UK Taxation: Calculation of Tax Obligations and Compliance Procedures

VerifiedAdded on 2020/07/22

|4

|4017

|452

Homework Assignment

AI Summary

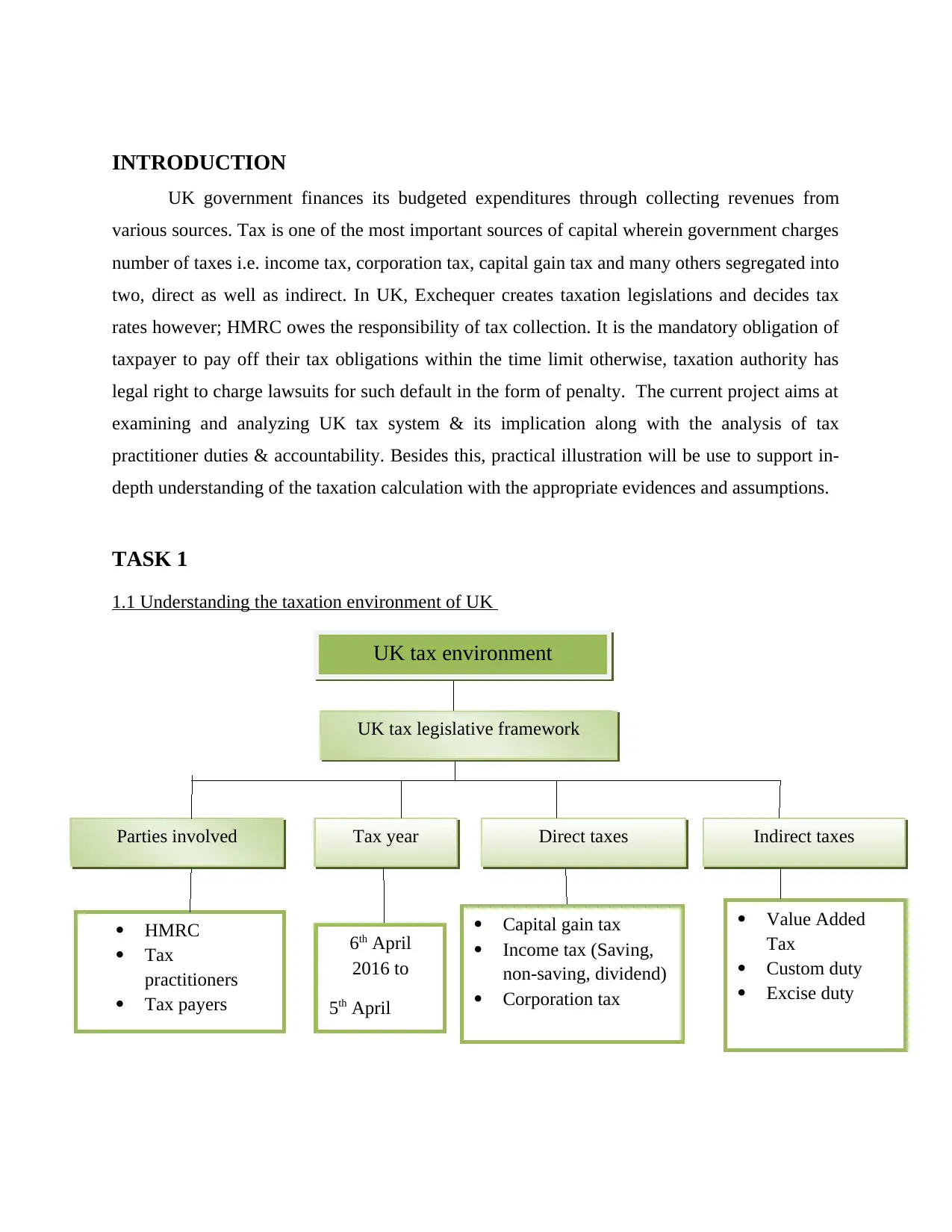

This assignment provides a comprehensive overview of the UK tax system, examining various aspects of taxation including income tax, corporation tax, and capital gains tax. It explores the roles and responsibilities of tax practitioners and taxpayers, detailing the obligations of tax compliance and the implications of non-compliance. The assignment includes practical calculations of taxable income, expenditures, and allowances for both employed and self-employed individuals, demonstrating how to complete tax documentation for tax return filing. Furthermore, it presents detailed scenarios involving the calculation of chargeable profits, tax obligations for companies, and the calculation of capital gains and losses, alongside the associated tax liabilities. The conclusion summarizes the key findings, and relevant references are provided to support the analysis.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.