Taxation Fundamentals Report: UK Taxation, Income, and Redundancy

VerifiedAdded on 2023/01/05

|10

|2145

|59

Report

AI Summary

This report provides a detailed analysis of taxation fundamentals, focusing on the UK tax system. It begins with an introduction to taxation, defining its importance and illustrating it with a case study of Fiona, a UK resident. The report calculates Fiona's income tax liability, considering various income sources, deductions, and expenses, including salary, bonus, interest, dividends, and pension contributions. It then delves into Section B, Part 1, explaining redundancy pay, its different types, and the tax implications of various benefits associated with it, such as gardening leave, payments for training, past due salaries, and statutory redundancy payments. Part 2 of Section B discusses overseas workday relief, explaining its benefits for non-domiciled UK residents and the importance of separate bank accounts for claiming this relief. The report references relevant books, journals, and online resources to support its findings.

Taxation

Fundamentals

Fundamentals

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION A.....................................................................................................................................1

Part 1............................................................................................................................................1

SECTION B.....................................................................................................................................3

Part 1............................................................................................................................................3

Part 2............................................................................................................................................5

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION A.....................................................................................................................................1

Part 1............................................................................................................................................1

SECTION B.....................................................................................................................................3

Part 1............................................................................................................................................3

Part 2............................................................................................................................................5

