Report on UK Taxation: System, Policies, and Practitioner Roles

VerifiedAdded on 2019/12/28

|19

|5326

|69

Report

AI Summary

This report provides a comprehensive analysis of the UK taxation system, examining various aspects such as different types of taxes (direct and indirect), including income tax, corporation tax, capital gains tax, VAT, and council tax. It explores the role of tax practitioners in assisting taxpayers with tax compliance, preparing accurate tax returns, and minimizing liabilities. The report also outlines the obligations of taxpayers, including honesty, cooperation, and timely submission of documents and payments, while also detailing the penalties for non-compliance. Furthermore, it includes calculations of net profitability and tax liabilities for both employed and self-employed individuals, considering various business expenditures and adjustments, providing a practical application of the tax principles discussed. The report emphasizes the importance of understanding and adhering to UK tax laws and regulations, and the role of HMRC in administering the taxation system.

Taxation

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

1.1....................................................................................................................................................4

1.2....................................................................................................................................................6

1.3....................................................................................................................................................7

TASK 2.................................................................................................................................................8

2.1....................................................................................................................................................8

2.2 ...................................................................................................................................................9

2.3..................................................................................................................................................10

TASK 3...............................................................................................................................................11

3.1..................................................................................................................................................11

3.2..................................................................................................................................................12

3.3..................................................................................................................................................12

4.1..................................................................................................................................................13

4.2..................................................................................................................................................13

4.3..................................................................................................................................................13

CONCLUSION..................................................................................................................................14

REFERENCES...................................................................................................................................16

2

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

1.1....................................................................................................................................................4

1.2....................................................................................................................................................6

1.3....................................................................................................................................................7

TASK 2.................................................................................................................................................8

2.1....................................................................................................................................................8

2.2 ...................................................................................................................................................9

2.3..................................................................................................................................................10

TASK 3...............................................................................................................................................11

3.1..................................................................................................................................................11

3.2..................................................................................................................................................12

3.3..................................................................................................................................................12

4.1..................................................................................................................................................13

4.2..................................................................................................................................................13

4.3..................................................................................................................................................13

CONCLUSION..................................................................................................................................14

REFERENCES...................................................................................................................................16

2

Index of Tables

Table 1: Calculation of net profitability by P&L a/c............................................................................8

Table 2: Computation of total taxable earnings and tax liability for 2016/17......................................9

Table 3: Calculations of taxable income and tax liability of Susan for employment for 2016-17....10

Table 4: Calculation of tax liability of Susan for 2016/17.................................................................10

Table 5: Calculation of chargeable profit for 2016/17........................................................................11

Table 6: Calculation of tax liability for 2016/17................................................................................12

Table 7: Calculation of capital gain taxes of Mr. Lucy for the year 2016-17.....................................14

3

Table 1: Calculation of net profitability by P&L a/c............................................................................8

Table 2: Computation of total taxable earnings and tax liability for 2016/17......................................9

Table 3: Calculations of taxable income and tax liability of Susan for employment for 2016-17....10

Table 4: Calculation of tax liability of Susan for 2016/17.................................................................10

Table 5: Calculation of chargeable profit for 2016/17........................................................................11

Table 6: Calculation of tax liability for 2016/17................................................................................12

Table 7: Calculation of capital gain taxes of Mr. Lucy for the year 2016-17.....................................14

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Every nation's government make taxation laws and regulations which all the citizens needs

to follow strictly, otherwise, it can arise legal obligations. Generally, tax is regarded as a process of

raising governmental funds to spend it on the public services such as health, safety and security,

education and society welfare. Referring UK, there are number of taxes levied by the government

such as corporation tax, income tax, capital gain taxes (CGT) etc. Moreover, its tax legislations

provide a clear understanding of the necessary provisions, rules and regulations, through which,

regulatory bodies can maintain control over the taxation system and framework.

The aim of this assignment is to conduct an in-depth evaluation and analysis of UK tax

environment, its policies and overall system. Through this, readers will be able to identifying

different types of taxes, including both the direct and indirect. Moreover, the role of tax

practitioners will be identified in adherence to tax compliance. Along with this, taxation liabilities

and tax payable will be calculated by taking into consideration the laws and policies. Furthermore,

it is also necessary for the British citizens to file their respective tax return from different source of

income in prescribed forms. Therefore, the report will make an analysis of various tax return forms

in which taxable amount needs to be file to the taxation authority.

TASK 1

1.1

4

Every nation's government make taxation laws and regulations which all the citizens needs

to follow strictly, otherwise, it can arise legal obligations. Generally, tax is regarded as a process of

raising governmental funds to spend it on the public services such as health, safety and security,

education and society welfare. Referring UK, there are number of taxes levied by the government

such as corporation tax, income tax, capital gain taxes (CGT) etc. Moreover, its tax legislations

provide a clear understanding of the necessary provisions, rules and regulations, through which,

regulatory bodies can maintain control over the taxation system and framework.

The aim of this assignment is to conduct an in-depth evaluation and analysis of UK tax

environment, its policies and overall system. Through this, readers will be able to identifying

different types of taxes, including both the direct and indirect. Moreover, the role of tax

practitioners will be identified in adherence to tax compliance. Along with this, taxation liabilities

and tax payable will be calculated by taking into consideration the laws and policies. Furthermore,

it is also necessary for the British citizens to file their respective tax return from different source of

income in prescribed forms. Therefore, the report will make an analysis of various tax return forms

in which taxable amount needs to be file to the taxation authority.

