UK Housing Market: Changes, Determinants, and COVID-19 Impact

VerifiedAdded on 2023/01/09

|12

|3991

|42

Report

AI Summary

This report provides a comprehensive analysis of the UK housing market, examining the fluctuations in average house prices between 2009 and 2019, along with the economic determinants influencing these prices. It delves into factors such as economic growth, unemployment, mortgage availability, interest rates, affordability, housing supply, and consumer confidence. The report also explores government actions during this period and predicts the impact of the COVID-19 pandemic on the UK housing market. Through the analysis of trends and economic indicators, the report aims to provide a clear understanding of the dynamics within the UK housing sector.

CONTEMPORARY

BUSINESS ENVIRONMENT

BUSINESS ENVIRONMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Change in housing prices in UK over the period of 2009 to 2019..........................................3

2. Economic determinants affecting the average housing prices in UK......................................5

3. Government action taken.........................................................................................................8

4. Impact of Covid- 19 on UK housing market...........................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Change in housing prices in UK over the period of 2009 to 2019..........................................3

2. Economic determinants affecting the average housing prices in UK......................................5

3. Government action taken.........................................................................................................8

4. Impact of Covid- 19 on UK housing market...........................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION

The housing market is the supply and demand of houses in a particular region which is

majorly determined by average house prices and the trends in the market. A housing market is

affected by supply, demand, rented sector, housing prices and government intervention. The

housing market of UK is volatile in nature. This report will highlight the change in the average

house prices in UK over a period of 2009 – 2019 and the economic determinants responsible for

these prices. The action of the government over this period is described and a prediction of

impact of Covid-19 on the housing market is determined.

MAIN BODY

1. Change in housing prices in UK over the period of 2009 to 2019

The real estate and housing in particular has always been an interesting sector of

investment as well as trading for people of UK (Antonakakis and Floros, 2016). The lucrative

and secured earning that the real estate and housing market of UK provides is the major point of

attraction for the people.

Figure 1: Change in UK housing prices

Source: UK Housing Market, 2020

The graph above indicates that the prices have steadily increased from the year 2010 to

2020 in the housing sector where every year has seen a rise in the prices collectively. The graph

indicates that in each year, there has been a rise irrespective of the fact that whether the prices

have risen by a higher percentage or by a lower percentage. The year 20196 can be seen as the

The housing market is the supply and demand of houses in a particular region which is

majorly determined by average house prices and the trends in the market. A housing market is

affected by supply, demand, rented sector, housing prices and government intervention. The

housing market of UK is volatile in nature. This report will highlight the change in the average

house prices in UK over a period of 2009 – 2019 and the economic determinants responsible for

these prices. The action of the government over this period is described and a prediction of

impact of Covid-19 on the housing market is determined.

MAIN BODY

1. Change in housing prices in UK over the period of 2009 to 2019

The real estate and housing in particular has always been an interesting sector of

investment as well as trading for people of UK (Antonakakis and Floros, 2016). The lucrative

and secured earning that the real estate and housing market of UK provides is the major point of

attraction for the people.

Figure 1: Change in UK housing prices

Source: UK Housing Market, 2020

The graph above indicates that the prices have steadily increased from the year 2010 to

2020 in the housing sector where every year has seen a rise in the prices collectively. The graph

indicates that in each year, there has been a rise irrespective of the fact that whether the prices

have risen by a higher percentage or by a lower percentage. The year 20196 can be seen as the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

one with the highest level of growth at 21200 points where in the year 2010 it was just at 14992

points. The highest cumulative e growth was between the years 2017 and 2018 where the prices

almost increased by approximately 100 basis points (UK Housing Market, 2020). The graph also

shows that 2020 is the year when the prices are expected to show a cumulative decline and this is

mainly due to the fact that the Covid- 19 pandemic and the global lockdown that was

implemented has affected the economy severely and due to this, the overall decline in the prices

is prominent. Another graph can be used to further analyse the different trends in the housing

market of UK:

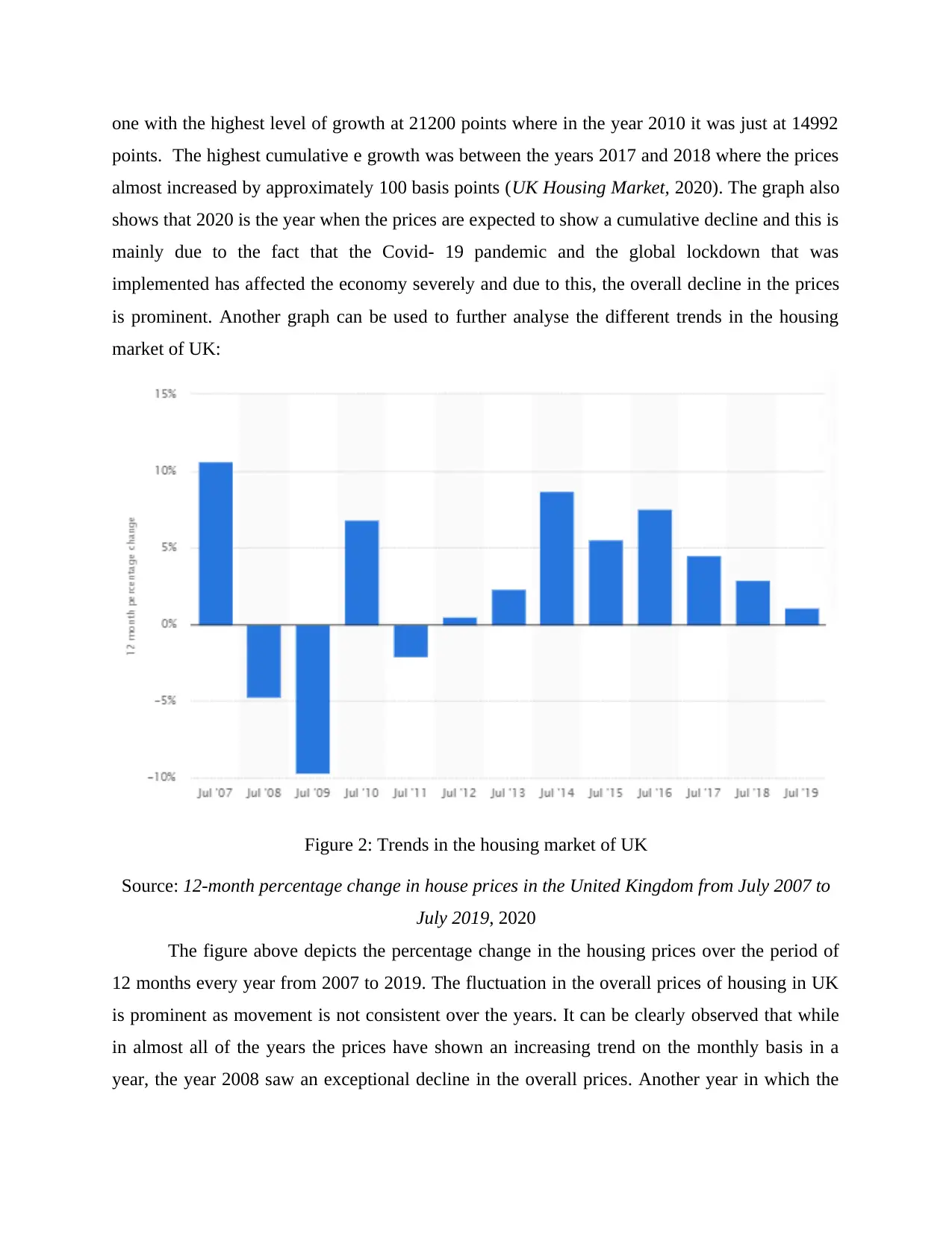

Figure 2: Trends in the housing market of UK

Source: 12-month percentage change in house prices in the United Kingdom from July 2007 to

July 2019, 2020

The figure above depicts the percentage change in the housing prices over the period of

12 months every year from 2007 to 2019. The fluctuation in the overall prices of housing in UK

is prominent as movement is not consistent over the years. It can be clearly observed that while

in almost all of the years the prices have shown an increasing trend on the monthly basis in a

year, the year 2008 saw an exceptional decline in the overall prices. Another year in which the

points. The highest cumulative e growth was between the years 2017 and 2018 where the prices

almost increased by approximately 100 basis points (UK Housing Market, 2020). The graph also

shows that 2020 is the year when the prices are expected to show a cumulative decline and this is

mainly due to the fact that the Covid- 19 pandemic and the global lockdown that was

implemented has affected the economy severely and due to this, the overall decline in the prices

is prominent. Another graph can be used to further analyse the different trends in the housing

market of UK:

Figure 2: Trends in the housing market of UK

Source: 12-month percentage change in house prices in the United Kingdom from July 2007 to

July 2019, 2020

The figure above depicts the percentage change in the housing prices over the period of

12 months every year from 2007 to 2019. The fluctuation in the overall prices of housing in UK

is prominent as movement is not consistent over the years. It can be clearly observed that while

in almost all of the years the prices have shown an increasing trend on the monthly basis in a

year, the year 2008 saw an exceptional decline in the overall prices. Another year in which the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decline can be observed even if at a smaller scale is in 2012 showing a 2% decline collectively.

The increase can be observed to be highest in the year 2007 when it was almost 10.6% and the

decline can be estimated to be highest in 2009 where it was almost 10% decline (12-month

percentage change in house prices in the United Kingdom from July 2007 to July 2019, 2020).

