Evaluating Trends & Development in UK Oil & Gas Industries Market

VerifiedAdded on 2023/04/21

|15

|2957

|216

Report

AI Summary

This report provides an overview of the UK retail petroleum market, focusing on the changes and trends impacting its supply chain. It examines the shift from vertically integrated supply chains to more decomposed and outsourced networks. The report highlights the changes in ownership structures, including the growth of hypermarkets and the exit of fuel suppliers. It also discusses the impact of changing demand for petrol and diesel, and the strategies companies have adopted to adapt. The report also touches upon the upstream supply chain and the reasons behind major oil companies divesting from downstream operations. The study uses data and statistics to illustrate the changes in the UK petroleum market.

Development in

oil and gas

industries

1

oil and gas

industries

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction .....................................................................................................................................3

Downstream supply chain of petroleum market .........................................................................4

Change in ownership structures...................................................................................................5

Growth in hypermarkets..............................................................................................................7

Exit of fuel suppliers....................................................................................................................7

Upstream supply chain of petroleum market ..............................................................................9

Conclusion ......................................................................................................................................9

References......................................................................................................................................11

2

Introduction .....................................................................................................................................3

Downstream supply chain of petroleum market .........................................................................4

Change in ownership structures...................................................................................................5

Growth in hypermarkets..............................................................................................................7

Exit of fuel suppliers....................................................................................................................7

Upstream supply chain of petroleum market ..............................................................................9

Conclusion ......................................................................................................................................9

References......................................................................................................................................11

2

ILLUSTRATION INDEX

Illustration 1: UK petrol stations, number of cars registered and average number of cars per

petrol station ....................................................................................................................................4

Illustration 2: Number of PFS and their percentage breakdown over the years..............................7

Illustration 3: Fuel sales, number of petrol stations and average volume of fuel sold per petrol

station ............................................................................................................................................10

3

Illustration 1: UK petrol stations, number of cars registered and average number of cars per

petrol station ....................................................................................................................................4

Illustration 2: Number of PFS and their percentage breakdown over the years..............................7

Illustration 3: Fuel sales, number of petrol stations and average volume of fuel sold per petrol

station ............................................................................................................................................10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INDEX OF TABLES

Table 1: Number of PFS by considering its ownership structure....................................................7

4

Table 1: Number of PFS by considering its ownership structure....................................................7

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

UK retail petroleum market can be defined as industry that works according to sales of

transportation and fuel used in transportation sector (i.e. diesel and petrol) to the business entities

and consumers through petrol filling stations network of the country (Brookes, Altinay and

Ringham, 2014). This sector is continuously expanding and facing severe changes in various

significant aspects such as demand drivers, retailers, PFS proximity and their functional

activities. Present study focuses on evaluation of various trends that impacts the working of UK

petroleum sector and its supply chain. For this aspect, supply chain in retail petroleum market

will be discussed by considering changes occurred in this industry. Further, implications will be

evaluated on the basis of UK statistics.

Application of diverse trends and changes that impacts the working of UK petroleum retail

market

The road transport fuels markets had attained substantial growth in the last decade while

there is significant reduction in the petrol filling stations. This sector had faced continuous

change due to structural change driven by the market forces and variation in consumer behavior

and their purchase decisions.

5

UK retail petroleum market can be defined as industry that works according to sales of

transportation and fuel used in transportation sector (i.e. diesel and petrol) to the business entities

and consumers through petrol filling stations network of the country (Brookes, Altinay and

Ringham, 2014). This sector is continuously expanding and facing severe changes in various

significant aspects such as demand drivers, retailers, PFS proximity and their functional

activities. Present study focuses on evaluation of various trends that impacts the working of UK

petroleum sector and its supply chain. For this aspect, supply chain in retail petroleum market

will be discussed by considering changes occurred in this industry. Further, implications will be

evaluated on the basis of UK statistics.

Application of diverse trends and changes that impacts the working of UK petroleum retail

market

The road transport fuels markets had attained substantial growth in the last decade while

there is significant reduction in the petrol filling stations. This sector had faced continuous

change due to structural change driven by the market forces and variation in consumer behavior

and their purchase decisions.

