UK Housing Market: Economic Determinants and COVID-19 Impact

VerifiedAdded on 2023/01/11

|15

|3672

|49

Report

AI Summary

This report delves into the UK housing market, examining the fluctuations in average house prices from 2009 to 2019. It identifies key economic determinants such as mortgage rates, supply and demand, income, interest rates, unemployment, economic growth, and consumer confidence that influence housing prices. The report also analyzes the effects of government actions during this period, including policies aimed at increasing housing supply and addressing affordability. Furthermore, it predicts the potential impact of COVID-19 on the UK housing market, considering factors like economic downturn, changes in consumer behavior, and shifts in investment patterns. The analysis covers the impact of the pandemic on the market, providing insights into the challenges and opportunities facing the housing sector. The report concludes with recommendations for policymakers and stakeholders to navigate the evolving housing landscape.

Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ABSTRACT

In present time most of the countries are facing problem of COVID-19 that impact on

economy in direct manner. In context of UK, the housing market fall down and various factors

that impact on the in direct manner. These variables are impact on the housing market and

market goes down. From the year 2009 to 2019 various changes are coming in this sector and

government also taken some action that impact on this sector. The COVID-19 disease how to

impact on the whole market especially housing market in negative manner.

In present time most of the countries are facing problem of COVID-19 that impact on

economy in direct manner. In context of UK, the housing market fall down and various factors

that impact on the in direct manner. These variables are impact on the housing market and

market goes down. From the year 2009 to 2019 various changes are coming in this sector and

government also taken some action that impact on this sector. The COVID-19 disease how to

impact on the whole market especially housing market in negative manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contents

ABSTRACT................................................................................................................................................2

INTRODUCTION.......................................................................................................................................5

MAIN BODY..............................................................................................................................................5

1. How have average house prices in the UK changed over the period from 2009 to 2019.....................5

2. What are the economic determinates of the changes............................................................................7

3. How has government action over the period 2009-2019 affected the UK housing market?...............10

4. Predict what would be the impact of COVID – 19 on UK housing market........................................11

RECOMMENDATIONS...........................................................................................................................12

CONCLUSION.........................................................................................................................................13

REFERENCES..........................................................................................................................................14

ABSTRACT................................................................................................................................................2

INTRODUCTION.......................................................................................................................................5

MAIN BODY..............................................................................................................................................5

1. How have average house prices in the UK changed over the period from 2009 to 2019.....................5

2. What are the economic determinates of the changes............................................................................7

3. How has government action over the period 2009-2019 affected the UK housing market?...............10

4. Predict what would be the impact of COVID – 19 on UK housing market........................................11

RECOMMENDATIONS...........................................................................................................................12

CONCLUSION.........................................................................................................................................13

REFERENCES..........................................................................................................................................14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

The housing market pertains to the housing affordability, generally in a given nation or

area. A main feature of the housing market is housing listed prices and housing market rate.

Property market implies a system of dealers seeking to invest properties and a matching buyer

system able to buy residences (Tsai, 2018). This report based on the average prices of UK

housing market that fluctuate in different years. This report contains 2009 to 2019 changes in

housing market, determinates, impact of COVID-19.

MAIN BODY

1. How have average house prices in the UK changed over the period from 2009 to 2019

The 2010s have been the least effective century since the 1990s for house price inflation,

early study is revealing. House prices rose 33 per cent in the 2010s, while the average property

fell 21 per cent in valuation in the 1990s, as per Nationwide statistics. The new house price

statistics released by HM Land Registry on GOV.UK for November 2019 indicate that property

prices in the United Kingdom rose by 2.2 percent in the year until November 2019, from 1.3

percent in the year until October 2019. In the UK, housing prices grew by 0.9 per cent in the year

until June 2019, steady in may 2019. There's been a huge decline in UK real wage growth during

the last 3 years, led primarily by a downturn in England's east and south. The smallest yearly

increase came in London, where rates fell to June 2019 by 2.7 per cent across the year, smaller

than the 3.1 per cent decline in May 2019. Every other couple of weeks since March 2018,

average housing prices in London have now fallen throughout the year.

With such an estimate of 157.2 thousand British pounds, the smallest costs for residences

in the UK were seen at the start of 2009. The average property price went up every other time

since January 2013. Since about February 2020 the economy actually stood, the average

household income in the UK was 230.3 thousand British pounds. Among both 2013 and 2014,

the largest rise in property prices since 2007 was reported, when property values rose by nearly

nine %.