From the year 2016 however, it can be observed that overall the prices have increased but the

percentage change has been lower because of the inflation factors as well.

Therefore, the overall analysis of the different graphs indicates that the movement of the

prices between the different years has been in a positive manner collectively showing positive

trends. The major reason behind the increased prices in the housing and real estate segment of

UK has mainly been due to the inflation in the prices, rising purchasing power, improving

employment status etc. are a variety of factors that have affected this rise or decline in the prices.

2. Economic determinants affecting the average housing prices in UK

The housing market is affected by multiple macro and micro economic factors like

economic growth, interest rates, income level, unemployment rate, availability of mortgages and

aggregate demand and housing supply (Antonakakis and Floros, 2016). With high demand and

low supply, the Housing market may witness a rise in the housing prices, ever-rising rent and

high risk of homelessness of the people of UK. The factors are described as follows: Economic growth: Economic growth refers to the increase in terms of goods and services

that are produced in a country over a period. This is a macroeconomic factor and defines

economic stability of UK. The demand for housing relies directly on the income. When

economic growth is high, the incomes of people tend to rise which means people can

spend more on housing. It increases demand and pushes the housing prices up. This rise

in the demand for houses is mostly referred to as a luxury good that is high elasticity of

income. But during a recession, there is a fall in the income levels of people which means

that they cannot afford to purchase properties. The ones who might have lost their jobs,

face salary cuts or business losses might fall behind on the payment of interests and

mortgages and end up with repossessed houses (Fothergill and Houston, 2016). Unemployment:This is a macroeconomic factor and majorly impacts the demand for high

priced properties like houses. It is directly related to the economic growth of UK.

Unemployment refers to a situation when someone of working age is unable to get a job

The increase can be observed to be highest in the year 2007 when it was almost 10.6% and the

decline can be estimated to be highest in 2009 where it was almost 10% decline (12-month

percentage change in house prices in the United Kingdom from July 2007 to July 2019, 2020).

From the year 2016 however, it can be observed that overall the prices have increased but the

percentage change has been lower because of the inflation factors as well.

Therefore, the overall analysis of the different graphs indicates that the movement of the

prices between the different years has been in a positive manner collectively showing positive

trends. The major reason behind the increased prices in the housing and real estate segment of

UK has mainly been due to the inflation in the prices, rising purchasing power, improving

employment status etc. are a variety of factors that have affected this rise or decline in the prices.

2. Economic determinants affecting the average housing prices in UK

The housing market is affected by multiple macro and micro economic factors like

economic growth, interest rates, income level, unemployment rate, availability of mortgages and

aggregate demand and housing supply (Antonakakis and Floros, 2016). With high demand and

low supply, the Housing market may witness a rise in the housing prices, ever-rising rent and

high risk of homelessness of the people of UK. The factors are described as follows: Economic growth: Economic growth refers to the increase in terms of goods and services

that are produced in a country over a period. This is a macroeconomic factor and defines

economic stability of UK. The demand for housing relies directly on the income. When

economic growth is high, the incomes of people tend to rise which means people can

spend more on housing. It increases demand and pushes the housing prices up. This rise

in the demand for houses is mostly referred to as a luxury good that is high elasticity of

income. But during a recession, there is a fall in the income levels of people which means

that they cannot afford to purchase properties. The ones who might have lost their jobs,

face salary cuts or business losses might fall behind on the payment of interests and

mortgages and end up with repossessed houses (Fothergill and Houston, 2016). Unemployment:This is a macroeconomic factor and majorly impacts the demand for high

priced properties like houses. It is directly related to the economic growth of UK.

Unemployment refers to a situation when someone of working age is unable to get a job

but is willing to work full-time. Rising unemployment can lead to fall in income levels

and affordability of people which in turn decreases the demand for houses thereby

decreasing housing prices. Even if there are housing needs, people would prefer to go for

low priced options or rented properties. They would switch their demand category from

luxury goods to normal good or necessity goods. Since 2008, the unemployment rate of

UK has remained low with slight increase during 2012 and again dropping in 2019 to

mere 3.8%. Availability of Mortgages: A mortgage refers to a loan from any bank or other financial

institutions that enables a person to purchase a home where the collateral being the home

itself and the loan is paid back overtime. There are various types of mortgages mainly

fixed-rate and variable rate mortgages. Fixed rate mortgage provides borrowers a fixed

rate of interest typically 10 to 30 years. A shorter term will lead to a higher monthly

mortgage payment (OMONDI, 2018). It can be useful for the borrower to establish a

household budget. Variable Rate mortgages have high interest rates that can be changed

over the term of the loan. An increased market rate can cause fluctuation to change the

monthly payments. House purchases majorly depend upon the supply of mortgages from

the financial markets of UK. This depends on the belief of building organizations and

societies, banks and lenders that borrowers may not default on loan pay-back. When this

