AC70046E Tax Systems and Policy: Comprehensive UK Property Taxation

VerifiedAdded on 2022/08/17

|16

|3571

|121

Homework Assignment

AI Summary

This assignment solution delves into the complexities of UK property taxation, addressing various scenarios and calculations relevant to income tax, savings, and investments. The analysis begins with an assessment of Don's IT, evaluating his income under both accrual and cash basis methods, considering property income, discretionary trust income, bank investment income, dividends, and gilt interest. The solution meticulously calculates tax liabilities, incorporating personal allowances, tax rates, and deductions. It then examines Don's income from multiple houses, providing detailed calculations for property business income, including expenses and rent-a-room relief. Furthermore, the assignment explores furnished holiday letting (FHL) regulations, outlining conditions for eligibility, income tax treatments, and capital allowances. It also provides guidance on finance cost treatments for residential properties and the implications of purchasing cottages in Wales. The solution further considers the capital gains tax (CGT) implications of transferring a property portfolio to a company. The assignment utilizes excerpts of regulations and case laws to provide a comprehensive and practical understanding of UK property taxation.

Running head: UK PROPERTY TAXATION

UK Property Taxation

Student Name

Group Number

Module Name

UK Property Taxation

Student Name

Group Number

Module Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

UK PROPERTY TAXATION

Table of Contents

Answer to part A........................................................................................................................2

Answer to part B........................................................................................................................6

Answer to part C(i).....................................................................................................................8

Answer to part C(ii)...................................................................................................................9

Answer to part C(iii)..................................................................................................................9

Answer to part C(iv).................................................................................................................11

References................................................................................................................................13

UK PROPERTY TAXATION

Table of Contents

Answer to part A........................................................................................................................2

Answer to part B........................................................................................................................6

Answer to part C(i).....................................................................................................................8

Answer to part C(ii)...................................................................................................................9

Answer to part C(iii)..................................................................................................................9

Answer to part C(iv).................................................................................................................11

References................................................................................................................................13

