Comprehensive Analysis of UK Business Taxation: VAT and More

VerifiedAdded on 2023/06/10

|40

|14658

|204

Report

AI Summary

This report provides a comprehensive overview of business taxation in the UK, focusing on self-assessment tax, VAT procedures, and corporation tax liabilities. Task 1 details the nature and purpose of self-assessment tax, determination of worker tax status, taxable amount calculations, and ethical considerations. It also evaluates taxpayer obligations and implications of non-compliance. Task 2 discusses UK tax law implications for both unincorporated and incorporated businesses, determination of capital gains taxes, chargeable gains subject to corporation taxes, adjusted profit calculations, and corporation tax liabilities. Task 3 describes VAT registration and administration procedures, computes tax under VAT schemes for small businesses, provides examples of VAT liability calculations, and discusses potential VAT penalties. The report includes practical examples and scenarios to illustrate key concepts and computations, offering valuable insights into the complexities of the UK tax system. Desklib provides access to this and other solved assignments for students.

Business Taxation

UNIT 603/4848/3

Learning Development Training

UNIT 603/4848/3

Learning Development Training

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION------------------------------------------------------------------------------------------------------------------------------- 3

TASK 1------------------------------------------------------------------------------------------------------------------------------------------- 4

NATURE AND PURPOSE OF SELF-ASSESSMENT TAX--------------------------------------------------------------------------------------------4

DETERMINATION OF TAX STATUS OF WORKERS------------------------------------------------------------------------------------------------5

DETERMINATION OF TAXABLE AMOUNTS AND CALCULATION OF TAX PAYABLE FOR A SCENARIO.-----------------------------------------7

COMPLETED SELF-ASSESSMENT TAX RETURN-------------------------------------------------------------------------------------------------10

ETHICAL ISSUES ARISING AT THE TIME OF PERFORMING TAX WORK-------------------------------------------------------------------------10

EVALUATION OF OBLIGATIONS OF TAX SYSTEM IMPOSES ON TAXPAYER AND IMPLICATION FOR TAXPAYER-------------------------------12

OF NON COMPLIANCE--------------------------------------------------------------------------------------------------------------------------12

TASK 2------------------------------------------------------------------------------------------------------------------------------------------ 13

DISCUSSION OF UK TAX LAW AND ITS IMPLICATIONS FOR UNINCORPORATED AND INCORPORATED-------------------------------------13

BUSINESSES-------------------------------------------------------------------------------------------------------------------------------------13

IMPLICATION OF UK TAX LAW FOR INCORPORATED BUSINESSES---------------------------------------------------------------------------14

IMPLICATION OF TAX LAW FOR UN-INCORPORATED BUSINESSES.--------------------------------------------------------------------------15

DETERMINATION OF CAPITAL GAIN TAXES PAYABLE AND CHARGEABLE GAINS SUBJECT TO CORPORATION-------------------------------15

TAXES.------------------------------------------------------------------------------------------------------------------------------------------15

Determination of Capital Gain Tax :--------------------------------------------------------------------------------------------- 16

DETERMINATION OF CHARGEABLE GAIN SUBJECT TO CORPORATION TAX------------------------------------------------------------------18

CALCULATION OF ADJUSTED PROFIT FOR CORPORATION TAX PURPOSES.------------------------------------------------------------------18

CALCULATION OF CORPORATION TAX LIABILITIES--------------------------------------------------------------------------------------------22

TASK 3------------------------------------------------------------------------------------------------------------------------------------------ 23

DESCRIBING THE REGISTRATION AND ADMINISTRATION PROCEDURES FOR VAT-----------------------------------------------------------23

COMPUTING TAX UNDER VAT SCHEMES FOR SMALL BUSINESS ORGANISATIONS----------------------------------------------------------26

Tax under flat rate:------------------------------------------------------------------------------------------------------------------ 27

Cash accounting scheme----------------------------------------------------------------------------------------------------------- 28

Annual accounting scheme-------------------------------------------------------------------------------------------------------- 28

PROVIDING EXAMPLES OF CALCULATION OF VAT LIABILITIES------------------------------------------------------------------------------29

DISCUSSING VAT PENALTIES THAT CAN ARISE-----------------------------------------------------------------------------------------------32

CONCLUSION--------------------------------------------------------------------------------------------------------------------------------- 34

REFERENCES---------------------------------------------------------------------------------------------------------------------------------- 35

INTRODUCTION------------------------------------------------------------------------------------------------------------------------------- 3

TASK 1------------------------------------------------------------------------------------------------------------------------------------------- 4

NATURE AND PURPOSE OF SELF-ASSESSMENT TAX--------------------------------------------------------------------------------------------4

DETERMINATION OF TAX STATUS OF WORKERS------------------------------------------------------------------------------------------------5

DETERMINATION OF TAXABLE AMOUNTS AND CALCULATION OF TAX PAYABLE FOR A SCENARIO.-----------------------------------------7

COMPLETED SELF-ASSESSMENT TAX RETURN-------------------------------------------------------------------------------------------------10

ETHICAL ISSUES ARISING AT THE TIME OF PERFORMING TAX WORK-------------------------------------------------------------------------10

EVALUATION OF OBLIGATIONS OF TAX SYSTEM IMPOSES ON TAXPAYER AND IMPLICATION FOR TAXPAYER-------------------------------12

OF NON COMPLIANCE--------------------------------------------------------------------------------------------------------------------------12

TASK 2------------------------------------------------------------------------------------------------------------------------------------------ 13

DISCUSSION OF UK TAX LAW AND ITS IMPLICATIONS FOR UNINCORPORATED AND INCORPORATED-------------------------------------13

BUSINESSES-------------------------------------------------------------------------------------------------------------------------------------13

IMPLICATION OF UK TAX LAW FOR INCORPORATED BUSINESSES---------------------------------------------------------------------------14

IMPLICATION OF TAX LAW FOR UN-INCORPORATED BUSINESSES.--------------------------------------------------------------------------15

