Impact of Economic Factors on UK Housing Market (2009-2019) Project

VerifiedAdded on 2023/01/09

|11

|3769

|91

Report

AI Summary

This report provides a comprehensive analysis of the UK housing market from 2009 to 2019. It begins by examining the fluctuations in average house prices across the UK, highlighting regional variations and trends. The report then delves into the economic determinants influencing these price changes, including economic growth, unemployment, interest rates, consumer confidence, mortgage availability, and the supply of housing. Furthermore, it explores the impact of government actions, such as the "Help to Buy" scheme and housing-related taxes, on the housing market. Finally, the report assesses the potential impact of the COVID-19 pandemic on the UK housing market. The analysis covers various factors, including the economic climate, demographics, and investor behavior. The report draws from data from various sources, including HM Land Registry and the Office for National Statistics, to provide a detailed overview of the UK housing market dynamics.

Project 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

1. Average house prices in the UK changed over the period from 2009 – 2019...................3

2 Various economic determinate that affects changes in pricing of house in UK.................5

3. Government action over the period 2009-2019 affected the UK Housing market............7

4 Impact of Coronavirus (COVID-19) on UK Housing Markets..........................................8

CONCLUSION..........................................................................................................................9

REFERENCES.........................................................................................................................11

INTRODUCTION......................................................................................................................3

1. Average house prices in the UK changed over the period from 2009 – 2019...................3

2 Various economic determinate that affects changes in pricing of house in UK.................5

3. Government action over the period 2009-2019 affected the UK Housing market............7

4 Impact of Coronavirus (COVID-19) on UK Housing Markets..........................................8

CONCLUSION..........................................................................................................................9

REFERENCES.........................................................................................................................11

INTRODUCTION

There are two types of environment, internal and external. The internal factors can be

easily controlled but the external factors are not in the control but certain steps can be taken

in order to reduce the impact of it on the businesses through appropriate decision making.

This report provides an insight about the changes in the average house prices in UK in last

decade ranging from 2009 to 2019 and it covers the key economic determinants that caused

these changes. It also covers the steps and the actions taken by the UK government in last

decade which influenced the UK housing market. At last, it also provided an insight about the

expected changes that might occur because of the impact of COVID – 19 on the housing

market of in the country (UK).