2

UK PROPERTY TAXATION

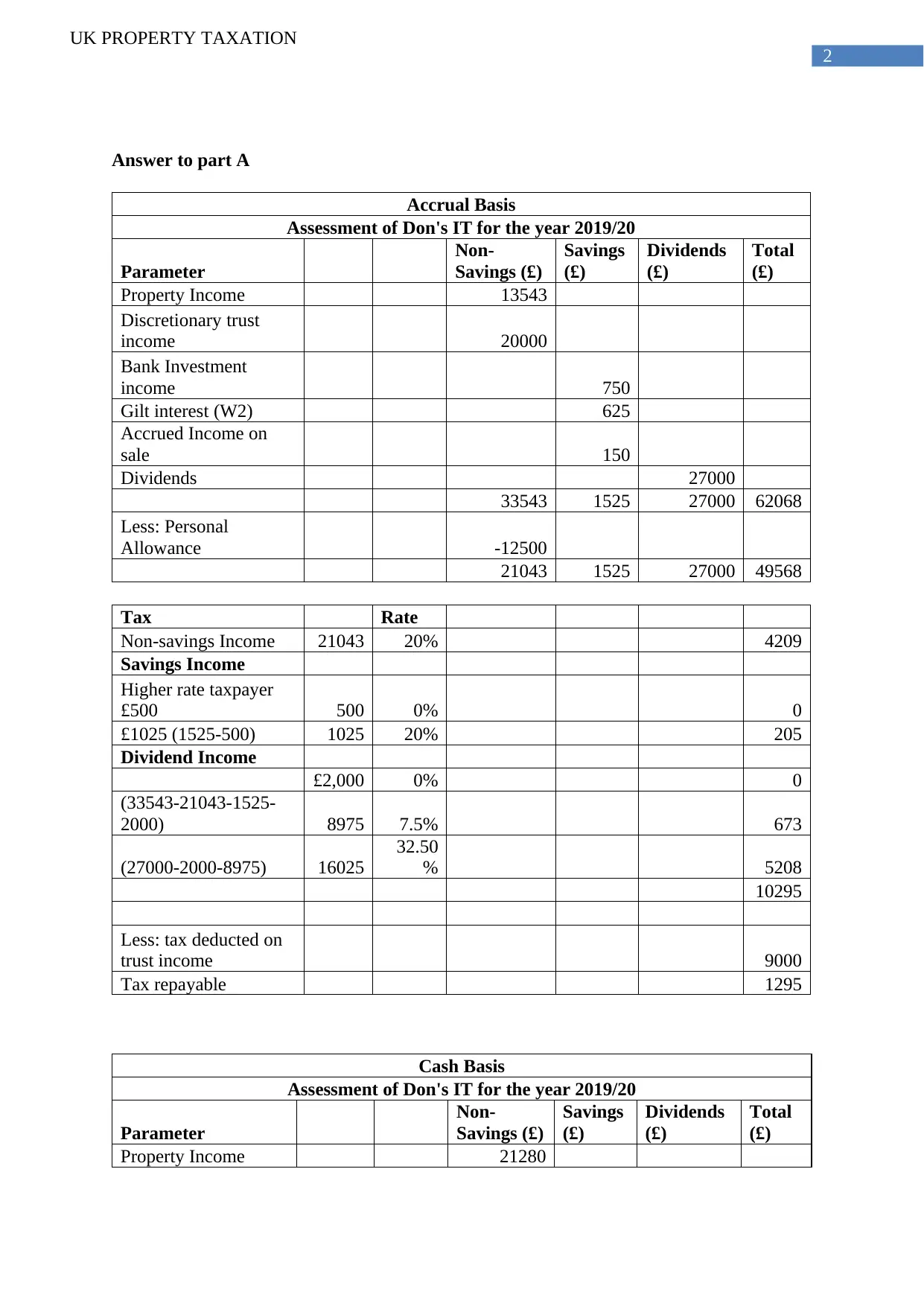

Answer to part A

Accrual Basis

Assessment of Don's IT for the year 2019/20

Parameter

Non-

Savings (£)

Savings

(£)

Dividends

(£)

Total

(£)

Property Income 13543

Discretionary trust

income 20000

Bank Investment

income 750

Gilt interest (W2) 625

Accrued Income on

sale 150

Dividends 27000

33543 1525 27000 62068

Less: Personal

Allowance -12500

21043 1525 27000 49568

Tax Rate

Non-savings Income 21043 20% 4209

Savings Income

Higher rate taxpayer

£500 500 0% 0

£1025 (1525-500) 1025 20% 205

Dividend Income

£2,000 0% 0

(33543-21043-1525-

2000) 8975 7.5% 673

(27000-2000-8975) 16025

32.50

% 5208

10295

Less: tax deducted on

trust income 9000

Tax repayable 1295

Cash Basis

Assessment of Don's IT for the year 2019/20

Parameter

Non-

Savings (£)

Savings

(£)

Dividends

(£)

Total

(£)

Property Income 21280

UK PROPERTY TAXATION

Answer to part A

Accrual Basis

Assessment of Don's IT for the year 2019/20

Parameter

Non-

Savings (£)

Savings

(£)

Dividends

(£)

Total

(£)

Property Income 13543

Discretionary trust

income 20000

Bank Investment

income 750

Gilt interest (W2) 625

Accrued Income on

sale 150

Dividends 27000

33543 1525 27000 62068

Less: Personal

Allowance -12500

21043 1525 27000 49568

Tax Rate

Non-savings Income 21043 20% 4209

Savings Income

Higher rate taxpayer

£500 500 0% 0

£1025 (1525-500) 1025 20% 205

Dividend Income

£2,000 0% 0

(33543-21043-1525-

2000) 8975 7.5% 673

(27000-2000-8975) 16025

32.50

% 5208

10295

Less: tax deducted on

trust income 9000

Tax repayable 1295

Cash Basis

Assessment of Don's IT for the year 2019/20

Parameter

Non-

Savings (£)

Savings

(£)

Dividends

(£)

Total

(£)