5

In accordance with the retail market survey, in late 1960 various petrol stations has been

demolished that has impacted overall working. It is because, organizations were required to pay

high fixed cost and there was low business margins. As a consequence, high volume was

required to attain the break even point (Santos and Svensson, 2013). Various independent

forecourts were not able to attain the desired volumes mainly at the remote locations. In addition

to this, organizations have to compete with the large entities due to which they were not able to

maintain competitive price in market and sell of fuel has also reduced. These factors had created

various barriers for the survival of small firm and henceforth they have to exit from the market.

As per the study of Energy Institute’s Retail Marketing Survey 2007 and 2012, the fueling

position in the UK has been increased due to reduction in PFS.

In present era, various firms are offering self services at the petrol station so they can

make huge saving in labor costs (Shuen, Feiler and Teece, 2014). By this strategy there were

able to attain cost advantage in comparison to the small petrol stations. Closure of PFS had made

reduction in the storage capacity of these stations. Due to this aspect, there is detrimental impact

6

Illustration 1: Ratio of cars registered and visit of cars at petrol stations

(Source: Study of UK petroleum market, 2012)

demolished that has impacted overall working. It is because, organizations were required to pay

high fixed cost and there was low business margins. As a consequence, high volume was

required to attain the break even point (Santos and Svensson, 2013). Various independent

forecourts were not able to attain the desired volumes mainly at the remote locations. In addition

to this, organizations have to compete with the large entities due to which they were not able to

maintain competitive price in market and sell of fuel has also reduced. These factors had created

various barriers for the survival of small firm and henceforth they have to exit from the market.

As per the study of Energy Institute’s Retail Marketing Survey 2007 and 2012, the fueling

position in the UK has been increased due to reduction in PFS.

In present era, various firms are offering self services at the petrol station so they can

make huge saving in labor costs (Shuen, Feiler and Teece, 2014). By this strategy there were

able to attain cost advantage in comparison to the small petrol stations. Closure of PFS had made

reduction in the storage capacity of these stations. Due to this aspect, there is detrimental impact

6

Illustration 1: Ratio of cars registered and visit of cars at petrol stations

(Source: Study of UK petroleum market, 2012)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

on resilience as overall stock was reduced in the available network. However, reduction in PFS

also make improvement in resilience as issue of short-term disruptions to supply. Although

impact of improvement is comparative low, because on site capacity tends to be limited that

indicates that the logistical challenges also need to be considered as critical aspect.

Downstream supply chain of petroleum market

UK petroleum retail market is considered as one of essential section that holds high ratio

of downstream oil market. In this, businesses are referring various elements that improves supply

chain and PFS system. Example of these key elements is domestic refineries, primary and

secondary distribution infrastructure, vehicle tanks and PFS retailers. In this segment, there have

been various changes in last 30 to 40 years. Initially in the 1960s, there was vertically integrated

supply chain and there are almost 19 refineries in the UK market (Thorogood and Younger,

2015). In addition to this, all the companies were part of PFS inclusive of organization having

ownership of refining assets. However, in the year 1970 these companies had to reassess their

cost based for the reduction of prices. As a consequence, there was duplication of network for the

organization that does not require own distribution terminals. Through this strategy, a cost

effective approach has been developed for reducing these terminals and to make optimum

utilization of available resources (Neumann and von Hirschhausen, 2015). This aspect has led to

development of partnerships and exchanges between oil companies. It is because; companies

operating in this sector were engaged in exchange of petroleum product for reducing distribution

cost.

Retailing companies in this sector had also improved the distribution system of fuel

products through assistance of logistic arrangements. For attaining this objective oil companies

had availed ownership of fleets of road tankers and direct recruitments were done for the drivers.

In addition to this, there was considerable decomposition in fuel supply chain because of

rationalization of storage minerals, exit of major players from refining and outsourcing of the

network that helps in fuel distribution by road(Day, Hall and Yánez-Arancibia, 2014). As a

consequence, supply chain management in retail petroleum had become more effective and

efficient. Effectiveness of supply chain had assisted in reduction of spare capacity in the system

through which resilience is minimized in situation of supply disruptions.

7

also make improvement in resilience as issue of short-term disruptions to supply. Although

impact of improvement is comparative low, because on site capacity tends to be limited that

indicates that the logistical challenges also need to be considered as critical aspect.

