PTAX5037 - Analysis of UK Taxation Principles and Tax Law Sources

VerifiedAdded on 2023/04/24

|14

|3083

|92

Report

AI Summary

This report provides an overview of the UK taxation system, comparing progressive and regressive tax models, detailing sources of tax law, and differentiating between tax avoidance and tax evasion. It highlights that progressive taxation minimizes the tax burden for low-income earners, while regressive taxation disproportionately affects them. The UK's tax laws originate from parliamentary acts but are interpreted by the courts. Tax avoidance involves legally exploiting loopholes to reduce tax liability, whereas tax evasion uses illegal methods. The report also covers proportional tax, income tax, national insurance, VAT, excise duties, corporation tax, and stamp duty. It emphasizes the legal implications of tax evasion, including potential imprisonment and fines, and notes taxpayers' rights to appeal HMRC decisions through a tribunal system. Desklib provides access to similar solved assignments and past papers for students.

Running head: PRINCIPLES OF TAXATION

Principles of Taxation

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Principles of Taxation

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PRINCIPLES OF TAXATION

Executive Summary:

The current report has provided a brief overview of the various taxation aspects associated with

the UK. It has been found that in case of progressive taxation system, the low-income earners

enjoy minimised tax burden, while the situation is just the opposite in case of regressive taxation

system. Moreover, the UK is identified to have certain sources of tax and the primary rules are

mentioned in the Acts of the Parliament; however, the ultimate decision lies in the hands of the

courts. Finally, it has been evaluated that tax avoidance and tax evasion are completely different

concepts. This is because tax avoidance involves using the loopholes of the current tax

regulations to minimise tax liability, while tax evasion intends to minimise tax liability by using

unfair means.

Executive Summary:

The current report has provided a brief overview of the various taxation aspects associated with

the UK. It has been found that in case of progressive taxation system, the low-income earners

enjoy minimised tax burden, while the situation is just the opposite in case of regressive taxation

system. Moreover, the UK is identified to have certain sources of tax and the primary rules are

mentioned in the Acts of the Parliament; however, the ultimate decision lies in the hands of the

courts. Finally, it has been evaluated that tax avoidance and tax evasion are completely different

concepts. This is because tax avoidance involves using the loopholes of the current tax

regulations to minimise tax liability, while tax evasion intends to minimise tax liability by using

unfair means.

2PRINCIPLES OF TAXATION

Table of Contents

Introduction:....................................................................................................................................3

a) Comparison and contrast of the progressive taxation system and the regressive taxation

system:.............................................................................................................................................3

b) Sources of tax law in the UK:.....................................................................................................6

c) Comparison and contrast of tax avoidance and tax evasion:.......................................................8

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

Table of Contents

Introduction:....................................................................................................................................3

a) Comparison and contrast of the progressive taxation system and the regressive taxation

system:.............................................................................................................................................3

b) Sources of tax law in the UK:.....................................................................................................6

c) Comparison and contrast of tax avoidance and tax evasion:.......................................................8

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PRINCIPLES OF TAXATION

Introduction:

It has been observed that the taxation system and government spending have direct effect

on the economy of a nation. The taxation policies are utilised to affect a number of economic

factors like levels of employment, inflation, exports and imports. These factors are deemed to

affect the behaviour of individuals as well as businesses. The current report would provide a

brief comparison of the progressive tax system and the regressive tax system by citing certain

instances. The next section would focus on the sources of tax law in the UK by taking into

account the primary rules of the tax system of the nation established from a number of resources.

Finally, the report would shed light on the difference between tax avoidance and tax evasion by

providing practical examples.

a) Comparison and contrast of the progressive taxation system and the regressive taxation

system:

The progressive taxation system is a tax system where there is an increase in tax rate with

an increase in the amount of tax. More precisely, it is a tax system where the tax rate depends on

the ability of an individual to pay, which implies high tax is collected from higher-income

individuals and lower tax is obtained from lower-income individuals (Brockmeyer 2014). Hence,

the taxpayers are segregated based on their level of income. This mechanism of tax intends to

minimise the tax incidence of individuals with lower income, since tax incidence is transferred to

the individuals with greater income.

When there is an increase in the amount subject to taxation, there is a decrease in overall

tax rate and this mechanism is deemed to be regressive. Specifically, regressive taxation system

could be defined as the one where increased tax is obtained from low-income earners and lower

Introduction:

It has been observed that the taxation system and government spending have direct effect

on the economy of a nation. The taxation policies are utilised to affect a number of economic

factors like levels of employment, inflation, exports and imports. These factors are deemed to

affect the behaviour of individuals as well as businesses. The current report would provide a

brief comparison of the progressive tax system and the regressive tax system by citing certain

instances. The next section would focus on the sources of tax law in the UK by taking into

account the primary rules of the tax system of the nation established from a number of resources.