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

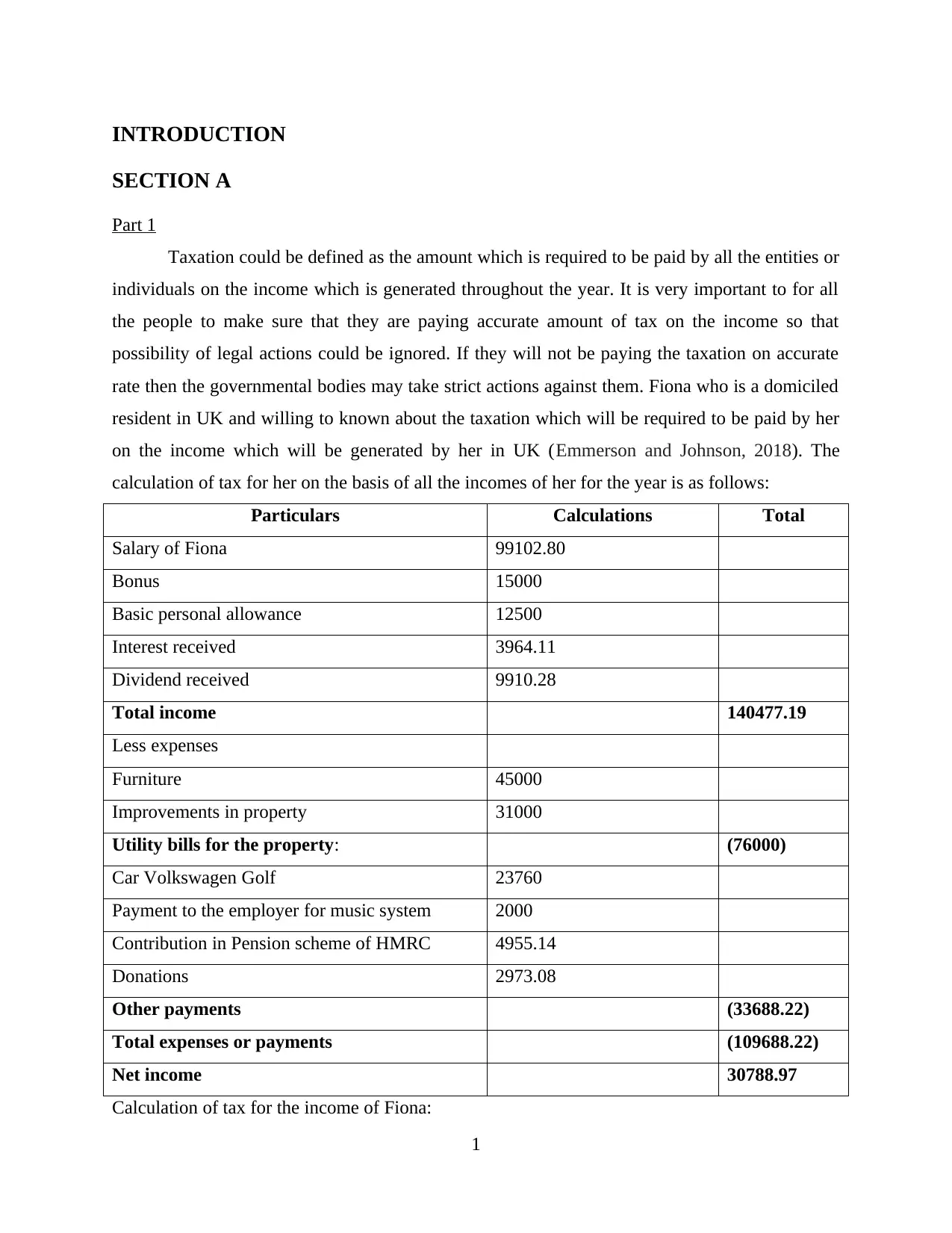

INTRODUCTION

SECTION A

Part 1

Taxation could be defined as the amount which is required to be paid by all the entities or

individuals on the income which is generated throughout the year. It is very important to for all

the people to make sure that they are paying accurate amount of tax on the income so that

possibility of legal actions could be ignored. If they will not be paying the taxation on accurate

rate then the governmental bodies may take strict actions against them. Fiona who is a domiciled

resident in UK and willing to known about the taxation which will be required to be paid by her

on the income which will be generated by her in UK (Emmerson and Johnson, 2018). The

calculation of tax for her on the basis of all the incomes of her for the year is as follows:

Particulars Calculations Total

Salary of Fiona 99102.80

Bonus 15000

Basic personal allowance 12500

Interest received 3964.11

Dividend received 9910.28

Total income 140477.19

Less expenses

Furniture 45000

Improvements in property 31000

Utility bills for the property: (76000)

Car Volkswagen Golf 23760

Payment to the employer for music system 2000

Contribution in Pension scheme of HMRC 4955.14

Donations 2973.08

Other payments (33688.22)

Total expenses or payments (109688.22)

Net income 30788.97

Calculation of tax for the income of Fiona:

1

SECTION A

Part 1

Taxation could be defined as the amount which is required to be paid by all the entities or

individuals on the income which is generated throughout the year. It is very important to for all

the people to make sure that they are paying accurate amount of tax on the income so that

possibility of legal actions could be ignored. If they will not be paying the taxation on accurate

rate then the governmental bodies may take strict actions against them. Fiona who is a domiciled

resident in UK and willing to known about the taxation which will be required to be paid by her

on the income which will be generated by her in UK (Emmerson and Johnson, 2018). The

calculation of tax for her on the basis of all the incomes of her for the year is as follows:

Particulars Calculations Total

Salary of Fiona 99102.80

Bonus 15000

Basic personal allowance 12500

Interest received 3964.11

Dividend received 9910.28

Total income 140477.19

Less expenses

Furniture 45000

Improvements in property 31000

Utility bills for the property: (76000)

Car Volkswagen Golf 23760

Payment to the employer for music system 2000

Contribution in Pension scheme of HMRC 4955.14

Donations 2973.08

Other payments (33688.22)

Total expenses or payments (109688.22)

Net income 30788.97

Calculation of tax for the income of Fiona:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

