Comprehensive Analysis of the UK Housing Market from 2009 to 2019

VerifiedAdded on 2023/01/11

|14

|3953

|1

Report

AI Summary

This report provides a comprehensive analysis of the UK housing market, focusing on the period from 2009 to 2019. It begins by evaluating the changes in average house prices, utilizing data from various sources like the House Price Index and local registries, with a specific focus on the Wembley, London area. The report then delves into the economic determinants influencing these price changes, including economic growth, unemployment, interest rates, disposable income, and the supply of new houses, as well as the impact of property location. Furthermore, the report examines the government's actions during this period, such as monetary and fiscal policies, and subsidies, and their effects on the housing market. Finally, it predicts the impact of the COVID-19 pandemic on the UK housing market, considering potential fluctuations and long-term effects. The analysis includes statistical data, graphs and discusses factors like Brexit and global economic crises influencing the market.

UK housing market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

1. Evaluate average house prices in the UK changed over the period from 2009 – 2019...........1

2. What are the economic determinants of the changes...............................................................3

3. Government action over the period 2009-2019 which affected the UK Housing Market.......9

4. Predict what would be the impact of COVID-19 on UK Housing Market...........................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

MAIN BODY..................................................................................................................................1

1. Evaluate average house prices in the UK changed over the period from 2009 – 2019...........1

2. What are the economic determinants of the changes...............................................................3

3. Government action over the period 2009-2019 which affected the UK Housing Market.......9

4. Predict what would be the impact of COVID-19 on UK Housing Market...........................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Economists and housing analysts foresee rates falling up to 13 percent across the UK, with

“brutal” falls in some regions as the property sector continue to recover throughout the COVID-

19 crisis. The array of the big researchers' predictions is considerably broader than average

(Begiazi and Katsiampa, 2019). At one extreme is the Centre for business and economics

Analysis, which forecasts that rates for 2020 will plunge by 13% "as a shortage of transactions,

high volatility and declining wages are taking their toll." However the property manager Savills

has said that the demand impact might be more like 5 percent, and a third of valuation surveyors

expect price losses might be restricted to 4 percent or less. This report is based on the UK

housing market and especially the Wembley London zone and impact on its price level. This

assessment covers the several topics such as average housing price in the UK throughout the

period of 2009 to 2019. Also evaluate the determinate which impact the change in housing

market price and evaluate the government actions which affect the UK housing market. In

addition, this report includes the impact of Covid-19 on UK housing market.

MAIN BODY

1. Evaluate average house prices in the UK changed over the period from 2009 – 2019

In the analysis of UK average housing prices are evaluated through House Price Index,

Scotland Registries, and Northern Ireland Land and Property Services residency sales figure. It is

analyzed by the National Statistics Office that applies index follow the mathematical approach

for different sources of data on property values and attributes to generate estimates of the rise in

real estate prices throughout the years and called a hedonic regression model. It is proposed that

the limited amount of selling purchases in other local authorities would result in volatility of fig

at these levels (Benbouzid, Mallick and Pilbeam, 2018). Geographies with small revenue

transactions should be examined in the perspective of their longer-term trends, rather than

relying on quarterly shifts.

London has experienced the fastest rates of rising house prices over the past decade-the

expected capital home has increased by 72 per percent-more than twice the overall UK house

price gain of 33.7 per cent. However the wealth has shown a marked downturn in recent years,

and house prices have dropped back from their high point in many areas of London.

1

Economists and housing analysts foresee rates falling up to 13 percent across the UK, with

“brutal” falls in some regions as the property sector continue to recover throughout the COVID-

19 crisis. The array of the big researchers' predictions is considerably broader than average

(Begiazi and Katsiampa, 2019). At one extreme is the Centre for business and economics

Analysis, which forecasts that rates for 2020 will plunge by 13% "as a shortage of transactions,

high volatility and declining wages are taking their toll." However the property manager Savills

has said that the demand impact might be more like 5 percent, and a third of valuation surveyors

expect price losses might be restricted to 4 percent or less. This report is based on the UK

housing market and especially the Wembley London zone and impact on its price level. This

assessment covers the several topics such as average housing price in the UK throughout the

period of 2009 to 2019. Also evaluate the determinate which impact the change in housing

market price and evaluate the government actions which affect the UK housing market. In

addition, this report includes the impact of Covid-19 on UK housing market.

MAIN BODY

1. Evaluate average house prices in the UK changed over the period from 2009 – 2019

In the analysis of UK average housing prices are evaluated through House Price Index,

Scotland Registries, and Northern Ireland Land and Property Services residency sales figure. It is

analyzed by the National Statistics Office that applies index follow the mathematical approach

for different sources of data on property values and attributes to generate estimates of the rise in

real estate prices throughout the years and called a hedonic regression model. It is proposed that

the limited amount of selling purchases in other local authorities would result in volatility of fig

at these levels (Benbouzid, Mallick and Pilbeam, 2018). Geographies with small revenue

transactions should be examined in the perspective of their longer-term trends, rather than

relying on quarterly shifts.

London has experienced the fastest rates of rising house prices over the past decade-the

expected capital home has increased by 72 per percent-more than twice the overall UK house

price gain of 33.7 per cent. However the wealth has shown a marked downturn in recent years,

and house prices have dropped back from their high point in many areas of London.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

