Detailed Analysis of UK Tax Liabilities for Individuals and Businesses

VerifiedAdded on 2023/06/07

|11

|2085

|196

Homework Assignment

AI Summary

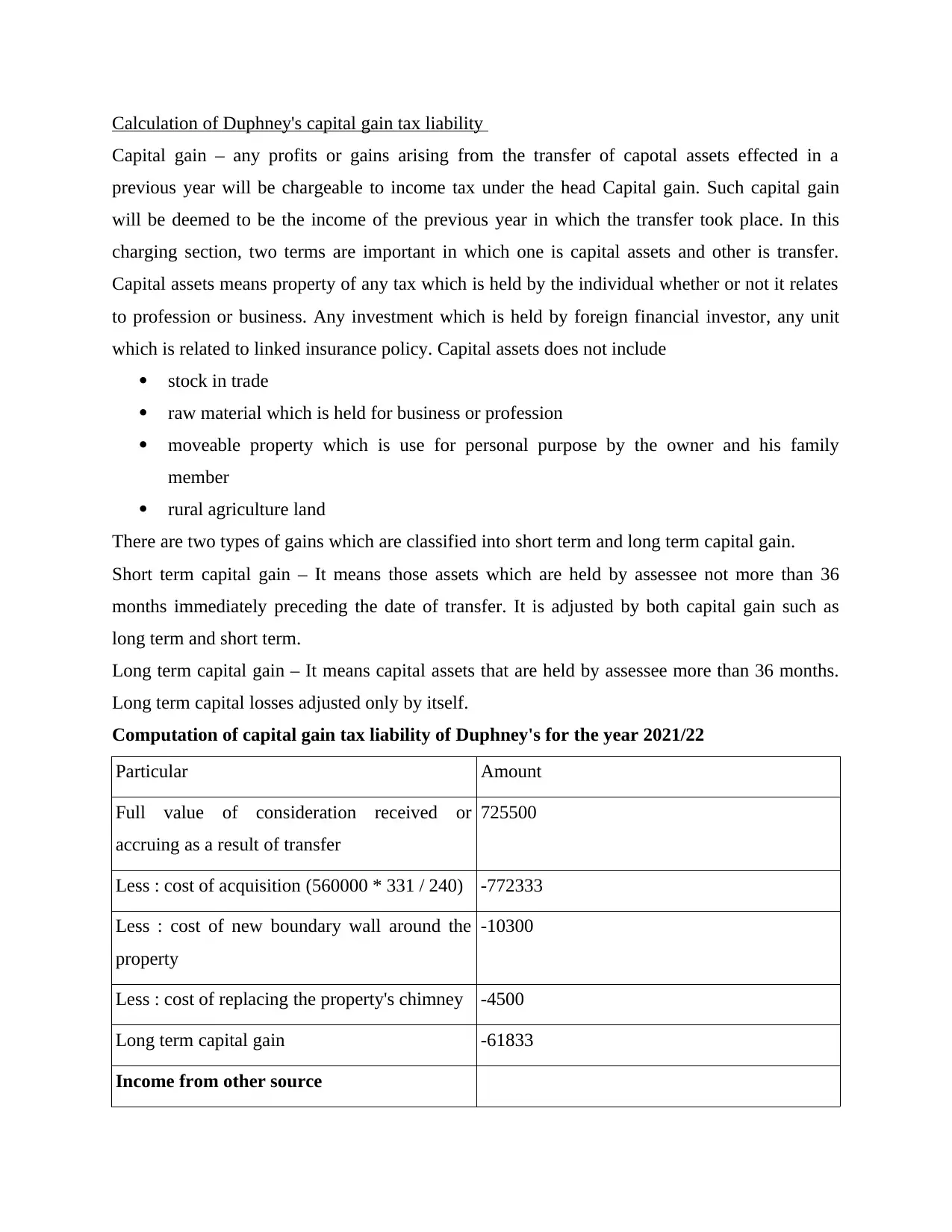

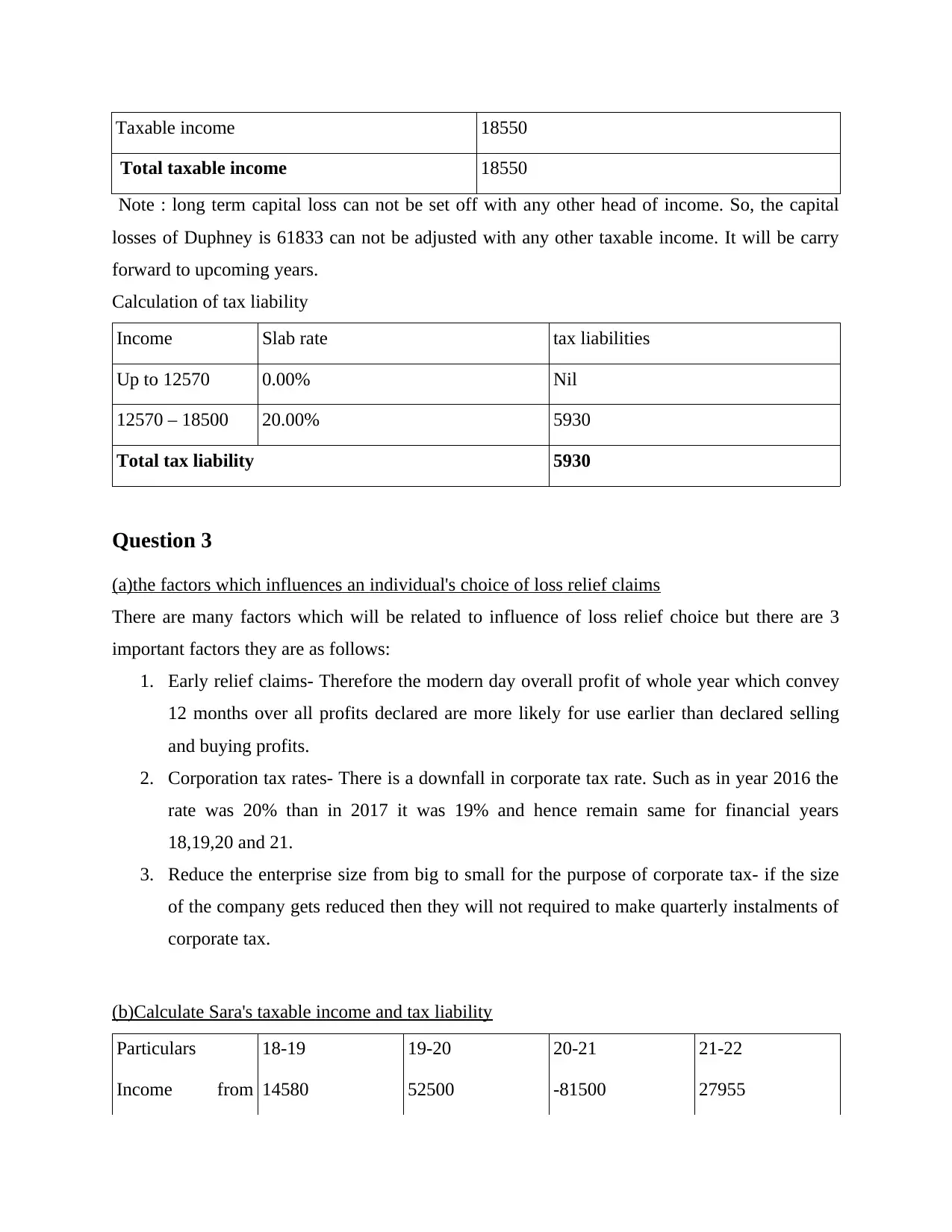

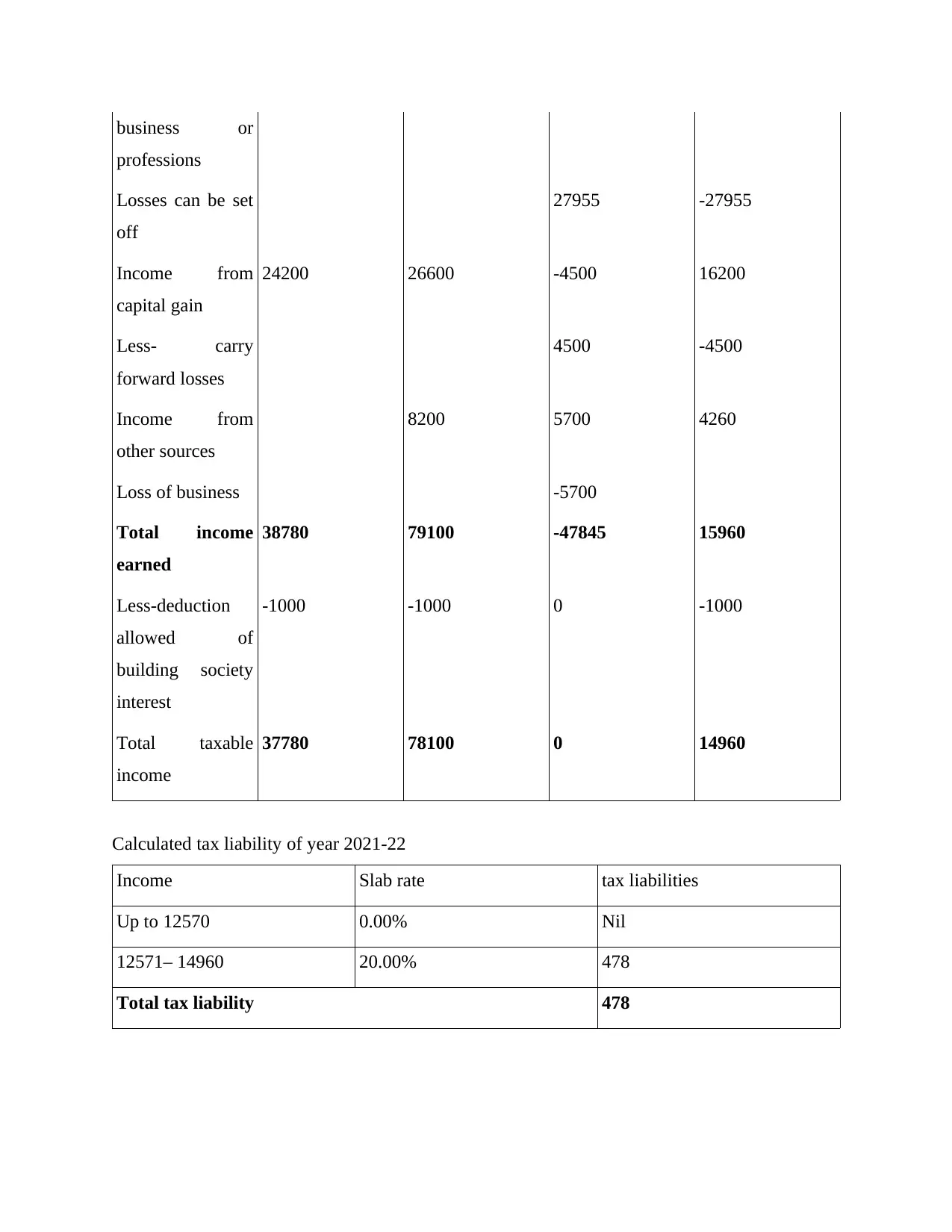