TASK 1

1.1

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

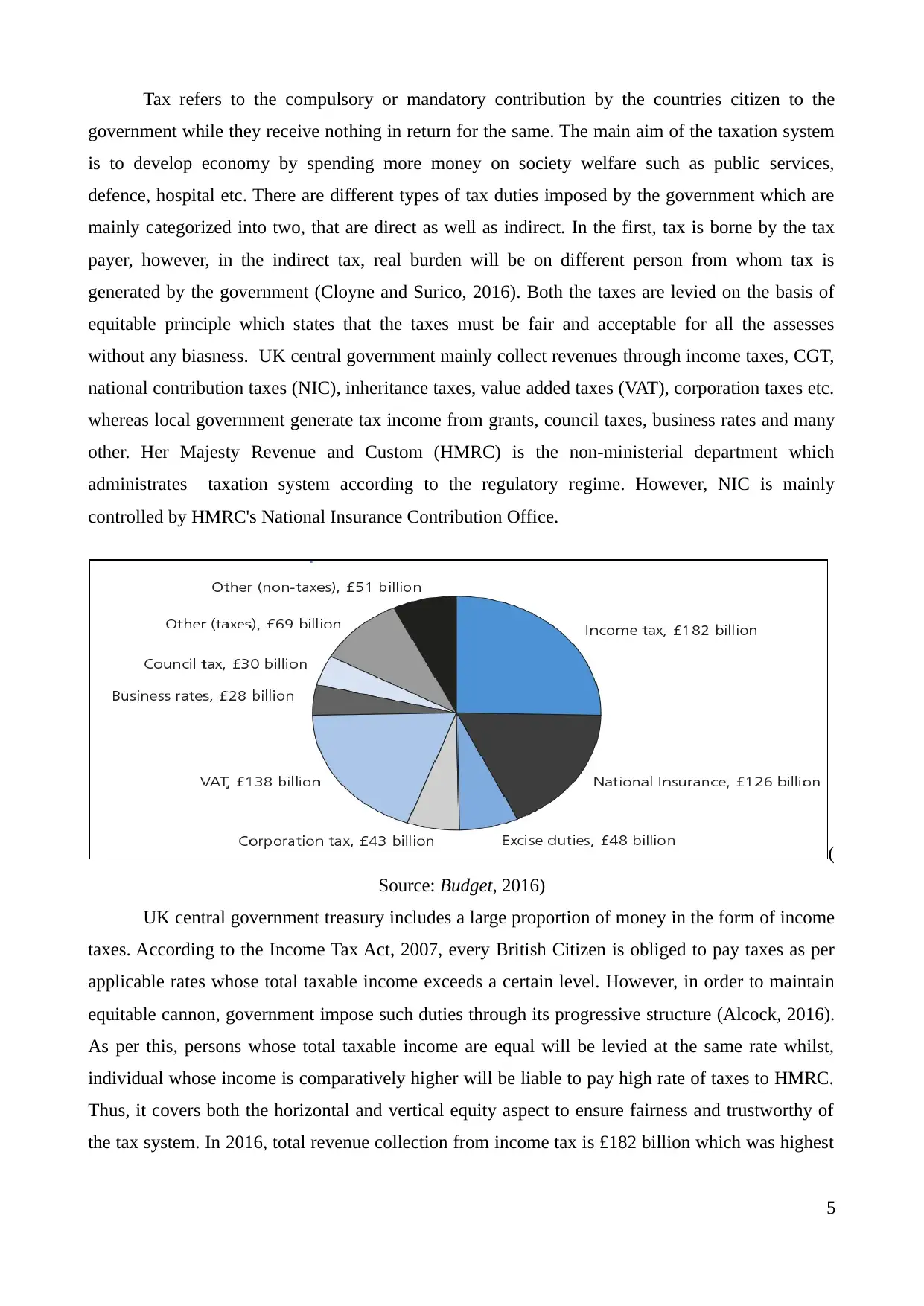

Tax refers to the compulsory or mandatory contribution by the countries citizen to the

government while they receive nothing in return for the same. The main aim of the taxation system

is to develop economy by spending more money on society welfare such as public services,

defence, hospital etc. There are different types of tax duties imposed by the government which are

mainly categorized into two, that are direct as well as indirect. In the first, tax is borne by the tax

payer, however, in the indirect tax, real burden will be on different person from whom tax is

generated by the government (Cloyne and Surico, 2016). Both the taxes are levied on the basis of

equitable principle which states that the taxes must be fair and acceptable for all the assesses

without any biasness. UK central government mainly collect revenues through income taxes, CGT,

national contribution taxes (NIC), inheritance taxes, value added taxes (VAT), corporation taxes etc.

whereas local government generate tax income from grants, council taxes, business rates and many

other. Her Majesty Revenue and Custom (HMRC) is the non-ministerial department which

administrates taxation system according to the regulatory regime. However, NIC is mainly

controlled by HMRC's National Insurance Contribution Office.

(

Source: Budget, 2016)

UK central government treasury includes a large proportion of money in the form of income

taxes. According to the Income Tax Act, 2007, every British Citizen is obliged to pay taxes as per

applicable rates whose total taxable income exceeds a certain level. However, in order to maintain

equitable cannon, government impose such duties through its progressive structure (Alcock, 2016).

As per this, persons whose total taxable income are equal will be levied at the same rate whilst,

individual whose income is comparatively higher will be liable to pay high rate of taxes to HMRC.

Thus, it covers both the horizontal and vertical equity aspect to ensure fairness and trustworthy of

the tax system. In 2016, total revenue collection from income tax is £182 billion which was highest

5

government while they receive nothing in return for the same. The main aim of the taxation system

is to develop economy by spending more money on society welfare such as public services,

defence, hospital etc. There are different types of tax duties imposed by the government which are

mainly categorized into two, that are direct as well as indirect. In the first, tax is borne by the tax

payer, however, in the indirect tax, real burden will be on different person from whom tax is

generated by the government (Cloyne and Surico, 2016). Both the taxes are levied on the basis of

equitable principle which states that the taxes must be fair and acceptable for all the assesses

without any biasness. UK central government mainly collect revenues through income taxes, CGT,

national contribution taxes (NIC), inheritance taxes, value added taxes (VAT), corporation taxes etc.

whereas local government generate tax income from grants, council taxes, business rates and many

other. Her Majesty Revenue and Custom (HMRC) is the non-ministerial department which

administrates taxation system according to the regulatory regime. However, NIC is mainly

controlled by HMRC's National Insurance Contribution Office.