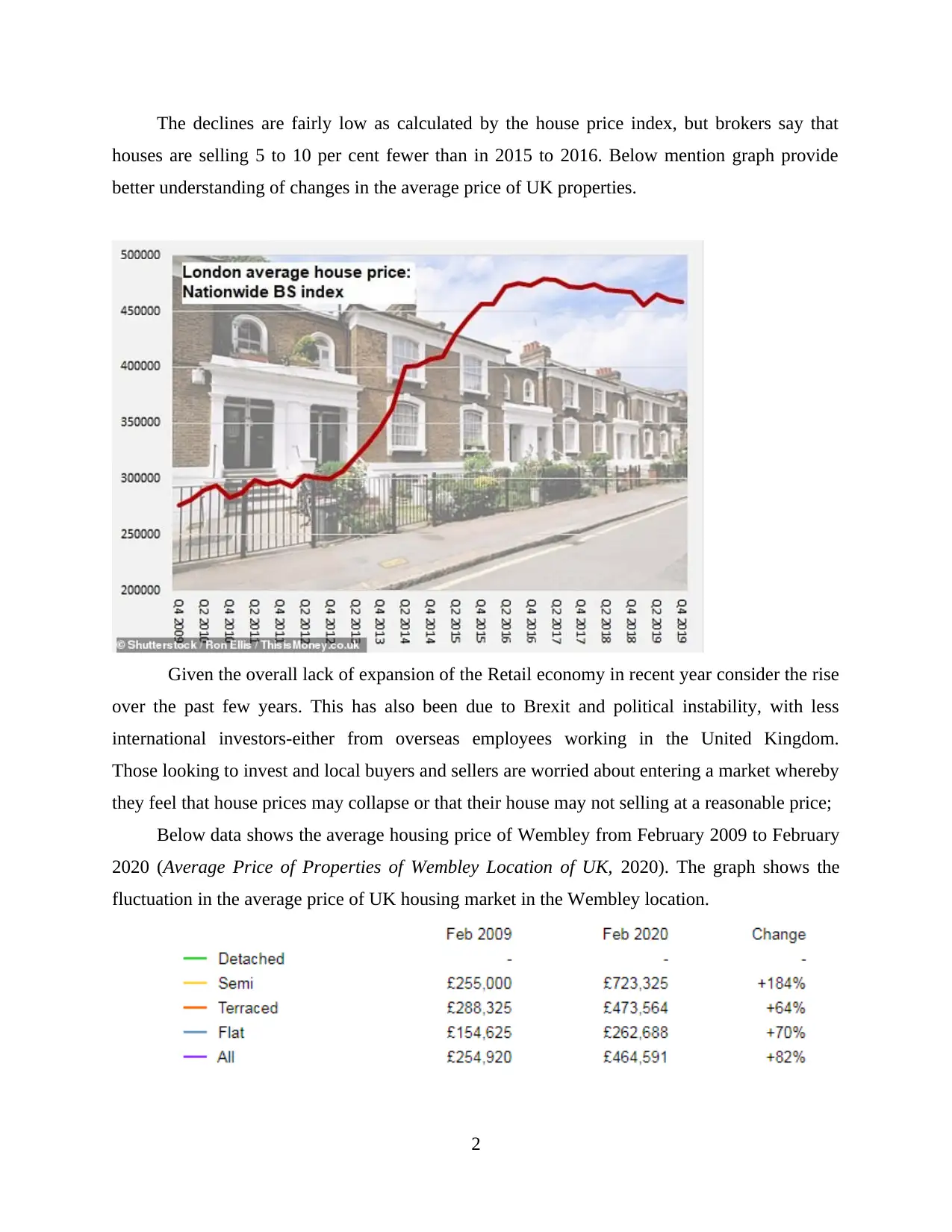

The declines are fairly low as calculated by the house price index, but brokers say that

houses are selling 5 to 10 per cent fewer than in 2015 to 2016. Below mention graph provide

better understanding of changes in the average price of UK properties.

Given the overall lack of expansion of the Retail economy in recent year consider the rise

over the past few years. This has also been due to Brexit and political instability, with less

international investors-either from overseas employees working in the United Kingdom.

Those looking to invest and local buyers and sellers are worried about entering a market whereby

they feel that house prices may collapse or that their house may not selling at a reasonable price;

Below data shows the average housing price of Wembley from February 2009 to February

2020 (Average Price of Properties of Wembley Location of UK, 2020). The graph shows the

fluctuation in the average price of UK housing market in the Wembley location.

2

houses are selling 5 to 10 per cent fewer than in 2015 to 2016. Below mention graph provide

better understanding of changes in the average price of UK properties.

Given the overall lack of expansion of the Retail economy in recent year consider the rise

over the past few years. This has also been due to Brexit and political instability, with less

international investors-either from overseas employees working in the United Kingdom.

Those looking to invest and local buyers and sellers are worried about entering a market whereby

they feel that house prices may collapse or that their house may not selling at a reasonable price;

Below data shows the average housing price of Wembley from February 2009 to February

2020 (Average Price of Properties of Wembley Location of UK, 2020). The graph shows the

fluctuation in the average price of UK housing market in the Wembley location.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