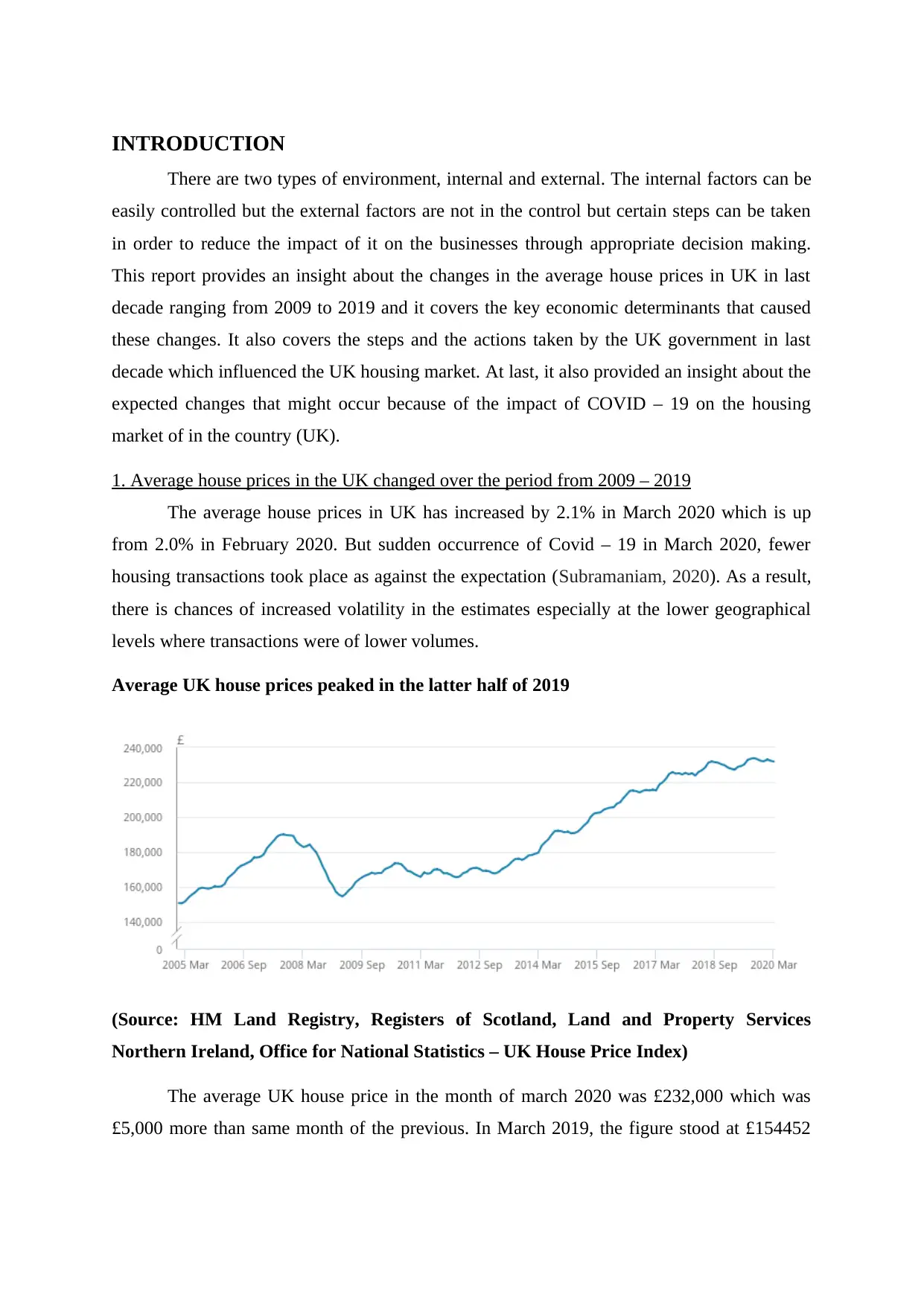

1. Average house prices in the UK changed over the period from 2009 – 2019

The average house prices in UK has increased by 2.1% in March 2020 which is up

from 2.0% in February 2020. But sudden occurrence of Covid – 19 in March 2020, fewer

housing transactions took place as against the expectation (Subramaniam, 2020). As a result,

there is chances of increased volatility in the estimates especially at the lower geographical

levels where transactions were of lower volumes.

Average UK house prices peaked in the latter half of 2019

(Source: HM Land Registry, Registers of Scotland, Land and Property Services

Northern Ireland, Office for National Statistics – UK House Price Index)

The average UK house price in the month of march 2020 was £232,000 which was

£5,000 more than same month of the previous. In March 2019, the figure stood at £154452

There are two types of environment, internal and external. The internal factors can be

easily controlled but the external factors are not in the control but certain steps can be taken

in order to reduce the impact of it on the businesses through appropriate decision making.

This report provides an insight about the changes in the average house prices in UK in last

decade ranging from 2009 to 2019 and it covers the key economic determinants that caused

these changes. It also covers the steps and the actions taken by the UK government in last

decade which influenced the UK housing market. At last, it also provided an insight about the

expected changes that might occur because of the impact of COVID – 19 on the housing

market of in the country (UK).

1. Average house prices in the UK changed over the period from 2009 – 2019

The average house prices in UK has increased by 2.1% in March 2020 which is up

from 2.0% in February 2020. But sudden occurrence of Covid – 19 in March 2020, fewer

housing transactions took place as against the expectation (Subramaniam, 2020). As a result,

there is chances of increased volatility in the estimates especially at the lower geographical

levels where transactions were of lower volumes.

Average UK house prices peaked in the latter half of 2019

(Source: HM Land Registry, Registers of Scotland, Land and Property Services

Northern Ireland, Office for National Statistics – UK House Price Index)

The average UK house price in the month of march 2020 was £232,000 which was

£5,000 more than same month of the previous. In March 2019, the figure stood at £154452

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which was lowest in this 10 year trend. After this, the started rising with little fluctuation and

in the March 2019 it stood at £227104.