The housing market pertains to the housing affordability, generally in a given nation or

area. A main feature of the housing market is housing listed prices and housing market rate.

Property market implies a system of dealers seeking to invest properties and a matching buyer

system able to buy residences (Tsai, 2018). This report based on the average prices of UK

housing market that fluctuate in different years. This report contains 2009 to 2019 changes in

housing market, determinates, impact of COVID-19.

MAIN BODY

1. How have average house prices in the UK changed over the period from 2009 to 2019

The 2010s have been the least effective century since the 1990s for house price inflation,

early study is revealing. House prices rose 33 per cent in the 2010s, while the average property

fell 21 per cent in valuation in the 1990s, as per Nationwide statistics. The new house price

statistics released by HM Land Registry on GOV.UK for November 2019 indicate that property

prices in the United Kingdom rose by 2.2 percent in the year until November 2019, from 1.3

percent in the year until October 2019. In the UK, housing prices grew by 0.9 per cent in the year

until June 2019, steady in may 2019. There's been a huge decline in UK real wage growth during

the last 3 years, led primarily by a downturn in England's east and south. The smallest yearly

increase came in London, where rates fell to June 2019 by 2.7 per cent across the year, smaller

than the 3.1 per cent decline in May 2019. Every other couple of weeks since March 2018,

average housing prices in London have now fallen throughout the year.

With such an estimate of 157.2 thousand British pounds, the smallest costs for residences

in the UK were seen at the start of 2009. The average property price went up every other time

since January 2013. Since about February 2020 the economy actually stood, the average

household income in the UK was 230.3 thousand British pounds. Among both 2013 and 2014,

the largest rise in property prices since 2007 was reported, when property values rose by nearly

nine %.

