Evaluation of the UK Housing Market: 2009-2019 Trends and Factors

VerifiedAdded on 2023/01/10

|13

|3746

|31

Report

AI Summary

This report provides a comprehensive analysis of the UK housing market from 2009 to 2019. It begins by examining the changes in average house prices, highlighting trends such as increasing costs, affordability issues, and price growth patterns. The report then delves into the economic determinants driving these changes, including economic growth, interest rates, affordability for first-time buyers, mortgage finance, employment levels, and the impact of house price bubbles and regional variations. Furthermore, it explores how government actions during this period, such as policy implementations, affected the housing market. Finally, the report concludes with predictions about the impact of COVID-19 on the UK housing market. The analysis utilizes graphs and data to support the findings, providing a detailed overview of the market's dynamics and the factors influencing them.

Housing market evaluation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

The ways in which average house prices in the UK changed over the period from 2009 – 2019

.....................................................................................................................................................1

The economic determinants of the changes for the average house prices in UK........................3

The ways in which government action over the period 2009-2019 affected the UK Housing

market..........................................................................................................................................6

Predictions for impact of COVID-19 on UK Housing Market....................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

The ways in which average house prices in the UK changed over the period from 2009 – 2019

.....................................................................................................................................................1

The economic determinants of the changes for the average house prices in UK........................3

The ways in which government action over the period 2009-2019 affected the UK Housing

market..........................................................................................................................................6

Predictions for impact of COVID-19 on UK Housing Market....................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The housing market is a market place where the key element is the average price of the

products traded in that market. Housing market of United Kingdom is the major contributor in

the nation’s Gross domestic product (Best and Kleven, 2018). The main aim of this report is to

build an understanding regarding the demand and supply of the housing properties and how this

balance between these determinants determine the average prices in housing market.

In this report, four questions regarding housing market of UK has been answered. The

considerate time period for UK housing market is from 2009 to 2019. In this report, the

determinants due to which average prices of UK housing market has changed will be identified

along with the impact of government’s actions on the UK housing market. Lastly, in this report

impact of COVID 19 on housing market has also been predicted.

MAIN BODY

The ways in which average house prices in the UK changed over the period from 2009 – 2019

Housing market in United Kingdom is the market when people buy or sell houses with the

purpose of investment, rent out or residential. The average house prices in UK have been

changed immensely in the period of between 2009 to 2019. By considering these changes,

various patterns of the change are identified which reflects the ways in which the average house

prices in UK has changed. Some of these identified ways are analysed below:

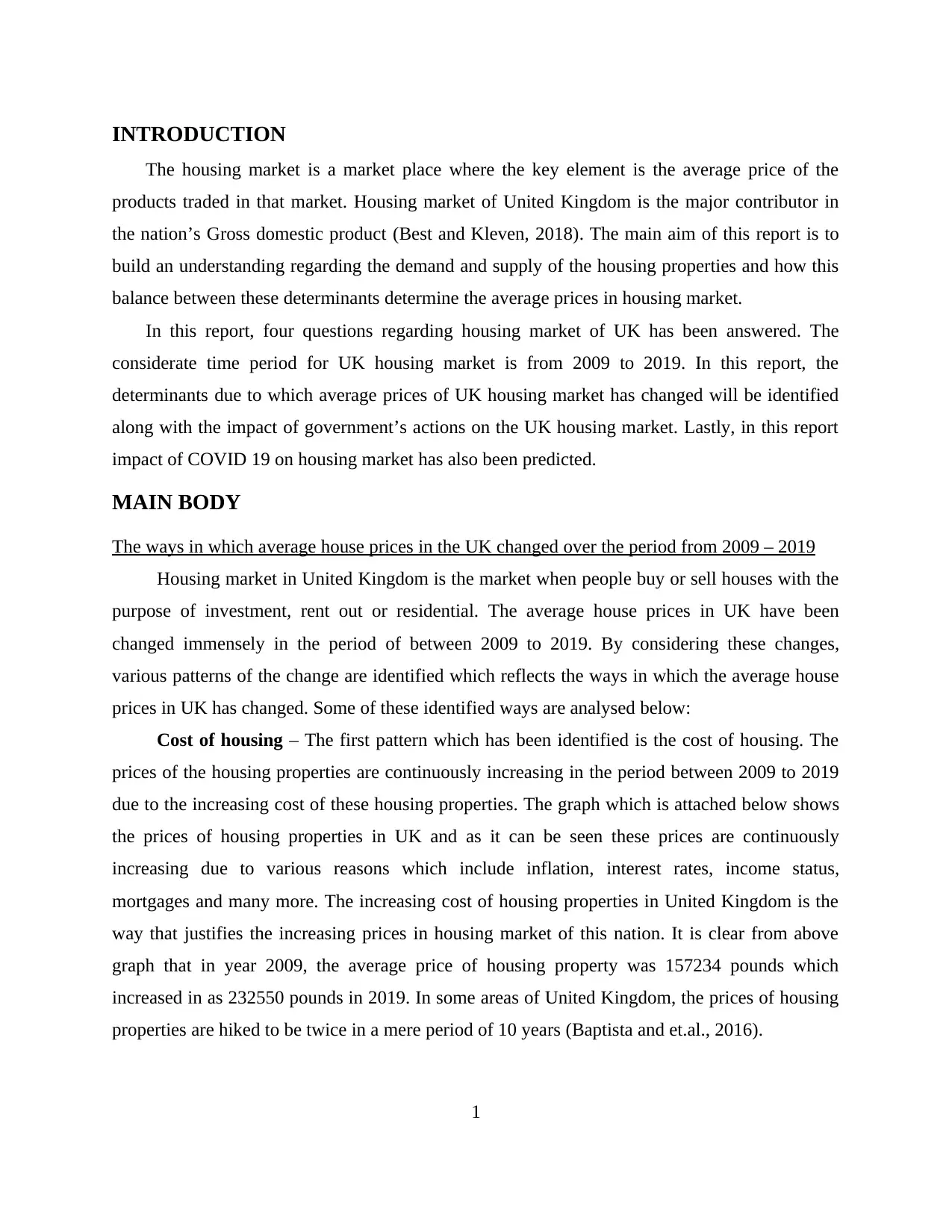

Cost of housing – The first pattern which has been identified is the cost of housing. The

prices of the housing properties are continuously increasing in the period between 2009 to 2019

due to the increasing cost of these housing properties. The graph which is attached below shows

the prices of housing properties in UK and as it can be seen these prices are continuously

increasing due to various reasons which include inflation, interest rates, income status,

mortgages and many more. The increasing cost of housing properties in United Kingdom is the

way that justifies the increasing prices in housing market of this nation. It is clear from above

graph that in year 2009, the average price of housing property was 157234 pounds which

increased in as 232550 pounds in 2019. In some areas of United Kingdom, the prices of housing

properties are hiked to be twice in a mere period of 10 years (Baptista and et.al., 2016).

1

The housing market is a market place where the key element is the average price of the

products traded in that market. Housing market of United Kingdom is the major contributor in

the nation’s Gross domestic product (Best and Kleven, 2018). The main aim of this report is to

build an understanding regarding the demand and supply of the housing properties and how this

balance between these determinants determine the average prices in housing market.

In this report, four questions regarding housing market of UK has been answered. The

considerate time period for UK housing market is from 2009 to 2019. In this report, the

determinants due to which average prices of UK housing market has changed will be identified

along with the impact of government’s actions on the UK housing market. Lastly, in this report

impact of COVID 19 on housing market has also been predicted.

MAIN BODY

The ways in which average house prices in the UK changed over the period from 2009 – 2019

Housing market in United Kingdom is the market when people buy or sell houses with the

purpose of investment, rent out or residential. The average house prices in UK have been

changed immensely in the period of between 2009 to 2019. By considering these changes,

various patterns of the change are identified which reflects the ways in which the average house

prices in UK has changed. Some of these identified ways are analysed below:

Cost of housing – The first pattern which has been identified is the cost of housing. The

prices of the housing properties are continuously increasing in the period between 2009 to 2019

due to the increasing cost of these housing properties. The graph which is attached below shows

the prices of housing properties in UK and as it can be seen these prices are continuously

increasing due to various reasons which include inflation, interest rates, income status,

mortgages and many more. The increasing cost of housing properties in United Kingdom is the

way that justifies the increasing prices in housing market of this nation. It is clear from above

graph that in year 2009, the average price of housing property was 157234 pounds which

increased in as 232550 pounds in 2019. In some areas of United Kingdom, the prices of housing

properties are hiked to be twice in a mere period of 10 years (Baptista and et.al., 2016).

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Source: Average house price in the United Kingdom, 2020)

Affordability of housing – The graph which is used above shows clearly that the prices

of housing properties in United Kingdom are continuously increasing but this graph also shows

that the changes in the price increase is not uniformed as with the price increase, the changes of

price increase has also differentiates (Cook and Vougas, 2009). In order to analyse it more

clearly, another graph is used which is attached below:

(Source: 12 month percentage change in house prices, 2019)

2

Affordability of housing – The graph which is used above shows clearly that the prices

of housing properties in United Kingdom are continuously increasing but this graph also shows

that the changes in the price increase is not uniformed as with the price increase, the changes of

price increase has also differentiates (Cook and Vougas, 2009). In order to analyse it more

clearly, another graph is used which is attached below:

(Source: 12 month percentage change in house prices, 2019)