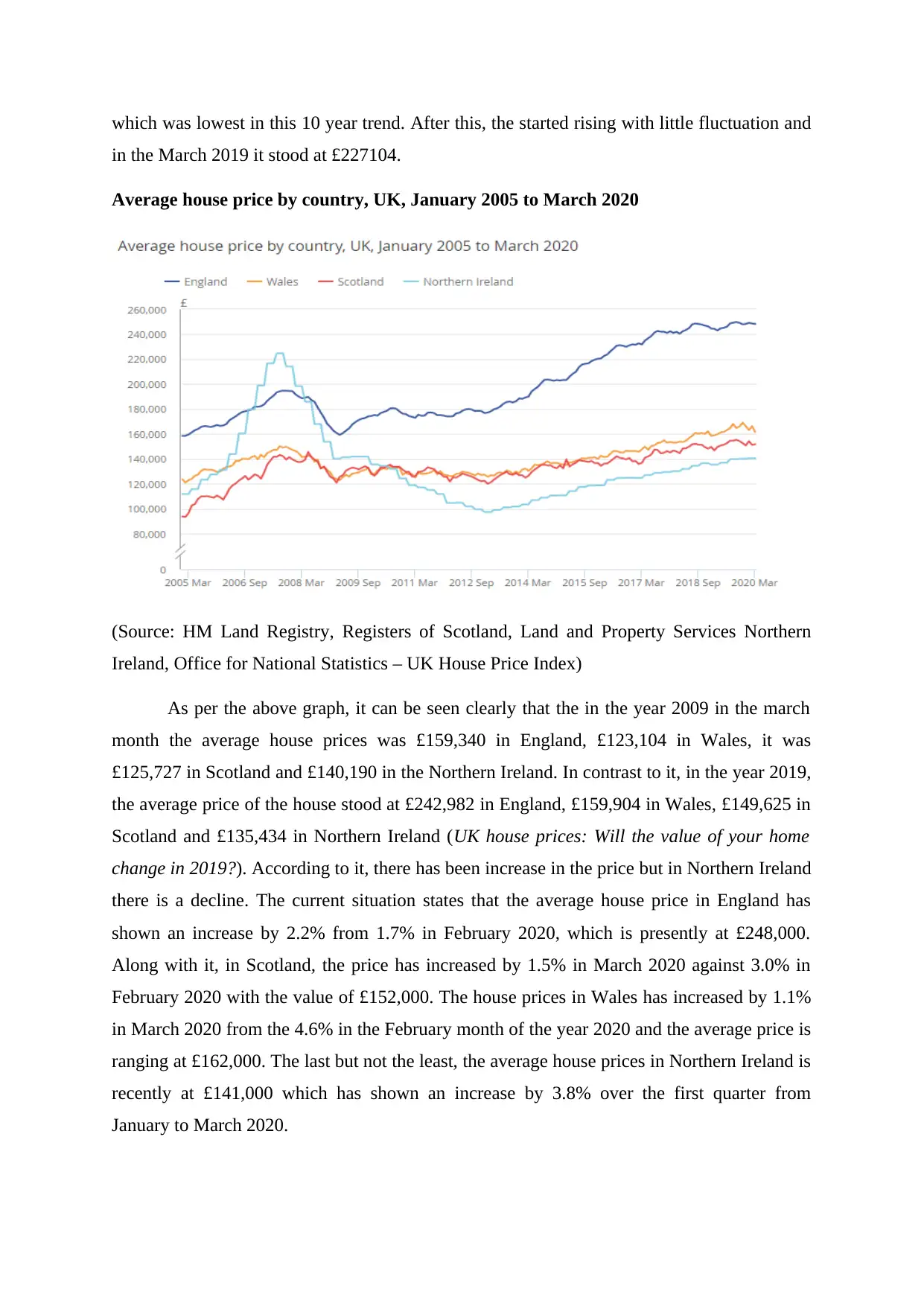

Average house price by country, UK, January 2005 to March 2020

(Source: HM Land Registry, Registers of Scotland, Land and Property Services Northern

Ireland, Office for National Statistics – UK House Price Index)

As per the above graph, it can be seen clearly that the in the year 2009 in the march

month the average house prices was £159,340 in England, £123,104 in Wales, it was

£125,727 in Scotland and £140,190 in the Northern Ireland. In contrast to it, in the year 2019,

the average price of the house stood at £242,982 in England, £159,904 in Wales, £149,625 in

Scotland and £135,434 in Northern Ireland (UK house prices: Will the value of your home

change in 2019?). According to it, there has been increase in the price but in Northern Ireland

there is a decline. The current situation states that the average house price in England has

shown an increase by 2.2% from 1.7% in February 2020, which is presently at £248,000.

Along with it, in Scotland, the price has increased by 1.5% in March 2020 against 3.0% in

February 2020 with the value of £152,000. The house prices in Wales has increased by 1.1%

in March 2020 from the 4.6% in the February month of the year 2020 and the average price is

ranging at £162,000. The last but not the least, the average house prices in Northern Ireland is

recently at £141,000 which has shown an increase by 3.8% over the first quarter from

January to March 2020.

in the March 2019 it stood at £227104.

Average house price by country, UK, January 2005 to March 2020

(Source: HM Land Registry, Registers of Scotland, Land and Property Services Northern

Ireland, Office for National Statistics – UK House Price Index)

As per the above graph, it can be seen clearly that the in the year 2009 in the march

month the average house prices was £159,340 in England, £123,104 in Wales, it was

£125,727 in Scotland and £140,190 in the Northern Ireland. In contrast to it, in the year 2019,

the average price of the house stood at £242,982 in England, £159,904 in Wales, £149,625 in

Scotland and £135,434 in Northern Ireland (UK house prices: Will the value of your home

change in 2019?). According to it, there has been increase in the price but in Northern Ireland

there is a decline. The current situation states that the average house price in England has

shown an increase by 2.2% from 1.7% in February 2020, which is presently at £248,000.

Along with it, in Scotland, the price has increased by 1.5% in March 2020 against 3.0% in

February 2020 with the value of £152,000. The house prices in Wales has increased by 1.1%

in March 2020 from the 4.6% in the February month of the year 2020 and the average price is

ranging at £162,000. The last but not the least, the average house prices in Northern Ireland is

recently at £141,000 which has shown an increase by 3.8% over the first quarter from

January to March 2020.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The average housing price in UK in January 2019 was at £232,000 as represented in

the chart which when compared to the country wise chart, it showed a big difference (UK

House Price Index: March 2020). In England, the average price was ranging at £245,000 as

an increase of 1.5% while in the Scotland the price was at £149,000, an increase of 1.3%, in

case of Wales the price is at £160,000 which is a rise of 4.6% while in Northern Ireland, it is

an increase of 5.5% amounting to £137,000. Even within England, there is a much difference

in the housing prices and the prices in London were completely distorting the Average of

England. In 2019, the average price in London was £568,000 a decrease of 1.9% over

January 2018.