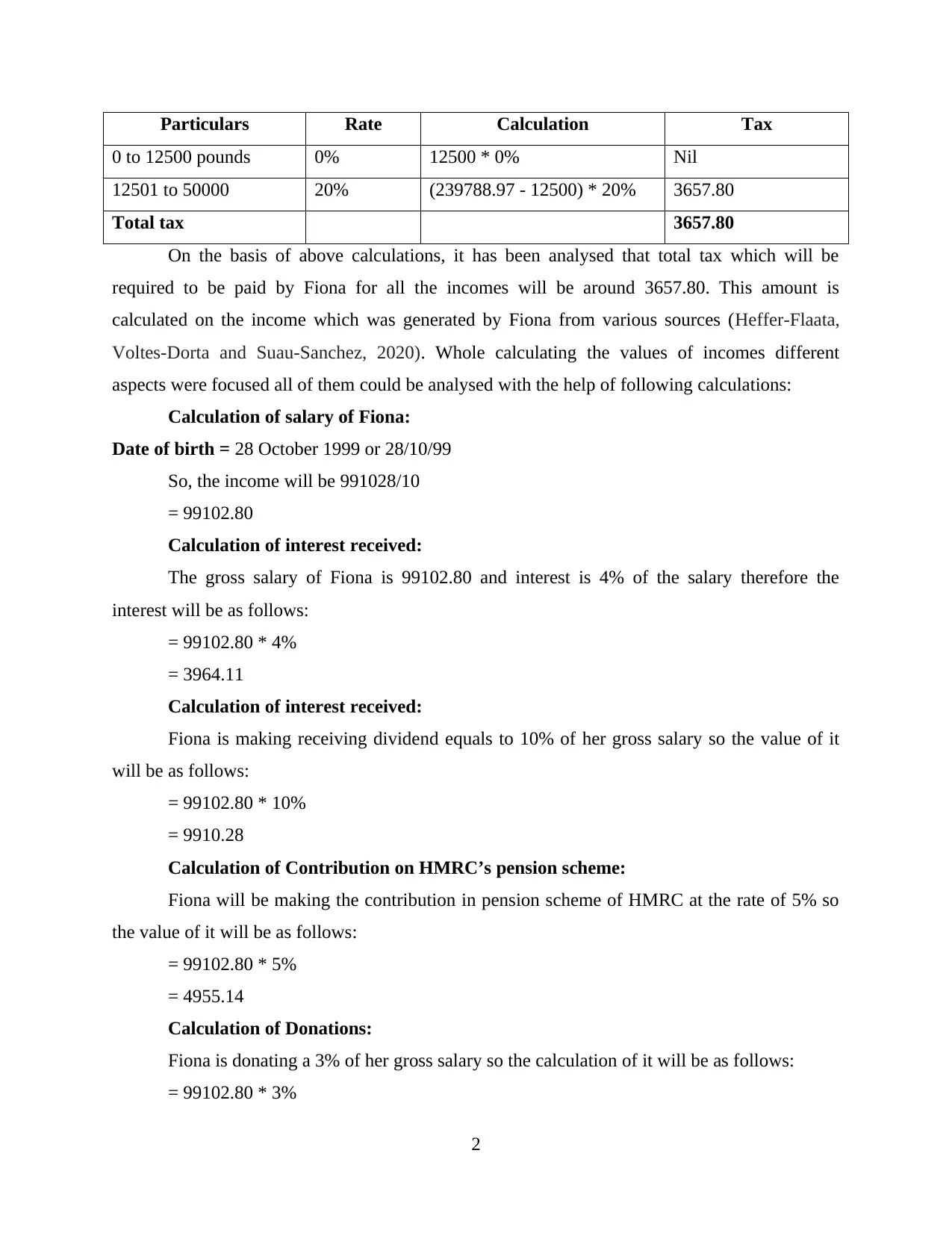

Particulars Rate Calculation Tax

0 to 12500 pounds 0% 12500 * 0% Nil

12501 to 50000 20% (239788.97 - 12500) * 20% 3657.80

Total tax 3657.80

On the basis of above calculations, it has been analysed that total tax which will be

required to be paid by Fiona for all the incomes will be around 3657.80. This amount is

calculated on the income which was generated by Fiona from various sources (Heffer-Flaata,