(

Source: Budget, 2016)

UK central government treasury includes a large proportion of money in the form of income

taxes. According to the Income Tax Act, 2007, every British Citizen is obliged to pay taxes as per

applicable rates whose total taxable income exceeds a certain level. However, in order to maintain

equitable cannon, government impose such duties through its progressive structure (Alcock, 2016).

As per this, persons whose total taxable income are equal will be levied at the same rate whilst,

individual whose income is comparatively higher will be liable to pay high rate of taxes to HMRC.

Thus, it covers both the horizontal and vertical equity aspect to ensure fairness and trustworthy of

the tax system. In 2016, total revenue collection from income tax is £182 billion which was highest

5

as compare to other tax forms. However, on the other side, NICs comprises both employees and

employers contributions on the basis of their earnings for some state benefits. This is assembled by

the HMRC through the “Pay As You Earn” system, denoted as PAYE (Jenkins, 2016). According to

the above graph, in 2016, HMRC generated £126 billion amount by NIC which was the second

largest source after income tax.

Contrary to this, all the UK based corporations like association, societies, clubs, co-

operations and other unincorporated bodies have to pay taxes on their total taxable gain generated

through operations, known as corporation tax. Classical, imputation and split rate system are the

main basis of taxing such gains and business profitability. In 2016, its total tax payments by the

corporations was £43 billion. However, inheritance tax is levied on the fund obtained in the form of

gift or transfer of property (Cloyne and Surico, 2016). Despite this, council tax is a type of local tax

which is imposed on domestic properties situated in England, Scottland and Wales. In addition to

this, UK national government impose VAT on the business earnings generated through sale of goods

and services. It was the 3rd highest contributor to government treasury as in 2016, it was 138 billion

pound. Apart from this, CGT is levied by the government on the gains or profits through the

disposal of long-term capital assets like plant and machinery, land and building and many others.

1.2

Every individual is not perfectly well-known with the different types of tax policies, rules

and regulations as they have only the basic knowledge of it. Therefore, specialists help assesses to

prepare accurate tax return and file it to HMRC, known as tax practitioners. They play an

inexorable role in the UK tax environment and also indirectly assist taxation authorities to generate

timely and right amount of taxes from the contributors. It must be keep in mind that this are not the

accountants, but still, they have well-knowledge of accounting because they are already trained

persons (Devereux, Liu and Loretz, 2014). It is the legal requirement for the practitioners to pursue

an exam and after passing, they have to work under the supervision of either a licensed or certified

accountant. It is essential for them to complete required qualification and obtain degree, so that,

they will be eligible to give legal advices to their clients.

Roles

The roles and responsibilities of practitioners are highly dependent upon whether he or she

is a certified public accountant (CPA) or licensed taxation specialists. Mainly, they have to prepare

necessary documents and arrange it appropriately for filling tax return. They works as an

intermediaries between tax payers and collectors (HMRC) as they submit required information to

the regulatory body, HMRC on the behalf of the contributors. Such specialists assist assesses to

6

employers contributions on the basis of their earnings for some state benefits. This is assembled by

the HMRC through the “Pay As You Earn” system, denoted as PAYE (Jenkins, 2016). According to

the above graph, in 2016, HMRC generated £126 billion amount by NIC which was the second

largest source after income tax.

Contrary to this, all the UK based corporations like association, societies, clubs, co-

operations and other unincorporated bodies have to pay taxes on their total taxable gain generated

through operations, known as corporation tax. Classical, imputation and split rate system are the

main basis of taxing such gains and business profitability. In 2016, its total tax payments by the

corporations was £43 billion. However, inheritance tax is levied on the fund obtained in the form of

gift or transfer of property (Cloyne and Surico, 2016). Despite this, council tax is a type of local tax

which is imposed on domestic properties situated in England, Scottland and Wales. In addition to

this, UK national government impose VAT on the business earnings generated through sale of goods

and services. It was the 3rd highest contributor to government treasury as in 2016, it was 138 billion

pound. Apart from this, CGT is levied by the government on the gains or profits through the

disposal of long-term capital assets like plant and machinery, land and building and many others.

1.2

Every individual is not perfectly well-known with the different types of tax policies, rules

and regulations as they have only the basic knowledge of it. Therefore, specialists help assesses to

prepare accurate tax return and file it to HMRC, known as tax practitioners. They play an

inexorable role in the UK tax environment and also indirectly assist taxation authorities to generate

timely and right amount of taxes from the contributors. It must be keep in mind that this are not the

accountants, but still, they have well-knowledge of accounting because they are already trained

persons (Devereux, Liu and Loretz, 2014). It is the legal requirement for the practitioners to pursue

an exam and after passing, they have to work under the supervision of either a licensed or certified

accountant. It is essential for them to complete required qualification and obtain degree, so that,

they will be eligible to give legal advices to their clients.

Roles

The roles and responsibilities of practitioners are highly dependent upon whether he or she

is a certified public accountant (CPA) or licensed taxation specialists. Mainly, they have to prepare

necessary documents and arrange it appropriately for filling tax return. They works as an

intermediaries between tax payers and collectors (HMRC) as they submit required information to

the regulatory body, HMRC on the behalf of the contributors. Such specialists assist assesses to

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

minimize their taxation liabilities by having an in-depth knowledge of the legislation. But still, it

must be noticed that they are not involved in any illegal activities such as tax evasions and also

necessarily comply with all the laws and principles (Tiley and Loutzenhiser, 2012). They are mainly

liable to give advices and suggestions to the payers, collect essential information and file correctly

the return. Moreover, they also compute taxation liabilities of their clients on the basis of their total

taxable earnings. They have to obey respective legislative rules and provisions while performing

their duties. They can reduce tax obligations of the payers through having efficient technical

knowledge of the laws. Despite this, they can improve policies and ensure perfect reporting system

as well.