Property Income 21280

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

UK PROPERTY TAXATION

Discretionary trust

income 20000

Bank Investment

income 750

Gilt interest (W2) 625

Accrued Income on

sale 150

Dividends 27000

41280 1525 27000 69805

Less: Personal

Allowance -12500

28780 1525 27000 57305

Tax Rate

Non-savings Income 28780 20% 5756

Savings Income

Higher rate taxpayer

£500 500 0% 0

£1025 (1525-500) 1025 20% 205

Dividend Income

£2,000 0% 0

£0 7.5% 0

£27,000 32.50% 8775

14736

Less: tax deducted on

trust income 9000

Tax repayable 5736

Working- Gilt Income £

Total Interest 21-05-2019

(£20,000 x 6% x 6/12) 600

Less: Accrued interest due

to the purchaser -50

550

Total Interest 21-12-2019

(£2500x 6% x 6/12) 75

625

UK PROPERTY TAXATION

Discretionary trust

income 20000

Bank Investment

income 750

Gilt interest (W2) 625

Accrued Income on

sale 150

Dividends 27000

41280 1525 27000 69805

Less: Personal

Allowance -12500

28780 1525 27000 57305

Tax Rate

Non-savings Income 28780 20% 5756

Savings Income

Higher rate taxpayer

£500 500 0% 0

£1025 (1525-500) 1025 20% 205

Dividend Income

£2,000 0% 0

£0 7.5% 0

£27,000 32.50% 8775

14736

Less: tax deducted on

trust income 9000

Tax repayable 5736

Working- Gilt Income £

Total Interest 21-05-2019

(£20,000 x 6% x 6/12) 600

Less: Accrued interest due

to the purchaser -50

550

Total Interest 21-12-2019

(£2500x 6% x 6/12) 75

625

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

UK PROPERTY TAXATION

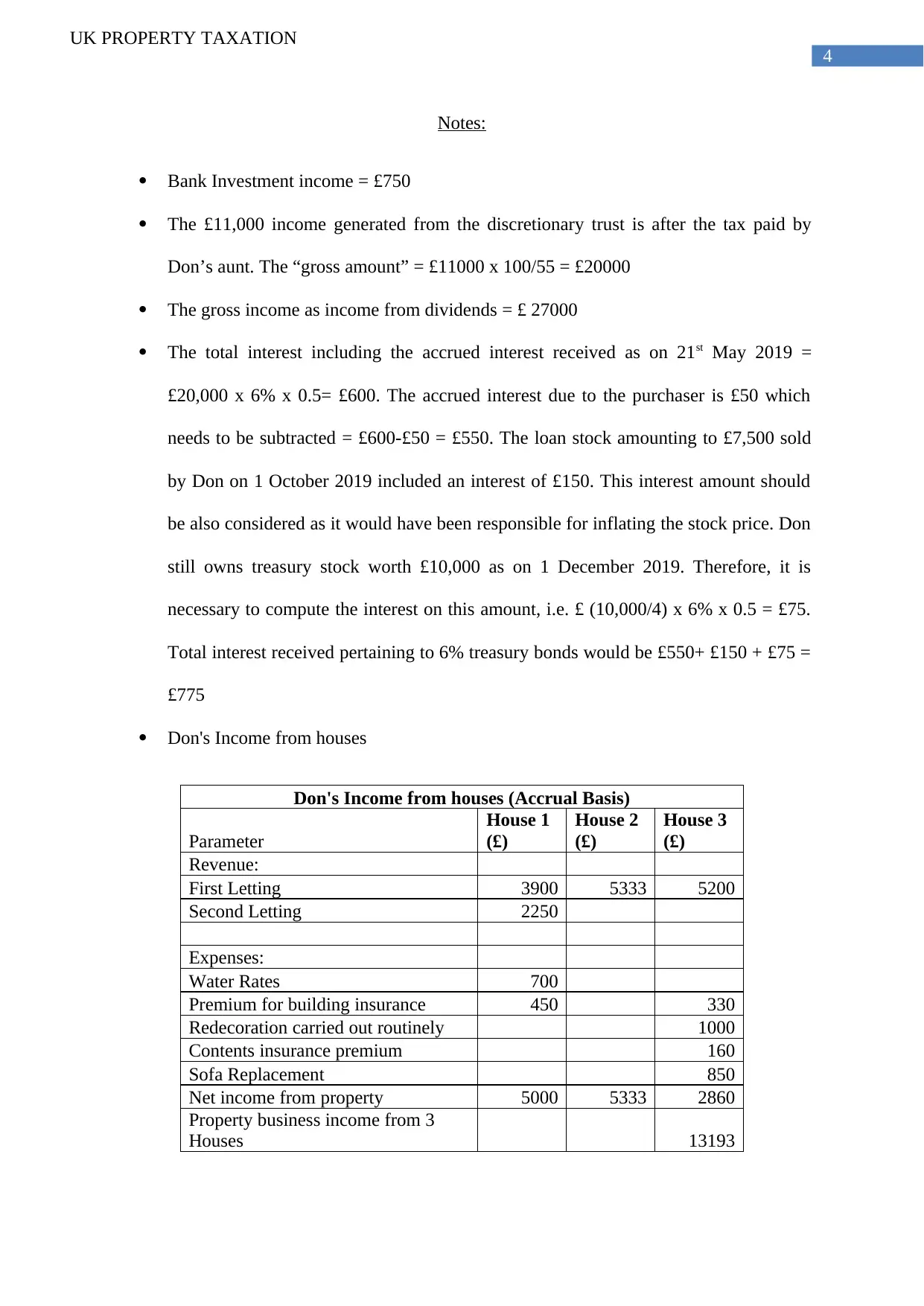

Notes:

Bank Investment income = £750

The £11,000 income generated from the discretionary trust is after the tax paid by

Don’s aunt. The “gross amount” = £11000 x 100/55 = £20000

The gross income as income from dividends = £ 27000

The total interest including the accrued interest received as on 21st May 2019 =

£20,000 x 6% x 0.5= £600. The accrued interest due to the purchaser is £50 which

needs to be subtracted = £600-£50 = £550. The loan stock amounting to £7,500 sold

by Don on 1 October 2019 included an interest of £150. This interest amount should

be also considered as it would have been responsible for inflating the stock price. Don

still owns treasury stock worth £10,000 as on 1 December 2019. Therefore, it is

necessary to compute the interest on this amount, i.e. £ (10,000/4) x 6% x 0.5 = £75.

