Analysis of Portfolio Outcomes and Hypothesis Testing Report

VerifiedAdded on 2020/06/04

|26

|9312

|28

Report

AI Summary

This report provides a detailed analysis of UK stock market portfolios, focusing on hypothesis testing and the efficient market hypothesis. It begins with an introduction to the efficient market hypothesis and the random walk hypothesis, followed by the calculation of average monthly logarithmic returns for two portfolios, Portfolio A and Portfolio B. The report includes descriptive statistical analysis, graphical representations, and the development and application of a T-test to compare the returns of the two portfolios. The findings indicate a significant mean difference between the returns generated by the two portfolios. The report also compares the results with previous research and provides an appendix with supporting data and analysis, including regression statistics for several companies. The analysis also touches upon the Bayer-Monsanto merger deal.

Hypothesis testing and

essay

essay

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART A...........................................................................................................................................1

INTRODUCTION...........................................................................................................................1

(A) Efficient market hypothesis and Random Walk hypothesis................................................1

INTERPRETATION OF PORTFOLIO OUTCOMES...................................................................2

(B) Calculation of average monthly logarithmic return of portfolio A and B............................2

c. Development of Hypothesis....................................................................................................7

D Application of T test................................................................................................................7

E. Discussion of findings............................................................................................................8

F Comparison of results with previous research.........................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

PART B..........................................................................................................................................16

INTRODUCTION:........................................................................................................................16

Study on Bayer- Monsanto merger deal:..................................................................................16

CONCLUSION..............................................................................................................................21

REFERENCES..............................................................................................................................23

APPENDIX....................................................................................................................................24

PART A...........................................................................................................................................1

INTRODUCTION...........................................................................................................................1

(A) Efficient market hypothesis and Random Walk hypothesis................................................1

INTERPRETATION OF PORTFOLIO OUTCOMES...................................................................2

(B) Calculation of average monthly logarithmic return of portfolio A and B............................2

c. Development of Hypothesis....................................................................................................7

D Application of T test................................................................................................................7

E. Discussion of findings............................................................................................................8

F Comparison of results with previous research.........................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

PART B..........................................................................................................................................16

INTRODUCTION:........................................................................................................................16

Study on Bayer- Monsanto merger deal:..................................................................................16

CONCLUSION..............................................................................................................................21

REFERENCES..............................................................................................................................23

APPENDIX....................................................................................................................................24

PART A

INTRODUCTION

Analysing the changes and variation took place in the stock market of UK which brings

information among investors and stakeholder for the purpose of investment decisions. In the

present report, there will be discussion based on various portfolio which will be compared with

the FTSE 100 index determining various outcomes through test like, regression and T-test

analysis. Further, this report will also reflect consist of recommendations based on Monsanto

investors as per currency decisions and reforms undertaken by Bayer. Along with this, there will

be analysis on the portfolios of various industries which will be analysed as per examining their

efficiency in performing operations in the capital market. Thus, the efficient portfolio has been

suggested to the investors in making appropriate investment in organisations.

(A) Efficient market hypothesis and Random Walk hypothesis

Efficient Market Hypothesis:

To identify the efficiency of market in context with share value which always reflect the

full information. This determination helps in analysing the efficiency of market on the basis of

intrinsic value of share which were being adjusted instantaneously and rationally to the

announcement of new information (Hamid & et.al., 2017). However, as per considering the

framework of FAMA, which has categorised the s market in 3 segmentations such as:

Weak form efficient: This is the market which represents all historical data as well as

forecasted price movements in application of various statistical tools. It represents the

extra returns made on portfolios (Emenike, 2017). It includes analysis relevant with rate

of return, trading volumes, sequence of past prices etc.

Semi-strong form efficient: This market is consisting of all information which

determines the current stock prices which reflects all historical information which are

publicly available such as annual financial disclosures, dividend pay outs, merger plans

etc.

Strong form efficient market: This is the market which has the strong data based on

which it becomes tough to bit the market (Malhotra, Tandon & Tandon, 2015). It

comprises of current stock value as well as historical data which are along with publicly

available information regarding operations.

Random walk hypothesis:

INTRODUCTION

Analysing the changes and variation took place in the stock market of UK which brings

information among investors and stakeholder for the purpose of investment decisions. In the

present report, there will be discussion based on various portfolio which will be compared with

the FTSE 100 index determining various outcomes through test like, regression and T-test

analysis. Further, this report will also reflect consist of recommendations based on Monsanto

investors as per currency decisions and reforms undertaken by Bayer. Along with this, there will

be analysis on the portfolios of various industries which will be analysed as per examining their

efficiency in performing operations in the capital market. Thus, the efficient portfolio has been

suggested to the investors in making appropriate investment in organisations.

(A) Efficient market hypothesis and Random Walk hypothesis

Efficient Market Hypothesis:

To identify the efficiency of market in context with share value which always reflect the

full information. This determination helps in analysing the efficiency of market on the basis of

intrinsic value of share which were being adjusted instantaneously and rationally to the

announcement of new information (Hamid & et.al., 2017). However, as per considering the

framework of FAMA, which has categorised the s market in 3 segmentations such as:

Weak form efficient: This is the market which represents all historical data as well as

forecasted price movements in application of various statistical tools. It represents the

extra returns made on portfolios (Emenike, 2017). It includes analysis relevant with rate

of return, trading volumes, sequence of past prices etc.

