UK Housing Market: Economic Determinants and Government Actions Report

VerifiedAdded on 2023/01/10

|13

|3921

|48

Report

AI Summary

This report provides a comprehensive analysis of the UK housing market between 2009 and 2019. It begins with an introduction to the contemporary business environment and the dynamic changes in the housing market. The report examines the fluctuations in average house prices over the decade, highlighting key trends and statistics. It then delves into the economic determinants influencing these changes, including economic growth, mortgage availability, interest rates, income levels, and consumer confidence. Furthermore, the report assesses the impact of government actions and policies on the UK housing market during this period. Finally, it offers predictions regarding the potential impact of COVID-19 on the future of the UK housing market, concluding with a summary of the key findings and a list of references.

Report

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

How have average house prices in the UK changed over the period from 2009 - 2019?...........3

TASK 2............................................................................................................................................6

What are the economic determinants of the changes outlined in your answer to Question 1?. . .6

TASK 3............................................................................................................................................8

How has government action over the period 2009-2019 affected the UK Housing market?......8

TASK 4............................................................................................................................................9

Predict what would be the impact of COVID-19 on UK Housing Market?................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

2

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

How have average house prices in the UK changed over the period from 2009 - 2019?...........3

TASK 2............................................................................................................................................6

What are the economic determinants of the changes outlined in your answer to Question 1?. . .6

TASK 3............................................................................................................................................8

How has government action over the period 2009-2019 affected the UK Housing market?......8

TASK 4............................................................................................................................................9

Predict what would be the impact of COVID-19 on UK Housing Market?................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

2

INTRODUCTION

Contemporary business environment are enhancing competitively as well as dynamically.

The main reason behind this fact is that it is changing at fast pace and also there are modification

into new concepts. It means that firms have to understand the requirements and development and

perform their business accordingly (Antonakakis and Floros, 2016). The main objective of this

report is to evaluate the UK housing market over last ten years. This report is based on UK

housing market which includes supply of housing, demand of housing, prices of house, rented

sector and intervention of government into housing market. This report covers the average house

price that changes over the period, economic determinants respective changes and government

action over that period. Along with this, prediction related to COVID-19 impact upon housing

market is also discussed in this report.

MAIN BODY

TASK 1

How have average house prices in the UK changed over the period from 2009 - 2019?

Housing market is considered as the demand and supply for houses mainly into specific

country. Its key elements are average house prices as well as trend in house prices. Moreover, it

includes some features such as demand for housing, supply of housing, prices of houses,

government intervention, rented sector and others (Arundel, 2017). Along with this, UK housing

market has few features like it is volatile due to several factors, has influences upon wider

economy such as when prices of houses are declining, customers spending trends are also

reducing. As it influences the economy and individuals’ homeowners so it is essential for them

to predict the future movements.

3

Contemporary business environment are enhancing competitively as well as dynamically.

The main reason behind this fact is that it is changing at fast pace and also there are modification

into new concepts. It means that firms have to understand the requirements and development and

perform their business accordingly (Antonakakis and Floros, 2016). The main objective of this

report is to evaluate the UK housing market over last ten years. This report is based on UK

housing market which includes supply of housing, demand of housing, prices of house, rented

sector and intervention of government into housing market. This report covers the average house

price that changes over the period, economic determinants respective changes and government

action over that period. Along with this, prediction related to COVID-19 impact upon housing

market is also discussed in this report.

MAIN BODY

TASK 1

How have average house prices in the UK changed over the period from 2009 - 2019?

Housing market is considered as the demand and supply for houses mainly into specific

country. Its key elements are average house prices as well as trend in house prices. Moreover, it

includes some features such as demand for housing, supply of housing, prices of houses,

government intervention, rented sector and others (Arundel, 2017). Along with this, UK housing

market has few features like it is volatile due to several factors, has influences upon wider

economy such as when prices of houses are declining, customers spending trends are also

reducing. As it influences the economy and individuals’ homeowners so it is essential for them

to predict the future movements.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