Voltes-Dorta and Suau-Sanchez, 2020). Whole calculating the values of incomes different

aspects were focused all of them could be analysed with the help of following calculations:

Calculation of salary of Fiona:

Date of birth = 28 October 1999 or 28/10/99

So, the income will be 991028/10

= 99102.80

Calculation of interest received:

The gross salary of Fiona is 99102.80 and interest is 4% of the salary therefore the

interest will be as follows:

= 99102.80 * 4%

= 3964.11

Calculation of interest received:

Fiona is making receiving dividend equals to 10% of her gross salary so the value of it

will be as follows:

= 99102.80 * 10%

= 9910.28

Calculation of Contribution on HMRC’s pension scheme:

Fiona will be making the contribution in pension scheme of HMRC at the rate of 5% so

the value of it will be as follows:

= 99102.80 * 5%

= 4955.14

Calculation of Donations:

Fiona is donating a 3% of her gross salary so the calculation of it will be as follows:

= 99102.80 * 3%

2

0 to 12500 pounds 0% 12500 * 0% Nil

12501 to 50000 20% (239788.97 - 12500) * 20% 3657.80

Total tax 3657.80

On the basis of above calculations, it has been analysed that total tax which will be

required to be paid by Fiona for all the incomes will be around 3657.80. This amount is

calculated on the income which was generated by Fiona from various sources (Heffer-Flaata,

Voltes-Dorta and Suau-Sanchez, 2020). Whole calculating the values of incomes different

aspects were focused all of them could be analysed with the help of following calculations:

Calculation of salary of Fiona:

Date of birth = 28 October 1999 or 28/10/99

So, the income will be 991028/10

= 99102.80

Calculation of interest received:

The gross salary of Fiona is 99102.80 and interest is 4% of the salary therefore the

interest will be as follows:

= 99102.80 * 4%

= 3964.11

Calculation of interest received:

Fiona is making receiving dividend equals to 10% of her gross salary so the value of it

will be as follows:

= 99102.80 * 10%

= 9910.28

Calculation of Contribution on HMRC’s pension scheme:

Fiona will be making the contribution in pension scheme of HMRC at the rate of 5% so

the value of it will be as follows:

= 99102.80 * 5%

= 4955.14

Calculation of Donations:

Fiona is donating a 3% of her gross salary so the calculation of it will be as follows:

= 99102.80 * 3%

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 2973.08

Total utilities payment:

According to the policy of the company Fiona will be required o be pay for all the

utilities of the company. In this case if the organisation will make any expense to develop or

improve the property then Fiona will be required to make payment of the same. During the year

31000 pounds were spent by the organisation on the improvement of the property so this amount

will be paid by Fiona to the enterprise (Holzmann and Piggott, 2018). Apart from this, company

also provided furniture at the cost of 45000 to Fiona. Total payment which will required to be

paid by her for utilities provided by the company will be as follows:

Improvements charges = 31000

Furniture charges = 45000

Total utilities = 76000 (45000 + 31000)