Downstream supply chain of petroleum market

UK petroleum retail market is considered as one of essential section that holds high ratio

of downstream oil market. In this, businesses are referring various elements that improves supply

chain and PFS system. Example of these key elements is domestic refineries, primary and

secondary distribution infrastructure, vehicle tanks and PFS retailers. In this segment, there have

been various changes in last 30 to 40 years. Initially in the 1960s, there was vertically integrated

supply chain and there are almost 19 refineries in the UK market (Thorogood and Younger,

2015). In addition to this, all the companies were part of PFS inclusive of organization having

ownership of refining assets. However, in the year 1970 these companies had to reassess their

cost based for the reduction of prices. As a consequence, there was duplication of network for the

organization that does not require own distribution terminals. Through this strategy, a cost

effective approach has been developed for reducing these terminals and to make optimum

utilization of available resources (Neumann and von Hirschhausen, 2015). This aspect has led to

development of partnerships and exchanges between oil companies. It is because; companies

operating in this sector were engaged in exchange of petroleum product for reducing distribution

cost.

Retailing companies in this sector had also improved the distribution system of fuel

products through assistance of logistic arrangements. For attaining this objective oil companies

had availed ownership of fleets of road tankers and direct recruitments were done for the drivers.

In addition to this, there was considerable decomposition in fuel supply chain because of

rationalization of storage minerals, exit of major players from refining and outsourcing of the

network that helps in fuel distribution by road(Day, Hall and Yánez-Arancibia, 2014). As a

consequence, supply chain management in retail petroleum had become more effective and

efficient. Effectiveness of supply chain had assisted in reduction of spare capacity in the system

through which resilience is minimized in situation of supply disruptions.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