Semi-strong form efficient: This market is consisting of all information which

determines the current stock prices which reflects all historical information which are

publicly available such as annual financial disclosures, dividend pay outs, merger plans

etc.

Strong form efficient market: This is the market which has the strong data based on

which it becomes tough to bit the market (Malhotra, Tandon & Tandon, 2015). It

comprises of current stock value as well as historical data which are along with publicly

available information regarding operations.

Random walk hypothesis:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This theory determines that the stock market prices of portfolio will as per the stock

market price which evolve the changes in prices randomly which is unclear and cannot be

predicted (Beskos & et.al., 2015). Considering the opinion of various authors which insist

various disputes in several areas such as:

The ensured collective rational will not perform individually.

There has been limits on the benefits based on allocative efficiency.

Market rationality will never be implied through market efficiency (Sakai & Hukushima,

2016).

INTERPRETATION OF PORTFOLIO OUTCOMES

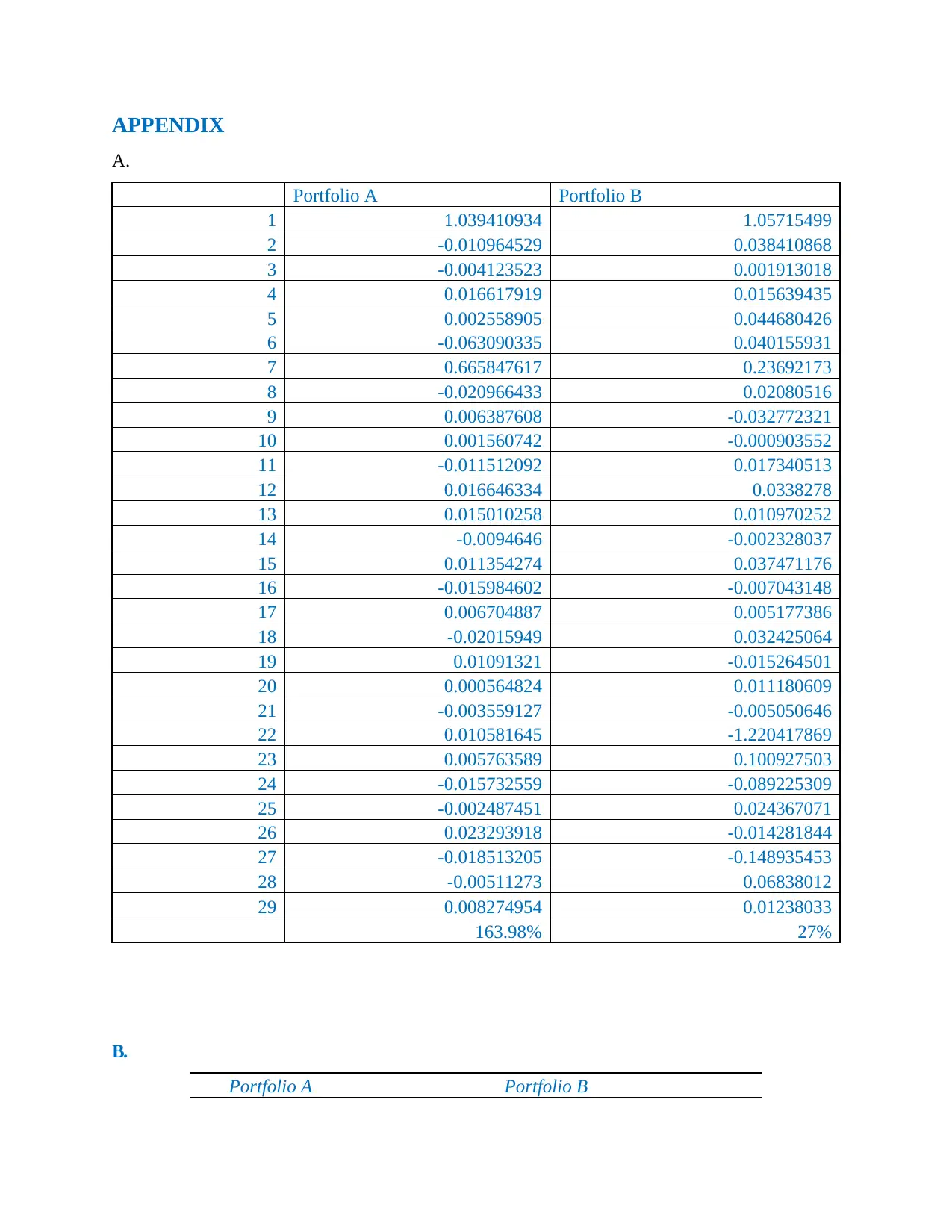

(B) Calculation of average monthly logarithmic return of portfolio A and B

As per analysing the average monthly returns on the portfolios there will be analysis as

listed in the Appendix A with consideration of following justification such as:

Appendix A

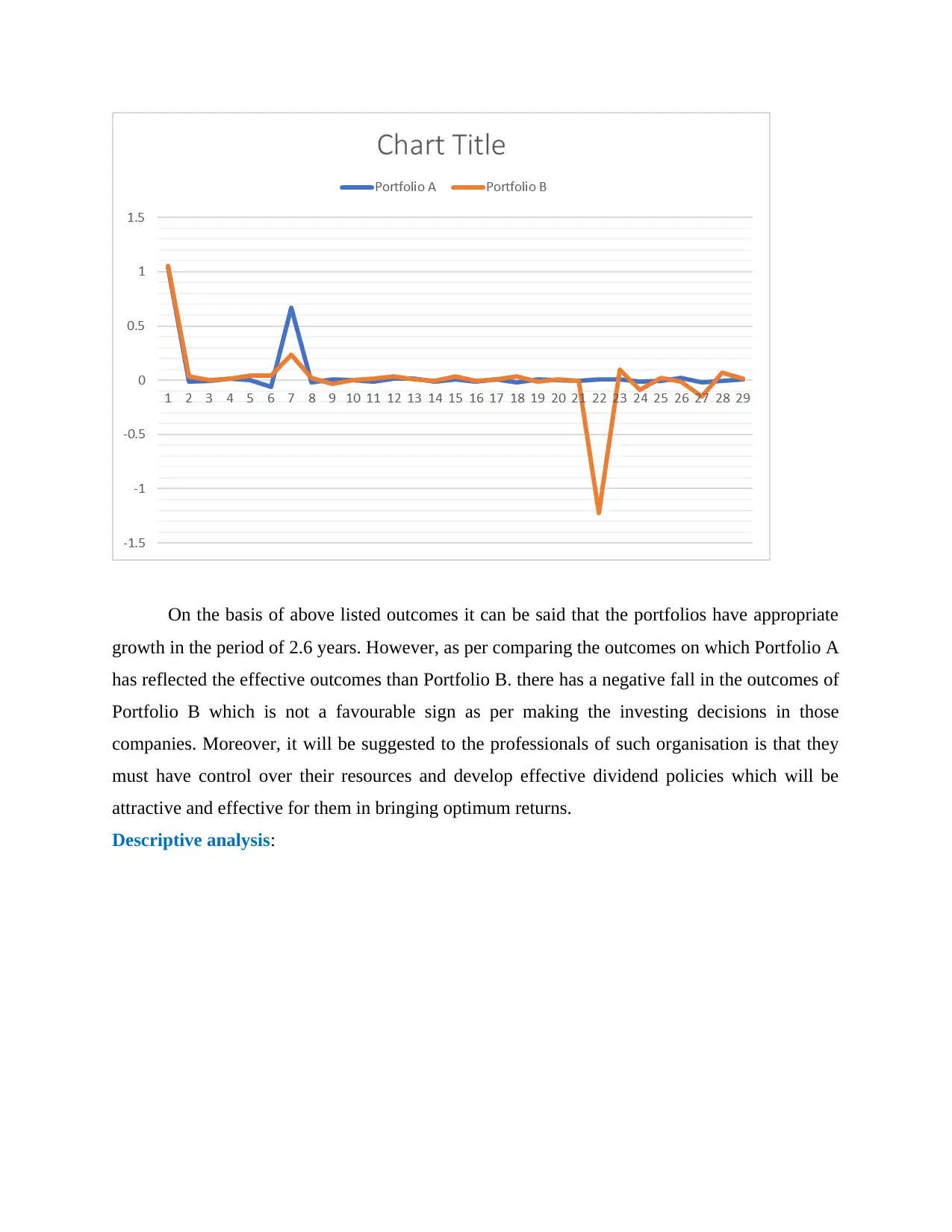

Interpretation:

Considering the above graph on which it can be said that there has been randomly

selected organisation in the portfolios which has reflected the outcomes. Looking through the

data set it can be said that there has been rise in the level of portfolio returns in the beginning as

the companies were performing well during that period. similarly, as per analysing the constant

market price which evolve the changes in prices randomly which is unclear and cannot be

predicted (Beskos & et.al., 2015). Considering the opinion of various authors which insist

various disputes in several areas such as:

The ensured collective rational will not perform individually.

There has been limits on the benefits based on allocative efficiency.

Market rationality will never be implied through market efficiency (Sakai & Hukushima,

2016).

INTERPRETATION OF PORTFOLIO OUTCOMES

(B) Calculation of average monthly logarithmic return of portfolio A and B

As per analysing the average monthly returns on the portfolios there will be analysis as

listed in the Appendix A with consideration of following justification such as:

Appendix A

Interpretation:

Considering the above graph on which it can be said that there has been randomly

selected organisation in the portfolios which has reflected the outcomes. Looking through the

data set it can be said that there has been rise in the level of portfolio returns in the beginning as

the companies were performing well during that period. similarly, as per analysing the constant

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

outcomes determined after such peek return on which it can be said that firm has managed their

resources in that manner which brings it a constant return.