Responsibilities

1. It is essential for the practitioners to comply strictly with the laws while performing different

functions.

2. They have to advise tax contributors to file an accurate tax return completely and honestly.

Moreover, they must provide full support to the taxpayers in the case of issues and

complexity regards to audit law (Doyle, Hughes and Summers, 2013).

3. It is important for the practitioners to not leak their client confidential information to the

third party without their prior approval.

4. They also need to keep up-to-date their knowledge with regards to the amendment in tax

laws and regulations, so that, they can explain it and advice appropriately to the clients.

5. Complying with the professional ethics and code of conduct such as honesty, integrity and

principle of discipline etc. is also essential for the practitioners (Devereux, Liu and Loretz,

2014).

1.3

Every British Citizen is adhere to the principles, regulations and legislative provisions of the

UK taxation system. The main obligations of the taxpayers and their respective agents are detained

here as under:

Honesty: Tax contributors must provide full and authentic information and reports about

their income to the taxation authority when file return. It is because, honesty in listing the taxes

helps HMRC to collect the right amount of taxes and spend it on the public services for the nation

growth (Hasseldine and Morris, 2013). Apart from this, taxpayers must be truth while

communicating with the regulatory bodies for the payment of their tax duties.

Co-operations: It is also necessary for the assesses to co-operate and coordinate closely

with the administrative bodies such as tax agencies and HMRC to provide them needed information

7

must be noticed that they are not involved in any illegal activities such as tax evasions and also

necessarily comply with all the laws and principles (Tiley and Loutzenhiser, 2012). They are mainly

liable to give advices and suggestions to the payers, collect essential information and file correctly

the return. Moreover, they also compute taxation liabilities of their clients on the basis of their total

taxable earnings. They have to obey respective legislative rules and provisions while performing

their duties. They can reduce tax obligations of the payers through having efficient technical

knowledge of the laws. Despite this, they can improve policies and ensure perfect reporting system

as well.

Responsibilities

1. It is essential for the practitioners to comply strictly with the laws while performing different

functions.

2. They have to advise tax contributors to file an accurate tax return completely and honestly.

Moreover, they must provide full support to the taxpayers in the case of issues and

complexity regards to audit law (Doyle, Hughes and Summers, 2013).

3. It is important for the practitioners to not leak their client confidential information to the

third party without their prior approval.

4. They also need to keep up-to-date their knowledge with regards to the amendment in tax

laws and regulations, so that, they can explain it and advice appropriately to the clients.

5. Complying with the professional ethics and code of conduct such as honesty, integrity and

principle of discipline etc. is also essential for the practitioners (Devereux, Liu and Loretz,

2014).

1.3

Every British Citizen is adhere to the principles, regulations and legislative provisions of the

UK taxation system. The main obligations of the taxpayers and their respective agents are detained

here as under:

Honesty: Tax contributors must provide full and authentic information and reports about

their income to the taxation authority when file return. It is because, honesty in listing the taxes

helps HMRC to collect the right amount of taxes and spend it on the public services for the nation

growth (Hasseldine and Morris, 2013). Apart from this, taxpayers must be truth while

communicating with the regulatory bodies for the payment of their tax duties.

Co-operations: It is also necessary for the assesses to co-operate and coordinate closely

with the administrative bodies such as tax agencies and HMRC to provide them needed information

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

on time. It helps to decrease the cost of revenue collection by imposing various tax duties.

Submission of the documents: It is the basic responsibility of the assesses and agents to

submit timely the documents to the HMRC department.

Payment on due date: Every tax payer has to pay their taxation liabilities to the taxation

agencies, when payment fall due (Dowling, 2014). It help individuals to avoid the possibility of

penalties and fines and assure easiness in the tax collection system.

Penalties of non-compliance

Paying taxes at right time assist assesses to save their money, otherwise, it may results

in penalties which is given as under:

Delay in tax payments Penalty percentage

After 30 days from the due date 5% of the tax payble

Later 6 months 5 % of the tax payments due plus 5% additional

Delayed payments by 12 months 5% of the unpaid taxes plus 5% penalties above

Apart from this, it is also mandatory for the tax contributors to file return on time,

otherwise, following penalties can be charged by HMRC, mentioned below:

Time of delay Penalty

Later 1 day £100

Later 3 months £10 for every day up-to 90 days but restricted

maximum to £900

Later 6 months £300 or 5% of the tax payable, which is higher.

Later 12 months Same as above

In some cases, penalties may also go beyond the

minimum amount of tax payment.