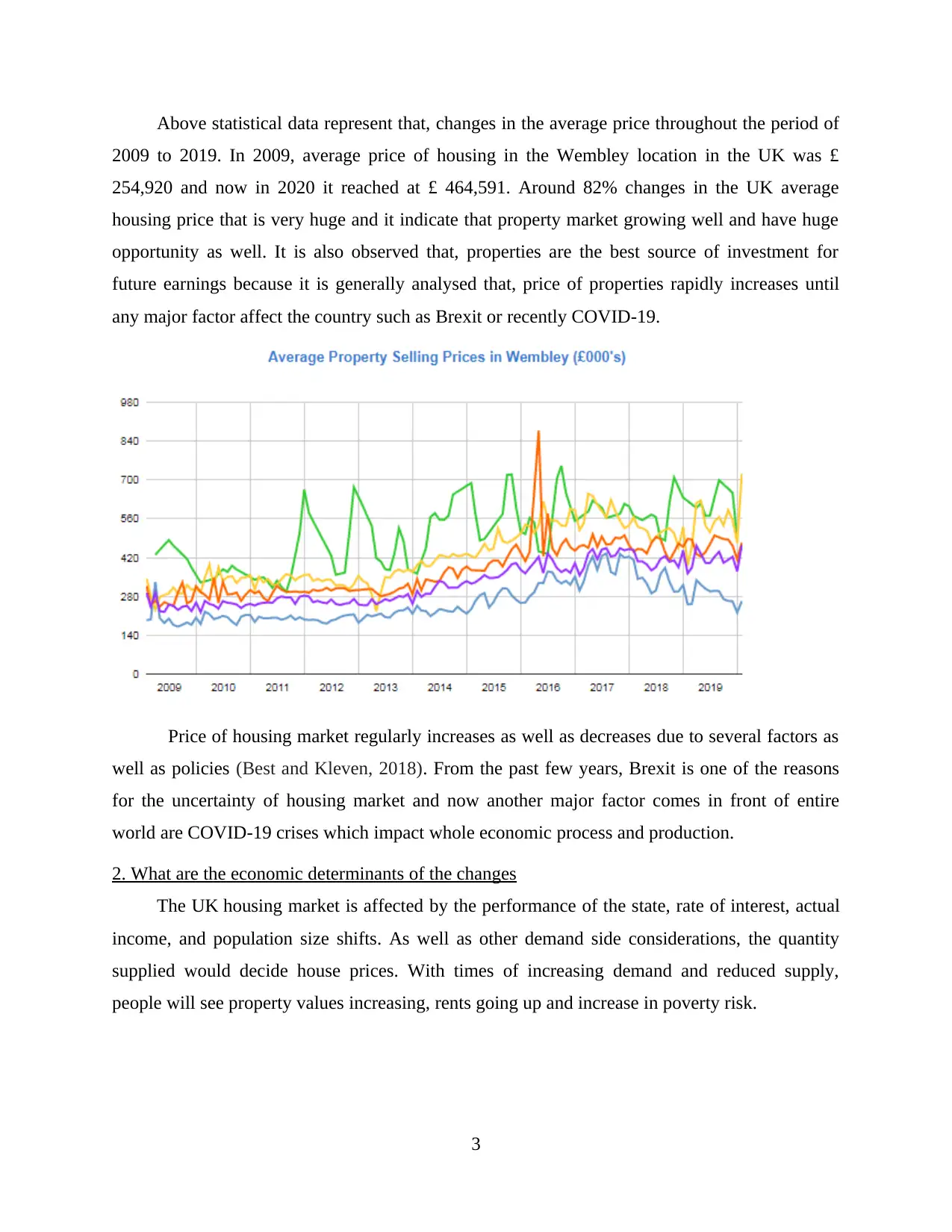

Above statistical data represent that, changes in the average price throughout the period of

2009 to 2019. In 2009, average price of housing in the Wembley location in the UK was £

254,920 and now in 2020 it reached at £ 464,591. Around 82% changes in the UK average

housing price that is very huge and it indicate that property market growing well and have huge

opportunity as well. It is also observed that, properties are the best source of investment for

future earnings because it is generally analysed that, price of properties rapidly increases until

any major factor affect the country such as Brexit or recently COVID-19.

Price of housing market regularly increases as well as decreases due to several factors as

well as policies (Best and Kleven, 2018). From the past few years, Brexit is one of the reasons

for the uncertainty of housing market and now another major factor comes in front of entire

world are COVID-19 crises which impact whole economic process and production.

2. What are the economic determinants of the changes

The UK housing market is affected by the performance of the state, rate of interest, actual

income, and population size shifts. As well as other demand side considerations, the quantity

supplied would decide house prices. With times of increasing demand and reduced supply,

people will see property values increasing, rents going up and increase in poverty risk.

3

2009 to 2019. In 2009, average price of housing in the Wembley location in the UK was £

254,920 and now in 2020 it reached at £ 464,591. Around 82% changes in the UK average

housing price that is very huge and it indicate that property market growing well and have huge

opportunity as well. It is also observed that, properties are the best source of investment for

future earnings because it is generally analysed that, price of properties rapidly increases until

any major factor affect the country such as Brexit or recently COVID-19.

Price of housing market regularly increases as well as decreases due to several factors as

well as policies (Best and Kleven, 2018). From the past few years, Brexit is one of the reasons

for the uncertainty of housing market and now another major factor comes in front of entire

world are COVID-19 crises which impact whole economic process and production.