DETERMINATION OF CAPITAL GAIN TAXES PAYABLE AND CHARGEABLE GAINS SUBJECT TO CORPORATION-------------------------------15

TAXES.------------------------------------------------------------------------------------------------------------------------------------------15

Determination of Capital Gain Tax :--------------------------------------------------------------------------------------------- 16

DETERMINATION OF CHARGEABLE GAIN SUBJECT TO CORPORATION TAX------------------------------------------------------------------18

CALCULATION OF ADJUSTED PROFIT FOR CORPORATION TAX PURPOSES.------------------------------------------------------------------18

CALCULATION OF CORPORATION TAX LIABILITIES--------------------------------------------------------------------------------------------22

TASK 3------------------------------------------------------------------------------------------------------------------------------------------ 23

DESCRIBING THE REGISTRATION AND ADMINISTRATION PROCEDURES FOR VAT-----------------------------------------------------------23

COMPUTING TAX UNDER VAT SCHEMES FOR SMALL BUSINESS ORGANISATIONS----------------------------------------------------------26

Tax under flat rate:------------------------------------------------------------------------------------------------------------------ 27

Cash accounting scheme----------------------------------------------------------------------------------------------------------- 28

Annual accounting scheme-------------------------------------------------------------------------------------------------------- 28

PROVIDING EXAMPLES OF CALCULATION OF VAT LIABILITIES------------------------------------------------------------------------------29

DISCUSSING VAT PENALTIES THAT CAN ARISE-----------------------------------------------------------------------------------------------32

CONCLUSION--------------------------------------------------------------------------------------------------------------------------------- 34

REFERENCES---------------------------------------------------------------------------------------------------------------------------------- 35

APPENDIX------------------------------------------------------------------------------------------------------------------------------------- 38

ADDITIONAL INFORMATION-------------------------------------------------------------------------------------------------------------------39

Investment Income------------------------------------------------------------------------------------------------------------------ 39

ADDITIONAL INFORMATION-------------------------------------------------------------------------------------------------------------------39

Investment Income------------------------------------------------------------------------------------------------------------------ 39

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Taxation is basically referring as an act of levying or imposing tax on individual or business by a

taxing authority. Tax is the main source of revenue for the three level of government of UK such

as central government and local government. In United Kingdom, Central government revenues

come primarily from income tax, national insurance contribution, value added tax, corporation

tax and last fuel duty. Grants from the federal government, business rates in England, Council

Tax, and, increasingly, fees and levies such as those for on-street parking, are the main sources

of revenue for local governments (Budak and James, 2018).

In the United Kingdom, around 32 million individuals pay taxes. Different UK tax regulations,

on the other hand, influence how income tax is collected. Scotland's tax bands differ somewhat

from those in England, Wales, and Northern Ireland. Income taxes, property taxes, capital gains

taxes, UK inheritance taxes, and VAT are all examples of basic UK taxes (van de Ven and

Hérault, 2022). Many of them are progressive taxes, which means that individuals with higher

earnings pay more. England, Scotland (though there are some special distinctions due to

Scotland's distinctive legal system), Wales, Northern Ireland, and several of the smaller islands

off the British coast are all covered by the British fiscal system. It also covers oil drilling

platforms in British territorial seas, while the Channel Islands and the Isle of Man are excluded.

The present report will cover the three task and in each task the detail discussion of taxation will

be taken place. In the first task, the report will cover a booklet stating information on Self-

Assessment Taxation. The report will also calculate the corporate tax liabilities based on own

chosen scenario or figures in order to include the deep information on taxations (Langenmayr

and Liu, 2020). Further, in the second task, the report will present the corporate tax information

along with the practical example or problems. Lastly, the third task of the report will cover the

written booklet discussing the Vat return and computation of tax under VAT scheme.

Taxation is basically referring as an act of levying or imposing tax on individual or business by a

taxing authority. Tax is the main source of revenue for the three level of government of UK such

as central government and local government. In United Kingdom, Central government revenues

come primarily from income tax, national insurance contribution, value added tax, corporation

tax and last fuel duty. Grants from the federal government, business rates in England, Council

Tax, and, increasingly, fees and levies such as those for on-street parking, are the main sources

of revenue for local governments (Budak and James, 2018).

In the United Kingdom, around 32 million individuals pay taxes. Different UK tax regulations,

on the other hand, influence how income tax is collected. Scotland's tax bands differ somewhat

from those in England, Wales, and Northern Ireland. Income taxes, property taxes, capital gains

taxes, UK inheritance taxes, and VAT are all examples of basic UK taxes (van de Ven and

Hérault, 2022). Many of them are progressive taxes, which means that individuals with higher

earnings pay more. England, Scotland (though there are some special distinctions due to

Scotland's distinctive legal system), Wales, Northern Ireland, and several of the smaller islands

off the British coast are all covered by the British fiscal system. It also covers oil drilling

platforms in British territorial seas, while the Channel Islands and the Isle of Man are excluded.

The present report will cover the three task and in each task the detail discussion of taxation will

be taken place. In the first task, the report will cover a booklet stating information on Self-

Assessment Taxation. The report will also calculate the corporate tax liabilities based on own

chosen scenario or figures in order to include the deep information on taxations (Langenmayr

and Liu, 2020). Further, in the second task, the report will present the corporate tax information

along with the practical example or problems. Lastly, the third task of the report will cover the

written booklet discussing the Vat return and computation of tax under VAT scheme.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 1

Nature and Purpose of Self-assessment tax

Self-assessment tax is known as any pending tax liabilities that need to be paid by the individual

at the end of the financial year after evaluating their total taxable income, reducing deductions

and taxes paid. This is a system HM Revenue & Customs uses to collect Income tax. Generally,

the tax is deducted automatically from wages, pensions and savings. People and business with

other income including various covid grants must report it in a self-assessment return. (gov.uk).

