UK Housing Market Analysis: 2009-2019 Trends and Coronavirus Impact

VerifiedAdded on 2023/01/10

|12

|3895

|92

Report

AI Summary

This report provides a comprehensive analysis of the UK housing market, examining the trends in average house prices from 2009 to 2019. It delves into the economic determinants that influence these price fluctuations, including economic growth, unemployment rates, interest rates, consumer confidence, mortgage availability, and population changes. The report also explores the impact of government actions on the housing market during this period. Furthermore, it includes a prediction of the potential impact of the Coronavirus pandemic on the UK housing market. The analysis covers both demand and supply-side factors, offering insights into the complex dynamics of the UK property sector. The study uses statistical data and graphs to demonstrate the trends and factors influencing the market.

Business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

1. Presenting the change in average price of house in UK over a period from the year 2009-

2019.............................................................................................................................................3

2. Stating the economic determinants of change represented in price of house .........................4

3. The manner in which action of government impacted housing market in UK from the

period of 2009-2019....................................................................................................................8

4. Predicting an impact of Coronavirus on the UK housing market ..........................................8

CONCLUSION ...............................................................................................................................9

REFERENCES .............................................................................................................................10

INTRODUCTION ..........................................................................................................................3

1. Presenting the change in average price of house in UK over a period from the year 2009-

2019.............................................................................................................................................3

2. Stating the economic determinants of change represented in price of house .........................4

3. The manner in which action of government impacted housing market in UK from the

period of 2009-2019....................................................................................................................8

4. Predicting an impact of Coronavirus on the UK housing market ..........................................8

CONCLUSION ...............................................................................................................................9

REFERENCES .............................................................................................................................10

INTRODUCTION

Business is been outlined as an entity that is engaged in the professional, commercialised

& industrial activities. It refers to an organized effort & activities of an individual in producing

and selling the goods and the services for earning profit. In other words, it refers to an

organization or the economic system where the goods & services are been exchanged for gaining

profits and earning money. The present study is based on UK housing market and provides a

deeper insights towards the change on in the price of houses over a period of 10 years.

Furthermore, the factors or components that influence the prices are also been highlighted in the

study. Moreover, it also includes the action taken by government along with its effect and

predicting effect of novel coronavirus on housing market in the future.