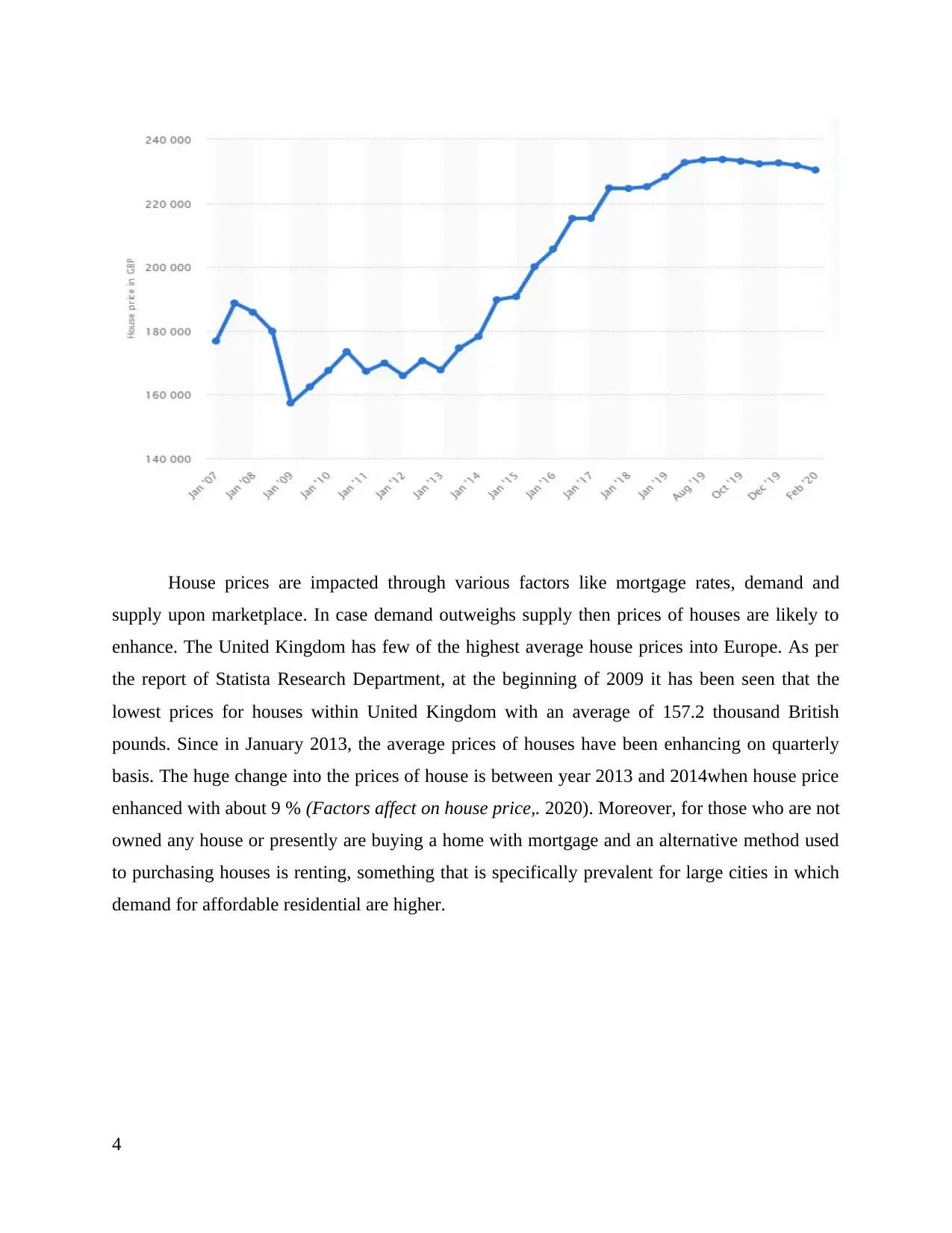

House prices are impacted through various factors like mortgage rates, demand and

supply upon marketplace. In case demand outweighs supply then prices of houses are likely to

enhance. The United Kingdom has few of the highest average house prices into Europe. As per

the report of Statista Research Department, at the beginning of 2009 it has been seen that the

lowest prices for houses within United Kingdom with an average of 157.2 thousand British

pounds. Since in January 2013, the average prices of houses have been enhancing on quarterly

basis. The huge change into the prices of house is between year 2013 and 2014when house price

enhanced with about 9 % (Factors affect on house price,. 2020). Moreover, for those who are not

owned any house or presently are buying a home with mortgage and an alternative method used

to purchasing houses is renting, something that is specifically prevalent for large cities in which

demand for affordable residential are higher.

4

supply upon marketplace. In case demand outweighs supply then prices of houses are likely to

enhance. The United Kingdom has few of the highest average house prices into Europe. As per

the report of Statista Research Department, at the beginning of 2009 it has been seen that the

lowest prices for houses within United Kingdom with an average of 157.2 thousand British

pounds. Since in January 2013, the average prices of houses have been enhancing on quarterly

basis. The huge change into the prices of house is between year 2013 and 2014when house price

enhanced with about 9 % (Factors affect on house price,. 2020). Moreover, for those who are not

owned any house or presently are buying a home with mortgage and an alternative method used

to purchasing houses is renting, something that is specifically prevalent for large cities in which

demand for affordable residential are higher.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

