Analysis of the UK Housing Market: 2009-2019 Trends and Factors

VerifiedAdded on 2023/01/11

|13

|3950

|95

Report

AI Summary

This report provides a comprehensive analysis of the UK housing market from 2009 to 2019, examining the changes in average housing prices during this period. It evaluates the economic determinants influencing these changes, including disposable income, interest rates, unemployment, and population. Furthermore, the report explores the government actions and policies implemented within the housing market during the same timeframe. Finally, it predicts the potential impact of the COVID-19 pandemic on the UK housing market. The analysis incorporates data from various sources, such as Halifax, the National Statistics Agency, and Countrywide, to provide a detailed overview of the market dynamics and factors affecting it.

Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

1. Explain the average housing prices in the UK which change over the period from 2009 to

2019.............................................................................................................................................1

2. Evaluate the economic determinants of the changes in the UK housing market price............3

3. Explain the government action over the period from 2009 to 2019 which affect the UK

Housing market............................................................................................................................5

4. Predict what would be the impact of COVID-19 on UK Housing Market.............................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

MAIN BODY..................................................................................................................................1

1. Explain the average housing prices in the UK which change over the period from 2009 to

2019.............................................................................................................................................1

2. Evaluate the economic determinants of the changes in the UK housing market price............3

3. Explain the government action over the period from 2009 to 2019 which affect the UK

Housing market............................................................................................................................5

4. Predict what would be the impact of COVID-19 on UK Housing Market.............................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

The contemporary business environment is highly dynamic, and so dealing with these

challenges calls for innovative strategies that could go above producing a decent product,

appealingly selling it and making available (Amankwah-Amoah, Osabutey and Egbetokun,

2018). Interacting with current and prospective stakeholders and customers is no longer an issue

of luxurious lifestyle, but a make much difference of competitive need. Marketing experts like

Kotler and Keller agree that the role of a communicator and promoter is eventually cast on any

organization. In the advancement of technology, the primary concern is not how to interact but

also what to say, with whom and how many of these. This is where the marketing approach falls

into the frame. This report is based on the UK housing market and changes over the last 10 years.

It covers the several tasks such as changes in the price of UK housing, determinants which affect

the housing sector, what actions taken by the government and what would be the impact of

COVID-19 recently on UK Housing market.

MAIN BODY

1. Explain the average housing prices in the UK which change over the period from 2009 to 2019

The analysis at house prices from the past decade will develop a clear understanding about

how often headline house price estimates are distorted by the city and commuting belt (Average

UK Housing Prices, 2020). London and the South East forced headline real price increases as a

small boom hit the economy in the soon to mid-2010, before reaching down as the economy

tanked from mid 2016. London has seen the maximum amount of house price rises in the

last years where average capital property has risen 72 % more than almost double to the average

UK house price increase of 33.7 per cent. However the capital has shown a noticeable decline in

recent times and housing prices are dropping back from their height in many parts of London

(Appiah And et.al., 2018). The collapses are fairly small as evaluated by the house price index

values, but representatives suggest that residences are selling 5 to 10 % less than in 2015 and

2016.

1

The contemporary business environment is highly dynamic, and so dealing with these

challenges calls for innovative strategies that could go above producing a decent product,

appealingly selling it and making available (Amankwah-Amoah, Osabutey and Egbetokun,

2018). Interacting with current and prospective stakeholders and customers is no longer an issue

of luxurious lifestyle, but a make much difference of competitive need. Marketing experts like

Kotler and Keller agree that the role of a communicator and promoter is eventually cast on any

organization. In the advancement of technology, the primary concern is not how to interact but

also what to say, with whom and how many of these. This is where the marketing approach falls

into the frame. This report is based on the UK housing market and changes over the last 10 years.

It covers the several tasks such as changes in the price of UK housing, determinants which affect

the housing sector, what actions taken by the government and what would be the impact of

COVID-19 recently on UK Housing market.

MAIN BODY

1. Explain the average housing prices in the UK which change over the period from 2009 to 2019

The analysis at house prices from the past decade will develop a clear understanding about

how often headline house price estimates are distorted by the city and commuting belt (Average

UK Housing Prices, 2020). London and the South East forced headline real price increases as a

small boom hit the economy in the soon to mid-2010, before reaching down as the economy

tanked from mid 2016. London has seen the maximum amount of house price rises in the

last years where average capital property has risen 72 % more than almost double to the average

UK house price increase of 33.7 per cent. However the capital has shown a noticeable decline in

recent times and housing prices are dropping back from their height in many parts of London

(Appiah And et.al., 2018). The collapses are fairly small as evaluated by the house price index

values, but representatives suggest that residences are selling 5 to 10 % less than in 2015 and