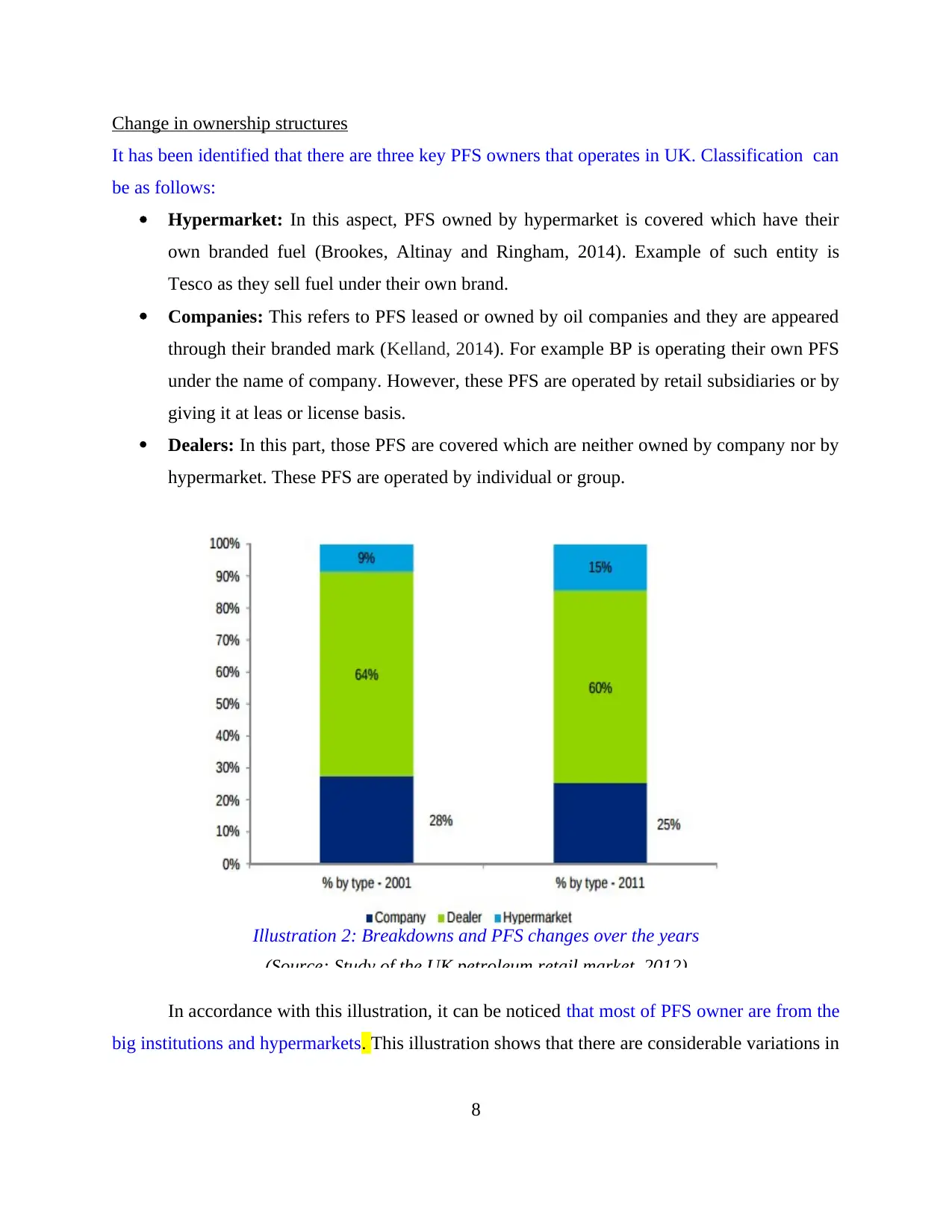

Change in ownership structures

It has been identified that there are three key PFS owners that operates in UK. Classification can

be as follows:

Hypermarket: In this aspect, PFS owned by hypermarket is covered which have their

own branded fuel (Brookes, Altinay and Ringham, 2014). Example of such entity is

Tesco as they sell fuel under their own brand.

Companies: This refers to PFS leased or owned by oil companies and they are appeared

through their branded mark (Kelland, 2014). For example BP is operating their own PFS

under the name of company. However, these PFS are operated by retail subsidiaries or by

giving it at leas or license basis.

Dealers: In this part, those PFS are covered which are neither owned by company nor by

hypermarket. These PFS are operated by individual or group.

In accordance with this illustration, it can be noticed that most of PFS owner are from the

big institutions and hypermarkets. This illustration shows that there are considerable variations in

8

Illustration 2: Breakdowns and PFS changes over the years

(Source: Study of the UK petroleum retail market, 2012)

It has been identified that there are three key PFS owners that operates in UK. Classification can

be as follows:

Hypermarket: In this aspect, PFS owned by hypermarket is covered which have their

own branded fuel (Brookes, Altinay and Ringham, 2014). Example of such entity is

Tesco as they sell fuel under their own brand.

Companies: This refers to PFS leased or owned by oil companies and they are appeared

through their branded mark (Kelland, 2014). For example BP is operating their own PFS

under the name of company. However, these PFS are operated by retail subsidiaries or by

giving it at leas or license basis.

Dealers: In this part, those PFS are covered which are neither owned by company nor by

hypermarket. These PFS are operated by individual or group.

In accordance with this illustration, it can be noticed that most of PFS owner are from the

big institutions and hypermarkets. This illustration shows that there are considerable variations in

8

Illustration 2: Breakdowns and PFS changes over the years

(Source: Study of the UK petroleum retail market, 2012)

declining of PFS by considering its ownership structure (Nejat, Gohari and Majid, 2015). This

aspect can be noticed by following table:

Table 1: Number of PFS by considering its ownership structure

Type of

ownership

2004 2011 % reduction in

PFS ratio during

2004 and 2011

Instant cut down

in PFS ratio

during 2004 and

2011

Organization 3047 2198 -28.00% -849

Merchandiser 6716 5301 -21.00% -1415

Supermarket 1104 1266 15.00% 162

Grand total 10867 8765 -19.00% -2101

According to this table there is significant decline in segment of company and dealer.

Despite of this decline these segments had captured more than 80%. However, fuel sold by these

segments are not in similar proportion because hypermarkets sold 39% of total volume followed

by dealer and company i.e. 33% and 29% respectively (Brookes, Altinay and Ringham, 2014).

These differences shows indicative of variations in the business models. In accordance with the

UK statistics of 2011 hypermarket had sold 11.2 million liters of motor fuel that is four times

higher in comparison to dealers and twice to company.

Growth in hypermarkets

Significant growth was characterized in fuel retailing in the late 1980's where objectives

of PFS were established at hypermarket locations to attract maximum number of customers.

Furthermore, organizations had provided various offers on fuel for increasing sales such as

discounted prices (Benes, Mursula and Selody, 2015). By these promotional strategies,

companies were able to attain good benefits. In addition to this, hypermarkets (ASDA,

Sainsbury, Tesco and Morrisons) were able to attain better margin in comparison to margin

earned by retailing entities.