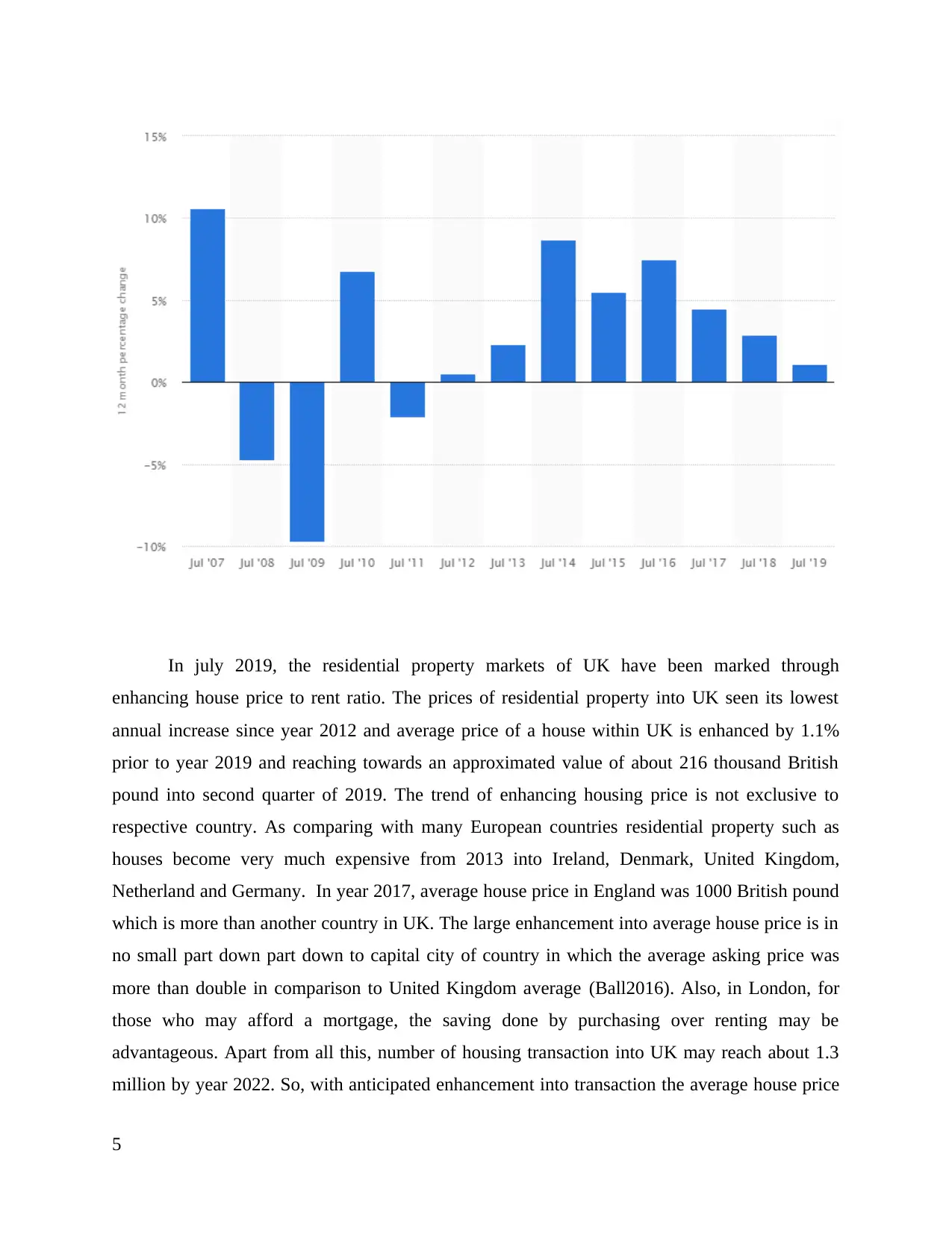

In july 2019, the residential property markets of UK have been marked through

enhancing house price to rent ratio. The prices of residential property into UK seen its lowest

annual increase since year 2012 and average price of a house within UK is enhanced by 1.1%

prior to year 2019 and reaching towards an approximated value of about 216 thousand British

pound into second quarter of 2019. The trend of enhancing housing price is not exclusive to

respective country. As comparing with many European countries residential property such as

houses become very much expensive from 2013 into Ireland, Denmark, United Kingdom,

Netherland and Germany. In year 2017, average house price in England was 1000 British pound

which is more than another country in UK. The large enhancement into average house price is in

no small part down part down to capital city of country in which the average asking price was

more than double in comparison to United Kingdom average (Ball2016). Also, in London, for

those who may afford a mortgage, the saving done by purchasing over renting may be

advantageous. Apart from all this, number of housing transaction into UK may reach about 1.3

million by year 2022. So, with anticipated enhancement into transaction the average house price

5

enhancing house price to rent ratio. The prices of residential property into UK seen its lowest

annual increase since year 2012 and average price of a house within UK is enhanced by 1.1%

prior to year 2019 and reaching towards an approximated value of about 216 thousand British

pound into second quarter of 2019. The trend of enhancing housing price is not exclusive to

respective country. As comparing with many European countries residential property such as

houses become very much expensive from 2013 into Ireland, Denmark, United Kingdom,

Netherland and Germany. In year 2017, average house price in England was 1000 British pound

which is more than another country in UK. The large enhancement into average house price is in

no small part down part down to capital city of country in which the average asking price was

more than double in comparison to United Kingdom average (Ball2016). Also, in London, for

those who may afford a mortgage, the saving done by purchasing over renting may be

advantageous. Apart from all this, number of housing transaction into UK may reach about 1.3

million by year 2022. So, with anticipated enhancement into transaction the average house price

5

may develop in all over UK. Thus, the average house price is changed due to various factors

such as unemployment, economic growth, interest rates and availability of mortgage (Statics

2009 to 2019 house price. 2020). So, the shortage of supply means that the requirement for

housing and therefore, competitive market will push up house prices where as an excess of

housing means that prices reduces to stimulate buyers.

TASK 2

What are the economic determinants of the changes outlined in your answer to Question 1?