2016.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

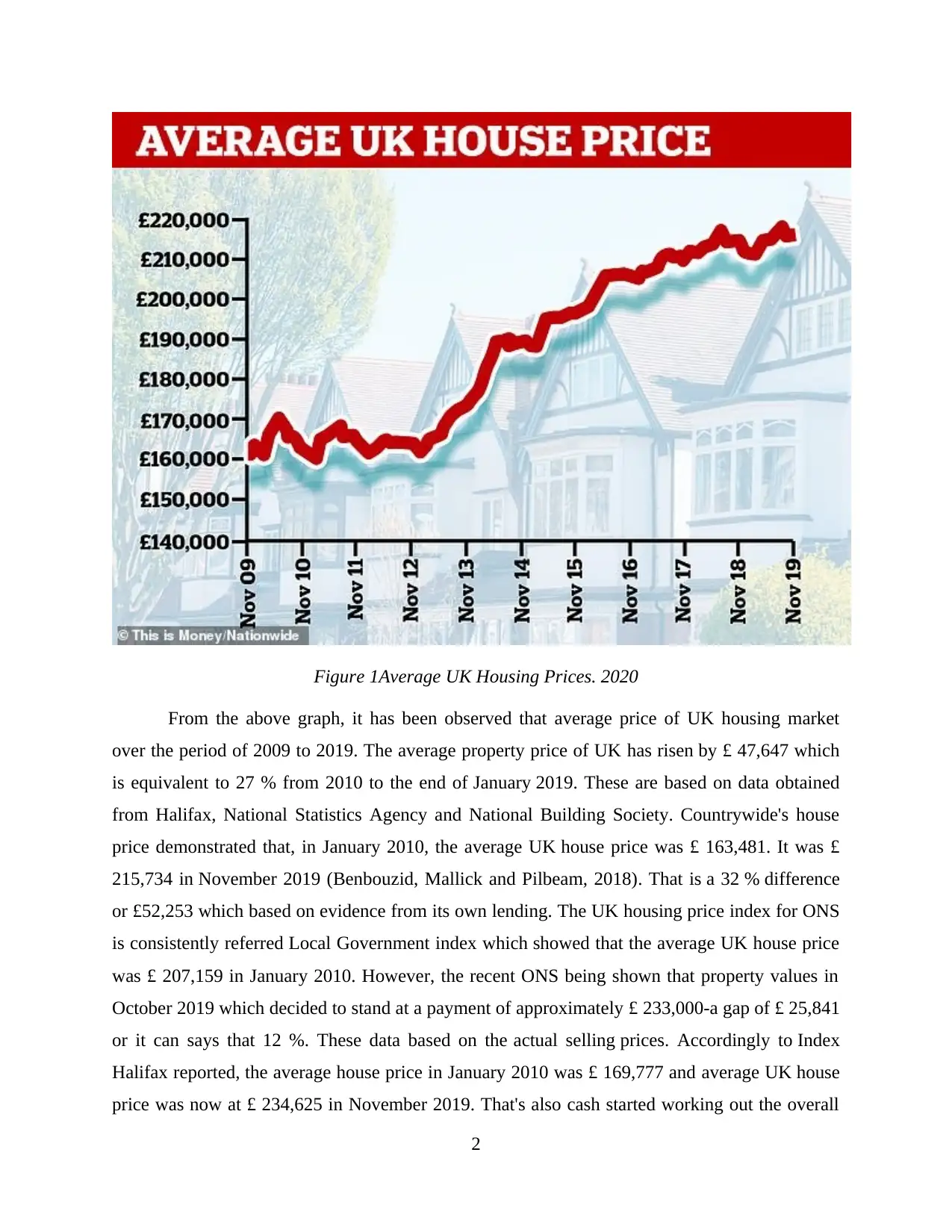

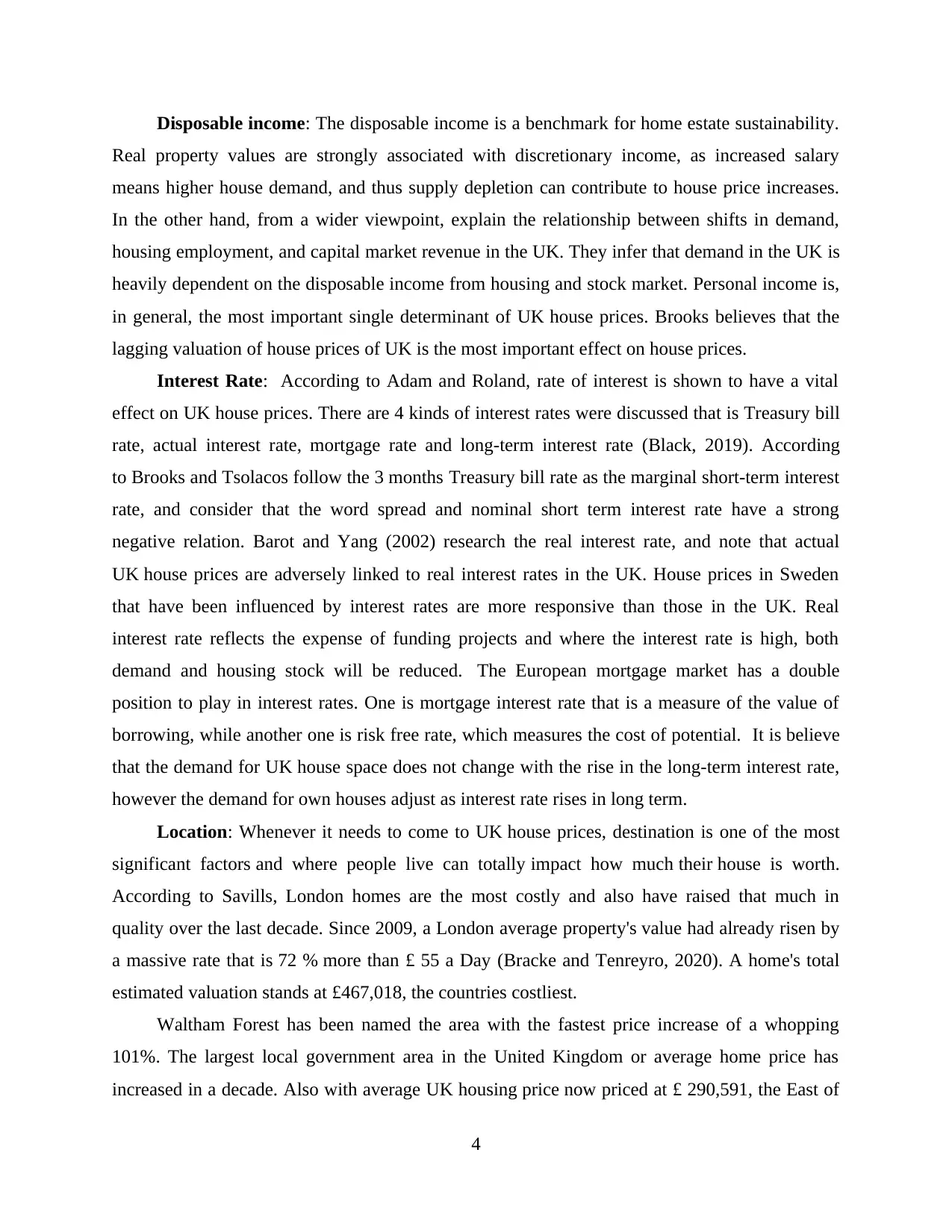

Figure 1Average UK Housing Prices. 2020

From the above graph, it has been observed that average price of UK housing market

over the period of 2009 to 2019. The average property price of UK has risen by £ 47,647 which

is equivalent to 27 % from 2010 to the end of January 2019. These are based on data obtained

from Halifax, National Statistics Agency and National Building Society. Countrywide's house

price demonstrated that, in January 2010, the average UK house price was £ 163,481. It was £

215,734 in November 2019 (Benbouzid, Mallick and Pilbeam, 2018). That is a 32 % difference

or £52,253 which based on evidence from its own lending. The UK housing price index for ONS

is consistently referred Local Government index which showed that the average UK house price

was £ 207,159 in January 2010. However, the recent ONS being shown that property values in

October 2019 which decided to stand at a payment of approximately £ 233,000-a gap of £ 25,841

or it can says that 12 %. These data based on the actual selling prices. Accordingly to Index

Halifax reported, the average house price in January 2010 was £ 169,777 and average UK house

price was now at £ 234,625 in November 2019. That's also cash started working out the overall

2

From the above graph, it has been observed that average price of UK housing market

over the period of 2009 to 2019. The average property price of UK has risen by £ 47,647 which

is equivalent to 27 % from 2010 to the end of January 2019. These are based on data obtained

from Halifax, National Statistics Agency and National Building Society. Countrywide's house

price demonstrated that, in January 2010, the average UK house price was £ 163,481. It was £

215,734 in November 2019 (Benbouzid, Mallick and Pilbeam, 2018). That is a 32 % difference

or £52,253 which based on evidence from its own lending. The UK housing price index for ONS

is consistently referred Local Government index which showed that the average UK house price

was £ 207,159 in January 2010. However, the recent ONS being shown that property values in

October 2019 which decided to stand at a payment of approximately £ 233,000-a gap of £ 25,841

or it can says that 12 %. These data based on the actual selling prices. Accordingly to Index

Halifax reported, the average house price in January 2010 was £ 169,777 and average UK house

price was now at £ 234,625 in November 2019. That's also cash started working out the overall