All resident of UK need to maintain and follow this regulation. The nature of self-assessment tax

is such that it helps the individual or businesses to pay balance tax on his assessed income after

the TDS and advance tax. The purpose of the self-assessment tax is to help the taxpayer to pay

any of the tax dues after the payment of advance tax that they need to pay before the end of the

financial year under the self-assessment tax (Holland, Lindop and Abdul Wahab, 2021). This is

paid by salaries' taxpayer, self-employed tax payer, corporate etc.

As the UK's tax, payment, and customs agencies, it taxes both domestic and foreign incomes of

everyone resident in the country. Employment and benefits from the job, profits from one’s own

business, state benefits, pensions, rent, interest from savings, dividends from a trust, and other

sources of income are all possibilities.

HM Revenue and Customs (HMRC) is in charge of tax administration and collection in the

United Kingdom. In 2020/21, the UK's tax collections were estimated to be at £584.5 billion,

down 7.7% from the previous tax year.

The self-assessment tax is generally computed on income from all sources and acts as a final

option for the tax payer to pay the whole tax. Any tax due because of the self-assessment tax

return must be paid by 31st January after the tax yearends. For example, the tax due for the tax

year 05.04.2021 must be paid by 31st January 22. The HMRC may charge late payment interest

and/or penalty if paid later than 31st January. In this way, it can be said that the nature and

purpose of self-assessment tax is to help the government of UK to collect the taxes from the

taxpayer and enhance the revenue of the government. The self-assessment tax is basically

progressive in nature which means the higher the income of taxpayer, the high the tax payment

Nature and Purpose of Self-assessment tax

Self-assessment tax is known as any pending tax liabilities that need to be paid by the individual

at the end of the financial year after evaluating their total taxable income, reducing deductions

and taxes paid. This is a system HM Revenue & Customs uses to collect Income tax. Generally,

the tax is deducted automatically from wages, pensions and savings. People and business with

other income including various covid grants must report it in a self-assessment return. (gov.uk).

All resident of UK need to maintain and follow this regulation. The nature of self-assessment tax

is such that it helps the individual or businesses to pay balance tax on his assessed income after

the TDS and advance tax. The purpose of the self-assessment tax is to help the taxpayer to pay

any of the tax dues after the payment of advance tax that they need to pay before the end of the

financial year under the self-assessment tax (Holland, Lindop and Abdul Wahab, 2021). This is

paid by salaries' taxpayer, self-employed tax payer, corporate etc.

As the UK's tax, payment, and customs agencies, it taxes both domestic and foreign incomes of

everyone resident in the country. Employment and benefits from the job, profits from one’s own

business, state benefits, pensions, rent, interest from savings, dividends from a trust, and other

sources of income are all possibilities.

HM Revenue and Customs (HMRC) is in charge of tax administration and collection in the

United Kingdom. In 2020/21, the UK's tax collections were estimated to be at £584.5 billion,

down 7.7% from the previous tax year.

The self-assessment tax is generally computed on income from all sources and acts as a final

option for the tax payer to pay the whole tax. Any tax due because of the self-assessment tax

return must be paid by 31st January after the tax yearends. For example, the tax due for the tax

year 05.04.2021 must be paid by 31st January 22. The HMRC may charge late payment interest

and/or penalty if paid later than 31st January. In this way, it can be said that the nature and

purpose of self-assessment tax is to help the government of UK to collect the taxes from the

taxpayer and enhance the revenue of the government. The self-assessment tax is basically

progressive in nature which means the higher the income of taxpayer, the high the tax payment

for them. It is computed by deducting the tax paid at source or advance tax from the total tax

liability of individual. For example, total tax liability of an individual is £25,000 and the advance

tax paid by that individual is £22,500. In such case, the additional £2,500 tax need to be paid by

that individual.

Determination of tax status of workers

In order to determine the tax status of workers, first it is important to understand the employment

status of the worker. It is because how worker is taxed depends on the employment status of the

worker, employed or self-employed for tax and national insurance contribution. HMRC has

introduced Check Employment Status for Tax (CEST) tool in order to understand and determine

the employment status of worker for tax as well as NIC purposes (Liu, 2018). This tool provides

the following determination based on the information provided by worker:

Employed for tax purpose

Self-employed for tax purpose

Off-payroll working rule apply

Off-payroll working rule do not apply.

Generally, the contract between employer and worker determines the status of the worker is

employed or self-employed. There are also other factors as below that play their role to

determine the status of the worker if they fall under employment or self-employment.

Mutuality of Obligation: When an employer is under an obligation to provide a work

and pay for that work and the worker is under the same obligation to accept the work and

perform the work as given, this is usually a relation of employment. Contra to this if

worker is self-employed if they will not guarantee of work and even if work is given to

them, they are free to accept or refuse the work.

Right of control: if worker is guided or told how to do the certain task then it is more

likely to form an employment. On the other hand, self-employment personal will have

their own control on how the task will be completed and the deadline for completion of

that task.

Provision Equipment: normally, an employee is not responsible for using their own

equipment to perform a duty. On the other hand, self-employed person will normally be

responsible for providing the necessary equipment to complete the task accepted.

liability of individual. For example, total tax liability of an individual is £25,000 and the advance

tax paid by that individual is £22,500. In such case, the additional £2,500 tax need to be paid by

that individual.

Determination of tax status of workers

In order to determine the tax status of workers, first it is important to understand the employment

status of the worker. It is because how worker is taxed depends on the employment status of the

worker, employed or self-employed for tax and national insurance contribution. HMRC has

introduced Check Employment Status for Tax (CEST) tool in order to understand and determine

the employment status of worker for tax as well as NIC purposes (Liu, 2018). This tool provides

the following determination based on the information provided by worker:

Employed for tax purpose

Self-employed for tax purpose

Off-payroll working rule apply

Off-payroll working rule do not apply.

Generally, the contract between employer and worker determines the status of the worker is

employed or self-employed. There are also other factors as below that play their role to

determine the status of the worker if they fall under employment or self-employment.