payback confidence is high, there will be high availability of cash and liquidity will

prevail. But when the confidence is low and housing prices fall, lenders may not lend to

new borrowers, resulting in negative equity and default of loans ultimately leading to

banks not lending to each other. After the credit crunch of 2008, raising funds have been

tough for building societies and banks of UK thereby tightening the lending criteria and

higher need for larger deposits. This has decreased the availability of mortgages and led

to a fall in demand. Interest rate:Interest rates have a major impact on the cost on mortgage payments. A

high rate of interest will increase the cost of payments for mortgages which will lead to a

lower demand for purchasing a house. High interest rates tend to make renting

comparatively a better choice for people rather than buying. Interest rates have a major

effect when homeowners possess variable mortgages. Interest rates depends upon various

factors like credit score- people with higher credit scores get lower interest rates as

and affordability of people which in turn decreases the demand for houses thereby

decreasing housing prices. Even if there are housing needs, people would prefer to go for

low priced options or rented properties. They would switch their demand category from

luxury goods to normal good or necessity goods. Since 2008, the unemployment rate of

UK has remained low with slight increase during 2012 and again dropping in 2019 to

mere 3.8%. Availability of Mortgages: A mortgage refers to a loan from any bank or other financial

institutions that enables a person to purchase a home where the collateral being the home

itself and the loan is paid back overtime. There are various types of mortgages mainly

fixed-rate and variable rate mortgages. Fixed rate mortgage provides borrowers a fixed

rate of interest typically 10 to 30 years. A shorter term will lead to a higher monthly

mortgage payment (OMONDI, 2018). It can be useful for the borrower to establish a

household budget. Variable Rate mortgages have high interest rates that can be changed

over the term of the loan. An increased market rate can cause fluctuation to change the

monthly payments. House purchases majorly depend upon the supply of mortgages from

the financial markets of UK. This depends on the belief of building organizations and

societies, banks and lenders that borrowers may not default on loan pay-back. When this

payback confidence is high, there will be high availability of cash and liquidity will

prevail. But when the confidence is low and housing prices fall, lenders may not lend to

new borrowers, resulting in negative equity and default of loans ultimately leading to

banks not lending to each other. After the credit crunch of 2008, raising funds have been

tough for building societies and banks of UK thereby tightening the lending criteria and

higher need for larger deposits. This has decreased the availability of mortgages and led

to a fall in demand. Interest rate:Interest rates have a major impact on the cost on mortgage payments. A

high rate of interest will increase the cost of payments for mortgages which will lead to a

lower demand for purchasing a house. High interest rates tend to make renting

comparatively a better choice for people rather than buying. Interest rates have a major

effect when homeowners possess variable mortgages. Interest rates depends upon various

factors like credit score- people with higher credit scores get lower interest rates as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

compared to people with lower credit scores. House location also effects the interest

rates. City areas generally have a higher rate of interest on mortgage payments. Down

payments also change the rate of interests as a higher down payment would mean low

interest rate. Loan term also reflects the interest rate. A Short term loan will mean lower

interest rates but high monthly payments. A 10-year fixed mortgage rate in UK as on

march 2020 is around 2.44 % as recorded by the Bank of England. Average interest rate

for mortgages in UK for a Two year- fixed rate is 1.42% and two-year variable rate is

2.5% as of March 2020. Affordability:The ratio of the prices of houses to earning have a major impact on the

demand. As there is an increase in the price of the houses in relation to the stable income

level, fewer consumers will be able to afford to purchase housing properties. The other

way in which affordability of houses is noted is by the percentage of take-home payment

that is spent on mortgages. This takes into consideration both the prices of the house that

is primarily the rate of interests and the cost of montage payments on monthly basis. The

affordability is affected by many macro and micro economic indicators like economic

growth, unemployment rate, income level, skill and educational level of people, supply of

housing, restrictions on planning, Growth of population, lending and credit facilities from

financial institutions and banks, government policies etc. high prices, insufficient

competition or market exclusivity, interaction of various factors affecting real estate

markets, uneven bargaining power between sellers and buyers etc. also determine the

affordability of average population of purchasers in the UK economy (Kenny, Elliott and

Bicquelet-Lock, 2018). The UK average prices of housing properties is around five times

the average earnings of the people. In city areas like London and Manchester, the house

prices are nine times the average earnings whereas in the northern areas it is only three

times the average earnings. When the interest rates were cut to below 0.5% in 2009, it led

to lower mortgage payments for owners of properties. Housing supply: A shortage in the supply of housing pushes the prices up. Houses are

supplied by construction companies and their position in the market and economy. The

firms are affected by many government policies, exchange rates, taxes and other

regulations and inflation. It is a very volatile sector and the investment has a high

correlation to the rate of the growth of the economy and its future prospects. Housing

rates. City areas generally have a higher rate of interest on mortgage payments. Down

payments also change the rate of interests as a higher down payment would mean low

interest rate. Loan term also reflects the interest rate. A Short term loan will mean lower

interest rates but high monthly payments. A 10-year fixed mortgage rate in UK as on

march 2020 is around 2.44 % as recorded by the Bank of England. Average interest rate

for mortgages in UK for a Two year- fixed rate is 1.42% and two-year variable rate is