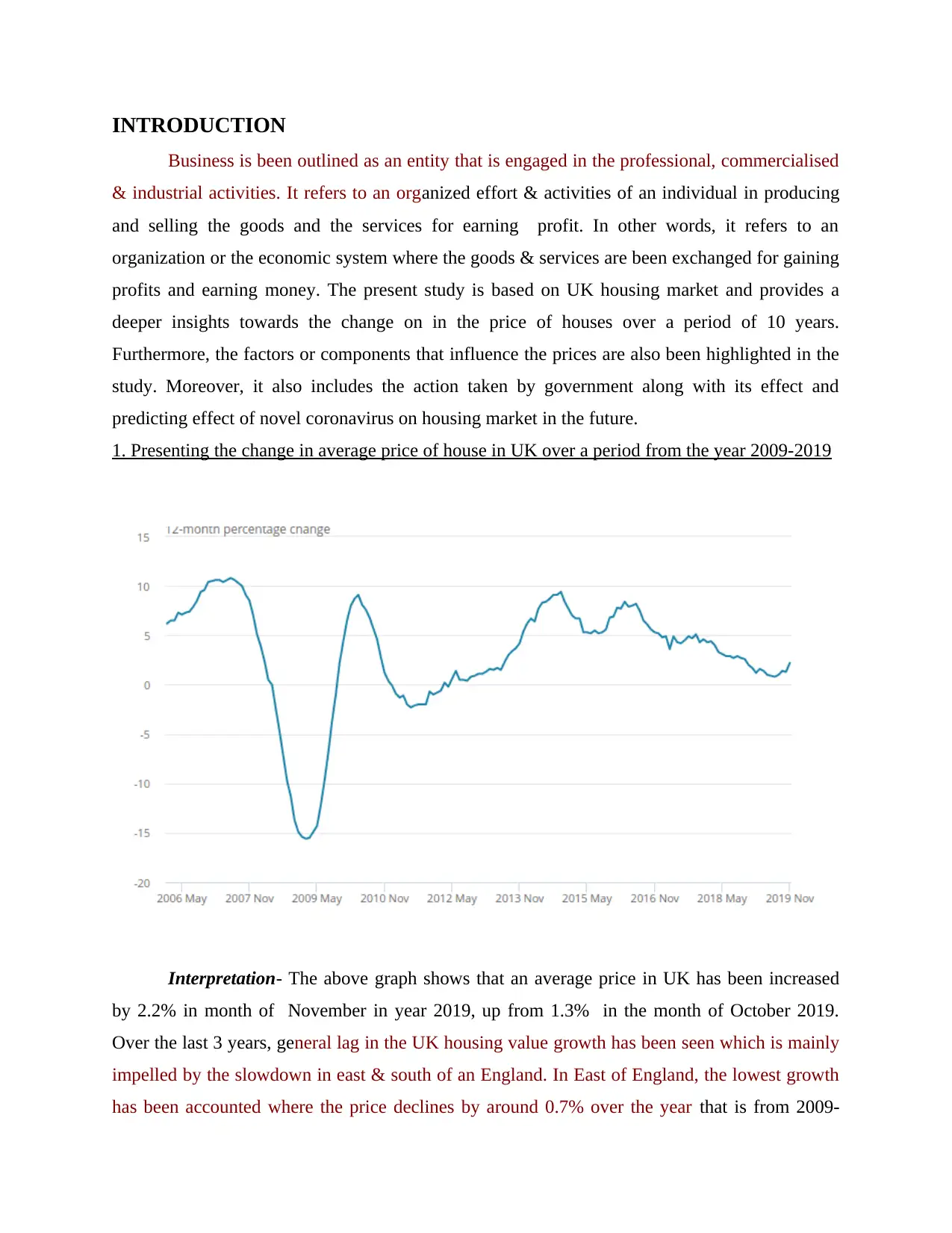

1. Presenting the change in average price of house in UK over a period from the year 2009-2019

Interpretation- The above graph shows that an average price in UK has been increased

by 2.2% in month of November in year 2019, up from 1.3% in the month of October 2019.

Over the last 3 years, general lag in the UK housing value growth has been seen which is mainly

impelled by the slowdown in east & south of an England. In East of England, the lowest growth

has been accounted where the price declines by around 0.7% over the year that is from 2009-

Business is been outlined as an entity that is engaged in the professional, commercialised

& industrial activities. It refers to an organized effort & activities of an individual in producing

and selling the goods and the services for earning profit. In other words, it refers to an

organization or the economic system where the goods & services are been exchanged for gaining

profits and earning money. The present study is based on UK housing market and provides a

deeper insights towards the change on in the price of houses over a period of 10 years.

Furthermore, the factors or components that influence the prices are also been highlighted in the

study. Moreover, it also includes the action taken by government along with its effect and

predicting effect of novel coronavirus on housing market in the future.

1. Presenting the change in average price of house in UK over a period from the year 2009-2019

Interpretation- The above graph shows that an average price in UK has been increased

by 2.2% in month of November in year 2019, up from 1.3% in the month of October 2019.

Over the last 3 years, general lag in the UK housing value growth has been seen which is mainly

impelled by the slowdown in east & south of an England. In East of England, the lowest growth

has been accounted where the price declines by around 0.7% over the year that is from 2009-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2019. This has been followed by the London, where the prices increased with a percentage value

of 0.2% over the years. Over the foregone years, the prices of UK house has been rising at fast

rate on the record for several years, as the sellers fell as more assured about prospect for housing

marketplace after a general selection as per the right-move (Chuang and et.al., 2018). An average

price of the properties in the market jumped by around 2.3%, a large rise for time period since

property site begin the cost of house index in the year 2002. Around 65000 of the UK geographic

area were been marketed over a period with average asked price of approx. pound 306810. In

accordance to right move, an option result provided panel of the stability for the movement after

instability period since Brexit vote that had caused some in putting off the move. Housing market

dislikes an uncertainty, unsettled the political look over last 3.5 years since EU referendum has

caused some movers in hesitating. There seems to be the release of such pent-up demand that

suggests presence in the store for spring market.

As of the July 2019, prices of residential property in UK reflects the lowest annual rise

since the year 2012. An average price of the house in UK increased through 1.1% within 12

months prior to the month of July 2019, by reaching estimated value of around 216 thousand

pounds within 2nd quarter of the year 2019. The trend of rising the prices of housing is seen in

entire UK as when the comparison of various European countries' residence property is made,

houses became as more and more expensive from the year 2013 onwards in UK. The prices are

not been expected to decline, it is predicted that the residential prices would be growing in

coming years because British government would begin to focus on the domestic issues after the

condition of Brexit.

Thus, average price of house in UK increased by 2.2% over years to November 2019, up

from the 1.3% in the month of October 2019. The average prices increased over year in England

to Pound 251000 that is 1.7%, Wales to Pound 173000 that is 7.8% ,Northern Ireland of pound

140000 and Scotland to pound 1550000 which is seen as 3.5%. An annual rise in the England

has been driven by North West & West Midlands. However, the lowest growth rate found East of

England resulting as negative 0.7% followed by the London as positive 0.2% in an overall UK.