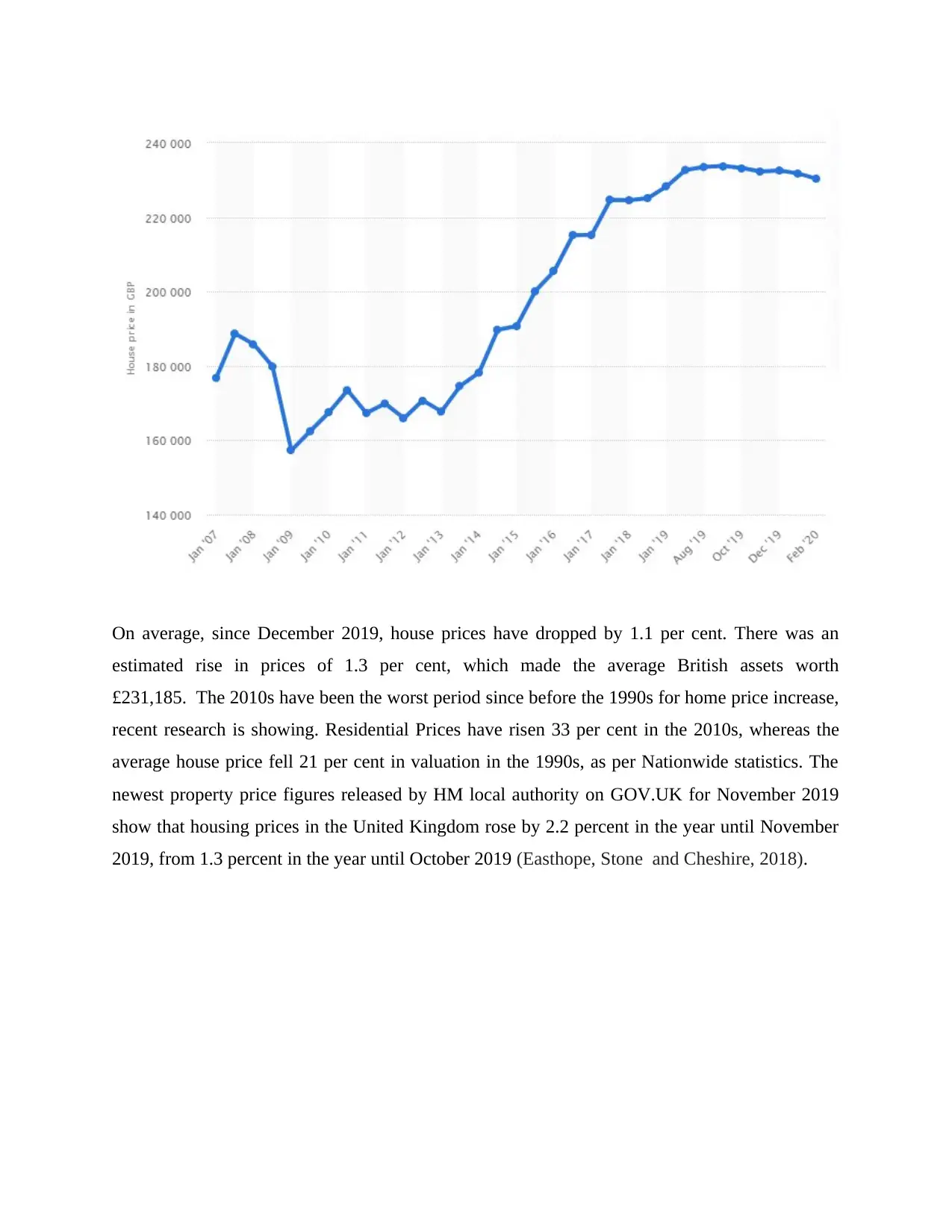

On average, since December 2019, house prices have dropped by 1.1 per cent. There was an

estimated rise in prices of 1.3 per cent, which made the average British assets worth

£231,185. The 2010s have been the worst period since before the 1990s for home price increase,

recent research is showing. Residential Prices have risen 33 per cent in the 2010s, whereas the

average house price fell 21 per cent in valuation in the 1990s, as per Nationwide statistics. The

newest property price figures released by HM local authority on GOV.UK for November 2019

show that housing prices in the United Kingdom rose by 2.2 percent in the year until November

2019, from 1.3 percent in the year until October 2019 (Easthope, Stone and Cheshire, 2018).

estimated rise in prices of 1.3 per cent, which made the average British assets worth

£231,185. The 2010s have been the worst period since before the 1990s for home price increase,

recent research is showing. Residential Prices have risen 33 per cent in the 2010s, whereas the

average house price fell 21 per cent in valuation in the 1990s, as per Nationwide statistics. The

newest property price figures released by HM local authority on GOV.UK for November 2019

show that housing prices in the United Kingdom rose by 2.2 percent in the year until November

2019, from 1.3 percent in the year until October 2019 (Easthope, Stone and Cheshire, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