Total interest received pertaining to 6% treasury bonds would be £550+ £150 + £75 =

£775

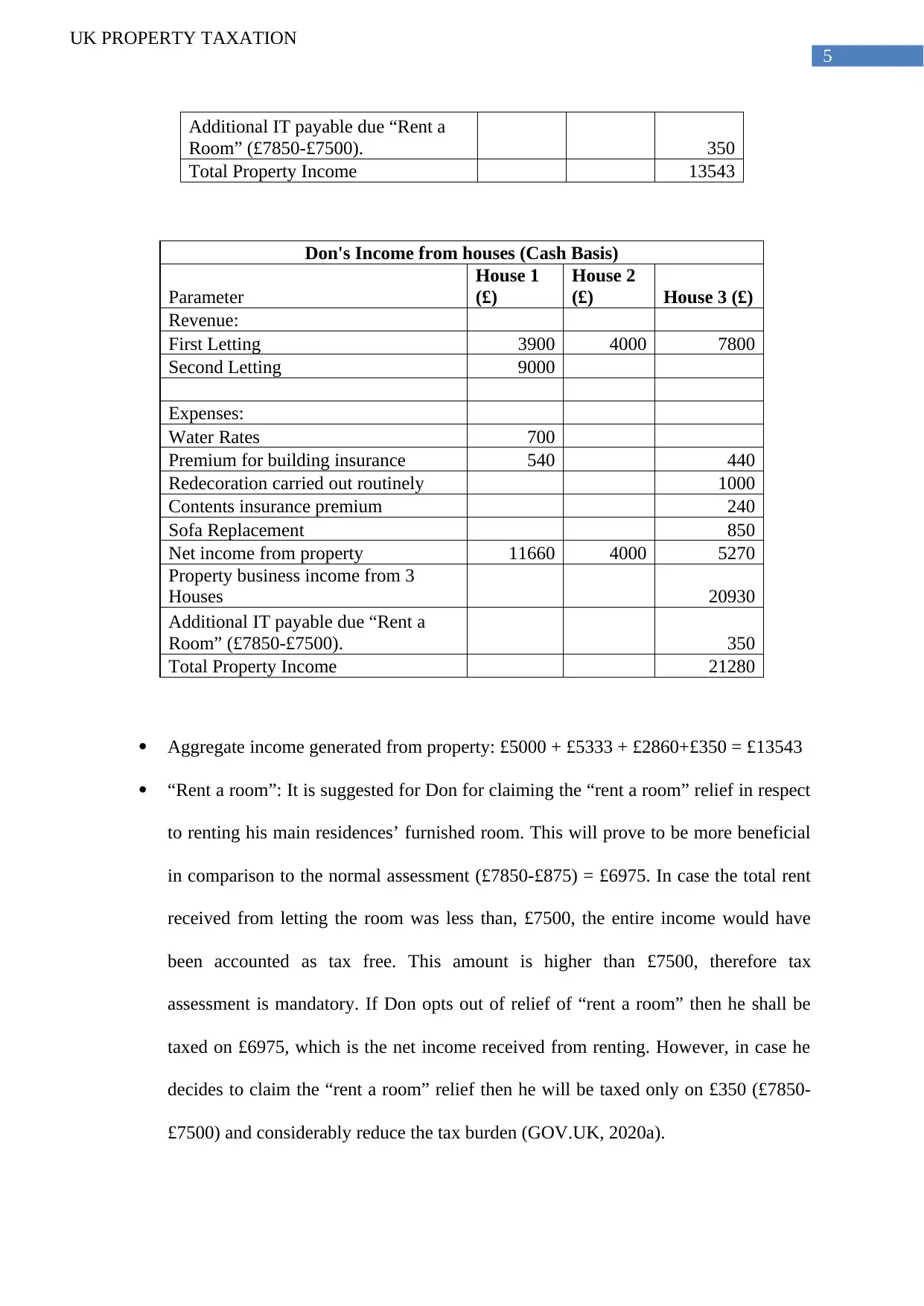

Don's Income from houses

Don's Income from houses (Accrual Basis)

Parameter

House 1

(£)

House 2

(£)

House 3

(£)

Revenue:

First Letting 3900 5333 5200

Second Letting 2250

Expenses:

Water Rates 700

Premium for building insurance 450 330

Redecoration carried out routinely 1000

Contents insurance premium 160

Sofa Replacement 850

Net income from property 5000 5333 2860

Property business income from 3

Houses 13193

UK PROPERTY TAXATION

Notes:

Bank Investment income = £750

The £11,000 income generated from the discretionary trust is after the tax paid by

Don’s aunt. The “gross amount” = £11000 x 100/55 = £20000

The gross income as income from dividends = £ 27000

The total interest including the accrued interest received as on 21st May 2019 =

£20,000 x 6% x 0.5= £600. The accrued interest due to the purchaser is £50 which

needs to be subtracted = £600-£50 = £550. The loan stock amounting to £7,500 sold

by Don on 1 October 2019 included an interest of £150. This interest amount should

be also considered as it would have been responsible for inflating the stock price. Don

still owns treasury stock worth £10,000 as on 1 December 2019. Therefore, it is

necessary to compute the interest on this amount, i.e. £ (10,000/4) x 6% x 0.5 = £75.