2. Stating the economic determinants of change represented in price of house

The housing industry is mainly induced by economic state, real income, interest rates,

change in population size etc. With the period of increasing demand and the limited supply, it

of 0.2% over the years. Over the foregone years, the prices of UK house has been rising at fast

rate on the record for several years, as the sellers fell as more assured about prospect for housing

marketplace after a general selection as per the right-move (Chuang and et.al., 2018). An average

price of the properties in the market jumped by around 2.3%, a large rise for time period since

property site begin the cost of house index in the year 2002. Around 65000 of the UK geographic

area were been marketed over a period with average asked price of approx. pound 306810. In

accordance to right move, an option result provided panel of the stability for the movement after

instability period since Brexit vote that had caused some in putting off the move. Housing market

dislikes an uncertainty, unsettled the political look over last 3.5 years since EU referendum has

caused some movers in hesitating. There seems to be the release of such pent-up demand that

suggests presence in the store for spring market.

As of the July 2019, prices of residential property in UK reflects the lowest annual rise

since the year 2012. An average price of the house in UK increased through 1.1% within 12

months prior to the month of July 2019, by reaching estimated value of around 216 thousand

pounds within 2nd quarter of the year 2019. The trend of rising the prices of housing is seen in

entire UK as when the comparison of various European countries' residence property is made,

houses became as more and more expensive from the year 2013 onwards in UK. The prices are

not been expected to decline, it is predicted that the residential prices would be growing in

coming years because British government would begin to focus on the domestic issues after the

condition of Brexit.

Thus, average price of house in UK increased by 2.2% over years to November 2019, up

from the 1.3% in the month of October 2019. The average prices increased over year in England

to Pound 251000 that is 1.7%, Wales to Pound 173000 that is 7.8% ,Northern Ireland of pound

140000 and Scotland to pound 1550000 which is seen as 3.5%. An annual rise in the England

has been driven by North West & West Midlands. However, the lowest growth rate found East of

England resulting as negative 0.7% followed by the London as positive 0.2% in an overall UK.

2. Stating the economic determinants of change represented in price of house

The housing industry is mainly induced by economic state, real income, interest rates,

change in population size etc. With the period of increasing demand and the limited supply, it

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will result in rising housing prices, increased risk of the homelessness and rising rents. The

analysis would be made based on the market forces that is demand and supply that are as

follows-

Demand side assessment-

Economic growth- With higher growth in the economy and rise in income, individual

would be able to spent more on the houses, this would increase the prices and demand of the

houses. As per the concept, demand for lodging is often times seen as income elastic where

rising income leads to larger proportion of an income spend on the houses (Banyte and Maliene,

2017). However, in recession, decline in income would indicate that individual cannot spend to

purchase & those who left their job might fall down their ,mortgage payments & ends up with

home repossession. This means that rising income encourages individual's demand in buying the

house and vice versa.

Unemployment- In case of rising unemployment, fewer individual will be able to afford

the purchasing of house. Moreover, fear of state might deter the individual from entering into

market of property (Tsai, 2018). On other state, if unemployment rate decreases, means that

most of the individual will be having their job and earns, this induces the demand for purchasing

house and resulted a growth in housing market.

Interest rates- This determinant plays a crucial role in identifying the mortgage cost and

repayments of interest. Majority of the UK homeowner prefers for taking out the rate of variable

mortgage instead of the landmass where the fixed rate of mortgage deals are seen as more

common. High rate of interest period would result to increase in the cost of the mortgage

payments & would cause lower demand in buying the house (Apergis and Payne, 2020). On

other note, lower rate of interest helps the individual in getting the loan at lower price and

interest rate which clearly increases the demand for housing market and due to this majority of

the individual tends to buy the house.

Confidence of Consumer- The need for the houses mainly reckon the consumer

confidence. Particularly, it depends on the individual's assurance regarding upcoming economy

& the housing market. It the individual anticipate the prices to increase then demand would rise

so that individual could gain from the rising wealth. In the boom, need for the houses increases

with a high pace than income (Cochrane and Poot, 2019). On other note, if an individual fears

house prices can fall, it will directly lead to defer the buying of house.

analysis would be made based on the market forces that is demand and supply that are as

follows-

Demand side assessment-

Economic growth- With higher growth in the economy and rise in income, individual

would be able to spent more on the houses, this would increase the prices and demand of the

houses. As per the concept, demand for lodging is often times seen as income elastic where

rising income leads to larger proportion of an income spend on the houses (Banyte and Maliene,

2017). However, in recession, decline in income would indicate that individual cannot spend to

purchase & those who left their job might fall down their ,mortgage payments & ends up with

home repossession. This means that rising income encourages individual's demand in buying the

house and vice versa.