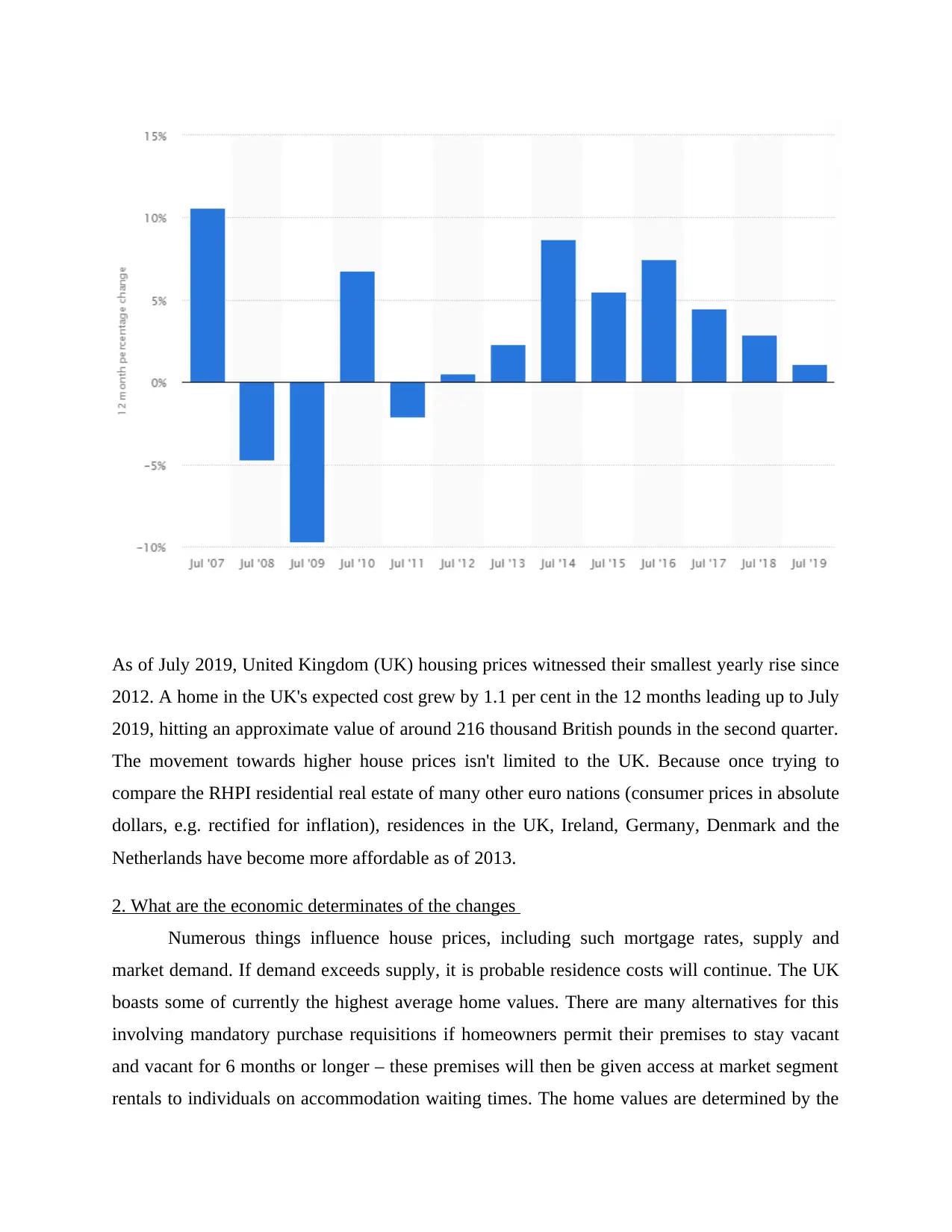

As of July 2019, United Kingdom (UK) housing prices witnessed their smallest yearly rise since

2012. A home in the UK's expected cost grew by 1.1 per cent in the 12 months leading up to July

2019, hitting an approximate value of around 216 thousand British pounds in the second quarter.

The movement towards higher house prices isn't limited to the UK. Because once trying to

compare the RHPI residential real estate of many other euro nations (consumer prices in absolute

dollars, e.g. rectified for inflation), residences in the UK, Ireland, Germany, Denmark and the

Netherlands have become more affordable as of 2013.

2. What are the economic determinates of the changes

Numerous things influence house prices, including such mortgage rates, supply and

market demand. If demand exceeds supply, it is probable residence costs will continue. The UK

boasts some of currently the highest average home values. There are many alternatives for this

involving mandatory purchase requisitions if homeowners permit their premises to stay vacant

and vacant for 6 months or longer – these premises will then be given access at market segment

rentals to individuals on accommodation waiting times. The home values are determined by the

2012. A home in the UK's expected cost grew by 1.1 per cent in the 12 months leading up to July

2019, hitting an approximate value of around 216 thousand British pounds in the second quarter.

The movement towards higher house prices isn't limited to the UK. Because once trying to

compare the RHPI residential real estate of many other euro nations (consumer prices in absolute

dollars, e.g. rectified for inflation), residences in the UK, Ireland, Germany, Denmark and the

Netherlands have become more affordable as of 2013.

2. What are the economic determinates of the changes

Numerous things influence house prices, including such mortgage rates, supply and

market demand. If demand exceeds supply, it is probable residence costs will continue. The UK

boasts some of currently the highest average home values. There are many alternatives for this

involving mandatory purchase requisitions if homeowners permit their premises to stay vacant

and vacant for 6 months or longer – these premises will then be given access at market segment

rentals to individuals on accommodation waiting times. The home values are determined by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

market. If demand rises (swing to the right) or if production starts to fall (move to the left), house

prices will rise in balance. Likewise, the steady state rate will drop if wages fall or if production

increases. So, in the 2000s, the home values grow so high, but fall in 2008. The reasons for this

lie mainly in changing house prices (Murie, 2018).

The long-term rise in property prices is exacerbated by property prices that outstrip

production. It has been approximated * that 175,000 more houses and apartments per year must

be formulated to meet the long term threshold of property prices. As noted earlier, new

developments are involved in just about 5 percent of property purchases. There are many

numerous factors which are described in the following which have impacted housing demand:

Income: It was time for increasingly increasing sales at the 2007 pleading. The economy was

beginning to experience a "boom" in economic theory. Most of the citizens started to invest their

excess income on rent; even first build a property or move to a better one. Numerous folks

assumed their earnings will also keep growing and were therefore ready to spread monetarily in

the near term by having an expensive residence, assured their monthly repayments would

become more cost effective surrounded by white time. By comparison, there were cycles of

downturn in 2008/09, with increasing unemployment and then either declining, or wages

increasing far more gradually. Individuals were far less fortunate to have the opportunity to pay

massive volumes.