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

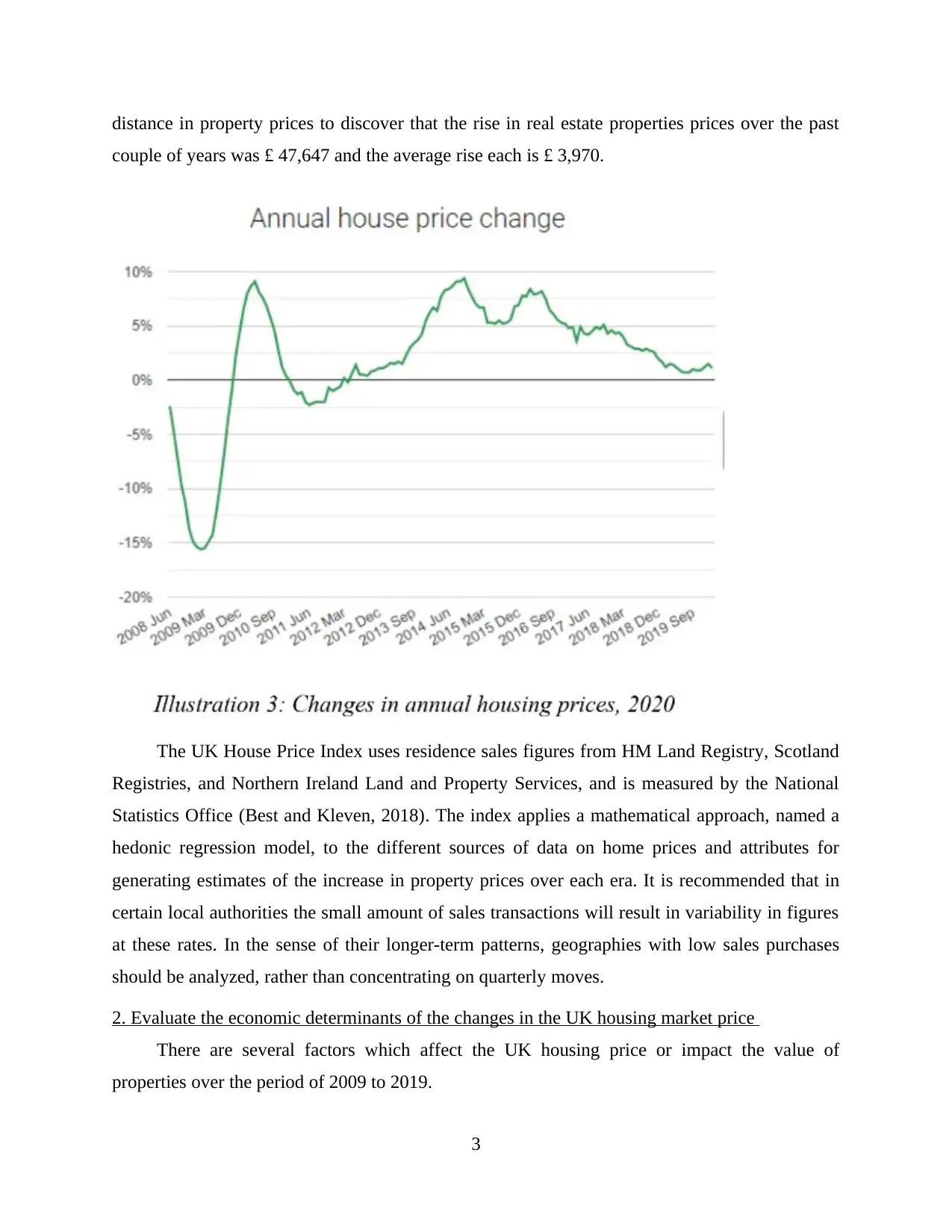

distance in property prices to discover that the rise in real estate properties prices over the past

couple of years was £ 47,647 and the average rise each is £ 3,970.

The UK House Price Index uses residence sales figures from HM Land Registry, Scotland

Registries, and Northern Ireland Land and Property Services, and is measured by the National

Statistics Office (Best and Kleven, 2018). The index applies a mathematical approach, named a

hedonic regression model, to the different sources of data on home prices and attributes for

generating estimates of the increase in property prices over each era. It is recommended that in

certain local authorities the small amount of sales transactions will result in variability in figures

at these rates. In the sense of their longer-term patterns, geographies with low sales purchases

should be analyzed, rather than concentrating on quarterly moves.

2. Evaluate the economic determinants of the changes in the UK housing market price

There are several factors which affect the UK housing price or impact the value of

properties over the period of 2009 to 2019.

3

couple of years was £ 47,647 and the average rise each is £ 3,970.

The UK House Price Index uses residence sales figures from HM Land Registry, Scotland

Registries, and Northern Ireland Land and Property Services, and is measured by the National

Statistics Office (Best and Kleven, 2018). The index applies a mathematical approach, named a

hedonic regression model, to the different sources of data on home prices and attributes for

generating estimates of the increase in property prices over each era. It is recommended that in

certain local authorities the small amount of sales transactions will result in variability in figures

at these rates. In the sense of their longer-term patterns, geographies with low sales purchases

should be analyzed, rather than concentrating on quarterly moves.

2. Evaluate the economic determinants of the changes in the UK housing market price

There are several factors which affect the UK housing price or impact the value of

properties over the period of 2009 to 2019.

3

Disposable income: The disposable income is a benchmark for home estate sustainability.

Real property values are strongly associated with discretionary income, as increased salary

means higher house demand, and thus supply depletion can contribute to house price increases.

In the other hand, from a wider viewpoint, explain the relationship between shifts in demand,

housing employment, and capital market revenue in the UK. They infer that demand in the UK is

heavily dependent on the disposable income from housing and stock market. Personal income is,

in general, the most important single determinant of UK house prices. Brooks believes that the

lagging valuation of house prices of UK is the most important effect on house prices.

Interest Rate: According to Adam and Roland, rate of interest is shown to have a vital

effect on UK house prices. There are 4 kinds of interest rates were discussed that is Treasury bill

rate, actual interest rate, mortgage rate and long-term interest rate (Black, 2019). According

to Brooks and Tsolacos follow the 3 months Treasury bill rate as the marginal short-term interest

rate, and consider that the word spread and nominal short term interest rate have a strong

negative relation. Barot and Yang (2002) research the real interest rate, and note that actual

UK house prices are adversely linked to real interest rates in the UK. House prices in Sweden

that have been influenced by interest rates are more responsive than those in the UK. Real

interest rate reflects the expense of funding projects and where the interest rate is high, both

demand and housing stock will be reduced. The European mortgage market has a double

position to play in interest rates. One is mortgage interest rate that is a measure of the value of

borrowing, while another one is risk free rate, which measures the cost of potential. It is believe

that the demand for UK house space does not change with the rise in the long-term interest rate,

however the demand for own houses adjust as interest rate rises in long term.

Location: Whenever it needs to come to UK house prices, destination is one of the most

significant factors and where people live can totally impact how much their house is worth.

According to Savills, London homes are the most costly and also have raised that much in

quality over the last decade. Since 2009, a London average property's value had already risen by

a massive rate that is 72 % more than £ 55 a Day (Bracke and Tenreyro, 2020). A home's total

estimated valuation stands at £467,018, the countries costliest.

Waltham Forest has been named the area with the fastest price increase of a whopping

101%. The largest local government area in the United Kingdom or average home price has

increased in a decade. Also with average UK housing price now priced at £ 290,591, the East of

4

Real property values are strongly associated with discretionary income, as increased salary

means higher house demand, and thus supply depletion can contribute to house price increases.

In the other hand, from a wider viewpoint, explain the relationship between shifts in demand,

housing employment, and capital market revenue in the UK. They infer that demand in the UK is

heavily dependent on the disposable income from housing and stock market. Personal income is,

in general, the most important single determinant of UK house prices. Brooks believes that the

lagging valuation of house prices of UK is the most important effect on house prices.