Finally, the report would shed light on the difference between tax avoidance and tax evasion by

providing practical examples.

a) Comparison and contrast of the progressive taxation system and the regressive taxation

system:

The progressive taxation system is a tax system where there is an increase in tax rate with

an increase in the amount of tax. More precisely, it is a tax system where the tax rate depends on

the ability of an individual to pay, which implies high tax is collected from higher-income

individuals and lower tax is obtained from lower-income individuals (Brockmeyer 2014). Hence,

the taxpayers are segregated based on their level of income. This mechanism of tax intends to

minimise the tax incidence of individuals with lower income, since tax incidence is transferred to

the individuals with greater income.

When there is an increase in the amount subject to taxation, there is a decrease in overall

tax rate and this mechanism is deemed to be regressive. Specifically, regressive taxation system

could be defined as the one where increased tax is obtained from low-income earners and lower

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PRINCIPLES OF TAXATION

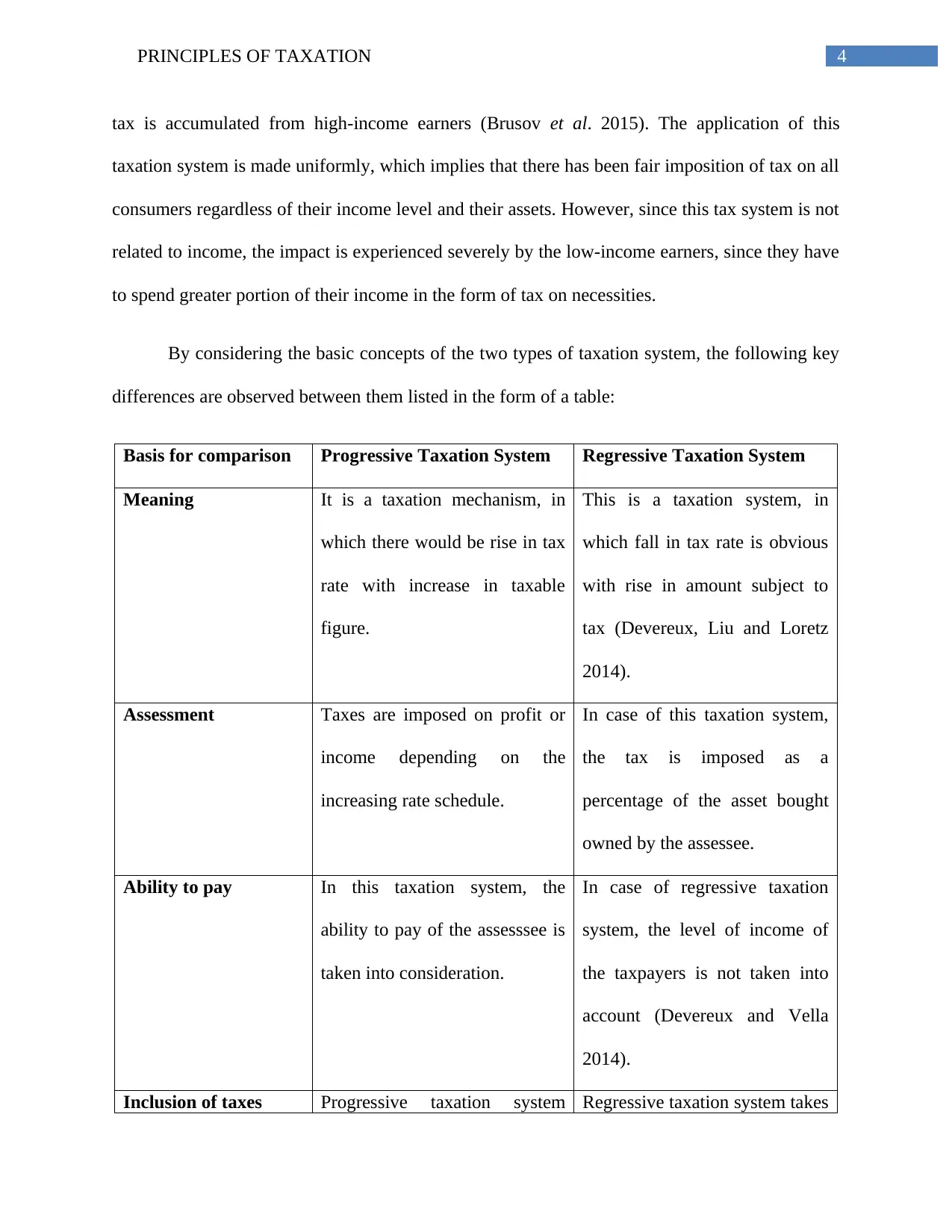

tax is accumulated from high-income earners (Brusov et al. 2015). The application of this

taxation system is made uniformly, which implies that there has been fair imposition of tax on all

consumers regardless of their income level and their assets. However, since this tax system is not

related to income, the impact is experienced severely by the low-income earners, since they have

to spend greater portion of their income in the form of tax on necessities.