2 Various economic determinate that affects changes in pricing of house in UK

It can be stated that there are several changes in pricing of house in UK during 2009-

2019 due to different factors such as economic condition, size and demographical structure,

interest rates and unemployment level within country (Wu and Lux, 2018). Therefore various

determinate that affect pricing of house in UK can be illustrated as follows:

Economic growth: It can be stated that demand of house changes or fluctuate as per

economic condition that is disposable income of customers, interest rates and unemployment.

Since, 2009 there is tremendously increase in price of house as people of UK are demanding

more and more house to live better lifestyles. Brexit is another component that leads to

economic slowdown thus decrease in overall income and expenditure so people are less likely

to make purchased of home.

Unemployment: It is another factors or determinate which influence changes in prices of UK

as people tend to decrease their overall demand with increase in unemployment level. As

less number of people of UK are ready to buy house at rising prices of house that may lead to

decrease in price of house. There is increase in level of unemployment level due to brexit

therefore people are less willing to spend in house that in turn affected prices of house in UK.

Interest rates: People decided to make purchase of house on basis of interest rates that are

charged by bank of England as it lead to increase in cost of monthly payment that individual

need to pay. Due to increase in overall interest rates of house cost of mortgage payment have

increase which affected decision making of people to make purchased of house (Braakmann

and McDonald, 2020). For example due to rise in interest rates in 1990-92 in UK has

contributed in decreased in demand of house thus bank has reduced interest for smooth flow

the chart which when compared to the country wise chart, it showed a big difference (UK

House Price Index: March 2020). In England, the average price was ranging at £245,000 as

an increase of 1.5% while in the Scotland the price was at £149,000, an increase of 1.3%, in

case of Wales the price is at £160,000 which is a rise of 4.6% while in Northern Ireland, it is

an increase of 5.5% amounting to £137,000. Even within England, there is a much difference

in the housing prices and the prices in London were completely distorting the Average of

England. In 2019, the average price in London was £568,000 a decrease of 1.9% over

January 2018.

2 Various economic determinate that affects changes in pricing of house in UK

It can be stated that there are several changes in pricing of house in UK during 2009-

2019 due to different factors such as economic condition, size and demographical structure,

interest rates and unemployment level within country (Wu and Lux, 2018). Therefore various

determinate that affect pricing of house in UK can be illustrated as follows:

Economic growth: It can be stated that demand of house changes or fluctuate as per

economic condition that is disposable income of customers, interest rates and unemployment.

Since, 2009 there is tremendously increase in price of house as people of UK are demanding

more and more house to live better lifestyles. Brexit is another component that leads to

economic slowdown thus decrease in overall income and expenditure so people are less likely

to make purchased of home.

Unemployment: It is another factors or determinate which influence changes in prices of UK

as people tend to decrease their overall demand with increase in unemployment level. As

less number of people of UK are ready to buy house at rising prices of house that may lead to

decrease in price of house. There is increase in level of unemployment level due to brexit

therefore people are less willing to spend in house that in turn affected prices of house in UK.

Interest rates: People decided to make purchase of house on basis of interest rates that are

charged by bank of England as it lead to increase in cost of monthly payment that individual

need to pay. Due to increase in overall interest rates of house cost of mortgage payment have

increase which affected decision making of people to make purchased of house (Braakmann

and McDonald, 2020). For example due to rise in interest rates in 1990-92 in UK has

contributed in decreased in demand of house thus bank has reduced interest for smooth flow

of economy. Bank of England have decreased or cut interest rates by 0.5% despite of that cost

of mortgage is continuously rising so that people less demand for house in UK.

Consumer confidence: Due to changes in consumer expectation and confidence level prices

of UK have changed over period of 2009-2019. Such as if consumers have more confidence

that prices of house will rise in future than they will take decision to make purchased of

house which lead to increase in overall prices of houses in UK. Thus, in just opposite case

when people have belief that prices of house will fall in future they will delay their purchased

in order to save their money.

Availability of mortgage: Most of the people planned to buy homes by taking mortgage so

that they can make payment in small amount form their respective salary earned. There was

less availability of fund or credit crunch with banks in 2007 in UK therefore bank of England

have make strict rules and policies for lending mortgage to people. Lot of money need to be

kept by individual as a deposit in order to take loans or mortgage that contributed in fall in

demand of house.

Supply of house: UK is facing shortage of house therefore decrease in availability of house

has contributed in tremendously increase in prices of house since 2009. It can be stated that

supply of house depend upon main two factors such as total number of new houses built and

existing available homes for people to live (De Mooij and Liu, 2020). It need long time to

built a house and increase supply within economy so prices of house are rising at increasing

rates as supply is not equivalent to demand of houses. There is limited supply of house as

compared to demand which have contributed towards increasing in overall prices of houses.