2

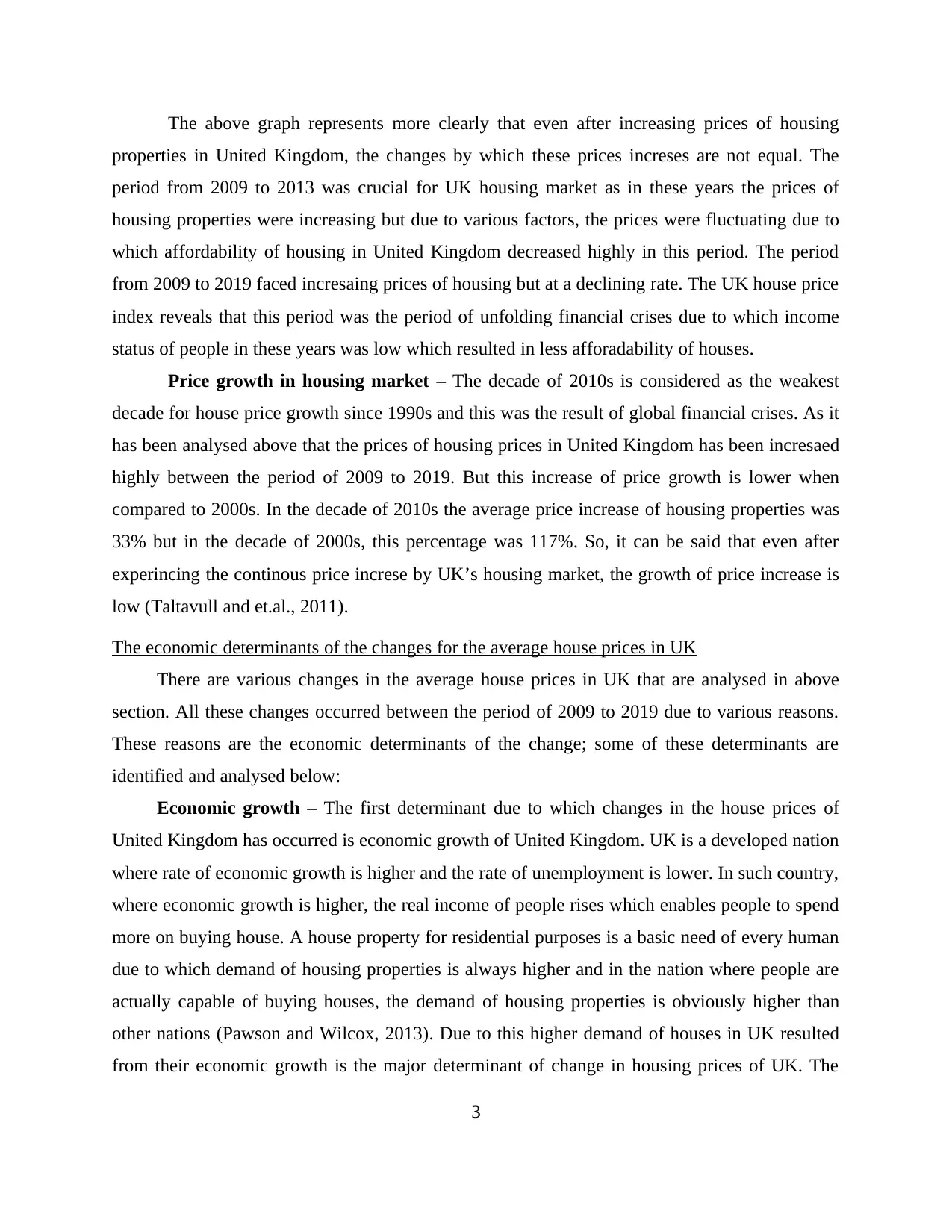

The above graph represents more clearly that even after increasing prices of housing

properties in United Kingdom, the changes by which these prices increses are not equal. The

period from 2009 to 2013 was crucial for UK housing market as in these years the prices of

housing properties were increasing but due to various factors, the prices were fluctuating due to

which affordability of housing in United Kingdom decreased highly in this period. The period

from 2009 to 2019 faced incresaing prices of housing but at a declining rate. The UK house price

index reveals that this period was the period of unfolding financial crises due to which income

status of people in these years was low which resulted in less afforadability of houses.

Price growth in housing market – The decade of 2010s is considered as the weakest

decade for house price growth since 1990s and this was the result of global financial crises. As it

has been analysed above that the prices of housing prices in United Kingdom has been incresaed

highly between the period of 2009 to 2019. But this increase of price growth is lower when

compared to 2000s. In the decade of 2010s the average price increase of housing properties was

33% but in the decade of 2000s, this percentage was 117%. So, it can be said that even after

experincing the continous price increse by UK’s housing market, the growth of price increase is

low (Taltavull and et.al., 2011).

The economic determinants of the changes for the average house prices in UK

There are various changes in the average house prices in UK that are analysed in above

section. All these changes occurred between the period of 2009 to 2019 due to various reasons.

