Report on UK Taxation: Tax Environment, Obligations, and Calculations

VerifiedAdded on 2020/02/03

|17

|4968

|303

Report

AI Summary

This report provides a detailed analysis of the UK taxation system. It begins with an introduction to the UK tax environment, outlining the roles and responsibilities of tax practitioners and the tax obligations of both taxpayers and agents, including the implications of non-compliance. The report then delves into practical calculations, including the determination of relevant income, expenses, and allowances for employed and self-employed individuals, along with the calculation of their respective tax liabilities and payment dates. Furthermore, it covers the completion of relevant documentation and tax returns. The report also includes the calculation of chargeable profits, tax liabilities, and income tax deductions, as well as the identification of chargeable assets, the calculation of capital gains and losses, and the determination of capital gains tax payable. The report provides a comprehensive overview of the UK tax system and its practical applications.

UK Taxation

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ...............................................................................................................................4

TASK 1.................................................................................................................................................4

1.1 UK tax environment ..................................................................................................................4

1.2 Roles and responsibilities of tax practitioners...........................................................................6

1.3 Tax obligations for the tax payers and agents and implications of non-compliance.................7

TASK 2 ................................................................................................................................................8

2.1 Calculate relevant income, expense and allowances.................................................................8

2.2 Calculating tax liabilities for employed and self-employed individuals and payment dates.....8

2.3 Complete relevant documentation and tax returns..................................................................10

TASK 3 ..............................................................................................................................................13

3.1 Calculation of chargeable profits.............................................................................................13

3.2 Calculation of tax liabilities and due payment dates...............................................................13

3.3 Explaining income tax deductions ..........................................................................................13

TASK 4...............................................................................................................................................13

4.1 Identify chargeable assets........................................................................................................13

4.2 Calculation of capital gains and losses....................................................................................14

4.3 Calculation of capital gains tax payable..................................................................................14

CONCLUSION..................................................................................................................................14

REFERENCES...................................................................................................................................15

2

INTRODUCTION ...............................................................................................................................4

TASK 1.................................................................................................................................................4

1.1 UK tax environment ..................................................................................................................4

1.2 Roles and responsibilities of tax practitioners...........................................................................6

1.3 Tax obligations for the tax payers and agents and implications of non-compliance.................7

TASK 2 ................................................................................................................................................8

2.1 Calculate relevant income, expense and allowances.................................................................8

2.2 Calculating tax liabilities for employed and self-employed individuals and payment dates.....8

2.3 Complete relevant documentation and tax returns..................................................................10

TASK 3 ..............................................................................................................................................13

3.1 Calculation of chargeable profits.............................................................................................13

3.2 Calculation of tax liabilities and due payment dates...............................................................13

3.3 Explaining income tax deductions ..........................................................................................13

TASK 4...............................................................................................................................................13

4.1 Identify chargeable assets........................................................................................................13

4.2 Calculation of capital gains and losses....................................................................................14

4.3 Calculation of capital gains tax payable..................................................................................14

CONCLUSION..................................................................................................................................14

REFERENCES...................................................................................................................................15

2

INTRODUCTION

In the United Kingdom, government imposes number of taxation obligations to both the

individuals as well as corporate sector. It is the main source of their income which is used by them

for economic welfare and development. Moreover, government make changes in the rules,

regulations and taxation provisions time to time for wider economic growth and success. Aim of the

present project report is to identify UK taxation environment, its structure and assessing the

obligatory provisions of tax payers for non-compliance of the same. Furthermore, assignment will

also focus on determining the roles and responsibilities of tax practitioners in making timely

taxation payment to the government. In addition to this, report will also calculate taxation liabilities

on chargeable income, capital gains and income tax deductions which are prescribed in the UK

taxation legislations.

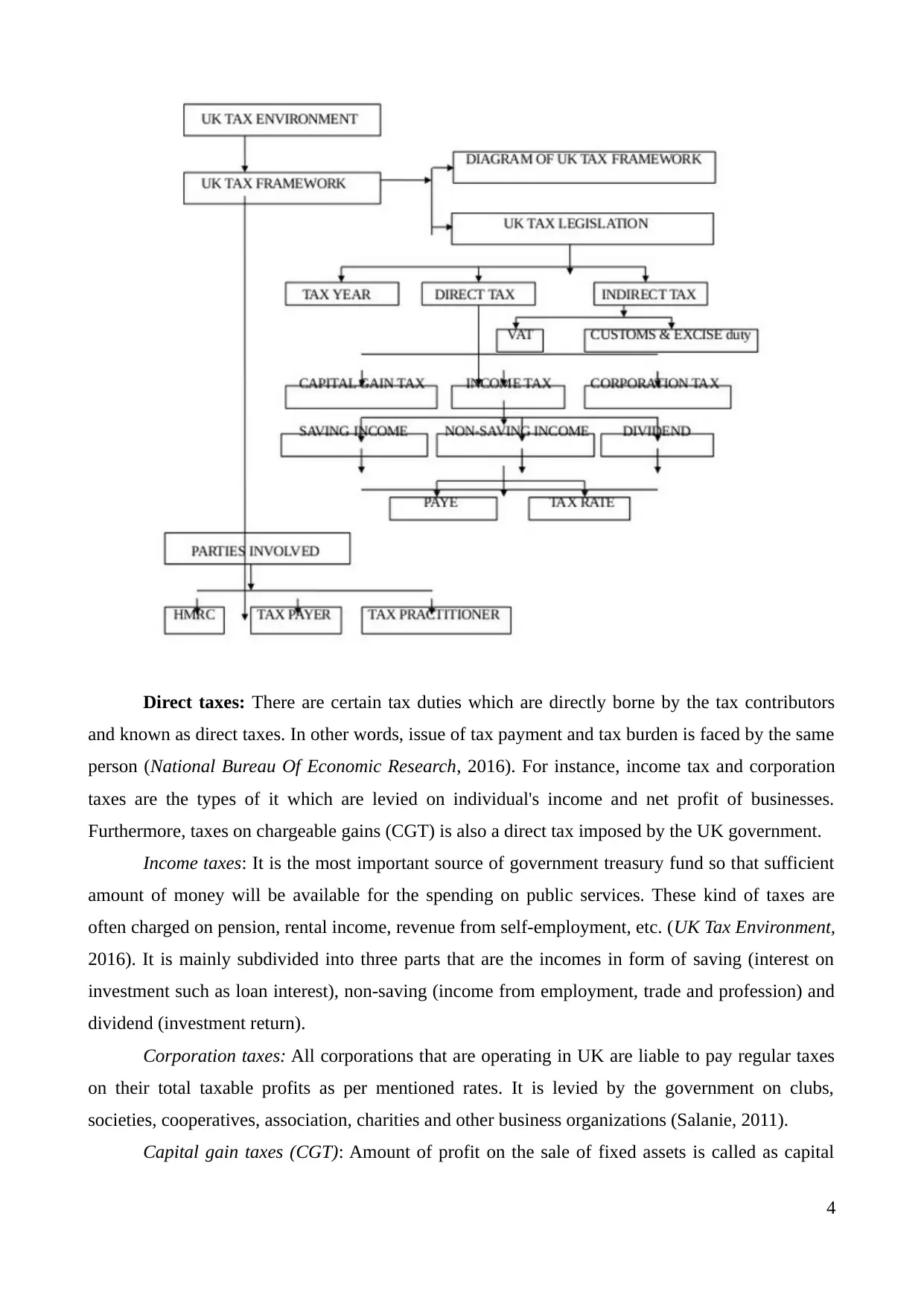

TASK 1

1.1 UK tax environment

As per the UK tax laws, every citizen whose total income is beyond the taxation limit is

responsible to pay taxation as per the prescribed rates. Tax is paid to the government via taxation

departments and Her Majesty's Revenues and Customs (HMRC). In UK, it is the responsibility of

HMRC to assure that every individual and corporation is paying timely taxes to the government so

that proper funds will be available in UK treasury for expenditures on public services, financial

support, safeguarding the monetary movements, enforcement activities, etc. (Jenkins, 2015).