As there are various things which influences the prices of house like supply and market

demand, mortgage and so on. In case demand is more than supply then it is obvious that

residence cost will go on. The United Kingdom boasts few of presently the higher average value

of home. There are various alternatives for it, including essential purchase requisition- if owner

of the home allows its premises to be vacant for six months. These premises will give

permission at market segment rentals to person upon accommodations. The values of houses are

determined through market (Best and Kleven, 2018). In case demand increase or production

initiates falling the prices of home will be in balance. Therefore, in year 2000, the house value

develops too higher but drop in year 2008. The main reason behind this is changing house prices.

The long term raise into the prices of property is exacerbated through property cost which

outstrips the production. These have been estimated that above 175,000 homes as well as

apartments per year should be developed for accomplishing longer term property price threshold.

As it is observed earlier that new developments are included in just about 5% of house buying.

There are some economic determinants that play essential role into the changes of average house

prices and housing demand which are discussed below:

Economic growth: Demand of housing is contingent upon income. Effective

development of economies and enhancing wages will permit firms to purchase more houses; it

will rise inflation as well as raise the price (Cook and Watson, 2016). In real, house price

inflation is considered as stretchy earnings; economic growth drives towards a larger household

income percentage are invested. Similarly, reducing wages into downward would means that the

individuals who are not capable to afford it. While those who keep its insurance may fell back

upon living expenditure as well as eventually wind up being burglarised of its homes.

6

such as unemployment, economic growth, interest rates and availability of mortgage (Statics

2009 to 2019 house price. 2020). So, the shortage of supply means that the requirement for

housing and therefore, competitive market will push up house prices where as an excess of

housing means that prices reduces to stimulate buyers.

TASK 2

What are the economic determinants of the changes outlined in your answer to Question 1?

As there are various things which influences the prices of house like supply and market

demand, mortgage and so on. In case demand is more than supply then it is obvious that

residence cost will go on. The United Kingdom boasts few of presently the higher average value

of home. There are various alternatives for it, including essential purchase requisition- if owner

of the home allows its premises to be vacant for six months. These premises will give

permission at market segment rentals to person upon accommodations. The values of houses are

determined through market (Best and Kleven, 2018). In case demand increase or production

initiates falling the prices of home will be in balance. Therefore, in year 2000, the house value

develops too higher but drop in year 2008. The main reason behind this is changing house prices.

The long term raise into the prices of property is exacerbated through property cost which

outstrips the production. These have been estimated that above 175,000 homes as well as

apartments per year should be developed for accomplishing longer term property price threshold.

As it is observed earlier that new developments are included in just about 5% of house buying.

There are some economic determinants that play essential role into the changes of average house

prices and housing demand which are discussed below:

Economic growth: Demand of housing is contingent upon income. Effective

development of economies and enhancing wages will permit firms to purchase more houses; it

will rise inflation as well as raise the price (Cook and Watson, 2016). In real, house price

inflation is considered as stretchy earnings; economic growth drives towards a larger household

income percentage are invested. Similarly, reducing wages into downward would means that the

individuals who are not capable to afford it. While those who keep its insurance may fell back

upon living expenditure as well as eventually wind up being burglarised of its homes.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Mortgage availability: The year between 1996 to 2006 is considered as to be the boom

periods; various financial institutions had interest in lending mortgage loans. It allows

individuals to] spend huge amounts of incomes. Financial institutions also authorized much

minimised reserved (Such as 100% housing loan). This simple application for mortgage implied

that house price is increased as more people can buy now. Thereafter year 2007, due to financial

crisis the banks and another financial institution has strained to obtain funds for borrowing

capital from markets. It also however stiffened its capital needs that require a highest payment

for building a property. It has reduced accessibility of student loan as well as reduces a price.

Interest rate deduction: No estimation of changing affects into home values which is

impacted through reduction of lending amounts between year 1991 and 2016. The approximated

relation into report NHPAU’S 'Affordability Issues'1 (2007) and 'Affordability Still Issues'2

(2008) depends upon raw data which covered the time period up to 2007. Therefore, the rate of

interests has enhanced consequently and developments into the business of mortgage have also

taken place along with the mortgages legislation and relationship among interest rates and

mortgages. These alterations are of level that shows, this model approximated for preceding

cycle which would not be utilised for month since year 2007.

Income: This was the time for enhancing at year 2007 pleading. The economy was

initiated to experiences a boom into economic theory. Most of the people begin to invest its

excess income upon rent; even first develop a property or move towards a better one (Khazragui

and Hudson, 2015). Various folks pursued that its earnings will also started developing as well as

are ready to spread monetarily into nearer term through having an costly house, ensured its

monthly income repayment will become very much cost effective. By comparing it has been

seen that there are downturn cycle in year 2008 or 2009, with enhancing unemployment and

thereafter whether reducing or wages rise accordingly. People were very much fortunate that

they have opportunity pay large volumes.

Interest rate: The mortgages repayment amount is influenced through interest rates. A

collection of sustained interest rates will considerably enhance costs of monthly mortgage as

well as leads towards low availability for room purchase (Knowles and Ferbrache, 2016). High

interest rates then rent is more appealing than purchase. In case borrowers have regular aggregate

loans, interest rates obtain large influences. For this, the stronger interest into 1990 to 1992 is

7

periods; various financial institutions had interest in lending mortgage loans. It allows

individuals to] spend huge amounts of incomes. Financial institutions also authorized much

minimised reserved (Such as 100% housing loan). This simple application for mortgage implied

that house price is increased as more people can buy now. Thereafter year 2007, due to financial

crisis the banks and another financial institution has strained to obtain funds for borrowing

capital from markets. It also however stiffened its capital needs that require a highest payment

for building a property. It has reduced accessibility of student loan as well as reduces a price.