By considering the basic concepts of the two types of taxation system, the following key

differences are observed between them listed in the form of a table:

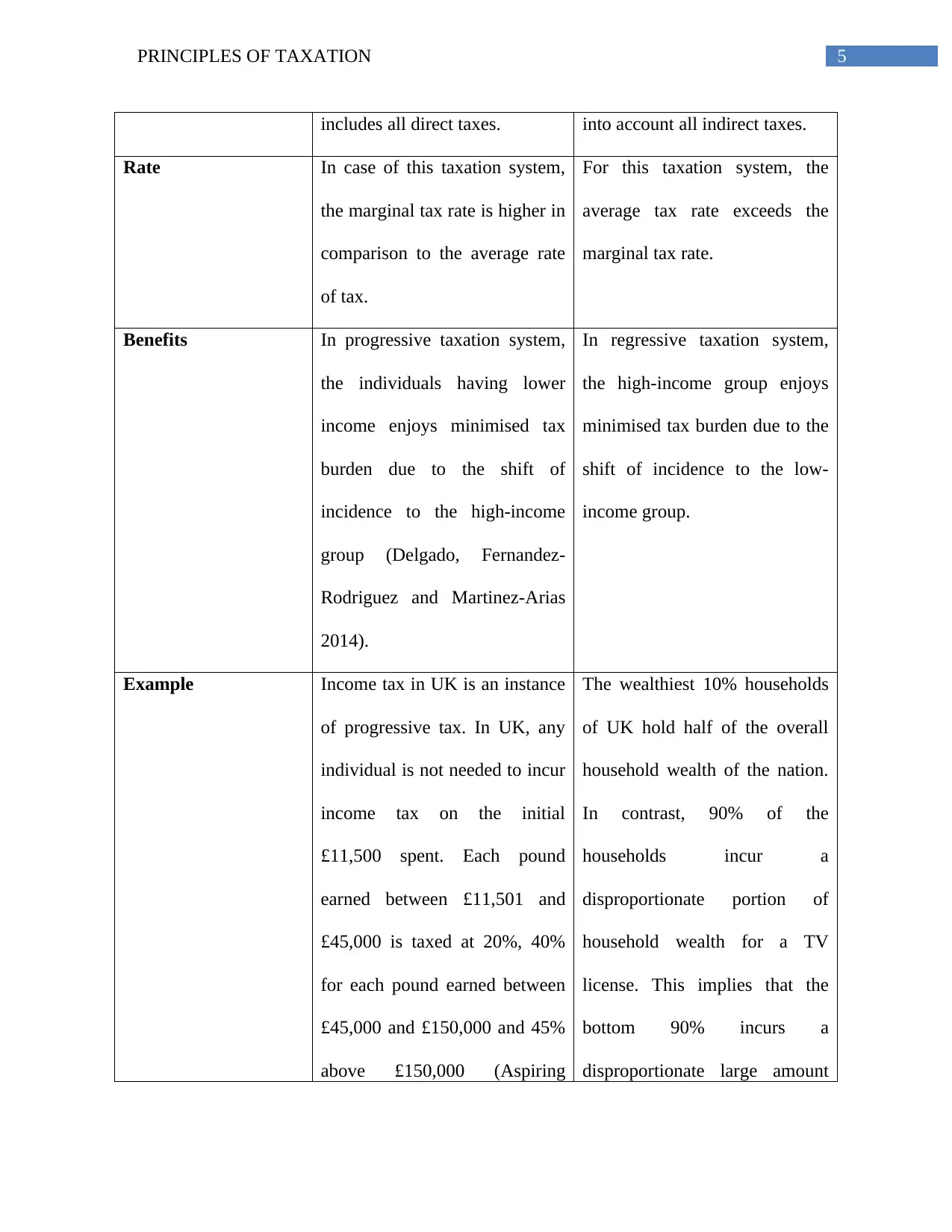

Basis for comparison Progressive Taxation System Regressive Taxation System

Meaning It is a taxation mechanism, in

which there would be rise in tax

rate with increase in taxable

figure.

This is a taxation system, in

which fall in tax rate is obvious

with rise in amount subject to

tax (Devereux, Liu and Loretz

2014).

Assessment Taxes are imposed on profit or

income depending on the

increasing rate schedule.

In case of this taxation system,

the tax is imposed as a

percentage of the asset bought

owned by the assessee.

Ability to pay In this taxation system, the

ability to pay of the assesssee is

taken into consideration.

In case of regressive taxation

system, the level of income of

the taxpayers is not taken into

account (Devereux and Vella

2014).

Inclusion of taxes Progressive taxation system Regressive taxation system takes

tax is accumulated from high-income earners (Brusov et al. 2015). The application of this

taxation system is made uniformly, which implies that there has been fair imposition of tax on all

consumers regardless of their income level and their assets. However, since this tax system is not

related to income, the impact is experienced severely by the low-income earners, since they have

to spend greater portion of their income in the form of tax on necessities.