According to the legislation, tax is calculated for every assessment year which ranges from 6th to 5th

April of the next year. There are two main categories of taxes imposed by the government that are

direct and indirect tax.

3

In the United Kingdom, government imposes number of taxation obligations to both the

individuals as well as corporate sector. It is the main source of their income which is used by them

for economic welfare and development. Moreover, government make changes in the rules,

regulations and taxation provisions time to time for wider economic growth and success. Aim of the

present project report is to identify UK taxation environment, its structure and assessing the

obligatory provisions of tax payers for non-compliance of the same. Furthermore, assignment will

also focus on determining the roles and responsibilities of tax practitioners in making timely

taxation payment to the government. In addition to this, report will also calculate taxation liabilities

on chargeable income, capital gains and income tax deductions which are prescribed in the UK

taxation legislations.

TASK 1

1.1 UK tax environment

As per the UK tax laws, every citizen whose total income is beyond the taxation limit is

responsible to pay taxation as per the prescribed rates. Tax is paid to the government via taxation

departments and Her Majesty's Revenues and Customs (HMRC). In UK, it is the responsibility of

HMRC to assure that every individual and corporation is paying timely taxes to the government so

that proper funds will be available in UK treasury for expenditures on public services, financial

support, safeguarding the monetary movements, enforcement activities, etc. (Jenkins, 2015).

According to the legislation, tax is calculated for every assessment year which ranges from 6th to 5th

April of the next year. There are two main categories of taxes imposed by the government that are

direct and indirect tax.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct taxes: There are certain tax duties which are directly borne by the tax contributors

and known as direct taxes. In other words, issue of tax payment and tax burden is faced by the same

person (National Bureau Of Economic Research, 2016). For instance, income tax and corporation

taxes are the types of it which are levied on individual's income and net profit of businesses.

Furthermore, taxes on chargeable gains (CGT) is also a direct tax imposed by the UK government.

Income taxes: It is the most important source of government treasury fund so that sufficient

amount of money will be available for the spending on public services. These kind of taxes are

often charged on pension, rental income, revenue from self-employment, etc. (UK Tax Environment,

2016). It is mainly subdivided into three parts that are the incomes in form of saving (interest on

investment such as loan interest), non-saving (income from employment, trade and profession) and

dividend (investment return).

Corporation taxes: All corporations that are operating in UK are liable to pay regular taxes

on their total taxable profits as per mentioned rates. It is levied by the government on clubs,

societies, cooperatives, association, charities and other business organizations (Salanie, 2011).

Capital gain taxes (CGT): Amount of profit on the sale of fixed assets is called as capital

4

and known as direct taxes. In other words, issue of tax payment and tax burden is faced by the same

person (National Bureau Of Economic Research, 2016). For instance, income tax and corporation

taxes are the types of it which are levied on individual's income and net profit of businesses.

Furthermore, taxes on chargeable gains (CGT) is also a direct tax imposed by the UK government.

Income taxes: It is the most important source of government treasury fund so that sufficient

amount of money will be available for the spending on public services. These kind of taxes are

often charged on pension, rental income, revenue from self-employment, etc. (UK Tax Environment,

2016). It is mainly subdivided into three parts that are the incomes in form of saving (interest on

investment such as loan interest), non-saving (income from employment, trade and profession) and

dividend (investment return).

Corporation taxes: All corporations that are operating in UK are liable to pay regular taxes

on their total taxable profits as per mentioned rates. It is levied by the government on clubs,

societies, cooperatives, association, charities and other business organizations (Salanie, 2011).

Capital gain taxes (CGT): Amount of profit on the sale of fixed assets is called as capital

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

gains and tax obligations on these profits are called CGT. It may be of two types, short-term as well

as long-term which is charged on gain resulting from the disposal a chargeable assets.

Indirect taxes: Another tax is indirect in which it is not actually bear by the person to whom

it has been levied (Sikka, 2015). The burden of tax is faced by another party such as custom duty,

excise duty, Value Added Taxes (VAT) etc.

All above taxes are charged by government by taking into consideration the equity principle

which states that tax structure or system must be fair for all tax contributors. Its progressive tax

structure indicates that all individuals whose income is equal will be obliged to pay taxes at same

rate and represent horizontal equity (Kaplow, 2011). However, as per the vertical equity, people that

are earning higher income will have to pay tax at high rate while lower earning people will have to

pay less amount of taxes. Central objective of equity cannon is to treat individuals favourably which

helps in effective redistribution of the income within community. Apart from this, schemes like

national insurance contribution, national insurance and non-contribution are also regulated and

administrated by the government.

1.2 Roles and responsibilities of tax practitioners

As already discussed, three parties; practitioners, contributors and HMRC are involved in

the UK tax framework. In this, practitioners are the people who prepare returns and file it on the

behalf of third party and in return, they get some fees or rewards. It is the legal obligation on

practitioners to work under the supervision of a certified accountant. They plays a significant role in

the UK taxation environment as their primary duty is to provide important advices and suggestions

to their clients in the preparation of an accurate tax return. Tax practitioners are the experts and

specialists in filling returns to the government as per statutory legislations. By this, contributors can

declare the right amount of tax obligations on their total taxable income while filling the return

(Sikka, 2015). With regard to the UK, practitioners assist contributors to show honest, authentic and

prominent information about their total taxable income and profit on which tax is needed to be paid.

They have responsibilities to accurately advise their clients according to the tax legislation and

jurisdiction. It is the duty of practitioners to make sure that entire data which is disclosed in the tax

return must be free from misleading information. Besides this, they also have to inform their clients

about the conflicts and issues in account’s auditing process. Apart from this, tax amendments and its

practical implications on reporting to the taxation authorities also need to be considered by the

practitioners (Gee, Haller and Nobes, 2010). For instance, keeping up-to-date their knowledge

according to the provisional changes in taxes on income, corporation taxes, auditing legislations and

its practices.

5

as long-term which is charged on gain resulting from the disposal a chargeable assets.

Indirect taxes: Another tax is indirect in which it is not actually bear by the person to whom

it has been levied (Sikka, 2015). The burden of tax is faced by another party such as custom duty,

excise duty, Value Added Taxes (VAT) etc.

All above taxes are charged by government by taking into consideration the equity principle

which states that tax structure or system must be fair for all tax contributors. Its progressive tax

structure indicates that all individuals whose income is equal will be obliged to pay taxes at same

rate and represent horizontal equity (Kaplow, 2011). However, as per the vertical equity, people that

are earning higher income will have to pay tax at high rate while lower earning people will have to

pay less amount of taxes. Central objective of equity cannon is to treat individuals favourably which

helps in effective redistribution of the income within community. Apart from this, schemes like

national insurance contribution, national insurance and non-contribution are also regulated and

administrated by the government.