2.5% as of March 2020. Affordability:The ratio of the prices of houses to earning have a major impact on the

demand. As there is an increase in the price of the houses in relation to the stable income

level, fewer consumers will be able to afford to purchase housing properties. The other

way in which affordability of houses is noted is by the percentage of take-home payment

that is spent on mortgages. This takes into consideration both the prices of the house that

is primarily the rate of interests and the cost of montage payments on monthly basis. The

affordability is affected by many macro and micro economic indicators like economic

growth, unemployment rate, income level, skill and educational level of people, supply of

housing, restrictions on planning, Growth of population, lending and credit facilities from

financial institutions and banks, government policies etc. high prices, insufficient

competition or market exclusivity, interaction of various factors affecting real estate

markets, uneven bargaining power between sellers and buyers etc. also determine the

affordability of average population of purchasers in the UK economy (Kenny, Elliott and

Bicquelet-Lock, 2018). The UK average prices of housing properties is around five times

the average earnings of the people. In city areas like London and Manchester, the house

prices are nine times the average earnings whereas in the northern areas it is only three

times the average earnings. When the interest rates were cut to below 0.5% in 2009, it led

to lower mortgage payments for owners of properties. Housing supply: A shortage in the supply of housing pushes the prices up. Houses are

supplied by construction companies and their position in the market and economy. The

firms are affected by many government policies, exchange rates, taxes and other

regulations and inflation. It is a very volatile sector and the investment has a high

correlation to the rate of the growth of the economy and its future prospects. Housing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

market is an important sector in the construction industry and is quite dynamic in nature.

Any slowdown in prices or prospects of houses means construction companies have to

cut-back on the plans of constructing new houses. This is also because of a low return on

building the new properties(Alwan, Jones and Holgate, 2017). High price of raw

materials like oil and steel also affect the profitability of construction firms. Currently,

UK is facing a shortage in the number of houses, even though there is a forecast of

growth but current rate remains low. There is a backlog in housing properties of around 5

million along with accommodation issues. This means that housing prices will rise

continuously for a long period which will lead to upward pressure on rental rates.

Consumer confidence: Investment in high priced properties like houses are full of risk.

Whether it is the payback or affordability of monthly interest rates, consumers tend to

evaluate everything in depth before committing to such huge investments. Confidence

and financial or real estate knowledge of buyers plays an important yet intangible role in

determining their ability to take risks. There is fear in people due to the high eise and fall

of housing prices which could limit them from purchasing properties and therefore

reduces the demand for Houses(Khan, Rouillard and Upadhayaya, 2019).

3. Government action taken

Government of UK has taken a series of actions in order to regulate and monitor the trade

practices that are taking place in the housing sector of UK. These series of actions help in

monitoring the deals and also control the overall amount that is put at stake (Cook and Watson,

2016). There are a series of actions that UK government has taken over the years and this can be

enumerated in following manner: Green Land Belt: This regulation of the UK government was put to mainly protect the

land that is rich in nature and wildlife from its exploitation by the retail industry. Under

this, the government of UK has put up clear segregations on the pieces of land which

cannot be brought or sold and will belong under the ownership of the UK government

(Antonakakis and Floros, 2016). Currently, the government of UK has reserved

approximately 17% land under the category of reserved so that the natural wildlife can be

protected and ecological balance can be maintained. This regulation has proved to be

Any slowdown in prices or prospects of houses means construction companies have to

cut-back on the plans of constructing new houses. This is also because of a low return on

building the new properties(Alwan, Jones and Holgate, 2017). High price of raw

materials like oil and steel also affect the profitability of construction firms. Currently,

UK is facing a shortage in the number of houses, even though there is a forecast of

growth but current rate remains low. There is a backlog in housing properties of around 5

million along with accommodation issues. This means that housing prices will rise

continuously for a long period which will lead to upward pressure on rental rates.

Consumer confidence: Investment in high priced properties like houses are full of risk.

Whether it is the payback or affordability of monthly interest rates, consumers tend to

evaluate everything in depth before committing to such huge investments. Confidence

and financial or real estate knowledge of buyers plays an important yet intangible role in

determining their ability to take risks. There is fear in people due to the high eise and fall

of housing prices which could limit them from purchasing properties and therefore

reduces the demand for Houses(Khan, Rouillard and Upadhayaya, 2019).