Interest rate deduction: No approximation of the effects of changes in home values caused by

falling lending rates among 1991 and 2016. The estimated relationships in the reports NHPAU's

'Affordability Issues'1 (2007) and 'Affordability Still Issues'2 (2008) based on raw data covering

the timpe period up to 2007. The interest rate rates have since increased dramatically, and

significant developments in the mortgage business have also taken place, including the

regulation of mortgages and the relation between mortgages and interest rates9. These alterations

are of a magnitude which implies that a model estimated for the preceding cycle would not be

used accurately for the months since 2007.

Unemployment: Unemployment is correlated with economic. Despite through unemployment,

less people can afford a home. Nevertheless, then again the threat of insecurity can deter users

from joining the housing market.

prices will rise in balance. Likewise, the steady state rate will drop if wages fall or if production

increases. So, in the 2000s, the home values grow so high, but fall in 2008. The reasons for this

lie mainly in changing house prices (Murie, 2018).

The long-term rise in property prices is exacerbated by property prices that outstrip

production. It has been approximated * that 175,000 more houses and apartments per year must

be formulated to meet the long term threshold of property prices. As noted earlier, new

developments are involved in just about 5 percent of property purchases. There are many

numerous factors which are described in the following which have impacted housing demand:

Income: It was time for increasingly increasing sales at the 2007 pleading. The economy was

beginning to experience a "boom" in economic theory. Most of the citizens started to invest their

excess income on rent; even first build a property or move to a better one. Numerous folks

assumed their earnings will also keep growing and were therefore ready to spread monetarily in

the near term by having an expensive residence, assured their monthly repayments would

become more cost effective surrounded by white time. By comparison, there were cycles of

downturn in 2008/09, with increasing unemployment and then either declining, or wages

increasing far more gradually. Individuals were far less fortunate to have the opportunity to pay

massive volumes.

Interest rate deduction: No approximation of the effects of changes in home values caused by

falling lending rates among 1991 and 2016. The estimated relationships in the reports NHPAU's

'Affordability Issues'1 (2007) and 'Affordability Still Issues'2 (2008) based on raw data covering

the timpe period up to 2007. The interest rate rates have since increased dramatically, and

significant developments in the mortgage business have also taken place, including the

regulation of mortgages and the relation between mortgages and interest rates9. These alterations

are of a magnitude which implies that a model estimated for the preceding cycle would not be

used accurately for the months since 2007.

Unemployment: Unemployment is correlated with economic. Despite through unemployment,

less people can afford a home. Nevertheless, then again the threat of insecurity can deter users

from joining the housing market.

Economic growth: Housing demand is contingent on income. Greater economic development

and rising wages will allow companies to consume more on homes; this will increase inflation

and drive up the price. In actuality, house price inflation is often noted as a stretchy earnings

(premium good); economic growth leads to a larger percentage of household income getting

invested. Likewise, declining wages in a downturn would mean those people can't even afford,

while those who keep their insurance can fall back on the living expenses and eventually wind up

being burglarized of their house.

Consumer confidence: Trust is significant in deciding as to if individuals would like to take

chances out a personal loan. Especially perceptions more toward the real estate market are

essential; customers will postpone purchasing if they think the house prices would fall (Ruiz and

Vargas-Silva, 2018).

Supply: Delivery shortages drive up the costs. Excess production would push down costs. For

instance, an approximate 700,000 new houses are built in the Irish real estate boom from 1996-

2006. When the real estate market crashed, an important overproduction remained to the market.

Property prices were 15 per cent, and costs dropped with production higher that request

Mortgage availability: In the 1996-2006 boom periods, numerous financial institutions had a

keen interest in lending mortgage loans. They enabled people to spend large larger amounts of

incomes (e.g. 5 percent revenue). Financial institutions also mandated much reduced reserves

(for example, 100 percent housing loans). This simplicity of applying for a mortgage implied that

price of housing expanded because more citizens could purchase now. After the 2007 financial

crisis, though, banks and other financial institutions have strained to collect funds to borrow on

the capital markets. They have however stiffened their capital requirements which require a

higher payment to build a property. This has decreased student loan accessibility and a decrease

in price.

Interest rate: The amount of mortgage repayments is influenced by interest rates. A

combination of sustained interest rates will significantly raise monthly mortgage costs and lead

to lower availability for a room purchase. Higher interest rate the rent comparatively more

appealing than the purchase. If borrowers have continuous aggregate loans, interest rates get a

larger influence. For instance, the strong increase in interest rates in 1990-92 triggered a very

and rising wages will allow companies to consume more on homes; this will increase inflation

and drive up the price. In actuality, house price inflation is often noted as a stretchy earnings

(premium good); economic growth leads to a larger percentage of household income getting

invested. Likewise, declining wages in a downturn would mean those people can't even afford,

while those who keep their insurance can fall back on the living expenses and eventually wind up

being burglarized of their house.