These reasons are the economic determinants of the change; some of these determinants are

identified and analysed below:

Economic growth – The first determinant due to which changes in the house prices of

United Kingdom has occurred is economic growth of United Kingdom. UK is a developed nation

where rate of economic growth is higher and the rate of unemployment is lower. In such country,

where economic growth is higher, the real income of people rises which enables people to spend

more on buying house. A house property for residential purposes is a basic need of every human

due to which demand of housing properties is always higher and in the nation where people are

actually capable of buying houses, the demand of housing properties is obviously higher than

other nations (Pawson and Wilcox, 2013). Due to this higher demand of houses in UK resulted

from their economic growth is the major determinant of change in housing prices of UK. The

3

properties in United Kingdom, the changes by which these prices increses are not equal. The

period from 2009 to 2013 was crucial for UK housing market as in these years the prices of

housing properties were increasing but due to various factors, the prices were fluctuating due to

which affordability of housing in United Kingdom decreased highly in this period. The period

from 2009 to 2019 faced incresaing prices of housing but at a declining rate. The UK house price

index reveals that this period was the period of unfolding financial crises due to which income

status of people in these years was low which resulted in less afforadability of houses.

Price growth in housing market – The decade of 2010s is considered as the weakest

decade for house price growth since 1990s and this was the result of global financial crises. As it

has been analysed above that the prices of housing prices in United Kingdom has been incresaed

highly between the period of 2009 to 2019. But this increase of price growth is lower when

compared to 2000s. In the decade of 2010s the average price increase of housing properties was

33% but in the decade of 2000s, this percentage was 117%. So, it can be said that even after

experincing the continous price increse by UK’s housing market, the growth of price increase is

low (Taltavull and et.al., 2011).

The economic determinants of the changes for the average house prices in UK

There are various changes in the average house prices in UK that are analysed in above

section. All these changes occurred between the period of 2009 to 2019 due to various reasons.

These reasons are the economic determinants of the change; some of these determinants are

identified and analysed below:

Economic growth – The first determinant due to which changes in the house prices of

United Kingdom has occurred is economic growth of United Kingdom. UK is a developed nation

where rate of economic growth is higher and the rate of unemployment is lower. In such country,

where economic growth is higher, the real income of people rises which enables people to spend

more on buying house. A house property for residential purposes is a basic need of every human

due to which demand of housing properties is always higher and in the nation where people are

actually capable of buying houses, the demand of housing properties is obviously higher than

other nations (Pawson and Wilcox, 2013). Due to this higher demand of houses in UK resulted

from their economic growth is the major determinant of change in housing prices of UK. The

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

period which is being considered is 2009 to 2019 and this period is the unfolding period from

financial crises due to which economic growth in this period is even higher. The change of

increasing house prices in UK is the result of UK’s economic growth.