Total interest received pertaining to 6% treasury bonds would be £550+ £150 + £75 =

£775

Don's Income from houses

Don's Income from houses (Accrual Basis)

Parameter

House 1

(£)

House 2

(£)

House 3

(£)

Revenue:

First Letting 3900 5333 5200

Second Letting 2250

Expenses:

Water Rates 700

Premium for building insurance 450 330

Redecoration carried out routinely 1000

Contents insurance premium 160

Sofa Replacement 850

Net income from property 5000 5333 2860

Property business income from 3

Houses 13193

5

UK PROPERTY TAXATION

Additional IT payable due “Rent a

Room” (£7850-£7500). 350

Total Property Income 13543

Don's Income from houses (Cash Basis)

Parameter

House 1

(£)

House 2

(£) House 3 (£)

Revenue:

First Letting 3900 4000 7800

Second Letting 9000

Expenses:

Water Rates 700

Premium for building insurance 540 440

Redecoration carried out routinely 1000

Contents insurance premium 240

Sofa Replacement 850

Net income from property 11660 4000 5270

Property business income from 3

Houses 20930

Additional IT payable due “Rent a

Room” (£7850-£7500). 350

Total Property Income 21280

Aggregate income generated from property: £5000 + £5333 + £2860+£350 = £13543

“Rent a room”: It is suggested for Don for claiming the “rent a room” relief in respect

to renting his main residences’ furnished room. This will prove to be more beneficial

in comparison to the normal assessment (£7850-£875) = £6975. In case the total rent

received from letting the room was less than, £7500, the entire income would have

been accounted as tax free. This amount is higher than £7500, therefore tax

assessment is mandatory. If Don opts out of relief of “rent a room” then he shall be

taxed on £6975, which is the net income received from renting. However, in case he

decides to claim the “rent a room” relief then he will be taxed only on £350 (£7850-

£7500) and considerably reduce the tax burden (GOV.UK, 2020a).

UK PROPERTY TAXATION

Additional IT payable due “Rent a

Room” (£7850-£7500). 350

Total Property Income 13543

Don's Income from houses (Cash Basis)

Parameter

House 1

(£)

House 2

(£) House 3 (£)

Revenue:

First Letting 3900 4000 7800

Second Letting 9000

Expenses:

Water Rates 700

Premium for building insurance 540 440

Redecoration carried out routinely 1000

Contents insurance premium 240

Sofa Replacement 850

Net income from property 11660 4000 5270

Property business income from 3

Houses 20930

Additional IT payable due “Rent a

Room” (£7850-£7500). 350

Total Property Income 21280

Aggregate income generated from property: £5000 + £5333 + £2860+£350 = £13543

“Rent a room”: It is suggested for Don for claiming the “rent a room” relief in respect

to renting his main residences’ furnished room. This will prove to be more beneficial

in comparison to the normal assessment (£7850-£875) = £6975. In case the total rent

received from letting the room was less than, £7500, the entire income would have

been accounted as tax free. This amount is higher than £7500, therefore tax

assessment is mandatory. If Don opts out of relief of “rent a room” then he shall be

taxed on £6975, which is the net income received from renting. However, in case he

decides to claim the “rent a room” relief then he will be taxed only on £350 (£7850-

£7500) and considerably reduce the tax burden (GOV.UK, 2020a).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

UK PROPERTY TAXATION

Answer to part B

As per the regulations of “furnished holiday letting (FHL)” in the UK, an individual

must rent a holiday home for at least “105 days out of 365 days” in a year to be eligible for

claiming favourable tax benefit.

Don should investigate the following conditions to check whether cottages are suitable for

renting:

The cottage must be located within the UK or the EEA

The property must have furniture pertaining to “normal occupation” thereby entitling

the tenants to use the same

The letting should be done with a motive to a earn profit (Taxadvisermagazine.com,

2020)

The dwelling must be available for renting for a minimum of 210 days for the general

public and let for 105 days (Pass the Property, 2018). However, any period above

“longer term occupation (LTO)” will be treated as an exception. This relates to any

dweller staying consecutively for 31 days in one stretch in the let property but no

more than 155 days.

In case the total LTO exceeds 155 days, the property will not be eligible for FHL in

that year

The qualifying properties within the “UK or the EEA” form a business, but an individual

will be considered to be having two separate letting businesses if he/she owns dwellings in

these regions (Melville, 2019, pg 69-70). Therefore, in case of losses, it is to be settled

against itself across the two letting businesses.

The “Period of grace (POG)”: If a renting property qualifies the aforementioned

conditions, it is eligible for FHL. The landlord may opt to treat the property as FHL up to two

UK PROPERTY TAXATION

Answer to part B

As per the regulations of “furnished holiday letting (FHL)” in the UK, an individual

must rent a holiday home for at least “105 days out of 365 days” in a year to be eligible for

claiming favourable tax benefit.

Don should investigate the following conditions to check whether cottages are suitable for

renting:

The cottage must be located within the UK or the EEA

The property must have furniture pertaining to “normal occupation” thereby entitling

the tenants to use the same

The letting should be done with a motive to a earn profit (Taxadvisermagazine.com,

2020)

The dwelling must be available for renting for a minimum of 210 days for the general

public and let for 105 days (Pass the Property, 2018). However, any period above

“longer term occupation (LTO)” will be treated as an exception. This relates to any

dweller staying consecutively for 31 days in one stretch in the let property but no

more than 155 days.

In case the total LTO exceeds 155 days, the property will not be eligible for FHL in

that year

The qualifying properties within the “UK or the EEA” form a business, but an individual

will be considered to be having two separate letting businesses if he/she owns dwellings in

these regions (Melville, 2019, pg 69-70). Therefore, in case of losses, it is to be settled

against itself across the two letting businesses.