TASK 2

2.1

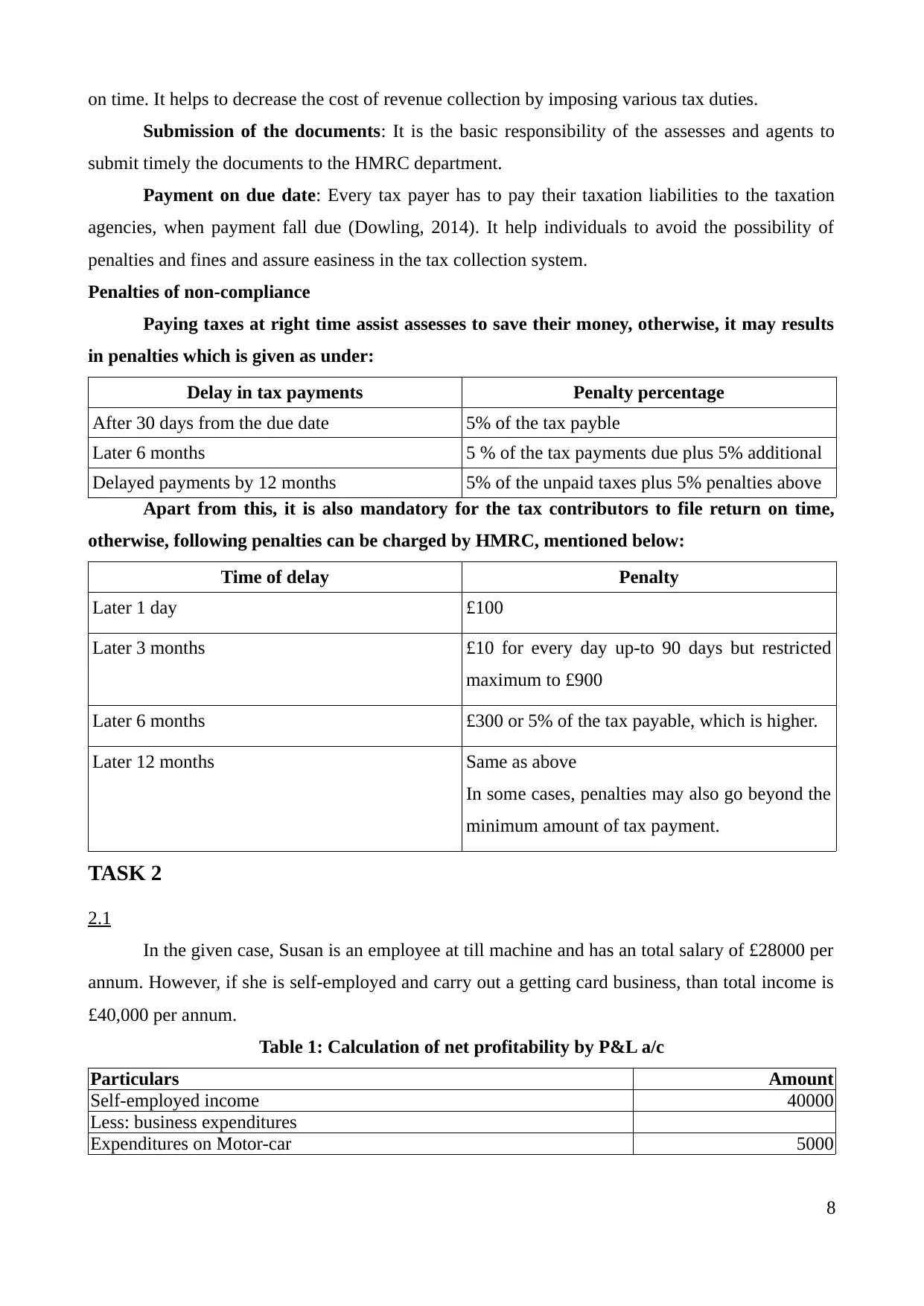

In the given case, Susan is an employee at till machine and has an total salary of £28000 per

annum. However, if she is self-employed and carry out a getting card business, than total income is

£40,000 per annum.

Table 1: Calculation of net profitability by P&L a/c

Particulars Amount

Self-employed income 40000

Less: business expenditures

Expenditures on Motor-car 5000

8

Submission of the documents: It is the basic responsibility of the assesses and agents to

submit timely the documents to the HMRC department.

Payment on due date: Every tax payer has to pay their taxation liabilities to the taxation

agencies, when payment fall due (Dowling, 2014). It help individuals to avoid the possibility of

penalties and fines and assure easiness in the tax collection system.

Penalties of non-compliance

Paying taxes at right time assist assesses to save their money, otherwise, it may results

in penalties which is given as under:

Delay in tax payments Penalty percentage

After 30 days from the due date 5% of the tax payble

Later 6 months 5 % of the tax payments due plus 5% additional

Delayed payments by 12 months 5% of the unpaid taxes plus 5% penalties above

Apart from this, it is also mandatory for the tax contributors to file return on time,

otherwise, following penalties can be charged by HMRC, mentioned below:

Time of delay Penalty

Later 1 day £100

Later 3 months £10 for every day up-to 90 days but restricted

maximum to £900

Later 6 months £300 or 5% of the tax payable, which is higher.

Later 12 months Same as above

In some cases, penalties may also go beyond the

minimum amount of tax payment.

TASK 2

2.1

In the given case, Susan is an employee at till machine and has an total salary of £28000 per

annum. However, if she is self-employed and carry out a getting card business, than total income is

£40,000 per annum.

Table 1: Calculation of net profitability by P&L a/c

Particulars Amount

Self-employed income 40000

Less: business expenditures

Expenditures on Motor-car 5000

8

Property expenses 8000

Repairs charges 1200

Utility payment 6000

Total expenditures 20200

Net profit (total income – total payment) 19800

Assumed adjustments:

1. Susan paid 1/4th of the total property expense in relation to the his own premises.

2. There are two cars used by Susan for her greeting card business, the cost of one car is

£10000 while another worth £12000. However, the Co2 emission was 118 gms/km and 140

gms/km respectively.

3. 1st Car is used 80% for business and other for 65% only.

4. Susan paid repairing expenditures which comprises both personal and trading purpose and

the ratio of it was 25% and 75% respectively.