9

aspect can be noticed by following table:

Table 1: Number of PFS by considering its ownership structure

Type of

ownership

2004 2011 % reduction in

PFS ratio during

2004 and 2011

Instant cut down

in PFS ratio

during 2004 and

2011

Organization 3047 2198 -28.00% -849

Merchandiser 6716 5301 -21.00% -1415

Supermarket 1104 1266 15.00% 162

Grand total 10867 8765 -19.00% -2101

According to this table there is significant decline in segment of company and dealer.

Despite of this decline these segments had captured more than 80%. However, fuel sold by these

segments are not in similar proportion because hypermarkets sold 39% of total volume followed

by dealer and company i.e. 33% and 29% respectively (Brookes, Altinay and Ringham, 2014).

These differences shows indicative of variations in the business models. In accordance with the

UK statistics of 2011 hypermarket had sold 11.2 million liters of motor fuel that is four times

higher in comparison to dealers and twice to company.

Growth in hypermarkets

Significant growth was characterized in fuel retailing in the late 1980's where objectives

of PFS were established at hypermarket locations to attract maximum number of customers.

Furthermore, organizations had provided various offers on fuel for increasing sales such as

discounted prices (Benes, Mursula and Selody, 2015). By these promotional strategies,

companies were able to attain good benefits. In addition to this, hypermarkets (ASDA,

Sainsbury, Tesco and Morrisons) were able to attain better margin in comparison to margin

earned by retailing entities.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In early 1990, there was also change in demand factors as demand of petrol was

continuously decreasing whereas demand of diesel was continuously increasing. Due to this

aspect, suppliers had modified their business strategies to meet the changing demand in market

(Skea, 2014). For this aspect, UK refineries were mainly established for refining of petrol that is

used in vehicles. Moreover, the oil used in heating and power generation has also been refined.

Transformation in demand mix leads to oversupply and enhance export of the UK and fuel

importers got the opportunity for developing product pricing and positioning.

With the changing trends in supply chain organization operating in this industry had

modified their operational tactics for better survival. In this manner, they are able to make

effective utilization of available resources in order to attain their aims and objectives in an

effective manner (Day, Hall and Yánez-Arancibia, 2014). In addition to this, retail players in

hypermarket are able to cope up with the market changes.

Exit of fuel suppliers

Fuel suppliers has been removed from the physical deliveries of fuel as it was undertaken

by road hauliers as they were mainly focused on the labour disputes in the industry. Road

hauliers had pressurized existing firms to cut down the pricing of the goods at supply chain

stages which may lead to various critical dispute situations (Nejat, Gohari and Majid, 2015). Exit

of major organization had motivated organizations for rationalization of networks in order to

satisfy demand in an effective manner. Further, import had provided an additional assistance to

the UK supply system through which developments in supply can be increase as it requires

diversified resources for accomplishment.

10

continuously decreasing whereas demand of diesel was continuously increasing. Due to this

aspect, suppliers had modified their business strategies to meet the changing demand in market

(Skea, 2014). For this aspect, UK refineries were mainly established for refining of petrol that is

used in vehicles. Moreover, the oil used in heating and power generation has also been refined.

Transformation in demand mix leads to oversupply and enhance export of the UK and fuel

importers got the opportunity for developing product pricing and positioning.

With the changing trends in supply chain organization operating in this industry had

modified their operational tactics for better survival. In this manner, they are able to make

effective utilization of available resources in order to attain their aims and objectives in an

effective manner (Day, Hall and Yánez-Arancibia, 2014). In addition to this, retail players in

hypermarket are able to cope up with the market changes.

Exit of fuel suppliers

Fuel suppliers has been removed from the physical deliveries of fuel as it was undertaken

by road hauliers as they were mainly focused on the labour disputes in the industry. Road

hauliers had pressurized existing firms to cut down the pricing of the goods at supply chain

stages which may lead to various critical dispute situations (Nejat, Gohari and Majid, 2015). Exit

of major organization had motivated organizations for rationalization of networks in order to

satisfy demand in an effective manner. Further, import had provided an additional assistance to

the UK supply system through which developments in supply can be increase as it requires

diversified resources for accomplishment.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