1.2 Roles and responsibilities of tax practitioners

As already discussed, three parties; practitioners, contributors and HMRC are involved in

the UK tax framework. In this, practitioners are the people who prepare returns and file it on the

behalf of third party and in return, they get some fees or rewards. It is the legal obligation on

practitioners to work under the supervision of a certified accountant. They plays a significant role in

the UK taxation environment as their primary duty is to provide important advices and suggestions

to their clients in the preparation of an accurate tax return. Tax practitioners are the experts and

specialists in filling returns to the government as per statutory legislations. By this, contributors can

declare the right amount of tax obligations on their total taxable income while filling the return

(Sikka, 2015). With regard to the UK, practitioners assist contributors to show honest, authentic and

prominent information about their total taxable income and profit on which tax is needed to be paid.

They have responsibilities to accurately advise their clients according to the tax legislation and

jurisdiction. It is the duty of practitioners to make sure that entire data which is disclosed in the tax

return must be free from misleading information. Besides this, they also have to inform their clients

about the conflicts and issues in account’s auditing process. Apart from this, tax amendments and its

practical implications on reporting to the taxation authorities also need to be considered by the

practitioners (Gee, Haller and Nobes, 2010). For instance, keeping up-to-date their knowledge

according to the provisional changes in taxes on income, corporation taxes, auditing legislations and

its practices.

5

They play an important role as they gather information about their clients, calculate their

taxable income and report it to the UK tax authority, HMRC. With this, they can compute

individuals as well as organization’s tax liabilities and manage their treasury funds. However, in

case of disputes and conflicts, practitioners guide people on the basis of their technical skills,

knowledge and experience to resolve the same (Prahalathan, 2012). They are not involved in any

illegal activity like tax evasions which refers to deliver the misleading information to HMRC and

thereby, reduces their tax payments. Complying with the UK legislation, ethical code of conduct

and representing truthful information are some of the responsibilities of tax practitioners.

Furthermore, they should not disclose their client’s information to any of the external parties or

other clients. It is because, they are liable to maintain proper security and confidentiality of their

client’s information.

1.3 Tax obligations for the tax payers and agents and implications of non-compliance

Tax legislations comprises set of mandatory requirements which an individual and

corporation needs to follow while determining their tax liability. Tax compliance is a strict

adherence to the taxation provisions, rules and regulations. In other words, willingness of the tax

payers to follow UK tax laws strictly is known as compliance (Lymer and Oats, 2009). There are

several basic requirements which an individual needs to follow as per the taxation legislation as

outlined below:

Proper maintenance of books and accounts

Compute correct amount of taxable income

Timely filling of tax return to the UK taxation authority, HMRC

Timely payment of taxation liabilities

Payment of penalties for incorrect filling of return or delayed payment of tax obligations

Audit the accounts by an independent auditor for ensuring true and fair presentation of

financial performance (Emmerson and Tetlow, 2015)

In accordance with the UK tax legislation, it is the liability of every British citizen is to

strictly follow principles, provisions, norms and regulations as prescribed in different acts. In this, if

tax payers possess positive attitude towards UK tax system then they will be surely willing to pay

correct amount of taxes on due date. Contrary to this, breach and violation of taxation provisions

may result in imposing penalties, fines and other lawsuits on the defaulter person. In addition to

this, easiness and transparency of taxation system increases tax compliance whereas complexity

may result in tax evasions (Davis and et.al., 2015). Further, aggressive nature of tax authorities and

officials, high penalties, etc. build a negative attitude in the minds of tax payers which in turn may

6

taxable income and report it to the UK tax authority, HMRC. With this, they can compute

individuals as well as organization’s tax liabilities and manage their treasury funds. However, in

case of disputes and conflicts, practitioners guide people on the basis of their technical skills,

knowledge and experience to resolve the same (Prahalathan, 2012). They are not involved in any

illegal activity like tax evasions which refers to deliver the misleading information to HMRC and

thereby, reduces their tax payments. Complying with the UK legislation, ethical code of conduct

and representing truthful information are some of the responsibilities of tax practitioners.

Furthermore, they should not disclose their client’s information to any of the external parties or

other clients. It is because, they are liable to maintain proper security and confidentiality of their

client’s information.

1.3 Tax obligations for the tax payers and agents and implications of non-compliance

Tax legislations comprises set of mandatory requirements which an individual and

corporation needs to follow while determining their tax liability. Tax compliance is a strict

adherence to the taxation provisions, rules and regulations. In other words, willingness of the tax

payers to follow UK tax laws strictly is known as compliance (Lymer and Oats, 2009). There are

several basic requirements which an individual needs to follow as per the taxation legislation as

outlined below:

Proper maintenance of books and accounts

Compute correct amount of taxable income

Timely filling of tax return to the UK taxation authority, HMRC

Timely payment of taxation liabilities

Payment of penalties for incorrect filling of return or delayed payment of tax obligations

Audit the accounts by an independent auditor for ensuring true and fair presentation of

financial performance (Emmerson and Tetlow, 2015)

In accordance with the UK tax legislation, it is the liability of every British citizen is to

strictly follow principles, provisions, norms and regulations as prescribed in different acts. In this, if

tax payers possess positive attitude towards UK tax system then they will be surely willing to pay

correct amount of taxes on due date. Contrary to this, breach and violation of taxation provisions

may result in imposing penalties, fines and other lawsuits on the defaulter person. In addition to

this, easiness and transparency of taxation system increases tax compliance whereas complexity

may result in tax evasions (Davis and et.al., 2015). Further, aggressive nature of tax authorities and

officials, high penalties, etc. build a negative attitude in the minds of tax payers which in turn may

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

result in non-compliance of the same. Moreover, if HMRC officials found any misleading

information in the filled return then they will have full freedom or right to impose law suits on such

person. It is the power available to taxation authority to reduce individual behaviour of non-

compliance. It is because, tax contributors may feel afraid that if they will disclose wrong or

misleading information then they can be sent to the jail and also, they will become liable to pay fine

(Andrienko, Apps and Rees, 2016). Henceforth, they will take practitioner assistant for filling

correct tax return and pay it timely.