Affordability of people: Increase in income of individual have contributed towards increase

in prices of house such as in during boom period 2007 prices of house increased by 5% due to

increase in disposable income of customers. On the other hand due to reduce in affordability

of people in case of Brexit have resulted in decreased in demand of house in UK in 2019.

Demographical structure: Number of people in UK wants to live their life independently

having their separate house that have lead to increase in demand and prices of houses. There

are various elements that lead to increase in prices of houses in UK which stated that

increasing number of divorce cases, many immigrate from eastern countries and east Europe

people want to have their home in UK (Berger and et.al., 2018). Other factors that have

impacted in prices of house is increase in number of older generation due to increasing life

of mortgage is continuously rising so that people less demand for house in UK.

Consumer confidence: Due to changes in consumer expectation and confidence level prices

of UK have changed over period of 2009-2019. Such as if consumers have more confidence

that prices of house will rise in future than they will take decision to make purchased of

house which lead to increase in overall prices of houses in UK. Thus, in just opposite case

when people have belief that prices of house will fall in future they will delay their purchased

in order to save their money.

Availability of mortgage: Most of the people planned to buy homes by taking mortgage so

that they can make payment in small amount form their respective salary earned. There was

less availability of fund or credit crunch with banks in 2007 in UK therefore bank of England

have make strict rules and policies for lending mortgage to people. Lot of money need to be

kept by individual as a deposit in order to take loans or mortgage that contributed in fall in

demand of house.

Supply of house: UK is facing shortage of house therefore decrease in availability of house

has contributed in tremendously increase in prices of house since 2009. It can be stated that

supply of house depend upon main two factors such as total number of new houses built and

existing available homes for people to live (De Mooij and Liu, 2020). It need long time to

built a house and increase supply within economy so prices of house are rising at increasing

rates as supply is not equivalent to demand of houses. There is limited supply of house as

compared to demand which have contributed towards increasing in overall prices of houses.

Affordability of people: Increase in income of individual have contributed towards increase

in prices of house such as in during boom period 2007 prices of house increased by 5% due to

increase in disposable income of customers. On the other hand due to reduce in affordability

of people in case of Brexit have resulted in decreased in demand of house in UK in 2019.

Demographical structure: Number of people in UK wants to live their life independently

having their separate house that have lead to increase in demand and prices of houses. There

are various elements that lead to increase in prices of houses in UK which stated that

increasing number of divorce cases, many immigrate from eastern countries and east Europe

people want to have their home in UK (Berger and et.al., 2018). Other factors that have

impacted in prices of house is increase in number of older generation due to increasing life

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expectancy at the same time children are also leaving home earlier that have contributed in

increasing prices of houses.

Speculation: This factor has also impacted on pricing of houses in UK as most of the people

use their capital gain to make purchase of house for better living. Many investors in UK are

attracted to invest their respective capital in house in order to get more return in future

circumstance. Therefore many investors buy homes not for their living but for earning money

in terms of rental charges and capital gains. Such people mostly sell its house in times of

boom or rise in prices of house in order to get maximum benefits of their capital invested.

Prices of accommodation: Due to increase in inflation rates in UK have lead to increase in

prices of house and rental charged therefore more people likes to have their personal house

for better living standard (Bogin and Doerner, 2019). So, increase in demand of house or

accommodation facilities because of increase in rent has lead to increase in house prices in

UK.

Therefore it can be stated from above analysis that various economic determinate

have contributed in increased and decreased in prices of houses. Prices of accommodation,

supply of houses, and affordability of house and demographical structure of UK have

impacted on overall prices trend of house in UK.

3. Government action over the period 2009-2019 affected the UK Housing market

The “Help to Buy” policy was introduced which aims at flagship housing policy of

the past ruling government to stimulate the housing demand. It consists of four instruments

which includes equity loans, mortgage guarantees and a new buy scheme in which the buyers

are allowed to purchase the new houses which are being built recently with the deposit of 5%

of the total purchase price (Bramley and Fitzpatrick, 2018). The main purpose for the

promotion of this policy was to increase the demand which would convert into new housing

being supplied and attaining the objective of higher homeownership. It also aims at

supporting those home buyers who find themselves being excluded from society as they don’t

have enough money. This scheme was introduced in the year 2011 which was a part of the

government housing strategy and was announced in 2012. Again, in April 2014, the new

scheme called the NewBuy scheme was introduced under the Help to Buy scheme.

The housing related tax also have a huge impact over the housing affordability which

is because in the supply constrained areas, the lower or higher tax have the effect of getting

capitalized into higher or lower property prices. Earlier, the UK government spending huge

increasing prices of houses.

Speculation: This factor has also impacted on pricing of houses in UK as most of the people

use their capital gain to make purchase of house for better living. Many investors in UK are

attracted to invest their respective capital in house in order to get more return in future

circumstance. Therefore many investors buy homes not for their living but for earning money

in terms of rental charges and capital gains. Such people mostly sell its house in times of

boom or rise in prices of house in order to get maximum benefits of their capital invested.