3. Government action taken

Government of UK has taken a series of actions in order to regulate and monitor the trade

practices that are taking place in the housing sector of UK. These series of actions help in

monitoring the deals and also control the overall amount that is put at stake (Cook and Watson,

2016). There are a series of actions that UK government has taken over the years and this can be

enumerated in following manner: Green Land Belt: This regulation of the UK government was put to mainly protect the

land that is rich in nature and wildlife from its exploitation by the retail industry. Under

this, the government of UK has put up clear segregations on the pieces of land which

cannot be brought or sold and will belong under the ownership of the UK government

(Antonakakis and Floros, 2016). Currently, the government of UK has reserved

approximately 17% land under the category of reserved so that the natural wildlife can be

protected and ecological balance can be maintained. This regulation has proved to be

effective in the monitoring of the land that is dealt with and also monitor the overall area

under housing consumption. Subsidiaries: The income tax department of UK has provided several benefits to the

buyers and sellers of the housing property of UK and there are a variety of exemptions as

well as subsidiaries that are available to them. The section 24 of the Income Tax Act

provides a variety of benefits to the housing property buyers in UK ( Emerole, 2018). The

different subsidiaries that were given have helped in controlling the prices of houses in

UK and has also made the objective of buying own house a feasible dream for the people

in UK. Despite the consistently high prices of housing in UK, the easy availability of loan

with reduced interests, the increased benefits that are available etc. have helped in

making the purchase of house an attractive option for UK buyers.

Putting caps on the maximum and minimum prices: Implementation of the regulation

where the maximum and minimum pricing limits have been set up- the government is the

best regulation that the government of UK has developed. This has helped them in

controlling the pricing trends and also link them up in accordance with the movement of

the economy (White and Ke, 2019). These maximum and minimum limits on prices keep

on changing based on the different factors associated with the economic growth where

the aspects such as the purchasing power of people, the employability levels, inflation

rate, availability of loans etc. are a variety of factors that affect the overall sale and

purchase of houses in UK.

There are a variety of other regulations as well that the UK government has taken such as the

implementation of the state ownership, regulation of the market etc. that help them in controlling

the overall housing market of UK. All these regulations collectively help in developing a

comprehensive and monitored system collectively.

4. Impact of Covid- 19 on UK housing market

The global pandemic of Covid- 19, has affected the overall operation of the industries

pertaining to all the relevant sectors in the economy. The influence of the Covid –19 pandemics

on the operation of the housing industry of UK has also been extremely prominent where the

different factors will affect the industry severely (Harding and et.al., 2018). These can be

illustrated as follows:

under housing consumption. Subsidiaries: The income tax department of UK has provided several benefits to the

buyers and sellers of the housing property of UK and there are a variety of exemptions as

well as subsidiaries that are available to them. The section 24 of the Income Tax Act

provides a variety of benefits to the housing property buyers in UK ( Emerole, 2018). The

different subsidiaries that were given have helped in controlling the prices of houses in

UK and has also made the objective of buying own house a feasible dream for the people

in UK. Despite the consistently high prices of housing in UK, the easy availability of loan

with reduced interests, the increased benefits that are available etc. have helped in

making the purchase of house an attractive option for UK buyers.

Putting caps on the maximum and minimum prices: Implementation of the regulation

where the maximum and minimum pricing limits have been set up- the government is the

best regulation that the government of UK has developed. This has helped them in

controlling the pricing trends and also link them up in accordance with the movement of

the economy (White and Ke, 2019). These maximum and minimum limits on prices keep

on changing based on the different factors associated with the economic growth where

the aspects such as the purchasing power of people, the employability levels, inflation

rate, availability of loans etc. are a variety of factors that affect the overall sale and

purchase of houses in UK.

There are a variety of other regulations as well that the UK government has taken such as the

implementation of the state ownership, regulation of the market etc. that help them in controlling

the overall housing market of UK. All these regulations collectively help in developing a

comprehensive and monitored system collectively.

4. Impact of Covid- 19 on UK housing market

The global pandemic of Covid- 19, has affected the overall operation of the industries

pertaining to all the relevant sectors in the economy. The influence of the Covid –19 pandemics

on the operation of the housing industry of UK has also been extremely prominent where the

different factors will affect the industry severely (Harding and et.al., 2018). These can be

illustrated as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Recession: It is expected that after this pandemic is over, the onset of the recession in the

economy of UK will be persistent over a considerable amount of time. The

implementation of the lockdown and the closing down of all the businesses has already

pushed the economic growth of the country significantly backwards for a number of

years. The failure to operate in the international market, the lack on any prominent

income sources etc. led to the downfall of the economy. Therefore, this predicts that this

recession will affect the housing industry of UK as well because the lack of money will

automatically put down purchasing of any property in the priority list of the residents of

UK thus creating a negative impact on the UK housing market. Expectations related to future prices: The pandemic is also bound to affect the prices in

future as well where the overall trends related to the prices of UK housing are bound to

decline significantly in the future market (Ivanovych, 2019). The downfall in the prices

will automatically arise due to lack of demand and the unavailability of the extra funds as

well which will reduce the amount of investment that is being made in the housing

industry of UK. When the real estate market will no longer be attractive, then it will

automatically lead to the development of a market situation where the growth is lower

and prospective buyers are also lower.