Unemployment- In case of rising unemployment, fewer individual will be able to afford

the purchasing of house. Moreover, fear of state might deter the individual from entering into

market of property (Tsai, 2018). On other state, if unemployment rate decreases, means that

most of the individual will be having their job and earns, this induces the demand for purchasing

house and resulted a growth in housing market.

Interest rates- This determinant plays a crucial role in identifying the mortgage cost and

repayments of interest. Majority of the UK homeowner prefers for taking out the rate of variable

mortgage instead of the landmass where the fixed rate of mortgage deals are seen as more

common. High rate of interest period would result to increase in the cost of the mortgage

payments & would cause lower demand in buying the house (Apergis and Payne, 2020). On

other note, lower rate of interest helps the individual in getting the loan at lower price and

interest rate which clearly increases the demand for housing market and due to this majority of

the individual tends to buy the house.

Confidence of Consumer- The need for the houses mainly reckon the consumer

confidence. Particularly, it depends on the individual's assurance regarding upcoming economy

& the housing market. It the individual anticipate the prices to increase then demand would rise

so that individual could gain from the rising wealth. In the boom, need for the houses increases

with a high pace than income (Cochrane and Poot, 2019). On other note, if an individual fears

house prices can fall, it will directly lead to defer the buying of house.

Mortgage availability- It is the most of the essence factor which determines an effective

requirement for the houses that depicts the disposition of the banks in lending mortgages. In case

the bank gives mortgage with higher multiples of income then effective demand for the house

seems as greater. Willingness of banks in lending mortgages finance could vary based on

strength of interbank loaning segment (Hwang, Cho and Shin, 2019). Credit crisis in 2008,

showed sharp rise in cost of the interbank lending and the fall in mortgage accessibility. Many of

the mortgage products has been withdrawn, by making it as more difficult for the homeowners

for getting on ladder of property.

For example- Mortgages like 125% & 100% mortgages had been withdrawn due to

which banks increasingly demand higher deposit before the lending mortgages.

Affordability- Increase income means that the individual are been able to expend for

spending more on the housing. During the time period of an economic growth, need for the

houses attend to increase (Ball, 2017). Also, the demand for the lodging tends to be as luxury

good, therefore, rise in the income cause greater percentage of the rise in demand. Contrary to it,

with increase in price of the house, individual cannot afford to buy the house and it leads to

decline in demand.

Population- With rising population, the desire for purchasing the house increases as more

individual would be requiring place to live in. As the population in England is been predicted to

grow and is resulted as growing in past periods, housing demand rises. For instance- growing no.

of single person who live alone led to increase in need for houses. Moreover, housing demand

does not only depend on people but likewise an average size of the household. Certain

demographic and the social factors causing rise in no. of householders at a faster rate as

compared to increase in population (Payne, 2020). Such demographic modification involve issue

like age of the individual leaving a home because of rising life expectancy outcome to more of

single old age individual, divorce rates leads to increased number of the single- parent families.

Renting cost- This reflects a 22% cost increase of the renting despite the financial crisis

& the housing crash. This helped in causing UK housing price towards rising after the year 2011.

If renting cost rises, then individual will make higher efforts in trying & buying the house

through the mortgage turn as relatively cheaper (Savva, 2018). House market of UK has been

buoyed through costly price of renting that encourages buy for letting the lenders and motivating

the households in stretching their budget as much as possible in getting on housing ladder.

requirement for the houses that depicts the disposition of the banks in lending mortgages. In case

the bank gives mortgage with higher multiples of income then effective demand for the house

seems as greater. Willingness of banks in lending mortgages finance could vary based on

strength of interbank loaning segment (Hwang, Cho and Shin, 2019). Credit crisis in 2008,

showed sharp rise in cost of the interbank lending and the fall in mortgage accessibility. Many of

the mortgage products has been withdrawn, by making it as more difficult for the homeowners

for getting on ladder of property.

For example- Mortgages like 125% & 100% mortgages had been withdrawn due to

which banks increasingly demand higher deposit before the lending mortgages.

Affordability- Increase income means that the individual are been able to expend for

spending more on the housing. During the time period of an economic growth, need for the

houses attend to increase (Ball, 2017). Also, the demand for the lodging tends to be as luxury

good, therefore, rise in the income cause greater percentage of the rise in demand. Contrary to it,

with increase in price of the house, individual cannot afford to buy the house and it leads to

decline in demand.