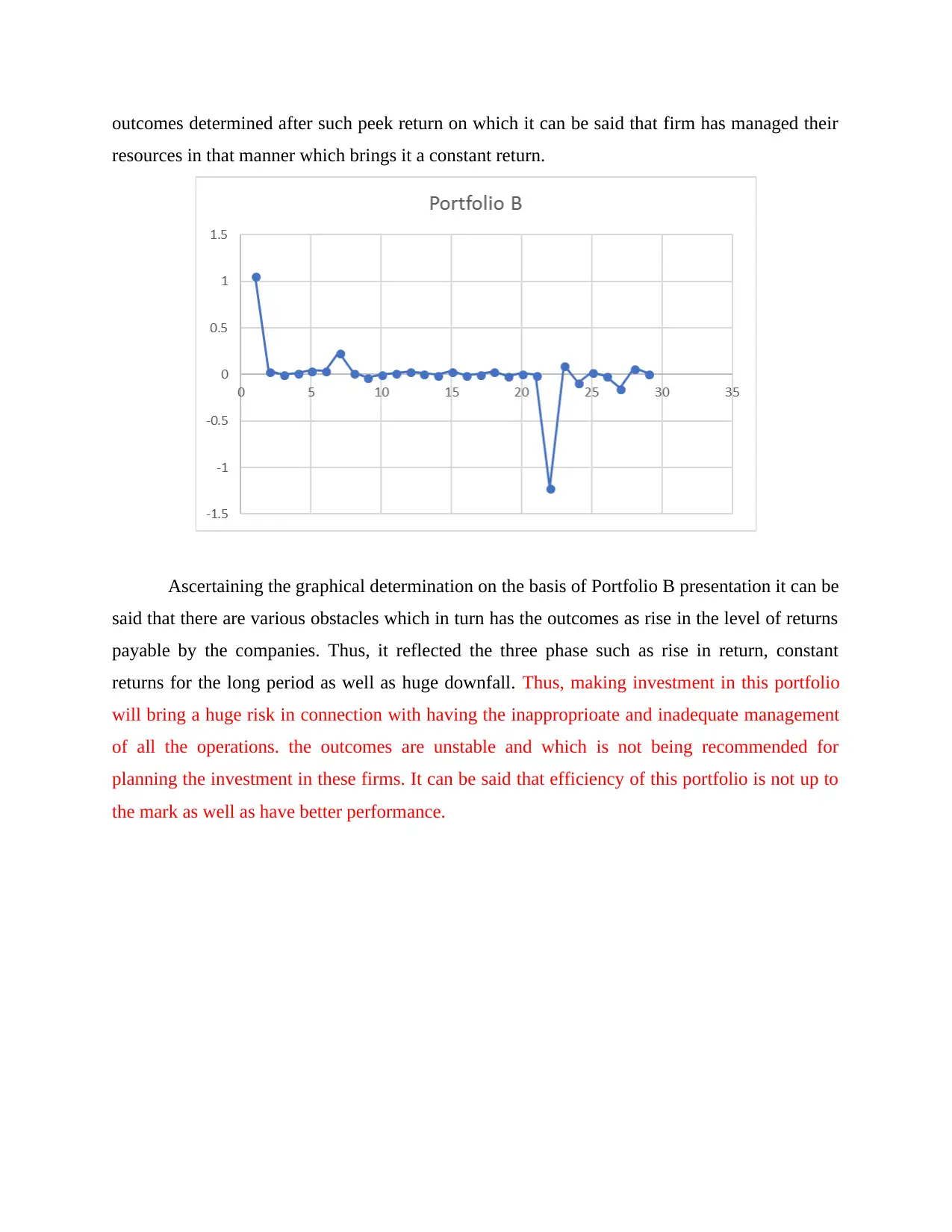

Ascertaining the graphical determination on the basis of Portfolio B presentation it can be

said that there are various obstacles which in turn has the outcomes as rise in the level of returns

payable by the companies. Thus, it reflected the three phase such as rise in return, constant

returns for the long period as well as huge downfall. Thus, making investment in this portfolio

will bring a huge risk in connection with having the inapproprioate and inadequate management

of all the operations. the outcomes are unstable and which is not being recommended for

planning the investment in these firms. It can be said that efficiency of this portfolio is not up to

the mark as well as have better performance.

resources in that manner which brings it a constant return.

Ascertaining the graphical determination on the basis of Portfolio B presentation it can be

said that there are various obstacles which in turn has the outcomes as rise in the level of returns

payable by the companies. Thus, it reflected the three phase such as rise in return, constant

returns for the long period as well as huge downfall. Thus, making investment in this portfolio

will bring a huge risk in connection with having the inapproprioate and inadequate management

of all the operations. the outcomes are unstable and which is not being recommended for

planning the investment in these firms. It can be said that efficiency of this portfolio is not up to

the mark as well as have better performance.

On the basis of above listed outcomes it can be said that the portfolios have appropriate

growth in the period of 2.6 years. However, as per comparing the outcomes on which Portfolio A

has reflected the effective outcomes than Portfolio B. there has a negative fall in the outcomes of

Portfolio B which is not a favourable sign as per making the investing decisions in those

companies. Moreover, it will be suggested to the professionals of such organisation is that they

must have control over their resources and develop effective dividend policies which will be

attractive and effective for them in bringing optimum returns.

Descriptive analysis:

growth in the period of 2.6 years. However, as per comparing the outcomes on which Portfolio A

has reflected the effective outcomes than Portfolio B. there has a negative fall in the outcomes of

Portfolio B which is not a favourable sign as per making the investing decisions in those

companies. Moreover, it will be suggested to the professionals of such organisation is that they

must have control over their resources and develop effective dividend policies which will be

attractive and effective for them in bringing optimum returns.