Unemployment: The rise in the unemployment will be one of the most prominent

outcomes of the Covid- 19 pandemic where the rise in the number of people who are

jobless will be significant. The lack of availability of any work in the companies has

automatically made them segregate the efficient employees from the inefficient ones and

the cuts in the salaries, delay in promotions and appraisals etc. have proved to be some

of the most prominent outcomes collectively (Stevens, 2018). This has led to the

increased number of people who no longer have employment and hence are no linger

capable of investing in the housing and real estate properties.

Apart from these factors, the all over decline in the collective market of the housing industry is

bound to be significant due to the fact that the overall income has dwindled which has led to a

reduction in the demand as well as people can no longer afford to fulfil their luxurious needs.

Therefore, the market has already fallen and is expected to fall further in the upcoming years

before the housing market and the real estate market collectively recovers.

economy of UK will be persistent over a considerable amount of time. The

implementation of the lockdown and the closing down of all the businesses has already

pushed the economic growth of the country significantly backwards for a number of

years. The failure to operate in the international market, the lack on any prominent

income sources etc. led to the downfall of the economy. Therefore, this predicts that this

recession will affect the housing industry of UK as well because the lack of money will

automatically put down purchasing of any property in the priority list of the residents of

UK thus creating a negative impact on the UK housing market. Expectations related to future prices: The pandemic is also bound to affect the prices in

future as well where the overall trends related to the prices of UK housing are bound to

decline significantly in the future market (Ivanovych, 2019). The downfall in the prices

will automatically arise due to lack of demand and the unavailability of the extra funds as

well which will reduce the amount of investment that is being made in the housing

industry of UK. When the real estate market will no longer be attractive, then it will

automatically lead to the development of a market situation where the growth is lower

and prospective buyers are also lower.

Unemployment: The rise in the unemployment will be one of the most prominent

outcomes of the Covid- 19 pandemic where the rise in the number of people who are

jobless will be significant. The lack of availability of any work in the companies has

automatically made them segregate the efficient employees from the inefficient ones and

the cuts in the salaries, delay in promotions and appraisals etc. have proved to be some

of the most prominent outcomes collectively (Stevens, 2018). This has led to the

increased number of people who no longer have employment and hence are no linger

capable of investing in the housing and real estate properties.

Apart from these factors, the all over decline in the collective market of the housing industry is

bound to be significant due to the fact that the overall income has dwindled which has led to a

reduction in the demand as well as people can no longer afford to fulfil their luxurious needs.

Therefore, the market has already fallen and is expected to fall further in the upcoming years

before the housing market and the real estate market collectively recovers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report it was concluded that the housing market of UK is very volatile

and dynamic in nature and faced many ups and downs over the decade of 2009-2019. There has

been a continuous rise in the housing prices over these years and is affected by economic

determinants like affordability, interest rates, housing supply, economic state of UK, availability

of mortgages and consumer confidence. Various government regulations like Green land belt

have helped in implementation of the state ownership and regulation of the market. The impact

of Covid-19 resulted in a major downfall in the housing market and its further effects in real-

estate market in the upcoming years.

From the above report it was concluded that the housing market of UK is very volatile

and dynamic in nature and faced many ups and downs over the decade of 2009-2019. There has

been a continuous rise in the housing prices over these years and is affected by economic

determinants like affordability, interest rates, housing supply, economic state of UK, availability

of mortgages and consumer confidence. Various government regulations like Green land belt

have helped in implementation of the state ownership and regulation of the market. The impact

of Covid-19 resulted in a major downfall in the housing market and its further effects in real-

estate market in the upcoming years.

REFERENCES

Books and journals

Alwan, Z., Jones, P. and Holgate, P., 2017. Strategic sustainable development in the UK

construction industry, through the framework for strategic sustainable development,

using Building Information Modelling. Journal of Cleaner Production.140. pp.349-358.

Antonakakis, N. and Floros, C., 2016. Dynamic interdependencies among the housing market,

stock market, policy uncertainty and the macroeconomy in the United

Kingdom. International Review of Financial Analysis. 44. pp.111-122.

Antonakakis, N. and Floros, C., 2016. Dynamic interdependencies among the housing market,

stock market, policy uncertainty and the macroeconomy in the United

Kingdom. International Review of Financial Analysis. 44.pp.111-122.

Cook, S. and Watson, D., 2016. A new perspective on the ripple effect in the UK housing

market: Comovement, cyclical subsamples and alternative indices. Urban

Studies. 53(14). pp.3048-3062.