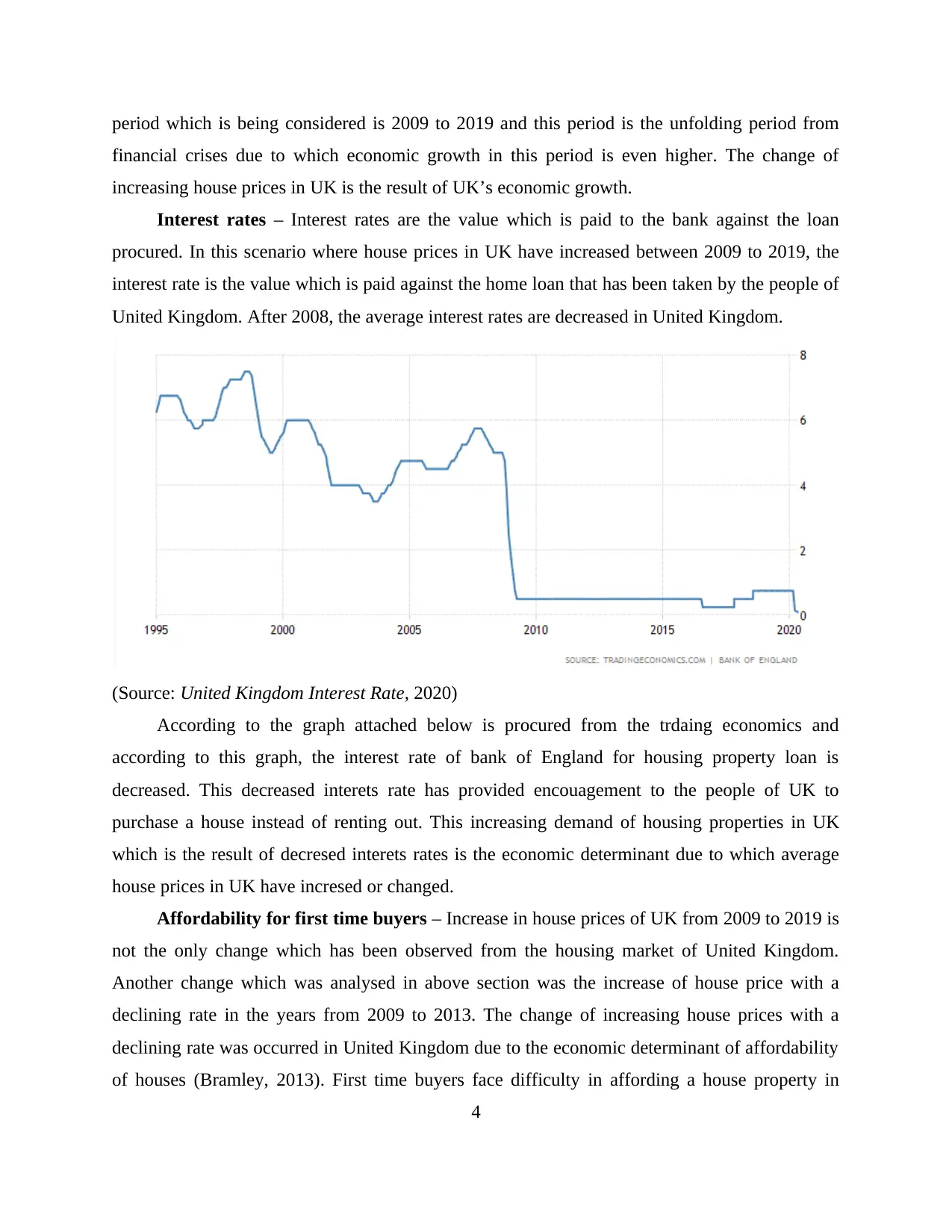

Interest rates – Interest rates are the value which is paid to the bank against the loan

procured. In this scenario where house prices in UK have increased between 2009 to 2019, the

interest rate is the value which is paid against the home loan that has been taken by the people of

United Kingdom. After 2008, the average interest rates are decreased in United Kingdom.

(Source: United Kingdom Interest Rate, 2020)

According to the graph attached below is procured from the trdaing economics and

according to this graph, the interest rate of bank of England for housing property loan is

decreased. This decreased interets rate has provided encouagement to the people of UK to

purchase a house instead of renting out. This increasing demand of housing properties in UK

which is the result of decresed interets rates is the economic determinant due to which average

house prices in UK have incresed or changed.

Affordability for first time buyers – Increase in house prices of UK from 2009 to 2019 is

not the only change which has been observed from the housing market of United Kingdom.

Another change which was analysed in above section was the increase of house price with a

declining rate in the years from 2009 to 2013. The change of increasing house prices with a

declining rate was occurred in United Kingdom due to the economic determinant of affordability

of houses (Bramley, 2013). First time buyers face difficulty in affording a house property in

4

financial crises due to which economic growth in this period is even higher. The change of

increasing house prices in UK is the result of UK’s economic growth.

Interest rates – Interest rates are the value which is paid to the bank against the loan

procured. In this scenario where house prices in UK have increased between 2009 to 2019, the

interest rate is the value which is paid against the home loan that has been taken by the people of

United Kingdom. After 2008, the average interest rates are decreased in United Kingdom.

(Source: United Kingdom Interest Rate, 2020)

According to the graph attached below is procured from the trdaing economics and

according to this graph, the interest rate of bank of England for housing property loan is

decreased. This decreased interets rate has provided encouagement to the people of UK to

purchase a house instead of renting out. This increasing demand of housing properties in UK

which is the result of decresed interets rates is the economic determinant due to which average

house prices in UK have incresed or changed.

Affordability for first time buyers – Increase in house prices of UK from 2009 to 2019 is

not the only change which has been observed from the housing market of United Kingdom.

Another change which was analysed in above section was the increase of house price with a

declining rate in the years from 2009 to 2013. The change of increasing house prices with a

declining rate was occurred in United Kingdom due to the economic determinant of affordability

of houses (Bramley, 2013). First time buyers face difficulty in affording a house property in

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

United Kingdom as in order to acquire mortgage, it is important to have a credibility so that bank

can ensure that the loaned amount will be repaid. Due to this lack of credibility, the affordability

of house for first time buyers is low.

Mortgage Finance – This is a facility which is given by bank to their client from which

clients can procure money from banks in order to purchase a house property in United Kingdom.

After the global financial crises in 2007, the government of UK had decreased the availability of

their mortgages for people. Competition in banking system lead towards eager to attract

customers with mortgage products but this competition finally results into credit crises. In order

to eliminate this situation of credit crises, the Bank of England has reduced the availability of

mortgage. This reduced availability had caused low demand of housing properties in 2009 to

2013 due to which in this period the prices of houses were increasing but with a declining rate

(Clapham and et.al., 2014).