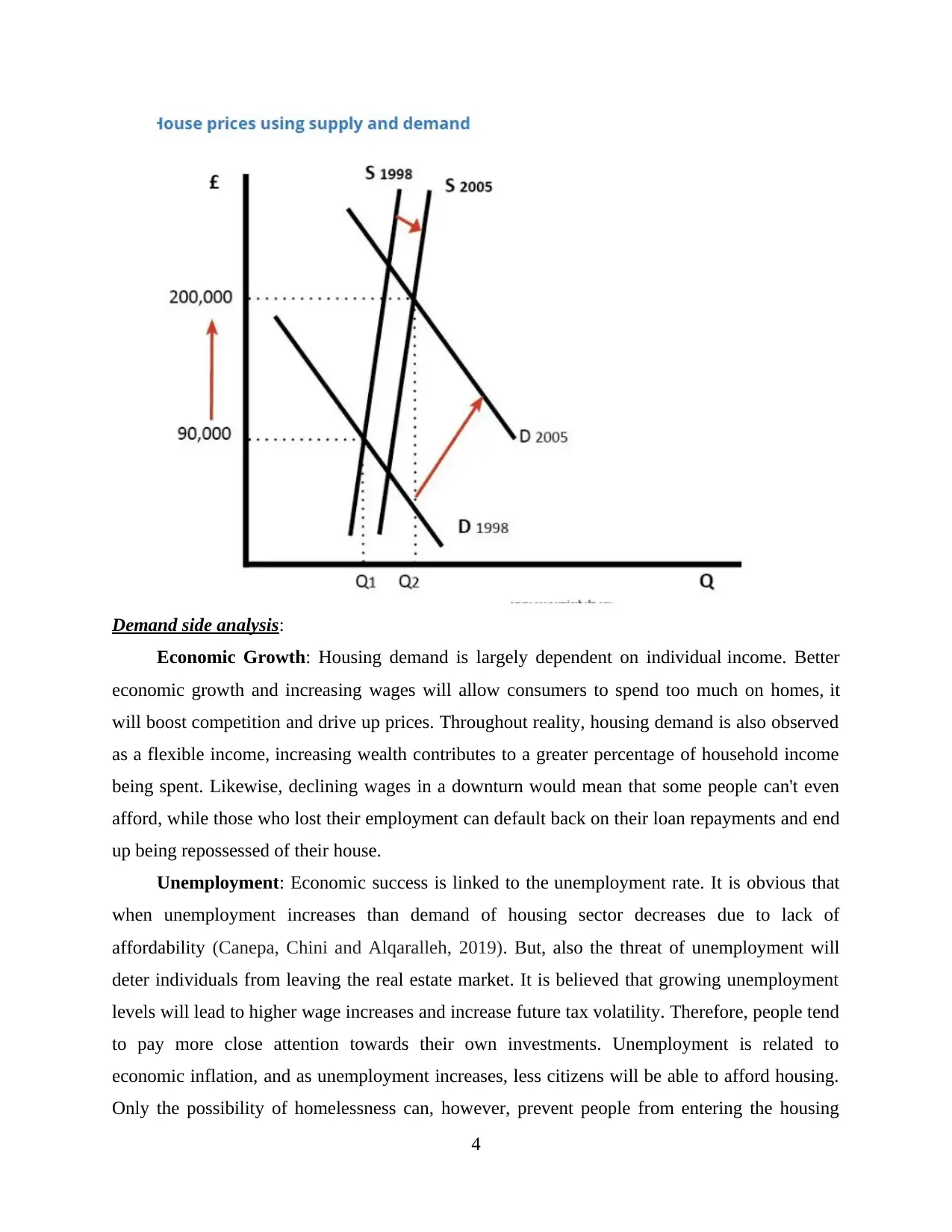

2. What are the economic determinants of the changes

The UK housing market is affected by the performance of the state, rate of interest, actual

income, and population size shifts. As well as other demand side considerations, the quantity

supplied would decide house prices. With times of increasing demand and reduced supply,

people will see property values increasing, rents going up and increase in poverty risk.

3

Demand side analysis:

Economic Growth: Housing demand is largely dependent on individual income. Better

economic growth and increasing wages will allow consumers to spend too much on homes, it

will boost competition and drive up prices. Throughout reality, housing demand is also observed

as a flexible income, increasing wealth contributes to a greater percentage of household income

being spent. Likewise, declining wages in a downturn would mean that some people can't even

afford, while those who lost their employment can default back on their loan repayments and end

up being repossessed of their house.

Unemployment: Economic success is linked to the unemployment rate. It is obvious that

when unemployment increases than demand of housing sector decreases due to lack of

affordability (Canepa, Chini and Alqaralleh, 2019). But, also the threat of unemployment will

deter individuals from leaving the real estate market. It is believed that growing unemployment

levels will lead to higher wage increases and increase future tax volatility. Therefore, people tend

to pay more close attention towards their own investments. Unemployment is related to

economic inflation, and as unemployment increases, less citizens will be able to afford housing.

Only the possibility of homelessness can, however, prevent people from entering the housing

4

Economic Growth: Housing demand is largely dependent on individual income. Better

economic growth and increasing wages will allow consumers to spend too much on homes, it

will boost competition and drive up prices. Throughout reality, housing demand is also observed

as a flexible income, increasing wealth contributes to a greater percentage of household income

being spent. Likewise, declining wages in a downturn would mean that some people can't even

afford, while those who lost their employment can default back on their loan repayments and end

up being repossessed of their house.

Unemployment: Economic success is linked to the unemployment rate. It is obvious that

when unemployment increases than demand of housing sector decreases due to lack of

affordability (Canepa, Chini and Alqaralleh, 2019). But, also the threat of unemployment will

deter individuals from leaving the real estate market. It is believed that growing unemployment

levels will lead to higher wage increases and increase future tax volatility. Therefore, people tend

to pay more close attention towards their own investments. Unemployment is related to

economic inflation, and as unemployment increases, less citizens will be able to afford housing.

Only the possibility of homelessness can, however, prevent people from entering the housing

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

market. Essentially, as the unemployment rate rise then British home sector demand often

decreases people would be unable to manage buying new houses since they are unemployed.