By considering the basic concepts of the two types of taxation system, the following key

differences are observed between them listed in the form of a table:

Basis for comparison Progressive Taxation System Regressive Taxation System

Meaning It is a taxation mechanism, in

which there would be rise in tax

rate with increase in taxable

figure.

This is a taxation system, in

which fall in tax rate is obvious

with rise in amount subject to

tax (Devereux, Liu and Loretz

2014).

Assessment Taxes are imposed on profit or

income depending on the

increasing rate schedule.

In case of this taxation system,

the tax is imposed as a

percentage of the asset bought

owned by the assessee.

Ability to pay In this taxation system, the

ability to pay of the assesssee is

taken into consideration.

In case of regressive taxation

system, the level of income of

the taxpayers is not taken into

account (Devereux and Vella

2014).

Inclusion of taxes Progressive taxation system Regressive taxation system takes

5PRINCIPLES OF TAXATION

includes all direct taxes. into account all indirect taxes.

Rate In case of this taxation system,

the marginal tax rate is higher in

comparison to the average rate

of tax.

For this taxation system, the

average tax rate exceeds the

marginal tax rate.

Benefits In progressive taxation system,

the individuals having lower

income enjoys minimised tax

burden due to the shift of

incidence to the high-income

group (Delgado, Fernandez-

Rodriguez and Martinez-Arias

2014).

In regressive taxation system,

the high-income group enjoys

minimised tax burden due to the

shift of incidence to the low-

income group.

Example Income tax in UK is an instance

of progressive tax. In UK, any

individual is not needed to incur

income tax on the initial

£11,500 spent. Each pound

earned between £11,501 and

£45,000 is taxed at 20%, 40%

for each pound earned between

£45,000 and £150,000 and 45%

above £150,000 (Aspiring

The wealthiest 10% households

of UK hold half of the overall

household wealth of the nation.

In contrast, 90% of the

households incur a

disproportionate portion of

household wealth for a TV

license. This implies that the

bottom 90% incurs a

disproportionate large amount

includes all direct taxes. into account all indirect taxes.

Rate In case of this taxation system,

the marginal tax rate is higher in

comparison to the average rate

of tax.

For this taxation system, the

average tax rate exceeds the

marginal tax rate.

Benefits In progressive taxation system,

the individuals having lower

income enjoys minimised tax

burden due to the shift of

incidence to the high-income

group (Delgado, Fernandez-

Rodriguez and Martinez-Arias

2014).

In regressive taxation system,

the high-income group enjoys

minimised tax burden due to the

shift of incidence to the low-

income group.

Example Income tax in UK is an instance

of progressive tax. In UK, any

individual is not needed to incur

income tax on the initial

£11,500 spent. Each pound

earned between £11,501 and

£45,000 is taxed at 20%, 40%

for each pound earned between

£45,000 and £150,000 and 45%

above £150,000 (Aspiring

The wealthiest 10% households

of UK hold half of the overall

household wealth of the nation.

In contrast, 90% of the

households incur a

disproportionate portion of

household wealth for a TV

license. This implies that the

bottom 90% incurs a

disproportionate large amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PRINCIPLES OF TAXATION

Accountants 2018). compared to the top 10%.

b) Sources of tax law in the UK:

The UK taxation system is applicable throughout the UK, which includes England,

Northern Ireland, Wales, few smaller islands of the British Coast and Scotland (although it has

some particular differences due to the unique legal system of the nation). Moreover, it includes

oil drilling platforms in the British territorial waters, although it does not take into consideration

the Isle of Man, the Republic of Ireland and the Channel Islands (Dyreng, Hoopes and Wilde

2016).

There are mainly three types of taxes in the UK, which are elucidated briefly as follows:

Proportional tax:

Proportional tax imposes the same percentage of tax on all individuals regardless of their

income level.

Progressive tax:

This system imposes a greater percentage of tax on high-income earning individuals. In

addition, this system is involved in utilising a marginal tax rate, which rises with the increase in

the taxable income amount.

Regressive tax:

Under this taxation system, higher taxes are imposed on low-income earning individuals

in comparison to the high-income earning individuals. For instance, if the sales tax in the state is

Accountants 2018). compared to the top 10%.

b) Sources of tax law in the UK:

The UK taxation system is applicable throughout the UK, which includes England,

Northern Ireland, Wales, few smaller islands of the British Coast and Scotland (although it has

some particular differences due to the unique legal system of the nation). Moreover, it includes

oil drilling platforms in the British territorial waters, although it does not take into consideration

the Isle of Man, the Republic of Ireland and the Channel Islands (Dyreng, Hoopes and Wilde

2016).

There are mainly three types of taxes in the UK, which are elucidated briefly as follows:

Proportional tax:

Proportional tax imposes the same percentage of tax on all individuals regardless of their

income level.