Mutuality of Obligation: When an employer is under an obligation to provide a work

and pay for that work and the worker is under the same obligation to accept the work and

perform the work as given, this is usually a relation of employment. Contra to this if

worker is self-employed if they will not guarantee of work and even if work is given to

them, they are free to accept or refuse the work.

Right of control: if worker is guided or told how to do the certain task then it is more

likely to form an employment. On the other hand, self-employment personal will have

their own control on how the task will be completed and the deadline for completion of

that task.

Provision Equipment: normally, an employee is not responsible for using their own

equipment to perform a duty. On the other hand, self-employed person will normally be

responsible for providing the necessary equipment to complete the task accepted.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Right of providing Substitution: If an employee, for whatever reason, unable to

perform their duties, they cannot supply a substitute to perform that duty. On the other

hand, self-employed people are free to provide substitute to complete the duty.

Financial Risk: Normally, an employee is not responsible for profit or loss from direct or

indirect result of the performance of the duty. On other hand, self-employed people are

responsible for the result of the performance of the duty, they may get profit or suffer a

loss.

Payment: Normally, an employee is paid by one employer and on-one else. On the other

hand, if a worker typically performs services for a number of different clients, they are

self-employed.

In summery, worker is considered as employed by you if most of the following statements apply

to them;

you can tell them what work to do, as well as how, where and when to do it

they have to do their work themselves

you can move the worker from task to task

they are contracted to work a set number of hours

they get a regular wage or salary, even if there is no work available

they have benefits such as paid leave or a pension as part of their contract

you pay them overtime pay or bonus payments

they manage anyone else who works for you

The worker is considered as self-employed if most of the following statements apply to them;

they can hire someone else to do the work you have given them, or take on helpers at

their own expense

they can decide what work is done and when, where, or how it is done

you pay them an agreed fixed price – it does not depend on how long the job takes to

finish

they can make a loss or a profit

they use their own money to buy business assets, pay for running costs and so on

they are responsible for putting right any unsatisfactory work, at their own expense and in

their own time

they provide significant tools and equipment that are fundamental for their work

If the worker is an employee then you have important responsibilities including deducting tax

and national Insurance from their pay and paying this deduction to HMRC.

perform their duties, they cannot supply a substitute to perform that duty. On the other

hand, self-employed people are free to provide substitute to complete the duty.

Financial Risk: Normally, an employee is not responsible for profit or loss from direct or

indirect result of the performance of the duty. On other hand, self-employed people are

responsible for the result of the performance of the duty, they may get profit or suffer a

loss.

Payment: Normally, an employee is paid by one employer and on-one else. On the other

hand, if a worker typically performs services for a number of different clients, they are

self-employed.

In summery, worker is considered as employed by you if most of the following statements apply

to them;

you can tell them what work to do, as well as how, where and when to do it

they have to do their work themselves

you can move the worker from task to task

they are contracted to work a set number of hours

they get a regular wage or salary, even if there is no work available

they have benefits such as paid leave or a pension as part of their contract

you pay them overtime pay or bonus payments

they manage anyone else who works for you

The worker is considered as self-employed if most of the following statements apply to them;

they can hire someone else to do the work you have given them, or take on helpers at

their own expense

they can decide what work is done and when, where, or how it is done

you pay them an agreed fixed price – it does not depend on how long the job takes to

finish

they can make a loss or a profit

they use their own money to buy business assets, pay for running costs and so on

they are responsible for putting right any unsatisfactory work, at their own expense and in

their own time

they provide significant tools and equipment that are fundamental for their work

If the worker is an employee then you have important responsibilities including deducting tax

and national Insurance from their pay and paying this deduction to HMRC.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If a worker or individual, that provide service to various customers on their own name on a

regular basis and the turnover from its services is more than £1,000 then in such case such

worker is considered as self-employed for the tax purpose and they need to file tax return under

self-employment status. The self-employed worker in UK pay Class 2 NIC in case if their profit

is more than £6,515 during the financial year 2021-22 (£6,725 for tax year 2022-23). In addition

to class 2 NIC, they also pay class 4 NIC in case if their profit is more than £9,568 for 2021-22

(£9,880 for 2022-23) (www.gov.uk).