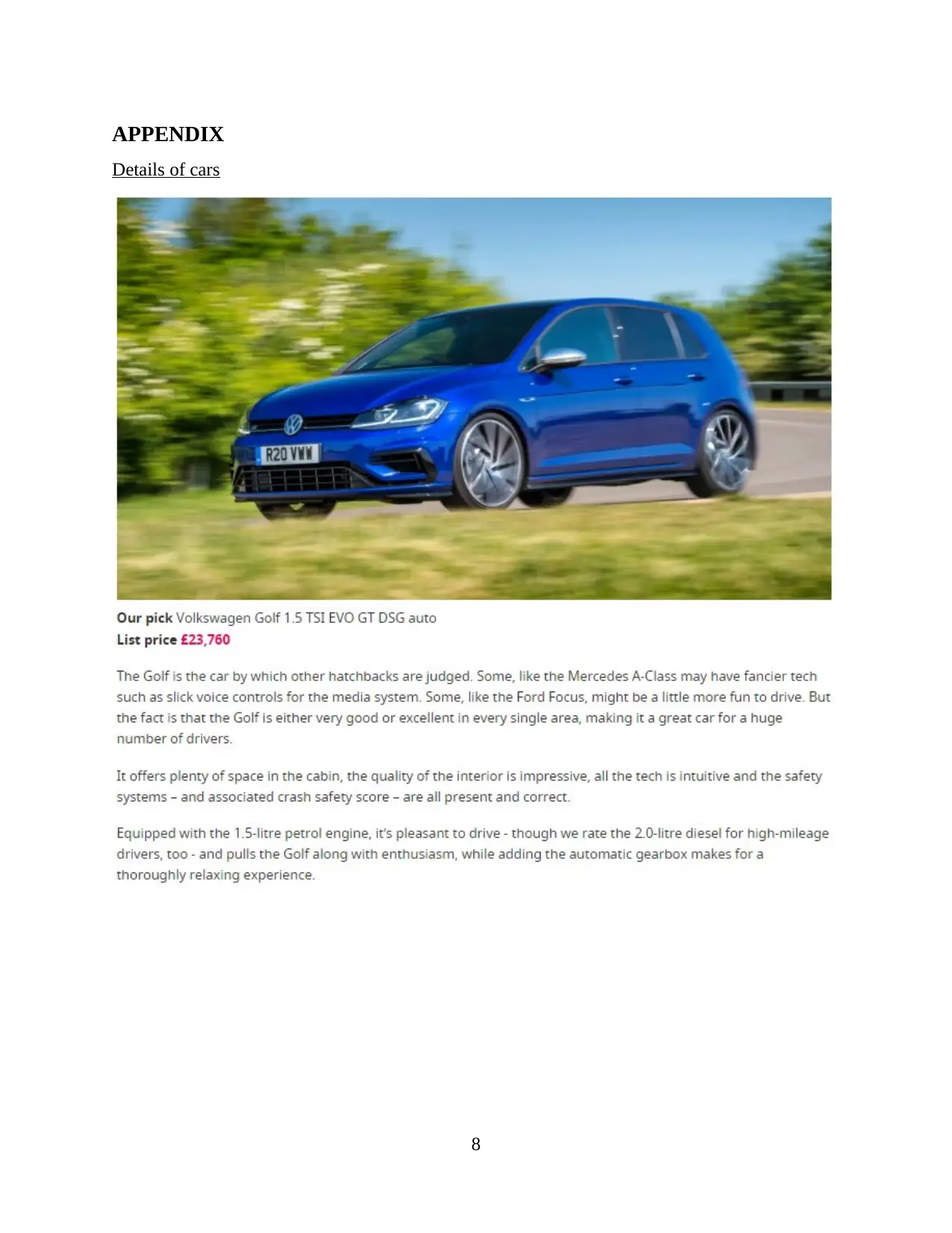

Details of car: The car which will be purchased by Fiona is Volkswagen Golf (Details of

Volkswagen Golf, 2020). All the details of it are as follows:

Elements Details

Details of make Slick voice controls for the media system

Model Volkswagen Golf 1.5

List price 23760 pounds

Type of engine TSI EVO GT DSG auto

CO2 Emission Less CO2 emission

All the details that are provided in above table are related to Volkswagen Golf which will

be bought by Fiona. The price of it is 23760 pounds and the cost of it is under 25000. With the

help of all the above notes Fiona will be able to get detailed information of tax which is required

to be paid by her on her income.

