has to be created. If change is part of a determinant

than it can leads to rise in price raise and whole curve can also shift towards right

(Morley, and Thomas, 2018). This clearly shown that price are more than there will be

high demand. In the housing market of UK the price rise has lead to shifting of the

demand curve towards right in last few years since 2009-2015 and the fall of housing

prices have lead to curve shift towards left.

Speculation in Housing market of UK: There is high demand has been because of the

market sentiment apart from economic fundamentals. The sentiment of market has

transformed as people are now less confident about buying houses. It has been stated in

reports that 15 percent of UL houses prices have not reflected properly in the system

basic principle but as speculation & froth. As the housing price fall there is no incentive

that is left to buy and people are ready and waiting for the housing prices to fall ( The

Different Determinants Of House Prices Economics Essay, 2020).

Supply constraints: The housing market of UK is suffering from sever supply

constraints that has affected total stock of housing. There are many new houses that are

but are relatively small. There is requirement of a change in demand can be enlarged that

changes in prices. There is requirement of very little growth of demand to enhance the

prices but it takes very small fall in demand and it leads to a important fall in prices in

1991.

Employment & earnings: There have been high level of employments in the financial

services sector and there has been a tremendous growth in the UK housing sector. There

has been a rise in big culture of bonus in city that has crated a upwards pressure on

prices rising on the London property market and it has spilled over all different countries

and regions in UK (Payne, 2020).

Demographic: There has been a shift towards acceleration in one person households that

has a positive impact on the demand of housing in these new years. For example in UK in

year 2008 there was a estimate 3.6 million one individual house and now are engaged in

England that represent approximately 25 percent of owner occupied dwellings, growth of

housing is estimated to enhance by 221,000 households every year on coming time period

of 20 years that is further impact the prices and demand in UK housing industry (What

influences house prices and why do governments, 2008).

Above discussed are some of the economic determinants that has affected the housing industry

of UK in all the recent changes that are taking place in the industry.

Government action over the period 2009-2019 affected the UK Housing market

There are several actions that have been taken by government of UK so that they are able to

manage the UK housing market and trends flourishing as mentioned below:

market sentiment apart from economic fundamentals. The sentiment of market has

transformed as people are now less confident about buying houses. It has been stated in

reports that 15 percent of UL houses prices have not reflected properly in the system

basic principle but as speculation & froth. As the housing price fall there is no incentive

that is left to buy and people are ready and waiting for the housing prices to fall ( The

Different Determinants Of House Prices Economics Essay, 2020).

Supply constraints: The housing market of UK is suffering from sever supply

constraints that has affected total stock of housing. There are many new houses that are

but are relatively small. There is requirement of a change in demand can be enlarged that

changes in prices. There is requirement of very little growth of demand to enhance the

prices but it takes very small fall in demand and it leads to a important fall in prices in

1991.

Employment & earnings: There have been high level of employments in the financial

services sector and there has been a tremendous growth in the UK housing sector. There

has been a rise in big culture of bonus in city that has crated a upwards pressure on

prices rising on the London property market and it has spilled over all different countries

and regions in UK (Payne, 2020).

Demographic: There has been a shift towards acceleration in one person households that

has a positive impact on the demand of housing in these new years. For example in UK in

year 2008 there was a estimate 3.6 million one individual house and now are engaged in

England that represent approximately 25 percent of owner occupied dwellings, growth of

housing is estimated to enhance by 221,000 households every year on coming time period

of 20 years that is further impact the prices and demand in UK housing industry (What

influences house prices and why do governments, 2008).

Above discussed are some of the economic determinants that has affected the housing industry

of UK in all the recent changes that are taking place in the industry.