TASK 2

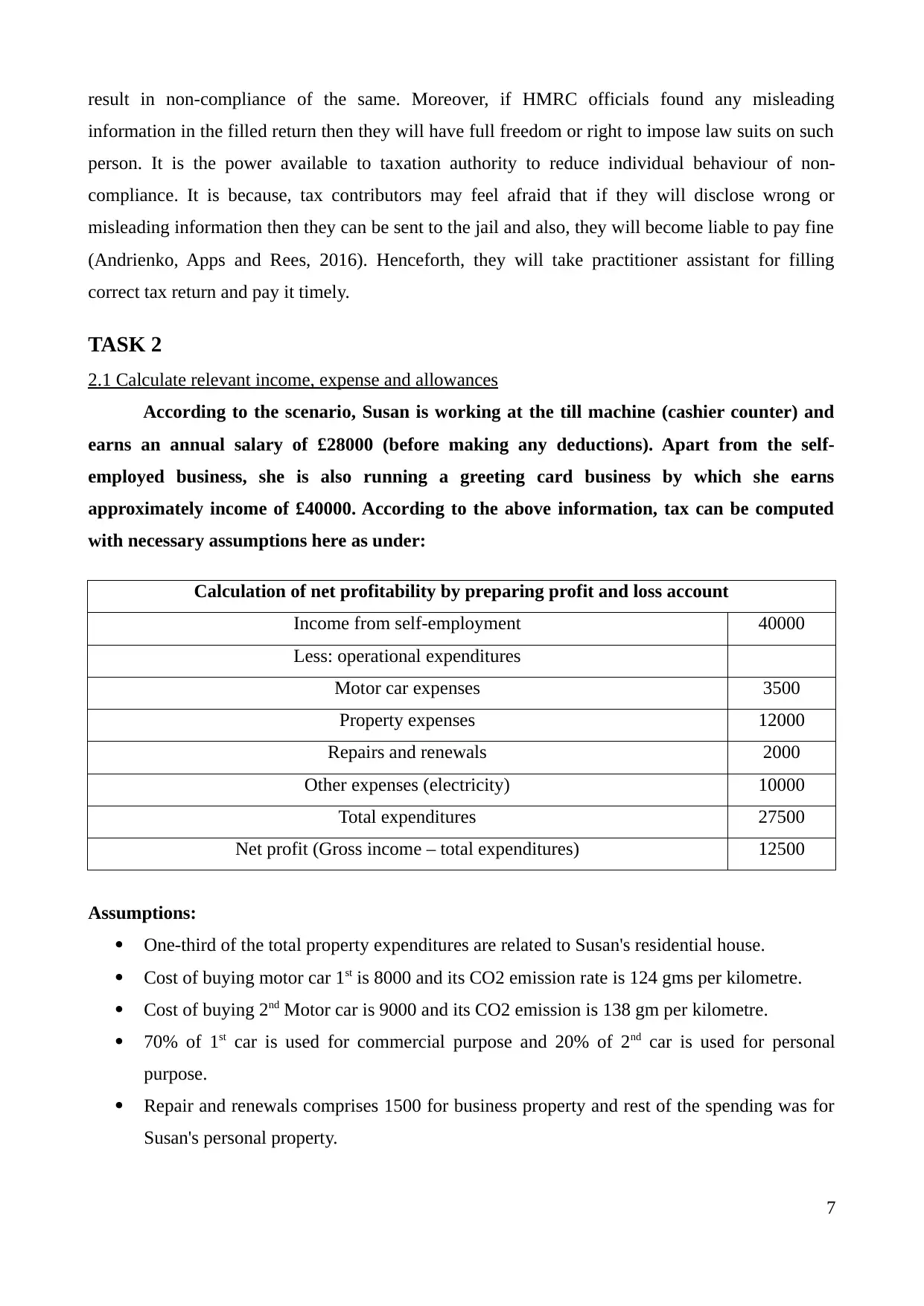

2.1 Calculate relevant income, expense and allowances

According to the scenario, Susan is working at the till machine (cashier counter) and

earns an annual salary of £28000 (before making any deductions). Apart from the self-

employed business, she is also running a greeting card business by which she earns

approximately income of £40000. According to the above information, tax can be computed

with necessary assumptions here as under:

Calculation of net profitability by preparing profit and loss account

Income from self-employment 40000

Less: operational expenditures

Motor car expenses 3500

Property expenses 12000

Repairs and renewals 2000

Other expenses (electricity) 10000

Total expenditures 27500

Net profit (Gross income – total expenditures) 12500

Assumptions:

One-third of the total property expenditures are related to Susan's residential house.

Cost of buying motor car 1st is 8000 and its CO2 emission rate is 124 gms per kilometre.

Cost of buying 2nd Motor car is 9000 and its CO2 emission is 138 gm per kilometre.

70% of 1st car is used for commercial purpose and 20% of 2nd car is used for personal

purpose.

Repair and renewals comprises 1500 for business property and rest of the spending was for

Susan's personal property.

7

information in the filled return then they will have full freedom or right to impose law suits on such

person. It is the power available to taxation authority to reduce individual behaviour of non-

compliance. It is because, tax contributors may feel afraid that if they will disclose wrong or

misleading information then they can be sent to the jail and also, they will become liable to pay fine

(Andrienko, Apps and Rees, 2016). Henceforth, they will take practitioner assistant for filling

correct tax return and pay it timely.

TASK 2

2.1 Calculate relevant income, expense and allowances

According to the scenario, Susan is working at the till machine (cashier counter) and

earns an annual salary of £28000 (before making any deductions). Apart from the self-

employed business, she is also running a greeting card business by which she earns

approximately income of £40000. According to the above information, tax can be computed

with necessary assumptions here as under:

Calculation of net profitability by preparing profit and loss account

Income from self-employment 40000

Less: operational expenditures

Motor car expenses 3500

Property expenses 12000

Repairs and renewals 2000

Other expenses (electricity) 10000

Total expenditures 27500

Net profit (Gross income – total expenditures) 12500

Assumptions:

One-third of the total property expenditures are related to Susan's residential house.

Cost of buying motor car 1st is 8000 and its CO2 emission rate is 124 gms per kilometre.

Cost of buying 2nd Motor car is 9000 and its CO2 emission is 138 gm per kilometre.

70% of 1st car is used for commercial purpose and 20% of 2nd car is used for personal

purpose.

Repair and renewals comprises 1500 for business property and rest of the spending was for