Interest Rate: According to Adam and Roland, rate of interest is shown to have a vital

effect on UK house prices. There are 4 kinds of interest rates were discussed that is Treasury bill

rate, actual interest rate, mortgage rate and long-term interest rate (Black, 2019). According

to Brooks and Tsolacos follow the 3 months Treasury bill rate as the marginal short-term interest

rate, and consider that the word spread and nominal short term interest rate have a strong

negative relation. Barot and Yang (2002) research the real interest rate, and note that actual

UK house prices are adversely linked to real interest rates in the UK. House prices in Sweden

that have been influenced by interest rates are more responsive than those in the UK. Real

interest rate reflects the expense of funding projects and where the interest rate is high, both

demand and housing stock will be reduced. The European mortgage market has a double

position to play in interest rates. One is mortgage interest rate that is a measure of the value of

borrowing, while another one is risk free rate, which measures the cost of potential. It is believe

that the demand for UK house space does not change with the rise in the long-term interest rate,

however the demand for own houses adjust as interest rate rises in long term.

Location: Whenever it needs to come to UK house prices, destination is one of the most

significant factors and where people live can totally impact how much their house is worth.

According to Savills, London homes are the most costly and also have raised that much in

quality over the last decade. Since 2009, a London average property's value had already risen by

a massive rate that is 72 % more than £ 55 a Day (Bracke and Tenreyro, 2020). A home's total

estimated valuation stands at £467,018, the countries costliest.

Waltham Forest has been named the area with the fastest price increase of a whopping

101%. The largest local government area in the United Kingdom or average home price has

increased in a decade. Also with average UK housing price now priced at £ 290,591, the East of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

England became the next area to see the highest increase of 57 per cent. With both the average

house price priced at £ 446,167, Cambridge was the place inside the East that has seen the most

development at 77 per cent.

Unemployment rate: The unemployment level reflects economic complexities. It

is consider the rate of unemployment to be a measure of the overall economic situation. There's

been a negative link between the yield on house prices as well as the rate of unemployment.

Expert said that, unemployment rate decreases in housing market boom periods, but the burst in

bubble would contribute to a rapid rise in unemployment rate (Calabrese And et.al., 2018). It

is assumed the increasing unemployment rate would result in faster wage growth and raise

potential income uncertainty. Additionally, individuals prefer to pay closer attention with their

own finances. Unemployment is linked to economic growth, because fewer people will be able

to afford housing when unemployment rises. However, even the threat of unemployment can

deter individuals from joining the housing market. Basically, when the rate of unemployment

increases then demand of UK housing market also reduces people are unable to afford

purchasing houses because they are jobless.

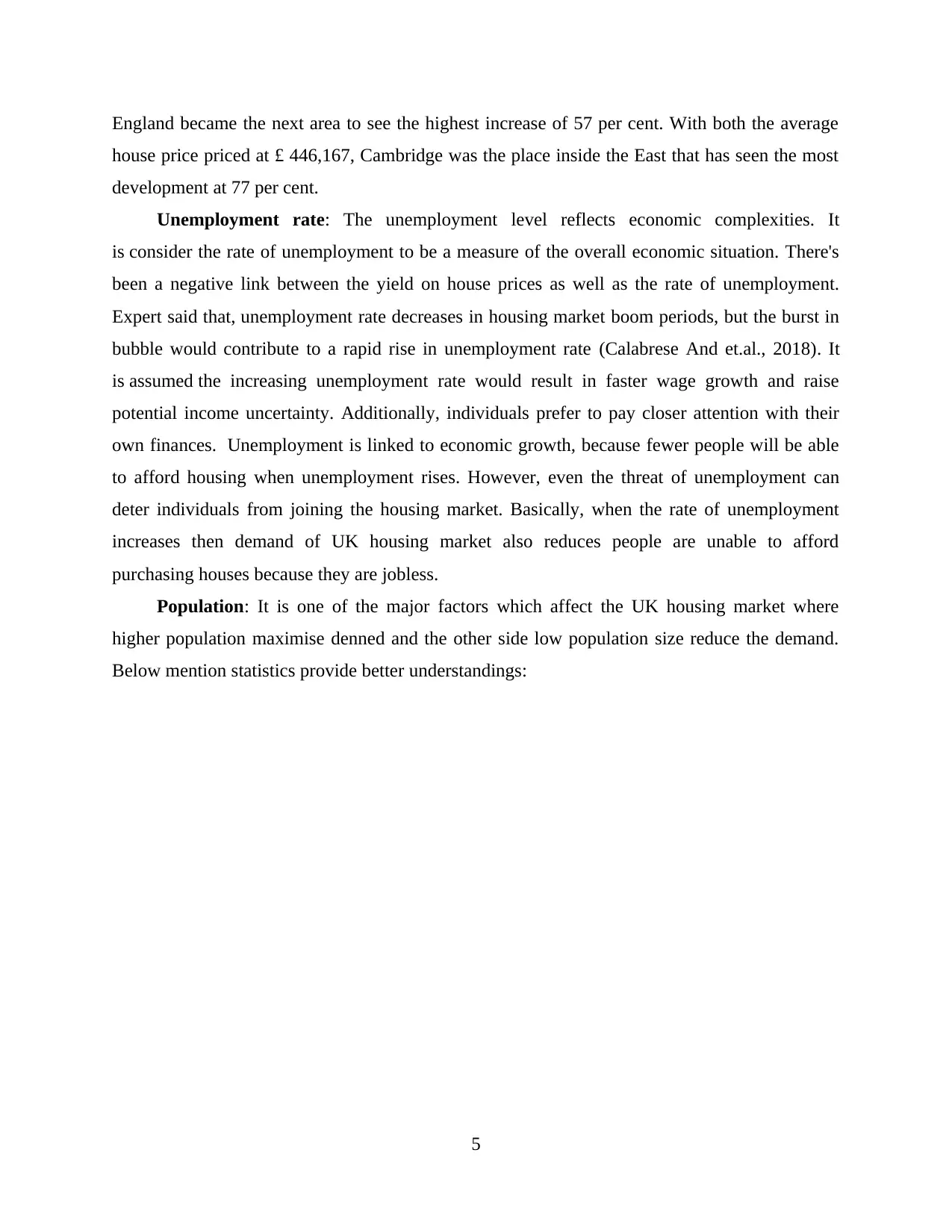

Population: It is one of the major factors which affect the UK housing market where