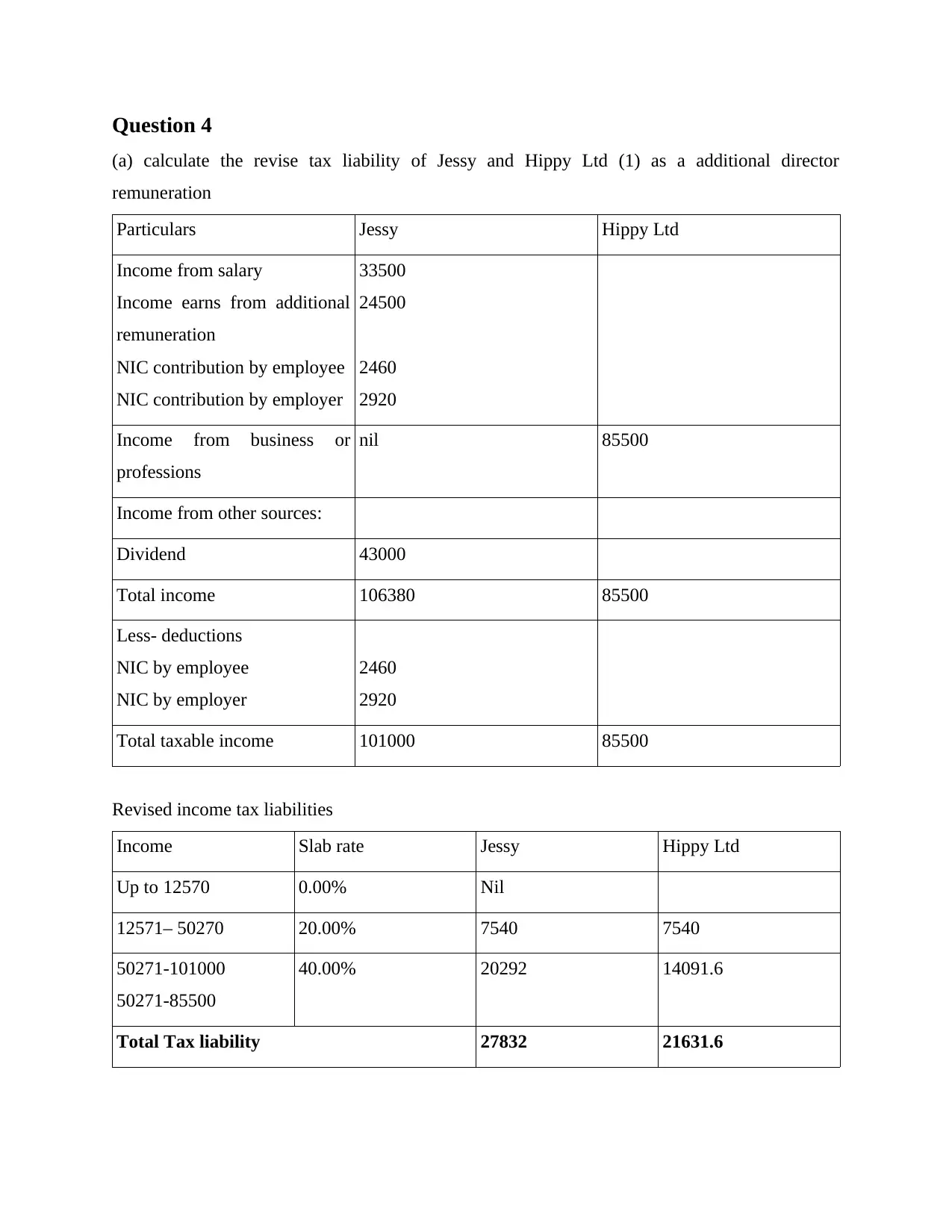

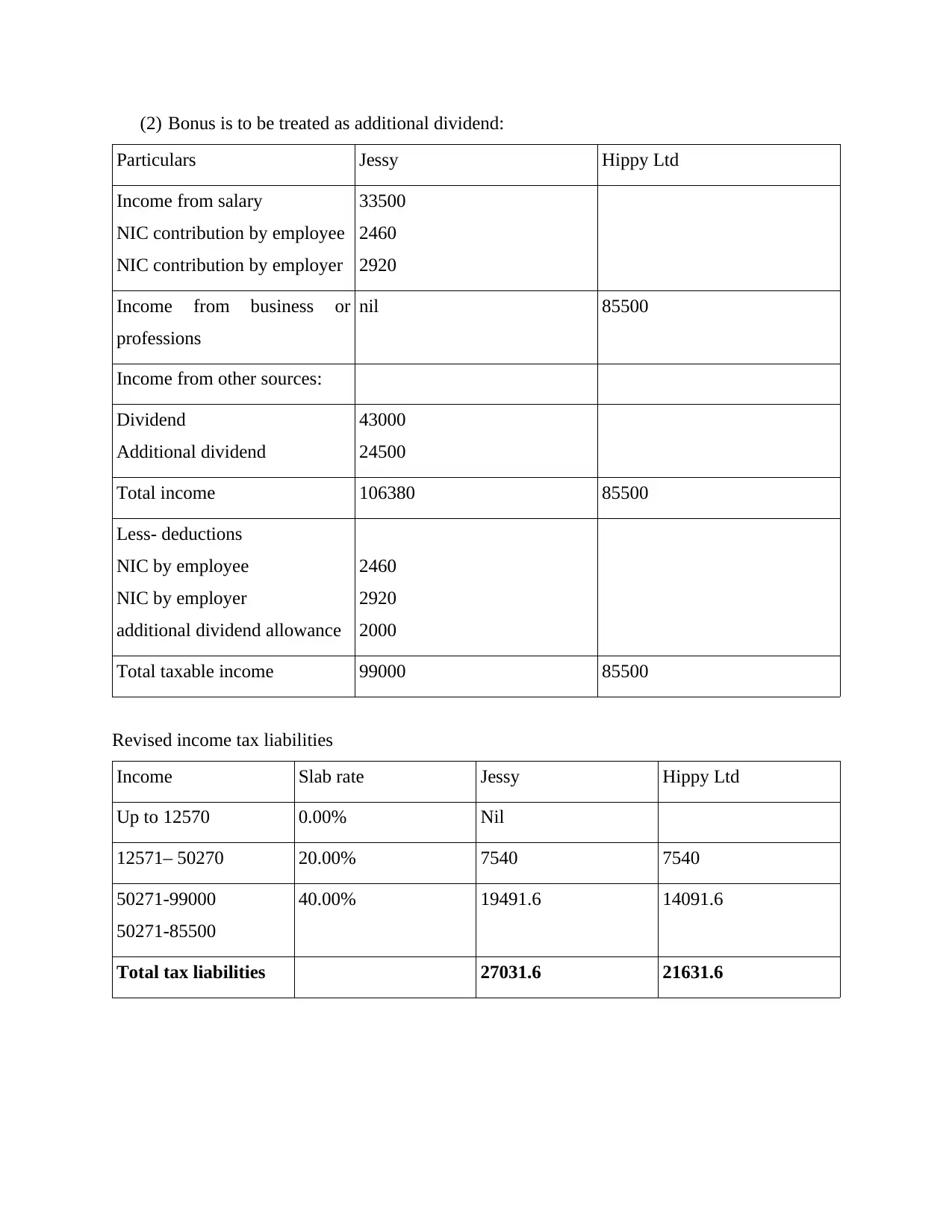

This assignment provides a comprehensive analysis of UK tax calculations, covering various aspects of income tax, inheritance tax, and capital gains tax. The solution begins with an introduction to accounting and taxation, defining different tax types and the sources of government revenue. It then details the steps involved in calculating income tax, including determining residential status, classifying income under different heads (salary, property, business, capital gains, and other sources), computing income under each head, and addressing exemptions, deductions, and loss set-offs. The assignment proceeds to calculate inheritance tax liabilities after death, capital gains tax, and factors influencing individual loss relief claims. It also calculates taxable income and tax liabilities for individuals and businesses, considering additional director remuneration and bonus payments. The solution concludes with references to relevant books and journals.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.