Government action over the period 2009-2019 affected the UK Housing market

There are several actions that have been taken by government of UK so that they are able to

manage the UK housing market and trends flourishing as mentioned below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

UK housing market has been at faint point starting of the global business criss that tool

place a decade ago because if the Brexit scenario because of the uncertainty of buyers. It is the

responsibility of Bank of England and Monetary policy committee (MPC) to set interest rates in

UK the government has made efforts to prevent the prices to be rising for housing industry of

UK by taking certain measures like bailing out banks and increasing the lending to Northern rock

and RBS. MPC is also making efforts to cut down the interest rates for making the borrowing

more cheaper. Government has enhanced the pressure level on banks to cut their rates. Reduction

in VAT rates and more spending can result into recession. Government has also intervened to for

correcting the market failure and achievement of higher greater degree by making the availability

of quality housing and stock. Housing is a very important aspects having relation with wealth

distribution because housing is considered as merit good (Kimand Chung, 2017).

In UK there has been a emphasis on regulation and social policy. There has been

development of housing act 1980 and this gave local authority a “right to buy”. There has been

high regulations in mortgage finance market to ensure that the market failure is from excess sub

prime lending in recent years. Self certification mortgages have also been banned under some

proposals with a view of lenders required to verify the borrowers income.

Impact of COVID-19 on Housing market of UK

The housing market of UK is thrown in a deep freeze because of the spread of COVID-19

virus and there are predictions that it will not be recorded in a period of coming one year from

now. Many people are in middle of buying houses are still willing to move but geographical area

position have been affected and many estate representative have sealed their offices as a

measures to reduce the spread of disease.

Houses prices have been rising since the starting of year 2020 and though there have been

many large uncertainness like political uncertainties and Brexit impact but there has been a

opposite trend in the year 2020 (Coronavirus brings UK housing market to near standstill: RICS,

2020). future sales expectation for the coming time period of three months are now weakest.

According to views of Paul Cheshire and Christian Hilber, there is a need to develop a

understanding of the impact on Rents and the real housing prices that might fall in the coming

future period of few years. There has been use of three time horizons to develop a detail

understanding of the impact of COVID-19 on the housing market of UK.

place a decade ago because if the Brexit scenario because of the uncertainty of buyers. It is the

responsibility of Bank of England and Monetary policy committee (MPC) to set interest rates in

UK the government has made efforts to prevent the prices to be rising for housing industry of

UK by taking certain measures like bailing out banks and increasing the lending to Northern rock

and RBS. MPC is also making efforts to cut down the interest rates for making the borrowing

more cheaper. Government has enhanced the pressure level on banks to cut their rates. Reduction

in VAT rates and more spending can result into recession. Government has also intervened to for

correcting the market failure and achievement of higher greater degree by making the availability

of quality housing and stock. Housing is a very important aspects having relation with wealth

distribution because housing is considered as merit good (Kimand Chung, 2017).

In UK there has been a emphasis on regulation and social policy. There has been

development of housing act 1980 and this gave local authority a “right to buy”. There has been

high regulations in mortgage finance market to ensure that the market failure is from excess sub

prime lending in recent years. Self certification mortgages have also been banned under some

proposals with a view of lenders required to verify the borrowers income.

Impact of COVID-19 on Housing market of UK

The housing market of UK is thrown in a deep freeze because of the spread of COVID-19

virus and there are predictions that it will not be recorded in a period of coming one year from

now. Many people are in middle of buying houses are still willing to move but geographical area

position have been affected and many estate representative have sealed their offices as a

measures to reduce the spread of disease.

Houses prices have been rising since the starting of year 2020 and though there have been

many large uncertainness like political uncertainties and Brexit impact but there has been a

opposite trend in the year 2020 (Coronavirus brings UK housing market to near standstill: RICS,

2020). future sales expectation for the coming time period of three months are now weakest.

According to views of Paul Cheshire and Christian Hilber, there is a need to develop a

understanding of the impact on Rents and the real housing prices that might fall in the coming

future period of few years. There has been use of three time horizons to develop a detail

understanding of the impact of COVID-19 on the housing market of UK.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Short term: There can be rise that will be driven by real income & a supply of living

accommodations in various larger parts nation. The house supply will be intransigent as the

planning system might by dysfunctional & the system of localized government to provide

finance virtually no incentives for different might license improvement. The COVID-19 criss

will produce a stasis as buying & selling will stop. After there has been no situation of low-down

then also transaction volume will fall substantially (COVID-19 and housing, 2020).

Construction of new houses will be restricted and there will be three major issues.