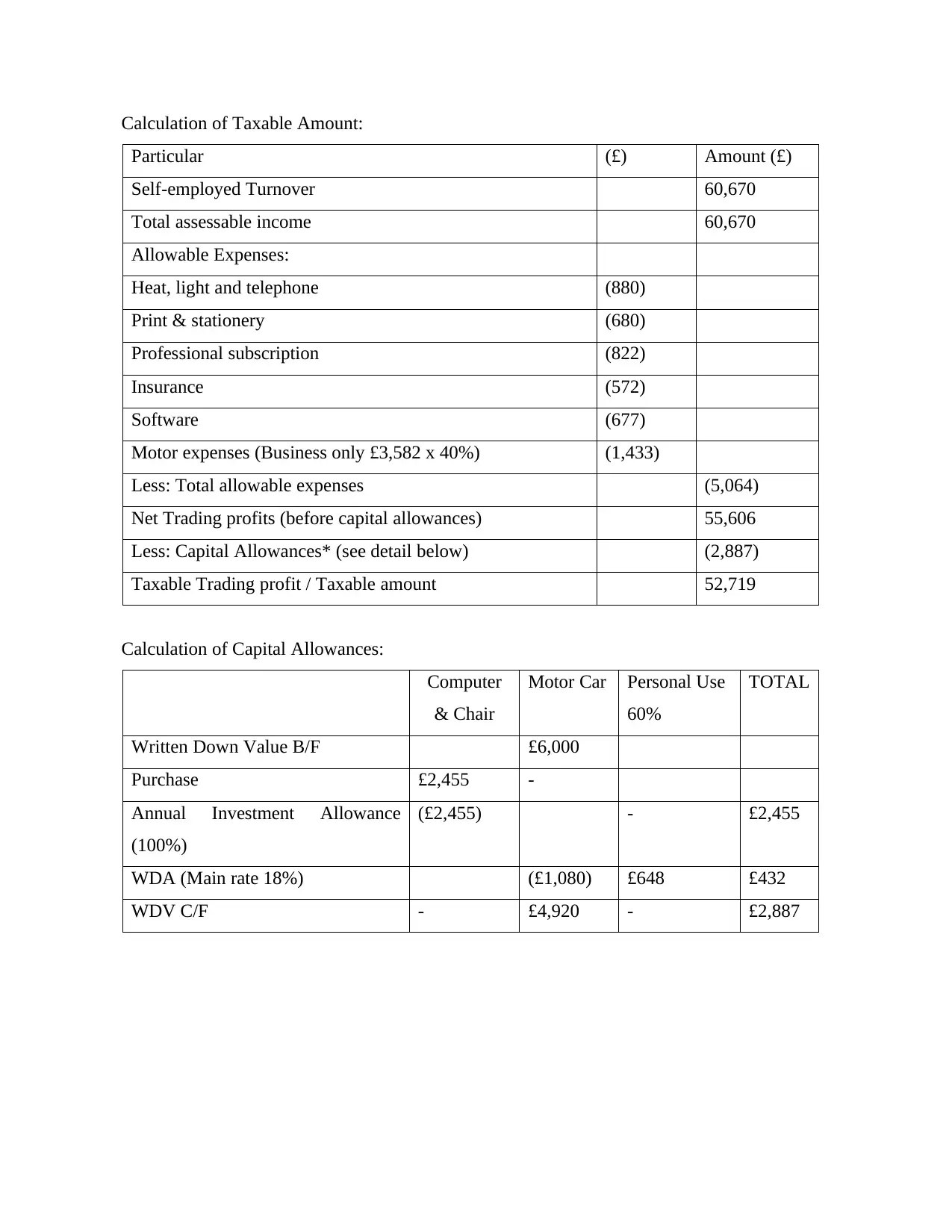

Determination of Taxable amounts and Calculation of Tax Payable for a scenario.

For the purpose of computation of taxable amount and tax payable the scenario is chosen is self-

employment. For example, Mr A is a self-employed individual that worked independently at

home. Their self-employed turnover for year 2021-2022 is £60,670. He incurs business

proportion of light, heat and telephone is £880, print & stationary £680, Professional

Subscription £822, Insurance 572, software £677, new computer & chair purchased for £2,455

and Motor expenses for the year ended 5 April 2022 was £3,582 out of which only 40% relates

to business use and remaining 60% is of private (Steenbergen and Weber, 2022). The motor

expense is for the use of car (Co2 emission 105g/km ) Mr A is using in the business that was

purchased in May 2018 with brought forward value of £6,000 as at 06.04.2021. For the tax year

5th April 2022, he also received bank interest income from UK banks £1,110, dividend from

Tesco shares £548 and overseas share dividend £98. Mr A has also contributed into a pension

scheme for £4,800 where basic tax relief has been claimed by the provider and made UK charity

of £550.

regular basis and the turnover from its services is more than £1,000 then in such case such

worker is considered as self-employed for the tax purpose and they need to file tax return under

self-employment status. The self-employed worker in UK pay Class 2 NIC in case if their profit

is more than £6,515 during the financial year 2021-22 (£6,725 for tax year 2022-23). In addition

to class 2 NIC, they also pay class 4 NIC in case if their profit is more than £9,568 for 2021-22

(£9,880 for 2022-23) (www.gov.uk).

Determination of Taxable amounts and Calculation of Tax Payable for a scenario.

For the purpose of computation of taxable amount and tax payable the scenario is chosen is self-

employment. For example, Mr A is a self-employed individual that worked independently at

home. Their self-employed turnover for year 2021-2022 is £60,670. He incurs business

proportion of light, heat and telephone is £880, print & stationary £680, Professional

Subscription £822, Insurance 572, software £677, new computer & chair purchased for £2,455

and Motor expenses for the year ended 5 April 2022 was £3,582 out of which only 40% relates

to business use and remaining 60% is of private (Steenbergen and Weber, 2022). The motor

expense is for the use of car (Co2 emission 105g/km ) Mr A is using in the business that was

purchased in May 2018 with brought forward value of £6,000 as at 06.04.2021. For the tax year

5th April 2022, he also received bank interest income from UK banks £1,110, dividend from

Tesco shares £548 and overseas share dividend £98. Mr A has also contributed into a pension

scheme for £4,800 where basic tax relief has been claimed by the provider and made UK charity

of £550.

Calculation of Taxable Amount:

Particular (£) Amount (£)

Self-employed Turnover 60,670

Total assessable income 60,670

Allowable Expenses:

Heat, light and telephone (880)

Print & stationery (680)

Professional subscription (822)

Insurance (572)

Software (677)

Motor expenses (Business only £3,582 x 40%) (1,433)

Less: Total allowable expenses (5,064)

Net Trading profits (before capital allowances) 55,606

Less: Capital Allowances* (see detail below) (2,887)

Taxable Trading profit / Taxable amount 52,719

Calculation of Capital Allowances:

Computer

& Chair

Motor Car Personal Use

60%

TOTAL

Written Down Value B/F £6,000

Purchase £2,455 -

Annual Investment Allowance

(100%)

(£2,455) - £2,455

WDA (Main rate 18%) (£1,080) £648 £432

WDV C/F - £4,920 - £2,887

Particular (£) Amount (£)

Self-employed Turnover 60,670

Total assessable income 60,670

Allowable Expenses:

Heat, light and telephone (880)

Print & stationery (680)

Professional subscription (822)

Insurance (572)

Software (677)

Motor expenses (Business only £3,582 x 40%) (1,433)

Less: Total allowable expenses (5,064)