Consumer confidence: Trust is significant in deciding as to if individuals would like to take

chances out a personal loan. Especially perceptions more toward the real estate market are

essential; customers will postpone purchasing if they think the house prices would fall (Ruiz and

Vargas-Silva, 2018).

Supply: Delivery shortages drive up the costs. Excess production would push down costs. For

instance, an approximate 700,000 new houses are built in the Irish real estate boom from 1996-

2006. When the real estate market crashed, an important overproduction remained to the market.

Property prices were 15 per cent, and costs dropped with production higher that request

Mortgage availability: In the 1996-2006 boom periods, numerous financial institutions had a

keen interest in lending mortgage loans. They enabled people to spend large larger amounts of

incomes (e.g. 5 percent revenue). Financial institutions also mandated much reduced reserves

(for example, 100 percent housing loans). This simplicity of applying for a mortgage implied that

price of housing expanded because more citizens could purchase now. After the 2007 financial

crisis, though, banks and other financial institutions have strained to collect funds to borrow on

the capital markets. They have however stiffened their capital requirements which require a

higher payment to build a property. This has decreased student loan accessibility and a decrease

in price.

Interest rate: The amount of mortgage repayments is influenced by interest rates. A

combination of sustained interest rates will significantly raise monthly mortgage costs and lead

to lower availability for a room purchase. Higher interest rate the rent comparatively more

appealing than the purchase. If borrowers have continuous aggregate loans, interest rates get a

larger influence. For instance, the strong increase in interest rates in 1990-92 triggered a very

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sharp decline in UK property prices, as many homebuyers were unable to purchase interest rate

rises (He, Lu and Berrens, 2018).

3. How has government action over the period 2009-2019 affected the UK housing market?

The most effective way the national government can ease the pressures of

accommodation costs on low-income families is by providing them incentives. Regulation that

raises wages such as accumulated additional tax, decent wages or a planned guaranteed

maximum wage often support disadvantaged households pay a mortgage. British housing costs

have first from at least 2002 to their yearly fall in 2009. Property values in London, as per the

British newspapers, reportedly saw the worst costs lower 5.3 per cent. The London property

values are or maybe one of UK's most common discussion topics. This is largely due to the fact

that house prices have almost doubled since before the mid-1990s. The Government is concerned

that insufficient residences have been constructed to satisfy the requirements of an increasing

and aging society. Its focus is to maximize production both of latest and reconfigured vacant

apartments. A total of 118,190 new construct residences were constructed in England in 2012, a

9 percent rise over the last year but a 31 percent decline over the high of 170,610 in 2008.

During the last 5 years, only 610,000 housing units have been built, compared to nearly 800,000

in the previous five, a decrease of 23%. This restriction on the availability of new

accommodation has ensured that house prices have remained fairly steady throughout the last 3

years, despite the complexity in getting funds from investors. Actually 15 % of the population is

in the rental market and this number is projected to almost double during the next 10 years. The

UK's affordable housing permeability is low – one of Europe's lowest – government's legislation

is concentrated on enhancing supply elastic properties so housing construction are more sensitive

to market changing requirements. There are defined various actions that are taken by the UK

government in context of Housing market from 2009 to 2019:

Build more social housing: Enabling broader independence for will local government

(community) to raise earnings to fund the development and procurement of housing benefit

could help counteract the decline for the past 10 - 20 years in the development of committee

facilities. An option is also to enhance funding for the 1,400 housing committee that are

obligating for developing and managing nearly 3 million homes in the UK.

rises (He, Lu and Berrens, 2018).

3. How has government action over the period 2009-2019 affected the UK housing market?

The most effective way the national government can ease the pressures of

accommodation costs on low-income families is by providing them incentives. Regulation that

raises wages such as accumulated additional tax, decent wages or a planned guaranteed

maximum wage often support disadvantaged households pay a mortgage. British housing costs

have first from at least 2002 to their yearly fall in 2009. Property values in London, as per the

British newspapers, reportedly saw the worst costs lower 5.3 per cent. The London property

values are or maybe one of UK's most common discussion topics. This is largely due to the fact

that house prices have almost doubled since before the mid-1990s. The Government is concerned

that insufficient residences have been constructed to satisfy the requirements of an increasing

and aging society. Its focus is to maximize production both of latest and reconfigured vacant

apartments. A total of 118,190 new construct residences were constructed in England in 2012, a

9 percent rise over the last year but a 31 percent decline over the high of 170,610 in 2008.