Descriptive analysis:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

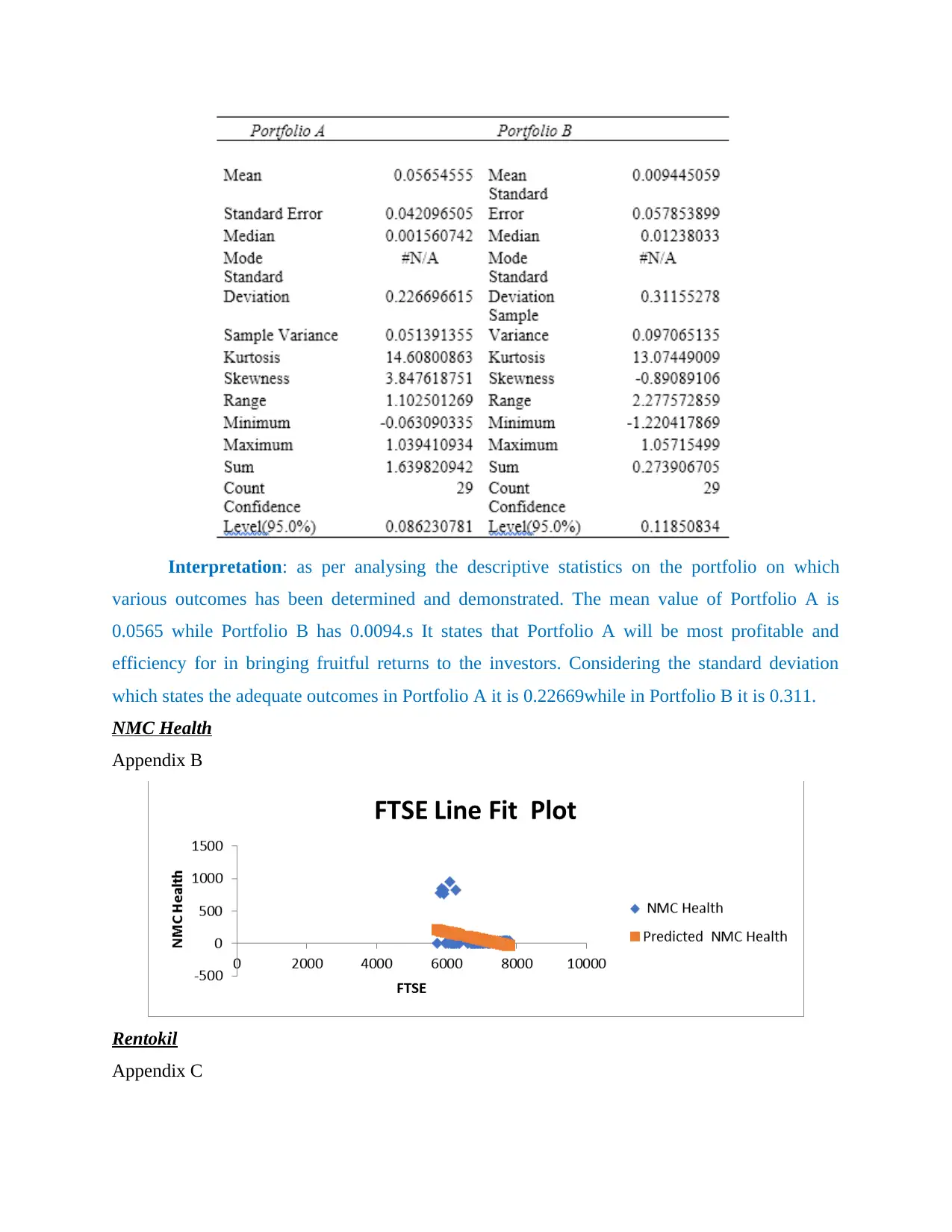

Interpretation: as per analysing the descriptive statistics on the portfolio on which

various outcomes has been determined and demonstrated. The mean value of Portfolio A is

0.0565 while Portfolio B has 0.0094.s It states that Portfolio A will be most profitable and

efficiency for in bringing fruitful returns to the investors. Considering the standard deviation

which states the adequate outcomes in Portfolio A it is 0.22669while in Portfolio B it is 0.311.

NMC Health

Appendix B

Rentokil

Appendix C

various outcomes has been determined and demonstrated. The mean value of Portfolio A is

0.0565 while Portfolio B has 0.0094.s It states that Portfolio A will be most profitable and

efficiency for in bringing fruitful returns to the investors. Considering the standard deviation

which states the adequate outcomes in Portfolio A it is 0.22669while in Portfolio B it is 0.311.