Interest rate deduction: No estimation of changing affects into home values which is

impacted through reduction of lending amounts between year 1991 and 2016. The approximated

relation into report NHPAU’S 'Affordability Issues'1 (2007) and 'Affordability Still Issues'2

(2008) depends upon raw data which covered the time period up to 2007. Therefore, the rate of

interests has enhanced consequently and developments into the business of mortgage have also

taken place along with the mortgages legislation and relationship among interest rates and

mortgages. These alterations are of level that shows, this model approximated for preceding

cycle which would not be utilised for month since year 2007.

Income: This was the time for enhancing at year 2007 pleading. The economy was

initiated to experiences a boom into economic theory. Most of the people begin to invest its

excess income upon rent; even first develop a property or move towards a better one (Khazragui

and Hudson, 2015). Various folks pursued that its earnings will also started developing as well as

are ready to spread monetarily into nearer term through having an costly house, ensured its

monthly income repayment will become very much cost effective. By comparing it has been

seen that there are downturn cycle in year 2008 or 2009, with enhancing unemployment and

thereafter whether reducing or wages rise accordingly. People were very much fortunate that

they have opportunity pay large volumes.

Interest rate: The mortgages repayment amount is influenced through interest rates. A

collection of sustained interest rates will considerably enhance costs of monthly mortgage as

well as leads towards low availability for room purchase (Knowles and Ferbrache, 2016). High

interest rates then rent is more appealing than purchase. In case borrowers have regular aggregate

loans, interest rates obtain large influences. For this, the stronger interest into 1990 to 1992 is

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

triggered a very drop into property price of UK. As various purchasers are not able to buy house

at raise interest rate.

Customer confidence: Trust is considered as an essential term during declining as if

people will like to undertake chances out a personal loan. Mainly, conception more towards real

state market are important; consumer will postpone purchasing if it will think about house prices

will fall.

Supply: Shortages of delivery enhance the costs. More production will drop down the

costs. For this, a estimated 700, 000 new houses are developed fall in Irish real estate which

boom from year 1996 to 2006. At the time, when real estate market gets crashed, an vital

overproduction remained to marketplace. Prices of property were 15% as well as cost reduced

with production more than required.

Unemployment: It is somehow correlated with economic. Instead of unemployment, less

number of individuals mat afford a house (Lichfield, Kettle and Whitbread, 2016). Nevertheless,

then again insecurity threats can discourage people from joining the housing market.

TASK 3

How has government action over the period 2009-2019 affected the UK Housing market?

The most effectual way the government of nation may ease a pressure upon

accommodation cost on low income families is through facilitating them some kind o incentives.

Regulation which grows wages like accumulated additional tax, decent wages and others.

Housing cost of British has initiated from year 2002 to its yearly fall into year 2009. Value f

property in London, according to British newspaper, it have been viewed the worst costs lower

5.3%. Also, the properties of London values are considered to be one of the most common

discussion topics. It is hugely because of the fact that prices of houses has almost doubled since

before mid – 1990s. The respective country government is focused that insufficient residences

has been developed for satisfying the requirements of enhancing society. It concentrates upon to

enhance reconfigured as well as latest vacant apartments (Montagnoli and Nagayasu, 2015). A

sum of 118,190 new residences was constructed in England in year 2012. Also, there is a rise of

9% over last year but 31% reduces over 170,610 in year 2008. During past 5 years, only 610, 000

housing units has been developed in comparison last five year is about 800,000 and also a

reduction of 23%. This constraint upon new accommodation availability have assured that prices

8

at raise interest rate.

Customer confidence: Trust is considered as an essential term during declining as if

people will like to undertake chances out a personal loan. Mainly, conception more towards real

state market are important; consumer will postpone purchasing if it will think about house prices

will fall.

Supply: Shortages of delivery enhance the costs. More production will drop down the

costs. For this, a estimated 700, 000 new houses are developed fall in Irish real estate which

boom from year 1996 to 2006. At the time, when real estate market gets crashed, an vital

overproduction remained to marketplace. Prices of property were 15% as well as cost reduced

with production more than required.

Unemployment: It is somehow correlated with economic. Instead of unemployment, less

number of individuals mat afford a house (Lichfield, Kettle and Whitbread, 2016). Nevertheless,

then again insecurity threats can discourage people from joining the housing market.

TASK 3

How has government action over the period 2009-2019 affected the UK Housing market?

The most effectual way the government of nation may ease a pressure upon

accommodation cost on low income families is through facilitating them some kind o incentives.

Regulation which grows wages like accumulated additional tax, decent wages and others.