During the last 5 years, only 610,000 housing units have been built, compared to nearly 800,000

in the previous five, a decrease of 23%. This restriction on the availability of new

accommodation has ensured that house prices have remained fairly steady throughout the last 3

years, despite the complexity in getting funds from investors. Actually 15 % of the population is

in the rental market and this number is projected to almost double during the next 10 years. The

UK's affordable housing permeability is low – one of Europe's lowest – government's legislation

is concentrated on enhancing supply elastic properties so housing construction are more sensitive

to market changing requirements. There are defined various actions that are taken by the UK

government in context of Housing market from 2009 to 2019:

Build more social housing: Enabling broader independence for will local government

(community) to raise earnings to fund the development and procurement of housing benefit

could help counteract the decline for the past 10 - 20 years in the development of committee

facilities. An option is also to enhance funding for the 1,400 housing committee that are

obligating for developing and managing nearly 3 million homes in the UK.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reducing the number of empty house: There are many alternatives for this involving mandatory

purchase requisitions if homeowners permit their premises to stay vacant for 6 months or longer.

These premises will then be given access at market segment rentals to individuals on

accommodation waiting times (Wu, 2018).

Stamp duty: Currently , the government expanded stamp duty to 3 per cent for features more

than £250,000 residences from £ 60,000-£ 250,000 pay 1 per cent characteristics features £

60,000 pay 0 per cent The increasing trend in inheritance tax was focused on reducing

requirement for characteristics over £250,000, particularly in real estate locations like London.

4. Predict what would be the impact of COVID – 19 on UK housing market

The corona virus has delayed the Existing labor real estate market. When the government

restricted house advertising and prohibited mortgage brokers from selling new assets as part of

the wider efforts to curb the impact of the disease outbreak. To reaction to the disease outbreak,

the Bank of England reduced interest rates to early March from 0.75 to 0.25 per cent. It then

reported a second drastic cut later that night, bringing borrowing costs to the lowest ever rate of

0.1 percent. While British people also can keep moving in the center of purchasing a home, real

estate browsing was delayed and the departments of mortgage brokers permanently closed as

portion of broader-ranging initiatives to minimize COVID-19 diseases. Property values and

interaction had gathered that since beginning of 2020, managed to help by decreased Brexit and

political instability, but this pattern has taken dramatically backwards.

Due to face of COVID-19 disease in UK housing market people demand for the house

and sales of house fall down about 80%. UK home prices had started to rebound from Brexit-

induced volatility by the end of 2019. And the so-called Boris bounce from the Tories' December

election victory set the stage for a good start to 2020. But then corona virus happened to come

along, going to send the UK into quarantine, meaning purchasers couldn't visit homes, a

relatively vital component because once moving soon. The spectacular economic fallout has also

made some individual more cautious about making massive acquisitions correct presently.

Although the effect of the corona virus infection on UK house prices is still not well known,

experts predict that in the second and third rounds of 2020, they will fall. During the corona virus

lockout, UK house prices fell as analysts informed the property market was hardly working

because of the constraints. Rightmove's new data shows that the average selling price of property

purchase requisitions if homeowners permit their premises to stay vacant for 6 months or longer.

These premises will then be given access at market segment rentals to individuals on

accommodation waiting times (Wu, 2018).

Stamp duty: Currently , the government expanded stamp duty to 3 per cent for features more

than £250,000 residences from £ 60,000-£ 250,000 pay 1 per cent characteristics features £

60,000 pay 0 per cent The increasing trend in inheritance tax was focused on reducing

requirement for characteristics over £250,000, particularly in real estate locations like London.

4. Predict what would be the impact of COVID – 19 on UK housing market

The corona virus has delayed the Existing labor real estate market. When the government

restricted house advertising and prohibited mortgage brokers from selling new assets as part of

the wider efforts to curb the impact of the disease outbreak. To reaction to the disease outbreak,

the Bank of England reduced interest rates to early March from 0.75 to 0.25 per cent. It then

reported a second drastic cut later that night, bringing borrowing costs to the lowest ever rate of

0.1 percent. While British people also can keep moving in the center of purchasing a home, real

estate browsing was delayed and the departments of mortgage brokers permanently closed as

portion of broader-ranging initiatives to minimize COVID-19 diseases. Property values and

interaction had gathered that since beginning of 2020, managed to help by decreased Brexit and

political instability, but this pattern has taken dramatically backwards.

