Taxation: Purpose, Structure, and Ethics - DFA 2104Y (3)

VerifiedAdded on 2021/04/27

|20

|2109

|578

Report

AI Summary

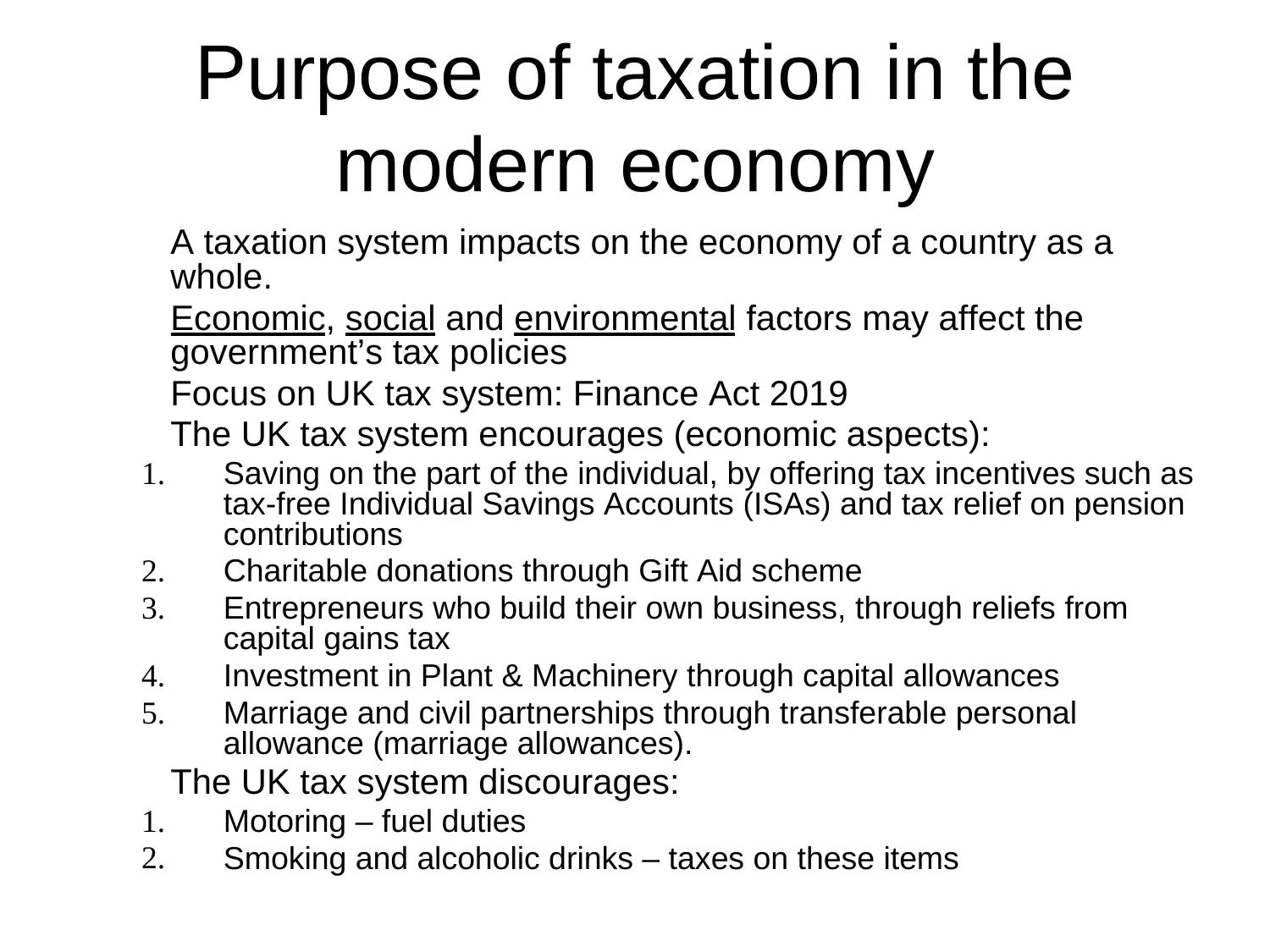

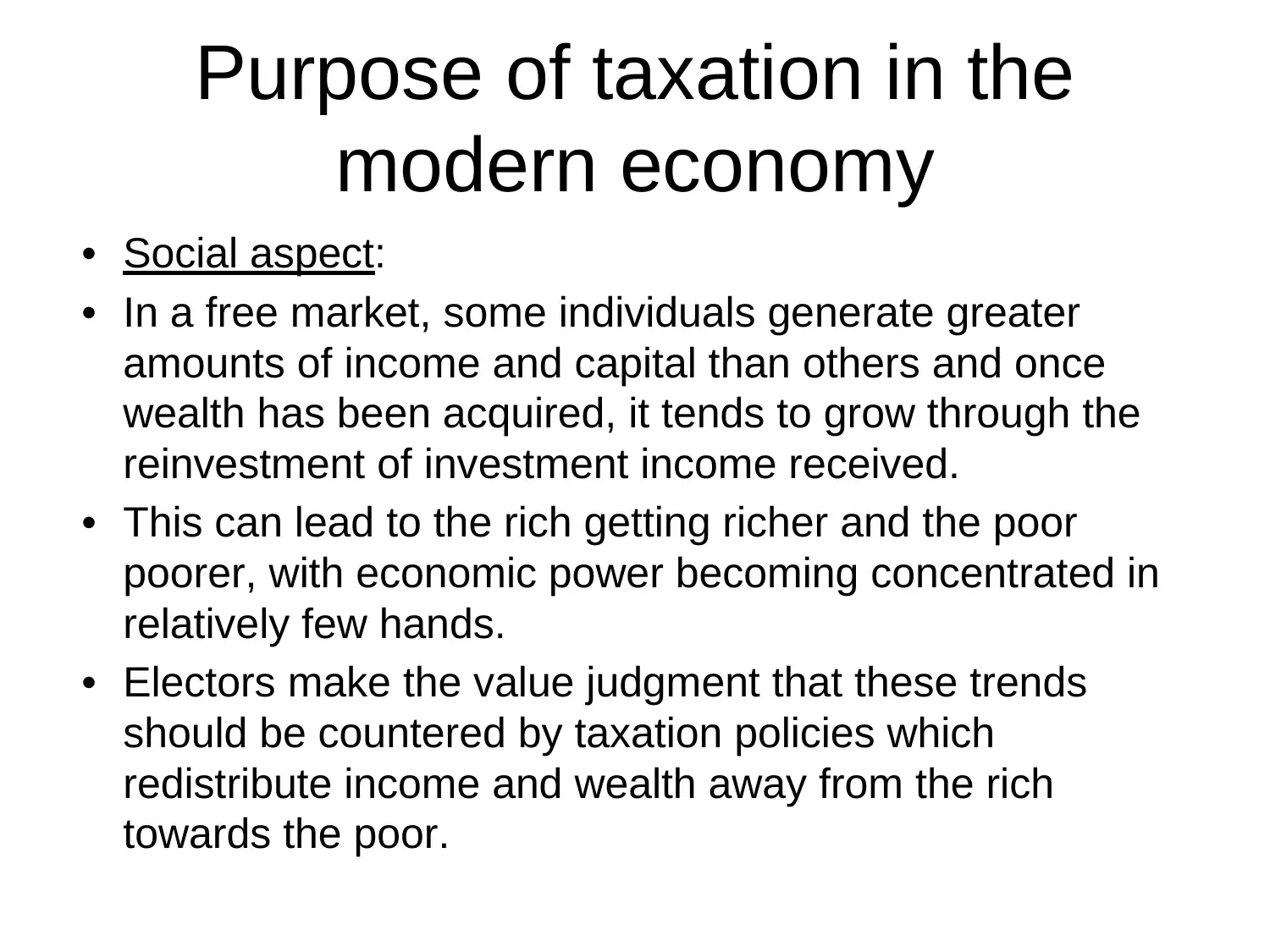