Prices of accommodation: Due to increase in inflation rates in UK have lead to increase in

prices of house and rental charged therefore more people likes to have their personal house

for better living standard (Bogin and Doerner, 2019). So, increase in demand of house or

accommodation facilities because of increase in rent has lead to increase in house prices in

UK.

Therefore it can be stated from above analysis that various economic determinate

have contributed in increased and decreased in prices of houses. Prices of accommodation,

supply of houses, and affordability of house and demographical structure of UK have

impacted on overall prices trend of house in UK.

3. Government action over the period 2009-2019 affected the UK Housing market

The “Help to Buy” policy was introduced which aims at flagship housing policy of

the past ruling government to stimulate the housing demand. It consists of four instruments

which includes equity loans, mortgage guarantees and a new buy scheme in which the buyers

are allowed to purchase the new houses which are being built recently with the deposit of 5%

of the total purchase price (Bramley and Fitzpatrick, 2018). The main purpose for the

promotion of this policy was to increase the demand which would convert into new housing

being supplied and attaining the objective of higher homeownership. It also aims at

supporting those home buyers who find themselves being excluded from society as they don’t

have enough money. This scheme was introduced in the year 2011 which was a part of the

government housing strategy and was announced in 2012. Again, in April 2014, the new

scheme called the NewBuy scheme was introduced under the Help to Buy scheme.

The housing related tax also have a huge impact over the housing affordability which

is because in the supply constrained areas, the lower or higher tax have the effect of getting

capitalized into higher or lower property prices. Earlier, the UK government spending huge

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

amount in subsidizing the building of the social housing which could help in increasing the

supply but then the social housing has fallen out and the government sell of it and also

stopped building the council housing. But the council housing provided boost to the UK’s

economy. The government has also taken initiative in reducing or discouraging the buy to let

properties and second homes. This source of demand is the major factor that has led to the

pushing up of the prices.

One policy that was introduced was to provide disincentives for buy to let and second

homes as an investment. This includes high tax rate such as stamp duty on the second homes.

Therefore, by reducing the demand from this market segment, would make the house prices

more affordable in respect to the ordinary home buyers. As per the latest, stamp duty land tax

which was announced in 2014 eliminates the longstanding anomaly in the taxation rule

(Mulheirn, 2019). Under the previous rule, the home buyers were required to pay the tax at

the one single rate on the entire property price which resulted into large discontinuous jump

in the liability. For instance, if the house is sold for £250,000 invites the tax liability of £2500

whereas in case the house is sold for £250001 then the liability will be of £7500. Therefore,

under the new rules, the tax is requiring to be paid within the tax band as in case of income

tax. Over 635,000 homes in England are empty and nearly 216,000 are vacant for more than

6 months. Therefore, the government is working on bringing the empty houses back to use

which is the most sustainable way of increasing the supply and reducing the negative

influence of it over the society (2010 to 2015 government policy: house building. 2015). The

government has also given New Homes Bonus on account of the long term empty houses

being brought back, from April 2011, the authorities have received more than £2.2 billion,

recognising more than 550,000 houses and over 93,000 empty houses which are being brough

back to use. Also, the councils are given flexibility of charging up to 50% extra council tax

on the housing properties which has been vacant and not furnished over or equal to 2 years.

4 Impact of Coronavirus (COVID-19) on UK Housing Markets

The global pandemic has led to the closure of the housing market in the UK from

mid-March’ 2020, in which the restrictions has been imposed on the citizens of UK to not be

move houses or rent the property to some one else at such time. This has caused holding of

about 450,000 property related transactions in the country (Fernandes, 2020). The UK

government has opened the housing market from the mid-May but there are several

requirements to be fulfilled by the purchasers, realtors and the estate agencies due of the

supply but then the social housing has fallen out and the government sell of it and also

stopped building the council housing. But the council housing provided boost to the UK’s

economy. The government has also taken initiative in reducing or discouraging the buy to let

properties and second homes. This source of demand is the major factor that has led to the

pushing up of the prices.

One policy that was introduced was to provide disincentives for buy to let and second

homes as an investment. This includes high tax rate such as stamp duty on the second homes.

Therefore, by reducing the demand from this market segment, would make the house prices

more affordable in respect to the ordinary home buyers. As per the latest, stamp duty land tax

which was announced in 2014 eliminates the longstanding anomaly in the taxation rule

(Mulheirn, 2019). Under the previous rule, the home buyers were required to pay the tax at

the one single rate on the entire property price which resulted into large discontinuous jump

in the liability. For instance, if the house is sold for £250,000 invites the tax liability of £2500

whereas in case the house is sold for £250001 then the liability will be of £7500. Therefore,

under the new rules, the tax is requiring to be paid within the tax band as in case of income

tax. Over 635,000 homes in England are empty and nearly 216,000 are vacant for more than

6 months. Therefore, the government is working on bringing the empty houses back to use

which is the most sustainable way of increasing the supply and reducing the negative

influence of it over the society (2010 to 2015 government policy: house building. 2015). The

government has also given New Homes Bonus on account of the long term empty houses

being brought back, from April 2011, the authorities have received more than £2.2 billion,

recognising more than 550,000 houses and over 93,000 empty houses which are being brough

back to use. Also, the councils are given flexibility of charging up to 50% extra council tax

on the housing properties which has been vacant and not furnished over or equal to 2 years.