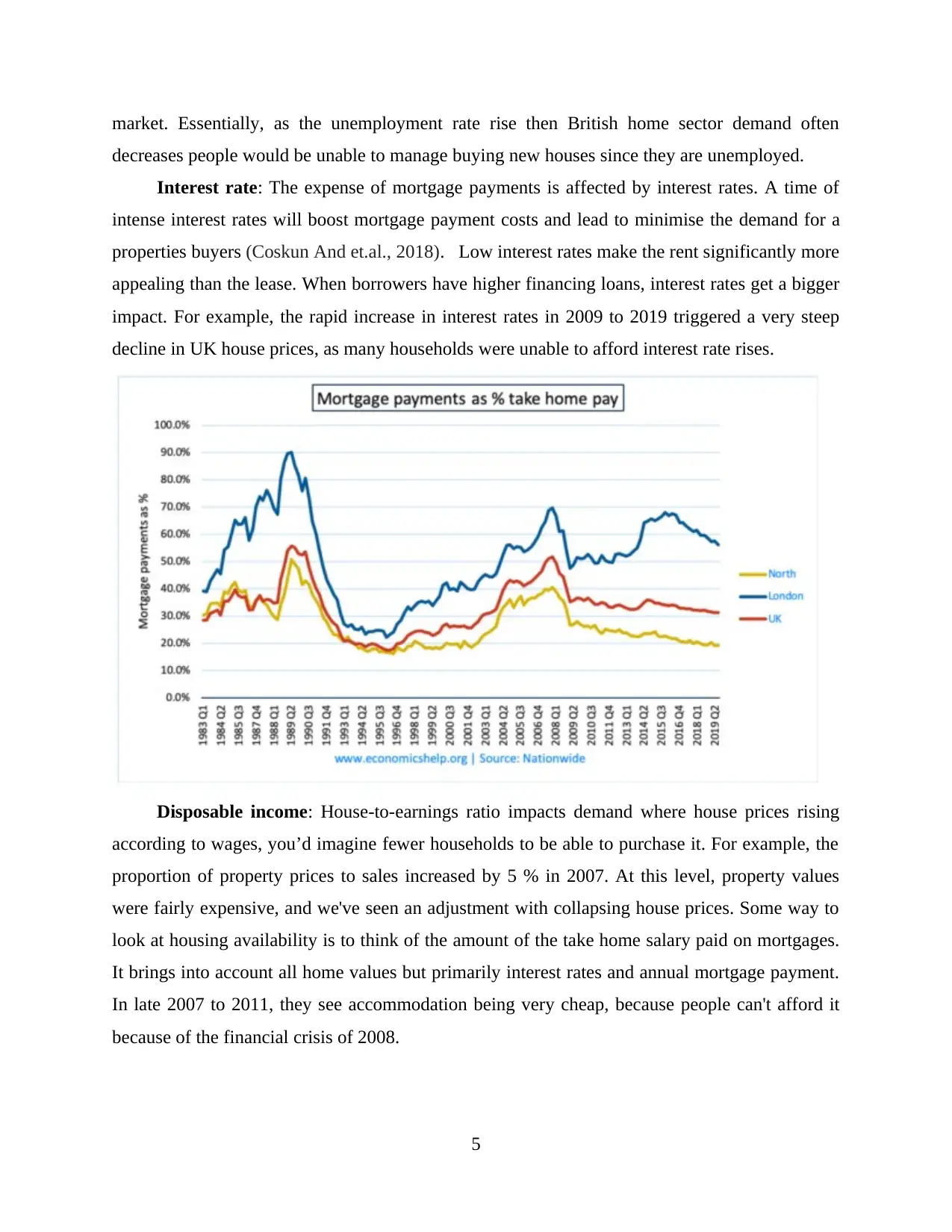

Interest rate: The expense of mortgage payments is affected by interest rates. A time of

intense interest rates will boost mortgage payment costs and lead to minimise the demand for a

properties buyers (Coskun And et.al., 2018). Low interest rates make the rent significantly more

appealing than the lease. When borrowers have higher financing loans, interest rates get a bigger

impact. For example, the rapid increase in interest rates in 2009 to 2019 triggered a very steep

decline in UK house prices, as many households were unable to afford interest rate rises.

Disposable income: House-to-earnings ratio impacts demand where house prices rising

according to wages, you’d imagine fewer households to be able to purchase it. For example, the

proportion of property prices to sales increased by 5 % in 2007. At this level, property values

were fairly expensive, and we've seen an adjustment with collapsing house prices. Some way to

look at housing availability is to think of the amount of the take home salary paid on mortgages.

It brings into account all home values but primarily interest rates and annual mortgage payment.

In late 2007 to 2011, they see accommodation being very cheap, because people can't afford it

because of the financial crisis of 2008.

5

decreases people would be unable to manage buying new houses since they are unemployed.

Interest rate: The expense of mortgage payments is affected by interest rates. A time of

intense interest rates will boost mortgage payment costs and lead to minimise the demand for a

properties buyers (Coskun And et.al., 2018). Low interest rates make the rent significantly more

appealing than the lease. When borrowers have higher financing loans, interest rates get a bigger

impact. For example, the rapid increase in interest rates in 2009 to 2019 triggered a very steep

decline in UK house prices, as many households were unable to afford interest rate rises.

Disposable income: House-to-earnings ratio impacts demand where house prices rising

according to wages, you’d imagine fewer households to be able to purchase it. For example, the

proportion of property prices to sales increased by 5 % in 2007. At this level, property values

were fairly expensive, and we've seen an adjustment with collapsing house prices. Some way to

look at housing availability is to think of the amount of the take home salary paid on mortgages.

It brings into account all home values but primarily interest rates and annual mortgage payment.

In late 2007 to 2011, they see accommodation being very cheap, because people can't afford it

because of the financial crisis of 2008.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Supply side analysis:

Supply of new houses: A decline in production brings UK housing market prices

higher and another side output surplus will drive down costs. For example, in the Irish real estate

boom from 1996-2006 an estimated 700,000 new houses were constructed. Any time the housing

sector crashed; there was a systemic over-supply to the industry. UK House prices have been

approaching 15 per cent, and prices are dropping with rising competition from production. In

contrast, housing supply has fallen behind British production. UK house rates did not fall as

much as they did with a crisis in Ireland and rapidly stabilized due to ongoing financial crunch.

Supplying accommodation relies on the available supply and development of new homes.

Available cases in the Housing market are to be rather inelastic, because it is a time-consuming

procedure to legally secure building approval to build the homes. Intervals of increases in house

prices can well not trigger an equivalent increase in production, particularly in countries like the

UK with constrained home building properties.

6

Supply of new houses: A decline in production brings UK housing market prices

higher and another side output surplus will drive down costs. For example, in the Irish real estate

boom from 1996-2006 an estimated 700,000 new houses were constructed. Any time the housing

sector crashed; there was a systemic over-supply to the industry. UK House prices have been

approaching 15 per cent, and prices are dropping with rising competition from production. In

contrast, housing supply has fallen behind British production. UK house rates did not fall as

much as they did with a crisis in Ireland and rapidly stabilized due to ongoing financial crunch.

Supplying accommodation relies on the available supply and development of new homes.

Available cases in the Housing market are to be rather inelastic, because it is a time-consuming

procedure to legally secure building approval to build the homes. Intervals of increases in house

prices can well not trigger an equivalent increase in production, particularly in countries like the

UK with constrained home building properties.