2.2

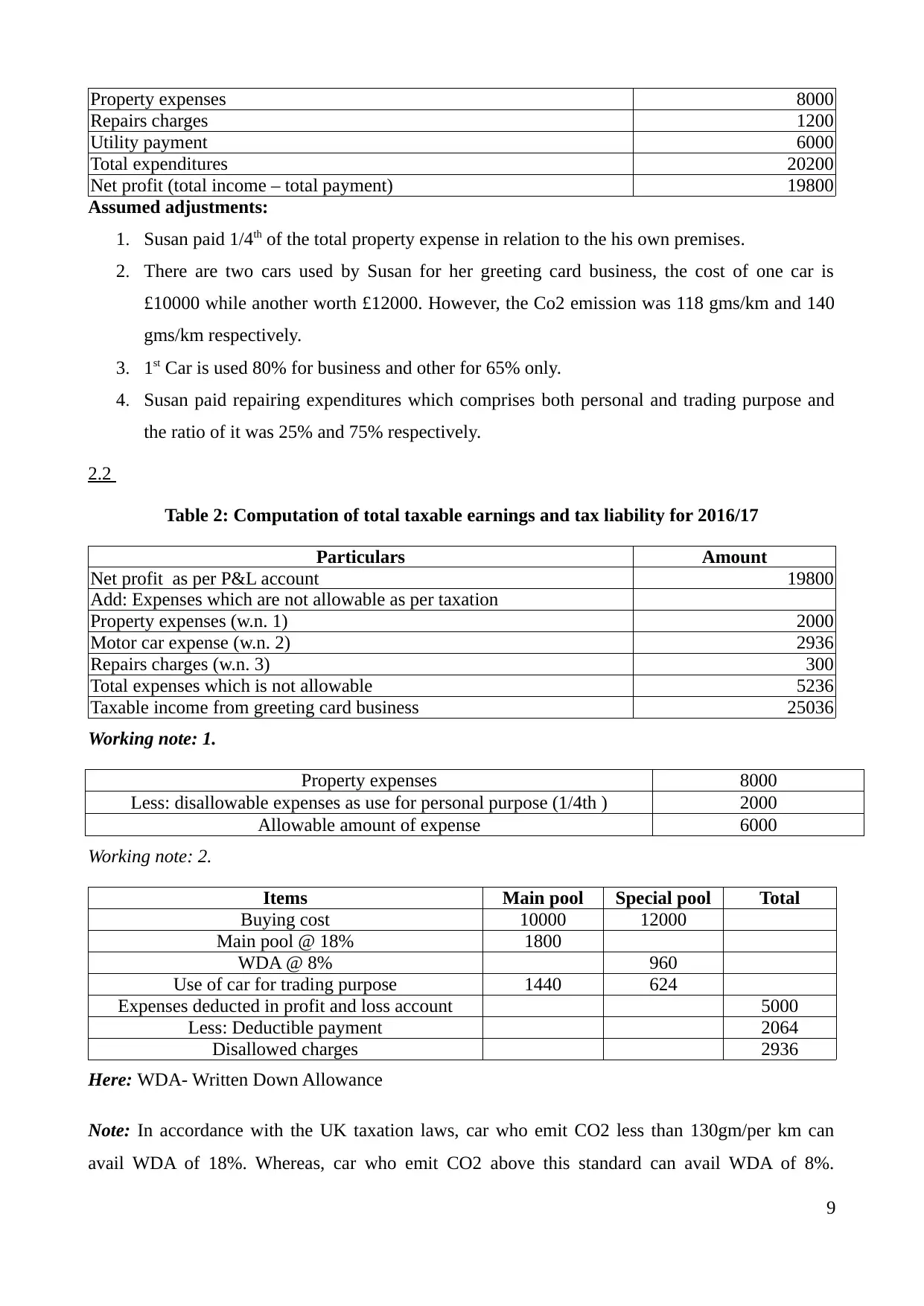

Table 2: Computation of total taxable earnings and tax liability for 2016/17

Particulars Amount

Net profit as per P&L account 19800

Add: Expenses which are not allowable as per taxation

Property expenses (w.n. 1) 2000

Motor car expense (w.n. 2) 2936

Repairs charges (w.n. 3) 300

Total expenses which is not allowable 5236

Taxable income from greeting card business 25036

Working note: 1.

Property expenses 8000

Less: disallowable expenses as use for personal purpose (1/4th ) 2000

Allowable amount of expense 6000

Working note: 2.

Items Main pool Special pool Total

Buying cost 10000 12000

Main pool @ 18% 1800

WDA @ 8% 960

Use of car for trading purpose 1440 624

Expenses deducted in profit and loss account 5000

Less: Deductible payment 2064

Disallowed charges 2936

Here: WDA- Written Down Allowance

Note: In accordance with the UK taxation laws, car who emit CO2 less than 130gm/per km can

avail WDA of 18%. Whereas, car who emit CO2 above this standard can avail WDA of 8%.

9

Repairs charges 1200

Utility payment 6000

Total expenditures 20200

Net profit (total income – total payment) 19800

Assumed adjustments:

1. Susan paid 1/4th of the total property expense in relation to the his own premises.

2. There are two cars used by Susan for her greeting card business, the cost of one car is

£10000 while another worth £12000. However, the Co2 emission was 118 gms/km and 140

gms/km respectively.

3. 1st Car is used 80% for business and other for 65% only.

4. Susan paid repairing expenditures which comprises both personal and trading purpose and

the ratio of it was 25% and 75% respectively.

2.2

Table 2: Computation of total taxable earnings and tax liability for 2016/17

Particulars Amount

Net profit as per P&L account 19800

Add: Expenses which are not allowable as per taxation

Property expenses (w.n. 1) 2000

Motor car expense (w.n. 2) 2936

Repairs charges (w.n. 3) 300

Total expenses which is not allowable 5236

Taxable income from greeting card business 25036

Working note: 1.

Property expenses 8000

Less: disallowable expenses as use for personal purpose (1/4th ) 2000

Allowable amount of expense 6000

Working note: 2.