Progressive tax:

This system imposes a greater percentage of tax on high-income earning individuals. In

addition, this system is involved in utilising a marginal tax rate, which rises with the increase in

the taxable income amount.

Regressive tax:

Under this taxation system, higher taxes are imposed on low-income earning individuals

in comparison to the high-income earning individuals. For instance, if the sales tax in the state is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PRINCIPLES OF TAXATION

5%, the individual having lower income would incur a higher percentage of the total income in

the form of sales tax (Egger et al. 2015).

There are some main types of taxes in UK, which include primarily the following:

Income tax is a tax on the income of the individuals, in which the basic income tax rate

is 20% incurred on income over the income tax threshold, as decided on the part of the

government (HMRC)

National insurance contributions are another kind of income tax, which are dependent on

an identical principle of taking a fixed income percentage

Consumption tax in the form of Value Added Tax (VAT), which is 17.50% in the UK

Excise duties on tobacco and alcohol

Corporation tax, which is a tax on business profit (Corporation Tax Act 2010)

Stamp duty, which is the tax incurred on the purchase of shares or houses

There has been no single source of UK tax law. The basic rules have been mentioned in the

Parliament Acts; however, the decision is on the courts for interpreting the acts along with

providing much of the details of the tax system (Farnsworth and Fooks 2015). Along with this,

HMRC is engaged in issuing a number of statements, leaflets and notices explaining the ways

through which the laws are enforced in practice. These statements assist in explaining the

interpretation of the law by the tax authority and they have to be complied with unless

challenged in the courts successfully.

The changes to the tax system, which contradict with the speech of the annual budget in

March, are intended primarily in taking effect as from the initiation of the next tax period

(Gemmell et al. 2018). In case of individuals, the tax year termed as year of assessment or fiscal

5%, the individual having lower income would incur a higher percentage of the total income in

the form of sales tax (Egger et al. 2015).

There are some main types of taxes in UK, which include primarily the following:

Income tax is a tax on the income of the individuals, in which the basic income tax rate

is 20% incurred on income over the income tax threshold, as decided on the part of the

government (HMRC)

National insurance contributions are another kind of income tax, which are dependent on

an identical principle of taking a fixed income percentage

Consumption tax in the form of Value Added Tax (VAT), which is 17.50% in the UK

Excise duties on tobacco and alcohol

Corporation tax, which is a tax on business profit (Corporation Tax Act 2010)

Stamp duty, which is the tax incurred on the purchase of shares or houses

There has been no single source of UK tax law. The basic rules have been mentioned in the

Parliament Acts; however, the decision is on the courts for interpreting the acts along with

providing much of the details of the tax system (Farnsworth and Fooks 2015). Along with this,

HMRC is engaged in issuing a number of statements, leaflets and notices explaining the ways

through which the laws are enforced in practice. These statements assist in explaining the

interpretation of the law by the tax authority and they have to be complied with unless

challenged in the courts successfully.

The changes to the tax system, which contradict with the speech of the annual budget in

March, are intended primarily in taking effect as from the initiation of the next tax period

(Gemmell et al. 2018). In case of individuals, the tax year termed as year of assessment or fiscal

8PRINCIPLES OF TAXATION

year as well, begins from 6th April to the following 5th April inclusive. For instance, the tax year

2017-18 would start on 6th April 2017 and it would end on 5th April 2018. However, in case of

business organisations, the tax year tends to show slight variation. The tax year for an

organisation initiates from 1st April to the following 31st March.

The taxpayers are needed to maintain effective records for making accurate tax return and if

needed, they could substantiate the figures entered on return. A taxpayer involved in business or

renting property needs to maintain records for five years after 31st January following the end of

the concerned tax year. In opposition, records could be kept for one year after 31st January

following the completion of the tax year.

In addition, the taxpayers need to provide complete and accurate information. The

dishonest behaviour like concealing an income source is tax evasion, which is against the law.

On summary conviction in the court of a magistrate, the offenders might be imprisoned for six

months and they might be imposed a fine of maximum of £5,000 (Griffith, Miller and O'Connell

2014). On a higher court indictment, the penalties are raised to maximum seven years coupled

with unlimited fine.

The taxpayers possess the right of appeal against particular HRMC (Her Majesty’s

Revenue and Customs) decisions. The appeals that could not be settled between HMRC and the

taxpayer are dealt by seeking assistance from the two-tier tribunal system.

c) Comparison and contrast of tax avoidance and tax evasion:

Tax avoidance could be defined as a method where the assessee tries to beat the primary

intention of the law legally by seeking benefits of the drawbacks in the legislation. On the other

hand, tax evasion is a method of minimising tax liability by illicit practices like inflating

year as well, begins from 6th April to the following 5th April inclusive. For instance, the tax year

2017-18 would start on 6th April 2017 and it would end on 5th April 2018. However, in case of

business organisations, the tax year tends to show slight variation. The tax year for an

organisation initiates from 1st April to the following 31st March.