Net Trading profits (before capital allowances) 55,606

Less: Capital Allowances* (see detail below) (2,887)

Taxable Trading profit / Taxable amount 52,719

Calculation of Capital Allowances:

Computer

& Chair

Motor Car Personal Use

60%

TOTAL

Written Down Value B/F £6,000

Purchase £2,455 -

Annual Investment Allowance

(100%)

(£2,455) - £2,455

WDA (Main rate 18%) (£1,080) £648 £432

WDV C/F - £4,920 - £2,887

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

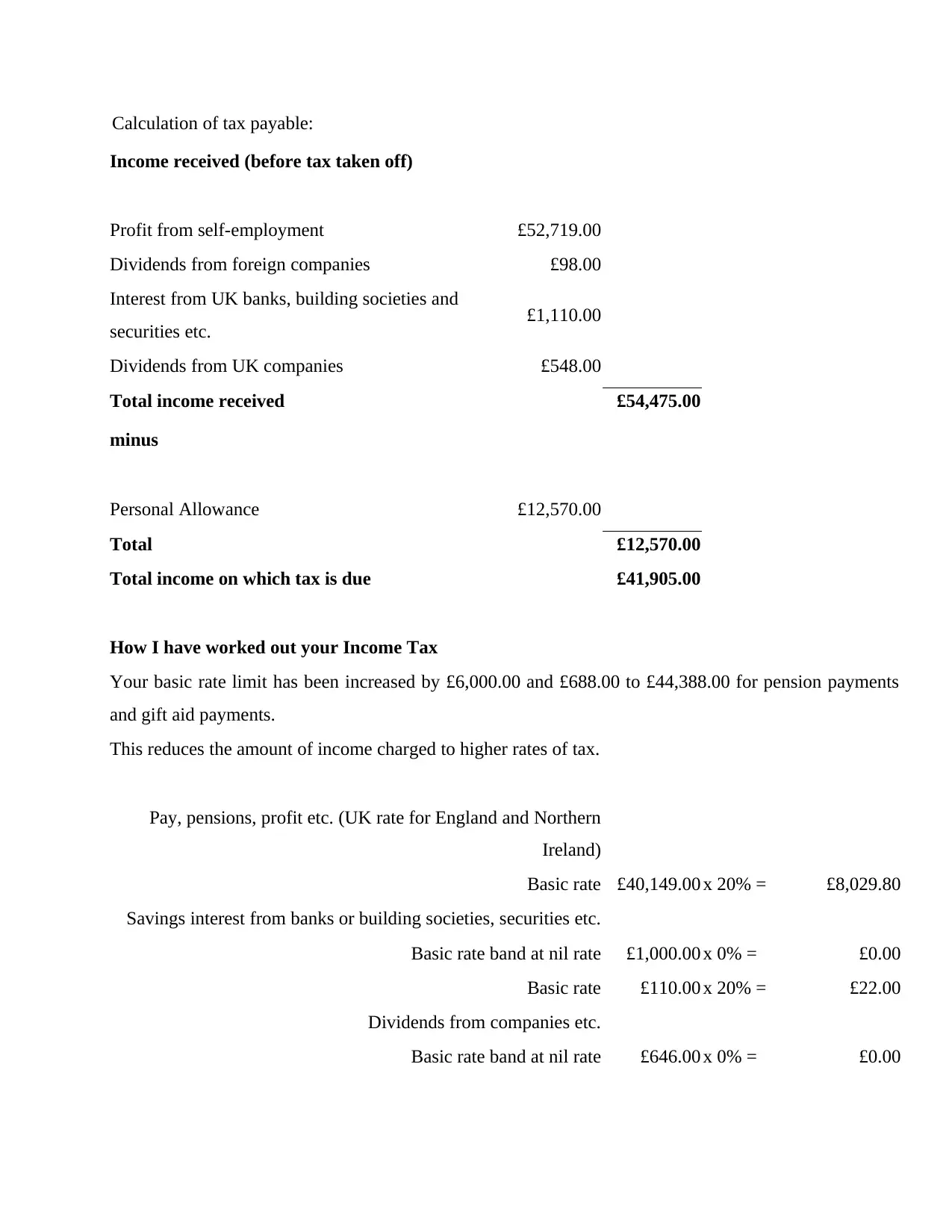

Calculation of tax payable:

Income received (before tax taken off)

Profit from self-employment £52,719.00

Dividends from foreign companies £98.00

Interest from UK banks, building societies and

securities etc. £1,110.00

Dividends from UK companies £548.00

Total income received £54,475.00

minus

Personal Allowance £12,570.00

Total £12,570.00

Total income on which tax is due £41,905.00

How I have worked out your Income Tax

Your basic rate limit has been increased by £6,000.00 and £688.00 to £44,388.00 for pension payments

and gift aid payments.

This reduces the amount of income charged to higher rates of tax.

Pay, pensions, profit etc. (UK rate for England and Northern

Ireland)

Basic rate £40,149.00 x 20% = £8,029.80

Savings interest from banks or building societies, securities etc.

Basic rate band at nil rate £1,000.00 x 0% = £0.00

Basic rate £110.00 x 20% = £22.00

Dividends from companies etc.

Basic rate band at nil rate £646.00 x 0% = £0.00

Income received (before tax taken off)

Profit from self-employment £52,719.00

Dividends from foreign companies £98.00

Interest from UK banks, building societies and

securities etc. £1,110.00

Dividends from UK companies £548.00

Total income received £54,475.00

minus

Personal Allowance £12,570.00

Total £12,570.00

Total income on which tax is due £41,905.00

How I have worked out your Income Tax

Your basic rate limit has been increased by £6,000.00 and £688.00 to £44,388.00 for pension payments

and gift aid payments.

This reduces the amount of income charged to higher rates of tax.

Pay, pensions, profit etc. (UK rate for England and Northern

Ireland)

Basic rate £40,149.00 x 20% = £8,029.80

Savings interest from banks or building societies, securities etc.