higher population maximise denned and the other side low population size reduce the demand.

Below mention statistics provide better understandings:

5

house price priced at £ 446,167, Cambridge was the place inside the East that has seen the most

development at 77 per cent.

Unemployment rate: The unemployment level reflects economic complexities. It

is consider the rate of unemployment to be a measure of the overall economic situation. There's

been a negative link between the yield on house prices as well as the rate of unemployment.

Expert said that, unemployment rate decreases in housing market boom periods, but the burst in

bubble would contribute to a rapid rise in unemployment rate (Calabrese And et.al., 2018). It

is assumed the increasing unemployment rate would result in faster wage growth and raise

potential income uncertainty. Additionally, individuals prefer to pay closer attention with their

own finances. Unemployment is linked to economic growth, because fewer people will be able

to afford housing when unemployment rises. However, even the threat of unemployment can

deter individuals from joining the housing market. Basically, when the rate of unemployment

increases then demand of UK housing market also reduces people are unable to afford

purchasing houses because they are jobless.

Population: It is one of the major factors which affect the UK housing market where

higher population maximise denned and the other side low population size reduce the demand.

Below mention statistics provide better understandings:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above statistics it is observed that, in the upcoming years population of England

going to increase which is an opportunity for the Housing market because it maximise the

demand of houses. Before 2009, population was below 55000 and it is predicted that till 2041 it

will be more than 60000.

Supply: A reduction in supply drives up prices of UK housing sector and another side

excess supply would drive down prices. For example, an approximate 700,000 new houses were

constructed in the Irish property boom from 1996-2006. Whenever the property market crashed,

a structural oversupply existed to the market. UK Housing prices hit 15 per cent, and prices are

falling with production increasing demand. Housing supply, by comparison, slipped behind

demand in the UK. Prices of UK housing did not plunge as high as they did in Ireland with a

shortage and quickly recovered because of continuing credit crisis. Housing supply relies on

available supply and building of new houses. Housing supply appears to be very inelastic, since

it is a time consuming process to really get construction permits to build the houses. Intervals of

house price rises may well not cause an equal increase in supply, particularly in countries like the

UK, with restricted home building property.

6

going to increase which is an opportunity for the Housing market because it maximise the

demand of houses. Before 2009, population was below 55000 and it is predicted that till 2041 it

will be more than 60000.

Supply: A reduction in supply drives up prices of UK housing sector and another side

excess supply would drive down prices. For example, an approximate 700,000 new houses were

constructed in the Irish property boom from 1996-2006. Whenever the property market crashed,

a structural oversupply existed to the market. UK Housing prices hit 15 per cent, and prices are

falling with production increasing demand. Housing supply, by comparison, slipped behind

demand in the UK. Prices of UK housing did not plunge as high as they did in Ireland with a

shortage and quickly recovered because of continuing credit crisis. Housing supply relies on

available supply and building of new houses. Housing supply appears to be very inelastic, since

it is a time consuming process to really get construction permits to build the houses. Intervals of

house price rises may well not cause an equal increase in supply, particularly in countries like the

UK, with restricted home building property.

6

UK housing sector fluctuates annually because of the uncertainty of the state's

economic situation, contraction accompanied by unemployment, demographic and so on

(Kasemsap, 2018). Interest rate and inflation rate are the most important to bring about

improvement in the housing sector. Rising unemployment, attrition, less earnings, increase in

income tax, banks’ strict regulations is the factors that would cause the housing market to crash.

Although the economy is shown in phase of care, some analysts still think it could be just a

temporary phenomenon. It means the economy seems to rebound and yet is not over in actual

credit crunch. Employment in the UK is still rising, that means they truly can't be enough

resources to invest in real estate in pockets. The global crisis prompted the United Kingdom

government to implement stricter immigration measures. It has consequently reduced the UK’s

incoming arrivals and demand for houses is not growing.

3. Explain the government action over the period from 2009 to 2019 which affect the UK

Housing market

There are several actions taken by the government through making polices from 2009 to

2019 in context of UK housing market. Some of them are as follow:

Net garden cities: Building new towns, in Milton Keynes' style, that allows a substantial

rise in UK housing market. Now there are proposals for a new settlement in Ebbsfleet, Kent

with high speed railway line to London. However, it will take quite a long time from making

plans to completing this. This also involves building on green space land, which can raise

objections.

Government subsidies: Extra government expenditure to subsidize 'social' housing supply

could greatly boost production (Nam, Lee Lee, 2019). Council homes has gone down out of

fashion at the moment in the last decades as the govt has attempted to sell off council homes and

cut back on council housing building. But, in the post-war era, it was council houses that gave a

major boost to UK housing stock. High the government spending encourages the people to

demand more and lower the spending discourages them.