The taxpayers are needed to maintain effective records for making accurate tax return and if

needed, they could substantiate the figures entered on return. A taxpayer involved in business or

renting property needs to maintain records for five years after 31st January following the end of

the concerned tax year. In opposition, records could be kept for one year after 31st January

following the completion of the tax year.

In addition, the taxpayers need to provide complete and accurate information. The

dishonest behaviour like concealing an income source is tax evasion, which is against the law.

On summary conviction in the court of a magistrate, the offenders might be imprisoned for six

months and they might be imposed a fine of maximum of £5,000 (Griffith, Miller and O'Connell

2014). On a higher court indictment, the penalties are raised to maximum seven years coupled

with unlimited fine.

The taxpayers possess the right of appeal against particular HRMC (Her Majesty’s

Revenue and Customs) decisions. The appeals that could not be settled between HMRC and the

taxpayer are dealt by seeking assistance from the two-tier tribunal system.

c) Comparison and contrast of tax avoidance and tax evasion:

Tax avoidance could be defined as a method where the assessee tries to beat the primary

intention of the law legally by seeking benefits of the drawbacks in the legislation. On the other

hand, tax evasion is a method of minimising tax liability by illicit practices like inflating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PRINCIPLES OF TAXATION

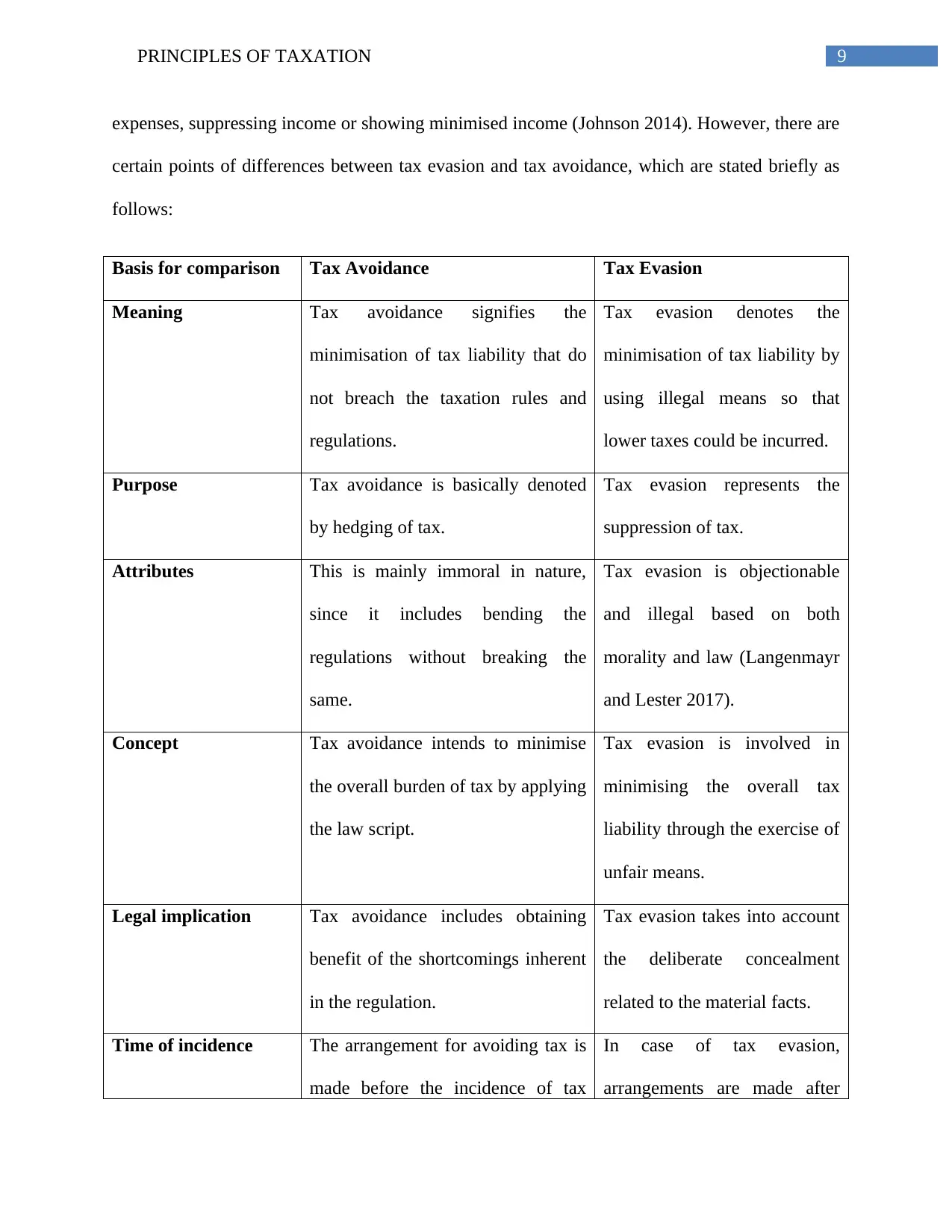

expenses, suppressing income or showing minimised income (Johnson 2014). However, there are

certain points of differences between tax evasion and tax avoidance, which are stated briefly as

follows:

Basis for comparison Tax Avoidance Tax Evasion

Meaning Tax avoidance signifies the

minimisation of tax liability that do

not breach the taxation rules and

regulations.