Basic rate band at nil rate £1,000.00 x 0% = £0.00

Basic rate £110.00 x 20% = £22.00

Dividends from companies etc.

Basic rate band at nil rate £646.00 x 0% = £0.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

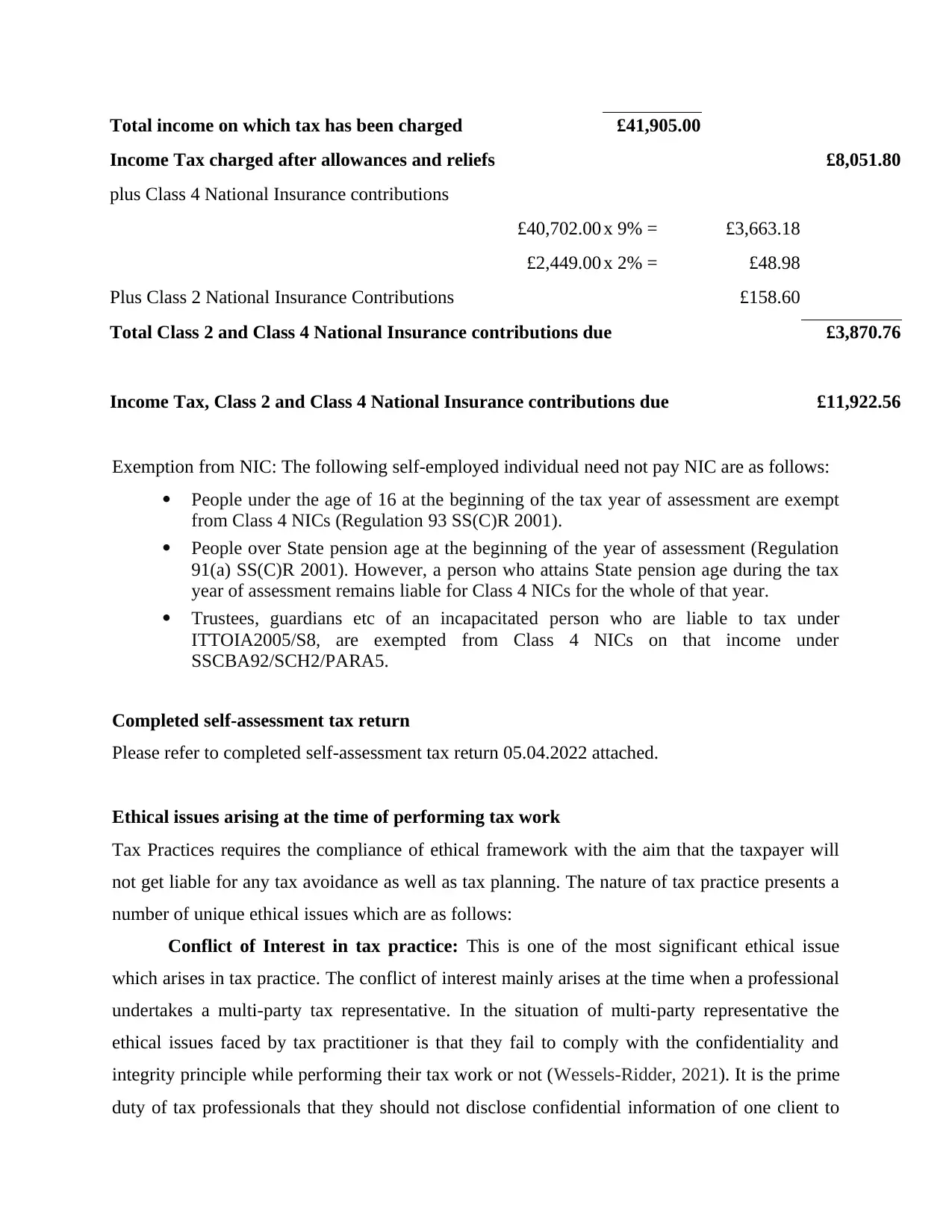

Total income on which tax has been charged £41,905.00

Income Tax charged after allowances and reliefs £8,051.80

plus Class 4 National Insurance contributions

£40,702.00 x 9% = £3,663.18

£2,449.00 x 2% = £48.98

Plus Class 2 National Insurance Contributions £158.60

Total Class 2 and Class 4 National Insurance contributions due £3,870.76

Income Tax, Class 2 and Class 4 National Insurance contributions due £11,922.56

Exemption from NIC: The following self-employed individual need not pay NIC are as follows:

People under the age of 16 at the beginning of the tax year of assessment are exempt

from Class 4 NICs (Regulation 93 SS(C)R 2001).

People over State pension age at the beginning of the year of assessment (Regulation

91(a) SS(C)R 2001). However, a person who attains State pension age during the tax

year of assessment remains liable for Class 4 NICs for the whole of that year.

Trustees, guardians etc of an incapacitated person who are liable to tax under

ITTOIA2005/S8, are exempted from Class 4 NICs on that income under

SSCBA92/SCH2/PARA5.

Completed self-assessment tax return

Please refer to completed self-assessment tax return 05.04.2022 attached.

Ethical issues arising at the time of performing tax work

Tax Practices requires the compliance of ethical framework with the aim that the taxpayer will

not get liable for any tax avoidance as well as tax planning. The nature of tax practice presents a

number of unique ethical issues which are as follows:

Conflict of Interest in tax practice: This is one of the most significant ethical issue

which arises in tax practice. The conflict of interest mainly arises at the time when a professional

undertakes a multi-party tax representative. In the situation of multi-party representative the

ethical issues faced by tax practitioner is that they fail to comply with the confidentiality and

integrity principle while performing their tax work or not (Wessels-Ridder, 2021). It is the prime

duty of tax professionals that they should not disclose confidential information of one client to

Income Tax charged after allowances and reliefs £8,051.80

plus Class 4 National Insurance contributions

£40,702.00 x 9% = £3,663.18

£2,449.00 x 2% = £48.98

Plus Class 2 National Insurance Contributions £158.60

Total Class 2 and Class 4 National Insurance contributions due £3,870.76

Income Tax, Class 2 and Class 4 National Insurance contributions due £11,922.56

Exemption from NIC: The following self-employed individual need not pay NIC are as follows:

People under the age of 16 at the beginning of the tax year of assessment are exempt

from Class 4 NICs (Regulation 93 SS(C)R 2001).