Susan's personal property.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

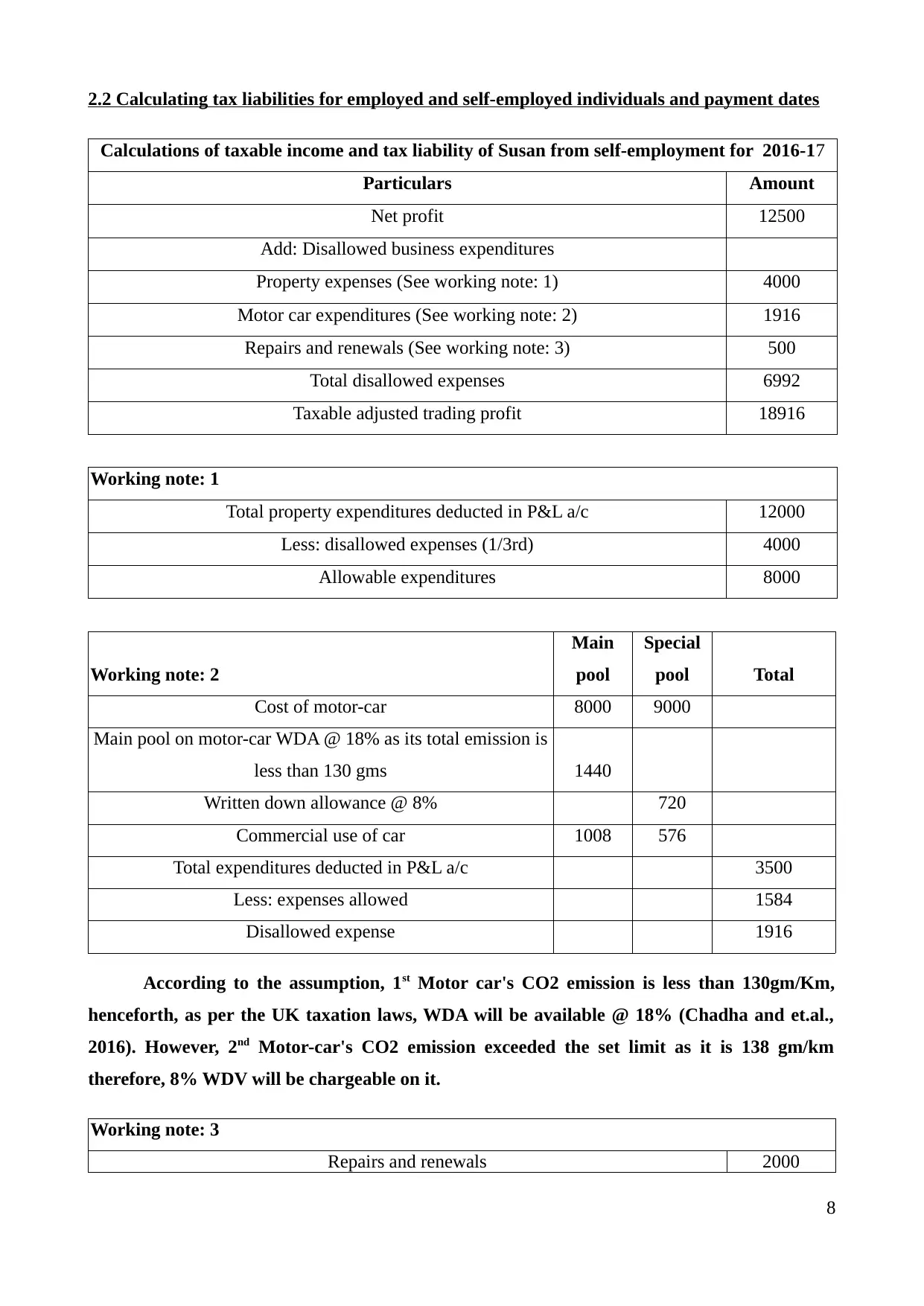

2.2 Calculating tax liabilities for employed and self-employed individuals and payment dates

Calculations of taxable income and tax liability of Susan from self-employment for 2016-17

Particulars Amount

Net profit 12500

Add: Disallowed business expenditures

Property expenses (See working note: 1) 4000

Motor car expenditures (See working note: 2) 1916

Repairs and renewals (See working note: 3) 500

Total disallowed expenses 6992

Taxable adjusted trading profit 18916

Working note: 1

Total property expenditures deducted in P&L a/c 12000

Less: disallowed expenses (1/3rd) 4000

Allowable expenditures 8000

Working note: 2

Main

pool

Special

pool Total

Cost of motor-car 8000 9000

Main pool on motor-car WDA @ 18% as its total emission is

less than 130 gms 1440

Written down allowance @ 8% 720

Commercial use of car 1008 576

Total expenditures deducted in P&L a/c 3500

Less: expenses allowed 1584

Disallowed expense 1916

According to the assumption, 1st Motor car's CO2 emission is less than 130gm/Km,

henceforth, as per the UK taxation laws, WDA will be available @ 18% (Chadha and et.al.,

2016). However, 2nd Motor-car's CO2 emission exceeded the set limit as it is 138 gm/km

therefore, 8% WDV will be chargeable on it.

Working note: 3

Repairs and renewals 2000

8

Calculations of taxable income and tax liability of Susan from self-employment for 2016-17

Particulars Amount

Net profit 12500

Add: Disallowed business expenditures

Property expenses (See working note: 1) 4000

Motor car expenditures (See working note: 2) 1916

Repairs and renewals (See working note: 3) 500

Total disallowed expenses 6992

Taxable adjusted trading profit 18916

Working note: 1

Total property expenditures deducted in P&L a/c 12000

Less: disallowed expenses (1/3rd) 4000

Allowable expenditures 8000

Working note: 2

Main

pool

Special

pool Total

Cost of motor-car 8000 9000

Main pool on motor-car WDA @ 18% as its total emission is

less than 130 gms 1440

Written down allowance @ 8% 720

Commercial use of car 1008 576

Total expenditures deducted in P&L a/c 3500

Less: expenses allowed 1584

Disallowed expense 1916

According to the assumption, 1st Motor car's CO2 emission is less than 130gm/Km,

henceforth, as per the UK taxation laws, WDA will be available @ 18% (Chadha and et.al.,

2016). However, 2nd Motor-car's CO2 emission exceeded the set limit as it is 138 gm/km

therefore, 8% WDV will be chargeable on it.