The “Period of grace (POG)”: If a renting property qualifies the aforementioned

conditions, it is eligible for FHL. The landlord may opt to treat the property as FHL up to two

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

UK PROPERTY TAXATION

years, if it fulfils for FHL in a single tax period (Melville, 2019, pg 70). The excess one year

is conceptualised as the POG. Even if the property fails to meet the 105 days eligibility

condition over the next two years, it would be accounted under FHL.

Averaging: A landlord having more than one FHL’s and where all of them fulfils the

criterion for FHL qualification except one, in which the dwelling fails to meet 105 days

eligibility, in such a case, the landlord may be entitled to be treated it as FHL, considering the

average number of days is the “minimum requirement of 105 days”. The claim associated to

averaging can be made by 31st January in the 2nd year post the election year. The POG cannot

be made in the same taxation year, where averaging election is made.

Income Tax Treatment: In case the properties qualify as FHL, Don will be able to

claim “capital allowances” on furniture and the equipment in the cottages such as heaters,

integral electrics and plumbing systems. Don will be entitled to write off a maximum of

£200,000 against 100% profit for such properties on a yearly basis. Additionally, he will be

able to exercise the reliefs which are associated to reduce or defer CGT at the time of selling

FHL. This is inclusive of any relief relating to roll-over, entrepreneurs’ relief and gift relief,

which may limit the total CGT payable for higher taxpayers from 28% to 10%. Furthermore,

the profits generated from FHL will allow more tax allowable pension contributions. The

current limitation of mortgage tax relief is not applicable to FHL and the entire amount of

interest paid may be deducted from profits. To take the full advantage of tax treatment, Don

needs to adhere all the qualifying conditions and select the appropriate options during “self-

assessment tax return” (Willerby, 2020).

UK PROPERTY TAXATION

years, if it fulfils for FHL in a single tax period (Melville, 2019, pg 70). The excess one year

is conceptualised as the POG. Even if the property fails to meet the 105 days eligibility

condition over the next two years, it would be accounted under FHL.

Averaging: A landlord having more than one FHL’s and where all of them fulfils the

criterion for FHL qualification except one, in which the dwelling fails to meet 105 days

eligibility, in such a case, the landlord may be entitled to be treated it as FHL, considering the

average number of days is the “minimum requirement of 105 days”. The claim associated to

averaging can be made by 31st January in the 2nd year post the election year. The POG cannot

be made in the same taxation year, where averaging election is made.

Income Tax Treatment: In case the properties qualify as FHL, Don will be able to

claim “capital allowances” on furniture and the equipment in the cottages such as heaters,

integral electrics and plumbing systems. Don will be entitled to write off a maximum of

£200,000 against 100% profit for such properties on a yearly basis. Additionally, he will be

able to exercise the reliefs which are associated to reduce or defer CGT at the time of selling

FHL. This is inclusive of any relief relating to roll-over, entrepreneurs’ relief and gift relief,

which may limit the total CGT payable for higher taxpayers from 28% to 10%. Furthermore,

the profits generated from FHL will allow more tax allowable pension contributions. The

current limitation of mortgage tax relief is not applicable to FHL and the entire amount of

interest paid may be deducted from profits. To take the full advantage of tax treatment, Don

needs to adhere all the qualifying conditions and select the appropriate options during “self-

assessment tax return” (Willerby, 2020).

8

UK PROPERTY TAXATION

Answer to part C(i)

The following advice to Don for the treatment of finance cost in respect of dwelling -

related loan on “let residential properties (LRP)” will be based on excerpts of regulation

from 6 April 2017 (Walker, 2019).

As per the present regulations, Don should consider the basic 20% IT rate for the tax

reduction on finance costs. The constraints on tax and deducted interest which acts as a

replacement will be phased out over a period of four years. The landlords have been given a

time of four years to make the necessary adjustments on income tax relief from April 2017

(GOV.UK, 2020b).

The relief obtained by LRP owners is mentioned as follows:

During 2017- 2018, the current allowable deduction on property income will be

restricted in proportion of “75% of finance cost and 25% to basic tax reduction”

During 2018- 2019, the deduction on property income will be restricted in proportion

of “50% of finance cost and 50% to basic tax reduction”

During 2019- 2020, the deduction on property income will be restricted in proportion

of “25% of finance cost and 75% to basic tax reduction”

During 2020- 2021, the cost against the dwelling related loan will be provided at basic

tax reduction rate

The finance costs incurred after 2020- 2021 will only be considered as tax reducer rather

than deduction.

The tax reducer for each LRP will be based on the following assumptions:

The profit obtained from LRP for the taxable period is computed after adjusting any

losses carried forward from the previous year or

UK PROPERTY TAXATION

Answer to part C(i)

The following advice to Don for the treatment of finance cost in respect of dwelling -

related loan on “let residential properties (LRP)” will be based on excerpts of regulation

from 6 April 2017 (Walker, 2019).