Borrowers income getting hit

Falling of real income with people

minimization of forced sales

Medium term: The scenario of buying a home will be postponed by many people as

prices might appear to be more affordable (Brener, 2020). The economic downturn is triggered

by COVID-19 impact according to the situations of great Britain in 1930. the building of social

living accommodations may be a bit resurgence. But the lower housing prices will nor lead to

improvement of affordability in the medium term and the main cause could have been depleted

savings and lower incomes (Sá, 2016).

Long term: There can be a situation of innovation boost that is communication

technology. Construction of houses is forecast to remain below the level required to satisfy the

situations of demand. People are willing to have preference for more work from home scenario

that can have two major implications like first people will demand more houses and second the

computing cost may become less. There can be a movement towards a cheaper land Spain that

can accept longer commute (Bracke, and Tenreyro, 2020). There can be a trend of higher paid

jobs and demand for housing might increase in cities like Hex-ham, Exeter, Norwich, Oxford,

Cambridge and there will be a house price pressures in such locations (COVID-19 and housing,

2020).

It can be said that there will be a impact on housing policies & housing markets., Real

house prices might fall in short & medium period of time without making houses few

unaffordable, areas of south east & London are hardest affected by COVID-19.

accommodations in various larger parts nation. The house supply will be intransigent as the

planning system might by dysfunctional & the system of localized government to provide

finance virtually no incentives for different might license improvement. The COVID-19 criss

will produce a stasis as buying & selling will stop. After there has been no situation of low-down

then also transaction volume will fall substantially (COVID-19 and housing, 2020).

Construction of new houses will be restricted and there will be three major issues.

Borrowers income getting hit

Falling of real income with people

minimization of forced sales

Medium term: The scenario of buying a home will be postponed by many people as

prices might appear to be more affordable (Brener, 2020). The economic downturn is triggered

by COVID-19 impact according to the situations of great Britain in 1930. the building of social

living accommodations may be a bit resurgence. But the lower housing prices will nor lead to

improvement of affordability in the medium term and the main cause could have been depleted

savings and lower incomes (Sá, 2016).

Long term: There can be a situation of innovation boost that is communication

technology. Construction of houses is forecast to remain below the level required to satisfy the

situations of demand. People are willing to have preference for more work from home scenario

that can have two major implications like first people will demand more houses and second the

computing cost may become less. There can be a movement towards a cheaper land Spain that

can accept longer commute (Bracke, and Tenreyro, 2020). There can be a trend of higher paid

jobs and demand for housing might increase in cities like Hex-ham, Exeter, Norwich, Oxford,

Cambridge and there will be a house price pressures in such locations (COVID-19 and housing,

2020).

It can be said that there will be a impact on housing policies & housing markets., Real

house prices might fall in short & medium period of time without making houses few

unaffordable, areas of south east & London are hardest affected by COVID-19.

CONCLUSION

There is a requirement of policy relaxation of true causes so that there can be because of

situation of affordability criss and long term reforms can be deal effectively. In these past few

years there has been a consistent modification in prices of houses in UK. Housing market and

fortunates of economy are interdependent to each other. A powerful economy has a very

optimistic impact on the certainty of congresses, confidence and wealth. This leads to a positive

impact on prices and demand in the housing market. Falling housing prices lead to reduction in

consumer wealth and crates a negative impact on consumer confidence and consumer spending.

All this leads to reduction in overall injections in the circular income flow between consumers

and producers in UK. There has been a complete prospective change for future because of the

impact related with the COVID-19 virus.

There is a requirement of policy relaxation of true causes so that there can be because of

situation of affordability criss and long term reforms can be deal effectively. In these past few

years there has been a consistent modification in prices of houses in UK. Housing market and

fortunates of economy are interdependent to each other. A powerful economy has a very

optimistic impact on the certainty of congresses, confidence and wealth. This leads to a positive

impact on prices and demand in the housing market. Falling housing prices lead to reduction in

consumer wealth and crates a negative impact on consumer confidence and consumer spending.

All this leads to reduction in overall injections in the circular income flow between consumers

and producers in UK. There has been a complete prospective change for future because of the

impact related with the COVID-19 virus.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.