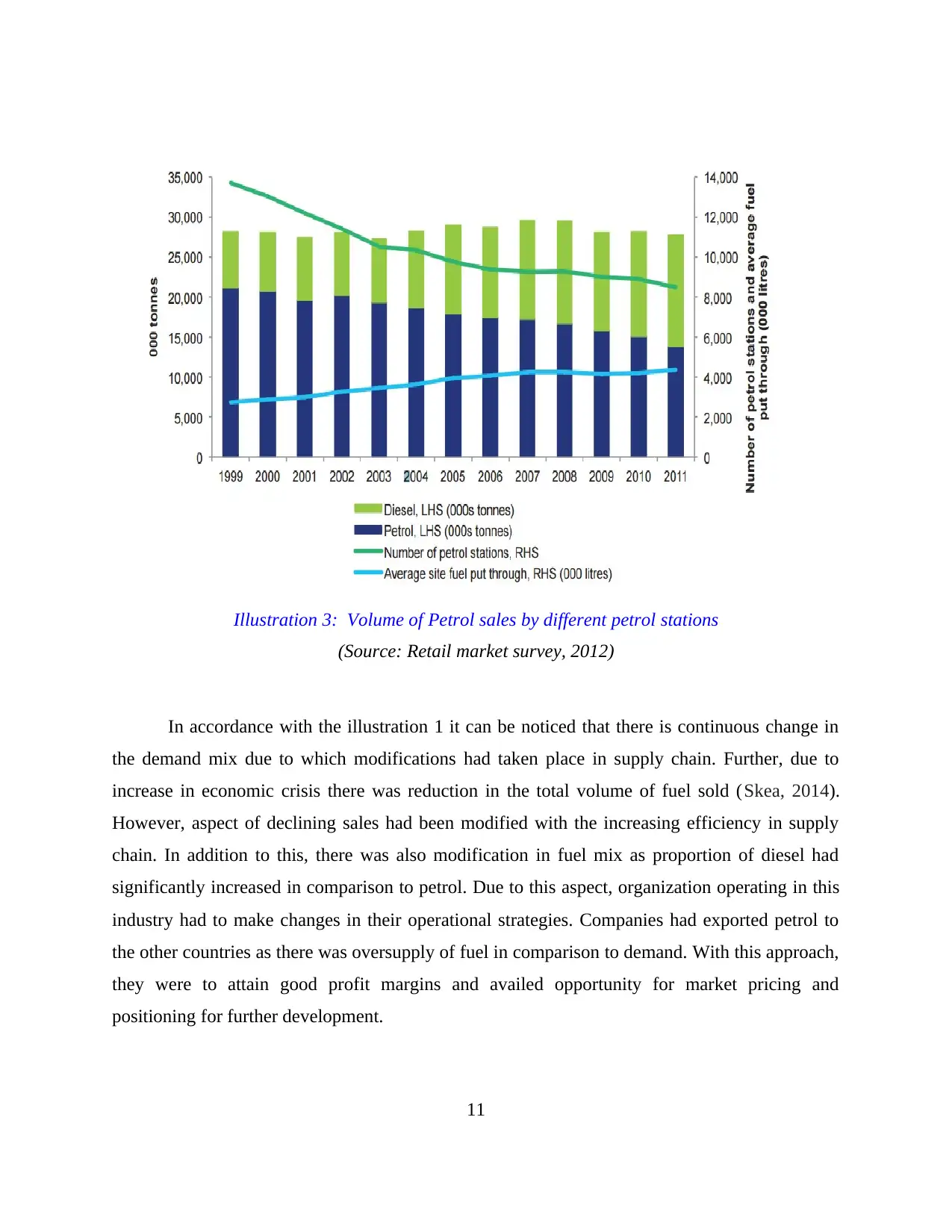

In accordance with the illustration 1 it can be noticed that there is continuous change in

the demand mix due to which modifications had taken place in supply chain. Further, due to

increase in economic crisis there was reduction in the total volume of fuel sold (Skea, 2014).

However, aspect of declining sales had been modified with the increasing efficiency in supply

chain. In addition to this, there was also modification in fuel mix as proportion of diesel had

significantly increased in comparison to petrol. Due to this aspect, organization operating in this

industry had to make changes in their operational strategies. Companies had exported petrol to

the other countries as there was oversupply of fuel in comparison to demand. With this approach,

they were to attain good profit margins and availed opportunity for market pricing and

positioning for further development.

11

Illustration 3: Volume of Petrol sales by different petrol stations

(Source: Retail market survey, 2012)

the demand mix due to which modifications had taken place in supply chain. Further, due to

increase in economic crisis there was reduction in the total volume of fuel sold (Skea, 2014).