Working note: 3

Repairs and renewals 2000

8

Less: amount spent for the commercial property 1500

Disallowed expense 500

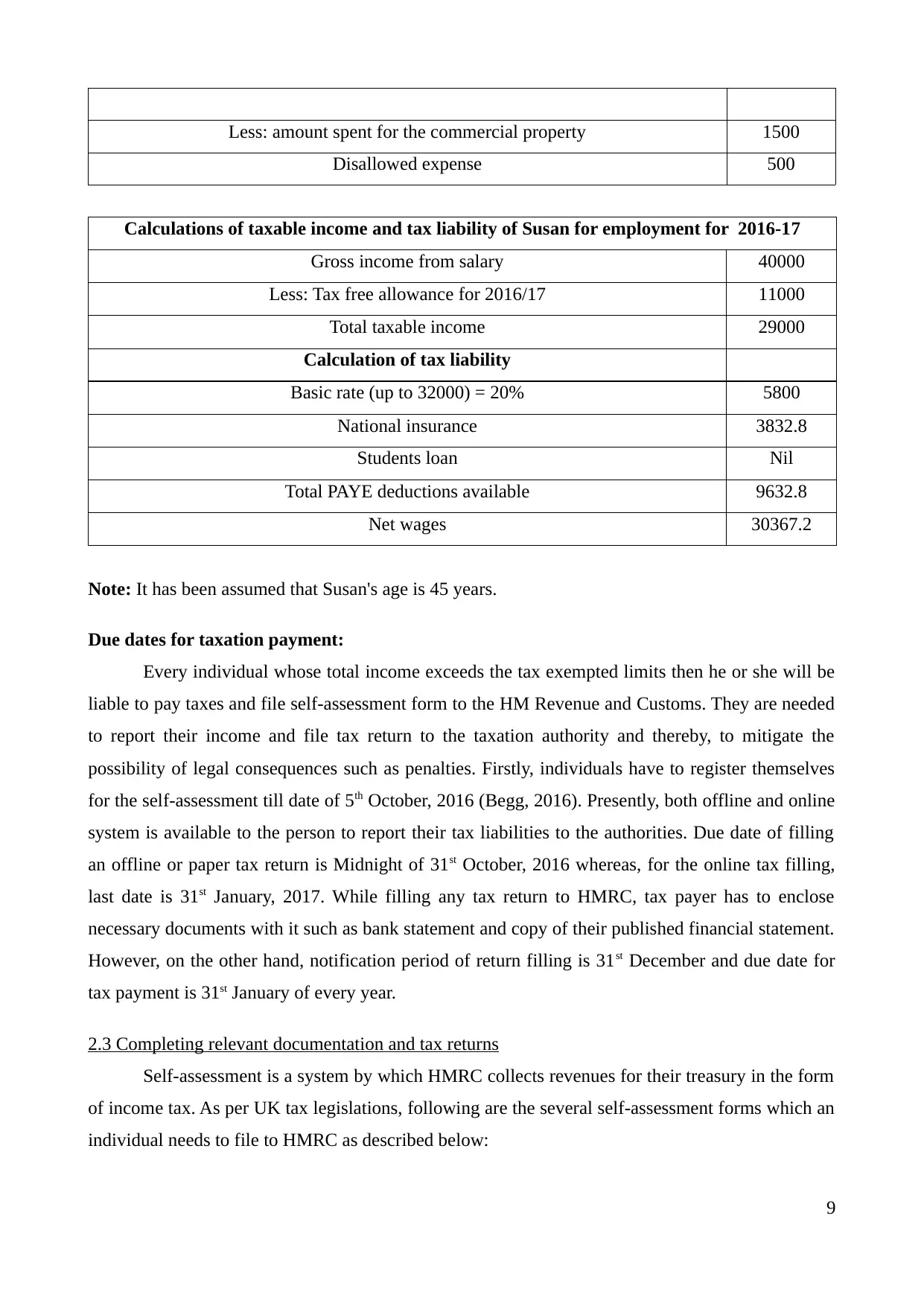

Calculations of taxable income and tax liability of Susan for employment for 2016-17

Gross income from salary 40000

Less: Tax free allowance for 2016/17 11000

Total taxable income 29000

Calculation of tax liability

Basic rate (up to 32000) = 20% 5800

National insurance 3832.8

Students loan Nil

Total PAYE deductions available 9632.8

Net wages 30367.2

Note: It has been assumed that Susan's age is 45 years.

Due dates for taxation payment:

Every individual whose total income exceeds the tax exempted limits then he or she will be

liable to pay taxes and file self-assessment form to the HM Revenue and Customs. They are needed

to report their income and file tax return to the taxation authority and thereby, to mitigate the

possibility of legal consequences such as penalties. Firstly, individuals have to register themselves

for the self-assessment till date of 5th October, 2016 (Begg, 2016). Presently, both offline and online

system is available to the person to report their tax liabilities to the authorities. Due date of filling

an offline or paper tax return is Midnight of 31st October, 2016 whereas, for the online tax filling,

last date is 31st January, 2017. While filling any tax return to HMRC, tax payer has to enclose

necessary documents with it such as bank statement and copy of their published financial statement.

However, on the other hand, notification period of return filling is 31st December and due date for

tax payment is 31st January of every year.

2.3 Completing relevant documentation and tax returns

Self-assessment is a system by which HMRC collects revenues for their treasury in the form

of income tax. As per UK tax legislations, following are the several self-assessment forms which an

individual needs to file to HMRC as described below:

9

Disallowed expense 500

Calculations of taxable income and tax liability of Susan for employment for 2016-17

Gross income from salary 40000

Less: Tax free allowance for 2016/17 11000

Total taxable income 29000

Calculation of tax liability

Basic rate (up to 32000) = 20% 5800

National insurance 3832.8

Students loan Nil

Total PAYE deductions available 9632.8

Net wages 30367.2

Note: It has been assumed that Susan's age is 45 years.

Due dates for taxation payment:

Every individual whose total income exceeds the tax exempted limits then he or she will be

liable to pay taxes and file self-assessment form to the HM Revenue and Customs. They are needed

to report their income and file tax return to the taxation authority and thereby, to mitigate the

possibility of legal consequences such as penalties. Firstly, individuals have to register themselves

for the self-assessment till date of 5th October, 2016 (Begg, 2016). Presently, both offline and online

system is available to the person to report their tax liabilities to the authorities. Due date of filling

an offline or paper tax return is Midnight of 31st October, 2016 whereas, for the online tax filling,

last date is 31st January, 2017. While filling any tax return to HMRC, tax payer has to enclose

necessary documents with it such as bank statement and copy of their published financial statement.

However, on the other hand, notification period of return filling is 31st December and due date for

tax payment is 31st January of every year.

2.3 Completing relevant documentation and tax returns

Self-assessment is a system by which HMRC collects revenues for their treasury in the form

of income tax. As per UK tax legislations, following are the several self-assessment forms which an

individual needs to file to HMRC as described below:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

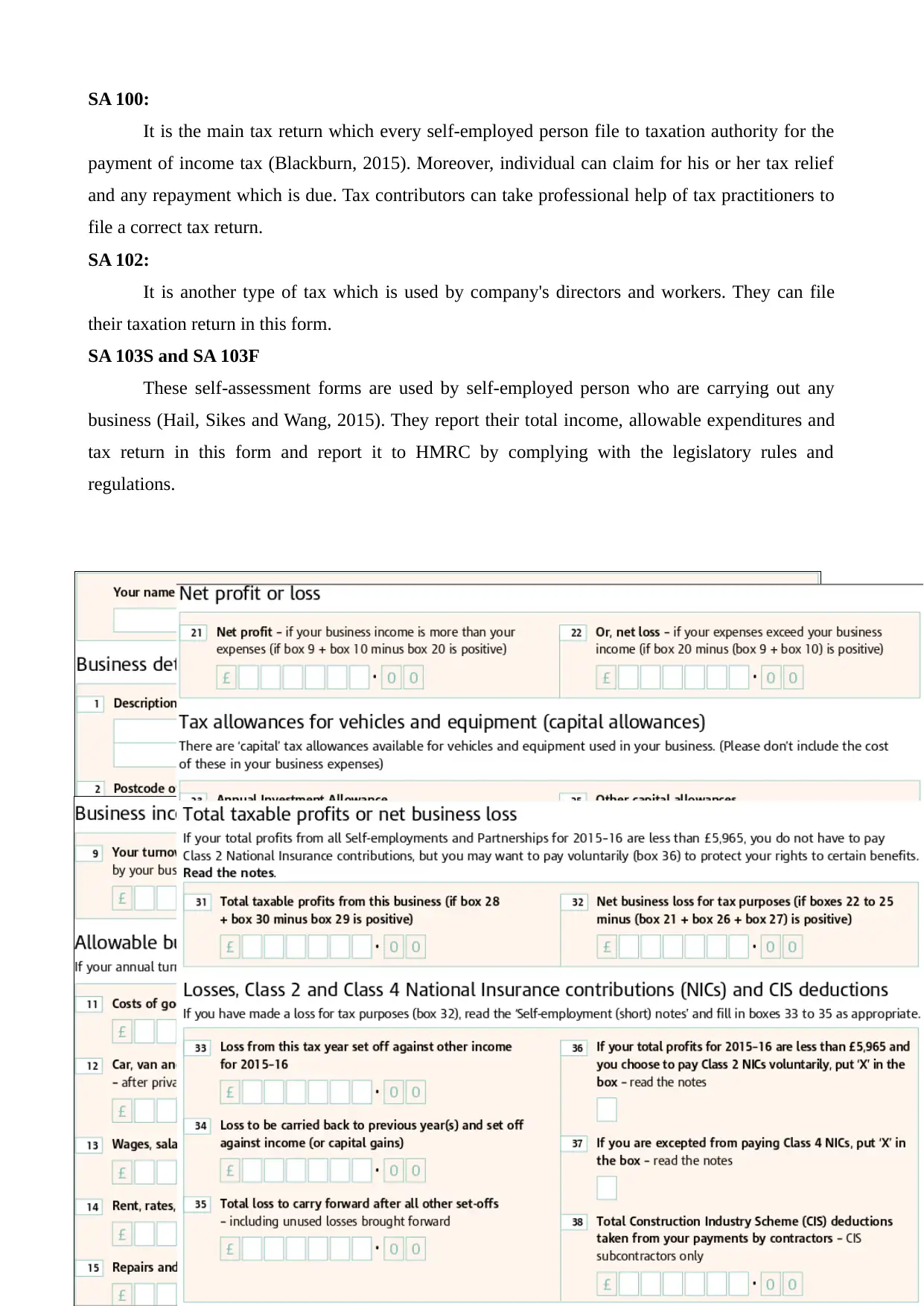

SA 100:

It is the main tax return which every self-employed person file to taxation authority for the

payment of income tax (Blackburn, 2015). Moreover, individual can claim for his or her tax relief

and any repayment which is due. Tax contributors can take professional help of tax practitioners to

file a correct tax return.