Tax evasion denotes the

minimisation of tax liability by

using illegal means so that

lower taxes could be incurred.

Purpose Tax avoidance is basically denoted

by hedging of tax.

Tax evasion represents the

suppression of tax.

Attributes This is mainly immoral in nature,

since it includes bending the

regulations without breaking the

same.

Tax evasion is objectionable

and illegal based on both

morality and law (Langenmayr

and Lester 2017).

Concept Tax avoidance intends to minimise

the overall burden of tax by applying

the law script.

Tax evasion is involved in

minimising the overall tax

liability through the exercise of

unfair means.

Legal implication Tax avoidance includes obtaining

benefit of the shortcomings inherent

in the regulation.

Tax evasion takes into account

the deliberate concealment

related to the material facts.

Time of incidence The arrangement for avoiding tax is

made before the incidence of tax

In case of tax evasion,

arrangements are made after

expenses, suppressing income or showing minimised income (Johnson 2014). However, there are

certain points of differences between tax evasion and tax avoidance, which are stated briefly as

follows:

Basis for comparison Tax Avoidance Tax Evasion

Meaning Tax avoidance signifies the

minimisation of tax liability that do

not breach the taxation rules and

regulations.

Tax evasion denotes the

minimisation of tax liability by

using illegal means so that

lower taxes could be incurred.

Purpose Tax avoidance is basically denoted

by hedging of tax.

Tax evasion represents the

suppression of tax.

Attributes This is mainly immoral in nature,

since it includes bending the

regulations without breaking the

same.

Tax evasion is objectionable

and illegal based on both

morality and law (Langenmayr

and Lester 2017).

Concept Tax avoidance intends to minimise

the overall burden of tax by applying

the law script.

Tax evasion is involved in

minimising the overall tax

liability through the exercise of

unfair means.

Legal implication Tax avoidance includes obtaining

benefit of the shortcomings inherent

in the regulation.

Tax evasion takes into account

the deliberate concealment

related to the material facts.