6

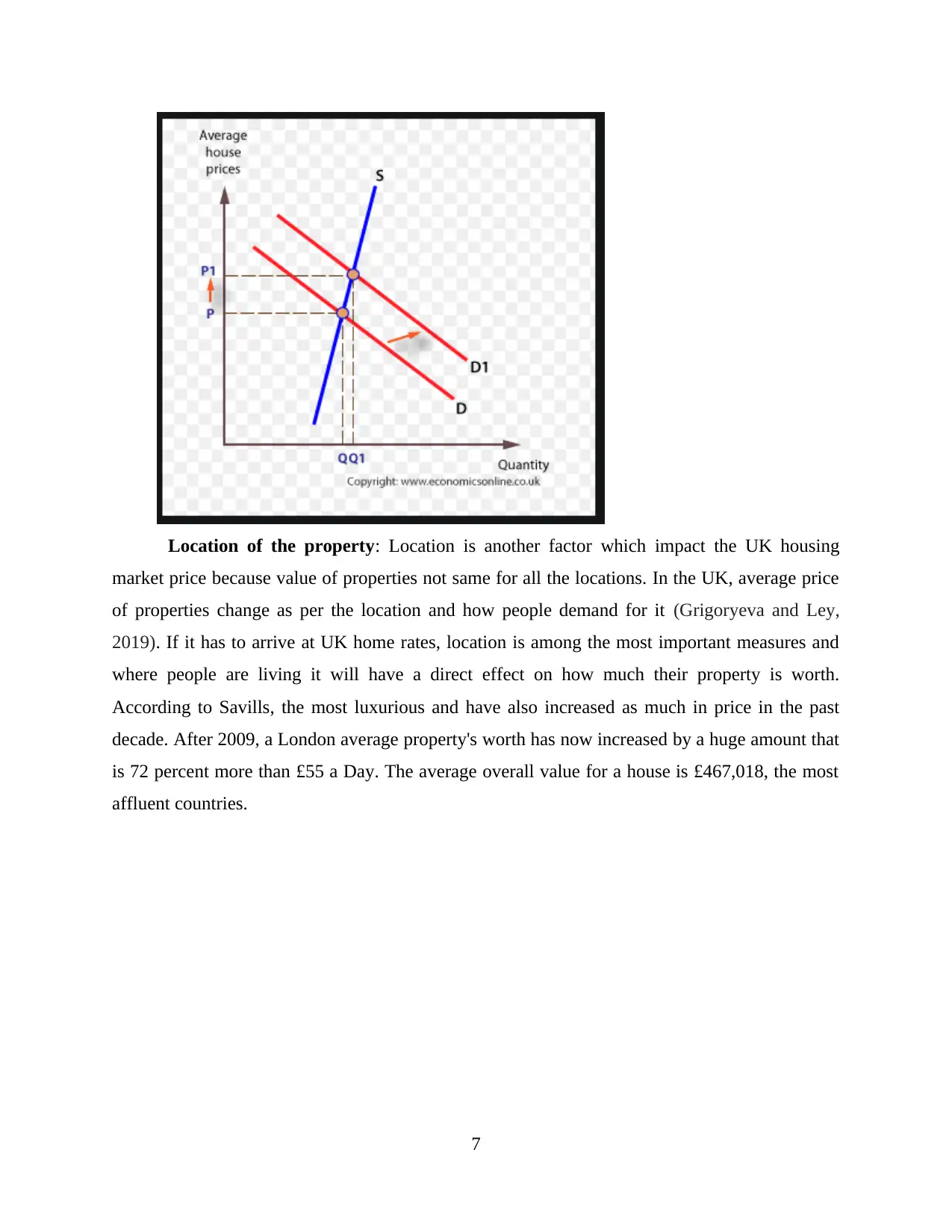

Location of the property: Location is another factor which impact the UK housing

market price because value of properties not same for all the locations. In the UK, average price

of properties change as per the location and how people demand for it (Grigoryeva and Ley,

2019). If it has to arrive at UK home rates, location is among the most important measures and

where people are living it will have a direct effect on how much their property is worth.

According to Savills, the most luxurious and have also increased as much in price in the past

decade. After 2009, a London average property's worth has now increased by a huge amount that

is 72 percent more than £55 a Day. The average overall value for a house is £467,018, the most

affluent countries.

7

market price because value of properties not same for all the locations. In the UK, average price

of properties change as per the location and how people demand for it (Grigoryeva and Ley,

2019). If it has to arrive at UK home rates, location is among the most important measures and

where people are living it will have a direct effect on how much their property is worth.

According to Savills, the most luxurious and have also increased as much in price in the past

decade. After 2009, a London average property's worth has now increased by a huge amount that

is 72 percent more than £55 a Day. The average overall value for a house is £467,018, the most