4 Impact of Coronavirus (COVID-19) on UK Housing Markets

The global pandemic has led to the closure of the housing market in the UK from

mid-March’ 2020, in which the restrictions has been imposed on the citizens of UK to not be

move houses or rent the property to some one else at such time. This has caused holding of

about 450,000 property related transactions in the country (Fernandes, 2020). The UK

government has opened the housing market from the mid-May but there are several

requirements to be fulfilled by the purchasers, realtors and the estate agencies due of the

occurrence of Coronavirus (COVID-19) in the nation. There are many impacts of the crisis

over the housing markets in UK are stated below.

Government Guidelines: The government authorities of the UK has imposed certain

mandatory guidelines in respect to all the parties who are being involved in the housing

market which mainly involves traders, agents, builders, purchaser, surveyors and so forth.

There are guidelines for the landlords and the tenants as well. The first and the foremost

important guideline is to maintain social distancing among each other and requires to be very

careful and cautious while executing any transaction in terms of safety. The other rules are

that no open house viewing would take place as it will cause gathering of large number of

people which can be dangerous at this point of time due to Coronavirus (COVID-19). Also,

the real estate agents are also encouraged to not conduct any contact with the potential client

who is showing the symptoms of Coronavirus (COVID-19). Even individuals were asked to

self-isolate themselves and are also advised to not move outside their house during this time

period. Apart from this, in aces where new house is being purchased, the viewing should be

done virtually wherever possible and also the physical viewing is restricted to a certain limit

in terms of number of members of the household. All these steps are being taken in order to

stop the spread of Coronavirus (COVID-19) through the functioning of the housing market in

UK.

Delivery of stalled demand: Before the nation Lockdown because of Covid – 19,

there were certain transaction that were stalled in UK’s housing market which lead to decline

in the demand by nearly 38% of its overall transaction which has caused huge problem for the

economic growth and development of the nation (Allen-Coghlan and McQuinn, 2020). As

per the reports, it is estimated that the loss of up to £7.9 billion in DIY and renovation spend

and along with that £395 million on paying removals companies in the UK housing market.

Now, that the market is reopened, it is expected that there will be increase in the demand for

the operations of the housing market where were earlier stalled due to the sudden lockdown

imposed because of Coronavirus (COVID-19).

Changing trends: The current situation is very hard for the country’s population due

to the coronavirus; thus, it is expected that there will be change in the consumer trends. The

young and the working population of the UK are in requirement of the houses, the elder

population or old aged people of UK are also expected to downsize their properties and

houses in order to provide financial support to their families during the crisis and the tough

over the housing markets in UK are stated below.

Government Guidelines: The government authorities of the UK has imposed certain

mandatory guidelines in respect to all the parties who are being involved in the housing

market which mainly involves traders, agents, builders, purchaser, surveyors and so forth.

There are guidelines for the landlords and the tenants as well. The first and the foremost

important guideline is to maintain social distancing among each other and requires to be very

careful and cautious while executing any transaction in terms of safety. The other rules are

that no open house viewing would take place as it will cause gathering of large number of

people which can be dangerous at this point of time due to Coronavirus (COVID-19). Also,

the real estate agents are also encouraged to not conduct any contact with the potential client

who is showing the symptoms of Coronavirus (COVID-19). Even individuals were asked to

self-isolate themselves and are also advised to not move outside their house during this time

period. Apart from this, in aces where new house is being purchased, the viewing should be

done virtually wherever possible and also the physical viewing is restricted to a certain limit

in terms of number of members of the household. All these steps are being taken in order to

stop the spread of Coronavirus (COVID-19) through the functioning of the housing market in

UK.

Delivery of stalled demand: Before the nation Lockdown because of Covid – 19,

there were certain transaction that were stalled in UK’s housing market which lead to decline

in the demand by nearly 38% of its overall transaction which has caused huge problem for the

economic growth and development of the nation (Allen-Coghlan and McQuinn, 2020). As

per the reports, it is estimated that the loss of up to £7.9 billion in DIY and renovation spend

and along with that £395 million on paying removals companies in the UK housing market.

Now, that the market is reopened, it is expected that there will be increase in the demand for

the operations of the housing market where were earlier stalled due to the sudden lockdown

imposed because of Coronavirus (COVID-19).

Changing trends: The current situation is very hard for the country’s population due

to the coronavirus; thus, it is expected that there will be change in the consumer trends. The

young and the working population of the UK are in requirement of the houses, the elder

population or old aged people of UK are also expected to downsize their properties and

houses in order to provide financial support to their families during the crisis and the tough

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

times. If in case this trend continuous and become popular among the old aged population,

then it will lead to destabilising the pricing strategies of the sellers and the real estate agents

in the UK housing market.

CONCLUSION

From the above it can be summarized that there are various factors having an

influence over the market economy of the country which makes it essential for the respective

authorities to make relevant decisions in order to manage the situation in a far better manner.