Time of incidence The arrangement for avoiding tax is

made before the incidence of tax

In case of tax evasion,

arrangements are made after

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PRINCIPLES OF TAXATION

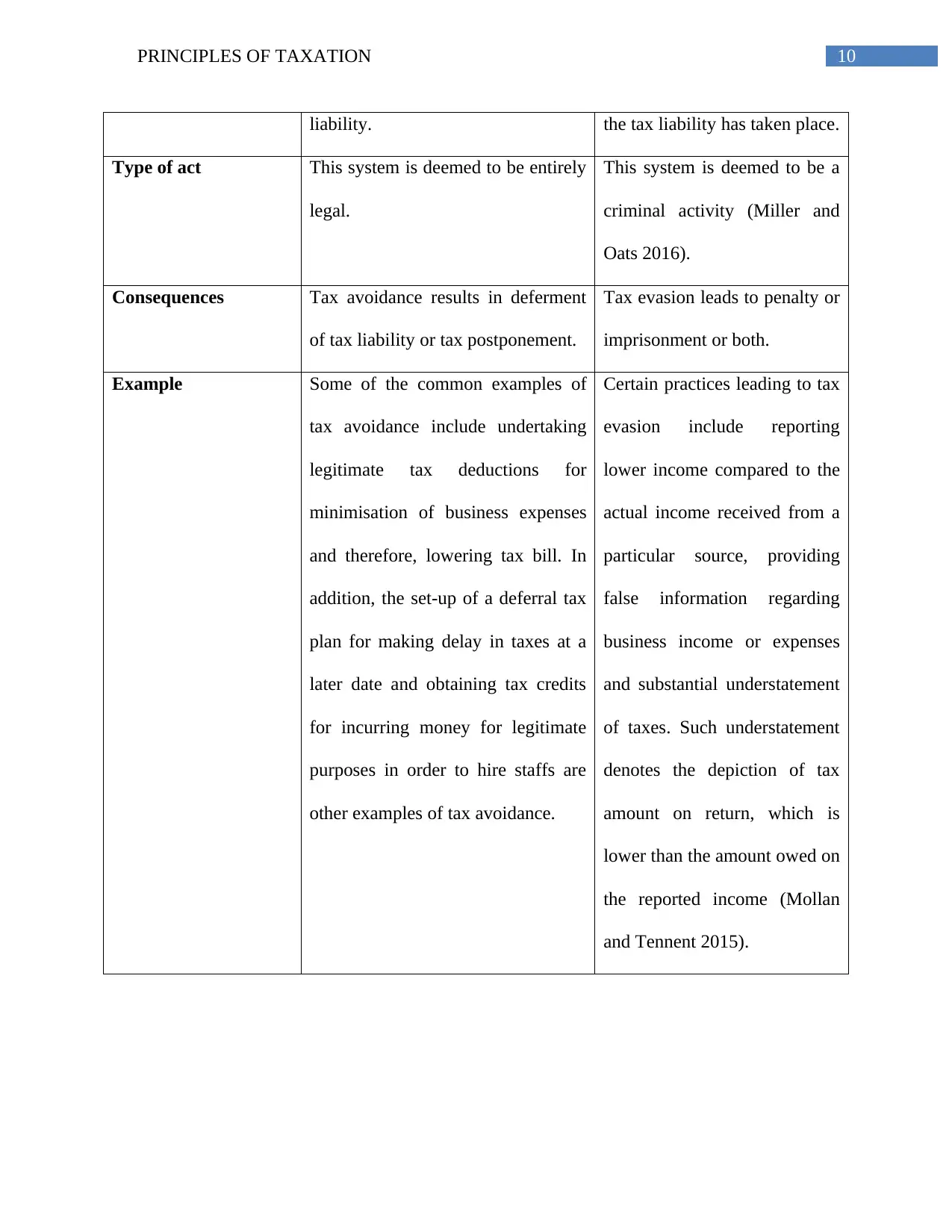

liability. the tax liability has taken place.

Type of act This system is deemed to be entirely

legal.

This system is deemed to be a

criminal activity (Miller and

Oats 2016).

Consequences Tax avoidance results in deferment

of tax liability or tax postponement.

Tax evasion leads to penalty or

imprisonment or both.

Example Some of the common examples of

tax avoidance include undertaking

legitimate tax deductions for

minimisation of business expenses

and therefore, lowering tax bill. In

addition, the set-up of a deferral tax

plan for making delay in taxes at a

later date and obtaining tax credits

for incurring money for legitimate

purposes in order to hire staffs are

other examples of tax avoidance.

Certain practices leading to tax

evasion include reporting

lower income compared to the

actual income received from a

particular source, providing

false information regarding

business income or expenses

and substantial understatement

of taxes. Such understatement

denotes the depiction of tax

amount on return, which is

lower than the amount owed on

the reported income (Mollan

and Tennent 2015).

liability. the tax liability has taken place.

Type of act This system is deemed to be entirely

legal.

This system is deemed to be a

criminal activity (Miller and

Oats 2016).

Consequences Tax avoidance results in deferment

of tax liability or tax postponement.

Tax evasion leads to penalty or

imprisonment or both.

Example Some of the common examples of

tax avoidance include undertaking

legitimate tax deductions for

minimisation of business expenses

and therefore, lowering tax bill. In

addition, the set-up of a deferral tax

plan for making delay in taxes at a

later date and obtaining tax credits

for incurring money for legitimate

purposes in order to hire staffs are

other examples of tax avoidance.

Certain practices leading to tax

evasion include reporting

lower income compared to the

actual income received from a

particular source, providing

false information regarding

business income or expenses

and substantial understatement

of taxes. Such understatement

denotes the depiction of tax

amount on return, which is

lower than the amount owed on

the reported income (Mollan

and Tennent 2015).

11PRINCIPLES OF TAXATION

Conclusion:

From the above discussion, it is inherent that there are certain differences between the

progressive taxation system and the regressive taxation system. It has been found that in case of

progressive taxation system, the low-income earners enjoy minimised tax burden, while the

situation is just the opposite in case of regressive taxation system. Moreover, the UK is identified

to have certain sources of tax and the primary rules are mentioned in the Acts of the Parliament;

however, the ultimate decision lies in the hands of the courts. Finally, it has been evaluated that

tax avoidance and tax evasion are completely different concepts. This is because tax avoidance

involves using the loopholes of the current tax regulations to minimise tax liability, while tax

evasion intends to minimise tax liability by using unfair means.

Conclusion:

From the above discussion, it is inherent that there are certain differences between the

progressive taxation system and the regressive taxation system. It has been found that in case of

progressive taxation system, the low-income earners enjoy minimised tax burden, while the

situation is just the opposite in case of regressive taxation system. Moreover, the UK is identified

to have certain sources of tax and the primary rules are mentioned in the Acts of the Parliament;

however, the ultimate decision lies in the hands of the courts. Finally, it has been evaluated that

tax avoidance and tax evasion are completely different concepts. This is because tax avoidance

involves using the loopholes of the current tax regulations to minimise tax liability, while tax

evasion intends to minimise tax liability by using unfair means.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.