NMC Health

Appendix B

Rentokil

Appendix C

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ITRK

Appendix D

DCC

Appendix E

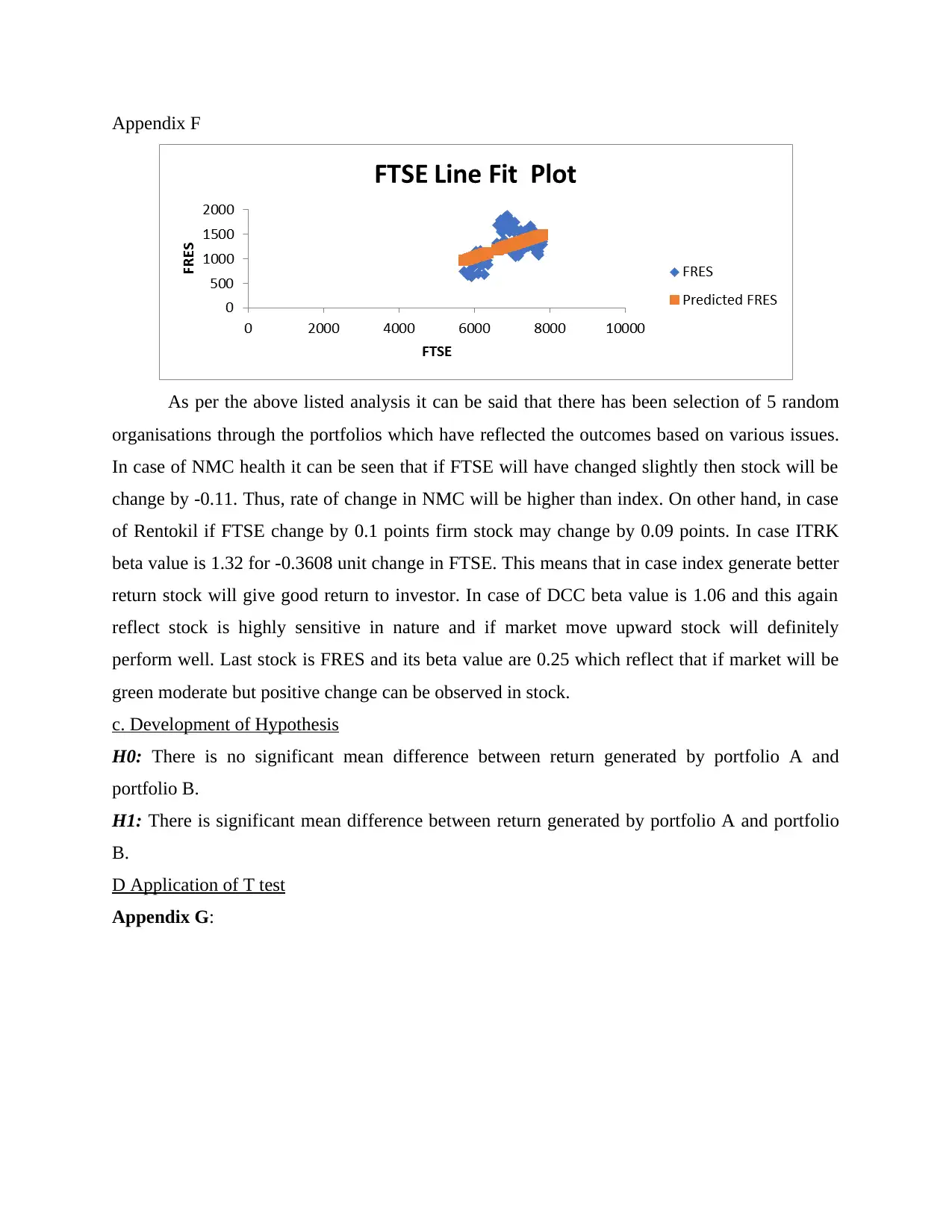

FRES

Appendix D

DCC

Appendix E

FRES

Appendix F

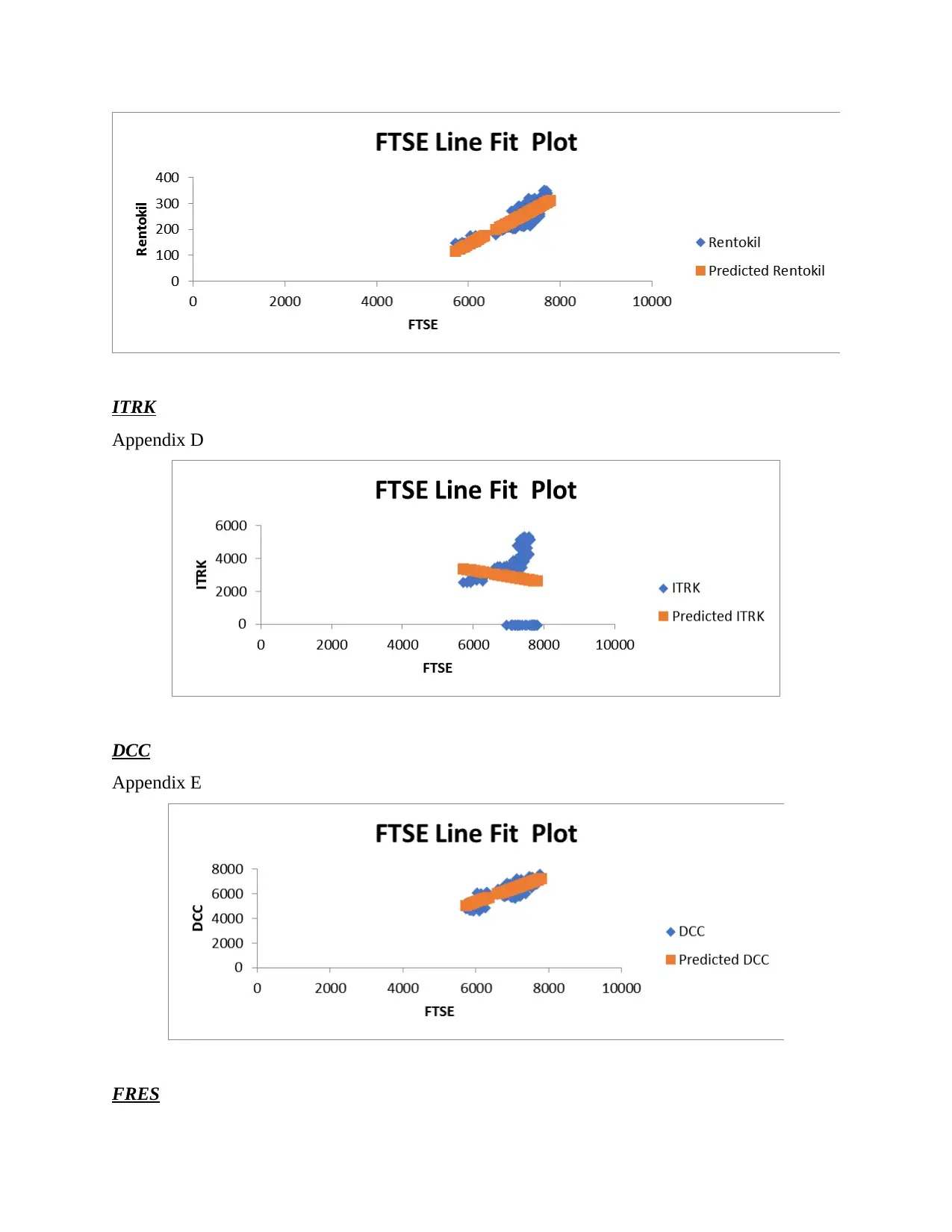

As per the above listed analysis it can be said that there has been selection of 5 random

organisations through the portfolios which have reflected the outcomes based on various issues.

In case of NMC health it can be seen that if FTSE will have changed slightly then stock will be

change by -0.11. Thus, rate of change in NMC will be higher than index. On other hand, in case

of Rentokil if FTSE change by 0.1 points firm stock may change by 0.09 points. In case ITRK

beta value is 1.32 for -0.3608 unit change in FTSE. This means that in case index generate better

return stock will give good return to investor. In case of DCC beta value is 1.06 and this again

reflect stock is highly sensitive in nature and if market move upward stock will definitely

perform well. Last stock is FRES and its beta value are 0.25 which reflect that if market will be

green moderate but positive change can be observed in stock.

c. Development of Hypothesis

H0: There is no significant mean difference between return generated by portfolio A and

portfolio B.

H1: There is significant mean difference between return generated by portfolio A and portfolio

B.

D Application of T test

Appendix G:

As per the above listed analysis it can be said that there has been selection of 5 random

organisations through the portfolios which have reflected the outcomes based on various issues.

In case of NMC health it can be seen that if FTSE will have changed slightly then stock will be

change by -0.11. Thus, rate of change in NMC will be higher than index. On other hand, in case

of Rentokil if FTSE change by 0.1 points firm stock may change by 0.09 points. In case ITRK

beta value is 1.32 for -0.3608 unit change in FTSE. This means that in case index generate better

return stock will give good return to investor. In case of DCC beta value is 1.06 and this again

reflect stock is highly sensitive in nature and if market move upward stock will definitely

perform well. Last stock is FRES and its beta value are 0.25 which reflect that if market will be

green moderate but positive change can be observed in stock.

c. Development of Hypothesis