SA 102:

It is another type of tax which is used by company's directors and workers. They can file

their taxation return in this form.

SA 103S and SA 103F

These self-assessment forms are used by self-employed person who are carrying out any

business (Hail, Sikes and Wang, 2015). They report their total income, allowable expenditures and

tax return in this form and report it to HMRC by complying with the legislatory rules and

regulations.

10

It is the main tax return which every self-employed person file to taxation authority for the

payment of income tax (Blackburn, 2015). Moreover, individual can claim for his or her tax relief

and any repayment which is due. Tax contributors can take professional help of tax practitioners to

file a correct tax return.

SA 102:

It is another type of tax which is used by company's directors and workers. They can file

their taxation return in this form.

SA 103S and SA 103F

These self-assessment forms are used by self-employed person who are carrying out any

business (Hail, Sikes and Wang, 2015). They report their total income, allowable expenditures and

tax return in this form and report it to HMRC by complying with the legislatory rules and

regulations.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SA104S or SA104F

SA104S is used by business partners to report their short version of partnership business

income which is filed in SA 100 tax return. However, SA104F is used by them to record full income

from their partnership organization.

SA 105

This self-assessment form is used by the person to file their income from the property which

is situated in UK (Tiley and Loutzenhiser, 2012).

SA106

It is used to file individual's foreign or international revenues and profitability to the taxation

authorities.

TASK 3

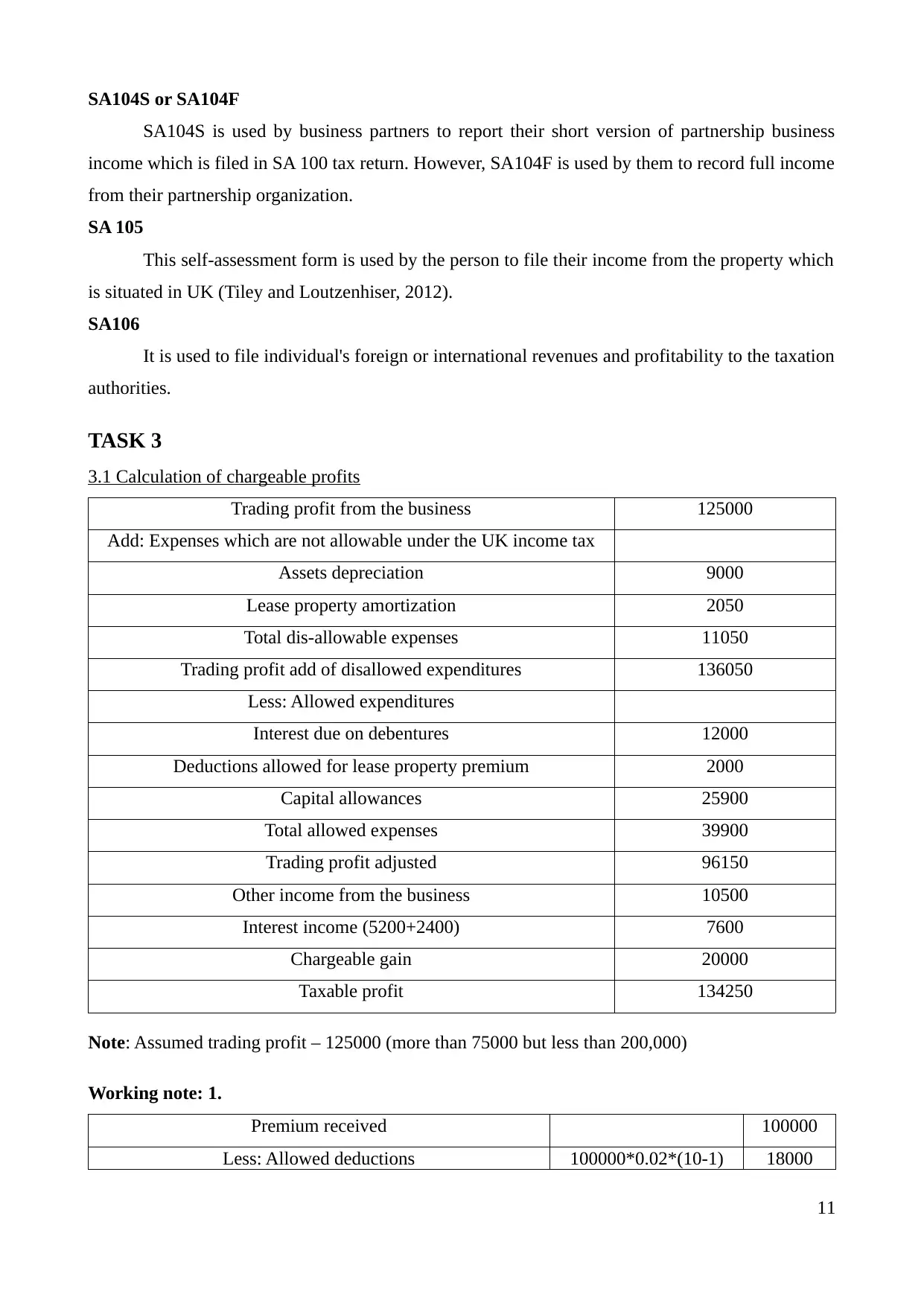

3.1 Calculation of chargeable profits

Trading profit from the business 125000

Add: Expenses which are not allowable under the UK income tax

Assets depreciation 9000

Lease property amortization 2050

Total dis-allowable expenses 11050

Trading profit add of disallowed expenditures 136050

Less: Allowed expenditures

Interest due on debentures 12000

Deductions allowed for lease property premium 2000

Capital allowances 25900

Total allowed expenses 39900

Trading profit adjusted 96150

Other income from the business 10500

Interest income (5200+2400) 7600

Chargeable gain 20000

Taxable profit 134250

Note: Assumed trading profit – 125000 (more than 75000 but less than 200,000)

Working note: 1.

Premium received 100000

Less: Allowed deductions 100000*0.02*(10-1) 18000

11

SA104S is used by business partners to report their short version of partnership business

income which is filed in SA 100 tax return. However, SA104F is used by them to record full income

from their partnership organization.

SA 105

This self-assessment form is used by the person to file their income from the property which

is situated in UK (Tiley and Loutzenhiser, 2012).

SA106

It is used to file individual's foreign or international revenues and profitability to the taxation

authorities.