Planning restrictions: Restrictions on planning in the UK are very rigid. Easing the lot of

regulations and trying to make the production more elastic will find things simpler for the

contractors. This may mean a reduction of the amount in secure greenbelt property. This may

also include simplifying the laws that home-builders would comply with. It can lead to

significant local concerns as people are protesting about the increased construction,

7

economic situation, contraction accompanied by unemployment, demographic and so on

(Kasemsap, 2018). Interest rate and inflation rate are the most important to bring about

improvement in the housing sector. Rising unemployment, attrition, less earnings, increase in

income tax, banks’ strict regulations is the factors that would cause the housing market to crash.

Although the economy is shown in phase of care, some analysts still think it could be just a

temporary phenomenon. It means the economy seems to rebound and yet is not over in actual

credit crunch. Employment in the UK is still rising, that means they truly can't be enough

resources to invest in real estate in pockets. The global crisis prompted the United Kingdom

government to implement stricter immigration measures. It has consequently reduced the UK’s

incoming arrivals and demand for houses is not growing.

3. Explain the government action over the period from 2009 to 2019 which affect the UK

Housing market

There are several actions taken by the government through making polices from 2009 to

2019 in context of UK housing market. Some of them are as follow:

Net garden cities: Building new towns, in Milton Keynes' style, that allows a substantial

rise in UK housing market. Now there are proposals for a new settlement in Ebbsfleet, Kent

with high speed railway line to London. However, it will take quite a long time from making

plans to completing this. This also involves building on green space land, which can raise

objections.

Government subsidies: Extra government expenditure to subsidize 'social' housing supply

could greatly boost production (Nam, Lee Lee, 2019). Council homes has gone down out of

fashion at the moment in the last decades as the govt has attempted to sell off council homes and

cut back on council housing building. But, in the post-war era, it was council houses that gave a

major boost to UK housing stock. High the government spending encourages the people to

demand more and lower the spending discourages them.

Planning restrictions: Restrictions on planning in the UK are very rigid. Easing the lot of

regulations and trying to make the production more elastic will find things simpler for the

contractors. This may mean a reduction of the amount in secure greenbelt property. This may

also include simplifying the laws that home-builders would comply with. It can lead to

significant local concerns as people are protesting about the increased construction,

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

overcrowding and loss of green regions. Another option will be to include funds to make

deselected brown field areas new homes.

Monetary policies: Some of the expertise suggested that, it’s the obligation of the Bank of

England to simplify house prices. This may include rising interest rates in order to prevent loan

having taken-out (Nikitina and Lapiņa, 2019). Nevertheless, the Bank of England is mainly

responsible for market and economic development. It is not monetary policy that is designed to

capture the housing market. When the Bank of England wants to raise housing prices, it may

interfere with the economic growth.

In the future, UK home prices are expected to increase by an average of 15.3 % in the next

5 years that is only 1% in 2020. There are also major geographical variations expected to occur.

According to Savills, they announced its projections for the periods up to 2024 and estimated

that Yorkshire as well as the Humber will have the highest increase of 21.6 per cent, due to the

power and flexibility of the national economy and the potential for higher loans to repay income.

The property agents has indicated the North would surpass South in the broader UK housing

market with both the North West projection predicted to see the highest 24 percent price increase

among 2020 and 2024.

Core central London assets are poised for a 20 % growth turnaround, while Greater

London is projected to see development of 4 % in the next 5 years. Notwithstanding worries over

Brexit, the impact on the economy is just like to short term, with rates set to increase in line with

earnings soon after as per Savills reports.

Government take all the necessary actions which are beneficial for the entire economy as

well as for UK housing market. Government spending, interest rate, restriction on planning for

construction, subsidy etc. all are provided to the people to encourage them to buy houses but due

to current circumstances where country survive from the large downturn that is Coviod-19 which

affect the entire economy of world.

4. Predict what would be the impact of COVID-19 on UK Housing Market

The Brexit and political impasse were the main issues across the UK for many years. But

now COVID-19 or corona virus may pose a new challenge. The world financial markets have

now been placed on their rockiest declining trend in decades. Many of those concerned with

long-term perspectives on the property sector have been undeterred throughout (Impact of

COVID-19 on UK Housing Market, 2020). Yet, since December, even more unwilling home

8

deselected brown field areas new homes.

Monetary policies: Some of the expertise suggested that, it’s the obligation of the Bank of

England to simplify house prices. This may include rising interest rates in order to prevent loan

having taken-out (Nikitina and Lapiņa, 2019). Nevertheless, the Bank of England is mainly

responsible for market and economic development. It is not monetary policy that is designed to

capture the housing market. When the Bank of England wants to raise housing prices, it may

interfere with the economic growth.

In the future, UK home prices are expected to increase by an average of 15.3 % in the next

5 years that is only 1% in 2020. There are also major geographical variations expected to occur.

According to Savills, they announced its projections for the periods up to 2024 and estimated

that Yorkshire as well as the Humber will have the highest increase of 21.6 per cent, due to the

power and flexibility of the national economy and the potential for higher loans to repay income.

The property agents has indicated the North would surpass South in the broader UK housing

market with both the North West projection predicted to see the highest 24 percent price increase

among 2020 and 2024.

Core central London assets are poised for a 20 % growth turnaround, while Greater

London is projected to see development of 4 % in the next 5 years. Notwithstanding worries over

Brexit, the impact on the economy is just like to short term, with rates set to increase in line with

earnings soon after as per Savills reports.

Government take all the necessary actions which are beneficial for the entire economy as

well as for UK housing market. Government spending, interest rate, restriction on planning for

construction, subsidy etc. all are provided to the people to encourage them to buy houses but due

to current circumstances where country survive from the large downturn that is Coviod-19 which

affect the entire economy of world.