Population- With rising population, the desire for purchasing the house increases as more

individual would be requiring place to live in. As the population in England is been predicted to

grow and is resulted as growing in past periods, housing demand rises. For instance- growing no.

of single person who live alone led to increase in need for houses. Moreover, housing demand

does not only depend on people but likewise an average size of the household. Certain

demographic and the social factors causing rise in no. of householders at a faster rate as

compared to increase in population (Payne, 2020). Such demographic modification involve issue

like age of the individual leaving a home because of rising life expectancy outcome to more of

single old age individual, divorce rates leads to increased number of the single- parent families.

Renting cost- This reflects a 22% cost increase of the renting despite the financial crisis

& the housing crash. This helped in causing UK housing price towards rising after the year 2011.

If renting cost rises, then individual will make higher efforts in trying & buying the house

through the mortgage turn as relatively cheaper (Savva, 2018). House market of UK has been

buoyed through costly price of renting that encourages buy for letting the lenders and motivating

the households in stretching their budget as much as possible in getting on housing ladder.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Supply side analysis-

A shirt of the supply pushes or increases the prices as surplus of supply cause the price to

decline. For instance- Boom in property of Irish of the year 1996-2006, an anticipated 700000

building new houses. When the property market has been break, market was left-handed with the

fundamental overmuch supply. Rates of vacancy reached to 15% & with the supply higher than

the need and the prices fell (Sulaiman, Mohammed and Ghani, 2018). Supply of the housing is

dependent on the existing stock and building new house. It seems as quite inelastic because for

getting permission of planning and in building houses depicted as the time-consuming process.

The period in which prices of houses rises, it might not cause equivalent rise in the supply,

specially in the countries like UK with a limited land for the house building.

Technology- With advancement in technology, building of the houses tends to rise as

individual can build their home within less or limited time frame. On other side, with existing

technologies, building of new house is seen as the time-consuming and complex task.

Price of the substitute goods- In case the price of rental houses gets lower and the house

built by the builders are selling the house at lower price then the building the home on own will

reduce as the individual would not have bear higher cement price and construction cost.

No. of suppliers- If the suppliers in establishing houses or flats is increasing then

individual tend to build more number of house as low cost would be accounted (Al-Masum and

Lee, 2019). However, in case number of the suppliers are less than an individual would not

prefer to built house.

Price of factors of the production- With rise in the price of factors of the production,

cost of constructing houses increases while decline in price of the production factors, the cost

declines and an individual tend to construct his own house.

Future price expectations- If it is expected that in future the prices of constructing the

houses will be rising then currently more individual will seek to build house. On other side, if in

future the price are expected to decline or fall then at present the individual would not build their

houses.

A shirt of the supply pushes or increases the prices as surplus of supply cause the price to

decline. For instance- Boom in property of Irish of the year 1996-2006, an anticipated 700000

building new houses. When the property market has been break, market was left-handed with the

fundamental overmuch supply. Rates of vacancy reached to 15% & with the supply higher than

the need and the prices fell (Sulaiman, Mohammed and Ghani, 2018). Supply of the housing is

dependent on the existing stock and building new house. It seems as quite inelastic because for

getting permission of planning and in building houses depicted as the time-consuming process.

The period in which prices of houses rises, it might not cause equivalent rise in the supply,

specially in the countries like UK with a limited land for the house building.

Technology- With advancement in technology, building of the houses tends to rise as

individual can build their home within less or limited time frame. On other side, with existing

technologies, building of new house is seen as the time-consuming and complex task.

Price of the substitute goods- In case the price of rental houses gets lower and the house

built by the builders are selling the house at lower price then the building the home on own will

reduce as the individual would not have bear higher cement price and construction cost.

No. of suppliers- If the suppliers in establishing houses or flats is increasing then

individual tend to build more number of house as low cost would be accounted (Al-Masum and

Lee, 2019). However, in case number of the suppliers are less than an individual would not

prefer to built house.

Price of factors of the production- With rise in the price of factors of the production,

cost of constructing houses increases while decline in price of the production factors, the cost

declines and an individual tend to construct his own house.