Housing cost of British has initiated from year 2002 to its yearly fall into year 2009. Value f

property in London, according to British newspaper, it have been viewed the worst costs lower

5.3%. Also, the properties of London values are considered to be one of the most common

discussion topics. It is hugely because of the fact that prices of houses has almost doubled since

before mid – 1990s. The respective country government is focused that insufficient residences

has been developed for satisfying the requirements of enhancing society. It concentrates upon to

enhance reconfigured as well as latest vacant apartments (Montagnoli and Nagayasu, 2015). A

sum of 118,190 new residences was constructed in England in year 2012. Also, there is a rise of

9% over last year but 31% reduces over 170,610 in year 2008. During past 5 years, only 610, 000

housing units has been developed in comparison last five year is about 800,000 and also a

reduction of 23%. This constraint upon new accommodation availability have assured that prices

8

of house has still remained fair throughout past three years rather than complexity in obtaining

finances from investors. In about 15% of population is into rental market as well as this number

is anticipated is doubled during upcoming ten years. The affordable housing permeability of UK

is lower especially in Europe. The legislation of government is focused upon increasing supply

elastic properties so constructions of house are very much sensitive towards the requirements of

changing marketplace (Nuuter, Tupenaite, 2015). Several actions which are undertaken through

government of United Kingdom in respect of housing market from year 2009 to 2019 are

discussed below:

Develop more social housing: Enabling wider independence for local government to

enhance earnings for funding the procurement as well as development of housing benefits. So, it

can assists counteract the fall for last 10 to 20 years into committee facilities development.

Moreover, an option also maximise funds for approx 1400 housing committee which are

necessary for maintaining and developing about 3 millions houses into United Kingdom.

Minimising the number of empty house: There are various alternatives for it, including

essential purchase requisition- if owner of the home allows its premises to be vacant for six

months. These premises will given permission at market segment rentals to person upon

accommodations.

Stamp Duty: Presently, the government explored stamp duty upto 3% for features above

£250,000 residences from £ 60,000-£ 250,000 and pay about 1% for characteristics. So, the

enhancing trends into inheritance tax were concentrated upon minimising needs for feature above

£250,000 especially into real estate location such as London.

TASK 4

Predict what would be the impact of COVID-19 on UK Housing Market?

The corona virus has delayed the existent labour real estate market. At the time when

government were restricted towards advertisement of houses as well as also prohibited the

mortgage brokers from selling new property as part of huge affords to curb disease outbreak

impact. Towards the reaction for this outbreak, the ban k of England minimised rates of interests

before March between 0.75 to 0.25 %/ this then reported a another uncertain cut later at that

night borrowing cost will bring towards lowest ever rate of 0.1. While people of British also keep

moving into home purchasing centre, real estate borrowing was delayed as well as mortgage

9

finances from investors. In about 15% of population is into rental market as well as this number

is anticipated is doubled during upcoming ten years. The affordable housing permeability of UK

is lower especially in Europe. The legislation of government is focused upon increasing supply

elastic properties so constructions of house are very much sensitive towards the requirements of

changing marketplace (Nuuter, Tupenaite, 2015). Several actions which are undertaken through

government of United Kingdom in respect of housing market from year 2009 to 2019 are

discussed below:

Develop more social housing: Enabling wider independence for local government to

enhance earnings for funding the procurement as well as development of housing benefits. So, it

can assists counteract the fall for last 10 to 20 years into committee facilities development.

Moreover, an option also maximise funds for approx 1400 housing committee which are

necessary for maintaining and developing about 3 millions houses into United Kingdom.

Minimising the number of empty house: There are various alternatives for it, including

essential purchase requisition- if owner of the home allows its premises to be vacant for six

months. These premises will given permission at market segment rentals to person upon

accommodations.

Stamp Duty: Presently, the government explored stamp duty upto 3% for features above

£250,000 residences from £ 60,000-£ 250,000 and pay about 1% for characteristics. So, the

enhancing trends into inheritance tax were concentrated upon minimising needs for feature above

£250,000 especially into real estate location such as London.

TASK 4

Predict what would be the impact of COVID-19 on UK Housing Market?

The corona virus has delayed the existent labour real estate market. At the time when

government were restricted towards advertisement of houses as well as also prohibited the

mortgage brokers from selling new property as part of huge affords to curb disease outbreak

impact. Towards the reaction for this outbreak, the ban k of England minimised rates of interests

before March between 0.75 to 0.25 %/ this then reported a another uncertain cut later at that

night borrowing cost will bring towards lowest ever rate of 0.1. While people of British also keep

moving into home purchasing centre, real estate borrowing was delayed as well as mortgage

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

brokers department get closed permanently as portion of wider ranging started reducing COVID-

19 disease. Value of property as well as interaction has collected that from beginning of year

2020, managed to assists through reduced Brexit as well as political stability but this concept

have undertaken in backwards term.