As per the present regulations, Don should consider the basic 20% IT rate for the tax

reduction on finance costs. The constraints on tax and deducted interest which acts as a

replacement will be phased out over a period of four years. The landlords have been given a

time of four years to make the necessary adjustments on income tax relief from April 2017

(GOV.UK, 2020b).

The relief obtained by LRP owners is mentioned as follows:

During 2017- 2018, the current allowable deduction on property income will be

restricted in proportion of “75% of finance cost and 25% to basic tax reduction”

During 2018- 2019, the deduction on property income will be restricted in proportion

of “50% of finance cost and 50% to basic tax reduction”

During 2019- 2020, the deduction on property income will be restricted in proportion

of “25% of finance cost and 75% to basic tax reduction”

During 2020- 2021, the cost against the dwelling related loan will be provided at basic

tax reduction rate

The finance costs incurred after 2020- 2021 will only be considered as tax reducer rather

than deduction.

The tax reducer for each LRP will be based on the following assumptions:

The profit obtained from LRP for the taxable period is computed after adjusting any

losses carried forward from the previous year or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

UK PROPERTY TAXATION

The sum of financial cost does not include any deductions associated to the rental

income

The higher portion of tax reduction for all the property businesses is restricted to an

“individual’s tax liability on adjusted total income”. The assessment of this income is done

by deducting individual’s general income from the total income, less allowance for a blind

person and personal allowance, whichever they are eligible for receiving.

Answer to part C(ii)

The decision to purchase cottages in Wales will involve finance costs such as

mortgage interest and loan arrangement fees and shall be deductible from rental income of

FHL irrespective of any limitations. In other words, the mortgage interest borne by Don can

be fully deducted from the profit, thereby making the deal more attractive for him to invest in

FHL rather than buy to let properties. However, in order to qualify for FHL, Don must fulfil

all the conditions (GOV.UK, 2017d).

It should be noted that as per the general description of the measure, the relief will be

restricted to basic rate of IT which was introduced from 6 April 2017. Additionally, this type

of relief will only include fees on repaying loans/mortgage and any kind of “interest on

loans to buy furnishings”. Therefore, Don will not be entitled for any relief associated to

“capital repayments of a mortgage or loan” (GOV.UK, 2020b).

Answer to part C(iii)

“Capital Gains Tax (CGT)”, may arise as a result of transferring the property

portfolio from an individual landlord to a company. CGT may be required for selling the

property at a very high market rate to a corporate entity. Based on the previous case laws,

rental businesses managed on a regular basis, where such a transfer of property is involved

UK PROPERTY TAXATION

The sum of financial cost does not include any deductions associated to the rental

income

The higher portion of tax reduction for all the property businesses is restricted to an

“individual’s tax liability on adjusted total income”. The assessment of this income is done

by deducting individual’s general income from the total income, less allowance for a blind

person and personal allowance, whichever they are eligible for receiving.

Answer to part C(ii)

The decision to purchase cottages in Wales will involve finance costs such as

mortgage interest and loan arrangement fees and shall be deductible from rental income of

FHL irrespective of any limitations. In other words, the mortgage interest borne by Don can

be fully deducted from the profit, thereby making the deal more attractive for him to invest in

FHL rather than buy to let properties. However, in order to qualify for FHL, Don must fulfil

all the conditions (GOV.UK, 2017d).

It should be noted that as per the general description of the measure, the relief will be

restricted to basic rate of IT which was introduced from 6 April 2017. Additionally, this type

of relief will only include fees on repaying loans/mortgage and any kind of “interest on

loans to buy furnishings”. Therefore, Don will not be entitled for any relief associated to

“capital repayments of a mortgage or loan” (GOV.UK, 2020b).

Answer to part C(iii)

“Capital Gains Tax (CGT)”, may arise as a result of transferring the property

portfolio from an individual landlord to a company. CGT may be required for selling the

property at a very high market rate to a corporate entity. Based on the previous case laws,

rental businesses managed on a regular basis, where such a transfer of property is involved

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

UK PROPERTY TAXATION

can be treated as CGT. This provides a landlord with a chance to depend on rollover relief as

per “S162 TCGA” 1992. Additionally, this legislation allows the businesses to exchange their

assets except cash to be exchanged on a going concern basis against stocks/shares. As a result

of this, there does not include any net gains, as they get nullified on issuing of stock.

Furthermore, S162 TCGA does not offer option to exercise claim of relief. This process

provides the company with the tax uplift relating to the dwellings with relevant ownership

proportion at current market value (Best & Kleven, 2018).

The pro rata limitation on the relief is applied in case the consideration made by

businesses is not satisfactory through issue of shares, thereby leaving a part of CGT to be

fulfilled by the company. These arrangements need to be protected by ESC D32, assuming

mortgage through obtaining businesses will lead to additional consideration which are not in

form of shares and HMRC treating the bank debts as borrowings pertaining to the business

(Wallis, 2014).

It should be noted whether property letting in regard to CGT should be treated as a

business is still unclear. By referring to the case of “Ramsay v HMRC (2013)”, we are able

to discern that there does not exist any statutory definition for CGT or IT purposes.