Future price expectations- If it is expected that in future the prices of constructing the

houses will be rising then currently more individual will seek to build house. On other side, if in

future the price are expected to decline or fall then at present the individual would not build their

houses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. The manner in which action of government impacted housing market in UK from the period of

2009-2019

The main problem faced by UK in respect to its housing market is that shortfall of affordable

houses, high deposit requirements along with increase in the demand of housing among the

young people have increased the demand for private renting. The UK government has

implemented various measures which includes new permitted development rights with respect to

conversion from commercial to residential use under the specific defined market conditions. But

the impact of these measures and the extent to which it will speed up on account of the response

to the housing supply along with the change in demand is yet to be seen (Brener, 2020). In the

year 2015, the government has taken initiative which aims at securing 1 million net addition in

the housing stock. Also, DCLG and the homes and Communities Agency (HCA) set out a plan in

order to achieve the target of accelerating the housing supply and to timely deliver the 300000

net additional houses in a year on an average. But there are certain points of concerns which are

not having enough support from the government in case of affordable rented housing specifically

at social rents. If the 300000 houses are built then it will have a positive impact over the UK

housing as it will result into increase in the occupancy because of lifting from the borrowing

caps.

In 2009, the impact of 2008 recession still had a influence over it. But the government

has forecasted the increase in the immigration which will result into upward trend and based on

this the government had estimated that the population will increase in the next 2 decades which

results into effectively managing the situation. The impact of this plan has positively affected the

UK housing market and its influence was for long term as it was expected that UK household

numbers to increase substantially in the same period as well. The core housing policies were

focussed on the supply side (Salt, 2018). The government has attempted to increase the supply

along with changing the planning system. It includes policies such as first time buyers and the

key workers to get property ladder. These policies were implemented to serve the key goals of

the policy of the Labour Government between the year 1997 to 2010. The government also

imposed policy called “Sustainable Communities: Building for the future”. The aim of the policy

will lead to tackling the geographical differences in the housing market. It also aims at speeding

up the new housing supply (McKee, Muir and Moore, 2017). The Housing Green Paper which

was the strategic policy, which involves the tangible housing supply in order to meet the rising

2009-2019

The main problem faced by UK in respect to its housing market is that shortfall of affordable

houses, high deposit requirements along with increase in the demand of housing among the

young people have increased the demand for private renting. The UK government has

implemented various measures which includes new permitted development rights with respect to

conversion from commercial to residential use under the specific defined market conditions. But

the impact of these measures and the extent to which it will speed up on account of the response

to the housing supply along with the change in demand is yet to be seen (Brener, 2020). In the

year 2015, the government has taken initiative which aims at securing 1 million net addition in

the housing stock. Also, DCLG and the homes and Communities Agency (HCA) set out a plan in

order to achieve the target of accelerating the housing supply and to timely deliver the 300000

net additional houses in a year on an average. But there are certain points of concerns which are

not having enough support from the government in case of affordable rented housing specifically

at social rents. If the 300000 houses are built then it will have a positive impact over the UK

housing as it will result into increase in the occupancy because of lifting from the borrowing

caps.

In 2009, the impact of 2008 recession still had a influence over it. But the government

has forecasted the increase in the immigration which will result into upward trend and based on

this the government had estimated that the population will increase in the next 2 decades which

results into effectively managing the situation. The impact of this plan has positively affected the

UK housing market and its influence was for long term as it was expected that UK household

numbers to increase substantially in the same period as well. The core housing policies were

focussed on the supply side (Salt, 2018). The government has attempted to increase the supply

along with changing the planning system. It includes policies such as first time buyers and the

key workers to get property ladder. These policies were implemented to serve the key goals of

the policy of the Labour Government between the year 1997 to 2010. The government also

imposed policy called “Sustainable Communities: Building for the future”. The aim of the policy

will lead to tackling the geographical differences in the housing market. It also aims at speeding

up the new housing supply (McKee, Muir and Moore, 2017). The Housing Green Paper which

was the strategic policy, which involves the tangible housing supply in order to meet the rising

demand of housing along with addressing the issue of affordability issues. All these policies

which are being implemented by the UK government has lead to increase in the supply of

housing and meeting with the demand along with the reasonable and affordable prices. This has

brought little stability in the UK housing market.

4. Predicting an impact of Coronavirus on the UK housing market

Housing prices in UK would be falling in coming periods but are seen as unlikely to drop as

dramatically in the year 2008. COVID-19 halted a residential market in UK after country's

government stopped the house viewings and protected the real estate agent from promoting the

new properties as the part of the broader moves for containing the spread of pandemic. Though,

future prices of house would depend on the time period for which this pandemic lasts but the

analysts are very much confident that lower rate of interest and the shortage of supply would

limit their decrease or fall. The novel coronavirus seems to have the long run implication for all

aspects of residential property (Than-Thi, Dong and Chen, 2019). As the restrictions are been

gradually lifted, sector started to operate again under the social distancing measures. A

significant recession might be seen in UK housing market as the consumer confidence would be

slow to the return. Although an official guideline allowed the construction sites for remaining as

open during the period of lock-down, but most of the large housebuilder had shut down because

of the difficulty in maintaining the social distancing. Halt in the construction is seen as inevitably

causing fall in delivery of the housing and number of the new builders sales this year.

