Comprehensive Guide to the Statement of Cash Flows (SCF) Analysis

VerifiedAdded on 2022/09/14

|9

|1362

|19

Homework Assignment

AI Summary

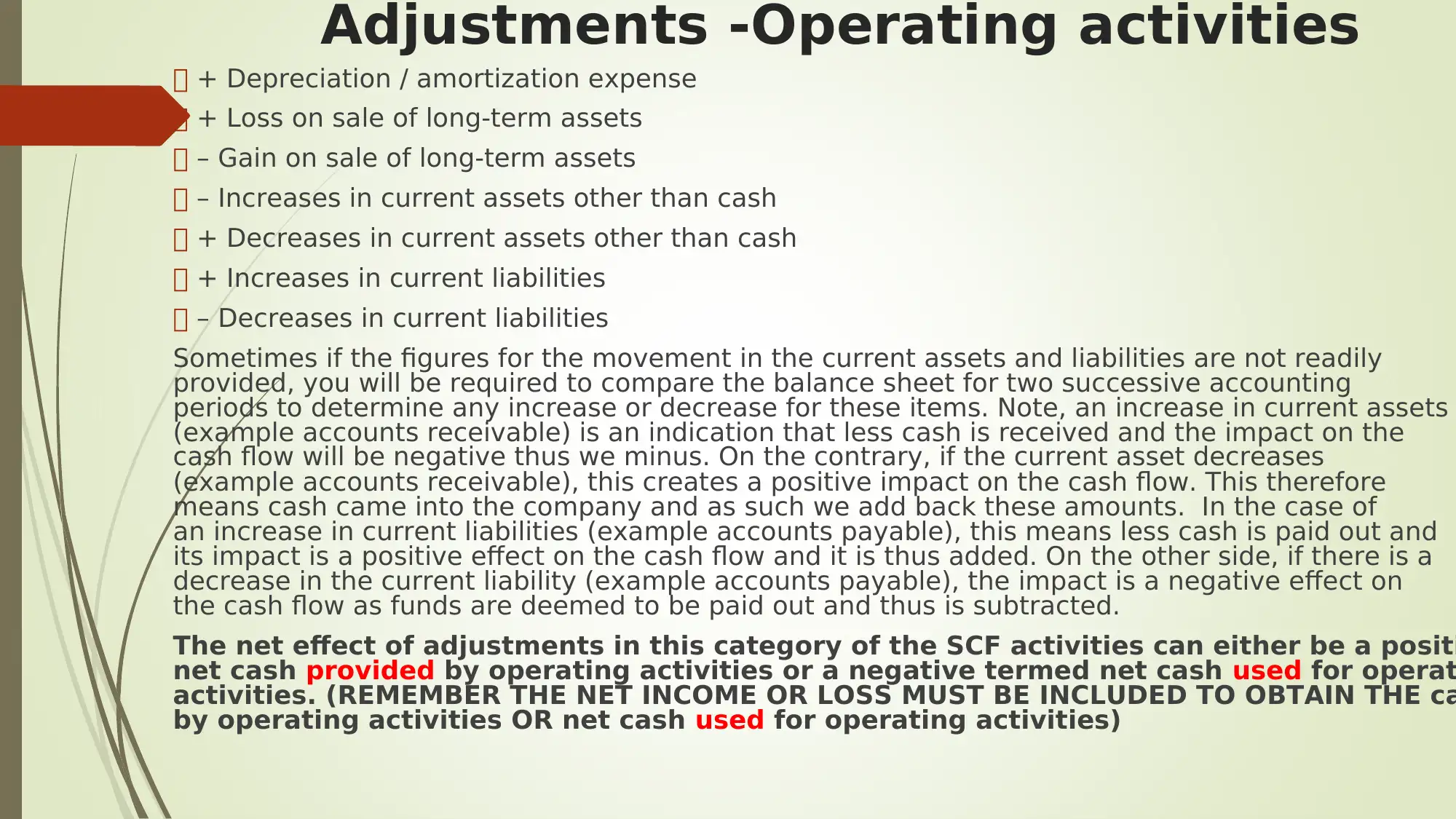

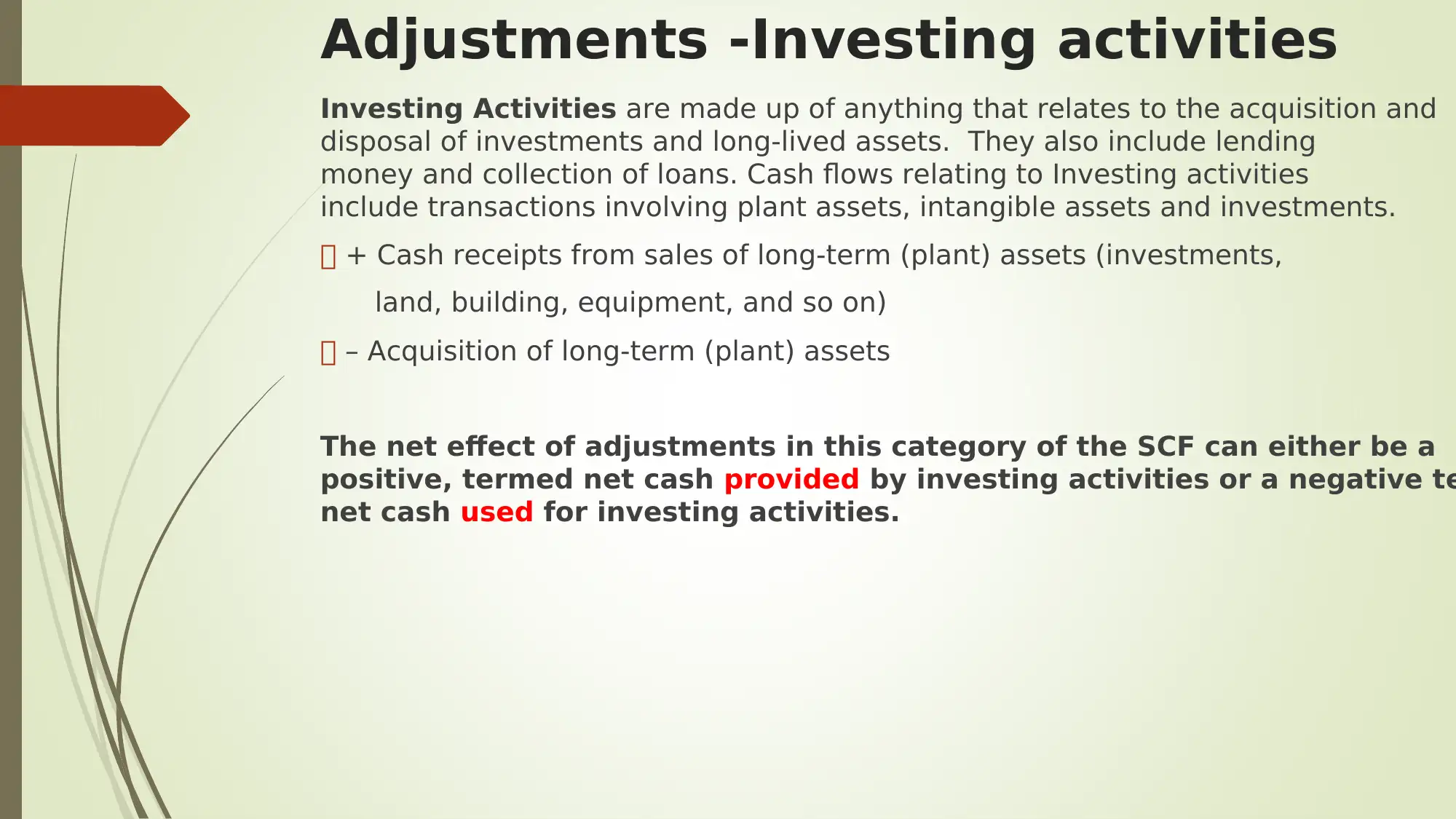

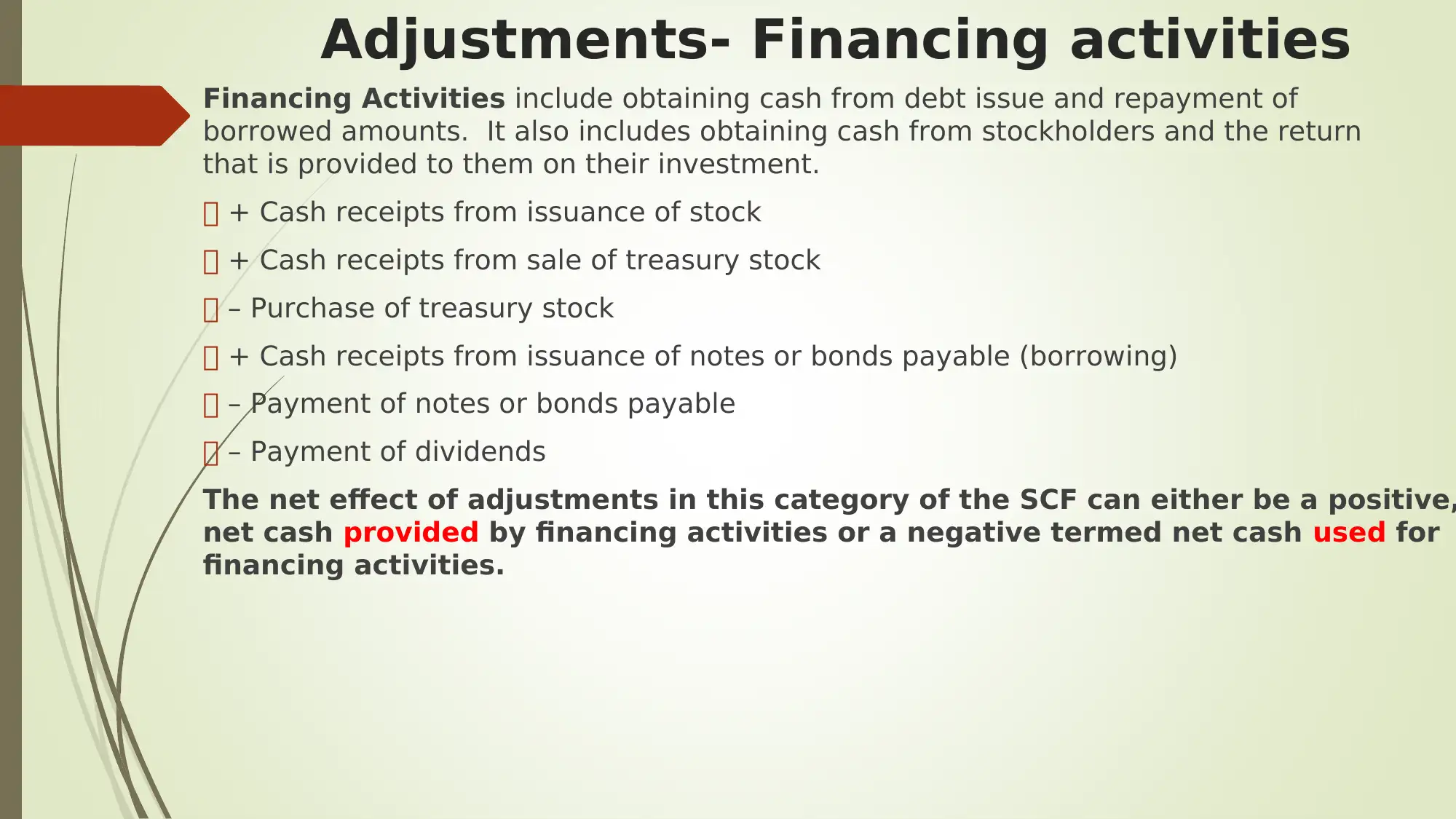

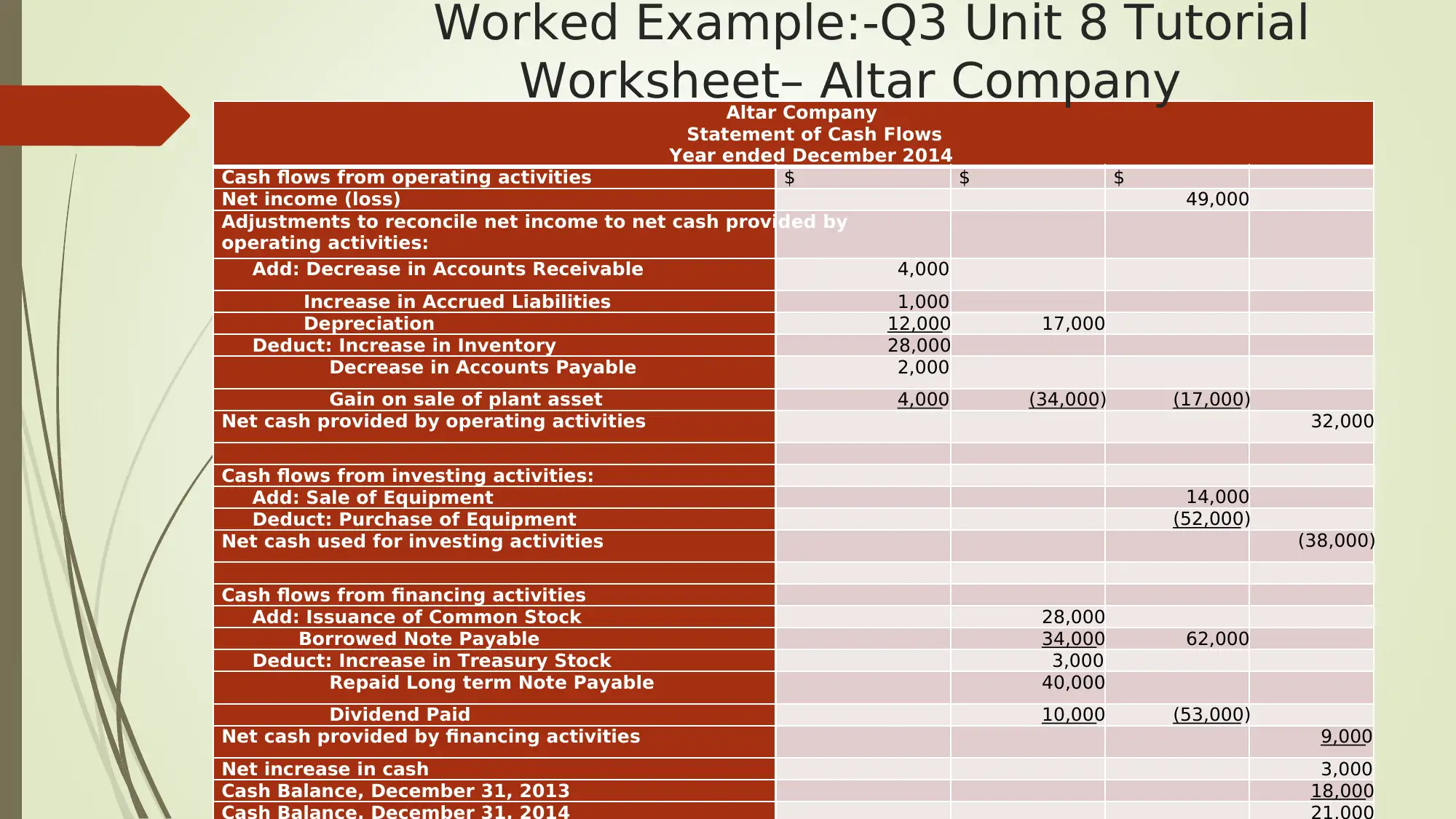

This document provides a comprehensive overview of the Statement of Cash Flows (SCF). It explains the purpose of the SCF, which is to report cash inflows and outflows during an accounting period and the ending cash balance. The document details the three main categories of cash flows: operating, investing, and financing activities, and explains the indirect method of preparing the SCF. It outlines the adjustments made to net income in the operating activities section, including depreciation, gains/losses on asset sales, and changes in current assets and liabilities. The document further explains investing activities (acquisition and disposal of long-lived assets) and financing activities (debt, equity, and dividends). A worked example using the Altar Company illustrates the practical application of the concepts, and it concludes with advice for students to practice using past papers for exam preparation.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.