Employment – This is the most important determinant which impacts the income level of

people, standard of living of people and the high prices of UK. United Kingdom is a developed

country where the rate of unemployment is low and in such nation the standard of living and

income level of people is high. The income of people of United Kingdom allows them to pursue

to buy a house which can match their standard of living. This scenario starts to shape up when

the income level of almost all the individual in UK is sound and everyone wants to buy a house.

This level of employment increases the demand of house properties in United Kingdom and with

respect to the law of demand, when the demand of a product increases, its price also increases.

So, it can be said that the high level of employment in UK is the result of high prices of houses in

UK.

House price bubbles – There are mainly two changes in the house prices of UK which are

analysed in above section. The first change is the increase in house prices from 2010 to 2019 and

second change was the price fluctuations in houses of United Kingdom in 2009 and 2010.

According to Taltavull, Poon and Garratt, (2012), the economy of UK has faced house price

crash twice in 20 years; the first one was between 1990 to 1992 and the second one was 2007 to

2010. The house price crash in 2009 and 2010 occurred due to house price volatility. When the

economy of UK came out of recession in 1992, the house prices began to raise immensely

recording highest house price in year 2000 but with increasing inflation and high considerable

5

can ensure that the loaned amount will be repaid. Due to this lack of credibility, the affordability

of house for first time buyers is low.

Mortgage Finance – This is a facility which is given by bank to their client from which

clients can procure money from banks in order to purchase a house property in United Kingdom.

After the global financial crises in 2007, the government of UK had decreased the availability of

their mortgages for people. Competition in banking system lead towards eager to attract

customers with mortgage products but this competition finally results into credit crises. In order

to eliminate this situation of credit crises, the Bank of England has reduced the availability of

mortgage. This reduced availability had caused low demand of housing properties in 2009 to

2013 due to which in this period the prices of houses were increasing but with a declining rate

(Clapham and et.al., 2014).

Employment – This is the most important determinant which impacts the income level of

people, standard of living of people and the high prices of UK. United Kingdom is a developed

country where the rate of unemployment is low and in such nation the standard of living and

income level of people is high. The income of people of United Kingdom allows them to pursue

to buy a house which can match their standard of living. This scenario starts to shape up when

the income level of almost all the individual in UK is sound and everyone wants to buy a house.

This level of employment increases the demand of house properties in United Kingdom and with

respect to the law of demand, when the demand of a product increases, its price also increases.

So, it can be said that the high level of employment in UK is the result of high prices of houses in

UK.

House price bubbles – There are mainly two changes in the house prices of UK which are

analysed in above section. The first change is the increase in house prices from 2010 to 2019 and

second change was the price fluctuations in houses of United Kingdom in 2009 and 2010.

According to Taltavull, Poon and Garratt, (2012), the economy of UK has faced house price

crash twice in 20 years; the first one was between 1990 to 1992 and the second one was 2007 to

2010. The house price crash in 2009 and 2010 occurred due to house price volatility. When the

economy of UK came out of recession in 1992, the house prices began to raise immensely

recording highest house price in year 2000 but with increasing inflation and high considerable

5

wealth effect, the house price inflation began to decrease in 2007 and in year 2009 and 2010,

these prices again observed a fall out.

Regional variations – Another change observed in the housing prices of UK was the

different price changes in every region of United Kingdom. This change occurred in UK due to

the economic determinant of regional variations. The highest average prices of UK are in

London and the South East. Regional differences are the variations caused by regional variations

in demand and supply. For example, the region of London has high population with full

employment, inward migration and relatively limited housing stock due to which the average

housing prices in this region are lower than the average housing prices in other regions of UK.

All the points which are identified above are the economic determinants which are the

reasons behind the change in the prices of housing market of United Kingdom.

The ways in which government action over the period 2009-2019 affected the UK Housing

market

The high demand and low supply of housing properties in United Kingdom is the one of

the major issues of this nation. This issue has been addressed by the government of UK many

times by implementing and executing different policies. Some of these policies or ways which

were implemented by UK’s government from 2009 to 2019 in order to affect their housing

market are identified and assessed below:

Intervention in determining the interest rate – Fixating an appropriate interest rate is the

part of monetary policy which is usually developed by central bank of the nation. In this case, the

Bank of England is responsible to develop a monetary policy and set an appropriate interest rate

range that can be used by other commercial banks of the nation. By considering the financial

crises in 2007, the government of UK intervene in 2010 to determine an interest rate which will

be used by all the banks (Mulliner and Maliene, 2013). This interest rate was lower than the

usual interest rate. This intervention or way of government of United Kingdom aimed to lower

cost of loan so that more people can be encouraged to acquire bank loans to buy housing

property and this action of government increased the demand and prices of housing properties in

UK.

Abolishment of stamp duty – The financial crises in United Kingdom has resulted into

slower market in this nation. This slower economy was a threat to the growth of UK; considering

6

these prices again observed a fall out.