According to the report, growth in the price of house stagnate in short term & price data

might fluctuate for some time period, as given lower number of the transactions are going

through. It has also been predicted a drop of 5% in the house this year and 5% rise in year 2021.

As the income and purchasing power of individual have decline, this results to decrease in the

prices of houses individual would not prefer to spend such large amount (Tsai, 2018). Moreover,

it leads to decline in the prices of constructing house as factors of production will not be

available. Housing market of Britain has faced a deep freeze by the measures for slowing down

the spread of COCID-19 and is not likely to recover. Further, its has also been represented that

rental pricing will lower down so individual would not prefer to buy houses and seeks for living

in the rental property.

The property market in UK has largely been reopened, but the experts believes that price

of houses would be falling this year as the economic uncertainty continues in wake of

which are being implemented by the UK government has lead to increase in the supply of

housing and meeting with the demand along with the reasonable and affordable prices. This has

brought little stability in the UK housing market.

4. Predicting an impact of Coronavirus on the UK housing market

Housing prices in UK would be falling in coming periods but are seen as unlikely to drop as

dramatically in the year 2008. COVID-19 halted a residential market in UK after country's

government stopped the house viewings and protected the real estate agent from promoting the

new properties as the part of the broader moves for containing the spread of pandemic. Though,

future prices of house would depend on the time period for which this pandemic lasts but the

analysts are very much confident that lower rate of interest and the shortage of supply would

limit their decrease or fall. The novel coronavirus seems to have the long run implication for all

aspects of residential property (Than-Thi, Dong and Chen, 2019). As the restrictions are been

gradually lifted, sector started to operate again under the social distancing measures. A

significant recession might be seen in UK housing market as the consumer confidence would be

slow to the return. Although an official guideline allowed the construction sites for remaining as

open during the period of lock-down, but most of the large housebuilder had shut down because

of the difficulty in maintaining the social distancing. Halt in the construction is seen as inevitably

causing fall in delivery of the housing and number of the new builders sales this year.

According to the report, growth in the price of house stagnate in short term & price data

might fluctuate for some time period, as given lower number of the transactions are going

through. It has also been predicted a drop of 5% in the house this year and 5% rise in year 2021.

As the income and purchasing power of individual have decline, this results to decrease in the

prices of houses individual would not prefer to spend such large amount (Tsai, 2018). Moreover,

it leads to decline in the prices of constructing house as factors of production will not be

available. Housing market of Britain has faced a deep freeze by the measures for slowing down

the spread of COCID-19 and is not likely to recover. Further, its has also been represented that

rental pricing will lower down so individual would not prefer to buy houses and seeks for living

in the rental property.

The property market in UK has largely been reopened, but the experts believes that price

of houses would be falling this year as the economic uncertainty continues in wake of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

coronavirus outbreak. It has been likely to seen that in the future prices of houses would be

fluctuating on a significant basis. An expert across a board expected that the property market to

take a hit this year and would bounce back in the future periods on a quick basis (Cochrane and

Poot, 2019). Different individual predicted the price differently as Knight Frank predicted drop

of 3% this year and increase of 5% in the year 2021.

CONCLUSION

The above report concludes that over the period of 10 year the price of housing market

has increased because of various economic factors that is interest rate, unemployment rate,

income, economic growth, population etc. This shows that in the past years there were many

causes due to which the price of the housing market has increased and this results to increase in

the demand of the house by the individual. There were several supplies related factors like price

of the substitute goods, number of the suppliers etc. which induces the housing market to grow.

fluctuating on a significant basis. An expert across a board expected that the property market to

take a hit this year and would bounce back in the future periods on a quick basis (Cochrane and

Poot, 2019). Different individual predicted the price differently as Knight Frank predicted drop

of 3% this year and increase of 5% in the year 2021.

CONCLUSION

The above report concludes that over the period of 10 year the price of housing market

has increased because of various economic factors that is interest rate, unemployment rate,

income, economic growth, population etc. This shows that in the past years there were many

causes due to which the price of the housing market has increased and this results to increase in

the demand of the house by the individual. There were several supplies related factors like price

of the substitute goods, number of the suppliers etc. which induces the housing market to grow.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journal

Al-Masum, M. A. and Lee, C. L., 2019. Modelling housing prices and market fundamentals:

evidence from the Sydney housing market. International Journal of Housing Markets and

Analysis.