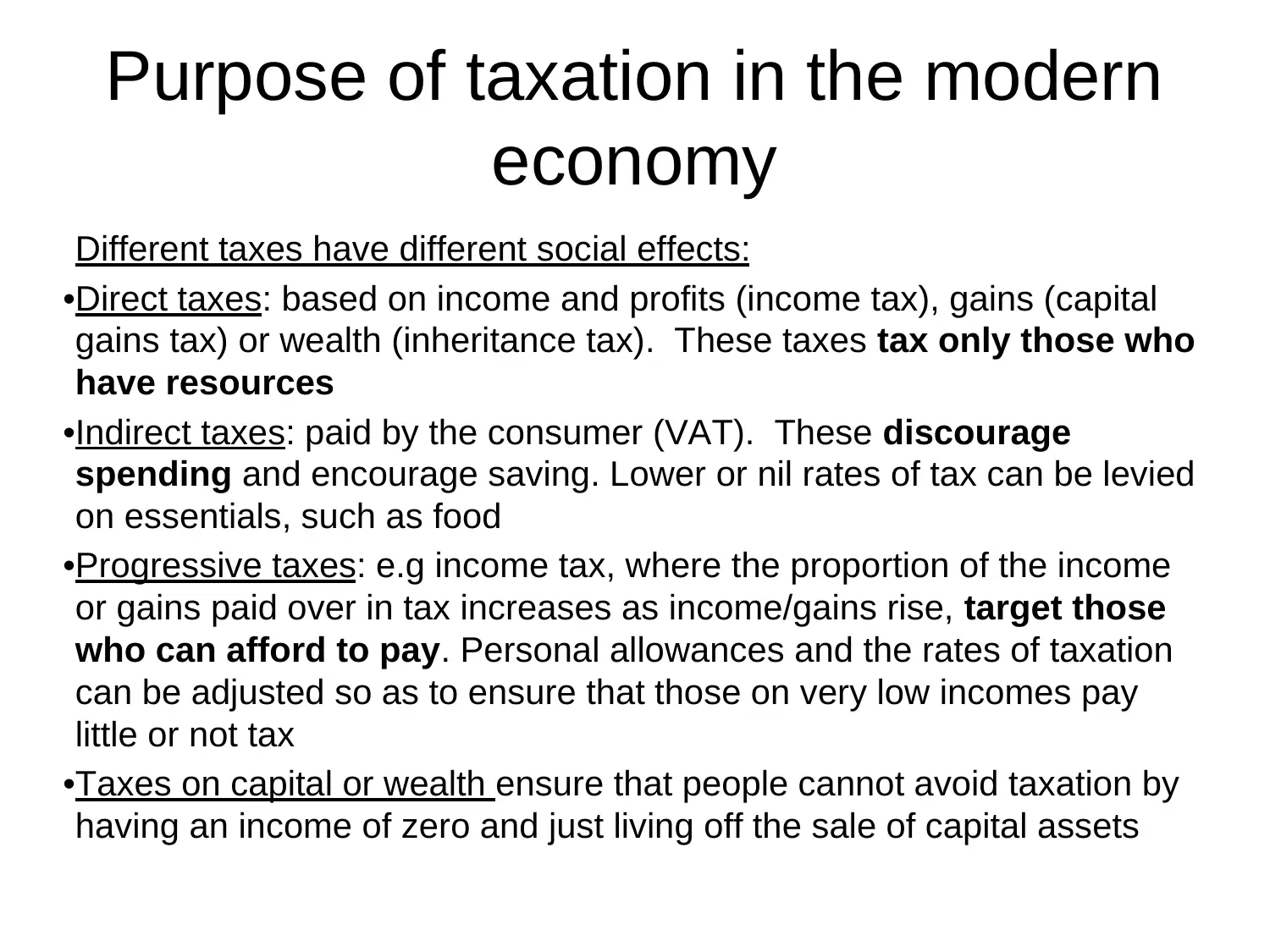

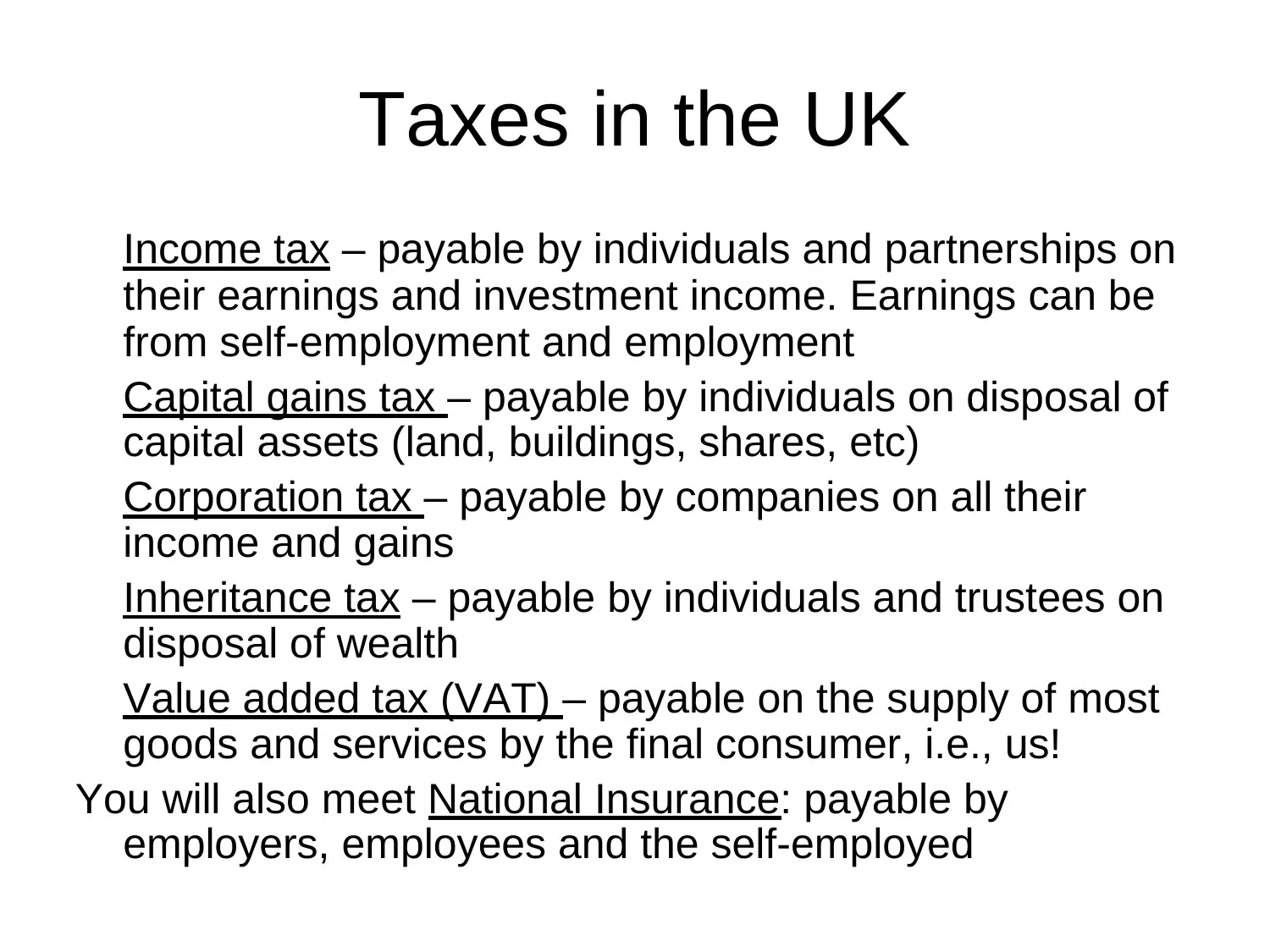

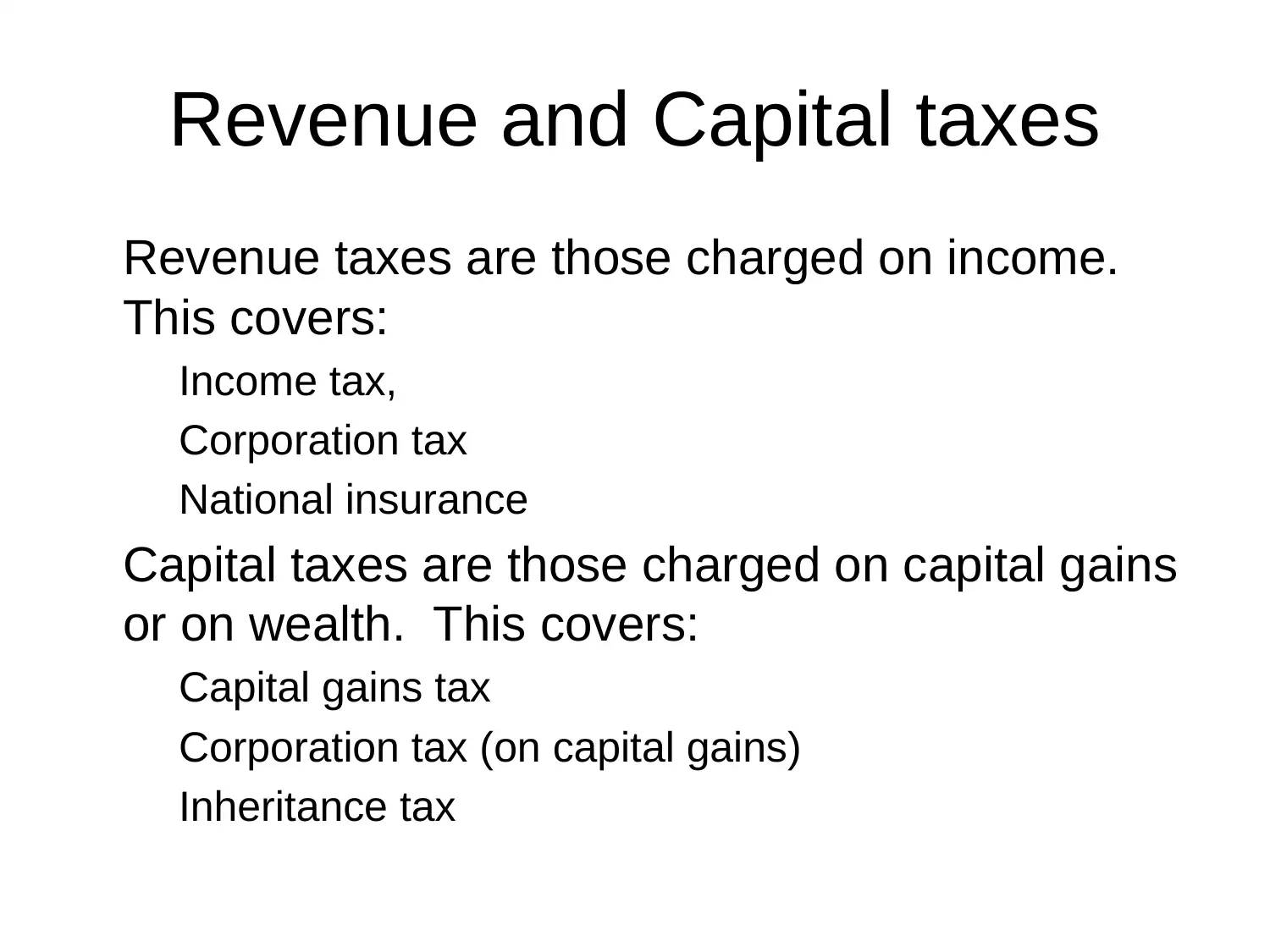

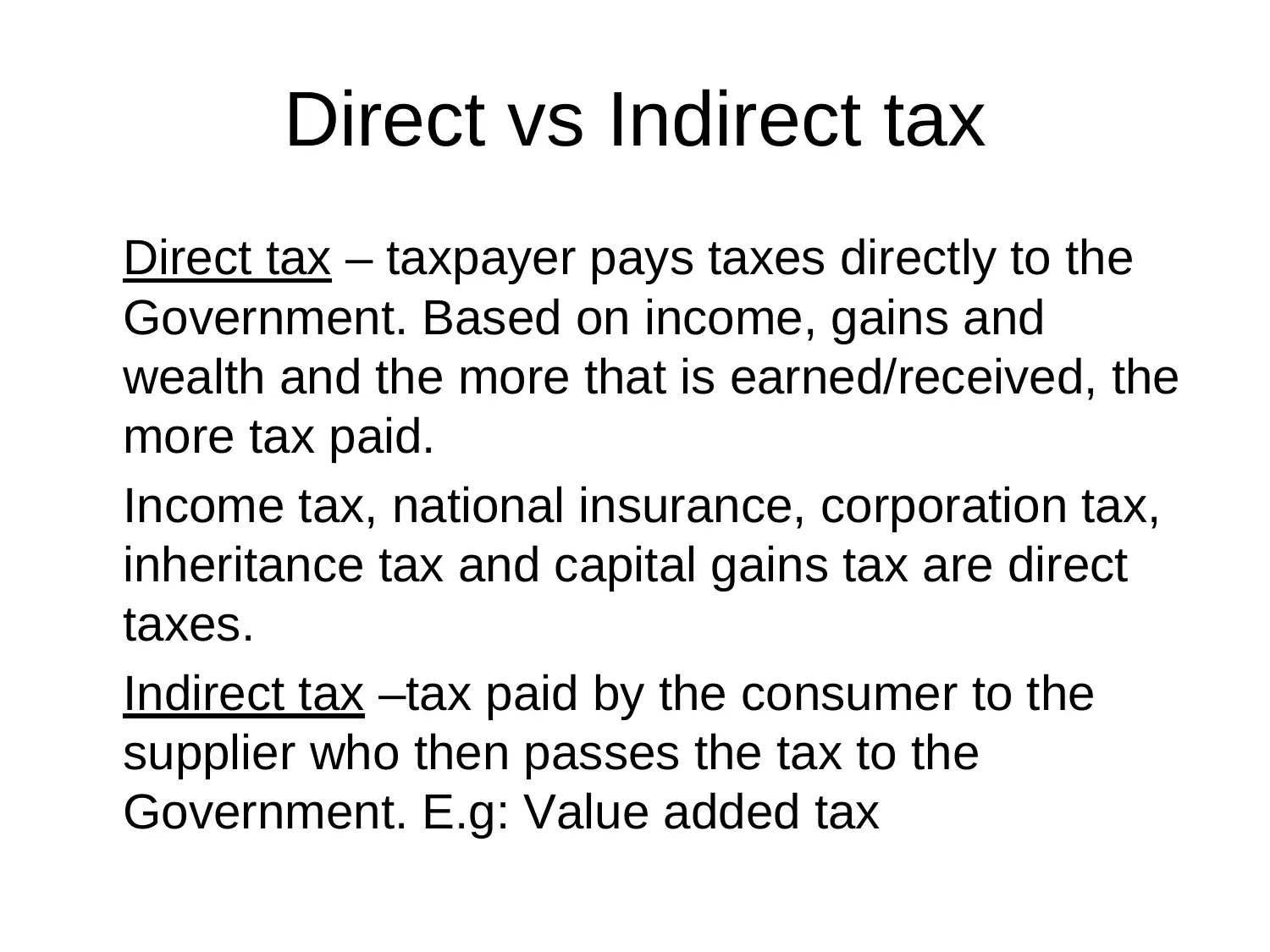

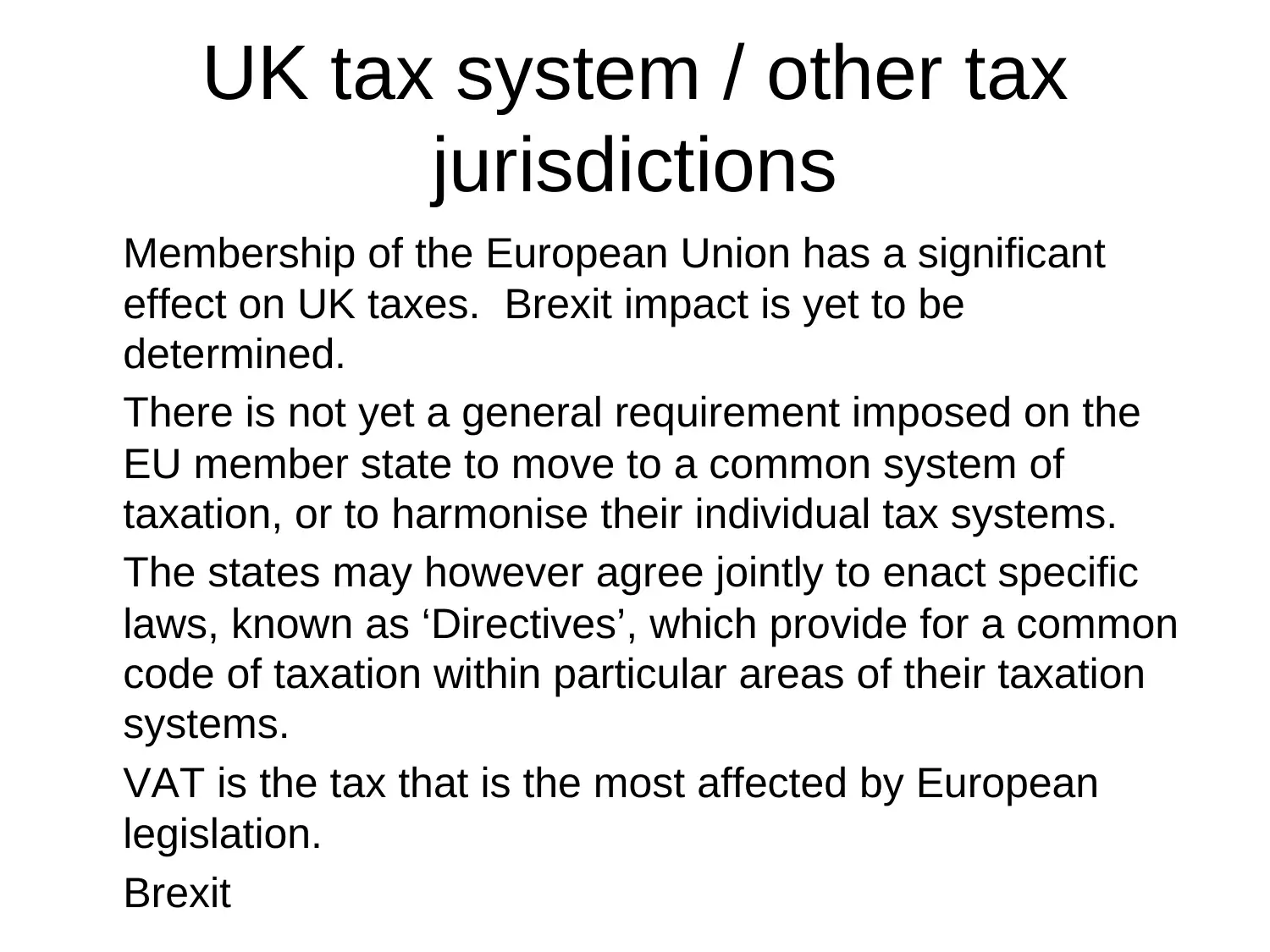

This report provides a comprehensive overview of the UK taxation system, focusing on its purpose, structure, and ethical considerations. It examines how the UK tax system encourages and discourages certain economic activities through various incentives and disincentives. The report delves into the social and environmental aspects of taxation, including the redistribution of wealth and the promotion of sustainable practices. It also details the structure of the UK tax system, including the roles of key bodies like Her Majesty's Treasury and HMRC. Furthermore, the report outlines the sources of revenue law, different types of taxes (direct and indirect), and the impact of European Union membership and double taxation agreements. The report differentiates between tax avoidance and tax evasion, explaining the General Anti-Abuse Rule (GAAR). Finally, the report explores the ethical responsibilities of accountants in tax matters, including the handling of client errors and potential tax evasion activities. The report concludes with a multiple-choice question (MCQ) to test understanding of the ethical considerations.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.