Moreover, the corona virus crisis has had an unprecedented impact upon UK housing

market. As UK house price initiated to recover from uncertainty that is caused through Brexit at

the end of year 2019. And the Boris bounce from Tories election victory in December set the

market up for stronger start in year 2020. But the lockdown in UK due to corona virus means

that the purchaser cannot visit houses. The housing market effectually stopped during lockdown

and also not nay person are allowed to viewing of properties as this would has breached the rules

of lockdown. So, it is predicted that the UK house prices may dropped at faster rate. Also, the

centre of Economic and Business research has predicted that house price will fall by 13% at the

end of year due to pandemic. Moreover, the impact will vary across region based upon how

badly the country’s personnel were hit (Surminski, 2018). It has been also anticipated that in

Northern Ireland, Humber and Yorkshire will fall in harder manner. Also, into these areas the

main industries of retail, manufacturing and other have been affected badly. Although the

respective country’s government has provided a huge package for supporting them. This lack of

demand will mean few ceases of business to operate various employees will lose its job as well

as also a cut into their incomes. As housing is considered as the single biggest expenses item for

various households that means shortfall into incomes which has incredible potential to interrupt

United Kingdom housing markets. In February 2020, it has been seen that there is annual

increase into house prices of about 2.8%. However, it has been predicted that COVID-19 can

poses a potential road bump. The housing market of UK began in the month of March with

likewise trends to last months as key market indicators viewed a sustained level of buyer as well

as seller activity. So, the average house prices in respective month get changed from February’s

record it is higher where as annual growth nudged up to 3%. Also, during lockdown due to

COVID-19, house price of UK reduced as analyst tell that the property market was not

performing well due to constraints. Right move’s information viewed that average house selling

price fell up to 0.2% to £311,950. Also, the UK house prices have been raised by 2.1 % in April

last year. Analysis have viewed that present vendors has remained predominantly upon industry

10

19 disease. Value of property as well as interaction has collected that from beginning of year

2020, managed to assists through reduced Brexit as well as political stability but this concept

have undertaken in backwards term.

Moreover, the corona virus crisis has had an unprecedented impact upon UK housing

market. As UK house price initiated to recover from uncertainty that is caused through Brexit at

the end of year 2019. And the Boris bounce from Tories election victory in December set the

market up for stronger start in year 2020. But the lockdown in UK due to corona virus means

that the purchaser cannot visit houses. The housing market effectually stopped during lockdown

and also not nay person are allowed to viewing of properties as this would has breached the rules

of lockdown. So, it is predicted that the UK house prices may dropped at faster rate. Also, the

centre of Economic and Business research has predicted that house price will fall by 13% at the

end of year due to pandemic. Moreover, the impact will vary across region based upon how

badly the country’s personnel were hit (Surminski, 2018). It has been also anticipated that in

Northern Ireland, Humber and Yorkshire will fall in harder manner. Also, into these areas the

main industries of retail, manufacturing and other have been affected badly. Although the

respective country’s government has provided a huge package for supporting them. This lack of

demand will mean few ceases of business to operate various employees will lose its job as well

as also a cut into their incomes. As housing is considered as the single biggest expenses item for

various households that means shortfall into incomes which has incredible potential to interrupt

United Kingdom housing markets. In February 2020, it has been seen that there is annual

increase into house prices of about 2.8%. However, it has been predicted that COVID-19 can

poses a potential road bump. The housing market of UK began in the month of March with

likewise trends to last months as key market indicators viewed a sustained level of buyer as well

as seller activity. So, the average house prices in respective month get changed from February’s

record it is higher where as annual growth nudged up to 3%. Also, during lockdown due to

COVID-19, house price of UK reduced as analyst tell that the property market was not

performing well due to constraints. Right move’s information viewed that average house selling

price fell up to 0.2% to £311,950. Also, the UK house prices have been raised by 2.1 % in April

last year. Analysis have viewed that present vendors has remained predominantly upon industry

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

with whole stock available for selling down 2.6% as on 23 rd march lockdown was implemented

(Corona virus impact on house prices, 2020)

People do not has a working economy when customers are not able to buy as well as

vendors are not capable to sale and thus, focused should be upon what is essential to stabilise the

economy during lockdown. Also, few owners of houses can be worried regarding the risk of

brief term drops into the values of homes another considered the long term view as well as stay

on their promises to move forward (Wu, 2015). It is managed for helping others through lending

institutions moving to an expand the lifespan of current loans offers by 3 months and through

proposed regulation upon adoptable project cost. Therefore, whole analysis is shows that

COVID-19 has pessimistic impact upon the housing market of United Kingdom.

CONCLUSION

As per the above report, it has been concluded that as business environment are changing in

dynamic and competitive way so firm have to understand the requirements and development and

perform their business accordingly. Moreover, the , UK housing market has few features like it is

volatile due to several factors, has influences upon wider economy such as when prices of houses

are declining, customers spending trends are also reducing. Also, it’s get changes over periods.

Along with this, some economic determinants such as economic growth, mortgage availability,

income, interest rate deduction and so on that play essential role into the changes of average

house prices and housing demand. Also, some government action has also impacted the housing

market of UK like develop more social housing, minimising the number of empty house, stamp

duty and others. Apart from all these, it has been predicted that that COVID-19 has pessimistic

impact upon the housing market of United Kingdom.

11

(Corona virus impact on house prices, 2020)

People do not has a working economy when customers are not able to buy as well as

vendors are not capable to sale and thus, focused should be upon what is essential to stabilise the

economy during lockdown. Also, few owners of houses can be worried regarding the risk of

brief term drops into the values of homes another considered the long term view as well as stay

on their promises to move forward (Wu, 2015). It is managed for helping others through lending

institutions moving to an expand the lifespan of current loans offers by 3 months and through

proposed regulation upon adoptable project cost. Therefore, whole analysis is shows that

COVID-19 has pessimistic impact upon the housing market of United Kingdom.