H0: There is no significant mean difference between return generated by portfolio A and

portfolio B.

H1: There is significant mean difference between return generated by portfolio A and portfolio

B.

D Application of T test

Appendix G:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

E. Discussion of findings

As per analysing the outcomes which are listed in the above table insists that portfolio B is

generating higher return in specific direction then portfolio A. The one tail level of significance

is 0.025<0.05 which means that there is significant mean difference between both variables or

portfolio A and B. Similarly, relevant time period it is observed that FTSE generate return of

163.98% but portfolio B generate return of 27% in which firms are selected by considering

technical analysis charts (Auger‐Méthé & et.al., 2015). However, as per considering the Efficient

market hypothesis it can be said that there is effective rise in the market share of the

organization. Thus, Portfolio is needed to have appropriate outcomes and return payable over the

operations.

F Comparison of results with previous research

The impacts incurred in the huge fluctuations in the capital market is basically based on

reforms which affected the market share value of the businesses. Efficient market hypothesis

theory failed to cover impact of market size, volatility, shareholder’s expectations, cyclical

fluctuations and asset bubbles (Efficient Markets Hypothesis, 2018). However, it has been

analyzed here that there has been changes in the UK’s most of the stocks as well as their beta

value in the operations.

As per analysing the outcomes which are listed in the above table insists that portfolio B is

generating higher return in specific direction then portfolio A. The one tail level of significance

is 0.025<0.05 which means that there is significant mean difference between both variables or

portfolio A and B. Similarly, relevant time period it is observed that FTSE generate return of

163.98% but portfolio B generate return of 27% in which firms are selected by considering

technical analysis charts (Auger‐Méthé & et.al., 2015). However, as per considering the Efficient

market hypothesis it can be said that there is effective rise in the market share of the

organization. Thus, Portfolio is needed to have appropriate outcomes and return payable over the

operations.