Items Main pool Special pool Total

Buying cost 10000 12000

Main pool @ 18% 1800

WDA @ 8% 960

Use of car for trading purpose 1440 624

Expenses deducted in profit and loss account 5000

Less: Deductible payment 2064

Disallowed charges 2936

Here: WDA- Written Down Allowance

Note: In accordance with the UK taxation laws, car who emit CO2 less than 130gm/per km can

avail WDA of 18%. Whereas, car who emit CO2 above this standard can avail WDA of 8%.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Therefore, in the given case, charged capital allowance rate for 1st car (118 gm/km Co2 emission)

and 2nd car (140 gm/km Co2 emission) are 18% and 8% respectively (Damayanti and et.al., 2015).

Working note: 3.

Repairs and renewals 1200

Less: amount spent for repairing own residence 300

Allowable repairing payment 900

Table 3: Calculations of taxable income and tax liability of Susan for employment for 2016-17

Gross salaried earnings 40000

Less: Tax free allowance 11000

Taxable earnings (40000-11000) 29000

Table 4: Calculation of tax liability of Susan for 2016/17

Basic tax rate (From zero to 32000): 20% (29000*20%) 5800

Contribution to national insurance 3832.8

Students loan Nil

Total PAYE deductions avail to Susan 9632.8

Net wages (40000-9632.8) 30367.2

Note: The age of Susan is taken 43 year

Due dates

As per the HMRC's rules and regulations, every assesses has liability to pay taxes on the due

date for the tax year from 6th April to 5th April of every year. In UK, the deadline for filling self-

assessment registration by Susan is 5th October, 2016. Moreover, according to the laws, taxes can be

paid either by paper formalities or online, for the offline return, the last date is Midnight of 31st

October, 2016, whereas for tax payments via web, deadline is Midnight of 31st January, 2017

(Yagan, 2015). On the other hand, if an individual pay taxes as he or she owe than the last date of

payment is Midnight 31st January, 2017. Person who make delayed payments to the HMRC will be

liable to pay penalties also to the authority.

2.3

After calculating Susan's tax liabilities, practitioners has to prepare and file tax return in

relevant document. There are several specified forms, in which, tax contributors has to file return,

described hereunder:

SA 100 form:

It is the main form of taxation return which is used by an individual for reporting their

10

and 2nd car (140 gm/km Co2 emission) are 18% and 8% respectively (Damayanti and et.al., 2015).

Working note: 3.

Repairs and renewals 1200

Less: amount spent for repairing own residence 300

Allowable repairing payment 900

Table 3: Calculations of taxable income and tax liability of Susan for employment for 2016-17

Gross salaried earnings 40000

Less: Tax free allowance 11000

Taxable earnings (40000-11000) 29000

Table 4: Calculation of tax liability of Susan for 2016/17

Basic tax rate (From zero to 32000): 20% (29000*20%) 5800

Contribution to national insurance 3832.8

Students loan Nil

Total PAYE deductions avail to Susan 9632.8

Net wages (40000-9632.8) 30367.2

Note: The age of Susan is taken 43 year

Due dates

As per the HMRC's rules and regulations, every assesses has liability to pay taxes on the due

date for the tax year from 6th April to 5th April of every year. In UK, the deadline for filling self-

assessment registration by Susan is 5th October, 2016. Moreover, according to the laws, taxes can be

paid either by paper formalities or online, for the offline return, the last date is Midnight of 31st

October, 2016, whereas for tax payments via web, deadline is Midnight of 31st January, 2017

(Yagan, 2015). On the other hand, if an individual pay taxes as he or she owe than the last date of

payment is Midnight 31st January, 2017. Person who make delayed payments to the HMRC will be

liable to pay penalties also to the authority.

2.3

After calculating Susan's tax liabilities, practitioners has to prepare and file tax return in

relevant document. There are several specified forms, in which, tax contributors has to file return,

described hereunder:

SA 100 form:

It is the main form of taxation return which is used by an individual for reporting their

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

income, capital gain, interest, pension and many others. Moreover, assesses can claim tax relief as

well as allowances from the taxation authority in the SA 100 (Evers, Miller and Spengel, 2015).

SA 102 form:

It is used by the employed person regardless part-time, full time or casual workers. It is used

by directors as well as employees to report income on the employment pages of SA 102.

SA 103S form:

Self-employed person use this form to give their business detail about income, allowable

and dis-allowable payments, capital allowances, net profit or loss etc (Wallis, 2016). Moreover, they

also report other information such as CIS deductions and NIC contribution etc. by strictly adhering

to the laws and regulations.

P60 form:

Being an employer, Susan has to provide form P60 to every personnel at the end of

respective tax year. This form is used by the businessman for self-assessment objective.

64 -8 form:

It is used to authorize tax practitioners to identify taxable income and tax liability on the

behalf of their clients. Through this, tax experts can communicate with tax agencies and the

authorities for their clients (Steven, 2015). It includes authorization for individual as well as

business tax affairs. Out of these, first consists of trusts, partnership and individuals under PAYE

system while second comprises value added taxes and PAYE for corporation and employers.

SA 105 form:

It is used to report earnings generated through UK-based land and property and also the

chargeable premiums from the lease. Thus, it is clear that assesses report their rental income in this

form.