CONCLUSION

As per the above report, it has been concluded that as business environment are changing in

dynamic and competitive way so firm have to understand the requirements and development and

perform their business accordingly. Moreover, the , UK housing market has few features like it is

volatile due to several factors, has influences upon wider economy such as when prices of houses

are declining, customers spending trends are also reducing. Also, it’s get changes over periods.

Along with this, some economic determinants such as economic growth, mortgage availability,

income, interest rate deduction and so on that play essential role into the changes of average

house prices and housing demand. Also, some government action has also impacted the housing

market of UK like develop more social housing, minimising the number of empty house, stamp

duty and others. Apart from all these, it has been predicted that that COVID-19 has pessimistic

impact upon the housing market of United Kingdom.

11

REFERENCES

Books and Journals

Antonakakis, N. and Floros, C., 2016. Dynamic interdependencies among the housing market,

stock market, policy uncertainty and the macroeconomy in the United

Kingdom. International Review of Financial Analysis. 44. pp.111-122.

Arundel, R., 2017. Equity inequity: Housing wealth inequality, inter and intra-generational

divergences, and the rise of private landlordism. Housing, Theory and Society. 34(2).

pp.176-200.

Ball, M., 2016. Housing provision in 21st century Europe. Habitat International. 54. pp.182-188.

Best, M. C. and Kleven, H. J., 2018. Housing market responses to transaction taxes: Evidence

from notches and stimulus in the UK. The Review of Economic Studies. 85(1). pp.157-

193.

Cook, S. and Watson, D., 2016. A new perspective on the ripple effect in the UK housing

market: Comovement, cyclical subsamples and alternative indices. Urban

Studies. 53(14). pp.3048-3062.

Khazragui, H. and Hudson, J., 2015. Measuring the benefits of university research: impact and

the REF in the UK. Research Evaluation. 24(1). pp.51-62.

Knowles, R. D. and Ferbrache, F., 2016. Evaluation of wider economic impacts of light rail

investment on cities. Journal of Transport Geography. 54. pp.430-439.

Lichfield, N., Kettle, P. and Whitbread, M., 2016. Evaluation in the Planning Process: The Urban

and Regional Planning Series (Vol. 10). Elsevier.

Montagnoli, A. and Nagayasu, J., 2015. UK house price convergence clubs and

spillovers. Journal of Housing Economics. 30. pp.50-58.

Nuuter, T., Lill, I. and Tupenaite, L., 2015. Comparison of housing market sustainability in

European countries based on multiple criteria assessment. Land Use Policy. 42. pp.642-

651.

Surminski, S., 2018. Fit for purpose and fit for the future? An evaluation of the UK's new flood

reinsurance pool. Risk Management and Insurance Review. 21(1). pp.33-72.

Wu, F., 2015. Commodification and housing market cycles in Chinese cities. International

Journal of Housing Policy. 15(1). pp.6-26.

12

Books and Journals

Antonakakis, N. and Floros, C., 2016. Dynamic interdependencies among the housing market,

stock market, policy uncertainty and the macroeconomy in the United

Kingdom. International Review of Financial Analysis. 44. pp.111-122.

Arundel, R., 2017. Equity inequity: Housing wealth inequality, inter and intra-generational

divergences, and the rise of private landlordism. Housing, Theory and Society. 34(2).

pp.176-200.

Ball, M., 2016. Housing provision in 21st century Europe. Habitat International. 54. pp.182-188.

Best, M. C. and Kleven, H. J., 2018. Housing market responses to transaction taxes: Evidence

from notches and stimulus in the UK. The Review of Economic Studies. 85(1). pp.157-

193.

Cook, S. and Watson, D., 2016. A new perspective on the ripple effect in the UK housing

market: Comovement, cyclical subsamples and alternative indices. Urban

Studies. 53(14). pp.3048-3062.

Khazragui, H. and Hudson, J., 2015. Measuring the benefits of university research: impact and

the REF in the UK. Research Evaluation. 24(1). pp.51-62.

Knowles, R. D. and Ferbrache, F., 2016. Evaluation of wider economic impacts of light rail

investment on cities. Journal of Transport Geography. 54. pp.430-439.

Lichfield, N., Kettle, P. and Whitbread, M., 2016. Evaluation in the Planning Process: The Urban

and Regional Planning Series (Vol. 10). Elsevier.

Montagnoli, A. and Nagayasu, J., 2015. UK house price convergence clubs and

spillovers. Journal of Housing Economics. 30. pp.50-58.

Nuuter, T., Lill, I. and Tupenaite, L., 2015. Comparison of housing market sustainability in

European countries based on multiple criteria assessment. Land Use Policy. 42. pp.642-

651.

Surminski, S., 2018. Fit for purpose and fit for the future? An evaluation of the UK's new flood

reinsurance pool. Risk Management and Insurance Review. 21(1). pp.33-72.

Wu, F., 2015. Commodification and housing market cycles in Chinese cities. International

Journal of Housing Policy. 15(1). pp.6-26.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.