However, aspect of declining sales had been modified with the increasing efficiency in supply

chain. In addition to this, there was also modification in fuel mix as proportion of diesel had

significantly increased in comparison to petrol. Due to this aspect, organization operating in this

industry had to make changes in their operational strategies. Companies had exported petrol to

the other countries as there was oversupply of fuel in comparison to demand. With this approach,

they were to attain good profit margins and availed opportunity for market pricing and

positioning for further development.

11

Illustration 3: Volume of Petrol sales by different petrol stations

(Source: Retail market survey, 2012)

By the implementation of above described strategies, hypermarkets were able to make

reduction in their prices and they had replaced traditional PFS owned by independent dealers and

oil companies. Consequently, there was increase in their market share as hypermarkets were

continuously increasing and PFS had declined (Mitchell, 2012). In accordance with this

approach, retail companies started to focus on non-fuel retail options for increasing their

convenience expense and covering cost of operational functions. Several companies had

integrated their operational functions to operate in more effective manner. For this aspect,

example of Esso and Tesco express can be considered.

Upstream supply chain of petroleum market

Upstream supply chain of UK retail petroleum market was also modified along with the

changes in downstream supply chain. Major giants such as Shell and Chervon in this industry

had sold their shares to the retail network. As a consequence, there was change in ownership

structure. These changes were driven mainly by the organizations through seeking higher returns

in the upstream activities in comparison to relative downstream oil activities. Higher returns

from the upstream supply chain had influenced major oil companies to divest to make exit from

the market of downstream oil operations (UKCS Oil and Gas Production Projections, 2015). In

this aspect, number of expansion activities has been performed at different strategic locations

even refineries are not working properly. It is because; these locations are considered as a

potential driver to make investment in import terminals to enhance the volume of fuel imports.

Number of modifications has been made in the ownership structure due to sales aspects

of refining sector. It is because; changes in UK pipelines were limited in comparison to changes

in oil downstream supply chain. Organization such as BP oil UK, Wincanton, Turners had made

increase in efficiencies in deliveries by making use of logistical expertise.

CONCLUSION

In accordance with the present study, it can be concluded that retail petroleum market in

UK had undergone severe changes in last few decades. It is because, there is decrease in PFS due

to which there is change in fragmentation of fuel supply chain from the downstream and

upstream petroleum market. In addition to this, flexibility in supply chain has been increased in

case of domestic refinery supply distributions because of penetration of imported petroleum

products. By this approach, there is also improvement in security and energy resilience.

12

reduction in their prices and they had replaced traditional PFS owned by independent dealers and

oil companies. Consequently, there was increase in their market share as hypermarkets were

continuously increasing and PFS had declined (Mitchell, 2012). In accordance with this

approach, retail companies started to focus on non-fuel retail options for increasing their

convenience expense and covering cost of operational functions. Several companies had

integrated their operational functions to operate in more effective manner. For this aspect,

example of Esso and Tesco express can be considered.

Upstream supply chain of petroleum market

Upstream supply chain of UK retail petroleum market was also modified along with the

changes in downstream supply chain. Major giants such as Shell and Chervon in this industry

had sold their shares to the retail network. As a consequence, there was change in ownership

structure. These changes were driven mainly by the organizations through seeking higher returns

in the upstream activities in comparison to relative downstream oil activities. Higher returns

from the upstream supply chain had influenced major oil companies to divest to make exit from

the market of downstream oil operations (UKCS Oil and Gas Production Projections, 2015). In

this aspect, number of expansion activities has been performed at different strategic locations

even refineries are not working properly. It is because; these locations are considered as a

potential driver to make investment in import terminals to enhance the volume of fuel imports.

Number of modifications has been made in the ownership structure due to sales aspects

of refining sector. It is because; changes in UK pipelines were limited in comparison to changes

in oil downstream supply chain. Organization such as BP oil UK, Wincanton, Turners had made

increase in efficiencies in deliveries by making use of logistical expertise.

CONCLUSION

In accordance with the present study, it can be concluded that retail petroleum market in

UK had undergone severe changes in last few decades. It is because, there is decrease in PFS due

to which there is change in fragmentation of fuel supply chain from the downstream and

upstream petroleum market. In addition to this, flexibility in supply chain has been increased in

case of domestic refinery supply distributions because of penetration of imported petroleum

products. By this approach, there is also improvement in security and energy resilience.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.