F Comparison of results with previous research

The impacts incurred in the huge fluctuations in the capital market is basically based on

reforms which affected the market share value of the businesses. Efficient market hypothesis

theory failed to cover impact of market size, volatility, shareholder’s expectations, cyclical

fluctuations and asset bubbles (Efficient Markets Hypothesis, 2018). However, it has been

analyzed here that there has been changes in the UK’s most of the stocks as well as their beta

value in the operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Auger‐Méthé, M. & et.al., (2015). Differentiating the Lévy walk from a composite correlated

random walk. Methods in Ecology and Evolution. 6(10). 1179-1189.

Beskos, A. & et.al., (2015). Asymptotic Analysis of the Random-Walk Metropolis Algorithm on

Ridged Densities. arXiv preprint arXiv:1510.02577.

Emenike, K. O. (2017). Empirical test for weak-form efficient market hypothesis of the Nigerian

stock exchange (Doctoral dissertation).

Hamid, K. & et.al., (2017). Testing the weak form of efficient market hypothesis: Empirical

evidence from Asia-Pacific markets.

Malhotra, N., Tandon, K., & Tandon, D. (2015). Testing the Empirics of Weak Form of Efficient

Market Hypothesis: Evidence from Asia-Pacific Markets. IUP Journal of Applied

Finance. 21(4).

Sakai, Y., & Hukushima, K. (2016). Eigenvalue analysis of an irreversible random walk with

skew detailed balance conditions. Physical Review E. 93(4). 043318.

Online

Efficient Markets Hypothesis. 2018. [Online]. Available through :<

https://corporatefinanceinstitute.com/resources/knowledge/trading-investing/efficient-

markets-hypothesis/>.

Books and Journals

Auger‐Méthé, M. & et.al., (2015). Differentiating the Lévy walk from a composite correlated

random walk. Methods in Ecology and Evolution. 6(10). 1179-1189.

Beskos, A. & et.al., (2015). Asymptotic Analysis of the Random-Walk Metropolis Algorithm on

Ridged Densities. arXiv preprint arXiv:1510.02577.

Emenike, K. O. (2017). Empirical test for weak-form efficient market hypothesis of the Nigerian

stock exchange (Doctoral dissertation).

Hamid, K. & et.al., (2017). Testing the weak form of efficient market hypothesis: Empirical

evidence from Asia-Pacific markets.

Malhotra, N., Tandon, K., & Tandon, D. (2015). Testing the Empirics of Weak Form of Efficient

Market Hypothesis: Evidence from Asia-Pacific Markets. IUP Journal of Applied

Finance. 21(4).

Sakai, Y., & Hukushima, K. (2016). Eigenvalue analysis of an irreversible random walk with

skew detailed balance conditions. Physical Review E. 93(4). 043318.

Online

Efficient Markets Hypothesis. 2018. [Online]. Available through :<

https://corporatefinanceinstitute.com/resources/knowledge/trading-investing/efficient-

markets-hypothesis/>.

APPENDIX

A.

Portfolio A Portfolio B

1 1.039410934 1.05715499

2 -0.010964529 0.038410868

3 -0.004123523 0.001913018

4 0.016617919 0.015639435

5 0.002558905 0.044680426

6 -0.063090335 0.040155931

7 0.665847617 0.23692173

8 -0.020966433 0.02080516

9 0.006387608 -0.032772321

10 0.001560742 -0.000903552

11 -0.011512092 0.017340513

12 0.016646334 0.0338278

13 0.015010258 0.010970252

14 -0.0094646 -0.002328037

15 0.011354274 0.037471176

16 -0.015984602 -0.007043148

17 0.006704887 0.005177386

18 -0.02015949 0.032425064

19 0.01091321 -0.015264501

20 0.000564824 0.011180609

21 -0.003559127 -0.005050646

22 0.010581645 -1.220417869

23 0.005763589 0.100927503

24 -0.015732559 -0.089225309

25 -0.002487451 0.024367071

26 0.023293918 -0.014281844

27 -0.018513205 -0.148935453

28 -0.00511273 0.06838012

29 0.008274954 0.01238033

163.98% 27%

B.

Portfolio A Portfolio B

A.

Portfolio A Portfolio B

1 1.039410934 1.05715499

2 -0.010964529 0.038410868

3 -0.004123523 0.001913018

4 0.016617919 0.015639435

5 0.002558905 0.044680426

6 -0.063090335 0.040155931

7 0.665847617 0.23692173

8 -0.020966433 0.02080516

9 0.006387608 -0.032772321

10 0.001560742 -0.000903552

11 -0.011512092 0.017340513

12 0.016646334 0.0338278

13 0.015010258 0.010970252

14 -0.0094646 -0.002328037

15 0.011354274 0.037471176

16 -0.015984602 -0.007043148

17 0.006704887 0.005177386

18 -0.02015949 0.032425064

19 0.01091321 -0.015264501

20 0.000564824 0.011180609

21 -0.003559127 -0.005050646

22 0.010581645 -1.220417869

23 0.005763589 0.100927503

24 -0.015732559 -0.089225309

25 -0.002487451 0.024367071

26 0.023293918 -0.014281844

27 -0.018513205 -0.148935453

28 -0.00511273 0.06838012

29 0.008274954 0.01238033

163.98% 27%

B.

Portfolio A Portfolio B

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.