SECTION B

Part 1

Redundancy pay could be defined as the pay which is provided by the employer to the

employee who has made a redundant. It is calculated on the basis of rate of pay of the employees

and the period of their service. There are two different types of it which are statutory and

contractual. The pay which is made according to law is statutory and the extra money which is

3

Total utilities payment:

According to the policy of the company Fiona will be required o be pay for all the

utilities of the company. In this case if the organisation will make any expense to develop or

improve the property then Fiona will be required to make payment of the same. During the year

31000 pounds were spent by the organisation on the improvement of the property so this amount

will be paid by Fiona to the enterprise (Holzmann and Piggott, 2018). Apart from this, company

also provided furniture at the cost of 45000 to Fiona. Total payment which will required to be

paid by her for utilities provided by the company will be as follows:

Improvements charges = 31000

Furniture charges = 45000

Total utilities = 76000 (45000 + 31000)

Details of car: The car which will be purchased by Fiona is Volkswagen Golf (Details of

Volkswagen Golf, 2020). All the details of it are as follows:

Elements Details

Details of make Slick voice controls for the media system

Model Volkswagen Golf 1.5

List price 23760 pounds

Type of engine TSI EVO GT DSG auto

CO2 Emission Less CO2 emission

All the details that are provided in above table are related to Volkswagen Golf which will

be bought by Fiona. The price of it is 23760 pounds and the cost of it is under 25000. With the

help of all the above notes Fiona will be able to get detailed information of tax which is required

to be paid by her on her income.

SECTION B

Part 1

Redundancy pay could be defined as the pay which is provided by the employer to the

employee who has made a redundant. It is calculated on the basis of rate of pay of the employees

and the period of their service. There are two different types of it which are statutory and

contractual. The pay which is made according to law is statutory and the extra money which is

3

mentioned in the contract is contractual pay (Kao, 2019). This amount if received on the top of

the pay which is made according to law. There are various types of benefits that are taxed

separately under the law for redundancy pay. Some of them are discussed below:

Gardening leave: When the employees are asked to serve out their redundancy notice

away from the work then it will be known as gardening leave and it means that the

individual is not actually working within the company but legally employed. Under this

period the individual will receive normal salary and the benefits. Apart from this, under

this period the individuals could be called back of there is a need of that person within the

organisation.

Payment for training and skill development of employee: The payment which is made by

the employer under the redundancy period will not be treated as income for the employee

therefore it will not be taxable for the period. The amount which will be received by the

individual for this perspective will be treated as other savings that the individual is

having.

Past due salary and bonus: When the employee will be receiving all the redundancy

payments then it will be very important for that person to make sure that all the due

salaries and bonuses are received because in this amount all of them will be included. All

these payments will not be taxable as all of them will be treated as savings (Liu, 2020).

Pay in lieu of unutilised holidays: While working within the organisation the employee

may have unutilised holidays and for an employer it is very important to make payment

of it to the employee. These payments are also required to be made by the employer who

will be making redundancy payment to the employee. These payments will also be tax

free because these will be considered as savings of the staff member.

Payment in lieu of notice: It is the amount where the employer compensates the

employee’s immediate dismissal by making the payment to their notice period. It protects

the rights of the employees for the amount that will be received by them during their

notice period.

Statutory redundancy pays up to 30000 pounds: All the redundancy payments are

considered as compensation payment. If the payment will be made under 30000 limits

then the amount of it will be tax free. This limit is applied per termination. If the

4

the pay which is made according to law. There are various types of benefits that are taxed

separately under the law for redundancy pay. Some of them are discussed below:

Gardening leave: When the employees are asked to serve out their redundancy notice

away from the work then it will be known as gardening leave and it means that the

individual is not actually working within the company but legally employed. Under this

period the individual will receive normal salary and the benefits. Apart from this, under

this period the individuals could be called back of there is a need of that person within the

organisation.

Payment for training and skill development of employee: The payment which is made by

the employer under the redundancy period will not be treated as income for the employee

therefore it will not be taxable for the period. The amount which will be received by the

individual for this perspective will be treated as other savings that the individual is

having.

Past due salary and bonus: When the employee will be receiving all the redundancy

payments then it will be very important for that person to make sure that all the due

salaries and bonuses are received because in this amount all of them will be included. All

these payments will not be taxable as all of them will be treated as savings (Liu, 2020).