affluent countries.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

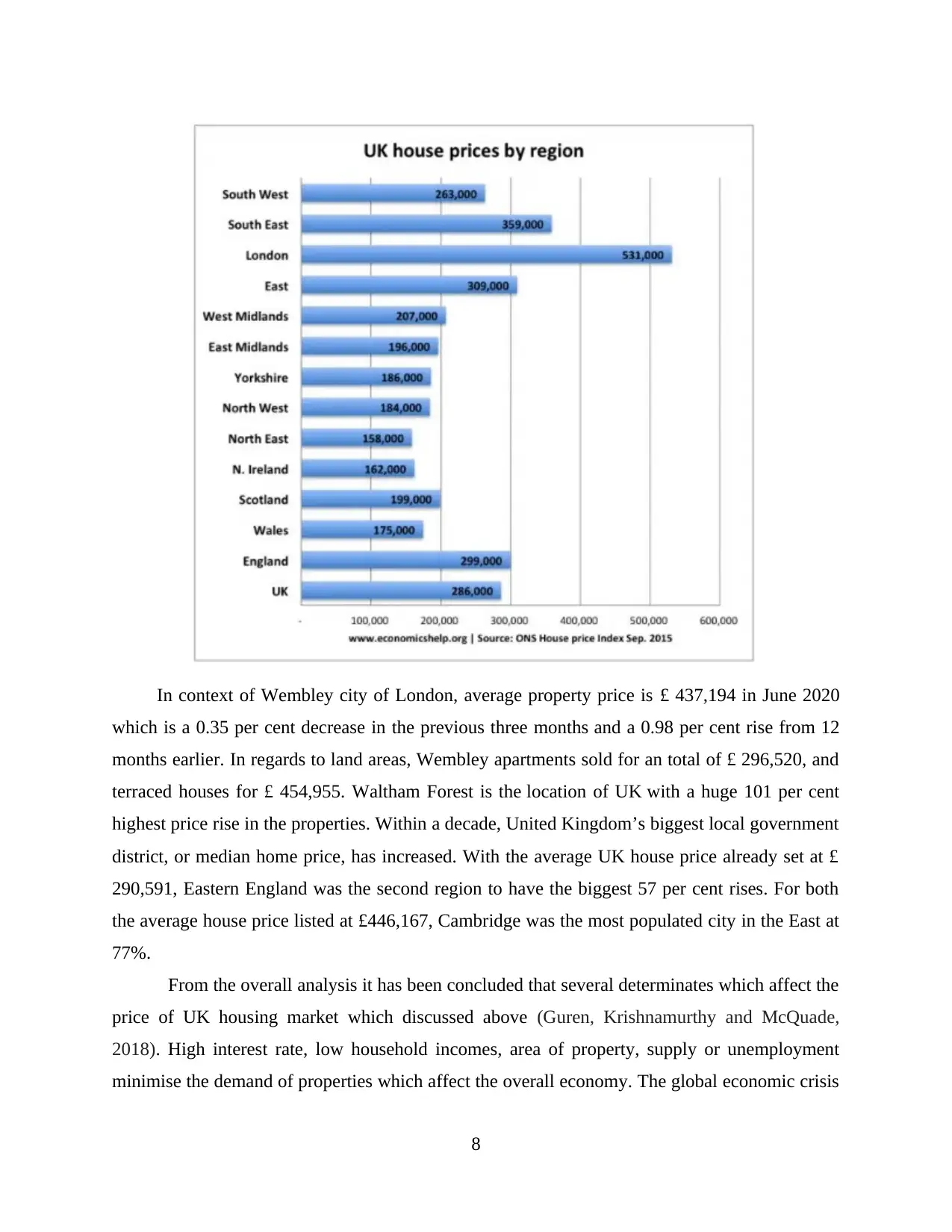

In context of Wembley city of London, average property price is £ 437,194 in June 2020

which is a 0.35 per cent decrease in the previous three months and a 0.98 per cent rise from 12

months earlier. In regards to land areas, Wembley apartments sold for an total of £ 296,520, and

terraced houses for £ 454,955. Waltham Forest is the location of UK with a huge 101 per cent

highest price rise in the properties. Within a decade, United Kingdom’s biggest local government

district, or median home price, has increased. With the average UK house price already set at £

290,591, Eastern England was the second region to have the biggest 57 per cent rises. For both

the average house price listed at £446,167, Cambridge was the most populated city in the East at

77%.

From the overall analysis it has been concluded that several determinates which affect the

price of UK housing market which discussed above (Guren, Krishnamurthy and McQuade,

2018). High interest rate, low household incomes, area of property, supply or unemployment

minimise the demand of properties which affect the overall economy. The global economic crisis

8

which is a 0.35 per cent decrease in the previous three months and a 0.98 per cent rise from 12

months earlier. In regards to land areas, Wembley apartments sold for an total of £ 296,520, and

terraced houses for £ 454,955. Waltham Forest is the location of UK with a huge 101 per cent

highest price rise in the properties. Within a decade, United Kingdom’s biggest local government

district, or median home price, has increased. With the average UK house price already set at £

290,591, Eastern England was the second region to have the biggest 57 per cent rises. For both

the average house price listed at £446,167, Cambridge was the most populated city in the East at

77%.

From the overall analysis it has been concluded that several determinates which affect the

price of UK housing market which discussed above (Guren, Krishnamurthy and McQuade,

2018). High interest rate, low household incomes, area of property, supply or unemployment

minimise the demand of properties which affect the overall economy. The global economic crisis

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

has urged the researcher of the United Kingdom to take tighter immigration initiatives.

Consequently, it has that the arriving arrivals from the UK and competition for houses is not that.

3. Government action over the period 2009-2019 which affected the UK Housing Market

Throughout the period, UK Housing market faces several changes and in order to balance

the economy, government will take several actions and those are discussed below:

Monetary and fiscal policy: Some of the experience indicated that simplifying property

values is the Bank of England’s responsibility. This would include interest rate increases to avoid

withdrawal of loans. The Bank of England is therefore largely responsible for business and

economic growth (Jacobs and Manzi, 2019). The goal of catching the housing market isn't

monetary policy. If the Bank of England needs to promote prices for housing, this may interact

with growth in the economy.

Government subsidies: Extra budget spending on subsidizing the supply of 'private'

housing could significantly boost demand. Currently over the last years, council houses have

fallen out of fashion because the govt has sought to auction off council housing and scale back

on public accommodation. Although, in the post-war period, this was council estates that brought

the UK residential property stock a major boost. Strong policy spending is motivating voters to

expect more and rising spending is stopping them.

New garden cities: Constructing new cities, in the style of Milton Keynes, allowing a

substantial rise in the UK property market. Now plans are being made for a new arrangement in

Ebbsfleet, Kent with high speed railway track to London. This will take quite some time to

complete this though from making preparations. That often entails building land on green space,

which may express concerns.

Restrictions on constructions: Restrictions on making plans are very rigid in the UK.

Easing the ton of legislation and looking to make the process more stable would consider it

easier for the contractors (Norris and Byrne, 2018). This can mean a decrease in the total of

protected greenbelt land. This could also require the simplification of the rules that household-

builders should value. As people speak up about the excessive construction, overpopulation and

loss of green areas, this can result in significant local concerns. Another alternative is to add

money to develop new homes for desirable Greenfield and Brownfield areas.

According to the government actions in the future, it is predicted that UK housing prices

are increase during the next 5 years by 15.3 per cent, which is just 1 per cent of the total GDP of

9

Consequently, it has that the arriving arrivals from the UK and competition for houses is not that.