People over State pension age at the beginning of the year of assessment (Regulation

91(a) SS(C)R 2001). However, a person who attains State pension age during the tax

year of assessment remains liable for Class 4 NICs for the whole of that year.

Trustees, guardians etc of an incapacitated person who are liable to tax under

ITTOIA2005/S8, are exempted from Class 4 NICs on that income under

SSCBA92/SCH2/PARA5.

Completed self-assessment tax return

Please refer to completed self-assessment tax return 05.04.2022 attached.

Ethical issues arising at the time of performing tax work

Tax Practices requires the compliance of ethical framework with the aim that the taxpayer will

not get liable for any tax avoidance as well as tax planning. The nature of tax practice presents a

number of unique ethical issues which are as follows:

Conflict of Interest in tax practice: This is one of the most significant ethical issue

which arises in tax practice. The conflict of interest mainly arises at the time when a professional

undertakes a multi-party tax representative. In the situation of multi-party representative the

ethical issues faced by tax practitioner is that they fail to comply with the confidentiality and

integrity principle while performing their tax work or not (Wessels-Ridder, 2021). It is the prime

duty of tax professionals that they should not disclose confidential information of one client to

another client while doing their tax work or preparing their tax return. Hence, one of the ethical

issue for tax professional is conflict of interest and confidentiality.

Tax Avoidance: Every company in the present time wants to minimize its tax liability

through proper tax planning. But this became one of the ethical issue when tax practitioner or

firms instead of using ethical way started using aggressive and unethical way to reduce the tax

liability of its client. Providing unethical tax avoidance strategies to the company is one of the

ethical issues. For example, in UK Public Accounts Committee has put allegation on tax firms

that they provide aggressive and unethical tax avoidance practices to the multinational

companies such as Amazon, Facebook, Google and Starbucks in order to reduce or eliminate

their tax expenses or cost. Hence, it can be said that tax aggressive tax avoidance in illegal

manner is one of the ethical issue that arises at the time of performing their tax.

It is because the tax professional are highly pressurized by their clients that they do not

want to pay tax, and they should adopt strategies to reduce their tax amount (Schiavone, 2020).

The example of tax avoidance includes use of overseas tax heaven or shift of local income to

foreign countries in order to pay nil or low tax rate in domestic country. Tax evasion is totally

different from tax avoidance because tax evasion is considered as fundamentally illegal action.

Recording of each client return requirement and retention: This is another most

significant practice ethical issues that mainly arises at the time of preparing tax return or working

out client tax computation. This indicates that tax professionals need to maintain its clients return

and retain it within their firm via proper record keeping. It is because on the request of client, the

tax practitioner can promptly return or provide any or all record of the client that have to be

required to comply with federal tax obligations. At the time of performing the tax work, adoption

of retention policy is one of the major or most important step that have to be followed by each

and every tax practitioner in UK. Further, the ethical issues faced by them is protecting the

confidential information of the clients (Panikian and et.al., 2021). Under this retention policy, the

tax professionals are required to keep record of all the original document of client and it is their

duty that they will store it in electronic form with strong password. Here, the small or even a

large dispute over fees between the client and tax practitioner would not allow tax professional to

disclose clients information in public. They cannot take sept back from their responsibility.

Hence, it can be said that, while performing the tax work and retaining client records, the

discloser of client information, demanding unreasonable fees or charges is an ethical issue.

issue for tax professional is conflict of interest and confidentiality.

Tax Avoidance: Every company in the present time wants to minimize its tax liability

through proper tax planning. But this became one of the ethical issue when tax practitioner or

firms instead of using ethical way started using aggressive and unethical way to reduce the tax

liability of its client. Providing unethical tax avoidance strategies to the company is one of the

ethical issues. For example, in UK Public Accounts Committee has put allegation on tax firms

that they provide aggressive and unethical tax avoidance practices to the multinational

companies such as Amazon, Facebook, Google and Starbucks in order to reduce or eliminate

their tax expenses or cost. Hence, it can be said that tax aggressive tax avoidance in illegal

manner is one of the ethical issue that arises at the time of performing their tax.

It is because the tax professional are highly pressurized by their clients that they do not

want to pay tax, and they should adopt strategies to reduce their tax amount (Schiavone, 2020).

The example of tax avoidance includes use of overseas tax heaven or shift of local income to

foreign countries in order to pay nil or low tax rate in domestic country. Tax evasion is totally

different from tax avoidance because tax evasion is considered as fundamentally illegal action.

Recording of each client return requirement and retention: This is another most

significant practice ethical issues that mainly arises at the time of preparing tax return or working

out client tax computation. This indicates that tax professionals need to maintain its clients return

and retain it within their firm via proper record keeping. It is because on the request of client, the

tax practitioner can promptly return or provide any or all record of the client that have to be

required to comply with federal tax obligations. At the time of performing the tax work, adoption

of retention policy is one of the major or most important step that have to be followed by each

and every tax practitioner in UK. Further, the ethical issues faced by them is protecting the

confidential information of the clients (Panikian and et.al., 2021). Under this retention policy, the

tax professionals are required to keep record of all the original document of client and it is their

duty that they will store it in electronic form with strong password. Here, the small or even a

large dispute over fees between the client and tax practitioner would not allow tax professional to

disclose clients information in public. They cannot take sept back from their responsibility.

Hence, it can be said that, while performing the tax work and retaining client records, the

discloser of client information, demanding unreasonable fees or charges is an ethical issue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 40

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.