Pay in lieu of unutilised holidays: While working within the organisation the employee

may have unutilised holidays and for an employer it is very important to make payment

of it to the employee. These payments are also required to be made by the employer who

will be making redundancy payment to the employee. These payments will also be tax

free because these will be considered as savings of the staff member.

Payment in lieu of notice: It is the amount where the employer compensates the

employee’s immediate dismissal by making the payment to their notice period. It protects

the rights of the employees for the amount that will be received by them during their

notice period.

Statutory redundancy pays up to 30000 pounds: All the redundancy payments are

considered as compensation payment. If the payment will be made under 30000 limits

then the amount of it will be tax free. This limit is applied per termination. If the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organsiation will be making this payment then the individual will not be responsible for

making any type of payment for tax.

Statutory redundancy pays above 30000 pounds: While making redundancy payment of

more than 30000 pounds it will be very important for the organisation as well as the

individual who will be receiving the payment will be responsible for paying tax. All the

pays that are made for more than 30000 pounds will be taxable under this United

Kingdom taxation laws.

According to Section 62 & sections 401- 416 ITEPA 2003, all the benefits that are paid to

the employee are considered das the service rendered under employment or the compensation of

the breach of employment contract (Section 62 & sections 401- 416 ITEPA 2003, 2003). All the

payments that are made by the employers in context to redundancy pay will be tax free and

treated as personal savings of the employee.

Part 2

All the employees who are resident in UK but not having any domicile for living in the

country can get benefits from a tax relief which is known as overseas workday relief for the days

that have worked outside UK when they were resident in country. It is very important for all the

staff members. While planning to claim overseas workday belief the individuals will be required

to be taxed on remittance basis. The employee will consider not to be taxed on remittance basis

and elect for the otherwise exempt foreign earnings to be taxed in the UK. The importance of the

belief could be understood with the help of following discussion:

If the employee will be resident in UK and not having any domicile for the same then the

individual can take benefit of overseas workday relief. With the help of it, the individual

can elect for the exemption of foreigner income which will be taxed in United Kingdom.

If the resident who is undomiciled will work outside of UK then the income could be

treated as exemption under this relief (Rudd, 2018).

For an individual who is willing to take benefit from this relief it will eb very important

to set up a separate bank accounts to claim the benefit. If they will not be having any

separate account then the salary from foreign bank will be paid in mixed fund account. It

may create confusion for the taxation authorities to analyse actual national and foreign

income. Due to this, the income tax authority may get confused.

5

making any type of payment for tax.

Statutory redundancy pays above 30000 pounds: While making redundancy payment of

more than 30000 pounds it will be very important for the organisation as well as the

individual who will be receiving the payment will be responsible for paying tax. All the

pays that are made for more than 30000 pounds will be taxable under this United

Kingdom taxation laws.

According to Section 62 & sections 401- 416 ITEPA 2003, all the benefits that are paid to

the employee are considered das the service rendered under employment or the compensation of

the breach of employment contract (Section 62 & sections 401- 416 ITEPA 2003, 2003). All the

payments that are made by the employers in context to redundancy pay will be tax free and

treated as personal savings of the employee.

Part 2

All the employees who are resident in UK but not having any domicile for living in the

country can get benefits from a tax relief which is known as overseas workday relief for the days

that have worked outside UK when they were resident in country. It is very important for all the

staff members. While planning to claim overseas workday belief the individuals will be required

to be taxed on remittance basis. The employee will consider not to be taxed on remittance basis

and elect for the otherwise exempt foreign earnings to be taxed in the UK. The importance of the

belief could be understood with the help of following discussion:

If the employee will be resident in UK and not having any domicile for the same then the

individual can take benefit of overseas workday relief. With the help of it, the individual

can elect for the exemption of foreigner income which will be taxed in United Kingdom.

If the resident who is undomiciled will work outside of UK then the income could be

treated as exemption under this relief (Rudd, 2018).