3. Government action over the period 2009-2019 which affected the UK Housing Market

Throughout the period, UK Housing market faces several changes and in order to balance

the economy, government will take several actions and those are discussed below:

Monetary and fiscal policy: Some of the experience indicated that simplifying property

values is the Bank of England’s responsibility. This would include interest rate increases to avoid

withdrawal of loans. The Bank of England is therefore largely responsible for business and

economic growth (Jacobs and Manzi, 2019). The goal of catching the housing market isn't

monetary policy. If the Bank of England needs to promote prices for housing, this may interact

with growth in the economy.

Government subsidies: Extra budget spending on subsidizing the supply of 'private'

housing could significantly boost demand. Currently over the last years, council houses have

fallen out of fashion because the govt has sought to auction off council housing and scale back

on public accommodation. Although, in the post-war period, this was council estates that brought

the UK residential property stock a major boost. Strong policy spending is motivating voters to

expect more and rising spending is stopping them.

New garden cities: Constructing new cities, in the style of Milton Keynes, allowing a

substantial rise in the UK property market. Now plans are being made for a new arrangement in

Ebbsfleet, Kent with high speed railway track to London. This will take quite some time to

complete this though from making preparations. That often entails building land on green space,

which may express concerns.

Restrictions on constructions: Restrictions on making plans are very rigid in the UK.

Easing the ton of legislation and looking to make the process more stable would consider it

easier for the contractors (Norris and Byrne, 2018). This can mean a decrease in the total of

protected greenbelt land. This could also require the simplification of the rules that household-

builders should value. As people speak up about the excessive construction, overpopulation and

loss of green areas, this can result in significant local concerns. Another alternative is to add

money to develop new homes for desirable Greenfield and Brownfield areas.

According to the government actions in the future, it is predicted that UK housing prices

are increase during the next 5 years by 15.3 per cent, which is just 1 per cent of the total GDP of

9

UK in 2020. Big regional differences are also predicted to occur. As per the Savills, it was

announced their estimates for the time frames up to 2024, where both Yorkshire and the Humber

would have the largest growth of 21.6% thanks to the efficiency and versatility of the national

economy and the demand for future loans to reimburse income. The home brokers suggested that

in the wider UK housing sector, the North will overtake the South in both the North West

prediction expected to see the largest price growth of 24 per cent between 2020 and 2024.

4. Predict what would be the impact of COVID-19 on UK Housing Market

UK house prices have began to rebound from Brexit induced volatility in late 2019. The

current findings by Right move indicate that the overall price of property coming on the market

in April fell to £ 311,950 by 0.2 percent. In comparison, UK home prices fell 2.1 per cent in

April last year (Pangallo, Nadal and Vignes, 2019). The estate website said that according to the

corona virus shutdown, there is no "fully operational in the UK housing market" and also that

new transaction is "nearly impossible." Meanwhile, after rising to an eight-month peak of 1.5

percent in January, UK inflation dropped down to 1.1 percent in February.

There is also a need for 300,000 new houses per year in the UK. This is not yet being done,

and progress on new construction sites has been largely paused. Although house builders has

invested more on purchasing new property and planning proposals on hold, this does not change

the perception for the property market and continues to buy strategic property to support the

home building industry. In the meantime, the housing market appears to be dogged by low

construction quality problems that are expected to intensify whether there was a downwards cost

pressure to sustain margins. At Jansons, they understand that properties are a long-term

investment and thus they are also aggressively seeking growth opportunities. Researchers’

transitioned to a modern way of operating to make sure it's really much as normal for us.

Previously, Knight Frank had estimated this year that the average UK house prices would

go down three per cent. It also predicted property prices will slip 2 per cent in Wembley London

(Impact of COVID-19 on UK housing market, 2020). The research was therefore based on the

assumption however by the end of May the UK lockout will be ended. After last week's

government decision that the lockout will be relaxed in phases until at least July, the housing

association now expects that British home prices will sink seven per cent. Primary London

property values will be slip 5 % and it was said by Knight Frank.

10

announced their estimates for the time frames up to 2024, where both Yorkshire and the Humber

would have the largest growth of 21.6% thanks to the efficiency and versatility of the national

economy and the demand for future loans to reimburse income. The home brokers suggested that

in the wider UK housing sector, the North will overtake the South in both the North West

prediction expected to see the largest price growth of 24 per cent between 2020 and 2024.

4. Predict what would be the impact of COVID-19 on UK Housing Market

UK house prices have began to rebound from Brexit induced volatility in late 2019. The

current findings by Right move indicate that the overall price of property coming on the market

in April fell to £ 311,950 by 0.2 percent. In comparison, UK home prices fell 2.1 per cent in

April last year (Pangallo, Nadal and Vignes, 2019). The estate website said that according to the

corona virus shutdown, there is no "fully operational in the UK housing market" and also that

new transaction is "nearly impossible." Meanwhile, after rising to an eight-month peak of 1.5

percent in January, UK inflation dropped down to 1.1 percent in February.

There is also a need for 300,000 new houses per year in the UK. This is not yet being done,

and progress on new construction sites has been largely paused. Although house builders has

invested more on purchasing new property and planning proposals on hold, this does not change

the perception for the property market and continues to buy strategic property to support the

home building industry. In the meantime, the housing market appears to be dogged by low

construction quality problems that are expected to intensify whether there was a downwards cost

pressure to sustain margins. At Jansons, they understand that properties are a long-term

investment and thus they are also aggressively seeking growth opportunities. Researchers’

transitioned to a modern way of operating to make sure it's really much as normal for us.

Previously, Knight Frank had estimated this year that the average UK house prices would

go down three per cent. It also predicted property prices will slip 2 per cent in Wembley London

(Impact of COVID-19 on UK housing market, 2020). The research was therefore based on the

assumption however by the end of May the UK lockout will be ended. After last week's

government decision that the lockout will be relaxed in phases until at least July, the housing

association now expects that British home prices will sink seven per cent. Primary London

property values will be slip 5 % and it was said by Knight Frank.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.