Regional variations – Another change observed in the housing prices of UK was the

different price changes in every region of United Kingdom. This change occurred in UK due to

the economic determinant of regional variations. The highest average prices of UK are in

London and the South East. Regional differences are the variations caused by regional variations

in demand and supply. For example, the region of London has high population with full

employment, inward migration and relatively limited housing stock due to which the average

housing prices in this region are lower than the average housing prices in other regions of UK.

All the points which are identified above are the economic determinants which are the

reasons behind the change in the prices of housing market of United Kingdom.

The ways in which government action over the period 2009-2019 affected the UK Housing

market

The high demand and low supply of housing properties in United Kingdom is the one of

the major issues of this nation. This issue has been addressed by the government of UK many

times by implementing and executing different policies. Some of these policies or ways which

were implemented by UK’s government from 2009 to 2019 in order to affect their housing

market are identified and assessed below:

Intervention in determining the interest rate – Fixating an appropriate interest rate is the

part of monetary policy which is usually developed by central bank of the nation. In this case, the

Bank of England is responsible to develop a monetary policy and set an appropriate interest rate

range that can be used by other commercial banks of the nation. By considering the financial

crises in 2007, the government of UK intervene in 2010 to determine an interest rate which will

be used by all the banks (Mulliner and Maliene, 2013). This interest rate was lower than the

usual interest rate. This intervention or way of government of United Kingdom aimed to lower

cost of loan so that more people can be encouraged to acquire bank loans to buy housing

property and this action of government increased the demand and prices of housing properties in

UK.

Abolishment of stamp duty – The financial crises in United Kingdom has resulted into

slower market in this nation. This slower economy was a threat to the growth of UK; considering

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this threat the government of UK introduced several measures to stimulate the housing market of

UK so that the phase of slower market can be reduced and eliminated. For this, government

abolished the stamp duty for first time buyers in 2010 so that they could be encouraged to buy

houses. This policy of abolishing the stamp duty was an action which government took to affect

the UK housing market and increase the demand and prices of houses so that economy can be

boost.

Help to buy scheme – Housing market is only a market place but also an industry which

contributes highly in the growth and GDP of a nation. In year 2013, when government of UK

observes scope of growth in UK, the government initiated a scheme named help to buy scheme.

This scheme was introduced to offer potential buyers an equity loan of 20% of the property’s

value. This loan was offered as an interest free mortgage for the first five years. This scheme

increased the demand of houses in UK which finally resulted into high house prices by 2014 in

UK (Montagnoli and Nagayasu, 2015).

Local Housing Allowance – The government of UK does not only initiate policies which

can increase the demand and prices of houses in UK but also introduced few policies which has

reduced the affordability of buying a house in this region. The government of UK decided to rise

the age up to which single people can only claim the benefit of housing to cover the cost of

shared accommodation. This policy of UK’s government has reduced the encouragement of

people to buy their own individual house which has impacted the housing market of UK.

Predictions for impact of COVID-19 on UK Housing Market

COVID-19 is a virus which has resulted into a situation of pandemic for entire world. In

such situation, the scenario of almost every industry is same as the economy of every country is

continuously degrading. Considering the impact of COVID 19, the influence of it on UK housing

market in near future is analysed below:

In year 2018 and 2019, the political condition of United Kingdom was uncertain due to the

BREXIT but in 2020 when the consequences of BREXIT were begin to diminish, the housing

market of UK was again healing and the prices of houses in UK were started to be raised, UK

faced pandemic in March 2020. This pandemic occurred to COVID-19 that resulted into

Lockdown (Nygaard, 2011). In near future, even if the world found a vaccine against COVID-

19, the world would still face financial crises. This financial crisis will also impact the housing

7

UK so that the phase of slower market can be reduced and eliminated. For this, government

abolished the stamp duty for first time buyers in 2010 so that they could be encouraged to buy

houses. This policy of abolishing the stamp duty was an action which government took to affect

the UK housing market and increase the demand and prices of houses so that economy can be

boost.

Help to buy scheme – Housing market is only a market place but also an industry which

contributes highly in the growth and GDP of a nation. In year 2013, when government of UK

observes scope of growth in UK, the government initiated a scheme named help to buy scheme.

This scheme was introduced to offer potential buyers an equity loan of 20% of the property’s

value. This loan was offered as an interest free mortgage for the first five years. This scheme

increased the demand of houses in UK which finally resulted into high house prices by 2014 in

UK (Montagnoli and Nagayasu, 2015).

Local Housing Allowance – The government of UK does not only initiate policies which

can increase the demand and prices of houses in UK but also introduced few policies which has

reduced the affordability of buying a house in this region. The government of UK decided to rise

the age up to which single people can only claim the benefit of housing to cover the cost of

shared accommodation. This policy of UK’s government has reduced the encouragement of

people to buy their own individual house which has impacted the housing market of UK.