This report showed how the external factors had influenced the complete housing market in

UK and what are steps which are being taken by the government for promoting the business.

The government of UK has taken and implemented various policies in order to effectively

handle the demand and supply of the houses in the market. The variation the average housing

prices over the decade has been examined with respect to the percent change and also country

wise along with the causes for these changes. Current, housing market situation occurred due

to COVID – 19 and its impact over the housing market has led to the opposite movement as

the growth has declined which was against the expectations.

then it will lead to destabilising the pricing strategies of the sellers and the real estate agents

in the UK housing market.

CONCLUSION

From the above it can be summarized that there are various factors having an

influence over the market economy of the country which makes it essential for the respective

authorities to make relevant decisions in order to manage the situation in a far better manner.

This report showed how the external factors had influenced the complete housing market in

UK and what are steps which are being taken by the government for promoting the business.

The government of UK has taken and implemented various policies in order to effectively

handle the demand and supply of the houses in the market. The variation the average housing

prices over the decade has been examined with respect to the percent change and also country

wise along with the causes for these changes. Current, housing market situation occurred due

to COVID – 19 and its impact over the housing market has led to the opposite movement as

the growth has declined which was against the expectations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Allen-Coghlan, M. and McQuinn, K., 2020. Property prices and Covid-19 related

administrative closures: What are the implications?

Berger, D and et.al., 2018. House prices and consumer spending. The Review of Economic

Studies, 85(3). pp.1502-1542.

Bogin, A. N. and Doerner, W. M., 2019. Property renovations and their impact on house

price index construction. Journal of Real Estate Research, 41(2). pp.249-283.

Braakmann, N. and McDonald, S., 2020. Housing subsidies and property prices: Evidence

from England. Regional Science and Urban Economics, 80. p.103374.

Bramley, G. and Fitzpatrick, S., 2018. Homelessness in the UK: who is most at

risk?. Housing Studies, 33(1), pp.96-116.

De Mooij, R. and Liu, L., 2020. At a cost: The real effects of transfer pricing

regulations. IMF Economic Review, 68(1), pp.268-306.

Fernandes, N., 2020. Economic effects of coronavirus outbreak (COVID-19) on the world

economy. Available at SSRN 3557504.

Mulheirn, I., 2019. Tackling the UK housing crisis: is supply the answer. UK Collaborative

Centre for Housing Evidence.

Subramaniam, P., 2020. UK House Price Growth Continues to Slow Down. Energy.

Wu, Y. and Lux, N., 2018. UK house prices: Bubbles or market efficiency? evidence from

regional analysis. Journal of Risk and Financial Management, 11(3). p.54.

Online

UK house prices: Will the value of your home change in 2019?. [Online]. Available

Through:< https://www.bbc.com/news/business-46543252>.

2010 to 2015 government policy: house building. 2015. [Online]. Available Through:<

www.gov.uk/government/publications/2010-to-2015-government-policy-house-

building/2010-to-2015-government-policy-house-building>.

UK House Price Index: March 2020. [Online]. Available Through:<

https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/

housepriceindex/march2020>.

Books and Journals

Allen-Coghlan, M. and McQuinn, K., 2020. Property prices and Covid-19 related

administrative closures: What are the implications?

Berger, D and et.al., 2018. House prices and consumer spending. The Review of Economic

Studies, 85(3). pp.1502-1542.

Bogin, A. N. and Doerner, W. M., 2019. Property renovations and their impact on house

price index construction. Journal of Real Estate Research, 41(2). pp.249-283.

Braakmann, N. and McDonald, S., 2020. Housing subsidies and property prices: Evidence

from England. Regional Science and Urban Economics, 80. p.103374.

Bramley, G. and Fitzpatrick, S., 2018. Homelessness in the UK: who is most at

risk?. Housing Studies, 33(1), pp.96-116.

De Mooij, R. and Liu, L., 2020. At a cost: The real effects of transfer pricing

regulations. IMF Economic Review, 68(1), pp.268-306.

Fernandes, N., 2020. Economic effects of coronavirus outbreak (COVID-19) on the world

economy. Available at SSRN 3557504.

Mulheirn, I., 2019. Tackling the UK housing crisis: is supply the answer. UK Collaborative

Centre for Housing Evidence.

Subramaniam, P., 2020. UK House Price Growth Continues to Slow Down. Energy.

Wu, Y. and Lux, N., 2018. UK house prices: Bubbles or market efficiency? evidence from

regional analysis. Journal of Risk and Financial Management, 11(3). p.54.

Online

UK house prices: Will the value of your home change in 2019?. [Online]. Available

Through:< https://www.bbc.com/news/business-46543252>.

2010 to 2015 government policy: house building. 2015. [Online]. Available Through:<

www.gov.uk/government/publications/2010-to-2015-government-policy-house-

building/2010-to-2015-government-policy-house-building>.

UK House Price Index: March 2020. [Online]. Available Through:<

https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/

housepriceindex/march2020>.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.