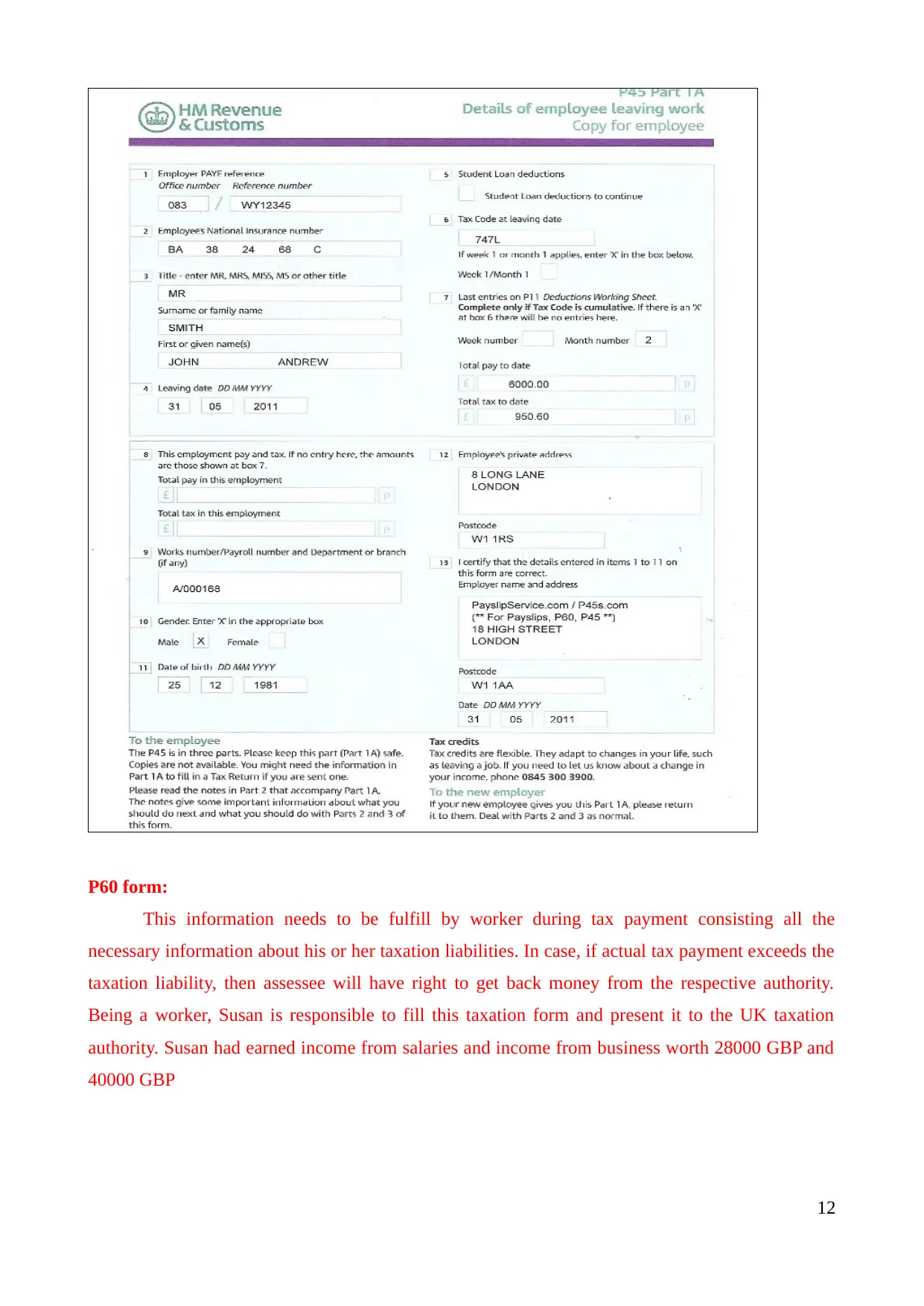

SA 45 form

Being an employer, it is the liability of person to pay tax on the behalf of their personnel, but

in case, if any of the employee goes on leave then it is the liability of employer to issue this form to

the employer to make them free from their respective taxation obligations. Henceforth, if Susan

leaves job then company has to issue this form, presented below:

11

well as allowances from the taxation authority in the SA 100 (Evers, Miller and Spengel, 2015).

SA 102 form:

It is used by the employed person regardless part-time, full time or casual workers. It is used

by directors as well as employees to report income on the employment pages of SA 102.

SA 103S form:

Self-employed person use this form to give their business detail about income, allowable

and dis-allowable payments, capital allowances, net profit or loss etc (Wallis, 2016). Moreover, they

also report other information such as CIS deductions and NIC contribution etc. by strictly adhering

to the laws and regulations.

P60 form:

Being an employer, Susan has to provide form P60 to every personnel at the end of

respective tax year. This form is used by the businessman for self-assessment objective.

64 -8 form:

It is used to authorize tax practitioners to identify taxable income and tax liability on the

behalf of their clients. Through this, tax experts can communicate with tax agencies and the

authorities for their clients (Steven, 2015). It includes authorization for individual as well as

business tax affairs. Out of these, first consists of trusts, partnership and individuals under PAYE

system while second comprises value added taxes and PAYE for corporation and employers.

SA 105 form:

It is used to report earnings generated through UK-based land and property and also the

chargeable premiums from the lease. Thus, it is clear that assesses report their rental income in this

form.

SA 45 form

Being an employer, it is the liability of person to pay tax on the behalf of their personnel, but

in case, if any of the employee goes on leave then it is the liability of employer to issue this form to

the employer to make them free from their respective taxation obligations. Henceforth, if Susan

leaves job then company has to issue this form, presented below:

11

P60 form:

This information needs to be fulfill by worker during tax payment consisting all the

necessary information about his or her taxation liabilities. In case, if actual tax payment exceeds the

taxation liability, then assessee will have right to get back money from the respective authority.

Being a worker, Susan is responsible to fill this taxation form and present it to the UK taxation

authority. Susan had earned income from salaries and income from business worth 28000 GBP and

40000 GBP

12

This information needs to be fulfill by worker during tax payment consisting all the

necessary information about his or her taxation liabilities. In case, if actual tax payment exceeds the

taxation liability, then assessee will have right to get back money from the respective authority.

Being a worker, Susan is responsible to fill this taxation form and present it to the UK taxation

authority. Susan had earned income from salaries and income from business worth 28000 GBP and

40000 GBP

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.