Emerole, G., 2018. Risks and opportunities in emerging markets international real estate

investment: A comparative analysis of Nigeria and South Africa. Journal of the Nigerian

Institution of Estate Surveyors and Valuers. 41(1). pp.71-78.

Fothergill, S. and Houston, D., 2016. Are big cities really the motor of UK regional economic

growth?. Cambridge Journal of Regions, Economy and Society.9(2). pp.319-334.

Harding, A. and et.al., 2018. Supply-side review of the UK specialist housing market and why it

is failing older people. Housing, Care and Support.

Ivanovych, B. A., 2019. Investing in real estate of Great Britain during Brexit. Публічне

урядування. (4 (19)).

Kenny, T., Elliott, T. and Bicquelet-Lock, A., 2018. Better planning for housing affordability:

Three approaches to solving the housing crisis in the UK. Journal of Urban Regeneration

& Renewal.11(3). pp.233-241.

Khan, H., Rouillard, J.F. and Upadhayaya, S., 2019. Consumer Confidence and Household

Investment (No. CEP 19-06).

OMONDI, O.B., 2018. EFFECTS OF MACRO-ECONOMIC VARIABLES ON MORTAGAGE

LOAN UPTAKE (Doctoral dissertation, KENYATTA UNIVERSITY).

Stevens, D. G., 2018. A behavioural data approach towards predicting direct real estate markets

in the United Kingdom (Doctoral dissertation, University of Cambridge).

White, M. and Ke, Q., 2019. Volatility Spillovers and Regional Office Market Connectedness in

the UK (No. eres2019_289). European Real Estate Society (ERES).

Online

12 month percentage change in house prices in the United Kingdom (UK) from July 2007 to July

2019. 2020. [Online]. Available through: <

https://www.statista.com/statistics/751619/house-price-change-uk/ >

UK Housing Market. 2020. [Online]. Available through:

<https://www.economicshelp.org/blog/5709/housing/market/ >

1

Books and journals

Alwan, Z., Jones, P. and Holgate, P., 2017. Strategic sustainable development in the UK

construction industry, through the framework for strategic sustainable development,

using Building Information Modelling. Journal of Cleaner Production.140. pp.349-358.

Antonakakis, N. and Floros, C., 2016. Dynamic interdependencies among the housing market,

stock market, policy uncertainty and the macroeconomy in the United

Kingdom. International Review of Financial Analysis. 44. pp.111-122.

Antonakakis, N. and Floros, C., 2016. Dynamic interdependencies among the housing market,

stock market, policy uncertainty and the macroeconomy in the United

Kingdom. International Review of Financial Analysis. 44.pp.111-122.

Cook, S. and Watson, D., 2016. A new perspective on the ripple effect in the UK housing

market: Comovement, cyclical subsamples and alternative indices. Urban

Studies. 53(14). pp.3048-3062.

Emerole, G., 2018. Risks and opportunities in emerging markets international real estate

investment: A comparative analysis of Nigeria and South Africa. Journal of the Nigerian

Institution of Estate Surveyors and Valuers. 41(1). pp.71-78.

Fothergill, S. and Houston, D., 2016. Are big cities really the motor of UK regional economic

growth?. Cambridge Journal of Regions, Economy and Society.9(2). pp.319-334.

Harding, A. and et.al., 2018. Supply-side review of the UK specialist housing market and why it

is failing older people. Housing, Care and Support.

Ivanovych, B. A., 2019. Investing in real estate of Great Britain during Brexit. Публічне

урядування. (4 (19)).

Kenny, T., Elliott, T. and Bicquelet-Lock, A., 2018. Better planning for housing affordability:

Three approaches to solving the housing crisis in the UK. Journal of Urban Regeneration

& Renewal.11(3). pp.233-241.

Khan, H., Rouillard, J.F. and Upadhayaya, S., 2019. Consumer Confidence and Household

Investment (No. CEP 19-06).

OMONDI, O.B., 2018. EFFECTS OF MACRO-ECONOMIC VARIABLES ON MORTAGAGE

LOAN UPTAKE (Doctoral dissertation, KENYATTA UNIVERSITY).

Stevens, D. G., 2018. A behavioural data approach towards predicting direct real estate markets

in the United Kingdom (Doctoral dissertation, University of Cambridge).

White, M. and Ke, Q., 2019. Volatility Spillovers and Regional Office Market Connectedness in

the UK (No. eres2019_289). European Real Estate Society (ERES).

Online

12 month percentage change in house prices in the United Kingdom (UK) from July 2007 to July

2019. 2020. [Online]. Available through: <

https://www.statista.com/statistics/751619/house-price-change-uk/ >

UK Housing Market. 2020. [Online]. Available through:

<https://www.economicshelp.org/blog/5709/housing/market/ >

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.