Predictions for impact of COVID-19 on UK Housing Market

COVID-19 is a virus which has resulted into a situation of pandemic for entire world. In

such situation, the scenario of almost every industry is same as the economy of every country is

continuously degrading. Considering the impact of COVID 19, the influence of it on UK housing

market in near future is analysed below:

In year 2018 and 2019, the political condition of United Kingdom was uncertain due to the

BREXIT but in 2020 when the consequences of BREXIT were begin to diminish, the housing

market of UK was again healing and the prices of houses in UK were started to be raised, UK

faced pandemic in March 2020. This pandemic occurred to COVID-19 that resulted into

Lockdown (Nygaard, 2011). In near future, even if the world found a vaccine against COVID-

19, the world would still face financial crises. This financial crisis will also impact the housing

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

market of UK. The households of UK will be cautious to invest highly in any activity and this

will decrease the demand in housing market of UK.

Another impact of COVID-19 on the housing market of UK is the affordability of houses.

An individual can be able to afford a house when they have employment. Due to pandemic

situation of COVID-19, UK has declared lockdown. Due to this lockdown, thousands of people

has lost their jobs and are unemployed. In this situation, when people do not have jobs, the

affordability of houses has been reduced. This impact of COVID-19 has predicted few more

impacts such as degrading of standard of living of people and less expenses as people will prefer

to save in order to fight against future pandemic situations.

Another impact of COVID-19 is the low availability and accessibility of houses in UK. The

COVID-19 has impacted many professions and industry and addition, this pandemic has resulted

in losses of many lives. This scenario has encouraged people to maintain social distancing; this

initiative of social distancing will be remain unchanged for a while. This will discourage people

from house viewings and interaction with real estate agents that will ultimately lead to low

availability and accessibility of houses in UK (Kemp, 2011).

The future house prices in United Kingdom are dependent on the variable that how long the

outbreak of COVID-19 will last. As the economy of UK has been impacted due to COVID-19 as

a whole. The financial institutions will provide loans at higher interest rates in order to ensure

high flow of money in economy. These high interest rate loans will discourage people from

buying a home in a situation when the pandemic as just finished. This will decrease the demand

of UK houses and there is also a possibility that the prices of UK houses can also reduce.

All the arguments which are presented above are only the predictions which are directed

towards the impact of COVID-19 on the housing market of United Kingdom.

CONCLUSION

From the above report, it has been concluded that housing market of United Kingdom is

only a market place for this country but also is an industry which contributes highly in the

growth of the economy of this country. The above report is the summarisation of housing market

of UK in the period of 2009 to 2019. From this summarisation it has been concluded that this

period of 10 years is divided into two phases, the first phase is the year 2009 and 2010 in which

8

will decrease the demand in housing market of UK.

Another impact of COVID-19 on the housing market of UK is the affordability of houses.

An individual can be able to afford a house when they have employment. Due to pandemic

situation of COVID-19, UK has declared lockdown. Due to this lockdown, thousands of people

has lost their jobs and are unemployed. In this situation, when people do not have jobs, the

affordability of houses has been reduced. This impact of COVID-19 has predicted few more

impacts such as degrading of standard of living of people and less expenses as people will prefer

to save in order to fight against future pandemic situations.

Another impact of COVID-19 is the low availability and accessibility of houses in UK. The

COVID-19 has impacted many professions and industry and addition, this pandemic has resulted

in losses of many lives. This scenario has encouraged people to maintain social distancing; this

initiative of social distancing will be remain unchanged for a while. This will discourage people

from house viewings and interaction with real estate agents that will ultimately lead to low

availability and accessibility of houses in UK (Kemp, 2011).

The future house prices in United Kingdom are dependent on the variable that how long the

outbreak of COVID-19 will last. As the economy of UK has been impacted due to COVID-19 as

a whole. The financial institutions will provide loans at higher interest rates in order to ensure

high flow of money in economy. These high interest rate loans will discourage people from

buying a home in a situation when the pandemic as just finished. This will decrease the demand

of UK houses and there is also a possibility that the prices of UK houses can also reduce.

All the arguments which are presented above are only the predictions which are directed

towards the impact of COVID-19 on the housing market of United Kingdom.

CONCLUSION

From the above report, it has been concluded that housing market of United Kingdom is

only a market place for this country but also is an industry which contributes highly in the

growth of the economy of this country. The above report is the summarisation of housing market

of UK in the period of 2009 to 2019. From this summarisation it has been concluded that this

period of 10 years is divided into two phases, the first phase is the year 2009 and 2010 in which

8

the housing market of UK was recovering from the financial crises and the second phase is from

2011 to 2019 in which housing market of UK was experiencing the high gains.

9

2011 to 2019 in which housing market of UK was experiencing the high gains.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.