Determining what constitutes a business is one of the potential difficulties in incorporating

the relief. Based on the final verdict of Upper Tribunal, the activities are usually associated

with managing “investment properties” can be regarded as running a company (Carr, 2016).

The actions of a company should include the following:

Having a stable/sound and recognised business values

Actions should depict intention to earn profit

Representing an oath which is being attended by the owners

UK PROPERTY TAXATION

can be treated as CGT. This provides a landlord with a chance to depend on rollover relief as

per “S162 TCGA” 1992. Additionally, this legislation allows the businesses to exchange their

assets except cash to be exchanged on a going concern basis against stocks/shares. As a result

of this, there does not include any net gains, as they get nullified on issuing of stock.

Furthermore, S162 TCGA does not offer option to exercise claim of relief. This process

provides the company with the tax uplift relating to the dwellings with relevant ownership

proportion at current market value (Best & Kleven, 2018).

The pro rata limitation on the relief is applied in case the consideration made by

businesses is not satisfactory through issue of shares, thereby leaving a part of CGT to be

fulfilled by the company. These arrangements need to be protected by ESC D32, assuming

mortgage through obtaining businesses will lead to additional consideration which are not in

form of shares and HMRC treating the bank debts as borrowings pertaining to the business

(Wallis, 2014).

It should be noted whether property letting in regard to CGT should be treated as a

business is still unclear. By referring to the case of “Ramsay v HMRC (2013)”, we are able

to discern that there does not exist any statutory definition for CGT or IT purposes.

Determining what constitutes a business is one of the potential difficulties in incorporating

the relief. Based on the final verdict of Upper Tribunal, the activities are usually associated

with managing “investment properties” can be regarded as running a company (Carr, 2016).

The actions of a company should include the following:

Having a stable/sound and recognised business values

Actions should depict intention to earn profit

Representing an oath which is being attended by the owners

11

UK PROPERTY TAXATION

In addition to the aforementioned actions, there should be a considerable amount of time

devoted to property -related work. By referring to the case of “Ramsay v HMRC (2013)”, we

are able to understand how the person maintained a mean of 20 hours/week in managing and

maintaining the properties. This shows that the quantity of activity being performed is more

important rather than quality (Rossmartin, 2020).

Answer to part C(iv)

“Stamp duty land tax (SDLT)” is applicable on buying new residential leasehold and

payable on rents over a certain threshold (England.shelter.org.uk, 2020). This amount is

payable on both lease premium of purchasing price based on SDLT residential rates and NPV

of the rent payable (GOV.UK, 2020c). Don need not pay any SDLT on NPV up to £125,000.

Any excess of this amount should be treated with 1% SDLT rate under NPV. The rate of

SDLT is applicable on the entire amount of consideration. The purchasing price threshold for

the applicable SDLT (updated 2nd November 2018) is listed as follows:

For “purchase price up to £125,000, the SDLT rate is 0”

For “purchase price more than £125,000 to £250,000, the SDLT rate is 1%”

For “purchase price more than £250,000 to £500,000, the SDLT rate is 3%”

For “purchase price more than £500,000 to £1 million, the SDLT rate is 4%”

For “purchase price more than £1 million to £ million, the SDLT rate is 5%”

For “purchase price more than £2 million (22 March 2012 onwards), the SDLT rate is

7%”

The announcement of restriction on relief for finance cost in summer 2015, has given

clear indication whether it is beneficial to hold residential property directly or in a

company (Scanlon, Whitehead & Blanc, 2017). The property is taxable in relation to

UK PROPERTY TAXATION

In addition to the aforementioned actions, there should be a considerable amount of time

devoted to property -related work. By referring to the case of “Ramsay v HMRC (2013)”, we

are able to understand how the person maintained a mean of 20 hours/week in managing and

maintaining the properties. This shows that the quantity of activity being performed is more

important rather than quality (Rossmartin, 2020).

Answer to part C(iv)

“Stamp duty land tax (SDLT)” is applicable on buying new residential leasehold and

payable on rents over a certain threshold (England.shelter.org.uk, 2020). This amount is

payable on both lease premium of purchasing price based on SDLT residential rates and NPV

of the rent payable (GOV.UK, 2020c). Don need not pay any SDLT on NPV up to £125,000.

Any excess of this amount should be treated with 1% SDLT rate under NPV. The rate of

SDLT is applicable on the entire amount of consideration. The purchasing price threshold for

the applicable SDLT (updated 2nd November 2018) is listed as follows:

For “purchase price up to £125,000, the SDLT rate is 0”

For “purchase price more than £125,000 to £250,000, the SDLT rate is 1%”

For “purchase price more than £250,000 to £500,000, the SDLT rate is 3%”

For “purchase price more than £500,000 to £1 million, the SDLT rate is 4%”

For “purchase price more than £1 million to £ million, the SDLT rate is 5%”

For “purchase price more than £2 million (22 March 2012 onwards), the SDLT rate is

7%”

The announcement of restriction on relief for finance cost in summer 2015, has given

clear indication whether it is beneficial to hold residential property directly or in a

company (Scanlon, Whitehead & Blanc, 2017). The property is taxable in relation to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.