Due to face of COVID-19 disease in UK housing market people demand for the house

and sales of house fall down about 80%. UK home prices had started to rebound from Brexit-

induced volatility by the end of 2019. And the so-called Boris bounce from the Tories' December

election victory set the stage for a good start to 2020. But then corona virus happened to come

along, going to send the UK into quarantine, meaning purchasers couldn't visit homes, a

relatively vital component because once moving soon. The spectacular economic fallout has also

made some individual more cautious about making massive acquisitions correct presently.

Although the effect of the corona virus infection on UK house prices is still not well known,

experts predict that in the second and third rounds of 2020, they will fall. During the corona virus

lockout, UK house prices fell as analysts informed the property market was hardly working

because of the constraints. Rightmove's new data shows that the average selling price of property

fell 0.2 percent to £311,950. UK prices have risen 2.1 per cent in April last year. Analysis has

shown that current vendors have stayed predominantly on the sector, with overall stock available

for selling down 2.6 per cent because the 23 March lockout was implemented. Miles Shipside,

director of Rightmove and a consultant on the housing market, said: "operatives disclose better

connection, with both producers and consumers eager to hang agreements around each other

(Wind and Dewilde, 2018).

Citizens do not have a working economy when consumers are unable to purchase and

vendors are unable to sale, and so the emphasis must be on what is necessary to properly the

economy stabilize until the lockout can be securely relieved. Although some homeowners may

be worried about the risk of brief-term drops in home values, others take the long-term view and

live up to their promises to go forward. This is managed to help by lending institutions going to

extend the lifespan of current loan offers by 3 months, and by proposed laws on adaptable

project cost. So overall analysis it is getting that corona virsus show negative impact on the UK

housing market (Murie, 2018).

RECOMMENDATIONS

As per the above report it has been recommended that the housing market the locking

down of the corona virus has pushed the UK housing market into somewhat of a delayed

suspension. Following March 27, whenever the government has declared it was going to

postpone rental property till after the recession, most market participants are being left high and

dry. Mortgage borrowers have removed goods from of the marketplace and social distance

initiatives have made the advertising, valuation and presentation of semi-vacant homes unlikely.

To grow in this market require contacting of more customer and providing belief to all the

houses are virus free and sanitize properly.

Vendors will lose their property now and they can be regarded by buyers — and much

has improved. With one item, the logistics of trying to navigate the industry is now much more

complex and difficult. Purchasers were instructed to take virtual tours before scheduling a

sighting. After they've seen a property in individual, they are asked by operatives to register a

wellbeing statement, or they may have their average temp inspected at the doorway.

shown that current vendors have stayed predominantly on the sector, with overall stock available

for selling down 2.6 per cent because the 23 March lockout was implemented. Miles Shipside,

director of Rightmove and a consultant on the housing market, said: "operatives disclose better

connection, with both producers and consumers eager to hang agreements around each other

(Wind and Dewilde, 2018).

Citizens do not have a working economy when consumers are unable to purchase and

vendors are unable to sale, and so the emphasis must be on what is necessary to properly the

economy stabilize until the lockout can be securely relieved. Although some homeowners may

be worried about the risk of brief-term drops in home values, others take the long-term view and

live up to their promises to go forward. This is managed to help by lending institutions going to

extend the lifespan of current loan offers by 3 months, and by proposed laws on adaptable

project cost. So overall analysis it is getting that corona virsus show negative impact on the UK

housing market (Murie, 2018).

RECOMMENDATIONS

As per the above report it has been recommended that the housing market the locking

down of the corona virus has pushed the UK housing market into somewhat of a delayed

suspension. Following March 27, whenever the government has declared it was going to

postpone rental property till after the recession, most market participants are being left high and

dry. Mortgage borrowers have removed goods from of the marketplace and social distance

initiatives have made the advertising, valuation and presentation of semi-vacant homes unlikely.

To grow in this market require contacting of more customer and providing belief to all the

houses are virus free and sanitize properly.

Vendors will lose their property now and they can be regarded by buyers — and much

has improved. With one item, the logistics of trying to navigate the industry is now much more

complex and difficult. Purchasers were instructed to take virtual tours before scheduling a

sighting. After they've seen a property in individual, they are asked by operatives to register a

wellbeing statement, or they may have their average temp inspected at the doorway.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.