TASK 3

3.1 Calculation of chargeable profits

Trading profit from the business 125000

Add: Expenses which are not allowable under the UK income tax

Assets depreciation 9000

Lease property amortization 2050

Total dis-allowable expenses 11050

Trading profit add of disallowed expenditures 136050

Less: Allowed expenditures

Interest due on debentures 12000

Deductions allowed for lease property premium 2000

Capital allowances 25900

Total allowed expenses 39900

Trading profit adjusted 96150

Other income from the business 10500

Interest income (5200+2400) 7600

Chargeable gain 20000

Taxable profit 134250

Note: Assumed trading profit – 125000 (more than 75000 but less than 200,000)

Working note: 1.

Premium received 100000

Less: Allowed deductions 100000*0.02*(10-1) 18000

11

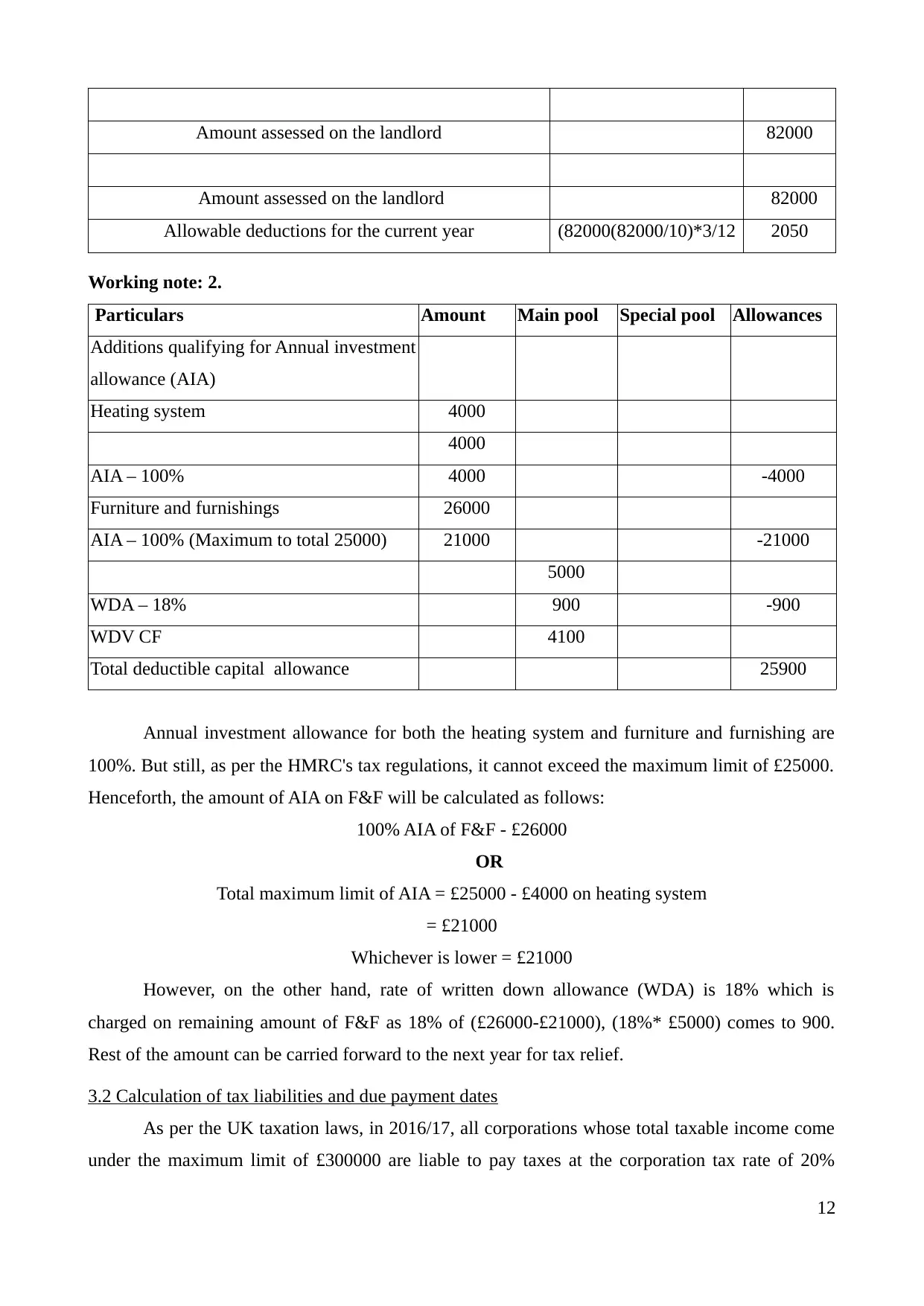

Amount assessed on the landlord 82000

Amount assessed on the landlord 82000

Allowable deductions for the current year (82000(82000/10)*3/12 2050

Working note: 2.

Particulars Amount Main pool Special pool Allowances

Additions qualifying for Annual investment

allowance (AIA)

Heating system 4000

4000

AIA – 100% 4000 -4000

Furniture and furnishings 26000

AIA – 100% (Maximum to total 25000) 21000 -21000

5000

WDA – 18% 900 -900

WDV CF 4100

Total deductible capital allowance 25900

Annual investment allowance for both the heating system and furniture and furnishing are

100%. But still, as per the HMRC's tax regulations, it cannot exceed the maximum limit of £25000.

Henceforth, the amount of AIA on F&F will be calculated as follows:

100% AIA of F&F - £26000

OR

Total maximum limit of AIA = £25000 - £4000 on heating system

= £21000

Whichever is lower = £21000

However, on the other hand, rate of written down allowance (WDA) is 18% which is

charged on remaining amount of F&F as 18% of (£26000-£21000), (18%* £5000) comes to 900.

Rest of the amount can be carried forward to the next year for tax relief.

3.2 Calculation of tax liabilities and due payment dates

As per the UK taxation laws, in 2016/17, all corporations whose total taxable income come

under the maximum limit of £300000 are liable to pay taxes at the corporation tax rate of 20%

12

Amount assessed on the landlord 82000

Allowable deductions for the current year (82000(82000/10)*3/12 2050

Working note: 2.

Particulars Amount Main pool Special pool Allowances

Additions qualifying for Annual investment

allowance (AIA)

Heating system 4000

4000

AIA – 100% 4000 -4000

Furniture and furnishings 26000

AIA – 100% (Maximum to total 25000) 21000 -21000

5000

WDA – 18% 900 -900

WDV CF 4100

Total deductible capital allowance 25900

Annual investment allowance for both the heating system and furniture and furnishing are

100%. But still, as per the HMRC's tax regulations, it cannot exceed the maximum limit of £25000.

Henceforth, the amount of AIA on F&F will be calculated as follows:

100% AIA of F&F - £26000

OR

Total maximum limit of AIA = £25000 - £4000 on heating system

= £21000

Whichever is lower = £21000

However, on the other hand, rate of written down allowance (WDA) is 18% which is

charged on remaining amount of F&F as 18% of (£26000-£21000), (18%* £5000) comes to 900.

Rest of the amount can be carried forward to the next year for tax relief.

3.2 Calculation of tax liabilities and due payment dates

As per the UK taxation laws, in 2016/17, all corporations whose total taxable income come

under the maximum limit of £300000 are liable to pay taxes at the corporation tax rate of 20%

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.