Apergis, N. and Payne, J. E., 2020. Florida metropolitan housing markets: examining club

convergence and geographical market segmentation. Journal of Housing Research. pp.1-19.

Ball, M., 2017. Housing policy and economic power: the political economy of owner

occupation (Vol. 828). Routledge.

Banyte, J. and Maliene, V., 2017. Analysis of Factors Influencing Property Market Dynamics in

the UK (No. eres2017_335). European Real Estate Society (ERES).

Brener, A., 2020. Housing and Financial Stability: Mortgage Lending and Macroprudential

Policy in the UK and US. Routledge.

Chuang, M. C. and et.al., 2018. Pricing mortgage insurance contracts under housing price cycles

with jump risk: evidence from the UK housing market. The European Journal of

Finance. 24(11). pp.909-943.

Cochrane, W. and Poot, J., 2019. The Effects of Immigration on Local Housing Markets (No.

19/07).

Hwang, S., Cho, Y. and Shin, J., 2019. Household Overconfidence in the UK Housing Market:

With Respect to Signals About Stock Market, Consumption, and Human

Capital. Consumption, and Human Capital (October 4, 2019).

Payne, S., 2020. Advancing understandings of housing supply constraints: housing market

recovery and institutional transitions in British speculative housebuilding. Housing

Studies. 35(2). pp.266-289.

Savva, C. S., 2018. Factors Affecting Housing Prices: International Evidence. Cyprus Economic

Policy Review. 12(2). pp.87-96.

Sulaiman, N., Mohammed, M. I. and Ghani, Z. A., 2018. Factors Influencing Reverse Mortgage

(RM) Product Market. Advanced Science Letters. 24(6). pp.4623-4625.

Than-Thi, H., Dong, M. C. and Chen, C. W., 2019, January. Bayesian modelling structural

changes on Housing Price Dynamics. In International Conference of the Thailand

Econometrics Society (pp. 83-104). Springer, Cham.

Books and journal

Al-Masum, M. A. and Lee, C. L., 2019. Modelling housing prices and market fundamentals:

evidence from the Sydney housing market. International Journal of Housing Markets and

Analysis.

Apergis, N. and Payne, J. E., 2020. Florida metropolitan housing markets: examining club

convergence and geographical market segmentation. Journal of Housing Research. pp.1-19.

Ball, M., 2017. Housing policy and economic power: the political economy of owner

occupation (Vol. 828). Routledge.

Banyte, J. and Maliene, V., 2017. Analysis of Factors Influencing Property Market Dynamics in

the UK (No. eres2017_335). European Real Estate Society (ERES).

Brener, A., 2020. Housing and Financial Stability: Mortgage Lending and Macroprudential

Policy in the UK and US. Routledge.

Chuang, M. C. and et.al., 2018. Pricing mortgage insurance contracts under housing price cycles

with jump risk: evidence from the UK housing market. The European Journal of

Finance. 24(11). pp.909-943.

Cochrane, W. and Poot, J., 2019. The Effects of Immigration on Local Housing Markets (No.

19/07).

Hwang, S., Cho, Y. and Shin, J., 2019. Household Overconfidence in the UK Housing Market:

With Respect to Signals About Stock Market, Consumption, and Human

Capital. Consumption, and Human Capital (October 4, 2019).

Payne, S., 2020. Advancing understandings of housing supply constraints: housing market

recovery and institutional transitions in British speculative housebuilding. Housing

Studies. 35(2). pp.266-289.

Savva, C. S., 2018. Factors Affecting Housing Prices: International Evidence. Cyprus Economic

Policy Review. 12(2). pp.87-96.

Sulaiman, N., Mohammed, M. I. and Ghani, Z. A., 2018. Factors Influencing Reverse Mortgage

(RM) Product Market. Advanced Science Letters. 24(6). pp.4623-4625.

Than-Thi, H., Dong, M. C. and Chen, C. W., 2019, January. Bayesian modelling structural

changes on Housing Price Dynamics. In International Conference of the Thailand

Econometrics Society (pp. 83-104). Springer, Cham.

Tsai, I. C., 2018. House price convergence in euro zone and non-euro zone countries. Economic

Systems. 42(2). pp.269-281.

Online

Housing Policies in the United Kingdom, Switzerland, and the United States. 2016. [Online].

Available Through:<https://www.adb.org/sites/default/files/publication/183139/adbi-

wp569.pdf>.

Systems. 42(2). pp.269-281.

Online

Housing Policies in the United Kingdom, Switzerland, and the United States. 2016. [Online].

Available Through:<https://www.adb.org/sites/default/files/publication/183139/adbi-

wp569.pdf>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.