For an individual who is willing to take benefit from this relief it will eb very important

to set up a separate bank accounts to claim the benefit. If they will not be having any

separate account then the salary from foreign bank will be paid in mixed fund account. It

may create confusion for the taxation authorities to analyse actual national and foreign

income. Due to this, the income tax authority may get confused.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is very important for a person who is willing to take advantage of overseas workday

relief to make sure that they are familiarise with it. For this purpose, they have to make

sure that they are not domiciled as it can benefit them to take tax advantage. Apart from

this, they have to keep their earnings separate and then they can apply for tax rebate on

the incomes that are not generated in UK (Sandford, 2018).

6

relief to make sure that they are familiarise with it. For this purpose, they have to make

sure that they are not domiciled as it can benefit them to take tax advantage. Apart from

this, they have to keep their earnings separate and then they can apply for tax rebate on

the incomes that are not generated in UK (Sandford, 2018).

6

REFERENCES

Books and Journals:

Emmerson, C. and Johnson, P., 2018. The taxation of pensions in the United Kingdom. The

taxation of pensions, pp.235-256.

Heffer-Flaata, H., Voltes-Dorta, A. and Suau-Sanchez, P., 2020. The Impact of Accommodation

Taxes on Outbound Travel Demand from the United Kingdom to European

Destinations. Journal of Travel Research, p.0047287520908931.

Holzmann, R. and Piggott, J. eds., 2018. The Taxation of Pensions. MIT Press.

Kao, W. C., 2019. The Relation between Tax Avoidance and Voluntary Disclosures of Taxation

in United Kingdom.

Liu, L., 2020. Where Does Multinational Investment Go with Territorial Taxation? Evidence

from the United Kingdom. American Economic Journal: Economic Policy, 12(1),

pp.325-58.

Rudd, R., 2018. The taxation of trusts: a comparative study of South Africa and the United

Kingdom (Doctoral dissertation).

Sandford, C. T., 2018. Taxing Personal Wealth: An Analysis of Capital Taxation in the United

Kingdom—History, Present Structure and Future Possibilities (Vol. 10). Routledge.

Online

Details of Volkswagen Golf. 2020. [Online]. Available through:

<https://www.buyacar.co.uk/cars/affordable-cars/cars-under-25000/1159/best-new-cars-

for-under-25000>

Section 62 & sections 401- 416 ITEPA 2003. 2003. [Online]. Available through:

< https://www.legislation.gov.uk/ukpga/2003/1/section/401 >

7

Books and Journals:

Emmerson, C. and Johnson, P., 2018. The taxation of pensions in the United Kingdom. The

taxation of pensions, pp.235-256.

Heffer-Flaata, H., Voltes-Dorta, A. and Suau-Sanchez, P., 2020. The Impact of Accommodation

Taxes on Outbound Travel Demand from the United Kingdom to European

Destinations. Journal of Travel Research, p.0047287520908931.

Holzmann, R. and Piggott, J. eds., 2018. The Taxation of Pensions. MIT Press.

Kao, W. C., 2019. The Relation between Tax Avoidance and Voluntary Disclosures of Taxation

in United Kingdom.

Liu, L., 2020. Where Does Multinational Investment Go with Territorial Taxation? Evidence

from the United Kingdom. American Economic Journal: Economic Policy, 12(1),

pp.325-58.

Rudd, R., 2018. The taxation of trusts: a comparative study of South Africa and the United

Kingdom (Doctoral dissertation).

Sandford, C. T., 2018. Taxing Personal Wealth: An Analysis of Capital Taxation in the United

Kingdom—History, Present Structure and Future Possibilities (Vol. 10). Routledge.

Online

Details of Volkswagen Golf. 2020. [Online]. Available through:

<https://www.buyacar.co.uk/cars/affordable-cars/cars-under-25000/1159/best-new-cars-

for-under-25000>

Section 62 & sections 401- 416 ITEPA 2003. 2003. [Online]. Available through:

< https://www.legislation.gov.uk/ukpga/2003/1/section/401 >

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPENDIX

Details of cars

8

Details of cars

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.