4. Predict what would be the impact of COVID-19 on UK Housing Market

The Brexit and political impasse were the main issues across the UK for many years. But

now COVID-19 or corona virus may pose a new challenge. The world financial markets have

now been placed on their rockiest declining trend in decades. Many of those concerned with

long-term perspectives on the property sector have been undeterred throughout (Impact of

COVID-19 on UK Housing Market, 2020). Yet, since December, even more unwilling home

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

buyers, delivery people and real estate developers have had much more confidence to move

ahead. It is expressed in a number of house price indexes, all of which have reported house price

and payment growth. In reality, December was the first month any area in the country witnessed

house prices rising. The country's expects says in the case of corona virus to peak in few weeks '

time that is an incredibly limited time frame in any market. Given that perhaps the world is

working difficult to obtain solutions and a disease antidote, the hope would be that the impact on

consumer interest will be equally short-lived. Any areas of the industry may be impacted on a

short-term, granulated basis. For starters, some peoples suffering from finances due to corona

virus, which might slow down their individual growth.

In Amsterdam and Paris, home prices and rents during past epidemics showed only fairly

short-lived and scattered declines in house prices and lower impacts on rental costs than incomes

(Rosenbach, 2018). While it is helpful, they are careful about attempting to derive clear

conclusions from these past examples: not least so because magnitude of the lockdown and

destruction now is stronger. COVID-19 is a real pandemic which simultaneously affects the

entire interrelated world economy. In fact, despite the naturally reduced risk of fatality, new

scientific awareness of illness transmission together with stronger social focus on saving lives.

This indicates much smaller mortality rates from COVID-19 than with the Paris-19th-

century Black Death or cholera outbreak with significantly greater economic effects. Besides the

use of simple analytical techniques, it is potentially also necessary to look only at impacts

on short term (over the next six to nine months); the moderate term (up to around 2024); and the

long term (over the next ten years). The more doubt adds to one's expectations the more one

stares intently. Nevertheless, humans’re trying to do our bit.

Although there is enormous uncertainty regarding the COVID-19 downturn, one thing is for

sure: it is probable to have long term effects on both housing prices and housing schemes in UK

(Wijburg, 2019). In the short and medium term, real house prices (and rents) may decline,

without solution is generated less inexpensive. For the children including those on lower incomes

people, especially in London and the South East, but for other people and industries hit the

hardest by COVID-19 where it will remain impossible to afford. When it comes to housing

policies, it should be prudent for politicians (of all colours) not to get on the nationalist band-

wagon.

9

ahead. It is expressed in a number of house price indexes, all of which have reported house price

and payment growth. In reality, December was the first month any area in the country witnessed

house prices rising. The country's expects says in the case of corona virus to peak in few weeks '

time that is an incredibly limited time frame in any market. Given that perhaps the world is

working difficult to obtain solutions and a disease antidote, the hope would be that the impact on

consumer interest will be equally short-lived. Any areas of the industry may be impacted on a

short-term, granulated basis. For starters, some peoples suffering from finances due to corona

virus, which might slow down their individual growth.

In Amsterdam and Paris, home prices and rents during past epidemics showed only fairly

short-lived and scattered declines in house prices and lower impacts on rental costs than incomes

(Rosenbach, 2018). While it is helpful, they are careful about attempting to derive clear

conclusions from these past examples: not least so because magnitude of the lockdown and

destruction now is stronger. COVID-19 is a real pandemic which simultaneously affects the

entire interrelated world economy. In fact, despite the naturally reduced risk of fatality, new

scientific awareness of illness transmission together with stronger social focus on saving lives.

This indicates much smaller mortality rates from COVID-19 than with the Paris-19th-

century Black Death or cholera outbreak with significantly greater economic effects. Besides the

use of simple analytical techniques, it is potentially also necessary to look only at impacts

on short term (over the next six to nine months); the moderate term (up to around 2024); and the

long term (over the next ten years). The more doubt adds to one's expectations the more one

stares intently. Nevertheless, humans’re trying to do our bit.

Although there is enormous uncertainty regarding the COVID-19 downturn, one thing is for

sure: it is probable to have long term effects on both housing prices and housing schemes in UK

(Wijburg, 2019). In the short and medium term, real house prices (and rents) may decline,

without solution is generated less inexpensive. For the children including those on lower incomes

people, especially in London and the South East, but for other people and industries hit the

hardest by COVID-19 where it will remain impossible to afford. When it comes to housing

policies, it should be prudent for politicians (of all colours) not to get on the nationalist band-

wagon.

9

There has to be a legislative response that reflects the real factors rather than the

manifestations of the economic crisis and the long-term solutions which are the best way to

really address our housing problems. They need to know from Germany, not just from successful

COVID-19 research but also from the community housing strategies.

CONCLUSION

From the above discussion it has been observed that in context of organization, there are

several factors which affect the entire market as well as economy. UK housing market face many

fluctuations over the period and between these time frame governments take several actions to

balance the market flow. There are some determinates as well which affect the housing price of

UK throughout the period.

10

manifestations of the economic crisis and the long-term solutions which are the best way to

really address our housing problems. They need to know from Germany, not just from successful

COVID-19 research but also from the community housing strategies.

CONCLUSION

From the above discussion it has been observed that in context of organization, there are

several factors which affect the entire market as well as economy. UK housing market face many

fluctuations over the period and between these time frame governments take several actions to

balance the market flow. There are some determinates as well which affect the housing price of

UK throughout the period.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.